Sample Category Title

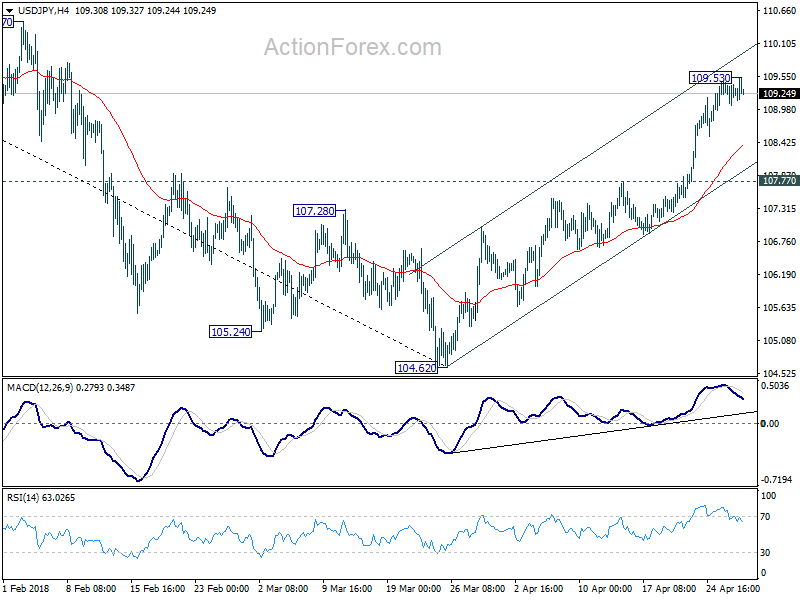

USD/JPY Mid-Day Outlook

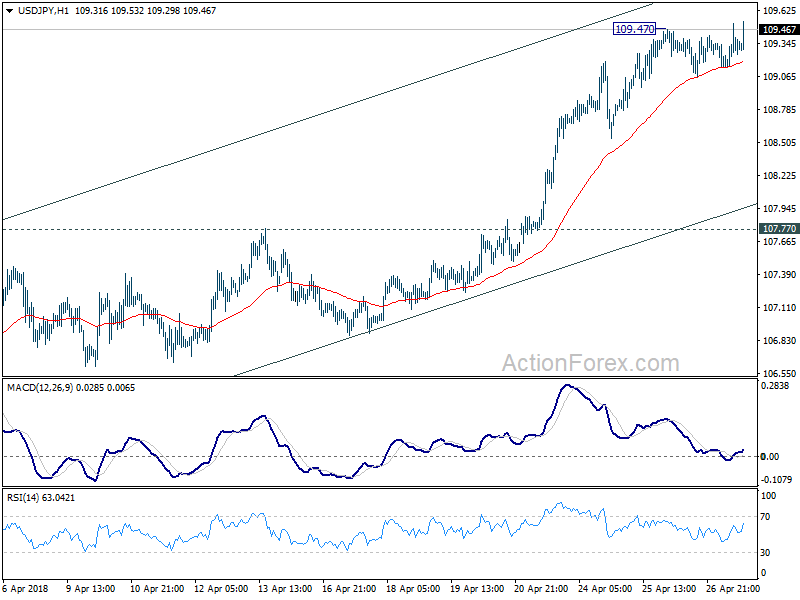

Daily Pivots: (S1) 109.09; (P) 109.27; (R1) 109.49; More...

USD/JPY edged higher to 109.53 but quickly retreated back to established range. Also, 4 hour MACD is staying below signal line. Intraday bias remains neutral first. Deeper retreat cannot be ruled out. But downside should be contained by 107.77 resistance turned support to bring another rally. Above 109.53 will resume the rise from 104.62 and target 61.8% retracement of 114.73 to 104.62 at 108.48 9 110.86 next.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.47).

