Sample Category Title

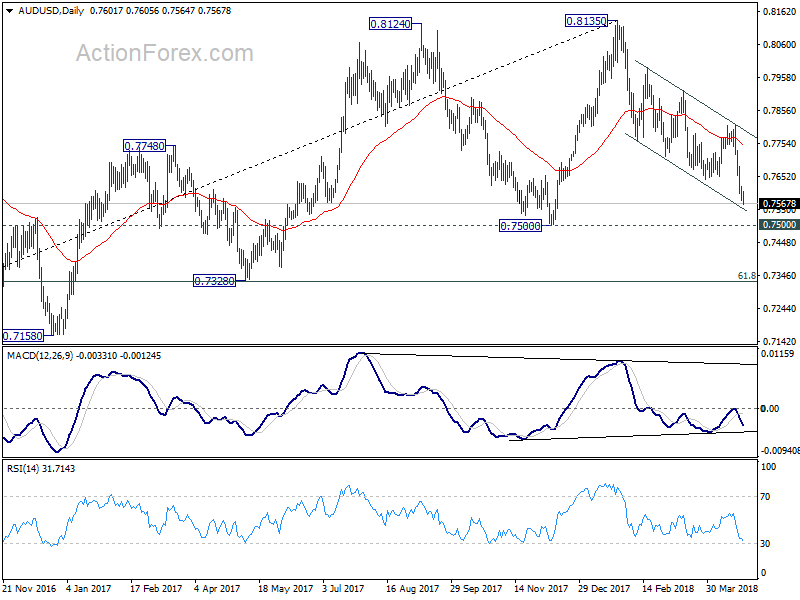

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7575; (P) 0.7598; (R1) 0.7625; More...

AUD/USD's decline continues today and reaches as low as 0.7564 so far. Intraday bias remains on the downside for 0.7500 key support level next. Decisive break there will indicate medium term reversal and target 0.7328 support next. On the upside, above 0.7620 minor resistance will turn intraday bias neutral and bring consolidations. But recovery should be limited below 0.7812 resistance to bring fall resumption.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Intermarket Movements to Drive Forex Trading with Light Calendar Today

Dollar traded mixed overnight as while 10 year yield breached 3% handle, there was no follow through selling in bonds that kept it above that level. On the other hand, the situation was complicated by the selloff in stocks due to earnings, which propelled Japanese Yen briefly higher. The greenback is regaining strength in Asian session. In particular, Dollar is already extending recent rally against Aussie, and Swiss Franc. With an exceptionally light calendar today, intermarket movements will be the main driver in FX.

Technically, in the currency markets, the first focus today is that EUR/CHF is heading back to 1.2 handle after brief consolations. Secondly, there will be some minor levels to pay attention. Those include 1.2181 temporary low in EUR/USD, 1.3917 temporary low in GBP/USD 109.19 temporary top in USD/JPY and 1.2860 temporary top in USD/CAD.

The economic calendar is exceptionally light today. Asian session was already quieter than usual with Australia and New Zealand on holiday. Japan released all industry activity index which rose 0.4% mom in February and that triggers little reaction in the markets. Looking ahead, Italy is on bank holiday today. Credit Suisse will release economic expectation for Swiss. China will release conference board leading index. US will release crude oil inventories. BoC Governor Stephen Poloz will speak today too. And traders will look through today's event for ECB rate decision tomorrow, and Q1 GDP of US and UK on Friday.

Having said that, the interaction between different financial markets would probably be the drivers today.

DOW closed sharply lower overnight by -424.56 pts or -1.74%, at 24023.13. The rebound from 23344.52 is confirmed to be complete at 24585.97, after failing to sustain above 55 day EMA. Further fall would be seen back to 23344.52 ahead, as long as 24585.97 holds. While there could be some support at that level, an eventual break is expected to 38.2% retracement of 15450.56 to 26616.71 at 23351.24.

US 10 year yield edged higher to 3.003 overnight and breached 3% handle briefly. Then, it failed to sustain above 3% and closed at 2.983, up only 0.010. Bear in mind again that 3% is an important psychological level for many investors. And there is a key resistance of 3.036, 2013 high. These could both limit the strength of TNX for the very near term.

