Sample Category Title

ECB Mersch: Inflation to rise gradually, contingent on highly accommodative monetary policy

ECB Executive Board member Yves Mersch said today that inflation will rise only gradually. He said in Sofia "overall, the underlying strength in the euro area economy continues to support our confidence that inflation will converge towards our aim over the medium term." But he added that " inflation convergence will likely proceed only gradually, and remains contingent on a highly accommodative monetary policy stance."

Also, Mersch added that "the transition towards policy normalization will begin once the Governing Council assesses there has been sustained adjustment in the path of inflation."

Separately, ECB Governing Council member Benoit Coeure said Eurozone growth isn't just recovery but an expansion. He added that there is solid and broad based expansion in the region.

Comments from both are strikingly similar to President Mario Draghi's yesterday.

UK Chancellor Hammond blamed weak GDP on weather. ONS Kent-Smith said impact was limited

The 0.1% qoq growth in UK in Q1 not only missed market expectations, it's also the weakest quarterly growth figure in five years.

Chancellor of the Exchequer Philip Hammond blamed the weak data on weather. He said in an email statement that "today's data reflects some impact from the exceptional weather that we experienced last month, but our economy is strong and we have made significant progress." He added that "our economy has grown every year since 2010 and is set to keep growing, unemployment is at a 40 year low, and wages are increasing."

On the other hand, Rob Kent-Smith, the ONS' head of national accounts said in a statement that "our initial estimate shows the UK economy growing at its slowest pace in more than five years with weaker manufacturing growth, subdued consumer-facing industries and construction output falling significantly." And, "while the snow had some impact on the economy, particularly in construction and some areas of retail, its overall effect was limited with the bad weather actually boosting energy supply and online sales."

EURUSD Sellers Targeting 1.2000 Level

The euro currency has continued to fall lower against the U.S dollar during the European trading, with price-action breaking below the 1.2095 support level, hitting 1.2064. The rising value of the U.S dollar has again been the driving force behind today’s fall in the EURUSD pair, with the greenback gaining across the board. Moving into the U.S session, further losses below the 1.2064 support level may provoke another fresh round of euro selling toward the 1.2000 level.

The EURUSD pair retains a bearish trading bias while trading below the 1.2154 level, key support is now found at the 1.2033 and 1.2000 levels.

If the EURUSD pair moves back above the 1.2216 level, buyers may move for a technical test of the key 1.2254 level.

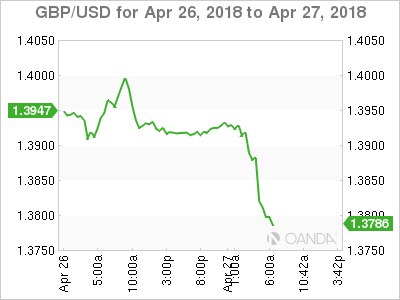

GBPUSD Pair Tumble After GDP Report

The British pound has moved sharply lower against the U.S dollar during the European trading session, after the United Kingdom released worse than expected Q1 GDP numbers. The GBPUSD pair currently trades close to the key 1.3800 level, with the intraday price-low at 1.3805, so far. Moving into the U.S session, traders are likely to focus on the 1.3800 support level, and the release of key U.S GDP data.

The GBPUSD pair is intraday bearish while trading below the 1.3886 level, further losses towards the 1.3770 and 1.3730 levels remains possible.

If the GBPUSD pair gains traction above the 1.3886 level, buyers may test towards the 1.3933 and 1.3991 support levels.

CAC Shrugs Off Soft French GDP, Consumer Data

The CAC index continues to head higher and at its highest level since January 29. Currently, the CAC is trading at 5464 points, up 0.24% on the day. On the release front, key French indicators looked sluggish. GDP dropped to 0.3% in the first quarter, down from 0.6% in Q4 of 2017. This missed the estimate of 0.4%. Consumer data was even worse. Consumer spending fell from 2.4% to o.1%, short of the forecast of 0.4%. Preliminary CPI also dropped sharply, falling from 1.0% to 0.1%, which matched the estimate. In the US, Advance GDP is expected in at 2.0%.

French stock markets have posted strong gains in recent weeks. Although the French economy has slowed down in the first quarter, it has been all smiles for the CAC index. The index is on its way to a fifth straight winning week and has rocketed 6.5% since late March. The improved global economy has been a boon for the stock markets, and with the ECB continuing to purchase billions worth of bonds for its stimulus program, French stocks remain an attractive option for investors.

