Sample Category Title

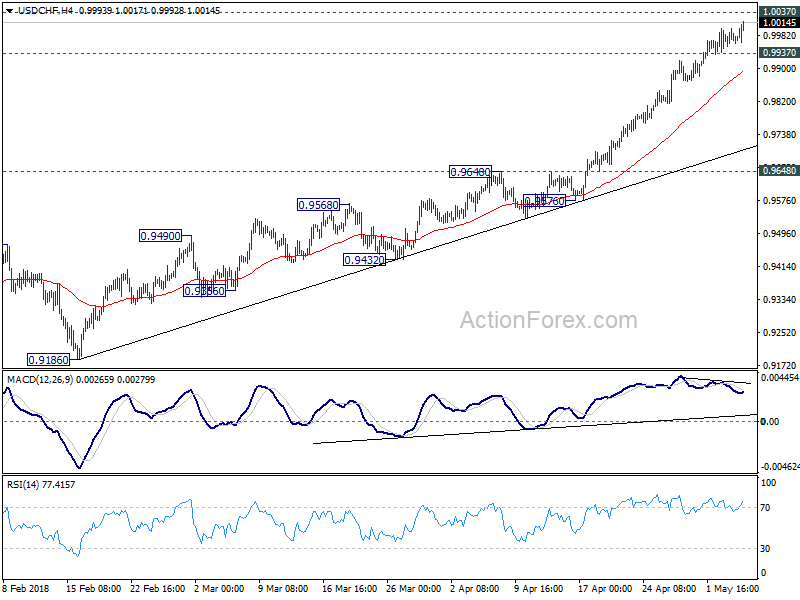

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9952; (P) 0.9976; (R1) 1.0017; More...

USD/CHF's rally continues in early US session and edges higher to 1.0017. While upside momentum is unconvincing as see in 4 hour MACD, intraday bias stays on the upside for further rally. Decisive break of 1.0037 resistance will extend the whole rally from 0.9186 towards 1.0342 key resistance On the downside, though, below 0.9937 minor support will indicate short term topping. And, in that case, deeper retreat could be seen to 4 hour 55 EMA (now at 0.9894) and below before staging another rise.

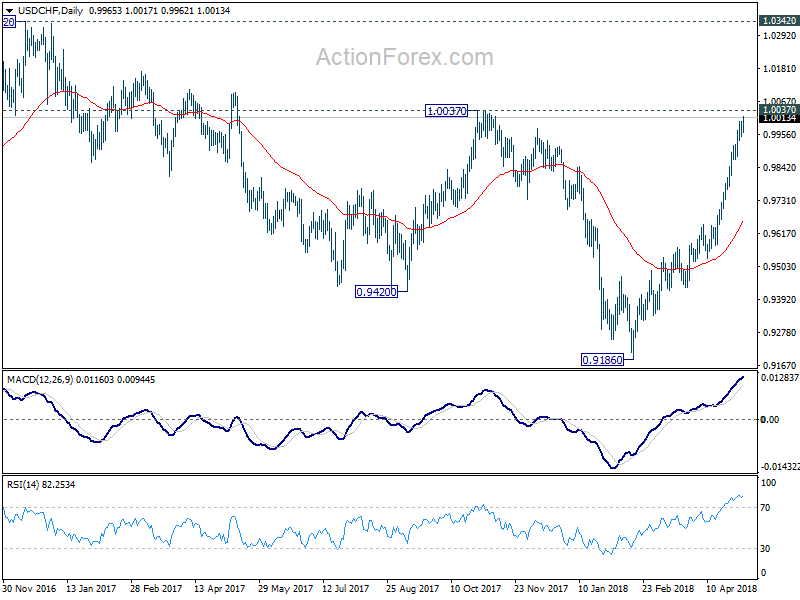

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.

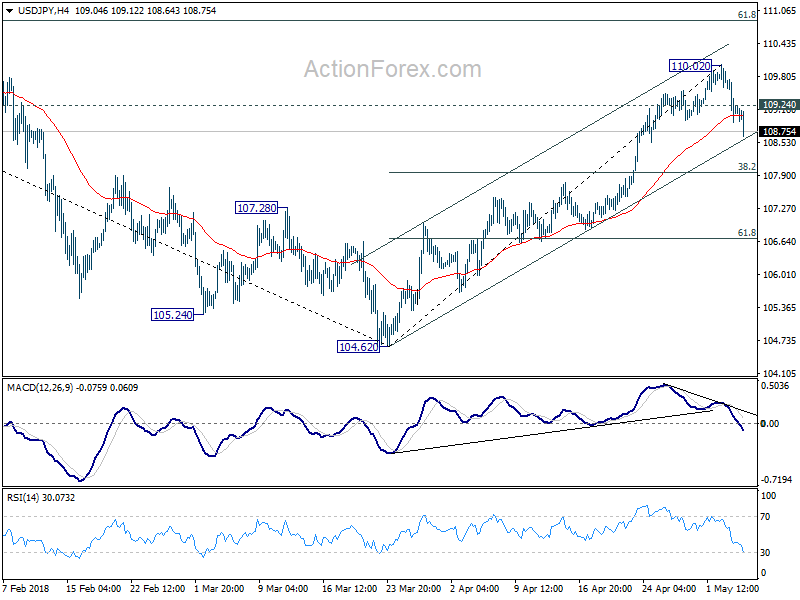

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.78; (P) 109.33; (R1) 109.74; More...

USD/JPY drops to as low as 108.64 so far as the correction from 110.02 short term top extends. Intraday bias stays on the downside for near term channel support (now at 108.56) and below. But we'd expect strong support from 38.2% retracement of 104.62 to 110.02 at 107.95 to contain downside and bring rebound. Above 109.24 minor resistance will bias back to the upside for 110.02. Break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.97).

It’s Still the Yen’s Show after US Non-Farm Payrolls and Wage Growth Missed Expectations

Dollar fails to regain spot light after worse than expected job data. Non-farm payroll showed 164k growth in April only, below expectation of 194k. Prior month's figure, though, was revised up from 103k to 135k. Unemployment rate dropped to 3.9%, down from 4.1% and beat expectation of 4.0%. That's also the lowest level since late 2000. But wage growth is another disappointment. Average hourly earnings rose only 0.1% mom, slowed from prior 0.3% and missed. expectation of 0.2% mom.

