Sample Category Title

Tight Ranges In First Day Of Holiday-Affected Trading Week

With Bank Holidays today in Japan, China and Russia, trading this morning has been taking place in low liquidity conditions. This is expected to continue tomorrow as May Day/Labour Day holidays curtail markets in many countries. Today, markets are higher across the board, with Equities and Commodities up. There is some movement today in FX but, like other markets, moves are generally small. GBPUSD is stable after is big fall on Friday and AUDUSD is down -0.11%, trading around 0.75716.

The BOJ Press Conference took place with Governor Kuroda saying that the BOJ had not changed their projected timing to reach their target. The timeframe was always just a forecast, not a firm limit. If the momentum towards the 2% target weakens they will consider additional easing. The BOJ Interest Rate Decision was also released, with rates left unchanged at -0.1%. The Monetary Policy Statement was also released with the key take away being the removal of the phrase committing to a time frame on hitting their 2% inflation target. USDJPY moved higher from 109.149 to 109.320 as a result.

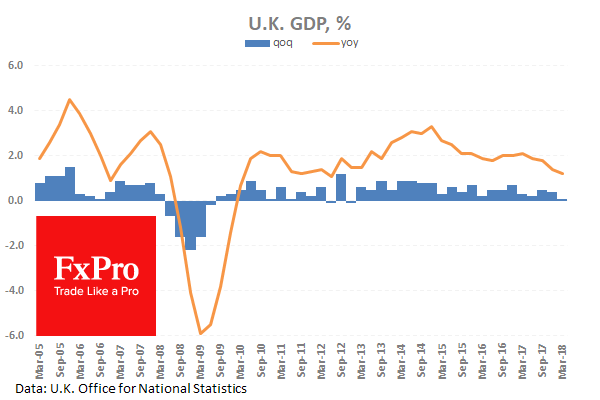

UK Gross Domestic Product (QoQ) (Q1) was 0.1% against an expected 0.3%, from 0.4% previously. Gross Domestic Product (YoY) (Q1) was 1.2% against an expected 1.4%, from 1.4% previously. UK GDP has been moving lower since highs of 1.1% and 1.0% in 2010 and 2012 respectively. A slip into negative territory is a clear and present risk with numbers being this low. GBPUSD fell from 1.38798 to a low of 1.38017 after the data was released.

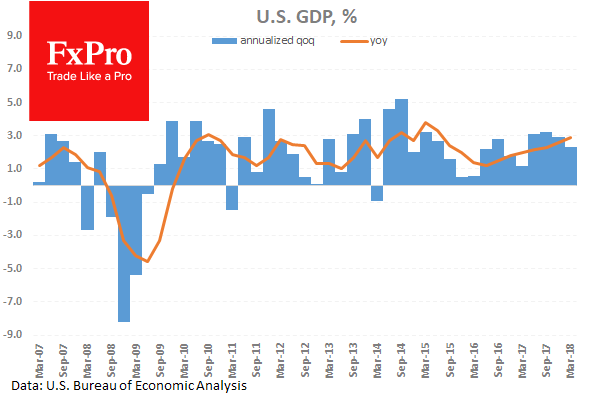

US Gross Domestic Product Annualized (Q1) was 2.3% against an expected 2.0%, from 2.9% previously. Gross Domestic Product Price Index (Q1) was 2.0% against an expected 2.2%, from 2.3% previously. These GDP figures were mixed, with the headline number beating expectations, despite representing a drop from the previous reading. Core Personal Consumption Expenditures (QoQ) (Q1) was 2.5% against an expected 2.4%, with a prior 1.9% reading from Q4. Personal Consumption Expenditure Prices (QoQ) (Q1) was 2.7% against an expected 2.6%, from a previous 2.7%. This data showed an increase in headline inflation, with the core data coming in higher than expected and beating the previous number. EURUSD fell from 1.20835 to 1.20632 as a result of this data.

EURUSD is up 0.09% overnight, trading around 1.21369.

USDJPY is up 0.12% in early session trading at around 109.148.

GBPUSD is up 0.10% this morning, trading around 1.37885.

Gold is down -0.07% in early morning trading at around $1,322.27.

WTI is down -0.15% this morning, trading around $67.86.