If the markets movements unfold like the above today, that is, stocks tumble and yield struggles to advance, we could see a reversal of fortune in Aussie and yen. That is, firmness in US yields will pressure both Aussie and Yen. But in case of risk aversion triggered by other factors, like earnings, Yen could be supported by risk aversion. This would be an interesting point to watch today.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2231 (R1) 1.2265; More....

Intraday bias in EUR/USD remains on the downside for 1.2154 support. Decisive break there should confirm the bearish case of medium term reversal. And EUR/USD should then target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. On the upside, 1.2245 minor resistance will turn bias neutral first. But risk will now stay on the downside as long as 1.2413 resistance holds.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 4:30 | JPY | All Industry Activity Index M/M Feb | 0.40% | 0.50% | -1.80% | -1.10% |

| 14:30 | USD | Crude Oil Inventories | -1.1M |

Chinese Press Speculates Room To Loosen Policy

General Trend:

- Asian equities track declines in the US

- Canon Inc declines ahead of expected Q1 earnings report

- Takeda declines over 9% after again raising bid for Shire

- LG Display moves between gains and losses; Q1 results below ests, cut Capex forecast

- Komatsu declines over 4% after results and comments from Caterpillar

- Taiwan officials comment on recent declines in the equity market

- Recently announced China PBoC RRR cut took effect today

- Chinese press continues to speculate about further RRR cuts

- PBoC drained liquidity in OMO in order to ensure ‘reasonable and stable’ bank liquidity

- Standard Chartered HK unit said to raise term deposit rates in the face of higher money market rates

- Various automakers comment at the Beijing auto show

- South Korea Q1 prelim GDP data due for release on Thursday

- Bank of Japan (BoJ) 2-day policy meeting begins on Thursday, decision and forecasts expected on Friday (April 27th)

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.7%; closed -0.2%

- TOPIX Electric Appliances index -1.1%, Iron & Steel -0.7%, Securities -0.7%

- Automakers outperform as USD/JPY moved above ¥109

- Kobe Steel, 5406.JP Japanese prosecutors have begun investigating Kobe Steel's quality data scandal, which could lead to charges - Nikkei; later confirmed by the company

- (JP) Japan LDP Official: Dissolving lower house is an option - Japan press

- (JP) JAPAN FEB ALL INDUSTRY ACTIVITY INDEX M/M: 0.4% V 0.5%E

Korea

- Kospi opened -0.8%

- (KR) South Korea Apr Consumer Confidence: 107.1 v 108.1 prior (1-yr low)

- LG Display, 034220.KR Reports Q1 (KRW) Net loss 59.5B v loss 9.5Be; Op loss 98.3B v profit 12.7Be; Rev 5.7T v 6.0Te

- (KR) South Korea Finance Ministry reiterates will take measures if herd behavior is seen in FX, FX rate to be determined by market

China/Hong Kong

- Hang Seng opened -0.5%, Shanghai Composite -0.5%

- Hang Seng Information Tech Index -2.3%, Telecom -1.3%, Financials -0.6%

- (CN) China does not need 'overly loose' monetary policy, domestic economy has no big downturn risks in 2018 - China Securities Journal

- (CN) China official sees 'big room' for future RRR cut, sees 600-800 bps in RRR cuts in 3 years - Chinese Press

- US President Trump confirms Mnuchin will visit China

- (CN) China PBoC Open Market Operation (OMO): skips OMO v injects CNY30B in 7-day reverse repos prior; Net: drains CNY150B v CNY30B prior

- (CN) China PBoC sets yuan reference rate at 6.3066 v 6.3229 prior

- (CN) China PBOC: RRR cut effective today, will offset impact of maturity; Reminder April 17th: (CN) CHINA PBOC CUTS RESERVE RATIO REQUIREMENT (RRR) BY 100BPS FOR QUALIFIED BANKS (targeted cut); effective Apr 25th

- Techcomp,[+59%], 1298.HK Holders to sell ~44.4% stake to Baodi International Investment; to resume trading on April 25th

- (CN) China officials are drafting guidelines on promoting imports as part of bid to balance foreign trade - CSJ

- (CN) Chinese press looks at comments from Politburo meeting noting that they reiterated monetary policy was stable and neutral but did not mention controlling M2 credit growth like the prior work report - CSJ

Australia/New Zealand

- ASX 200 closed for holiday

Other Asia

- (ID) Indonesia Central Bank urges companies to hedge FX needs beyond regulatory minimum to help maintain Rupiah stability

