Sample Category Title

The Dollar Is Not Quite Ready For Prime Time Just Yet

The USD, not quite ready for prime time just yet

The technology sector woes continue as Google parent Alphabet Inc shed more than 5 % on a massive drop in gross margins as Google continues to burn through cash in its attempt to challenge Amazon in “smart world” technology and cratering other FAANG stocks in its wake. Apple was also down 1.7 percent, falling for the fifth straight session of fears of slowing demand for iPhones.

While there has been a sense of post-earnings pessimism permeating the markets suggesting this is about as good as it is going to get. Comments from industrial bellwether Caterpillar during the company’s earnings conference call that Q1 results were the companies “high water mark” for the year, had investors rehashing doubts about the global growth narrative and fuelled further downward momentum on US equity market.

The sudden surge in US yields had already been weighing on equity sentiment, but when you factor in the skid in technology stocks and Caterpillar less than reassuring outlook, it makes for a very rough day on the trading floor.

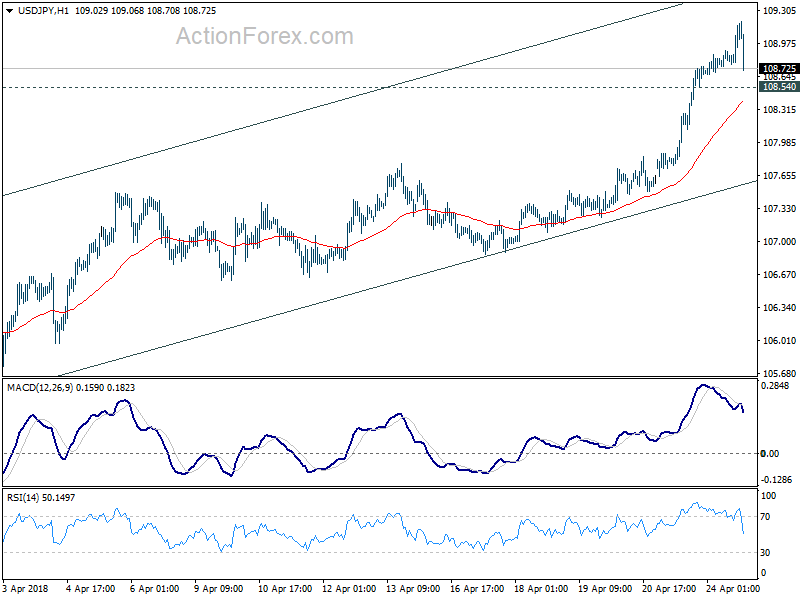

After testing the 100-day moving average on USDJPY and reverting lower. The US dollar appears not quite ready for prime time just yet. Nevertheless, beyond the technical troubles, the failure to take out the 3 % ten year UST level in convincing fashion has temporary quashed momentum.

Oil Markets

After Brent Crude printed its highest price since 2014, prices turned lower after the market was caught off guard and completely surprised by the comments from President Trump suggesting that the US and France could reach an agreement on the Iran nuclear deal. However, with an overall shrinking appetite for risk assets in the wake of the US equity sell-off, that too has offered little support for prices either. Nevertheless, when compounded by the API reporting a surprise build in crude, traders are a bit flustered by the shifting landscape.

Without a doubt, back peddling and unpredictability continue to frame the Donald Trump presidency; but we should expect Iran nuclear significance to remain front and centre.

In the meantime, traders will turn to the immediate task, Crude inventories and the US GDP, which could have a notable influence on energy prices.

The market remains extraordinarily long Oil, but there has been a lot of fresh money chasing it higher. The danger is being caught in a crowded trade scenario especially for those investors that are buying near the top, and we may have seen a bit of that influence in play overnight.

However, unlike trading on real fundamental supply and demand dynamics, geopolitical uncertainty takes volatility to an entirely new level due to headline risk.

Gold Prices

Gold prices have rebounded off the weekly lows as the US dollar upward momentum has temporarily ceded and the downward momentum building in equity markets has perked up some haven appeal. As s traders put geopolitical and trade risk in the rear-view mirror for the time being how the dollar flourishes and wilts will be the primary driver of near-term gold sentiment,. When the equity walls come crumbling down, gold offers the best support.

Currency Markets

The Euro

Is the Draghi painting the Euro into a corner or is the Euro painting Draghi into the corner. Such is the decision traders are facing heading into the ECB announcement. Certainly, Draghi cannot continue to talk the Euro down with the US Treasury forever vigilant on currency manipulation With everyone rushing to be short EURUSD into the statement, it opens the potential for a nasty whipsaw on the slightest of a hawkish lean.

