Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.89; (P) 149.42; (R1) 149.81; More...

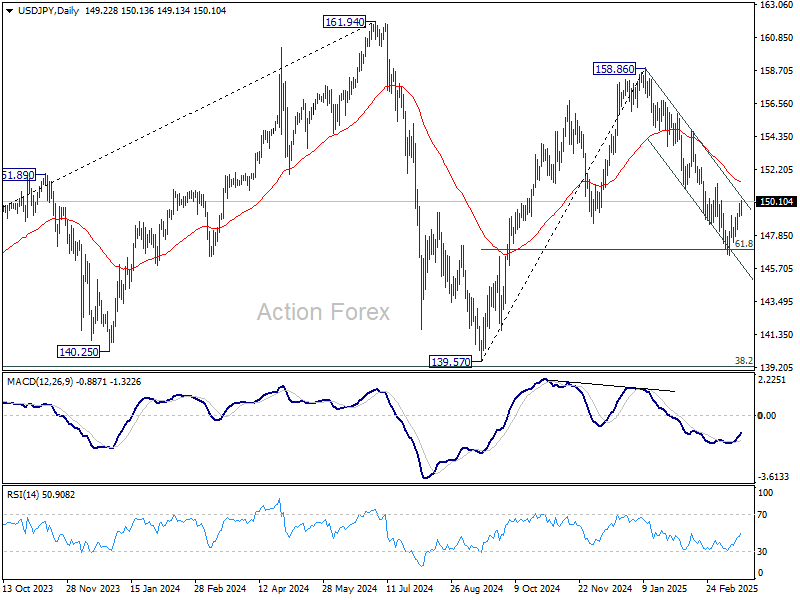

No change in USD/JPY's outlook for now. Recovery from 146.52 is seen as a corrective move. Upside should be limited by 150.92 support turned resistance. On the downside, below 148.22 minor support will bring retest of 146.52 low first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. However, decisive break of 150.92 will dampen this bearish view and turn bias to the upside for 154.79 resistance instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

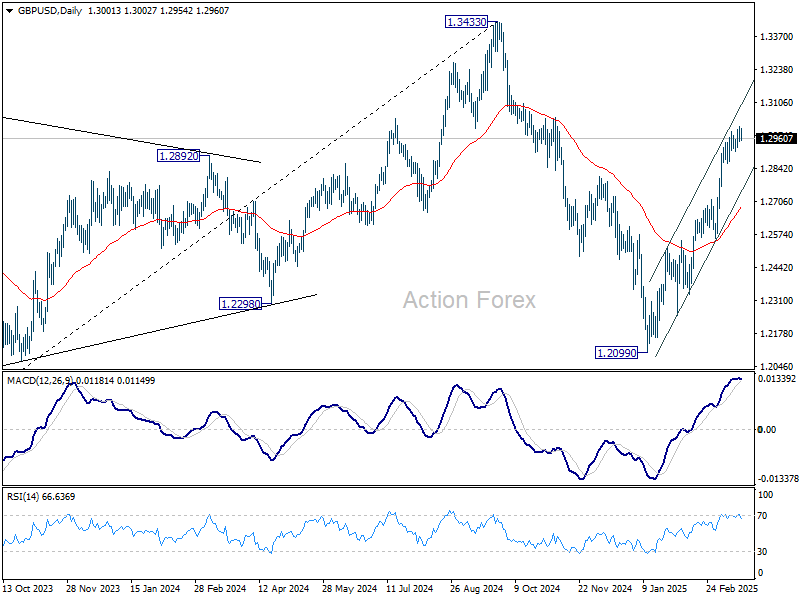

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2967; (P) 1.2988; (R1) 1.3025; More...

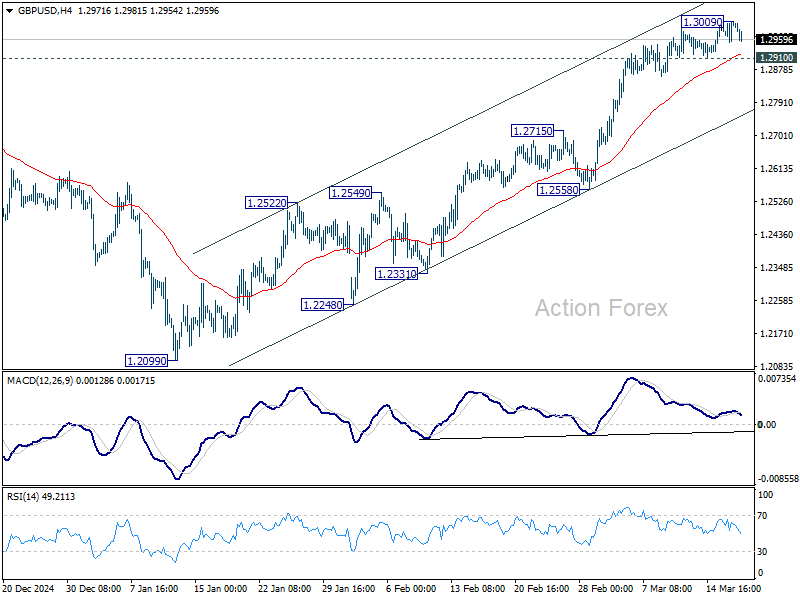

Intraday bias in GBP/USD is turned neutral first with current retreat. Another rise is expected as long as 1.2910 support holds. Above 1.3009 will resume the rally from 1.2099 to retest 1.3433 high. However, firm break of 1.2910 will indicate short term topping, likely with bearish divergence condition in 4H MACD. That would turn intraday bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

Dollar Recovers as Markets Await Fed Projections, Gold Loses Some Momentum

Dollar is recovering across the board as markets enter the US session, though the move appears to be more caution-driven than a shift in sentiment. With FOMC rate decision looming, traders are taking a more neutral stance rather than doubling down on Dollar’s recent weakness. Fed is widely expected to keep rates steady at 4.25-4.50%, so the real focus will be on the updated economic projections. Given the uncertainty surrounding US trade policy, these forecasts could offer the first glimpse of how policymakers are factoring in US President Donald Trump’s tariffs into their outlook.

