Sample Category Title

XAUUSD Intraday Analysis

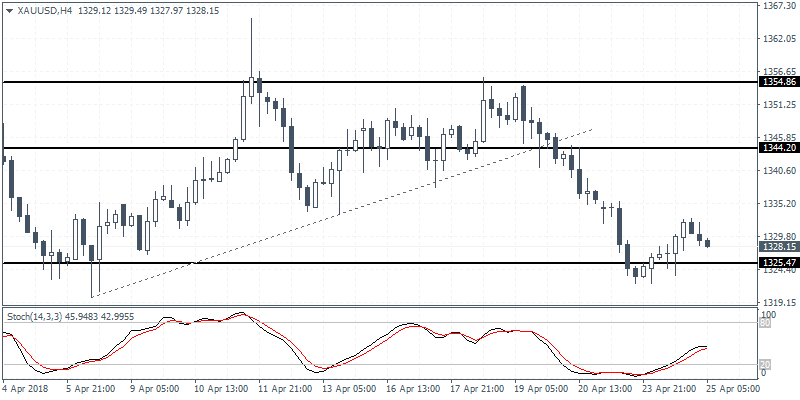

XAUUSD (1328.15): Gold prices attempted to rebound yesterday but the gains were erased rather quickly. The current decline could see gold prices testing the support level at 1325.50 level. This could mark a short term lower high that could suggest a possible correction to the upside. The resistance level at 1344.00 remains a key level of interest which gold prices could test in the near term if the support level at 1325.50 holds. In the event of a break down below 1325.50, we expect to see a short term new low being posted.

USD/JPY Daily Outlook

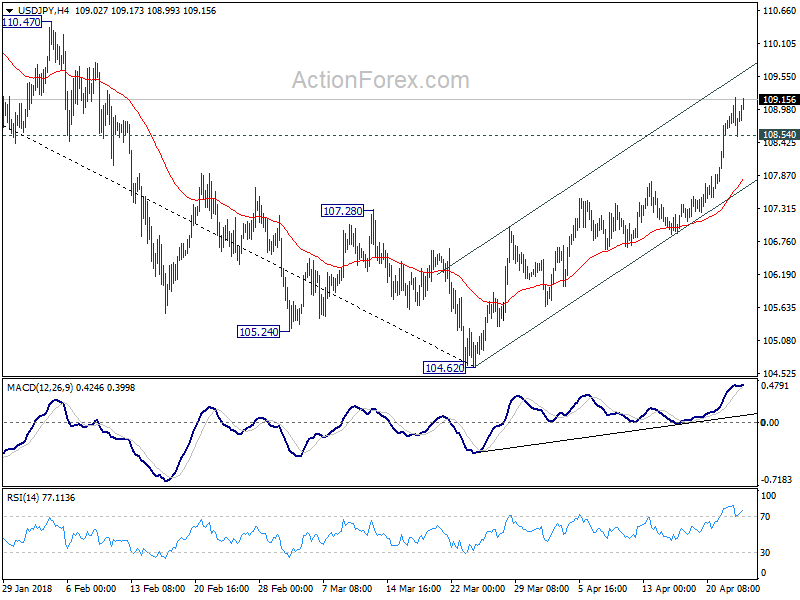

Daily Pivots: (S1) 108.50; (P) 108.85; (R1) 109.15; More...

With 108.54 minor support intact, intraday bias in USD/JPY remains on the upside for further rise. Current rally from 104.62 should extend to 61.8% retracement of 114.73 to 104.62 at 108.48 9 110.86 next. On the downside, below 108.54 minor support will turn bias neutral and bring consolidation first, before staging another rise.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.47).