Japanese Yen

Not a lot of dynamics to review. The USDJPY was tracking US yields, and on the failure to clear, the 3 % hurdle convincingly the USDJPY came off. The equity market purge did not help risk sentiment which asl also played on the improving JPY hand.

The Malaysian Ringgit

While ten year US yields failed to gain traction above 3 %, the US equity market sell-off will dent global risk sentiment making the ASEAN basket of currencies less attractive.

While the regional equity sentiment was showing signs of tentatively stabilising as market chatter has increased about a possible RRR cut in China, the overnight sell-off in both US industrials and tech sectors should weigh negatively in today’s session.

Nevertheless, investors continue to pair back MYR currency exposure as locals are turning increasingly risk-averse thinking the election results could be a lot tighter than initially predicted.

Also, with OIL prices coming of weekly highs, the Ringgit will find little support in that light.

DOW heading back to 23344.52 support after failing to stand above 55 day EMA

DOW closed sharply lower overnight by -424.56 pts or -1.74%, at 24023.13. The rebound from 23344.52 is confirmed to be complete at 24585.97, after failing to sustain above 55 day EMA. While the strength of the rebound was disappointing, the overall development is in line with our view. That is, price actions from 26616.71 high are developing into a medium term correction that's not completed yet

Further fall would be seen back to 23344.52 ahead, as long as 24585.97 holds. While there could be some support at that level, and eventual break is expected to 38.2% retracement of 15450.56 to 26616.71 at 23351.24. That was our original target. Judging from the descending triangle shape of the pattern from 23360.29, we're now slightly leaning to the case of deeper fall to 50% retracement at 21033.63 before completing the correction.

US 10 year yield yet to own 3% level

US 10 year yield edged higher to 3.003 overnight and breached 3% handle briefly. Then, it failed to sustain above 3% and closed at 2.983, up only 0.010. Comparing to Monday, it's slightly better as it closed above open of regular trading hours. But from hourly chart point of view, TNX is losing some momentum. Hourly MACD dipped below signal line while RSI also dipped from overbought region. That's what we usually see when a bullish move is taking, or about to take, a breath.

And bear in mind again that 3% is an important psychological level for many investors. And there is a key resistance of 3.036, 2013 high. These could both limit the strength of TNX for the very near term. And, judge from the reactions in forex markets too. Dollar only managed to extend gains against Yen and Swiss Franc yesterday when TNX breached 3%. We might see some sluggish trading today. But of course, ECB, UK and US GDP are still expected to trigger more volatility before the week ends.

Eco Data 4/25/18

[php_everywhere instance="1"]

Gold Rebounds After Sharp Losses, US Consumer Confidence Shines

Gold has posted gains in the Tuesday session, recovering some of the losses from Monday. In the North American session, the spot price for an ounce of gold is $1331.42, up 0.48% on the day. In the US, CB Consumer Confidence jumped to 128.7, beating the estimate of 126.0 points. US New Home Sales also looked sharp, jumping to 694 thousand and crushing the estimate of 625 thousand. This marked a 4-month high. However, manufacturing data was not as strong, as Richmond Manufacturing Index dropped 3 points, well off the estimate of a 16-point gain. This was the first contraction since October 2016.

Gold started the trading week with considerable losses, as higher yields for 10-year US treasury bills pushed the dollar broadly higher. The yields rose to 2.99% on Monday and punched above the symbolic 3% level on Tuesday. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The dollar has also benefitted from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria. Still, gold has reversed directions on Tuesday and gained back much of the Monday losses.

The trade battle between China and the US has become a geopolitical hotspot, dominating the headlines and shaken global markets. After a series of tit-for-tat tariffs between the economic giants, there has been widespread concern that these moves could lead to a trade war which would slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute. The markets will be hoping for a truce between the sides, as any further tariffs are sure to spook investors, which would likely boost gold, a traditional safe-haven in times of crisis.

US stocks in deep selling mode, USD/JPY follows DOW lower

US stocks suffer steep selloff as led by 3M, Caterpillar and Google. At the time of writing, DOW is trading down nearly -1.5%. The development, with rejection from 55 H EMA, suggests that rebound from 23344.52 has completed at 24858.97. Focus is now on 24000 handle. Firm break there could bring retest of 23344.52 low.