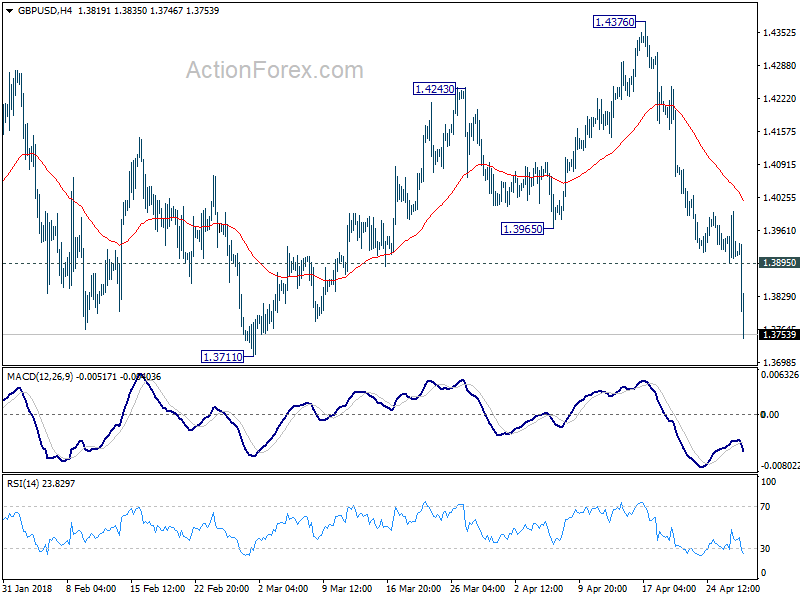

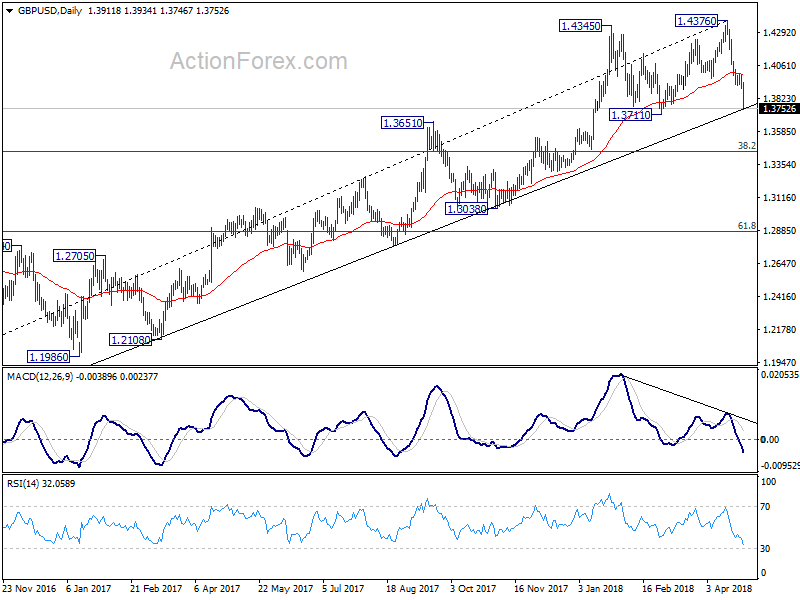

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3872; (P) 1.3934; (R1) 1.3975; More...

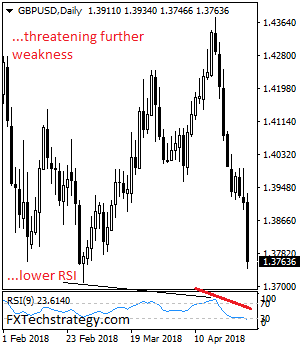

GBP/USD's decline from 1.4376 resumed after brief consolidation and accelerated to as low as 1.3746 so far. Intraday bias remains on the downside for 1.3711 key support level. Decisive break there should confirm medium term reversal and target 1.3448 fibonacci level. On the upside, above 1.3895 will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4257) again. Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

Dollar Rally Exhausted after Multiple Boosts this Week, Sterling and Euro Tumbled on GDP Misses

Dollar's rally seem to be a bit exhausted in early US session. After all, the greenback was lifted firstly by yield earlier this week, then by ECB yesterday. Additional buying jumped in after French GDP miss and than UK GDP miss in European session. Hence, even though the greenback is picking up its rally against Euro and Sterling after stronger than expected US GDP, the movement is limited. Dollar is also stuck in tight range against Yen, Aussie and Loonie.