- (ID) Indonesia Central Bank sells $179.5M in 6 and 9 month FX bills

- (TW) Taiwan Central Bank Gov Yang: Chance to raise key rate in June isn't high

North America

- US equity markets ended lower: Dow -1.7%, S&P500 -1.3%, Nasdaq -1.7%, Russell 2000 -0.6%

- S&P500 Industrials -2.8%, Materials -2.7%

- Southwest Airlines LUV Completed all engine inspections under emergency order; continuing additional voluntary engine reviews; Declines comment on the results of the inspections of engine fan blades

- (US) Weekly API Oil Inventories: Crude: +1.1M v -1.0M prior

- (CA) Canada Foreign Min Freeland: NAFTA negotiations to continue tomorrow; prepared to respond to new proposals

- (CA) China rating agency Dagong Global Credit cuts Canada sovereign outlook to Negative

- (US) Republican Lesko wins special election for Arizona US House Seat (as expected) - US Press

Europe

- (DE) Reportedly Germany to lower 2018 GDP growth outlook to 2.3% from 2.4% - press

- (IT) Italy 5-Star Party leader Di Maio: talks with the Northern League have ended; idea of a coalition govt with the center-right has passed

- Shire, SHP.UK Takeda makes revised proposal in cash and shares totaling £49/shr (£27.26 in new Takeda shares and £21.75 in cash) for total value of £46B

- (UK) EU said to be prepared to offer Britain a better trade deal if the UK decides to stay inside the customs union after Brexit - financial press

- Kering [KER.FR]: Reports Q1 Rev € 3.12B v €2.80Be

- OSRAM [OSR.DE]: Reports preliminary Q2 rev €1.01B, adj EBITDA margin 15.1%; cuts FY18 guidance

- Iberdrola [IBE.ES]: Reports Q1 Net €838M v €810Me, EBITDA €2.32B v €2.25Be, Rev €9.34B v €8.3B y/y

Levels as of 02:00ET

- Hang Seng -1.0%; Shanghai Composite -0.4%; Kospi -1.0%

- Equity Futures: S&P500 -0.3%; Nasdaq100 -0.3%, Dax -0.2%; FTSE100 -0.1%

- EUR 1.2239-1.2211; JPY 109.08-108.79; AUD 0.7606-0.7571;NZD 0.7117-0.7090

- Jun Gold -0.4% at $1,327/oz; Jun Crude Oil -0.1% at $67.61/brl; May Copper -0.2% at $3.13/lb

Risk-Off Returns As 10 Year US Treasuries Test 3% Level

The market turned yesterday as the 3% level on the US 10 Year was tested and the 2-10 yield spread climbed from multi-year lows set earlier in the month. This caused some weakness in the USD, although it has regained some strength this morning. Equities were down over 1% yesterday in risk-off markets, with USDJPY also taking a hit despite starting the day strong. JPY crosses took the hit late in the day but have recovered well overnight. Gold moved higher to $1332.50 resistance but has fallen lower again, while oil fell from its $69.30 high to support at $67.50. Markets are set to remain choppy today as traders seek direction on a day of light economic calendar activity, with US Treasuries remaining in focus.

German IFO – Current Assessment (Apr) was 105.7 v an expected 106.0, from 125.9 previously which was revised down to 110.6. IFO – Expectations (Apr) were 98.7 v an expected 99.5, from 104.4 prior, which was revised down to 101.0. IFO – Business Climate (Apr) was 102.1 v an expected 102.7, v 114.7 previously, which was revised down to 105.7. This index rebased yesterday, from the year 2005 to a base year of 2015. This means last month’s Business Climate reading of 114.7 changed to 103.2. This was to include the service sector for the first time, which makes up nearly 60% of GDP. The data showed a weakening business climate in Germany, as expected. This data cannot be ignored as it surveys 7,000 businesses and is a leading indicator of economic direction. EURUSD moved higher from 1.21988 to 1.22110 after the release.

US House Price Index (MoM) (Feb) was 0.6% v an expected 0.5%, v 0.8% previously, which was revised up to 0.9%. This data slipped lower after a strong improvement last month but beat the expected 0.5%. S&P/Case-Schiller Home Price Index (YoY) (Feb) was 6.8% v an expected reading of 6.3%, against a prior 6.4%. This data point has been holding steady since the late 2014 low. The data surprised to the upside, with the highest reading since September 2014. This shows a strong housing market in the US, although supply remains an issue. USDJPY moved higher from 108.787 to 109.061 as a result of this data.