China Official PMIs Stay In Expansion Territory

General Trend:

- Asian equity markets trade generally higher, although participation limited; China and Japan closed for holidays

- Hang Seng outperforms led by financial index: ICBC, Bank of China, Agbank and Bocom all gain after Q1 earnings reports

- Singapore's DBS reports Q1 results above ests; shares rise

- M&A in focus: Sprint confirms merger with T-Mobile; Marathon Petroleum expected to make bid for Andeavor; REIT DCT Industrial to be acquired by Prologis; Sainsbury in talks to acquire Asda from Walmart

- China April official manufacturing and non-manufacturing PMIs generally little changed m/m

- Trump to meet with North Korea's Kim within 3-4 weeks

- Following last week's inter-Korean summit, North Korea said to pledge to close nuclear test site in May

- Reserve Bank of Australia (RBA) rate decision due on Tuesday, quarterly statement on monetary policy (including forecasts) expected on Friday, May 4th

- Market closures expected on Tuesday's session include China, HK, Indonesia, India, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand

- US Fed decision expected on Wed, May 2nd: US payrolls due on Friday

- This week's US/China trade talks in focus

Headlines/Economic Data

Japan

- Nikkei 225 closed for holiday

- (JP) Japan PM Abe Cabinet approval rating 43% v 42% in March – Nikkei Poll

- (JP) Bank of Japan (BOJ) announced Bond purchases for month of May (released on Friday, April 27th)

Korea

- Kospi opened +0.4%

- (KR) According to South Korea officials North Korea has pledged to close its nuclear test site in May and invite foreign inspectors to verify the closure; This is notable but not new, the site has been inactive since the mountain it is located under started to collapse due to testing - press

- Samsung Electronics, 005930.KR Trading halted starting today, for 3 days, as part of first-ever stock split action, which is 50-for-1

- (KR) North and South Korea signed the Panmunjeom Declaration Friday, it minimized economic cooperation but left room for the possibility in the future

- (KR) SOUTH KOREA INDUSTRIAL PRODUCTION M/M: -2.5% V -0.4%E; Y/Y: -4.3% V -1.6%E

- (KR) South Korea Mar Retail Sales m/m: 2.7% v 1.0% prior; y/y: 2.7% v 6.3% prior

- (KR) South Korea Mar Construction Output y/y: -6.3% v 0.9% prior

China/Hong Kong

- Hang Seng opened +0.8%, Shanghai Composite closed for holiday

- Hang Seng Financials index gains over 2%, Property/Construction +1.5%

- (CN) CHINA APR GOVT OFFICIAL MANUFACTURING PMI: 51.4 V 51.3E; NON-MANUFACTURING PMI: 54.8 V 54.5E

- (CN) China Securities Regulatory Commission (CSRC) eases restrictions on foreign investment in security joint ventures, removing the restriction of single foreign investors to a 30% stake in JVs - China Securities

- (CN) China President Xi and India PM Modi in an informal visit reached broad consensus on the overarching, long-term and strategic issues of global and bilateral importance – Xinhua

- (CN) According to China Ministry of Commerce (MOFCOM) trade volume between China and Russia expected to reach $100B or more in 2018 – Xinhua

- (CN) China Securities Regulatory Commission (CSRC) approves 2 IPO applications that will raise a total of CNY1.5B - Xinhua

- (HK) Hong Kong government said to not easily withdraw measures aimed at cooling the property market - HK Press

- 486.HK Oleg Deripaska agreed to sell down his majority ownership in EN+ Group PLC, the holding company that owns 48% of Rusal

- Xiaomi: Follow Up: Speculated to plan to submit application for HK IPO later this week - HK Media

Australia/New Zealand

- ASX 200 opened -0.1%, closed +0.5%

- ASX 200 Financials index +0.9%; Resources -0.4%

- (NZ) New Zealand Treasury: Sees 2018 annual inflation less than 2%; H1 2018 annual GDP growth below 3%

- Origin Energy, ORG.AU Reports Q3 (A$) Rev 491.9M v 385.3M y/y; production 62.7 pje v 79.7 y/y; Sales 61.2 pje v 56.0 y/y

- Ramelius Resources, RMS.AU Guides Q4 production 58-62K oz; Raises FY18 production 205-215K oz (prior 200-210K oz)