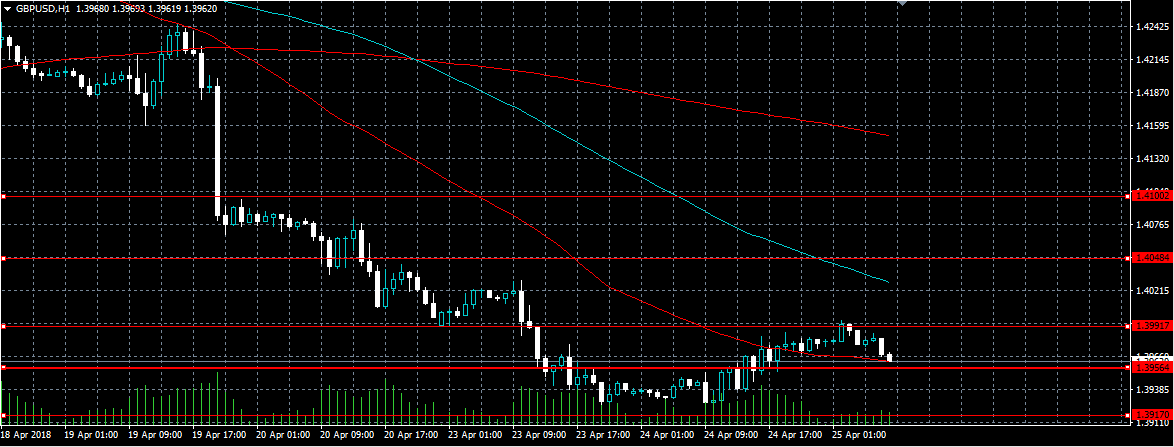

GBPUSD Intraday Analysis

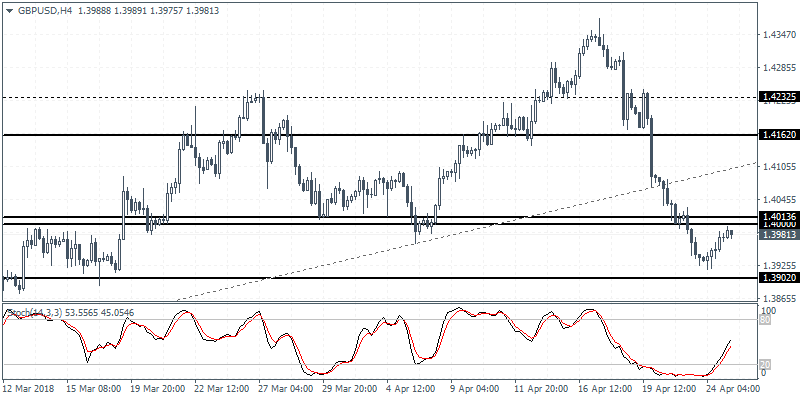

GBPUSD (1.3981): The British pound was seen posting a modest recovery, but price action remains biased to the downside below the resistance level of 1.4000. If this resistance level holds, GBPUSD is expected to maintain the range within 1.4000 and 1.3900 region. In the near term, there is a potential for GBPUSD to retest the breakout from the rising trend line near 1.4070. Further gains could push the GBPUSD toward the resistance zone of 1.4162. To the downside, we expect the support level at 1.3900 likely to hold the declines for now