USD/JPY suffers steep selloff immediately after the release, hitting as low as 108.65 so far, comparing to day high at 109.23. But the greenback is staying in tight range against other major currencies including Euro, Sterling, Swiss Franc, Aussie and Canadian. It's actually still the Yen's show right now as EUR/JPY dives to as low as 130.01, comparing with day high at 130.93. GBP/JPY hits as low as 147.32, comparing to day high at 148.29.

For Dollar, levels to watch are 1.2031 minor resistance in EUR/USD, 1.3629 minor resistance in GBP/USD, 0.7583 minor resistance in AUD/USD and 0.9937 minor support in USD/CHF. As long as these level holds, Dollar's rally is still expected to resume sooner rather than later.

US gave China a "detailed list of asks" in Beijing

It's reported that US Treasury Secretary Steven Mnuchin gave China a "detailed list of asks" during their trade negotiation talks in Beijing. In short, US asks China to narrow trade surplus by US 200B by 2020, reduce trade imbalance immediately, halt subsidies for advanced tech, cut tariffs on all products to levels no higher than that of US, refrain from targeting US farmers and agricultural products, refrain from retaliating against US restrictions on investments from China.

In an editorial in the official China Xinhua, it's set that China and the US "reached agreements" on some issues in the trade talks. And both sides agreed to set up a "work mechanism" to keep close communications. But there are "considerable differences" that still exist on some issues and "continued hard work is required for more progress".

Eurozone PMIs not yet at "worringly low level"

Eurozone PMI services was finalized at 54.7 in April, revised down from 55.0. Prior month's reading was 54.9. Eurozone PMI composite was finalized at 55.1, revised down from 55.2. Prior month's reading was 55.2. German PMI composite dropped to 19-month low at 54.6. Italy PMI composite dropped to 15-month low at 52.9. On the other hand, France PMI composite rose to 2 month high at 56.9. Ireland PMI composite rose to 3 month high at 57.6.

Chris Williamson, Chief Business Economist at IHS Markit noted that "the final PMI numbers confirm the marked, broadbased fading of the eurozone's growth spurt so far this year." However, it's not yet a "worryingly low level" even though there will be further easing in the coming months.

Constancio: ECB is now a modern, effective and prepared central bank

In a speech titled "Past and future of the ECB monetary policy", ECB Vice President Vitor Constancio reviewed the four phases in the ECB journey since 1999. They are the beginning, pre-crisis, global financi crisis and great financial, and ultra-low and QE. And after going through the journey, the "new unconventional instruments, along with forward guidance, negative rates and reverse repos belong now to the monetary policy toolkit to be used whenever necessary." And ECB will have "no excuse" no to fulfil its mandate.

ECB has also joined the "community of central banks of other major jurisdictions using flexible inflation targeting regimes and asset purchases as non-standard measures." ECB is now a "modern, effective and prepared central bank to serve the goals of monetary union." Full speech here

RBA to stay patient despite slightly more positive than expected forecasts

In RBA's latest Statement on Monetary Policy, economic projections were largely unchanged. Overall, the projections are slightly more positive than expected. But there wouldn't be any change to the expectation that RBA will stand pat throughout 2018, at least. There was no downward revision in GDP forecast. Underlying inflation forecasts were revised slightly up. On the negative side, unemployment rate will take longer to drop again.

Unrevised, year-average GDP growth is forecast to be at 3.00% in 2018 and 3.25% in 2019. CPI inflation is forecast to rise to 2.25% at 2018 year end and stay there till June 2020.

The first change is that unemployment rate forecast was raised to 5.50% in June 2018 and December 2018, revised up from 5.25%. Onwards, unemployment rate is projected to drop to 5.25% in June 2019 and stay there till June 2020.

The second change is that underlying inflation is expected to be higher at 2.00% in June 2018 and December 2018, revised up from 1.75%. Then underlying inflation is projected to stay a 2.00% till picking up again to 2.25% in June 2020.

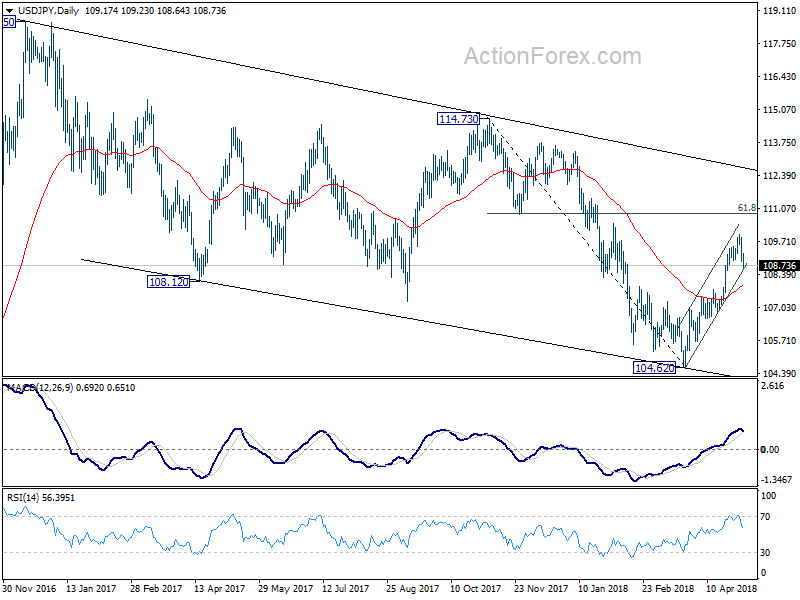

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.78; (P) 109.33; (R1) 109.74; More...

USD/JPY drops to as low as 108.64 so far as the correction from 110.02 short term top extends. Intraday bias stays on the downside for near term channel support (now at 108.56) and below. But we'd expect strong support from 38.2% retracement of 104.62 to 110.02 at 107.95 to contain downside and bring rebound. Above 109.24 minor resistance will bias back to the upside for 110.02. Break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.97).