- (AU) AUSTRALIA MAR PRIVATE SECTOR CREDIT M/M: 0.5% V 0.4%E; Y/Y: 5.1% V 4.9%E

- (AU) Fitch Report: Housing downturn could pressure bank ratings in Australia

- (AU) Australia APRA: March loan balances A$2.6T, +0.5% m/m

- (NZ) New Zealand Apr ANZ Activity Outlook: 17.8 v 21.8 prior; Business Confidence: -23.4 v -20.0 prior

- (AU) Australia Apr Melbourne Institute Inflation m/m: 0.5% v 0.1% prior; y/y: 2.0% v 2.1% prior

- (AU) Australia Apr TD Inflation Gauge m/m: 0.5% v 0.1% prior

- (AU) Australia Mar HIA New Home Sales m/m: -2.0% v -0.7% prior

- AGL.AU Received highly conditional A$250M cash proposal from Alinta and Chow Tai Fook for Liddell

Other Asia

- DBS.SG Reports Q1 (S$) Net 1.51B v 1.4Be, Net interest income 2.13B v 1.83B y/y, Rev 3.36B v 2.89B y/y

North America

- S Confirms agreement to merge with T-Mobile in all stock transaction with enterprise value of $146B; Jonh Legere named CEO

- TWTR Sold data in 2015 to Aleksandr Kogan, the Cambridge University academic who gathered millions of Facebook users' information without their knowledge - UK press

- BIDU Enters into Definitive Agreements to Divest its Financial Services Business (FSG); Through deal FSG which will be renamed as Du Xiaoman Financial will raise ~$1.9B

- ANDV Marathon Petroleum said to plan to acquire Andeavor for more than $20B or ~$150/share (cash and stock) - US financial press

- WMT Sainsbury confirms in talks to acquire Asda from Walmart in deal said to be worth £10B - press

- (US) Commerce Sec Ross: White House plans to extend the steel and aluminum tariffs to some countries, but not all, following the scheduled expiration on May 1st

Europe

- (UK) UK PM May accepts resignation of Home Sec Amber Rudd -

- (IT) Five Start leader signals no Italy government possible with democrats - press

Levels as of 02:00ET

- Hang Seng +1.7%; Shanghai Composite +0.2%; Kospi +0.7%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.6%, Dax +0.2%; FTSE100 +0.1%

- EUR 1.2134-1.2119; JPY 109.18-109.02; AUD 0.7582-0.7559;NZD 0.7089-0.7063

- Jun Gold -0.1% at $1,322/oz; Jun Crude Oil -0.3% at $67.92/brl; Jul Copper +0.3% at $3.08/lb

In The US , The Key Figure Today Is PCE Inflation

Market movers today

A busy data week is off to strong start with important inflation releases from Germany and the US. Later this week we get Chinese Caixin PMI, US ISM manufacturing, FOMC meeting, euro area inflation not to forget nonfarm payrolls. We also have the Norges Bank meeting on Thursday but that's likely to be a non-event, see 'Selected Market News' below.

Today, in Germany , the inflation prints will give final guidance ahead of the flash euro area estimate released on Thursday. Friday's French and Spanish inflation estimates were mixed.

In the US , the key figure today is PCE inflation . Based on the GDP report Friday, it seems like PCE core rose 0.1%m/m in March (assuming no revisions to previous months), which is lower than what most expected previously. This should still be enough to boost the yearly core rate to 1.9% due to the base effects from the drop in wireless telephone service prices last year. Irrespective, we still expect the Fed to move on with the hiking cycle this year.

In the Scandies , focus turns to Norwegian retail sales, credit growth and Norges Bank's daily NOK purchases . For more information see 'Scandi Markets' on page 2.

Selected market news

Asian equities have followed US and European counterparties this morning by trading in green territory. The rise follows a strong weekly finish to the US earnings season, slightly better than expected Chinese PMIs (see next section) as well as improved risk appetite following Kim Jong Un's pledge to fully denuclearize North Korea during his historical visit to South Korea.

This morning the official Chinese manufacturing PMI showed a drop to 51.4 (from 51.5). We expect the private manufacturing PMI (due Wednesday) to show a similar modest drop as growth in export markets is waning and as slower housing activity feeds through to manufacturing. Noteworthy, this morning's non-manufacturing index showed a surprising rise.

UK Q1 GDP disappointed Friday by growing only 0.1% q/q - the worst quarterly growth rate since 2012 - casting doubt whether the Bank of England is going to hike next week, as almost all expected just a few weeks ago. We think it is a close call now and think the PMIs for April are going to be extremely important for the Bank of England's decision.