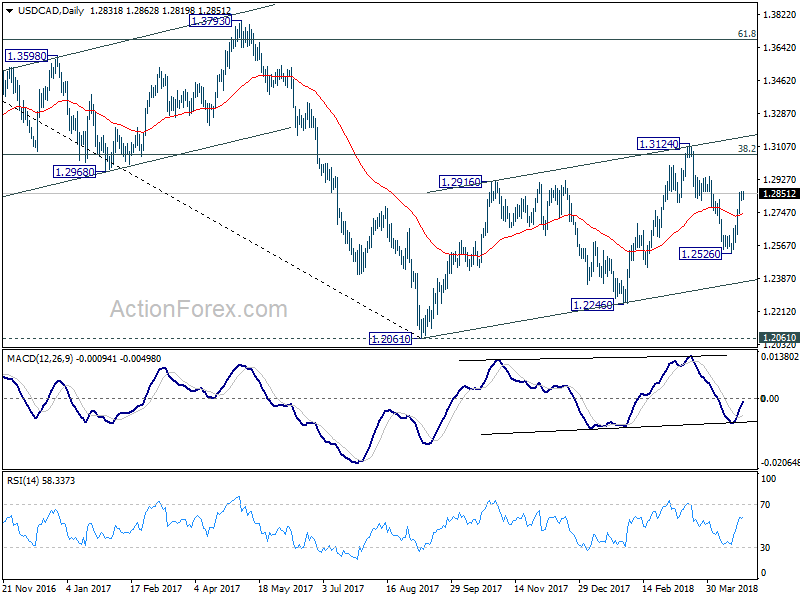

USD/CAD Daily Outlook

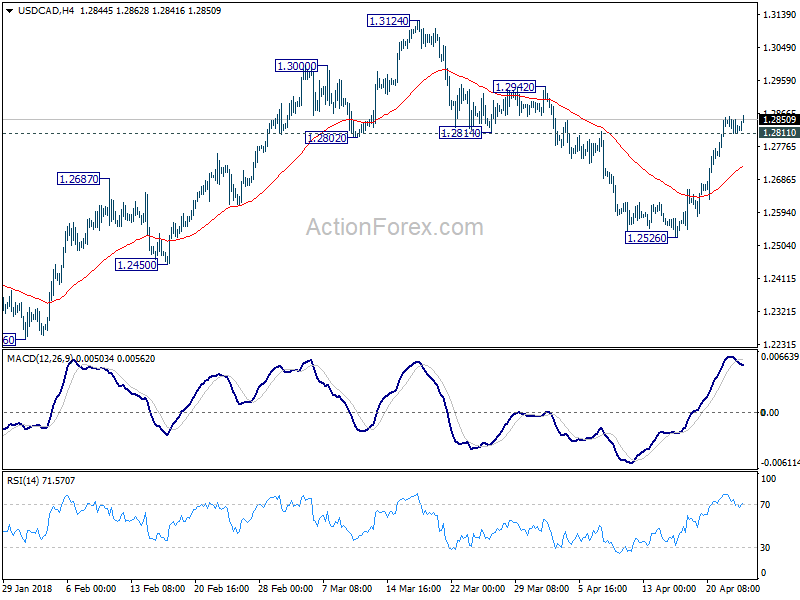

Daily Pivots: (S1) 1.2808; (P) 1.2834; (R1) 1.2857; More....

USD/CAD's rise resumes after brief consolidation and intraday bias remains on the upside. Current rally from 1.2526 should target a test on 1.3124 resistance next. On the downside, below 1.1.2811 minor support will turn intraday bias neutral first. But for now, further rise will be expected as long as 4 hour 55 EMA (now at 1.2719) holds.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685.

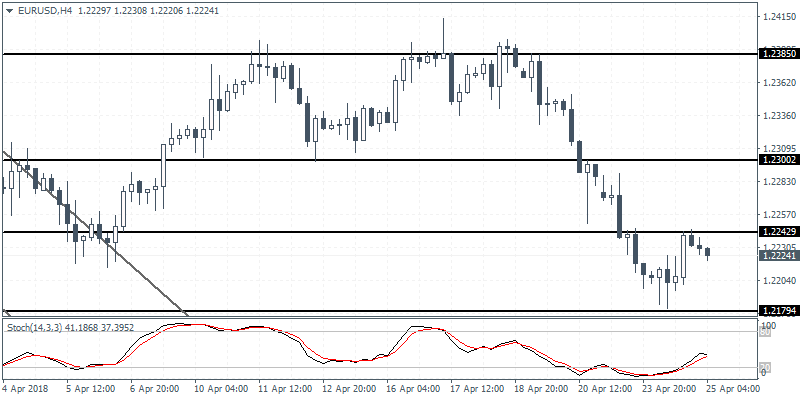

EURUSD Intraday Analysis

EURUSD (1.2224): The EURUSD currency pair was seen posting a modest rebound following the declines from the past few days. After price action fell to an 8-week low. The rebound off the lows from 1.2203 sent prices briefly higher only to test the upper resistance level at 1.2250. In the near term, we expect the EURUSD to consolidate within the resistance and support levels of 1.2250 and 1.2200 region. A breakout from this range could most likely signal the next direction in the currency pair. We expect to see the EURUSD retesting the upper main resistance level of 1.2300.