Since the last FOMC meeting in December, the U.S. has implemented its first set of tariffs under the Trump administration. Now, the markets are preparing for the ambitious reciprocal tariffs set to take effect in early April. While tariff impacts may not be fully reflected in Fed’s projections yet, traders will be looking for any revisions to growth and inflation forecasts that could indicate whether policymakers are growing more concerned about trade war risks. If the Fed acknowledges increased downside risks to growth or upward pressures on inflation, markets could adjust their rate cut expectations accordingly.

Meanwhile, Euro is on the weaker side as Eurozone CPI for February was finalized slightly lower than initial estimates. Comments from ECB officials today are typically cautious. French ECB Governing Council member François Villeroy de Galhau reiterated that the timing and size of rate cuts will depend on data. Meanwhile, ECB Vice President Luis de Guindos emphasized that defense spending remains Europe’s top priority, but warned that budget stability must be maintained within the bloc’s fiscal rules.

For the day so far, Dollar is the strongest performer, followed by the Loonie and Sterling. On the weaker side, Kiwi is the worst performer, followed by Aussie and Euro. Yen and Swiss Franc are positioning in the middle.

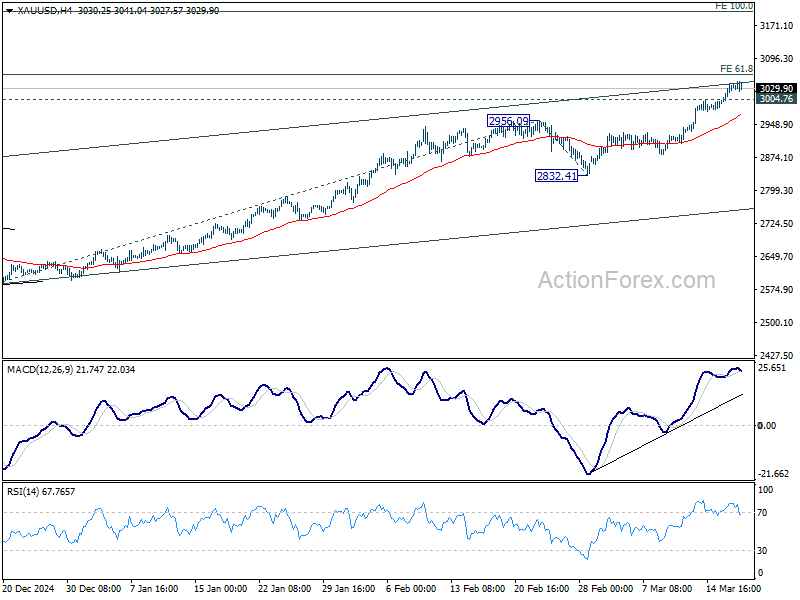

Technically, Gold is losing momentum as it approaches 61.8% projection of 2584.24 to 2956.09 from 2832.41 at 3062.21. This level is close to a key medium-term rising channel resistance, making it a critical test for gold bulls. A break below 3004.76 resistance-turned-support would signal the first rejection at the resistance zone, and leads to a near term pullback.

However, if Dollar resumes its selloff after Fed’s announcement, Gold could break through 3062.21, probably triggering upside acceleration towards 100% projection at 3204.26.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is down -0.81%. CAC is up 0.36%. UK 10-year yield is up 0.003 at 4.65. Germany 10-year yield is down -0.007 at 2.806. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 0.12%. China Shanghai SSE fell -0.10%. Singapore Strait Times rose 0.34%. Japan 10-year JGB yield rose 0.026 to 1.531.

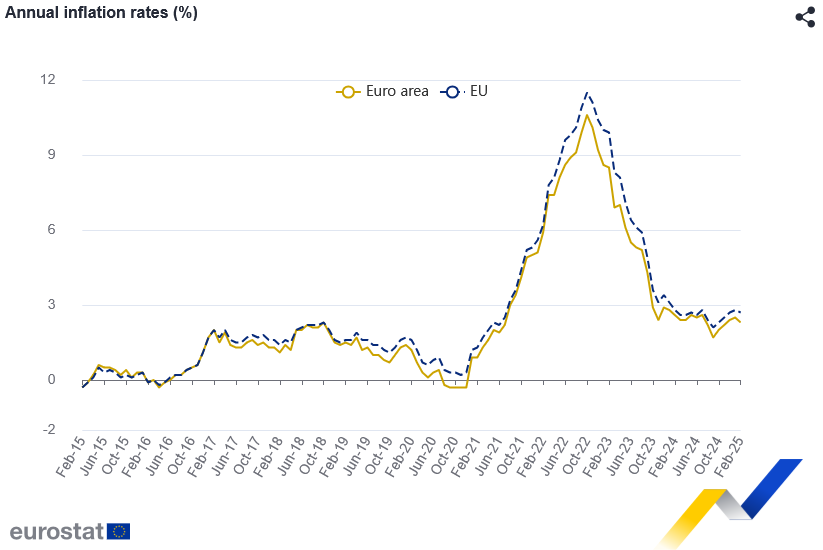

Eurozone CPI finalized at 2.3% in Feb, core CPI at 2.6%

Eurozone headline CPI was finalized at 2.3% yoy in February, down from 2.5% yoy in January. Core CPI , which excludes energy, food, alcohol, and tobacco, eased slightly to 2.6% yoy from 2.7% yoy.