In Norway , the NAV labour market report revealed another monthly drop in gross unemployment. Meanwhile, at -231 people the decline was smaller than expected and follows a similar March drop that we suspected was temporarily distorted by the timing of Easter. Meanwhile, this report now suggests that the labour market is slacker than we, markets and Norges Bank previously expected, see chart . Possible explanatory factors could be a faster cyclical rise in the participation rate and/or higher productivity growth. That said, recent data releases have more broadly been disappointing. Irrespective of this, Thursday's Norges Bank meeting is likely to be a non-event as it is a short meeting with no monetary policy report or press conference, and as in recent years Norges Bank has given very little new information at these interim meetings. We stick to our call of a 25bp September rate hike.

On Friday, Russia's central bank (CBR) kept its key rate unchanged at 7.25%, as geopolitical tension reintroduces climbing inflation risk. However, the CBR sees the target well anchored in 2018-19. We expect the CBR to cut to 6.50% by the end of 2018 and to 6.00% by end-2019.

Australia’s Private Sector Credit Came In Better-Than-Expected In March

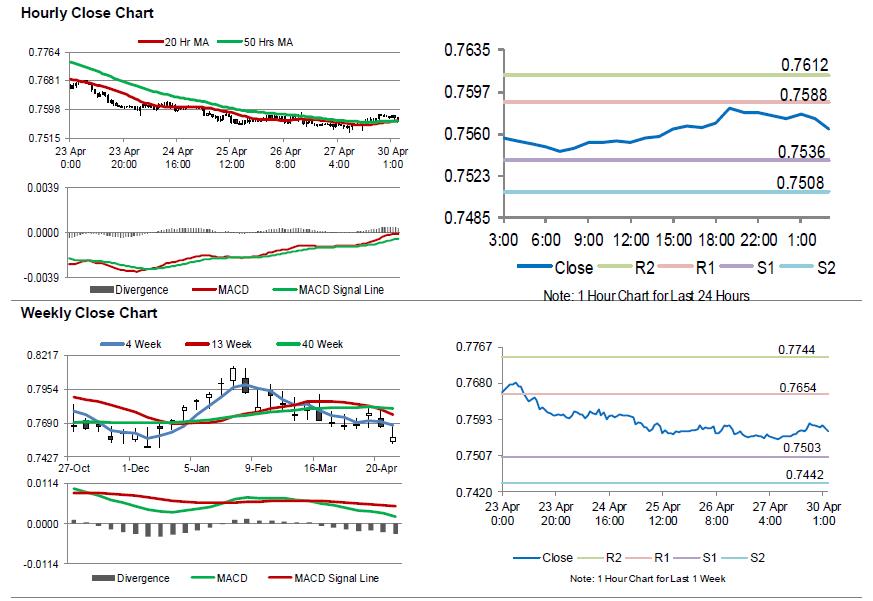

For the 24 hours to 23:00 GMT, the AUD rose 0.32% against the USD and closed at 0.7579 on Friday.

LME Copper prices declined 1.29% or $88.5/MT to $6797.0/MT. Aluminium prices rose 2.04% or $45.0/MT to $2249.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7564, with the AUD trading 0.20% lower against the USD from Friday's close.

Data released overnight indicated that Australia's private sector credit grew 0.5% on a monthly basis in March, beating market expectations for a rise of 0.4%. The private sector credit had recorded a rise of 0.4% in the prior month.

Elsewhere in China, Australia's largest trading partner, the NBS manufacturing PMI declined to a level of 51.4 in April, less than market expectations for a fall to a level of 51.3. The PMI had recorded a level of 51.5 in the previous month. Additionally, the nation's NBS non-manufacturing PMI recorded an unexpected rise to a level of 54.8 in April, confounding market consensus for a fall to a level of 54.5. The PMI had registered a reading of 54.6 in the previous month.

The pair is expected to find support at 0.7536, and a fall through could take it to the next support level of 0.7508. The pair is expected to find its first resistance at 0.7588, and a rise through could take it to the next resistance level of 0.7612.