US GDP grew 2.3% annualized in Q1. While that was a slowdown from 2.9% growth in Q4, it beat expectation of 2.0%. The figure is also realistically well that could be sustained. Price index rose 2.0%, below expectation of 2.2%. Employment cost index rose 0.8%, above expectation of 0.7%.

GBP dives as UK Q1 GDP grew only 0.1% qoq, weakest in five years

GBP dives sharply as Q1 GDP grew merely 0.1% qoq much worse than expectation of 0.3% qoq and prior quarter's 0.4% qoq. Also, that's the weakest quarterly growth figure in five years. Annual rate was unchanged at 1.4% yoy. Index of services rose 0.4% 3mo3m below expectation of 0.6%. The data could be the final nail to close the case of a May BoE rate hike. After all, with CPI slowed more than expected to 2.5% yoy in March, there is a lot of room for BoE to wait until November before raising interest rate again.

Chancellor of the Exchequer Philip Hammond blamed the weak data on weather. He said in an email statement that "today's data reflects some impact from the exceptional weather that we experienced last month, but our economy is strong and we have made significant progress." He added that "our economy has grown every year since 2010 and is set to keep growing, unemployment is at a 40 year low, and wages are increasing."

On the other hand, Rob Kent-Smith, the ONS' head of national accounts said in a statement that "our initial estimate shows the UK economy growing at its slowest pace in more than five years with weaker manufacturing growth, subdued consumer-facing industries and construction output falling significantly." And, "while the snow had some impact on the economy, particularly in construction and some areas of retail, its overall effect was limited with the bad weather actually boosting energy supply and online sales."

SNB Jordan: Premature tightening would risk unnecessarily jeopardizing the positive economic momentum

SNB Chairman Thomas Jordan said today that recent surge in EUR/CHF just represents "a reduction in the significant overvaluation" of the Swiss Franc. But he maintained that "our currency nevertheless remains highly valued". And he maintained that SNB should continue with an expansionary monetary policy with negative interest rate. In addition, "our continued willingness to intervene in the foreign exchange market as necessary".

Jordan further explained that "both instruments remain essential as the situation is still fragile. While the foreign exchange market has largely shrugged off recent equity market turbulence, circumstances in the financial markets - and thus by extension monetary conditions for the economy - could rapidly deteriorate again."

Also, he pointed out that "inflation remains low and inflationary pressure is modest despite our expansionary monetary policy. Tightening monetary conditions would be premature at this juncture, and would risk unnecessarily jeopardizing the positive economic momentum that has been established."

Euro selloff extends after French GDP miss

Fresh selling was seen in Euro after French data miss. French GDP growth slowed to 0.3% qoq in Q1, down from prior quarter's 0.7% qoq and missed expectation of 0.4% qoq. Annual rate decelerated to 2.1% yoy, down from 2.6% yoy, and missed expectation of 2.3% yoy. From Germany, import price index rose 0.0% in March. Unemployment dropped -7k in April. Unemployment rate was unchanged at 5.3%.

Also from Eurozone, Business climate dropped to 1.35 in April, above expectation of 1.28. Economic confidence was unchanged at 112.7 above expectation of 112.0. Industrial confidence was unchanged at 7, above expectation of 5.8. Services confidence dropped to 14.9, below expectation of 15.9. Consumer confidence was finalized at 0.4.

ECB Mersch: Inflation to rise gradually, contingent on highly accommodative monetary policy

ECB Executive Board member Yves Mersch said today that inflation will rise only gradually. He said in Sofia "overall, the underlying strength in the euro area economy continues to support our confidence that inflation will converge towards our aim over the medium term." But he added that " inflation convergence will likely proceed only gradually, and remains contingent on a highly accommodative monetary policy stance."