The largest driver of Eurozone inflation was services, contributing +1.66 percentage points, followed by food, alcohol, and tobacco (+0.52 pp). Non-energy industrial goods and energy made smaller contributions, with energy adding just +0.01 pps.

In the broader EU, inflation was finalized at 2.7% yoy, down from 2.8% yoy in January. Inflation disparities across member states remain stark, with France (0.9%), Ireland (1.4%), and Finland (1.5%) registering the lowest rates, while Hungary (5.7%), Romania (5.2%), and Estonia (5.1%) recorded the highest. Compared to January, inflation declined in 14 member states, remained unchanged in six, and increased in seven.

BoJ holds rates, flags exchange rate as key inflation factor

BoJ kept its uncollateralized overnight call rate unchanged at around 0.50%, as widely expected.

In its statement, BoJ noted that growth is expected to remain above potential, while inflation progress remains on track toward its 2% target. However, policymakers flagged high levels of uncertainty, particularly citing global trade tensions and policy shifts in major economies as key risks.

A notable shift in BoJ’s tone was its heightened focus on exchange rate movements as a key factor influencing inflation. The central bank acknowledged that with firms increasingly raising wages and prices, exchange rate developments are, compared to the past, "more likely to affect prices".

This suggests that further depreciation in Yen could accelerate price increases, and influence future monetary policy decisions.

Japan’s export rises 11.4% yoy in Feb, up for fifth straight month

Japan’s exports surged 11.4% yoy to JPY 9,191B in February, marking the fifth consecutive month of growth, driven by strong demand from both the US and China. Exports to the US rose 10.5% yoy, while shipments to China saw an even stronger 14.1% yoy increase.

Meanwhile, imports declined by -0.7% yoy, marking their first drop in three months, as demand for crude oil and coal weakened. This shift in trade dynamics helped Japan return to a trade surplus of JPY 584.5B, the first positive balance in two months.

On a seasonally adjusted basis, exports rose 4.0% mom to JPY 9,688B, while imports fell -4.1% mom to JPY 9,505B, leading to a JPY 182B surplus.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2967; (P) 1.2988; (R1) 1.3025; More...

Intraday bias in GBP/USD is turned neutral first with current retreat. Another rise is expected as long as 1.2910 support holds. Above 1.3009 will resume the rally from 1.2099 to retest 1.3433 high. However, firm break of 1.2910 will indicate short term topping, likely with bearish divergence condition in 4H MACD. That would turn intraday bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