US New Home Sales (MoM) (Mar) were 0.694M against an expected reading of 0.630M, from 0.618M previously, which was revised up to 0.667M. New Home Sales Change (MoM) (Mar) was 4.0% against an expected 1.9%, from -0.6% previously, which was revised up to 3.6%. On the back of strong Existing Home Sales data on Monday, the trend improved further after having fallen for three months since the November high. The improvement in these figures shows a pickup in confidence in the US housing market, with a beat on the headline number, but, more importantly, big positive revisions. This rounds out what has been a very good couple of days for US Housing data. USDJPY hit a low of 108.935 after the release but subsequently turned higher to 109.125.

EURUSD is down -0.15% overnight, trading around 1.22128.

USDJPY is up 0.21% in early session trading at around 109.041.

GBPUSD is down -0.10% this morning trading, around 1.39618.

Gold is down -0.26% in early morning trading at around $1,326.79.

WTI is down -0.24% this morning, trading around $67.59.

Elliott Wave Analysis: SPX May Start A New Leg Lower

SPX short-term Elliott Wave analysis suggests that the decline to 2553.8 low ended intermediate wave (W). Above from there, the rally ended in intermediate wave (X) at 2717.49 high and the same time also completed the correction against 3/13/2018 peak (2801.9). The Index however still needs to break below wave (W) at 2553.8 low, and more importantly below 2/10 low (2532.69) to confirm that the next leg lower has started.

The internal of Intermediate wave (X) unfolded as a double three Elliott Wave structure, where Minor wave W ended at 2672.08. Minor wave X ended at 2586.27 and Minor wave Y of (X) ended at 2717.49. Down from there, the index made a 3 waves reaction lower as a zigzag Elliott Wave structure where Minute wave (a) ended at 2657.99 and Minute wave (b) bounce ended at 2683.55 high. Minute wave (c) of ((w)) appears complete at 2617.32 low. This level is within the 100%-123.6% Fibonacci extension area of Minute (a)-(b) at 2609.9 – 2624.01. Near-term, expect the index to rally in Minute wave ((x)) to correct cycle from 4/18 high (2717.52) before further downside is seen, provided that pivot at 2717.52 high stays intact.

SPX 1 Hour Elliott Wave Chart

The US Bond Market Remains Under Pressure And Overnight

Market movers today

There are no significant economic data releases on the calendar, so financial markets will continue to focus on the rise in global yields and its implications for risk assets, including emerging markets.

In Turkey , central bank rate decision is announced today. While the recent TRY weakness has brought more intrigue into the decision, last week's TRY's rally on Erdogan's early election plan is bringing some relief, keeping the central bank away from a hike, we believe. We expect the benchmark repo rate to stay at 8.00%, although the late-liquidity window rate may be raised, which is the most relevant monetary policy rate at the moment.

In Sweden , residential developer Bonava presents its Q1 earnings report which might attract some attention as construction activity is important from a growth perspective.

Selected market news

The US bond market remains under pressure and overnight, the yield on 10 year US treasuries finally broke above the pivotal 3.0% mark and reached a new four year high. The break above 3% was only very temporary though, yields edged lower again and stand at 2.9977 this morning.

US equity markets were weighed down by rising yields and as the Richmond manufacturing index was much weaker than expected in April, falling 18 points to -3. All three regional PMIs released so far this month (Empire, Richmond and Philly) have declined on an ISM-weighted basis, suggesting a softening in manufacturing activity in April or at least that ISM has peaked. Our base case is still that the ISM manufacturing will fall over the next six months.

The S&P500 index closed 1.34% lower yesterday and Chinese and Japanese markets also trade lower this morning amid concerns about rising US yields. In February, rising bond yields was one of the reasons behind the equities correction that followed, and while volatility in the US interest rate market remains relatively low and equity price fluctuations are still well off the highs seen in February and March this year, yesterday's sell-off in US equities indicate that rising bond yields once again could derail investor optimism. Hence, while the break of the 3% level in the 10 year US yield likely has created room for higher yields near term, we continue to hold the view that it is too early to call for a major fixed income sell-off - especially in Europe - given the business cycle outlook and still dovish central banks.