And, due to the selloff in stocks while 10 year yield is still struggling to stay above 3% handle, USD/JPY is having a relatively deep pull back. Focus is back on 108.54 minor support. Touching there will already mean temporary topping . That is, recent rise from 104.62 is taking a breath. And, some consolidations would be seen before another rise.

British Pound Halts Slide as UK Surprises With Budget Surplus

The British pound has steadied in the Tuesday session, after recording five consecutive losing sessions. In North American trade, GBP/USD is trading at 1.3975, up 0.25% on the day. On the release front, the UK posted a budget surplus of GBP 0.3 billion in March, beating the estimate of GBP -1.1 billion. CBI Industrial Order Expectations, which has dropped sharply in recent months, held steady at 4 points. This matched the forecast. Over in the US, CB Consumer Confidence jumped to 128.7, beating the estimate of 126.0 points. US New Home Sales also looked sharp, jumping to 694 thousand and crushing the estimate of 625 thousand. This marked a 4-month high. However, manufacturing data was not as strong, as Richmond Manufacturing Index dropped 3 points, well off the estimate of a 16-point gain. This was the first contraction since October 2016.

The US dollar started the week with strong gains, courtesy of higher yields for 10-year US treasury bills, which rose to 2.996% on Monday. The T-bills punched past the symbolic 3% threshold on Tuesday. Higher yields for US-T bills have made them more attractive than European or Japanese counterparts and pushed the US currency higher. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The dollar has also benefitted from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

Is the US-China trade war heading to a trade truce? The markets have been marked by volatility in recent weeks, in response to tariffs which the US and China have imposed on the other. US President Trump has threatened to slap tariffs on up to $150 billion on Chinese goods, and China has promised to respond with heavy tariffs on US imports. The escalating crisis has raised fears that a trade war between the two economic giants could slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute.

As 10-Year US Yields Break above 3%, is the Dollar Turning a Corner?

The US dollar broke above the 109-yen level for the first time since early February this week, taking the dollar bears, who have been betting on more losses for the beleaguered greenback, by surprise. The sudden shift to a more bullish sentiment, in the short term at least, comes amid a surge in US Treasury yields, which has led to a widening in the spread of US sovereign bond yields with its peers. But as the dollar climbs to three-month highs against a basket of currencies, is this the start of a trend reversal or simply short covering?

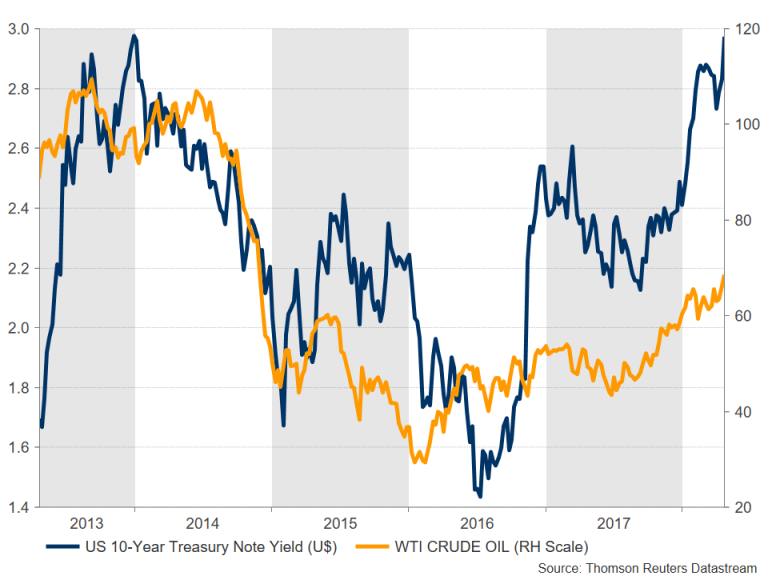

The main trigger for the past week’s spike in the yield of 10-year Treasury notes was the sharp rally in oil prices which took the benchmark WTI and Brent crude prices to more than three-year highs. Higher oil prices are seen as inflationary as they tend to increase costs for both consumers and businesses. The resultant boost to future inflation expectations is positive for rate hike expectations.