Australia Inflation Eases, Slow Day Ahead

The U.S. dollar was seen managing to hold some of the gains following the strong rebound from Monday. However, the dollar was mixed with the USD mostly stronger against the Japanese yen.

Economic data showed that the Australian quarterly CPI data showed a 0.4% increase on the quarter. This was lower than the forecasts of 0.5% and down from 0.6% increase posted in the previous quarter of 2017. The trimmed mean CPI was slightly higher at 0.5% on the quarter, matching the estimates.

The German Ifo business climate data showed a decline as the index fell to 102.1 compared to 103.3 previously. The slower pace of data signaled that economic growth might have slowed down in Germany.

Data from the U.S. showed that the CB consumer confidence data came out at 128.7, beating estimates of 126.0. It was also higher compared to the 127.0 reading posted previously.

Looking ahead, the economic calendar is quiet today. The weekly crude oil inventory report is expected and the BoC's Poloz is expected speak later in the day.

Dollar Initially Maintained A Positive Momentum

Markets

Yesterday, the US 10-y yield testing the psychological barrier of 3.0% was the key feature for global bond trading. The outcome of the this market battle was also important for other markets. EMU confidence data, including the German IFO business survey, were again soft, but didn’t improve bond sentiment in a profound way. Selling reaccelerated in US dealings. It even looked that a stronger than expected US consumer confidence and US new home sales would be able to force the 10-y yield break. The 3.0% level flashed on the screens, but the test was rejected. The rise in (US) yields (and other, corporate related issues) finally triggered a setback on the equity markets. This equity correction counterbalanced/blocked the upward momentum in core yields. In a daily perspective, the US yield curve bear steepened, with the 10 and 30-yield rising 4bp +. The US 10-y closed at 2.9995!. German yields finished the day little changed, even marginally lower.

Today, the US and EMU eco calendar is almost empty. This won’t prevent the battle for key US yield levels to continue. Asian equities show modest losses. A further stock market correction might slow the rise in core bond yields. However, a test/ break of the key resistance in the US 10-yr (3.05%/3.07%) and 30-yr yield (3.22%) might still be on the cards if upcoming US eco data remain solid. The German 10-yr yield bounced off key support levels (0.46%/0.48%), consolidating since the end of March. Last week’s move suggests the start of a new upleg, but the approaching ECB meeting is a hampering factor short term.

Yesterday, the dollar initially maintained a positive momentum. USD/JPY jumped temporary north of 109 and EUR/USD set a minor new correction low below 1.22. However, the dollar rally was blocked later in the session as the rise in US yields eased and as sentiment turned risk-off. Even so, the correction of the US currency remained modest. This morning, the dollar is holding within reach of the recent peaks against most majors. A correction on the equity market markets might make the picture a bit murky for the dollar. However, we have the impression that the dollar maintains the benefit of the doubt. The EUR/USD 1.2155 rang bottom is again on the radar. The trade-weighted USD (DXY) is close to a comparable level (91 range top). A break would improve the ST picture of the USD.

Yesterday, EUR/GBP continued the consolidation pattern in the mid 0.87 area. UK eco data (Budget data and CBI order data) were mixed and had little impact on sterling. Sterling held off the recent lows despite ongoing noise on Brexit and despite reduced market expectations on a BoE rate hike. Today, there are no important eco data in the UK. So global sentiment and Brexit headlines (debate on the customs union) will again set the tone for sterling trading. For now, the EUR/GBP 0.88 resistance looks quite solid short term.

News Headlines

US equity indices turned south after a positive open. Higher bond yields and uncertainty on the outlook for corporate earnings after strong Q1 earnings weighed on equities. The Dow Jones and the Nasdaq closed the session 1.70% lower. Asians equities are also trading in negative territory, but losses are more modest than in the US.

U.S. President Trump indicated that a new NAFTA agreement could reached in the near future. Foreign trade Ministers from Canada, the US and Mexico met in Washington. Especially the progress made on the key issue of automobile production looks promising.