Also, Mersch added that "the transition towards policy normalization will begin once the Governing Council assesses there has been sustained adjustment in the path of inflation."

Separately, ECB Governing Council member Benoit Coeure said Eurozone growth isn't just recovery but an expansion. He added that there is solid and broad based expansion in the region.

They basically repeated what President Mario Draghi said yesterday.

BoJ stands pat, raised growth forecast, lowered inflation forecast

BoJ announced to keep monetary policy unchanged by 8-1 vote. Short term interest rate is held at -0.1%. The central bank will also continue with JGB purchases to keep 10 year yield at around 0%. The current pace of JPY 80T annual purchase is also maintained. BoJ revised up fiscal 2018 real GDP growth forecast to 1.6%, up from 1.4%. Fiscal 2019 GDP growth was also raised to 0.8%, up from 0.7%. On the other hand, Fiscal 2018 core CPI forecast was lowered to 1.3%, down from 1.4%. Fiscal 2019 core CPI, ex-sales tax hike, was kept unchanged at 1.8%.

Also from Japan, Tokyo CPI slowed to 0.6% yoy in April, down from 0.8% yoy and missed expected of 0.8% yoy. Industrial production rose 1.2% mom in March, well above expectation of 0.5% mom. Retail sales rose 1.0% yoy in March, below expectation of 1.5% yoy. Unemployment rate was unchanged at 2.5%.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3872; (P) 1.3934; (R1) 1.3975; More...

GBP/USD's decline from 1.4376 resumed after brief consolidation and accelerated to as low as 1.3746 so far. Intraday bias remains on the downside for 1.3711 key support level. Decisive break there should confirm medium term reversal and target 1.3448 fibonacci level. On the upside, above 1.3895 will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4257) again. Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

Economic Indicators Update

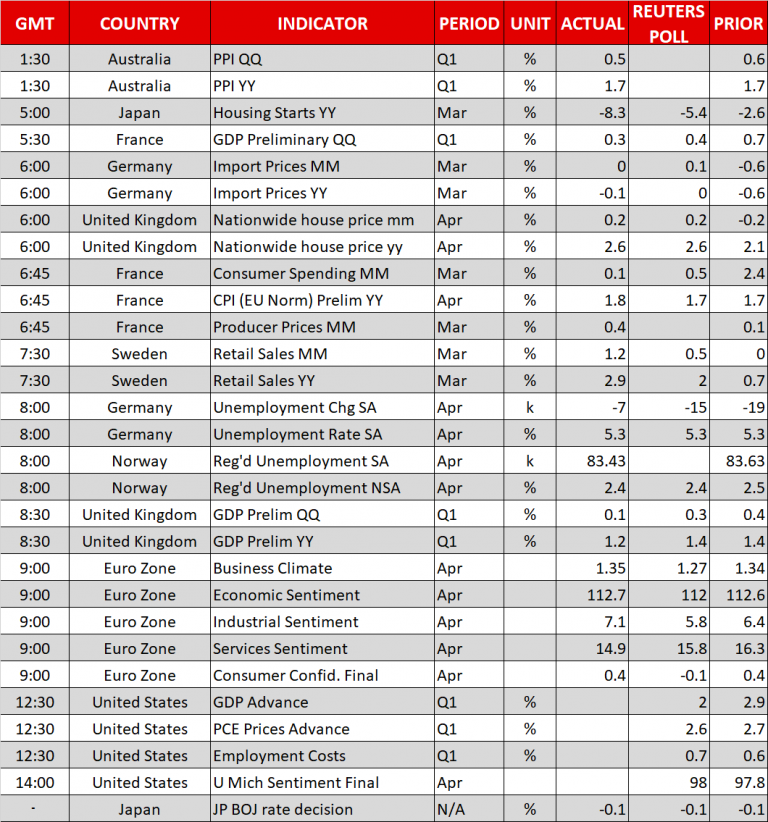

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance Mar | -86M | 200M | 217M | 172M |