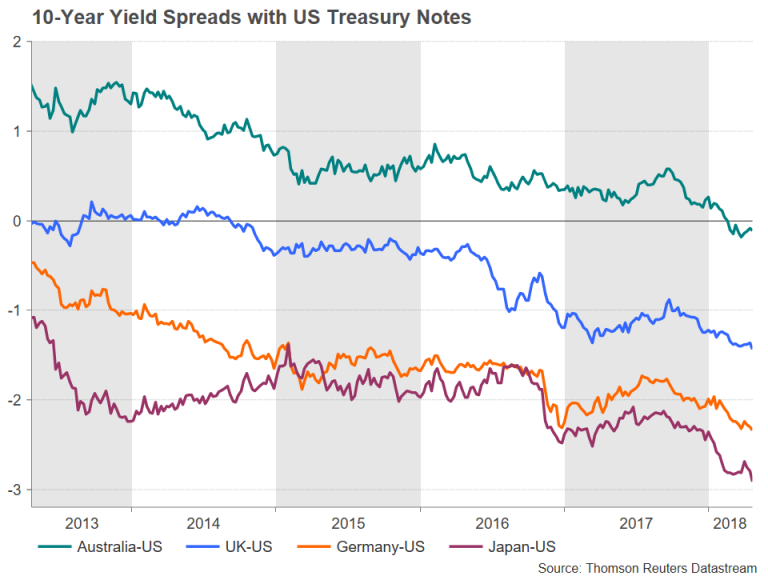

Ten-year Treasury yields crossed above 3% on Tuesday for the first time since January 2014; short-term yields have also been setting new highs. The last time 10-year yields attempted to break above the psychological 3% level back in February, it sparked a market turmoil and a global sell-off in equities. However, markets appear readier this time round in contemplating 10-year yields above 3%. More significantly though, the positive relationship between the dollar and treasury yields was re-established during the latest jump in bond yields.

That relationship became broken in 2017 when US yields saw modest declines before starting to steadily climb again in September, but the dollar stuck to its downtrend for the duration of the year. If this indeed is a sign that investors are moving their focus back to yield spreads, the dollar could be in line for more gains.

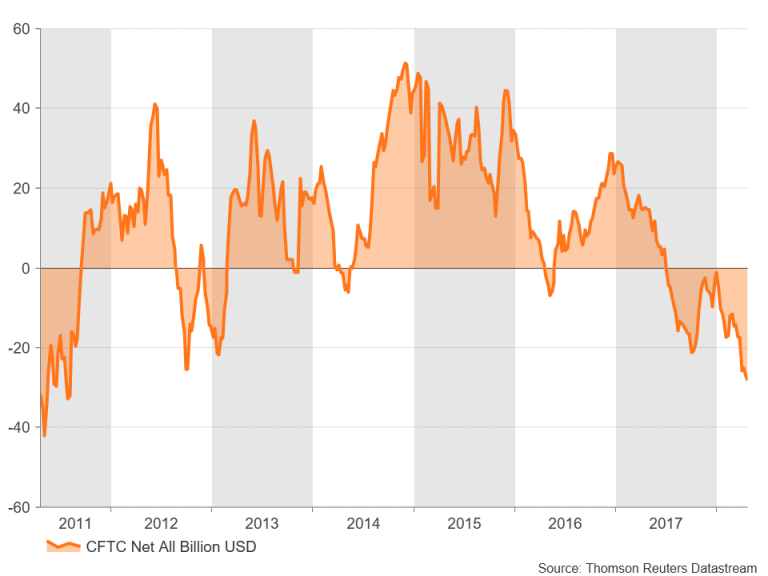

However, it may be premature to interpret the dollar’s strong gains as a trend reversal as the latest data from the Commodity Futures Trading Commission shows traders raised their bearish bets on the US currency, increasing their net short dollar positions to the highest since August 2011 at the end of last week. This could be an indication that the current upturn is merely a technical rebound driven by short covering or by unwinding of trades by dollar bears who were caught off-guard by the recent dollar-positive developments. The gains could also be exasperated by a weaker Japanese yen as safe-haven demand recedes on fading geopolitical risks.

This is evident when looking at the greenback’s broader measure, the dollar index, which has been trading sideways since mid-January and has yet to show a convincing sign of breaking out of its range. The index already appears to have met resistance around the 91 level – the upper bound of the three-month old range. Dollar/yen also looks to have found a barrier at a key level. The pair’s ascent to two-month highs is slowing around the psychological 109 handle, which happens to be the 50% Fibonacci retracement of the down move from 113.38 to 104.55. Should these resistance levels hold, the dollar could retreat lower again. A move below key support areas at 106.50 yen and 89.75 would see the current positive momentum being erased.