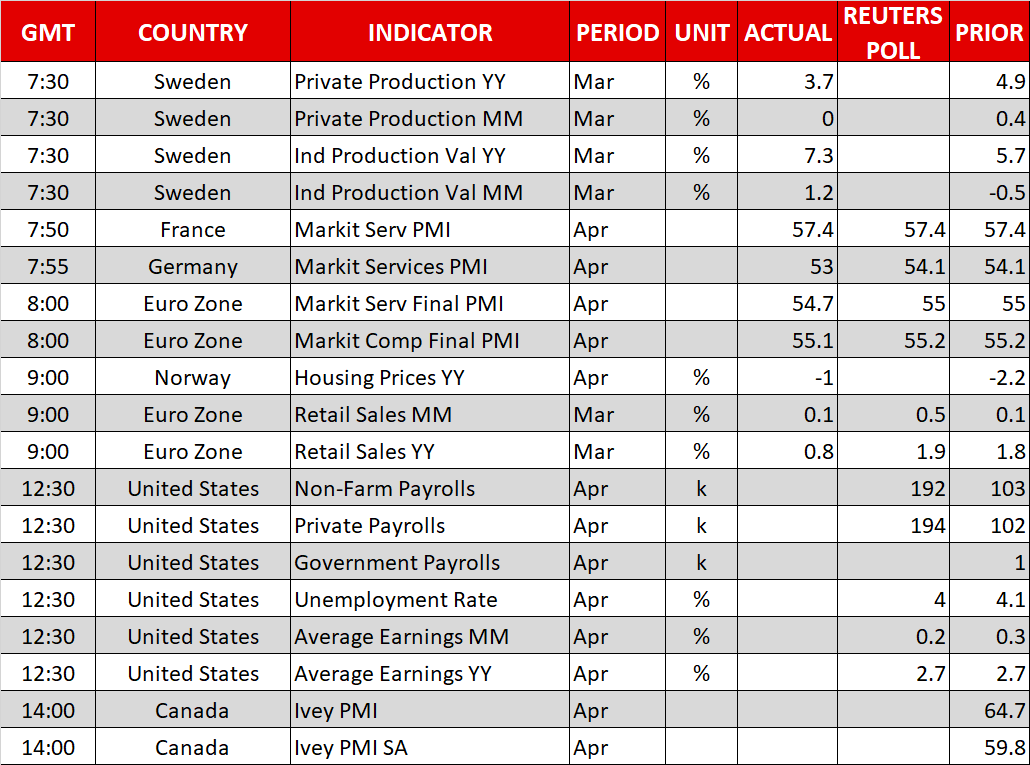

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 01:45 | CNY | Caixin PMI Services Apr | 52.9 | 52.3 | 52.3 | |

| 07:45 | EUR | Italy Services PMI Apr | 52.6 | 53 | 52.6 | |

| 07:50 | EUR | France Services PMI Apr F | 57.4 | 57.4 | 57.4 | |

| 07:55 | EUR | Germany Services PMI Apr F | 53 | 54.1 | 54.1 | |

| 08:00 | EUR | Eurozone Services PMI Apr F | 54.7 | 55 | 55 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Mar | 0.10% | 0.50% | 0.10% | 0.30% |

| 12:30 | USD | Change in Non-farm Payrolls Apr | 164K | 194K | 103K | 135K |

| 12:30 | USD | Unemployment Rate Apr | 3.90% | 4.00% | 4.10% | |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.10% | 0.20% | 0.30% | |

| 14:00 | CAD | Ivey PMIs Index Apr | 60.2 | 59.8 |

Non-farm payroll and wage growth missed expectations, unemployment rate dropped to lowest since 2000

US non-farm payrolls rose 164k in April, below expectation of 194k. Prior month's figure was revised up from 103k to 135k.

Unemployment rate dropped to 3.9% , down from 4.1% and beat expectation of 4.0%. That's the lowest level since the end of 2000.

Average hourly earnings rose 0.1% mom only, below expectation of 0.2% mom.

Notable buying is seen in the Japan yen after the report, with USD/JPY driving to as low as 108.65 so far. But Dollar is steady against Euro, Swiss, Sterling, Aussie and Canadian, in tight range.