Bank Of Japan Preview: Steady as She Goes

- We expect the Bank of Japan to maintain its 'QQE with yield curve control' policy unchanged at the next monetary policy meeting ending on Friday 27 April.

- We do not expect new super dovish deputy Wakatabe to team up with Kataoka in the dissenting camp but instead pull board consensus slightly more dovish.

- Currently we consider the probability of further easing to be at least as high as the probability of tightening, but we do not see any changes to policies within a oneyear horizon.

- We expect USD/JPY to continue to trade mostly sideways within 105-110 in the near term, targeting 108 in 3M. In our view, it would require a substantial dovish shift in the Bank of Japan's rhetoric for USD/JPY to settle above 110.

New deputy could pull board consensus more dovish

Since the beginning of the year, we have seen some change in the communications strategy from the Bank of Japan (BoJ). They used to refrain from answering questions related to future tightening, which left markets completely in the dark and caused some very jumpy reactions when Kuroda on occasions hinted at something related anyway. On 3 April, Kuroda said in parliament that internal discussions are at least taking place in the BoJ on the subject. He added that 'open talk” of tapering or ending its stimulus would confuse markets.

Since the last meeting in March, the two deputies Iwata and Nakaso have been replaced by career central banker Masayoshi Amamiya and Professor Masazumi Wakatabe. Amaniya is likely to be located somewhere in the middle of the pack, when it comes to the board members' policy stance – he did after all mastermind much of the policy measures himself, when he was head of both the bank's monetary affairs group and markets division. Wakatabe, on the other hand, has been a vocal advocator of aggressive easing and he has previously expressed criticism of yield curve control, questioning whether it is enough to revamp inflation expectations. In December, he mentioned that options for further stimulus included raising the bond purchase guideline by JPY10trn a year, and even increasing the inflation target to three percent to lift up expectations. These comments align best with the one dissenter on the board, Goushi Kataoka, who has expressed a desire to reach the inflation target before the consumption tax hike in October next year and a possible economic downturn in the United States. We do not expect Wakatabe to actually join forces with Kataoka, but rather for board consensus to shift slightly more dovish. Kuroda has previously expressed a preference for unanimity among the governors.

The economy is losing momentum

Growth is primarily driven by foreign demand whereas private consumption is still looking weak. As growth in Japan's most important export markets is becoming slightly more subdued and exporters now have to deal with a stronger JPY, we expect the economic upswing to lose some momentum. Q1 figures so far look fairly weak, and that is likely to be reflected in the BoJ's quarterly macroeconomic outlook released alongside the statement on monetary policy. We thus expect some small downward revisions of the GDP forecast

We will also be getting a new inflation forecast from the BoJ. 'According to sources familiar with the matter”, the FY2019 forecast will stay roughly unchanged – in January it stood at 1.8 percent. We still consider this very optimistic. Kuroda has also stated on several occasions that risks are skewed to the downside on the forecasts. The forecast for FY2018 from January at 1.4 percent is also very optimistic. The BoJ has been consistently overoptimistic on inflation for a number of years. Three years ago, it forecast inflation in FY2017 for the first time at 1.9 percent. Since then, the forecast has been revised down six times until the figure was final last Friday at 0.7 percent, still lower than the previous forecast. So far, it looks like wage increases have gone up somewhat with the spring wage negotiations but it is not likely to induce much of a pickup in inflation until inflation expectations pick up as well.

Currently we see the possibility of further easing from the BoJ as at least as likely as tightening. However, we do not see any policy changes within a one-year horizon and expect the BoJ to move steadily forward with the current policy framework. With the current pace at which the BoJ is picking up government bonds, policies are long lasting and we consider the potential gains from increasing the 10-year rate target to be largely outweighed by the risk of causing damage to the economic recovery.

USD/JPY range bound as the BoJ remains on autopilot

USD/JPY has gained substantially over the past month supported by general USD appreciation and not least rising yields in the US. While the break of 108 on 23 April most likely has widened the trading range to 105-110, it would, in our view, require a substantial dovish shift in the BoJ's rhetoric on Friday (not our call) for USD/JPY to settle above 110. Short-term technical indicators, such as RSI, suggest that USD/JPY looks increasingly overbought and we expect USD/JPY to continue to trade mostly sideways in the near term targeting 108 in 3M.