| 23:01 | GBP | GfK Consumer Confidence Apr | -9 | -7 | -7 | |

| 23:30 | JPY | Jobless Rate Mar | 2.50% | 2.50% | 2.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Apr | 0.60% | 0.80% | 0.80% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | 1.00% | 1.50% | 1.60% | 1.70% |

| 23:50 | JPY | Industrial Production M/M Mar P | 1.20% | 0.50% | 2.00% | |

| 01:30 | AUD | PPI Q/Q Q1 | 0.50% | 0.40% | 0.60% | |

| 01:30 | AUD | PPI Y/Y Q1 | 1.70% | 1.20% | 1.70% | |

| 03:05 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Mar | -8.30% | -4.80% | -2.60% | |

| 05:30 | EUR | French GDP Q/Q Q1 A | 0.30% | 0.40% | 0.70% | |

| 06:00 | EUR | German Import Price Index M/M Mar | 0.00% | 0.10% | -0.60% | |

| 07:55 | EUR | German Unemployment Change Apr | -7K | -15K | -19K | -18K |

| 07:55 | EUR | German Unemployment Claims Rate Apr | 5.30% | 5.30% | 5.30% | |

| 08:30 | GBP | Index of Services 3M/3M Feb | 0.40% | 0.60% | 0.60% | |

| 08:30 | GBP | GDP Q/Q Q1 A | 0.10% | 0.30% | 0.40% | |

| 09:00 | EUR | Eurozone Economic Confidence Apr | 112.7 | 112 | 112.6 | 112.7 |

| 09:00 | EUR | Eurozone Business Climate Indicator Apr | 1.35 | 1.28 | 1.34 | 1.44 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | 7 | 5.8 | 6.4 | 7 |

| 09:00 | EUR | Eurozone Services Confidence Apr | 14.9 | 15.9 | 16.3 | 15.9 |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | 0.4 | 0.4 | 0.4 | |

| 12:30 | USD | GDP Annualized Q/Q Q1 A | 2.30% | 2.00% | 2.90% | |

| 12:30 | USD | GDP Price Index Q1 A | 2.00% | 2.20% | 2.30% | |

| 12:30 | USD | Employment Cost Index Q1 | 0.80% | 0.70% | 0.60% | |

| 14:00 | USD | U. of Mich. Sentiment Apr F | 98 | 97.8 |

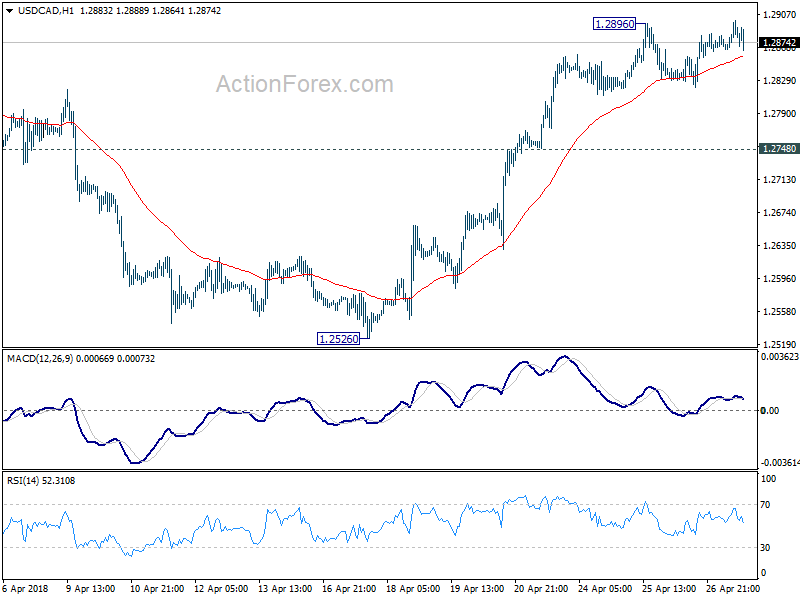

US GDP grew 2.3% in Q1, beat expectations. USDJPY and USDCAD still holding in tight range

USD buying is picking up again after stronger than expected data. US GDP grew 2.3% annualized in Q1. While that was a slowdown from 2.9% growth in Q4, it beat expectation of 2.0%. The figure is also realistically well that could be sustained. Price index rose 2.0%, below expectation of 2.2%. Employment cost index rose 0.8%, above expectation of 0.7%.