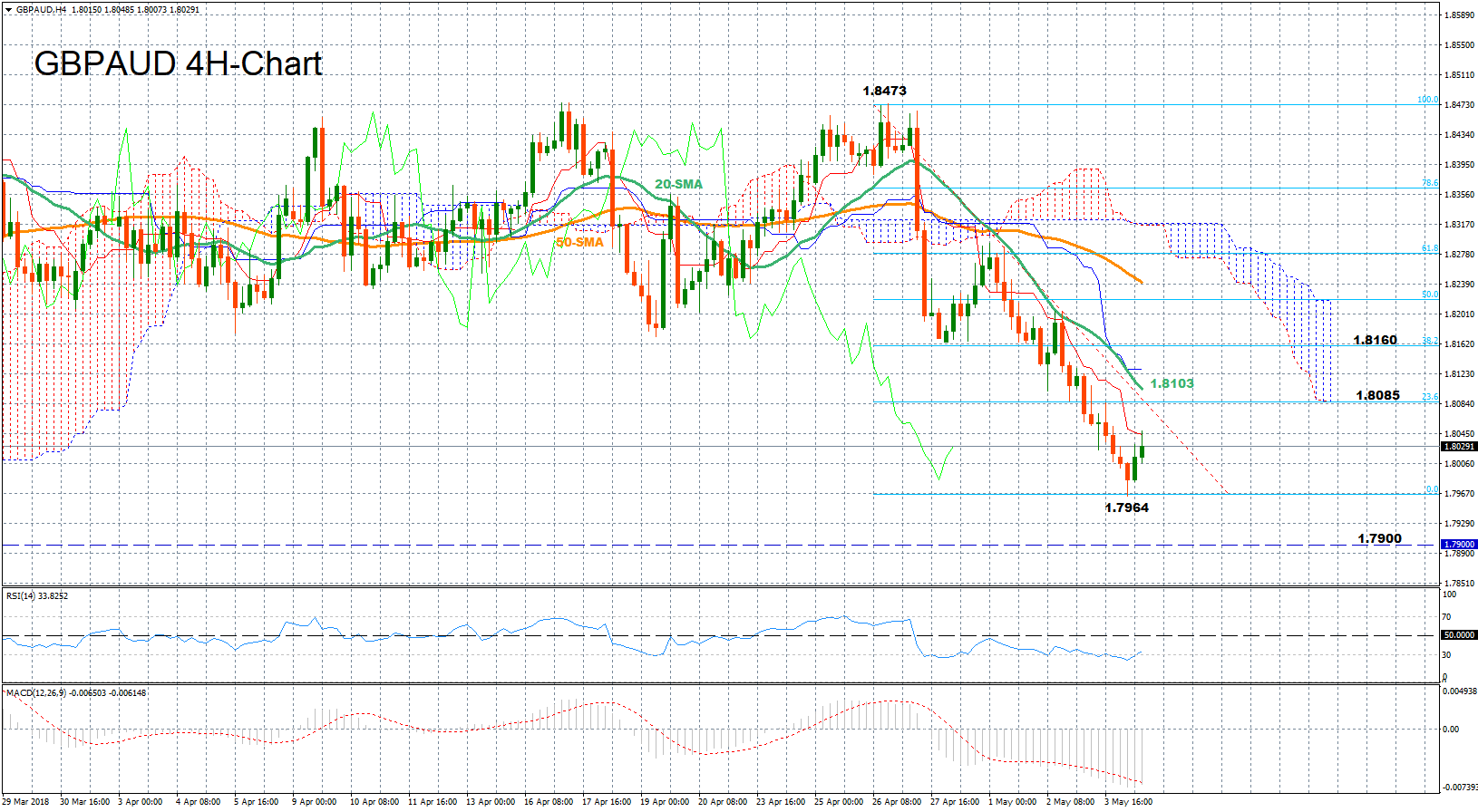

GBPAUD Rebounds; Downside Trend to Remain in Place

GBPAUD bounced up after it hit a 6 ½-week low of 1.7964 today as the RSI inched down to oversold levels, signaling that the recent downfall could be overstretched. The RSI is now back above 30 and is moving upwards, while the MACD is still in negative territory but is pushing up momentum to cross above its red signal line. Both suggesting that the pair could post further gains in the near-term.

However, looking at the simple moving average lines (SMA), the 20-period SMA continues to deviate below the 50-period SMA, therefore, despite any short-term rebound the broader trend could remain on the downside. This is also confirmed by the Ichimoku indicators as the red Tenkan-sen line shows no sign of pulling up to meet the blue Kjjun-sen line.

Should the pair stretch up, the 23.6% Fibonacci of 1.8085 of the dowleg from 1.8473 to 1.7964 could offer nearby resistance ahead of the 20-period SMA which currently stands at 1.8103. Even higher, the 38.2% Fibonacci of 1.8160 could be a stronger obstacle for the bulls to break through; this is the bottom of the March 3 – May 2 range-bound trading.

Alternatively, if the market weakens, support could come from the 1.7964 trough. Any violation of this point could extend the downward trajectory towards the 1.7900 psychological level.

Greenback Firms As Markets Await US Employment Data

Here are the latest developments in global markets:

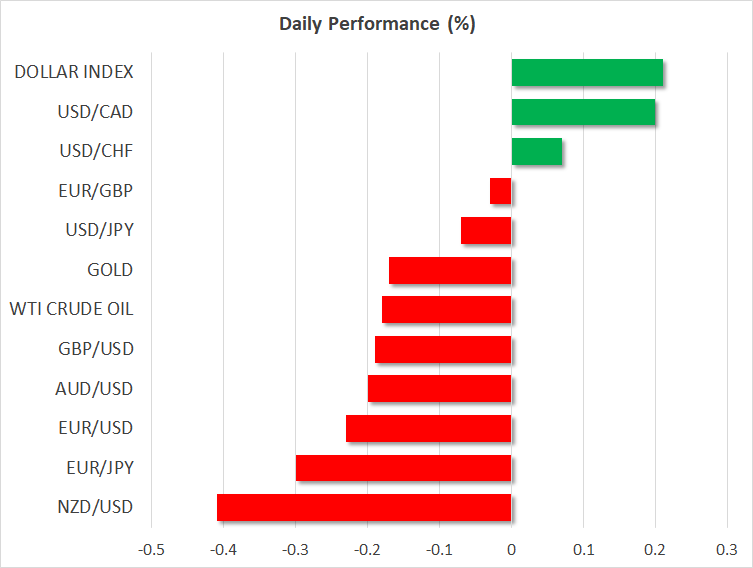

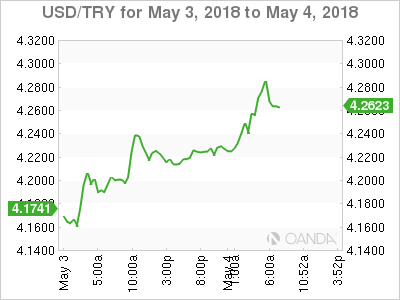

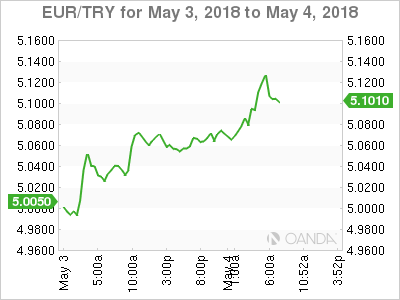

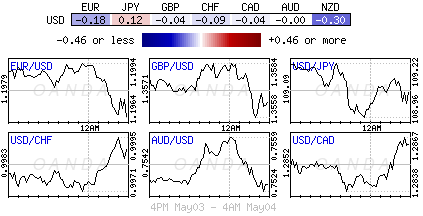

FOREX: The dollar index, which gauges the greenback’s strength versus six major currencies, edged higher by 0.20% during the European session to 92.55, approaching the four-month high of 92.63 reached on Wednesday. Euro/dollar remained under selling pressure after Eurozone’s retail sales and final services PMI figures were weaker than expected, slipping by 0.23%. Meanwhile, dollar/yen retreated to 109.05 (-0.08%), with the focus remaining on whether US jobs data will provide the spark for another push higher. Pound/dollar touched an almost four-month low on Thursday at 1.3537 and was still trading negative today by 0.15% as traders remained skeptical of whether the BoE will deliver a rate hike in May. The antipodean currencies headed lower, with aussie/dollar erasing earlier gains and kiwi/dollar falling, towards 0.7516 (-0.19%) and 0.7010 (-0.41%) respectively. Dollar/loonie was moving sideways around 1.2872. Elsewhere, the Turkish lira weakened to a fresh record low versus the greenback. Dollar/lira advanced by 1.74% to 4.2852, after briefly touching a new high of 4.2894.