Today, the eco calendar in the US and European only contains second tier data releases. The earnings season is in full swing with, amongst many others, Boeing, Twitter, Visa, AT&T and Facebook reporting results. Markets will also look forward to tomorrow’s ECB policy meeting/press conference.

GBPUSD Intraday Bullish Above 1.3956

The British pound continues to recover to the upside against the greenback, hitting 1.3994, as the U.S dollar index starts to correct lower after a strong start to the week. The GBPUSD pair currently trades around the 1.3960 level, after finding strong dip-buying demand from the 1.3917 level. With a lack of market moving macroeconomic data from the United Kingdom, technical traders a likely to focus on the U.S dollar index and the pivotal 1.3992 level.

The GBPUSD pair is intraday bullish while trading above the 1.3956 level, further gains towards the 1.4048 and 1.4100 levels remains possible.

If the GBPUSD pair fails to gain traction above the 1.3992 level, sellers may test towards the 1.3917 and 1.3880 support levels.

USDJPY Testing Key 109.00 Level

The U.S dollar has started to recover higher against the Japanese yen currency, after earlier dropping lower, alongside global equity market prices. The USDJPY pair is currently trading around the 109.00 level in early Wednesday trading, after finding strong technical resistance from the 109.19 level. Traders are likely to remain focused on the key 108.50 to 109.00 price-range, and the high correlation the pair has with equity market sentiment.

The USDJPY pair is only intraday bullish while trading above the pivotal 108.50 level, resistance is now found at the 109.19 and 109.78 levels.

If the USDJPY pair trades below 108.50 level, price-action may test towards the 107.92 and 107.60 support levels.

BOC Governor Speech Headlines Quiet Day For Economic Calendar

A dearth of economic data could make for a quiet trading session on Wednesday. Aside from a speech with possible policy implications, there isn't much in the way of compelling data.

In Europe, a report on French consumer confidence will make its way through the financial markets at 06:45 GMT. The April consumer confidence index is projected to hold steady at 100.

The Centre for European Economic Research will deliver its monthly report on Swiss business expectations at 08:00 GMT. The report could influence movement in the Swiss franc.

Shifting gears to North America, the US Mortgage Bankers Association will report on weekly mortgage applications for the period ended 20 April. The report is scheduled for release at 11:00 GMT.

Meanwhile, the US Energy Information Administration (EIA) will release its weekly crude inventory report at 14:30 GMY. Crude stockpiles are forecast to decline by more than 2.6 million barrels in the week ended 20 April.

In terms of monetary policy, Bank of Canada (BOC) Governor Stephen Poloz will deliver a speech at 20.15 GMT. The BOC has taken a step back from its hawkish outlook now that the Canadian economy is showing signs of weakening. That said, Canada is still expected to raise interest rates this year.

The economic calendar heats up in the latter half of the week as the European Central Bank (ECB) delivers a verdict on interest rates and the US government reports on durable goods orders and gross domestic product (GDP). The Japanese central bank will also deliver a rate verdict later this week, which should give traders plenty to consider heading into the weekend.

USD/CAD

After a tumultuous week, the Canadian dollar began its long road to recovery on Tuesday as the greenback failed to extend its rally. At the time of writing, the USD/CAD exchange rate was valued at 1.2837, where it was little changed from the previous close. The pair has skyrocketed more than 200 pips since last Thursday amid rising US bond yields.

EUR/USD

Europe's common currency pushed higher on Tuesday as the dollar lost ground on major currencies following a bullish start to the week. EUR/USD bottomed below 1.2200 during the previous session but has since rebounded to around 1.2223. Immediate resistance is seen at 1.2260, followed by 1.2290, which corresponds to the 23 April high. On the flipside, support is located at 1.2215, followed by 1.2180.

GBP/USD

Cable attempted a recovery on Tuesday, but gains were firmly capped below 1.4000. At the time of writing, GBP/USD was valued at 1.3978, where it was little changed. The 1.4000 level continues to offer resistance. A firm bottom is difficult to gauge at this point given cable's precipitous declines over the past week.