Ethereum Gives Way

Market picture

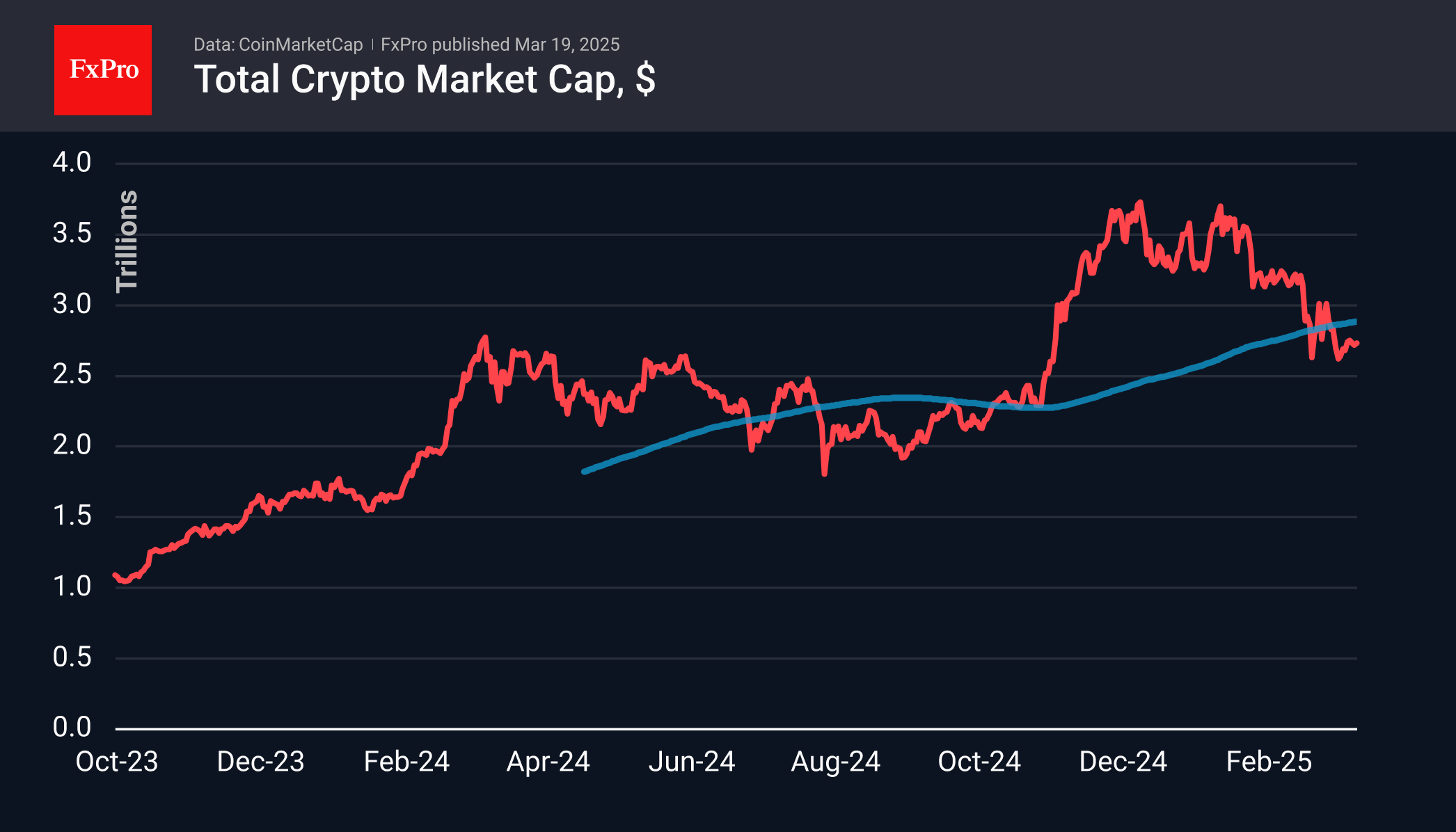

The crypto market remains in a downtrend. Its cap rose 0.2% over the past 24 hours to $2.72 trillion and generally remains in a very tight range with a short-term ceiling of $2.75 trillion. Just over a month ago, similar local resistance was half a trillion higher.

The crypto market remains in a downtrend, with resistance lowered to $2.75 trln from $3.25 trln