STOCKS: European stocks gained some ground overall despite a decline in Asian markets as investors assessed trade talks between the US and China. The benchmark European STOXX 600 rose by 0.25%, while the blue-chip Euro STOXX 50 was down by 0.03%. The German DAX 30 moved higher by 0.30%, the French CAC 40 dived by 0.20%, the Spanish IBEX 35 edged up by 0.15% and the British FTSE 100 advanced by 0.51%. In the US, futures tracking the S&P 500, Dow Jones, and Nasdaq 100 are currently in the red – pointing to a lower open today – albeit only marginally so.

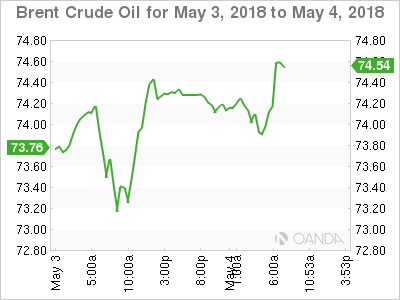

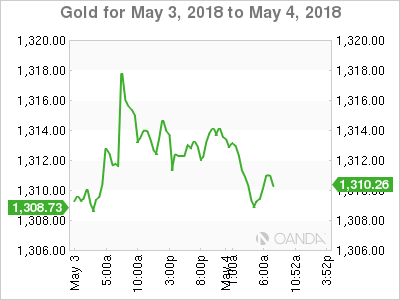

COMMODITIES: Oil prices eased today as the market awaited news from Washington on possible new US sanctions against Iran. West Texas Intermediate crude fell by 0.20% to $68.29 a barrel and Brent declined by 0.22% to $73.46 a barrel. Gold turned negative on a firmer dollar, dropping by 0.14%, while investors turned their focus on the US jobs data later in the day.

Day ahead: US employment report to dominate attention

The main event today will be the release of the US employment report for April, at 1230 GMT. Nonfarm payrolls are expected to have risen by 192k, much higher than the 103k recorded in March. Meanwhile, the unemployment rate is projected to tick down to 4.0%, from 4.1% in the previous month. As for the all-important average hourly earnings, the forecast is for the monthly rate to have slipped to 0.2%, from 0.3% previously, which would keep the yearly rate unchanged at 2.7%.

As has been the case with recent jobs reports, attention is likely to fall mainly on earnings. Payrolls and the unemployment are of course very important, but a strong set of numbers on that front would simply confirm what investors already know; that employment growth remains strong. On the other hand, wage growth is the missing piece of the puzzle for the Fed. It has not picked up in a meaningful way despite a tight labor market, confounding policymakers that expect rising wages to push up inflation. Accelerating wages would signal higher inflation down the road, sparking bets for a more hawkish Fed, and vice versa. Therefore, the dollar is likely to move in tandem with any surprise in earnings today; higher in case of a beat, and lower should they disappoint.

US stock markets are likely to be affected by the jobs data as well. Expectations for higher interest rates typically spell bad news for equity indices, while anything that suggests rates may stay low for longer is usually positive. Thus, should strong data spark bets for a more hawkish Fed, then equities are likely to experience declines, whereas a disappointment in the figures could lead to a move higher.

Elsewhere, Canada’s Ivey PMI for April will be in focus at 1400 GMT.

In energy markets, the Baker Hughes oil rig count at 1700 GMT should provide a fresh indication of whether US production continues to soar.

As for the speakers, the New York and San Francisco Fed Presidents, William Dudley and John Williams, will deliver remarks at 1445 and 1730 GMT respectively. A few hours later at 2130 GMT, Fed Board Governor Randal Quarles will step up to the rostrum. All these officials are voting members of the FOMC this year, so their comments will be closely watched. This may be especially true in the case of John Williams, who will be replacing Dudley as the influential head of the New York Fed soon.

European PMI Services Continues The Trend Of Disappointing Data

- Focus on upcoming US jobs report. The US-China trade talks have produced positive headlines but provided little inspiration for risk to rally

- Major European PMI Services data was disappointing during the session (Beats: None ; Misses: Euro Zone, Germany, Italy, Spain; In-line: France)

Asia:

- RBA Quarterly Statement reiterated the view that the board saws no strong case for near-term move in cash rate; higher rates likely to be “appropriate” at some time if economy improved as expected

- China Apr Caixin PMI Services: 52.9 v 52.3e

- North Korea said to agree to full denuclearization by 2020 and accepted IAEA inspections of its nuclear facilities

- Japan, China and South Korea Finance leaders statement highlighted the risks posed by rising trade protectionism

Europe:

- Some UK officials said to believe that Brexit transition period will need to be extended potentially for years because any new customs regime will not be ready to come into force in time

- UK may not be able to leave customs union until 2023 as it would take 5 years to implement the technological Irish border fix

- Brexit Secretary Davis said to have hinted he might quit the Cabinet because of Britain’s customs union row

- UK PM May Conservative Party said to hold on to overall control of London’s Wandsworth council in local government elections

- NIESR cuts UK 2018 growth forecast from 1.9% to 1.5%. BoE would not raise interest rates in May (meeting is next week) but was still set to start continuing normalizing its policy and hike again in August

Americas:

- Treasury Sec Mnuchin stated that the US and China were having very good conversation on trade

Economic Data:

- (IN) India Apr Services PMI: 51.4 v 50.3 prior, Composite PMI: 51.9 v 50.8 prior