There were no dramatic comments from the ECB on Thursday, as the bank maintained its monetary policy and guidance. The rate statement said that “the Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases'. The stimulus program of EUR 30 billion/month is scheduled to remain in place until September, so investors shouldn’t even think about an interest rate hike until sometime in 2019. In his press conference, Mario Draghi said that the eurozone economy had slowed in the first quarter, but expressed “caution tempered by an unchanged confidence' that the ECB would realize its target of around 2 percent inflation. Although the ECB has said that it plans to wind up stimulus in September, this is not a date set in stone – if second-quarter numbers are not strong, the ECB could continue to the stimulus scheme into 2019.

Dismal UK GDP Deals Sterling Knockout Blow

Buying sentiment towards the British Pound was dealt a severe blow on Friday, following reports that the U.K economy grew much slower than expected in Q1.

U.K GDP growth slowed to 0.1% in the first quarter, much worse than the expected 0.3%, and its weakest since 2012. While the snow had some negative impacts on GDP, the bad weather really can’t bear all the blame - its effects on growth were small. Today’s dismal GDP figures have not only dented confidence in the health of the U.K economy, but also in the Bank of England’s ability to raise interest rates in May. With the Pound notorious for its extreme sensitivity to monetary policy speculation, further downside is likely as investors heavily reduce bets of a rate hike next month.

The British Pound collapsed like a house of cards, following the downside surprise in the U.K GDP figures. An appreciating Dollar has not helped matters for the GBPUSD, with prices tumbling towards 1.3800 as of writing. The combination of Pound weakness and Dollar strength is likely to encourage investors to attack the GBPUSD ruthlessly moving forward. Focusing on the technical picture, the currency pair is turning heavily bearish on the daily charts. A breakdown below 1.3800 could encourage a decline towards 1.3700 and 1.3640, respectively.

Dollar Flexes Ahead of U.S GDP Release

King Dollar has appreciated against a basket of major currencies ahead of this afternoon’s estimate of first-quarter GDP growth. Seasonal factors are expected to see GDP growth cool in Q1, but this could have little impact on the Dollar’s mojo. With rising U.S bond yields and expectations of higher U.S interest rates heavily supporting the Dollar, it is likely to hold its own against most majors. Focusing on the technical picture, the Dollar index remains firmly bullish on the daily charts. The current upside momentum could instill bulls with enough confidence to challenge 92.00. A breakout above 92.00 may result in a further incline higher towards 92.50. Alternatively, if bulls fail to break above the 92.00 level, prices could retrace back to 91.50.

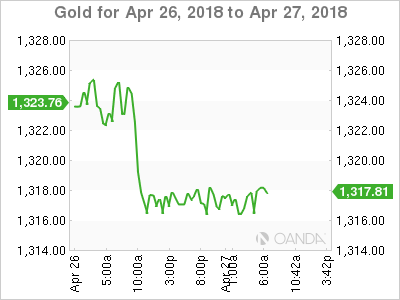

Commodity spotlight – Gold

Gold prices wallowed at near five-week lows of around $1317 during Friday’s trading session as a strengthening Dollar, higher U.S bond yields and easing geopolitical tensions dented appetite for the safe-haven asset. The yellow metal is likely to receive further punishment if the Dollar continues to appreciate. Taking a look at the technical picture, Gold has scope to depreciate towards $1300 if bears can maintain control below $1324.