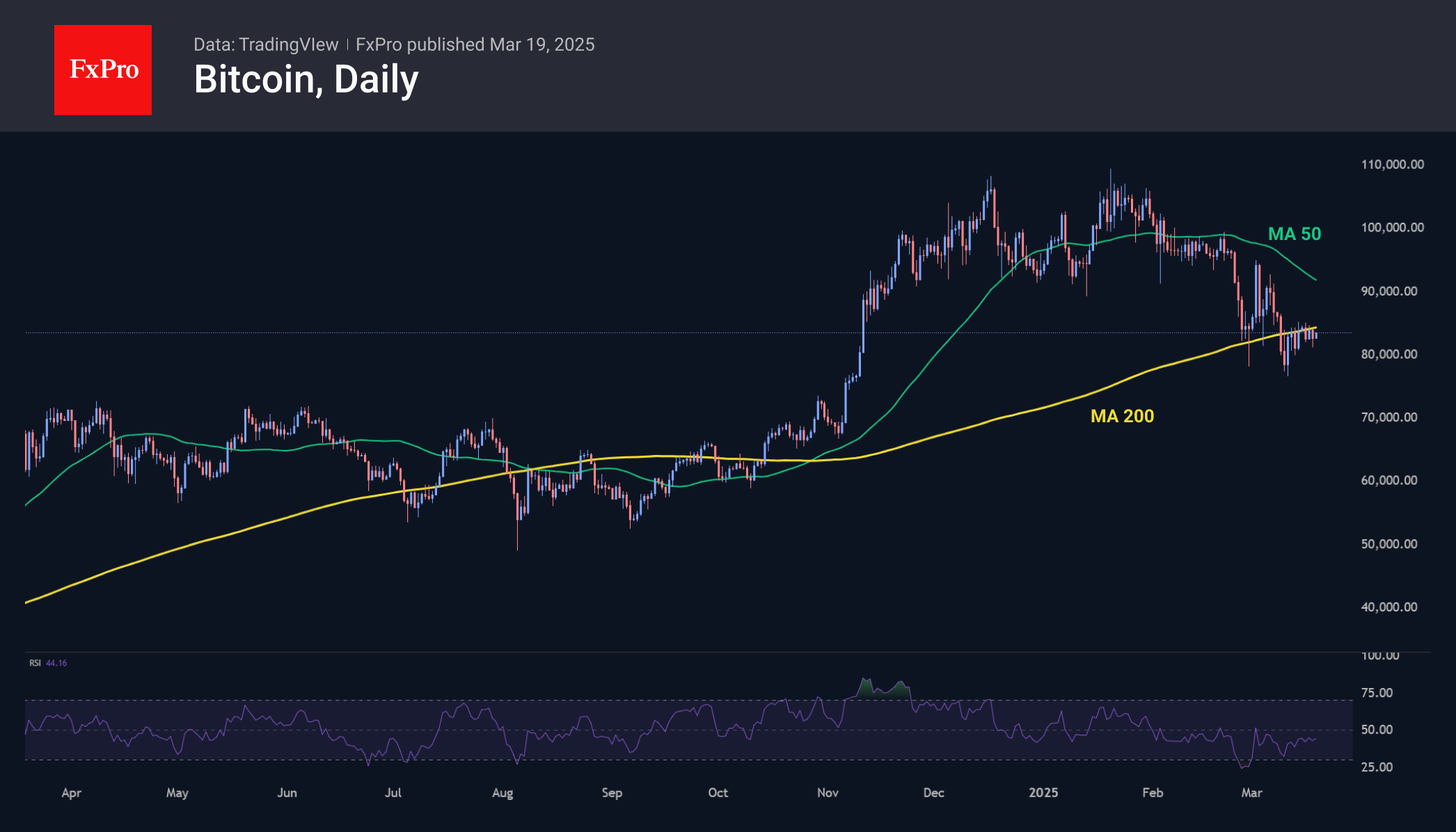

While almost all altcoins combined have been broadly stable at 30% market share since July 2023, Ethereum has been giving away its share since July 2024, falling to 8%, a five-year low. BTC’s share has been growing for more than two years, reaching 60.7%. Interest from institutional traders and governments has so far not extended beyond the first cryptocurrency, which they see as a strategic reserve asset rather than the practicality offered by altcoins, including ETH.

Bitcoin reversed to the downside again on Tuesday, touching its 200-day average. Nevertheless, it gained around 2% from the start of the day to $83.3K on Wednesday. Ultimately, it is worth paying closer attention to the dynamics of the crypto market after the Fed’s comments, as this could be the start of a longer trend.

News Background

Standard Chartered downgraded its 2025 Ethereum forecast from $10,000 to $4,000. One of the reasons is the growing influence of L2 solutions, especially the Base platform. The changes made to Ethereum in recent years, “while perhaps necessary, have damaged its value”.

The US Securities and Exchange Commission is set to relax storage requirements for crypto assets. Current SEC commissioner Mark Uyeda has ordered a review of a proposal to tighten storage rules for cryptocurrencies.

The GMCI Meme Coin Index, tracked by The Block, is down 90% from its peak in December, indicating a cooling of interest in this type of risky asset.

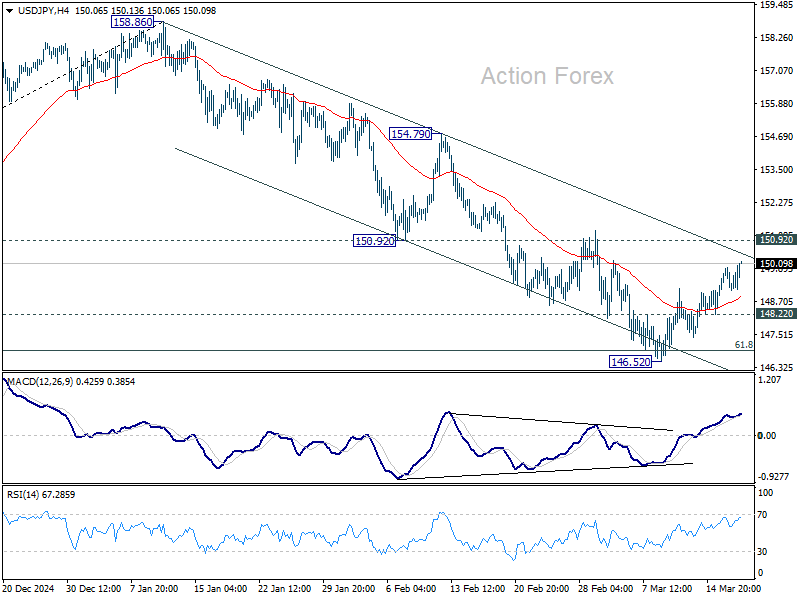

USD/JPY Outlook: Near-Term Recovery Faces Headwinds from Pivotal 150.00 Resistance

USDJPY attacked again pivotal 150 barrier (psychological / bear-channel upper boundary / 30 DMA) in early Wednesday, offsetting initial negative signal from Tuesday’ bearish inverted hammer that was formed after strong upside rejection just under 150 zone.

Yen was deflated by BoJ’s decision to keep interest rates unchanged at 0.5%, as policymakers responded to growing uncertainty over negative impacts from tariffs but also highlighted increased risk that trade war escalation may fuel inflation.

Mixed daily studies add to warning signals about possible stall of recovery leg from 148.53 (Mar 11 low) which was sparked by a double bear trap under 146.95 Fibo support.

Another failure at 150 pivot would increase downside risk, though near-term bias would remain with bulls as long as the price holds above 20DMA (148.86).

Firm break of 150 barrier to spark stronger acceleration higher and expose targets at 151.30/88 (Mar 3 lower top /200DMA).

Conversely, loss of 20DMA handle would weaken near term structure and generate initial signal that corrective phase might be over.

Res: 150.00; 150.73; 151.00; 151.30.

Sup: 149.14; 148.86; 148.35; 147.73.

Bank of Japan Maintains Rate, Yen Hits 150

The Japanese yen continues to lose ground against the US dollar. In the European session, USD/JPY is trading at 149.74, up 0.32% on the day. Earlier, the yen reached the symbolic 150 level for the first time in two weeks.

BoJ notes concern about US trade policy

There were no surprises from the Bank of Japan, which maintained rates at 0.50%. The decision was widely expected and the yen has posted modest losses today. The Bank's rate statement noted that "inflation expectations have risen moderately ", an acknowledgement of upwards pressure on inflation.

Governor Kazuo Ueda said at his press conference that "wage and price conditions are on track, possibly stronger than expected". However, Ueda added that the US and global outlook were "uncertain" and the Bank would determine its rate path based on upcoming data.