Moving ahead, investors would keep a close watch on the Reserve Bank of Australia's (RBA) monetary policy decision, due to be announced in the early hours of tomorrow.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

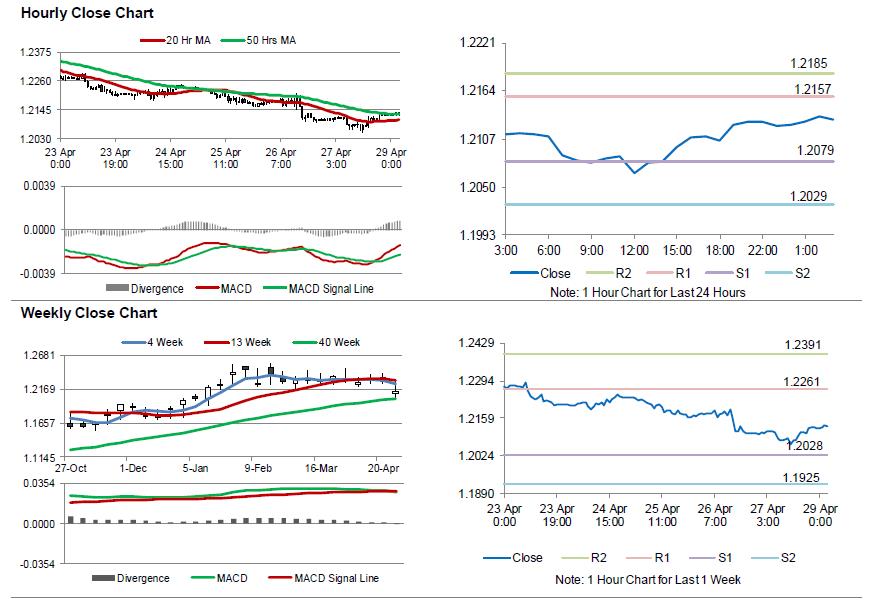

German Unemployment Rate Remained Unchanged In April

For the 24 hours to 23:00 GMT, the EUR rose 0.19% against the USD and closed at 1.2128 on Friday.

On the macro front, the Euro-zone’s final consumer confidence index rose to a level of 0.4 in April, confirming the preliminary print and compared to a reading of 0.1 in the previous month. Meanwhile, the region’s economic sentiment indicator remained unchanged at a level of 112.7 in April, defying market expectations for a drop to a level of 112.0.

Separately, Germany’s seasonally adjusted unemployment rate remained steady at 5.3% in April, meeting market consensus and highlighting strength in the nation’s labour market.

The US Dollar pared some of its losses against a basket of major currencies on Friday, following better-than-expected first-quarter gross domestic product (GDP) print in the US.

Data indicated that the flash annualised GDP in the US climbed more-than-anticipated by 2.3% on a quarterly basis in the first three months of 2018, compared to market expectations for an advance of 2.0%. The nation’s GDP had recorded a rise of 2.9% in the previous quarter.

In other economic news, the US final Reuters/Michigan consumer sentiment index dropped less than initially estimated to a level of 98.8 in April, compared to a reading of 101.4 in the prior month, while the preliminary figures had indicated a fall to a level of 97.8.

In the Asian session, at GMT0300, the pair is trading at 1.213, with the EUR trading slightly higher against the USD from Friday’s close.

The pair is expected to find support at 1.2079, and a fall through could take it to the next support level of 1.2029. The pair is expected to find its first resistance at 1.2157, and a rise through could take it to the next resistance level of 1.2185.

Moving ahead, traders would focus on the release of Germany’s flash inflation numbers for April and retail sales data for March, due in a few hours. Also, the US pending home sales, personal income as well as spending data, all for March, scheduled to release later today, will keep investors on their toes.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