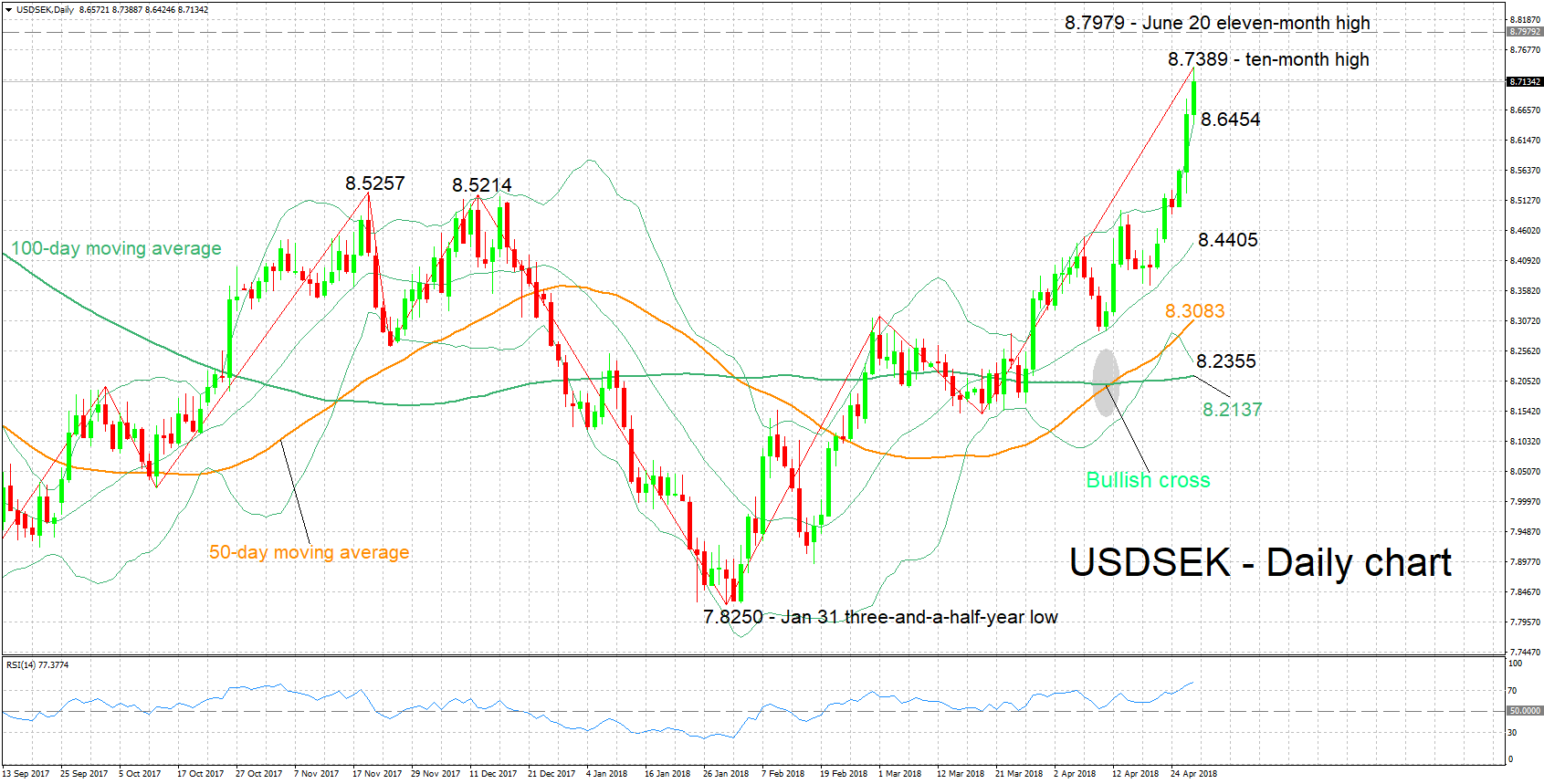

USDSEK Bullish In The Short – And Medium-Term, RSI Overbought

USDSEK hit a fresh 10-month high of 8.7389 earlier on Friday. Indicative of the positive bias in the short-term is the fact that the pair finished higher in all but one of the five previous trading days.

Adding to the conviction for a bullish momentum is the rising RSI. However, the indicator has entered overbought territory above 70, rendering a pullback in the near term possible.

Further gains might meet a barrier around the 11-month high of 8.7979 posted in late June, while an upside break will increasingly start shifting the attention to the 9.00 round figure.

In case of declines, support could come around the upper Bollinger band at 8.6454, with steeper losses potentially meeting support around 8.5257 – this is a previous peak with the range around it encapsulating another top from the recent past at 8.5214.

The medium-term picture is bullish, with trading taking place above the 50- and 100-day moving average lines. Price action also seems to verify the positive signal given by the bullish (golden) cross recorded in mid- to late-April when the 50-day MA moved above the 100-day one. For the record, the pair is trading higher by 6.5% year-to-date.

Overall, both the short- and medium-term outlooks are looking positive, with the overbought RSI cautioning though that some selling in USDSEK might take place in the near term.

Pound Takes A Swan Dive After Q1 GDP Data

Friday April 27: Five things the markets are talking about

Overnight, global equities have nudged a tad higher, supported by a plethora of strong earnings results in the tech sector mostly.

The market has also been keeping an eye on the historic meeting between North Korea’s Kim Jong-un and South Korea’s Moon Jae-in. Thus far, holding talks over Kim’s nuclear weapons program has helped to ease some regional geopolitical tensions.

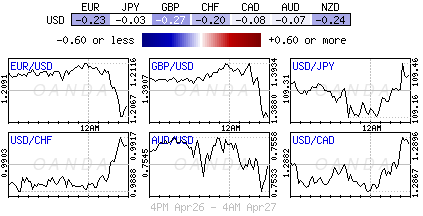

The ‘big’ dollar remains better bid, despite U.S treasury yields retreating below the psychological +3% yield level.