The BoJ has stressed that it will continue to hike rates if it sees that inflation is kept sustainable by rising wages. The BoJ wanted to see strong wage gains at the recent wage negotiations and should be pleased that large employers are offering wage hikes of around 5%.

Governor Ueda also expressed concern about US trade policy, saying "it is hard to qualify the risk" of US tariffs on Japan economic and inflation outlook. The US hasn't slapped tariffs on Japan but the country relies heavily on its export sector and Japanese manufacturers reported a decrease in confidence in March.

Fed expected to hold rates

The Federal Reserve meets later today and is virtually certain to maintain the benchmark rates at 4.25%-4.5%. The economic outlook has darkened recently, with the stock market selloff and an escalating trade war. The markets have priced in another hold at the May meeting at 83%, up from 56% in early March, according to CME FedWatch.

Eurozone CPI finalized at 2.3% in Feb, core CPI at 2.6%

Eurozone headline CPI was finalized at 2.3% yoy in February, down from 2.5% yoy in January. Core CPI , which excludes energy, food, alcohol, and tobacco, eased slightly to 2.6% yoy from 2.7% yoy.

The largest driver of Eurozone inflation was services, contributing +1.66 percentage points, followed by food, alcohol, and tobacco (+0.52 pp). Non-energy industrial goods and energy made smaller contributions, with energy adding just +0.01 pps.

In the broader EU, inflation was finalized at 2.7% yoy, down from 2.8% yoy in January. Inflation disparities across member states remain stark, with France (0.9%), Ireland (1.4%), and Finland (1.5%) registering the lowest rates, while Hungary (5.7%), Romania (5.2%), and Estonia (5.1%) recorded the highest. Compared to January, inflation declined in 14 member states, remained unchanged in six, and increased in seven.

Japanese Yen Continues to Slide as Bank of Japan Disappoints Markets

The USD/JPY pair surged to 149.58 on Wednesday, marking its fourth consecutive day of gains as the Japanese yen extended its decline. The Bank of Japan's (BoJ) latest policy decision failed to inspire confidence, leaving investors underwhelmed and further weakening the yen.

Key factors driving USD/JPY movement

As expected, the Bank of Japan maintained its benchmark interest rate at 0.5% while reiterating its forecast that the Japanese economy will grow above its potential level. However, the central bank also acknowledged emerging signs of economic fragility, adopting a cautious tone in its outlook. Policymakers emphasised the need to gather and analyse more data before making significant moves, particularly in light of global economic risks.

A key concern is the potential impact of US tariff hikes, which could weigh heavily on Japan's export-driven economy. Investors are now closely monitoring comments from BoJ Governor Kazuo Ueda for further insights into the central bank's strategy and future policy direction.

Recent data has painted a mixed picture of Japan's economic health. The monthly Reuters Tankan survey revealed growing pessimism among Japanese manufacturers in March, citing concerns over US trade policies and China's slowing economy. On a brighter note, Japan's trade balance shifted to a surplus in February, driven by robust export growth. However, this improvement has done little to strengthen the yen amid broader market concerns.