- (SE) Sweden Apr Services PMI: 60.1 v 59.2 prior

- (FR) France Mar Trade Balance: -€5.3B v -€5.0Be

- (FR) France Mar Current Account Balance: -€1.3B v -€0.9B prior

- (FR) France Mar YTD Budget Balance: -€33.1B v -€28.5B prior

- (ES) Spain Apr Net Unemployment M/M: -86.7K v -100.6Ke

- (HU) Hungary Mar Retail Sales Y/Y: 7.1% v 6.0%e

- (ES) Spain Apr Services PMI: 55.6 v 56.1e (53rd month of expansion), Composite PMI: 55.4 v 55.5e

- (ZA) South Africa Apr PMI (whole economy): 50.4 v 52.0e (3rd month of expansion)

- (SE) Sweden Mar Private Sector Production M/M: 0.0% v 0.3%e; Y/Y: 3.7% v 4.2%e

- (SE) Sweden Mar Industrial Orders M/M: -1.7% v +0.2% prior; Y/Y: -1.9% v +0.7% prior

- (SE) Sweden Mar Industry Production Value Y/Y: 7.3% v 5.1%e, Service Production Value Y/Y: 4.8% v 4.5%e

- (IT) Italy Apr Services PMI: 52.6 v 53.0e (22nd month of expansion), Composite PMI: 52.9 v 53.7e

- (FR) France Apr Final Services PMI: 57.4 v 57.4e (confirmed 22nd month of expansion), Composite PMI: 56.9 v 56.9e

- (DE) Germany Apr Final Services PMI: 53.0 v 54.1e (confirmed 58th month of expansion), Composite PMI: 54.6 v 55.3e

- (EU) Euro Zone Apr Final Services PMI: 54.7 v 55.0e (confirmed 58th month of expansion, Composite PMI: 55.1 v 55.2e

- (UK) Apr New Car Registrations Y/Y: +10.4% v -15.7% prior

- (RU) Russia Narrow Money Supply w/e Apr 27th: 9.91T v 9.87T prior

- (CN) China Q1 Preliminary Current Account: -$28.2B v +62.3B q/q

- (TW) Taiwan Apr Foreign Reserves: $457.1B v $457.2B prior

- (EU) Euro Zone Mar Retail Sales M/M: 0.1% v 0.5%e; Y/Y: 0.8% v 1.9%e

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.2% at 385.5, FTSE +0.5% at 7537, DAX +0.2% at 12713, CAC-40 -0.3% at 5487, IBEX-35 +0.2% at 10058, FTSE MIB +0.4% at 24157, SMI +0.4% at 8878, S&P 500 Futures -0.1%]

- Market Focal Points/Key Themes: European Indices trade mixed this morning ahead of US Non Farm Payrolls and after mixed earnings this morning. The French CAC underperforms weighed down by banking names, with BNP Paribas and SocGen both trading lower after missing estimates. In the UK HSBC trades lower after a profit miss. In other notable earners BMW trades lower after weaker Revenue numbers, Airliners IAG trades higher while Air France trades lower after warning on lower operating profits due to the recent strikes. Looking ahead notable earners include Alibaba, Celgene and Aon.

Movers

- Consumer Discretionary [ Int Cons Airlines [IAG.UK] +5.7% (Earnings), Pearson [PSON.UK] +5.1% (Earnings), Air France [AF.FR] -7% (Earnings), Oriflame [ORI.SE] -17% (Earnings) ]

- Industrials [BMW [BMW.DE] -1.6% (Earnings), Basf [BAS.DE] +1.1% (Earnings) ]

- Financials [HSBC [HSBA.UK] -3% (Earnings), BNP Paribas [BNP.FR] -2.5% (Earnings), SocGen [GLE.FR] -6.5% (Earnings)]

- Energy [Vestas Wind [VWS.DK] -3% (Earnings) )

Speakers

- ECB’s Constancio (Portugal, term expires in May): Caution in removing stimulus is justified by the subdued inflation dynamics. Unconventional tools should be used when ever needed

- France Survey of Industrial Investment noted that businesses were planning on increasing investment by 5% in 2018 (compares to 4% in prior survey)

- The five largest European nations said to be favorable to a digital tax

- US delegation in China said to have reiterated its demand that China narrow its trade surplus by $200B by 2020. US asked China not to target US farmers in trade moves and halt some subsidies for made-in China by 2025. US also asked China to issue investment negative list by July 1st . Asked China to strengthen IP protection and enforcement. The US requested to meet China quarterly for review process

- US and China said to have reached consensus on some issues in trade talks but have areas of major disagreements in others that still exist

Currencies

- The USD was holding onto slight gains near 2018 highs against most major pairs ahead of the US jobs report for April. Monetary policy divergence had remained the overall theme in recent months. Divergence among the G3 trajectories has placed the USD into a higher gear in recent weeks

- EUR/USD remained below the 1.20 level as major Services PMI data disappoint in most cases and highlighted the recent ECB cautiousness on normalization.

- Emerging market currencies continue to experience turmoil. Argentina Central Bank hiked rated by another 300bps for the 2nd time in a week to stem capital outflows while the Turkish Lira continued to probe record lows against the USD

Fixed Income

- Bund Futures trade 2 ticks higher at 159.20 ahead of the US employment report. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 122.65 higher by 15 ticks, near the highs made in April. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Friday’s liquidity report showed Thursday's excess liquidity fell to €1.900T from €1.901T prior. Use of the marginal lending facility decreased from €74M to €53M.