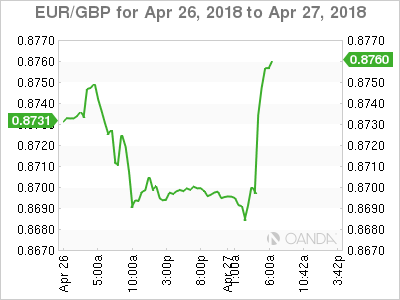

Elsewhere, the EUR is on the back foot after regional growth data from France and Spain eased, while the yen was little changed after the Bank of Japan (BoJ) maintained its stimulus, as expected.

In the U.K, the pound has taken a ‘swan dive’ after data this morning revealed that their economy grew at the slowest pace in five years in Q1.

Commodities have retreated, led lower mostly by oil.

On tap: In the U.S, the market will be focusing on Q1 GDP data (08:30 am EDT).

1. Stocks remain better bid

In Japan, stocks rallied to three-month highs overnight as chip-related firms rallied after brisk earnings forecasts. The Nikkei share average ended up +0.7%. For the week, the Nikkei gained +1.4% and posted a fifth consecutive gain. The broader Topix advanced +0.3%.

Note: Markets will be closed on Monday in Japan for a national holiday.

Down-under, Aussie shares closed near a six-week high on Friday, led by health care stocks. The S&P/ASX 200 index rose +0.7% and racked up a weekly gain of around +1.4%. In S. Korea, the Kospi was underpinned by optimism as leaders of North and South Korea held their first summit in over a decade, rising +0.8%.

In Hong Kong, shares ended higher overnight, led by IT and energy stocks. The Hang Seng index ended up +0.9%, while the China Enterprises Index rallied +1%. For the week, the Hang Seng fell -0.5%, while HSCE rose +0.1%.

In China, stocks ended higher, led by healthcare. The blue-chip CSI300 index ended flat, while the Shanghai Composite Index edged up +0.2%. For the week, CSI300 slipped -0.1%, while SSEC gained +0.3%.

In Europe, the FTSE 100 is rallying (+0.45%) as sterling tumbles (-0.7%) after data shows a sharp U.K economic slowdown (see below) and now casts doubt over prospects for a BoE May rate hike.

U.S stocks are set to open in the ‘red’ (-0.2%).

Indices: Stoxx600 +0.1% at 383.9, FTSE +0.4 at 7451, DAX +0.7% at 12586, CAC-40 +0.1% at 5460, IBEX-35 +0.1% at 9905, FTSE MIB -0.6% at 23885, SMI +0.1% at 8839, S&P 500 Futures -0.3%

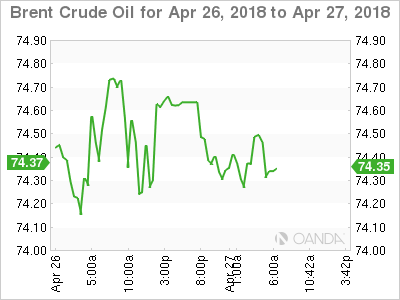

2. Oil prices ease, but concerns persist over Iran supplies, gold unchanged

Ahead of the U.S open, oil prices have eased a tad, but Brent crude remains supported on dips amid concerns that Iran may face renewed sanctions.

Brent crude futures are down -27c, or -0.4%, at +$74.47 a barrel, after rising +1% yesterday. U.S West Texas Intermediate (WTI) crude has fallen -19c, or -0.3%, to +$68 a barrel. The contract gained +0.2% on Thursday.

Note: Brent is heading for a third week of gains, up by +0.5%, while WTI is set to drop -0.4% for the week.

Dealers expect that the U.S will, in May, re-impose sanctions against Iran, who is a major oil producer and member of the OPEC. President Trump indicated this week that he would decide by May 12 whether to restore U.S sanctions on Iran.

Also supporting prices is global demand and the declining output in Venezuela, OPEC’s biggest producer in S. America.

For the crude ‘bears’, further gains have been capped by rising U.S production as shale drillers ramp up activity in sync with higher oil prices.

Gold prices continue to trade atop their five-week low ahead of the U.S open and is set for a decline of more than -1% this week, weighed down by a strong dollar, high U.S. Treasury yields and easing geo-political concerns. Spot gold is unchanged at +$1,316.58 per ounce, not far from a low of +$1,315.06 an ounce hit in yesterday’s session. It will be the yellow metals biggest weekly decline in four. U.S gold futures are unchanged at +$1,317.50 per ounce.

3. Sovereign yields fall

Sovereign yields are under pressure again.

The ECB’S caution, combined with eurozone inflation that’s slow to adjust to Draghi’s target, is keeping investors’ in the hunt for yield and carry in eurozone government bonds.