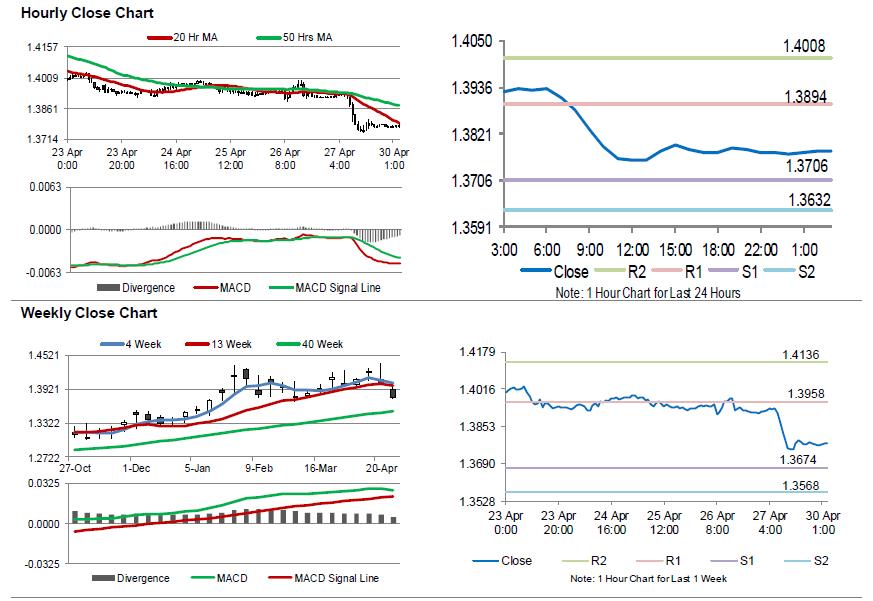

UK Posted Its Slowest Rate Of Economic Growth Since 2012 In 1Q 2018

For the 24 hours to 23:00 GMT, the GBP declined 0.96% against the USD and closed at 1.3781 on Friday, after downbeat British economic growth figures diminished the odds of a May interest rate hike.

Data indicated that UK's flash gross domestic product (GDP) rose less-than-expected by 0.1% QoQ in the first three months of 2018, expanding at its weakest pace in over 5 years. The nation's GDP had registered a reading of 0.4% in the previous quarter, while market participants had envisaged for an increase of 0.3%.

In the Asian session, at GMT0300, the pair is trading at 1.3779, with the GBP trading marginally lower against the USD from Friday's close.

The pair is expected to find support at 1.3706, and a fall through could take it to the next support level of 1.3632. The pair is expected to find its first resistance at 1.3894, and a rise through could take it to the next resistance level of 1.4008.

Amid no macroeconomic releases in the UK today, investor sentiment would be determined by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.22% against the JPY and closed at 109.11 on Friday.

In the Asian session, at GMT0300, the pair is trading at 109.1, with the USD trading slightly lower against the JPY from Friday’s close.

The pair is expected to find support at 108.87, and a fall through could take it to the next support level of 108.65. The pair is expected to find its first resistance at 109.43, and a rise through could take it to the next resistance level of 109.77.

Going forward, Japan’s final Nikkei manufacturing PMI for April, set to release overnight, will be on investors’ radar.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

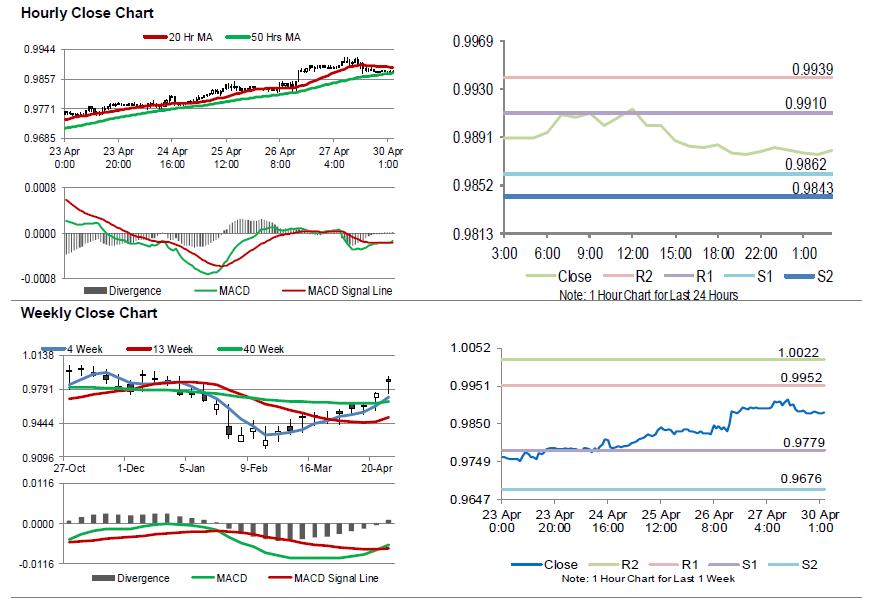

Swiss Franc Trading Slightly Lower This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.14% against the CHF and closed at 0.9877 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9881, with the USD trading marginally higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9862, and a fall through could take it to the next support level of 0.9843. The pair is expected to find its first resistance at 0.9910, and a rise through could take it to the next resistance level of 0.9939.