EUR/USD is on track for 1.2 handle while USD/CHF is also heading to parity. GBP/USD is within touching distance to 1.3711 key support after post UK GDP selloff.

But it should also be noted that USD/JPY and USD/CAD are somewhat stuck in very tight range despite rally attempt. 109.50 in USD/JPY and 1.2900 in USD/CAD will now be the focus in the current US session.

GBPUSD: Tumbles On Sell Off

GBPUSD: The pair tumbled on sell off on Friday leaving risk of further decline on the cards. Support lies at the 1.3700 level where a break will turn attention to the 1.3650 level. Further down, support lies at the 1.3600 level. Below here will set the stage for more weakness towards the 1.3550 level. Conversely, resistance stands at the 1.3800 levels with a turn above here allowing more strength to build up towards the 1.3850 level. Further out, resistance resides at the 1.3900 level followed by the 1.3950 level. On the whole, GBPUSD remains biased to downside.

Japan 225 Index Builds Base around 2-Month High; Rebounds on Long-Term Uptrend Line

Japan 225 index has advanced considerably since roughly the end of March, hitting a two-month high of 22526 during Friday’s trading. Price action at the moment is taking place not far below this peak. In a longer-timeframe, the index has been developing in an uptrend since June 2016 and this week it surpassed the 20-week simple moving average.

In the near term, a fresh upside push is possible with prices looking to post a third straight session of gains today. The RSI indicator appears to be in the positive territory and is pointing upwards, while the moving averages of stochastic oscillator entered the overbought zone, suggesting further bullish outlook.

Should the positive momentum gain further traction though, fresh resistance could come at the 23536 resistance level. A break above this level could lead prices towards the 24191 strong barrier, identified on January 23.

To the downside, immediate support is likely to come from the 20- and 40-SMAs at 21871 and 21621 respectively. A breach of this level could push prices lower towards 20322, which coincides with the long-term ascending trend line.

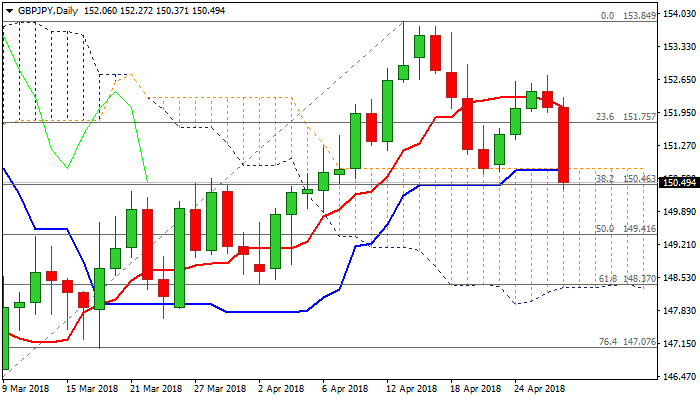

GBPJPY – Close Below Cracked Daily Cloud Top / Fibo 38.2% Support Would be Strong Bearish Signal

The cross was sharply lower on Friday, driven lower by downbeat UK GDP data, losing 1% for the day so far.

Strong bearish acceleration penetrated thick daily cloud (spanned between 150.79 and 148.31), as cloud top contained previous attack at 20 Apr, where corrective pullback from 153.86 high stalled.

Fresh bears broke below former correction low at 150.69 and also cracked next pivot at 150.46 (Fibo 38.2% of 144.98/153.84 rally), looking for close below these supports to generate stronger bearish signal on completion of failure swing pattern on daily chart and break of pivotal Fibo support.

Psychological 150 support is coming in focus with extension towards 149.66 (55SMA) and 148.97 (200SMA), seen on break.

Daily MA’s are turning into bearish setup, while 14-d momentum is attempting into negative territory, maintaining bearish pressure.