While in the U.K, dealers are now pricing only a +20% chance that the BoE will raise interest rates at the next meeting in May, after this morning’s disappointing Q1 GDP data. The market had been pricing in a +50% chance last week.

In Japan overnight, the Bank of Japan (BoJ) kept its overnight rates steady as expected. In their statement, the BoJ omitted its prior reference related to reaching +2% inflation target around 2019/20 and remained committed to achieving the +2% inflation target at the earliest time possible.

The yield on 10-year Treasuries has dipped -2 bps to +2.97%, while in Germany; the 10-year Bund yield declined -3 bps to -0.57%, the lowest in more than a week. In the U.K, the 10-year Gilt yield has plummeted -6 bps to +1.444%, the lowest in a month.

4. Dollar in demand

The USD is trying to close out this week on firm footing against G7 currency pairs despite the U.S 10-year yield curve moving back below the psychological +3% level. All this week, the greenback found support on the back of rate differentials, especially as the ‘normalization process’ getting dialled back in both Europe and Japan.

The GBP (£1.3803, -0.93%) has plummeted after UK Q1 GDP registered a big miss, deeming that the slowdown was broader than expected and not only weather related. The probability of a BoE May rate hike has fallen to +20%. A month ago it was considered a done deal.

According to many techies, the EUR/USD (€1.2085) in on the verge of a technical breakout to the downside, which would wipe all of its 2018 gains. Will this morning’s U.S GDP data be the impetus?

USD/JPY (¥109.28) remains steady despite the BoJ dropping its phase of achieving the inflation target in 2019/20. Kuroda downplayed the removal of the text, noting, “It did not erase the timeframe due to concerns about having to delay it again.”

5. U.K economy grows at its slowest pace in five-years

Data this morning showed that the U.K. economy grew at its slowest pace in more than five years in Q1, dampening the case for an interest rate increase from the BoE next month.

The ONS that GDP expanded +0.1% in Q1 when compared with the previous three-months – an annualized rate of +0.4%.

This marked a visible slowdown from Q4, 2017, when the economy expanded +0.4%. The market was expecting a quarterly increase of +0.3%.

The ONS cited a contraction in construction as dragging on the U.K.’s economic growth, although added that the impact of the snowy weather during the quarter was limited.

Note: In February, the BoE signalled that further rises would likely be necessary to curb inflation, which accelerated sharply, spurred by the pound’s post-referendum collapse.

Euro Slide Continues As Cautious ECB Holds Course

EUR/USD has posted slight losses in the Friday session. Currently, the pair is trading at 1.2086, down 0.15% on the day. On the release front, French Flash GDP dropped to 0.3%, shy of the estimate of 0.4%. German unemployment rolls dropped by 7 thousand, a weaker reading than the estimate of a decline of 15 thousand. In the US, Advance GDP is expected in at 2.0%, and UoM Consumer Sentiment is forecast to soften to 98.0 points.

The sliding euro has posted gains in only one session since April 16, and the downward trend continued on Thursday after the ECB rate announcement. There were no dramatic comments from the ECB on Thursday, as the bank maintained its monetary policy and guidance. The rate statement said that “the Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases”. The stimulus program of EUR 30 billion/month is scheduled to remain in place until September, so investors shouldn’t even think about an interest rate hike until sometime in 2019. In his press conference, Mario Draghi said that the eurozone economy had slowed in the first quarter, but expressed “caution tempered by an unchanged confidence” that the ECB would realize its target of around 2 percent inflation. Although the ECB has said that it plans to wind up stimulus in September, this is not a date set in stone – if second-quarter numbers are not strong, the ECB could continue to the stimulus scheme into 2019.

The US dollar has been on a tear against its rivals, and the euro has fallen 2.1% since April 16. Much of the credit for the dollar rally goes to rising yields on US bonds, which hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed above the symbolic level of 3.0%, which led to investors snapping up bonds at the expense of equities. As oil prices have been moving higher, this has led to expectations of higher inflation, which in turn, has increased sentiment that the Federal Reserve will increase rates four times in 2018, rather than three hikes. This has made the US dollar more attractive to investors.