Ahead in the day, market participants would look forward to Switzerland’s KOF leading indicator data for April.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

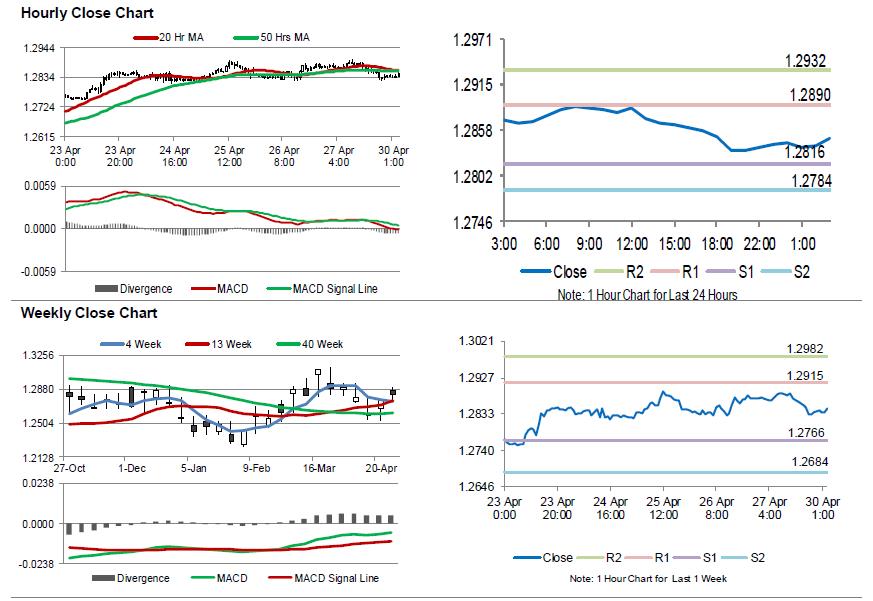

Loonie Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.31% against the CAD and closed at 1.2834 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.2848, with the USD trading 0.11% higher against the CAD from Friday’s close.

The pair is expected to find support at 1.2816, and a fall through could take it to the next support level of 1.2784. The pair is expected to find its first resistance at 1.2890, and a rise through could take it to the next resistance level of 1.2932.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

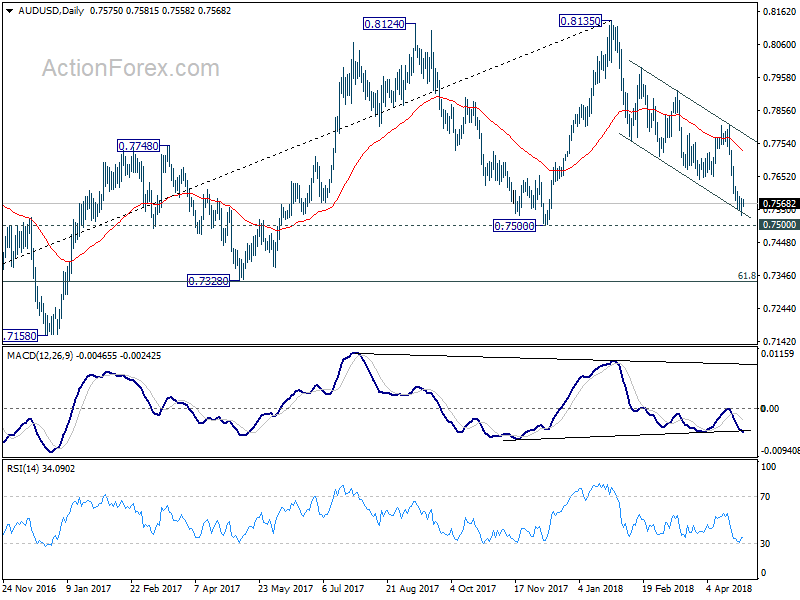

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7546; (P) 0.7564; (R1) 0.7598; More...

Intraday bias in AUD/USD remains neutral for consolidation above 0.7531 temporary low. Upside of recovery should be limited by 0.7642 support turned resistance to bring another decline. Below 0.7531 will resume larger fall from 0.8135 to 0.7500 key support level. On the upside, however, firm break of 0.7642 will be an early sign of near term reversal and turn focus back to 0.7812 resistance.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Decisive break of 0.7500 key support will suggest that such correction is completed. In that case, deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.