- Corporate issuance saw 9 issuers raise $8.8B in the primary market

Looking Ahead

- (RU) Russia Apr Sovereign Wealth Funds: Wellbeing Fund: $B v $65.9B prior

- (IN) India to sell combined INR120B in 2020, 2026, 2031, 2033 and 2046 bonds

- 05:30 (ZA) South Africa to sell ZAR600M in I/L 2029, 2038 and 2050 bonds

- 06:00 (UK) DMO to sell combined £2.5B in 1-month, 6-month and 12-month Bills (£0.5B, £0.5B and £1.5B respectively)

- 06:30 (IS) Iceland to sell 2022 and 2028 RIKB Bonds

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 07:30 (TR) Turkey Apr Effective Exchange Rate (REER): No est v 83.42 prior

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:00 (RU) Russia Apr CPI M/M: 0.4%e v 0.3% prior; Y/Y: 2.5%e v 2.4% prior; CPI YTD: 1.2%e v 0.8% prior, CPI Core M/M: 0.2%e v 0.1% prior; Y/Y: 1.9%e v 1.8% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Change in Nonfarm Payrolls: +192Ke v +103K prior, Change in Private Payrolls: +190Ke v +102K prior, Change in Manufacturing Payrolls: +20Ke v +22K prior

- 08:30 (US) Apr Average Hourly Earnings M/M: 0.2%e v 0.3% prior; Y/Y: 2.7%e v 2.7% prior; Average Weekly Hours: 34.5e v 34.5 prior

- 08:30 (US) Apr Unemployment Rate: 4.0%e v 4.1% prior, Underemployment Rate: No est v 8.0% prior, Labor Force Participation Rate: 62.9%e v 62.9% prior

- 09:00 (BR) Brazil Apr Services PMI: No est v 50.4 prior, Composite PMI: No est v 51.5 prior

- 09:00 (RU) Russia Gold and Forex Reserve w/e Apr 27th: No est v $463.8B prior

- 09:00 (DE) ECB’s Weidmann (Germany) in Frankfurt

- 10:00 (CA) Canada Apr Ivey Purchasing Managers Index (seasonally adj): No est v 59.8 prior; PMI unadj: No est v 64.7 prior

- 11:00 (CO) Colombia Mar Exports: $3.4Be v $2.9B prior

- 11:00 (EU) Potential sovereign ratings after EU close (France and Luxembourg Sovereign Debt to be rated by Moody's)

- 12:00 (US) Fed's Dudley (dove, FOMC voter)

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 15:00 (US) Fed's Williams (moderate, voter)

- 17:30 (US) Fed's Quarles (hawk, FOMC voter)

- 20:00 (US) Fed's Bostic (FOMC voter, dove):

DAX Rebounds, Markets Await US Employment Data

The DAX index has moved upwards in the Friday session. Currently, the DAX is at 12,738 points, up 0.39% on the day. On the release front, German and Eurozone Services PMIs for April came in at 53.0 and 54.7 points, respectively, as both missed their estimates. Eurozone retail sales also disappointed, as the reading of 0.1% was well short of the forecast of 0.5%. In the US, the focus is on employment numbers, with the markets expecting mixed news. Wage growth is expected to edge lower to 0.2%, while nonfarm payrolls are forecast to rebound sharply, with an estimate of 190 thousand.

Eurozone and German services numbers softened in April. German Services PMI was the weakest since September 2016, and the eurozone reading also softened compared to March. This points to weaker expansion in services business activity, another indication of weaker eurozone growth in the first quarter of 2018. German numbers are raising concerns about the strength of the eurozone’s largest economy. Manufacturing PMI weakened for a fourth consecutive month in April, and retail sales posted a fourth straight decline. Inflation is also under pressure and remains well below the ECB target of 2 percent.

The Federal Reserve maintained the benchmark rate at a target of 1.5% to 1.75% on Wednesday. The markets were looking for some discussion about inflation and were not disappointed. The rate statement was significant, with policymakers noting that “overall inflation has moved closer to 2 percent”. This was more hawkish than the March statement, in which the rate statement said that inflation indicators “have continued to run below 2 percent”. With inflation moving closer to the Fed target of 2 percent, there is a stronger likelihood that the Fed will upgrade its rate projection from three to four hikes in 2018. The odds of a fourth rate hike this year stand at 50%. The Fed rate statement also noted that “market-based measures of inflation compensation remain low”, a reference to soft wage growth, which is at 2.7%, lower than the 3% rate that the Fed would like to see.

U.S Dollar Steady Ahead Of Jobs Report

Friday May 4: Five things the markets are talking about

Global markets attention now turns to the health of the U.S. economy, with wages growth and jobs data due in a few hours (08:30 am EDT).

On Wednesday, the Federal Reserve kept rates on hold as expected, admitting inflation is near target without suggesting any need to accelerate its gradual hiking path.

So, what will U.S non-farm payroll (NFP) tell us?

February and March brought some volatility to the payrolls growth trend, but the average of the two suggested no real change.

With other data appearing to ‘normalize’ following the transitory effect of last year’s storms and hurricanes, the consensus expects a return to a steadier trend, with payrolls up +200k this month.

For the other headline numbers, the market is looking for the unemployment rate to finally slip to +4.0% (something the consensus had looked for the prior two months), and average hourly earnings to be up +0.2%. The workweek would be +34.5 hours for the fifth consecutive month.

Note: The Fed is generally pleased to see inflation getting back to its target, but earnings growth remains well below pre-recession rates. They are apparently willing to let it accelerate extremely gradually.

Elsewhere, for now, Sino-U.S trade talks continue, even after both sides appeared to dial back their expectations.

Note: U.S and China said to have reached consensus on some issues in trade talks but have areas of major disagreements in others that still exist

1. Stocks mixed results

Stocks in Europe have found some traction despite a decline in Asia as investors assess the implications of ongoing trade talks between the U.S and China.

Note: Japanese markets were closed Friday for a public holiday.

Down-under, Aussie credit-market concerns sent yield-sensitive utilities stocks down -1.3%, pushing the S&P/ASX 200 index -0.5% lower. The benchmark index has ended its five-day winning streak. In S. Korea, the Kospi fell -0.7% because of weakness in financial stocks and a near-2% drop by index heavyweight Samsung.

In Hong Kong, stock indexes continued to lag behind on Friday on worries about U.S/China trade tensions and on speculation about Chinese money being rerouted to invest in IPO. The Hang Seng Index, which has fallen in six of the past nine trading days, was -1.2% and achieved its sixth weekly drop in the past seven-weeks.

In China, stocks ended lower overnight, capping a listless week, as investors anxiously await the outcome of the Sino-U.S trade talks being held in Beijing. The blue-chip CSI300 index ended down -0.5%, while the Shanghai Composite Index closed -0.3%.