UK Q1 GDP Misses Expectations To A 5-Year Low

Notes/Observations

- UK Q1 GDP misses expectations for its slowest annual pace since 2012; weather effect was deemed limited

- European GDP and inflation data backs recent ECB view of moderation (GDP Misses: France, Spain; Inflation Misses: Spain)

- Bank of Japan (BoJ) policy statement omitted its prior reference related to reaching 2% inflation target around FY19/20; remained committed to achieving the 2% inflation target at the earliest time possible

- Two Koreas agreed to end 7-decade war and pursue complete denuclearization

Asia:

- Japan Mar Jobless Rate: 2.5% v 2.5%e; Job-to-applicant Ratio: 1.59 v 1.59e

- Japan Mar Preliminary Industrial Production M/M: 1.2% v 0.5%e; Y/Y: 2.2% v 2.0%e

- Japan Mar Retail Sales M/M: -0.7% v 0.0%e; Retail Trade Y/Y: 1.0% v 1.5%e

- (JP) Bank of Japan (BOJ) left its policy steady with Interest Rate on Excess Reserves (IOER) unchanged at -0.10%, maintained the 10-year JGB Yield Curve Control (YCC) at 0.00% and kept the annual pace of JGB holdings at ¥80T. Vote was again 8-1 with Kataoka dissenting

- BoJ Quarterly Report removed the phrase on reaching 2% price target around FY19/20 (next fiscal year)

- Kim Jong-Un become the 1st North Korean leader to set foot in South Korea since the end of the Korean War in 1953; suggests possibility of more meetings with South Korea

Europe:

- ECB's Nowotny (Austria) said to call for debate on future path of ECB policy when the QE bond purchases end in Sept with his position said to be position shared by a few other ECB members

- ECB policymakers said to be keen not to upset market expectations for end of QE in 2018 with a 1st potential rate hike mid-2019. ECB decision on QE seen in June or July but also speculation that it could be delayed until Sept

- EU chief Brexit negotiator Barnier: Market participants should prepare for no transition; it's not true that EU27 businesses needed the city of London

- UK Home Sec Rudd said to have cast doubt on the govt policy of not being in a customs union with the EU after Brexit. Would not be "drawn" on the issue but added that discussions to be had about it in cabinet to agree a "final position

Americas:

- NAFTA countries reportedly aiming for May 1st agreement but large differences remain

- Mexico Econ Min Guajardo: NAFTA discussions were progressing slowly with many issues still to resolve

- Trump administration said to have toughened one of its most contentious demands and proposing that an even higher percentage of content in autos made in the NAFTA zone come from factories where workers are paid at least $15-17 an hour

- US Senate confirmed Pompeo as Secretary of State

Economic Data:

- (FR) France Q1 Advance GDP Q/Q: 0.3% v 0.4%e; Y/Y: 2.1% v 2.3%e

- (DE) Germany Mar Import Price Index M/M: 0.0% v 0.1%e; Y/Y: -0.1% v 0.0%e

- (UK) Apr Nationwide House Price Index M/M: +0.2%e v -0.2% prior; Y/Y: 2.7%e v 2.1% prior

- (FI) Finland Apr Consumer Confidence: 23.2 v 24.7 prior; Business Confidence: 13 v 11 prior

- (FR) France Apr Preliminary CPI M/M: 0.1% v 0.1%e; Y/Y: 1.6% v 1.6%e

- (FR) France Apr Preliminary CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.8% v 1.7%e

- (FR) France Mar PPI M/M: 0.4% v 0.1% prior; Y/Y: 2.5% v 1.5% prior

- (FR) France Mar Consumer Spending M/M: 0.1% v 0.5%e; Y/Y: 2.3% v 2.5%e

- (ES) Spain Q1 Preliminary GDP Q/Q: 0.7% v 0.7%e; Y/Y: 2.9% v 3.0%e

- (ES) Spain Apr Preliminary CPI M/M: 0.8%v 1.0%e; Y/Y: 1.1% v 1.2%e

- (ES) Spain Apr Preliminary CPI EU Harmonized M/M: 0.8% v 0.8%e; Y/Y: 1.1% v 1.2%e

- (ES) Spain Mar Adj Retail Sales Y/Y: 1.9% v 1.3%e; Retail Sales (uandj) Y/Y: 1.5% v 2.1% prior

- (HU) Hungary Mar Unemployment Rate: 3.9 v 3.8% prior

- (TR) Turkey Apr Economic Confidence: 98.3 v 100.2 prior

- (AT) Austria Q1 Preliminary GDP Q/Q: 0.7% v 0.9% prior; Y/Y: 3.1% v 3.1% prior

- (SE) Sweden Mar Household Lending Y/Y: 6.9% v 7.0% prior

- (SE) Sweden Mar Retail Sales M/M: 1.2% v 0.5%e; Y/Y: 2.9% v 2.0%e

- (SE) Sweden Feb Non-Manual Workers Wages Y/Y: 2.4% v 2.5% prior

- (DE) Germany Apr Unemployment Change: -7K v -15Ke; Unemployment Claims Rate: 5.3% v 5.3%e