Technical analysis of USD/JPY

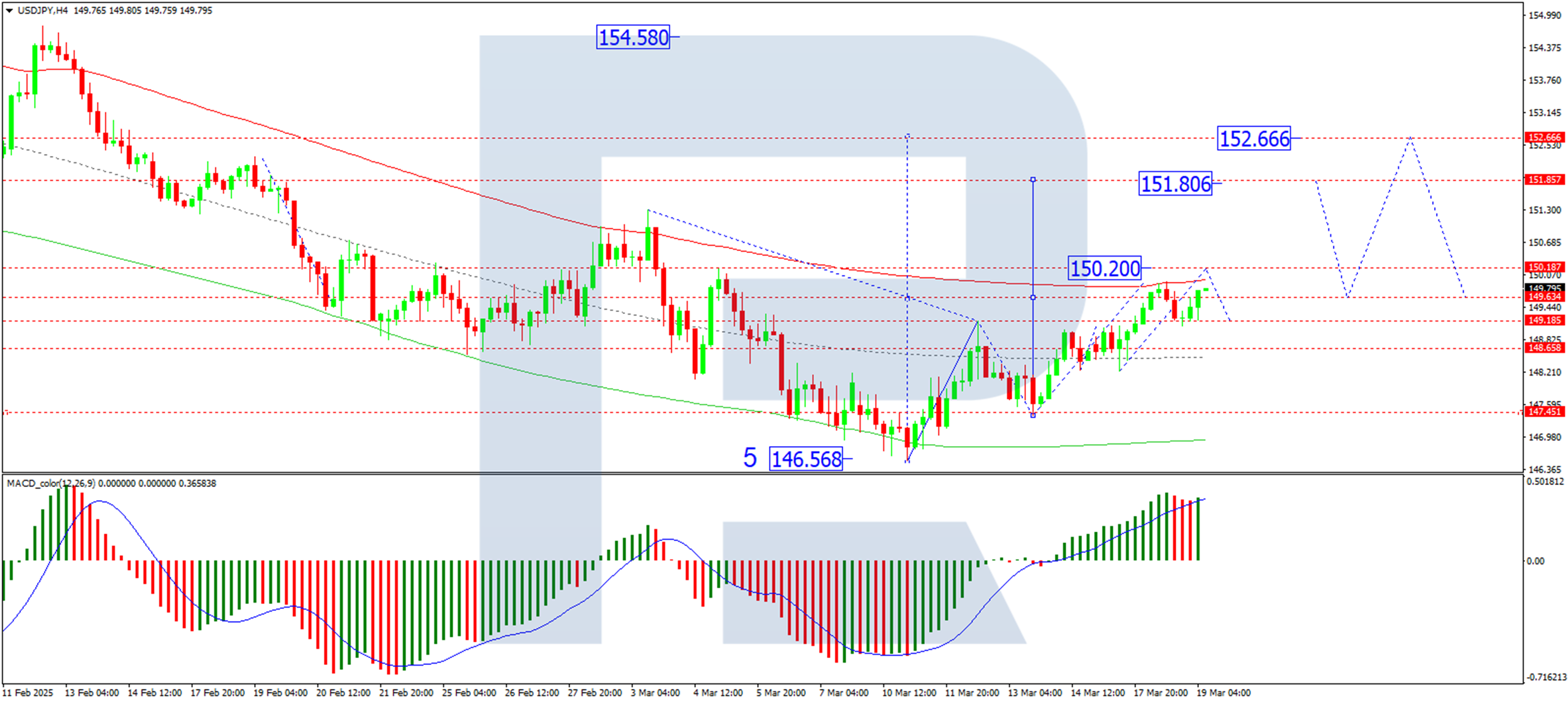

On the H4 chart, USD/JPY is forming a bullish wave structure, targeting 150.20. Upon reaching this level, a corrective pullback to 149.20 is possible, likely establishing a consolidation range near the current highs. A breakout above this range could signal further upward momentum, with the next target at 151.80. This scenario is supported by the MACD indicator, with its signal line remaining above zero and trending upwards.

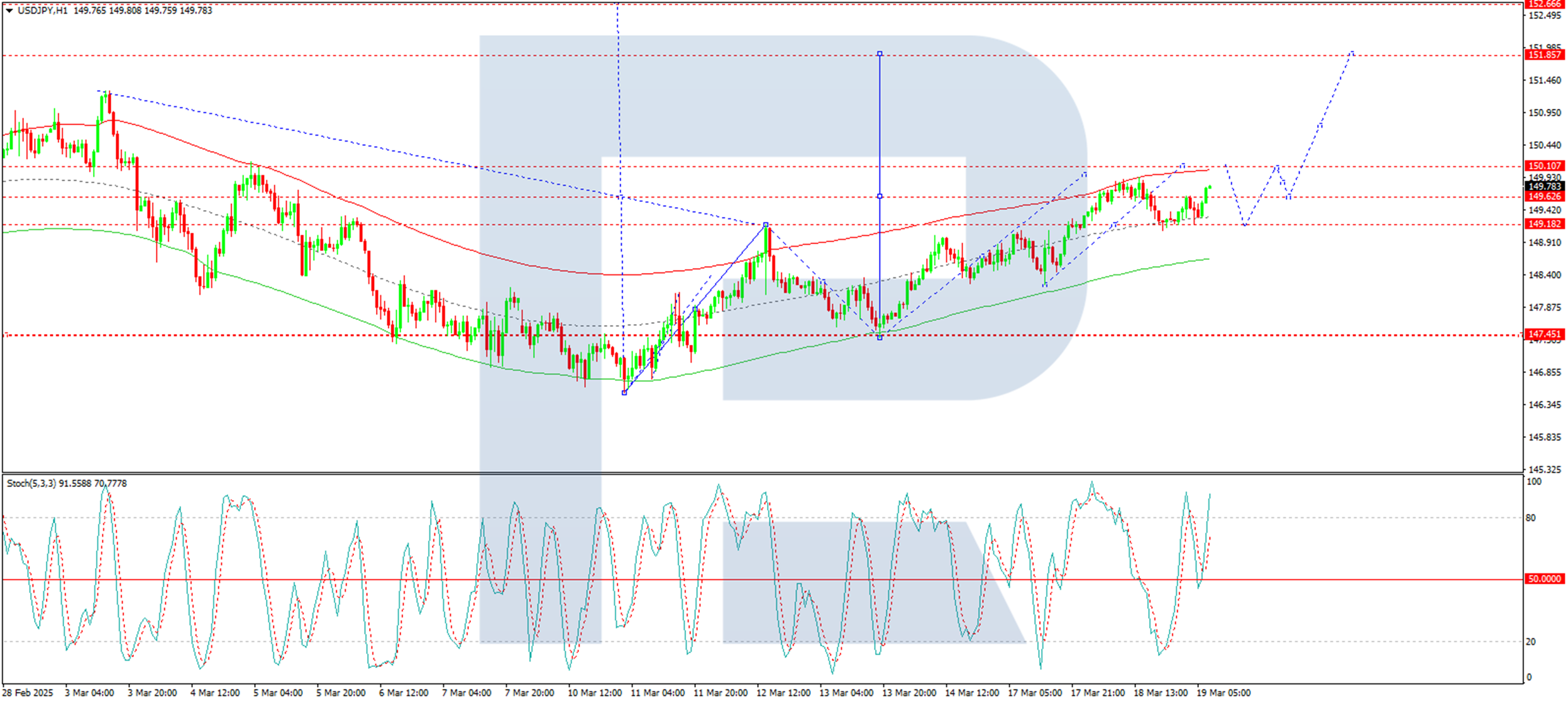

The H1 chart shows USD/JPY developing a growth wave toward 150.20, representing the midpoint of the third wave in the current structure. A consolidation range is expected to form around 149.62, with an upward breakout potentially opening the path to 151.80. The Stochastic oscillator corroborates this outlook, with its signal line above 50 pointing upward.