However, if the dollar was successful in breaking above these critical levels, it could help generate momentum for a more sustained uptrend, bringing into focus the 110-yen and 91.80 levels. A more bullish dollar is certainly endorsed by US economic fundamentals.

While recent data out of the US have not been spectacular, neither has it been poor, suggesting the American economy continues to grow at a solid and steady pace. In comparison, Eurozone indicators have been consistently falling short of expectations in the first four months of 2018, and Japanese data haven’t fared much better either.

The sluggish start to the year has led many investors to backtrack on earlier projections that the European Central Bank and the Bank of Japan would make an early exit from their respective stimulus programs. This has once again left the Federal Reserve as the only major central bank with a confident tightening path and FOMC members are now openly discussing the possibility of four rate hikes in 2018 instead of three. Futures markets have also started to price in a steeper rate path, with the odds of a fourth-rate hike currently approaching 50%.

Should the 10-year yield continue to rise above 3%, it could set the stage for a new bullish phase for the dollar, marking the end of a 15-month downtrend. However, even in the event that sentiment for the greenback was to turn more convincingly bullish, a bigger question that would arise is how far would the rally go given the hanging risks from President Trump’s protectionist policies and the country’s deteriorating fiscal outlook.

Consumer Confidence Gets a Boost in April

Consumer confidence rose 1.7 points to 128.7 in April, surprising consensus which anticipated a decline. The index improved in April for both the present situation and expectations.

Consumer Confidence Rises to Second Highest of the Cycle

The Conference Board's measure of consumer confidence rose to 128.7 in April from 127.0 in March. April's reading is the second highest of the cycle after February's print of 130.0. The move in April was unexpected as consensus had anticipated another decline on continued uncertainty surrounding trade policy. Consumers appear to have already shaken that concern, which did weigh on confidence in March. April was a stronger month for consumers' assessment of the present situation and expectations. Much of the improvement resulted from fewer unfavorable responses regarding the labor market and business conditions.

The index measuring consumers' assessment of the present situation rose to 159.6 in April from 158.1 in March. April's present situation index is also at its second-highest level of the cycle, having reached its height in February. The uptick in April was because the share of respondents with a neutral assessment of business conditions and current job availability both rose. Fewer respondents appraised current business situations as 'bad' and 'good'. Similarly, the share viewing jobs as 'plentiful' declined, and the share saying jobs are 'hard to get' declined. The greatest share of respondents appraised the labor market as 'jobs not so plentiful', which is the balanced view.

Consumers' expectations index improved to 108.1 in April from 106.2 in March. There was an increase in the share of consumers expecting better business conditions in six months and a decrease in the share expecting conditions to worsen. That movement contrasts March, when uncertainty stemming from trade rhetoric and volatility in the stock market likely dampened expectations for some consumers. The share expecting better conditions has almost recovered to February's level. Consumers' expectations for job availability in six months were also more favorable in February, as a larger share answered they expect more jobs. The share expecting fewer jobs in six months held steady at 12.5 percent. Income expectations were also more favorable in April on net. That improvement was also due to a more balanced assessment this month, as the share expecting income to increase in six months declined, but the share expecting it to decrease also declined.

The takeaway from the April print is that consumers appear to have already moved on from the increase in uncertainty we saw in March. Their high level of confidence bodes well for a rebound in consumer spending in coming months. The prospect of rising interest rates is not lost on consumers, as the share expecting higher rates next year rose to 72.2 percent in April. The return of volatility to the stock markets has brought the share expecting higher stock prices next year from 51.0 percent in January to 32.7 percent in April, which is in line with the share expecting no change and those expecting a decrease. Some consumers appear to be planning major purchases before interest rates rise. The share planning to purchase a home in the next six months rose to its cycle high in April. The share planning to buy an automobile or make a major appliance purchase also rose noticeably.

Mexican EM Guajardo on NAFTA: We will not accept any type of restrictions in aluminum or steel

As Mexican Economy Minister Ildefonso Guajardo is meeting Canadian and US counterparts to continue NAFTA renegotiation, he emphasized that a deal "depends on the commitment and flexibilities around the table". And he expressed firmly that "Mexico has been very clear: we will not accept any type of restrictions in aluminum or steel".

Earlier today, Moises Kalach expressed his optimism that "in the coming 10 days we can really have a new agreement in principle." Kalach is head of the international negotiating arm of the CCE business lobby, which represents the Mexican private sector at the NAFTA talks.