- (IT) Italy Mar PPI M/M: 0.4% v 0.3% prior; Y/Y: 2.4% v 1.8% prior

- (NO) Norway Apr Unemployment Rate: 2.4%e v 2.5% prior

- (TW) Taiwan Q1 Preliminary GDP Y/Y: 2.8% v 3.0%e

- (UK) Q1 Advance GDP Q/Q: 0.1% v 0.3%e; Y/Y: 1.2% v 1.4%e (slowest annual pace since 2012)

- (UK) Feb Index of Services M/M: -0.2% v +0.1%e; 3M/3M: 0.4% v 0.6%e

- (PT) Portugal Apr Consumer Confidence: 2.4 v 2.0 prior; Economic Climate Indicator: 2.1 v 2.1 prior

- (EU) Euro Zone Apr Business Climate Indicator: 1.35 v 1.28e; Consumer Confidence(Final): 0.4 v 0.4e, Economic Confidence: 112.7 v 112.0e, Industrial Confidence: 7.1 v 5.8e, Services Confidence: 14.9 v 15.9e

Fixed Income Issuance:

- (IT) Italy Debt Agency (Tesoro) sold total €5.75B vs. €4.75-5.75B indicated range in 5-year and 10-year BTP Bonds

- Sold €B vs. €2.25-2.75B indicated range in 0.95% Mar 2023 BTP bonds; Avg Yield: % v 0.68% prior; Bid-to-cover: x v 1.78x prior

- Sold €B vs. €2.5-3.0B indicated range in 2.00% Feb 2028 BTP bonds; Avg Yield: % v 1.83% prior; Bid-to-cover: x v 1.30x prior

- (IT) Italy Debt Agency (Tesoro) sold €3.5B vs. €3.0-3.5B indicated range in Sept 2025 CCTeu (Floating Rate Note); Avg Yield: 0.23% v 0.35% prior; Bid-to-cover: 1.42x v 1.45x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.1% at 383.9, FTSE +0.4 at 7451, DAX +0.7% at 12586, CAC-40 +0.1% at 5460, IBEX-35 +0.1% at 9905, FTSE MIB -0.6% at 23885, SMI +0.1% at 8839, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes:

- European Indices trade mixed with mixed earnings in Europe coupled with strong earnings in the tech space in the US. The FTSE advances after further weakness in Sterling on weaker than expected Advanced GDP data.

- Major auto name Daimler reported results which slightly missed estimates, however shares advance on a raised EBIT outlook. French auto name Renault trades lower after missing on Revenues. Elsewhere Electrolux is a notable faller on a sharp drop in profits, while Sanofi trades lower despite an EPS beat.

- Spanish Bank names BBVA and Caixabank also trade higher after earnings.

- Looking ahead notable earners include Oil giants Exxon and Chevron.

Movers

- Consumer Discretionary [Travis Perkins [TPK.UK] -1.4% (Earnings) ]

- Financials [BBVA [BBVA.ES] +2.3% (Earnings), RBS [RBS.UK] -1.8% (Earnings)]

- Industrials [Daimler [DAI.DE] +0.3% (Earnings), Renault [RNO.FR] -4.1% (Earnings), Electrolux [ELUXB.SE] -10.7% (Earnings), Airbus [AIR.FR] -0.3% (Earnings) ]

- Healthcare [ Sanofi [SAN.FR] -1.9% (Earnings)]

- Technology [Rexel [RXL.FR] -7% (Earnings)) ]

Speakers

- BOJ Gov Kuroda post rate decision press conference noted that there was no change in view for projected timing for target but the focus on time frame was not good for communication. Did not erase timeframe due to concerns about having to delay it again (**Note: last delayed back in July 2017). BOJ remained committed to achieving the 2% inflation target at the earliest time possible. Reiterated that would adjust policy as needed to achieve the inflation target

- ECB's Mersch (Luxembourg) reiterated ECB Council View that wages continued to edge higher and should contribute to price pressures. Inflation convergence would likely proceed only gradually, and remained contingent on a highly accommodative monetary policy stance

- SNB's Jordan reiterated view that negative interest rates and FX intervention remained essential. Tightening of monetary conditions would be premature at this time and would risk unnecessarily jeopardizing positive economic momentum

- ECB Survey of Professional Forecasters (SPF) maintained 2018 HICP (EU Harmonized CPI) at 1.5% while cutting 2019 and 2020 HICP (EU Harmonized CPI) outlook by 0.1% respectively. The survey raised 2018 GDP growth from 2.3% to 2.4% and 2019 GDP growth from 1.9% to 2.0% but cut 2020 to 1.6%

- Northern League leader Salvini said to be possible ready to break from Berlusconi's Forza Italia and form a govt with the Five Star Movement. The story was later refuted by another press outlet. (**Note: A break with Berlusconi could bring back talks with Five Star on a coalition govt)