The sell-off in the US fixed income market is likely to remain the key driver for the cross and while the flattening of the US yield curve remains a challenge for Japanese investors, as the rising FX hedge cost erodes the return in US FI assets, we think that the combination of a neutral speculative JPY positioning and higher US 10Y yields could be a supporting factor for USD/JPY near term (as long as US interest rates volatility does not increase). Longer term, we expect USD/JPY to gradually recover supported by continued solid global growth outlook and Fed-BoJ divergence and we expect the cross to eventually return to the 110-115 range in 6-12M. We target the cross at 110 in 6M and 112 in 12M.

How is US Yield’s Breach of 3% Related to Recent Crude Oil Rally?

The two most astonishing features in the financial market over the past week were soaring US Treasury yields and crude oil prices. After making a fresh 4-year high last Friday, the 10-year yield extended gains and eventually broke above 3% this week. Meanwhile, both crude oil benchmarks rallied to new highs in more than 3 years last week. These are consistent with increasing US inflation expectations and heightening speculations of further Fed funds rate hike. The abovementioned phenomena are by no means coincidence. Rather, they are interrelated.

The first chart below shows that movements of oil price and 10-year US yield have been closely linked. The second chart suggests that the correlation between the two has fluctuated significantly over decades. However, the correlation has been positive, and increasingly so, since last year.

Demand/supply is the key driving force of oil price. While the recent strength in oil price has been driven by tighter supply as a result of OPEC/ non-OPEC commitment to reduce output and geopolitical tensions mainly in Syria and concerns over US possible sanctions against Iran, the demand side of the equation has indeed improved. The Paris-based International Energy Agency (IEA) revised higher its global demand growth forecast to 1.5M bpd for this year, up +0.2M bpd from the previous month’s projection. The agency attributed the revision to strong demand from China and India, which taken together take up almost half of the world’s demand growth. Meanwhile, both US Energy Department (EIA) and OPEC have also upgraded their demand growth forecasts.

As a critical factor of production in various sectors and industries, higher oil demand is an indication of stronger economic activities, hence reflection of the macroeconomic health. At the same time, energy, as a key component of inflation, takes up over 7% of the weight in US headline CPI. Rising oil price inevitably lifts inflation.

Treasury yields of longer maturities typically reflect investors’ expectations of future short-term interest rates. There are indeed the market expectations of future Fed funds rates, of which the outlook is determined by inflation and employment. With US unemployment rate steadied at record low level of 4.1% for six months in a row, the focus is on inflation. Here is where oil price and Treasury yields converge. Upbeat US data have sustained yields at elevated levels. Recent rally in oil prices have heightened inflation expectations which in turn intensified speculations for future Fed funds rate hikes. Such speculations have evidenced in the bump in 10-year yields.

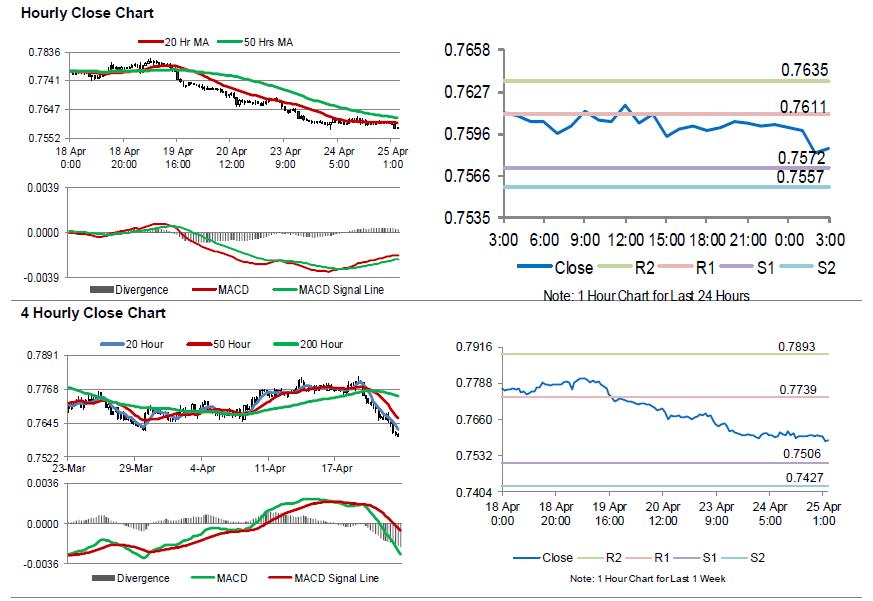

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7603.