In Europe, regional bourses trade mixed ahead of U.S jobs data. The French CAC underperforms weighed down by banking names missing estimates.

U.S stocks are set to open in the ‘red’ (-0.1%).

Indices: Stoxx600 +0.2% at 385.5, FTSE +0.5% at 7537, DAX +0.2% at 12713, CAC-40 -0.3% at 5487, IBEX-35 +0.2% at 10058, FTSE MIB +0.4% at 24157, SMI +0.4% at 8878, S&P 500 Futures -0.1%

2. Oil steady as U.S decision on Iran looms, gold lower

Oil prices have steadied overnight, consolidating after recent gains, as global supplies remained tight and the market waits for news on possible new U.S. sanctions against Iran.

Brent crude oil is down -30c at +$73.32 a barrel. The benchmark contract hit a four-year closing high of +$75.17 on Monday. U.S light crude (WTI) is -20c down at +$68.23.

Oil traders are concerned that U.S sanctions against Iran could cut oil supplies. President Trump has until May 12 to decide whether to restore the sanctions on Iran that was lifted after an agreement over its disputed nuclear program.

Also pressuring prices this week was Wednesday’s EIA report showing U.S crude inventories increasing by +6.2m barrels to +435.96m in the week to April 27, the highest level in 2018.

And more U.S oil will likely flow as U.S drillers’ added +5 oilrigs looking for new production in the week to April 27, according to Baker Hughes.

Ahead of the U.S open, gold prices have turned negative on a firmer dollar, while the market focuses on this morning’s U.S jobs data for a fresh catalyst. Spot gold is down -0.1% at +$1,309.93 per ounce and is heading for its third consecutive weekly decline.

3. Sovereign yields decline on risk aversion

After U.S 10-year Treasury yields briefly crossed the psychological +3% handle last week, equity investors have been worrying that a faster pace of monetary tightening could make stocks less attractive compared with bonds. However, since then, heightened geo-political risk aversion has supported Treasury prices and flattened the U.S curve again.

Note: The Fed this week signalled that they might allow a slight “overshoot in inflation,” which is now close to officials’ +2% target.

In the U.K, despite the below-forecast PMI index for April on the U.K’s important services sector, the BoE could still “possibly” hike interest rates next week (May 10), but the consensus is betting against it. Too many, it would be “out of character” for the normally cautious BoE to add policy uncertainty with a surprise policy move.

Note: Futures prices are pricing in the next U.K hike for November on clearer evidence of a sustained rebound in GDP growth. However, if Q2 GDP and wage growth surprise to the upside, fixed income could reprice for a August hike.

The yield on U.S 10-year Treasuries have declined -1 bps to +2.94%, the lowest in more than two weeks. In Germany, the 10-year Bund yield has decreased less than -1 bps to +0.53%, the lowest in a fortnight, while in the U.K, the 10-year Gilt yield increased less than -1 bps to +1.39%.

4. Dollar steady ahead of jobs report

The USD is holding onto its slight gains atop of this year highs against a plethora of G7 and Emerging Market currencies. Monetary policy divergence had remained the overall theme in recent months – divergence amongst the ECB, BoJ and FOMC is the biggest support.

EUR/USD (€1.1960) remains below the psychological €1.20 level as major Euro services PMI data and retail sales disappointed earlier this morning. The single unit is also being penalized by the recent ECB cautiousness on ‘normalization.’

Elsewhere, Emerging Market (EM) currencies continue to experience turmoil. In Argentina, the central bank hiked rates by another +300 bps for the second time in a week to stem capital outflows while the Turkish Lira (TRY) continues to probe record lows against the USD. Fixed income dealers believe that Turkish monetary policy remains too loose to deal with an overheating economy.

5. Euro retail sales and PMI’s disappoint

Data this morning showed that March’s +0.1% rise in eurozone retail sales was weaker than the consensus forecast of a +0.5% increase.

Note: Market expectations were lowered after disappointing German retail sales data published earlier this week.

Other data showed that April’s final euro-zone PMI’s suggest that the slowdown in GDP growth in Q1 is not the start of marked downturn. The final Composite PMI was revised down slightly from the flash estimate of 55.2 to 55.1, weaker than the Q1 average of 57.0. But on past form, the PMI is still consistent with quarterly GDP growth of about +0.5%.

March’s euro-zone retail sales data suggest that consumer spending had a weak Q1 and April’s composite PMI implies that the pace of GDP growth is unlikely to fully rebound after a slow Q1.

Euro Shrugs Off Soft Services PMI, US Employment Data Next

EUR/USD has posted slight gains on Friday, erasing the gains seen on Thursday. Currently, the pair is trading at 1.1959, up 0.24% on the day. On the release front, German and Eurozone Services PMIs for April came in at 53.0 and 54.7 points, respectively, as both missed their estimates. In the US, the focus is on employment numbers, with the markets expecting mixed news. Wage growth is expected to edge lower to 0.2%, while nonfarm payrolls are forecast to rebound sharply, with an estimate of 190 thousand. We’ll also hear from four FOMC members during the day.

German Services PMI was the weakest since September 2016, and the eurozone reading also softened compared to March. This points to weaker expansion in services business activity, another indication of weaker eurozone growth in the first quarter of 2018. German numbers are raising concerns about the strength of the eurozone’s largest economy. Manufacturing PMI weakened for a fourth consecutive month in April, and retail sales posted a fourth straight decline. Inflation is also under pressure and remains well below the ECB target of 2 percent.

As expected, the Federal Reserve maintained the benchmark rate at a target of 1.5% to 1.75% on Wednesday. The rate statement was significant, with policymakers noting that 'overall inflation has moved closer to 2 percent'. This was more hawkish than the March statement, in which the rate statement said that inflation indicators 'have continued to run below 2 percent'. With inflation moving closer to the Fed target of 2 percent, there is a stronger likelihood that the Fed will upgrade its rate projection from three to four hikes in 2018. The odds of a fourth rate hike this year stand at 50%. The Fed rate statement also noted that 'market-based measures of inflation compensation remain low', a reference to soft wage growth, which is at 2.7%, lower than the 3% rate that the Fed would like to see.