- Sweden Central Bank (Riksbank) Dep Gov Skingsley panel comments on eKrona noted that was possible that cash would be phased out in coming years

- Turkey President Chief Adviser Ertem: Fiscal policy steps needed to support the central bank decisions

- Thailand Central Bank said to cut issuance of bills in order to support Baht currency (THB)

- Thailand Finance Ministry said to see Central bank keeping policy steady in 2018

- Two Koreas agreed to end 7-decade war and pursue complete denuclearization. Aim to declare end to war this year (**Note: conflict began in 1950 with no peace treat signed at the 1953 armistice) and set up a peace zone in West Sea. To open roads and railroads between the two countries

Currencies

- USD continued its firm tone against the major pairs despite the US 10-year yield curve moving back below the 3% level. Policy divergence continued to aid the greenback as normalization process getting dialed back in both Europe and Japan.

- The moderation in European growth continued as softer GDP data was seen in the session by France, Spain and UK. Various inflation data also stressed the headwinds towards moving to target range

- The GBP currency slumped after UK Q1 GDP registered a big miss with ONS deeming the slowdown was broader than expected and not only weather related. GBP/USD fell over 0.7% to test the lower end of the 1.38 level. The probability of a May BOE rate hike fell to under 40% after being a ‘done deal’ just weeks ago

- EUR/USD off another 0.2% to test 1.2070 and on the verge of a technical breakout to the downside as the 2018 gains evaporate.

- USD/JPY was steady at 109.35 despite the BOJ dropping its phase of achieving the inflation target in FY19/20. BOJ downplayed the removal of the text noting that it did not erase timeframe due to concerns about having to delay it again.

Fixed Income

- Bund Futures trade 21 ticks higher at 158.55 finding support with the ECB signaling no rush for the exit. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 121.97 higher by 59 ticks, as Britain's economy registers worst quarter in more than 5 years. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Friday’s liquidity report showed Thursday's excess liquidity rose to €1.879T from €1.863T prior. Use of the marginal lending facility rose from €30M to €40M.

- Corporate issuance saw 2 issuers raise $3.5B in the primary market

Looking Ahead

- (EU) Informal Eurogroup/Ecofin minister begin 2-day meeting in Sofia, Bulgaria

- 05:30 (PL) Poland to sell Bonds

- 06:00 (IE) Ireland Mar Retail Sales Volume M/M: No est v -0.2% prior; Y/Y: No est v 2.0% prior

- 06:00 (UK) DMO to sell combined £2.5B in 1-month, 6-month and 12-month Bills (£0.5B, £0.5B and £1.5B respectively)

- 06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to leave Key Rate unchanged at 7.25%

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Apr FGV Inflation IGPM M/M: 0.5%e v 0.6% prior; Y/Y: 1.8%e v 0.2% prior

- 07:30 (IN) India Weekly Forex Reserves

- 07:30 (CL) Chile Central Bank Traders Survey

- 08:00 (PL) Poland Central Bank (NBP) Apr Minutes

- 08:00 (BR) Brazil Mar National Unemployment Rate: 12.9%e v 12.6% prior

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond issuance

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Q1 Advance GDP Annualized Q/Q: 2.0%e v 2.9% prior; Personal Consumption: 1.1%e v 4.0% prior

- 08:30 (US) Q1 Advance GDP Price Index: 2.2%e v 2.3% prior; Core PCE Q/Q: 2.5%e v 1.9% prior

- 08:30 (US) Q1 Employment Cost Index (ECI): 0.7%e v 0.6% prior

- 09:00 (BE) Belgium Q1 Preliminary GDP Q/Q: No est v 0.5% prior; Y/Y: No est v 1.9% prior

- 09:00 (MX) Mexico Mar Trade Balance: $0.3Be v $1.1B prior

- 09:00 (BR) Brazil Mar Federal Debt Total (BRL): No est v 3.582T prior

- 10:00 (US) Apr Final University of Michigan Confidence: 98.0e v 97.8 prelim

- 11:00 (CO) Colombia Mar National Unemployment Rate: No est v 10.8% prior; Urban Unemployment Rate: No est v 11.9% prior

- 11:00 (EU) potential sovereign rating after European close (Belgium and Finland Sovereign Debt to be rated by Moody's ; Germany. Italy and UK Sovereign Debt to be rated by S&P; UK, Netherlands and Ukraine Sovereign Debt to be rated by Fitch

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 15:00 (US) Mar Agriculture Prices Received: No est v -0.2% prior

- 15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to cut Overnight Lending Rate by 25bps to 4.25%