Broken cloud top marks initial resistance at 150.79, reinforced by daily Kijun-sen and only weekly close above would sideline immediate downside risk.

Res: 150.79; 150.97; 151.43; 151.91

Sup: 150.37; 150.00; 149.66; 148.97

Canadian Dollar Continues to Trade Quietly, US Advance GDP Next

The Canadian dollar is showing limited movement in the Thursday session. Currently, USD/CAD is trading at 1.2885, up 0.11% on the day. In the US, durable goods orders are expected to soften, and unemployment claims are forecast to drop slightly. There are no Canadian events on the schedule. On Friday, the US releases Advance GDP and UoM Consumer Sentiment.

Bank of Canada Governor Stephen Poloz testified before a parliamentary committee earlier this week, and his message about the economy was positive. Poloz said that he expected the economy to improve after a disappointing first quarter, and forecast that inflation would push above BoC’s target of 2% later in 2018. The bank maintained the benchmark rate at 1.25% last week, but is expected to raise rates as early as May. Policymakers are hoping that the NAFTA negotiations will make sufficient progress to enable the sides to announce an agreement framework, with the fine print to be finalized later in the year.

The US dollar continues to shine and the Canadian dollar has dropped 2.1% since April 16. On Friday, the US dollar has pushed the Canadian currency to the 1.29 level for the first time since April 3. Much of the credit for the greenback rally goes to rising yields on US bonds, which hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed above the symbolic level of 3.0%, which led to investors snapping up bonds at the expense of equities. As oil prices have been moving higher, this has led to expectations of higher inflation, which in turn, has increased sentiment that the Federal Reserve will increase rates four times in 2018, rather than three hikes. This has made the US dollar more attractive to investors.

SNB Jordan: Premature tightening would risk unnecessarily jeopardizing the positive economic momentum

SNB Chairman Thomas Jordan said today that recent surge in EUR/CHF just represents "a reduction in the significant overvaluation" of the Swiss Franc. But he maintained that "our currency nevertheless remains highly valued". And he maintained that SNB should continue with an expansionary monetary policy with negative interest rate. In addition, "our continued willingness to intervene in the foreign exchange market as necessary".

Jordan further explained that "both instruments remain essential as the situation is still fragile. While the foreign exchange market has largely shrugged off recent equity market turbulence, circumstances in the financial markets – and thus by extension monetary conditions for the economy – could rapidly deteriorate again."

Also, he pointed out that "inflation remains low and inflationary pressure is modest despite our expansionary monetary policy. Tightening monetary conditions would be premature at this juncture, and would risk unnecessarily jeopardizing the positive economic momentum that has been established."

Pound Dives To 2-Month Lows On UK GDP Growth Miss, US GDP Growth Next

Here are the latest developments in global markets:

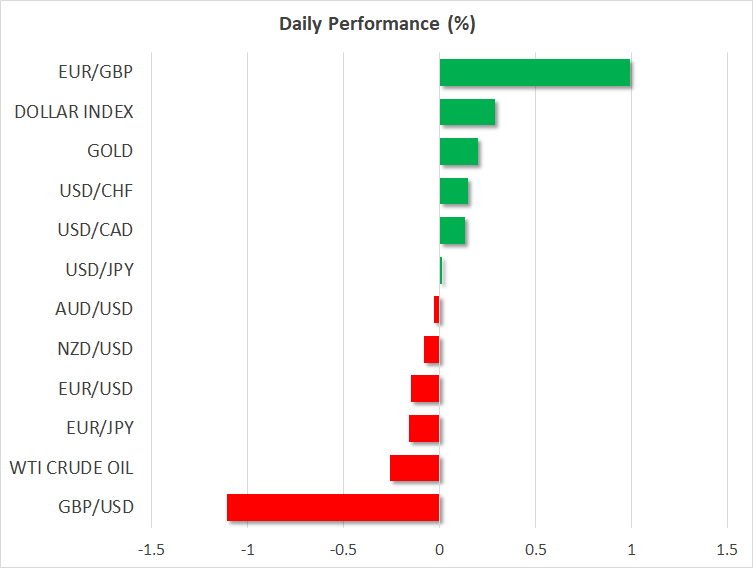

FOREX: Dollar bulls were set to win another battle for the fifth week mainly on the face of rising Treasury yields and in the absence of negative trade headlines. Geopolitical risks eased further as well after the North and South Korean leaders signed on Friday a declaration to end the war between the regions and confirmed their common prospects to denuclearize the Korean peninsula ahead of a crucial meeting between the North Korean leader and the US President at the end of May or early June. Dollar/yen remained mostly bid above the 109 key-level, last seen at 109.33 (+0.04%) and little changed after the BoJ decided to keep its rates steady but remove the timeframe for achieving its inflation goal. Against a basket of major currencies though, the dollar managed to win further ground as the pound and the euro were heading downwards on the day, with the dollar index hitting a fresh 3 ½ -month high of 91.90 (+0.28%). Particularly, pound/dollar dived to a two-month trough of 1.3778 (-0.91%) as the UK economy experienced the lowest growth rate in five years in Q1 2018. Euro/dollar was weaker as well at 1.2086 (-0.11%) despite Eurozone’s economic sentiment coming in better than expected in April. In the wake of the data, euro/pound recovered losses made during the past four-days, peaking at 0.8767 (+0.81%). Aussie/dollar and kiwi/dollar were flat at 0.7561 and 0.7063 respectively, near four-month lows. Dollar/loonie was also steady at 1.2869.

STOCKS: Upbeat earnings results in the banking sector and a recovery in tech stocks helped European shares to extend yesterday’s gains and tick another green box for the fifth consecutive week. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.08% and 0.07% respectively at 0900 GMT, with the satellite firm SES being the biggest winner after its Q1 2018 earnings surpassed projections. The German DAX 30 surged by 0.76%, the British FTSE 100 jumped by 0.45% hitting almost 3-month highs as the pound was diving on the back of disappointing UK GDP growth data, while the French CAC 40 climbed by 0.12%. The Italian FTSE MIB declined by 0.65%. In Asia, stocks closed higher, while in the US, futures tracking stock indices were in the red, pointing to a negative open.

COMMODITIES: A rising dollar weighed on oil prices today, with WTI crude and Brent retreating to $67.94 (-0.37%) and $74.51(-0.31%) per barrel respectively. Fears whether the US will re-impose sanctions on Iran, however, continued to linger in the background, limiting the pullback in prices. Note that on May 12, the US President will decide whether to hold or leave the 2015 nuclear deal with Iran. In precious metals, gold remained near to its opening price, trading at $1,317.70 (+0.06%) per ounce, on track to close lower for the second week

Day Ahead: US GDP Growth and University of Michigan consumer sentiment int the spotlight

Friday’s calendar features key US data releases in the remainder of the day, with the dollar probably going through another round of volatility today if the numbers surprise ahead of a busy week, including the Fed’s next policy meeting, the NFP employment numbers, and core PCE inflation numbers.

US GDP growth figures for the first quarter are due at 1230 GMT, with analysts predicting a growth rate of 2.0% on an annualized basis, significantly below Q4 2017’s reading of 2.9%. While the pullback could be in line with the measure’s trend in recent years, a surprising miss could pressure the dollar. Alternatively, stronger-than-expected releases could help the greenback to continue its bullish run. Investors will also take a look at Q1 employment costs and the advance estimate of core PCE prices which will be published along with the GDP report.

At 1400 GMT, the focus will turn to April’s final readings on consumer sentiment delivered by the University of Michigan.

In oil markets, investors will keep a close eye on the US oil rig count issued by the Baker Hughes company at 1700 GMT. Potential increases in active drilling rigs could add losses to oil prices.

Turning to today’s public appearances, at 1400 GMT, Bank of England Governor Mark Carney will speak at the launch of the EconoME programme.

In politics, the German Chancellor Angela Merkel is meeting US President Donald Trump today in an attempt to avert a trade war between the EU and the US.