LME Copper prices rose 0.92% or $64.0/MT to $6987.0/MT. Aluminium prices declined 9.38% or $230.0/MT to $2222.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7586, with the AUD trading 0.22% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7572, and a fall through could take it to the next support level of 0.7557. The pair is expected to find its first resistance at 0.7611, and a rise through could take it to the next resistance level of 0.7635.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

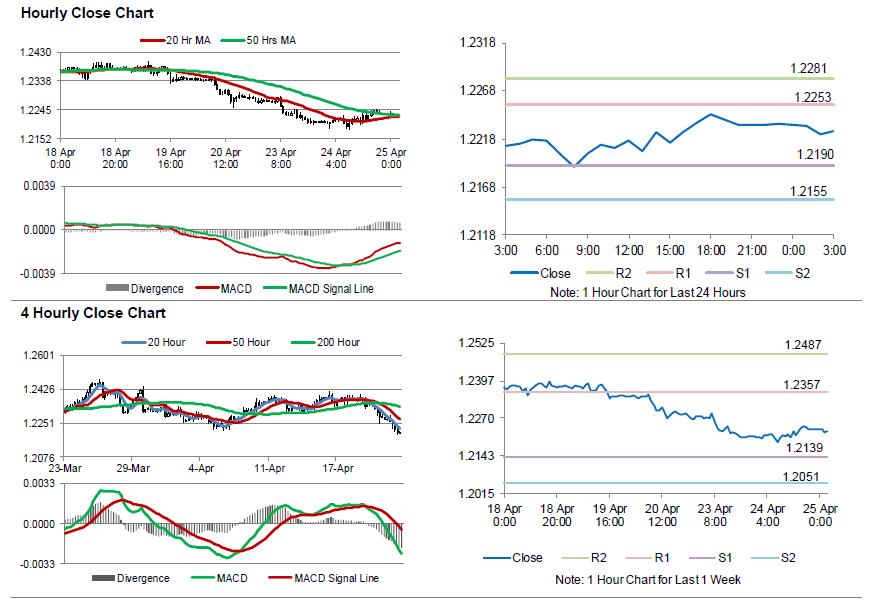

German Business Morale At A More Than 1-Year Low In April

For the 24 hours to 23:00 GMT, the EUR rose 0.21% against the USD and closed at 1.2234.

Macroeconomic data indicated that Germany’s Ifo business climate index declined more-than-anticipated to a level of 102.1 in April, hitting its lowest level since March 2017, thus suggesting that the upbeat mood amongst German businesses is waning. In the prior month, the index had registered a level of 103.3, while markets had expected for a fall to a level of 102.8. Moreover, the nation’s Ifo business expectations index eased to a level of 98.7 in April, compared to a revised level of 100.0 in the prior month. Market expectation was for the index to drop to a level of 99.5. Additionally, the nation’s Ifo current assessment index fell more-than-anticipated to a level of 105.7 in April, compared to market consensus for a drop to a level of 106.0. In the prior month, the index had recorded a revised level of 106.6.

In the US, data revealed that the CB consumer confidence index recorded an unexpected rise to a level of 128.7 in April, as Americans grew more optimistic about both current conditions and the near-term outlook. The index had registered a revised reading of 127.0 in the prior month, while investors had envisaged for a fall to a level of 126.0. Furthermore, the nation’s new home sales surprisingly advanced 4.0% on a monthly basis, to a level of 694.0K in March, surging to an 11-month high level, thus boosting optimism over the health of the nation’s housing sector. New home sales had recorded a revised reading of 667.0K in the previous month, while markets were anticipating new home sales to fall to a level of 630.0K.

In the Asian session, at GMT0300, the pair is trading at 1.2226, with the EUR trading 0.07% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2190, and a fall through could take it to the next support level of 1.2155. The pair is expected to find its first resistance at 1.2253, and a rise through could take it to the next resistance level of 1.2281.

With no macroeconomic releases in the Euro-zone today, investors would direct their attention to the US MBA mortgage applications data, slated to release later today.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.