Conclusion

The Japanese yen's decline reflects market disappointment with the Bank of Japan's cautious stance and lack of decisive action. While Japan's trade balance has shown improvement, concerns over global economic risks and domestic manufacturing sentiment continue to weigh on the currency. From a technical perspective, USD/JPY remains in a bullish trend, with key resistance levels at 150.20 and 151.80. Traders should monitor BoJ Governor Ueda's statements and upcoming economic data for further clues on the yen's trajectory.

Gold Price Surpasses $3,000 per Ounce for the First Time in History

Just five days ago, we noted that gold was approaching the $3,000 level and suggested that a breakout could occur this month.

Yesterday, as shown on the XAU/USD chart, the spot price of gold rose above the psychological $3,000 mark for the first time ever. The new all-time high now stands at around $3,045.

Why Is Gold Rising?

Bullish sentiment is being driven by traders positioning themselves ahead of a key event—the Federal Reserve’s interest rate decision, set to be announced today. According to ForexFactory, analysts expect rates to remain unchanged at 4.5%, but surprises cannot be ruled out.

Additionally, gold is becoming more attractive as a safe-haven asset. As reported by Reuters:

→ Tensions in the Middle East are escalating—Israel warns of further casualties, as airstrikes in Gaza have already resulted in over 400 deaths.

→ Gold is gaining amid uncertainty over US tariffs.

Technical Analysis of XAU/USD Chart

In the short term, gold’s price action has formed movements that outline an ascending channel (marked in blue), with key developments including:

→ A breakout (as shown by the arrow) above not only the psychological $3,000 level but also the upper boundary of the channel.

→ A prior consolidation zone formed between $3,000 and $2,980.

It seems the bulls were looking for confirmation and confidence before attempting to break through resistance. The fact that they succeeded suggests this resistance zone may now act as support, making a retest of $3,000 possible.

However, the future direction of gold prices will largely depend on the news backdrop. Brace for volatility—the Fed's interest rate decision will be released today at 21:00 GMT+3, followed by a press conference by Chair Jerome Powell at 21:30 GMT+3.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

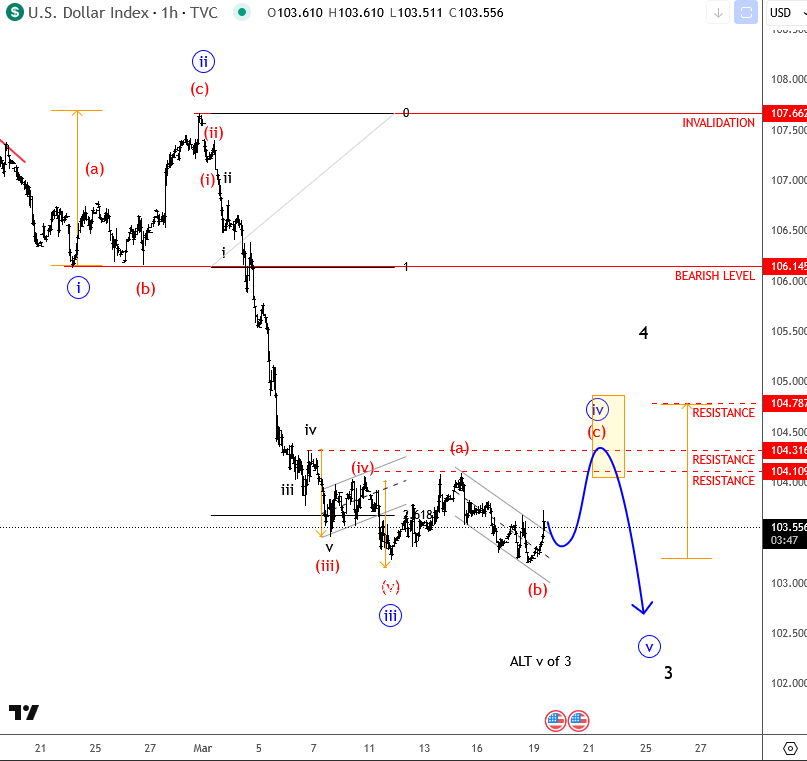

Elliott Waves Shows Corrective Wave Four on DXY

The US dollar weakened slightly yesterday despite lower stocks, which remain in consolidation ahead of the key Fed decision—or more importantly, the press conference—where we may get more clarity on whether policy will become even more dovish. This is especially relevant given the sharp stock market drop in last few weeks amid uncertainty over Trump’s tariffs. If Powell sounds dovish, stocks could stabilize, US yields could ease, and the dollar could face even more downside pressure, as it is already in a strong impulsive sell-off.

Looking at the dollar index on the hourly time frame, the market only retested the previous lows around 103.25 and is now attempting to break out of the downward channel. This suggests that we could still be in a higher-degree, complex wave four consolidation, as discussed yesterday. If so, there is still a chance for a retest of the 104.10 to 104.30 resistance area. Above that, the key level to watch is 104.80, where wave four would equal wave two in length.

I'm still watching EURUSD for potential longs, but it's best to be patient and wait for the Fed decision first. After the event, we may get clearer opportunities to enter.