Sample Category Title

Euro Holds Weak, US Consumer Confidence In Focus

Here are the latest developments in global markets:

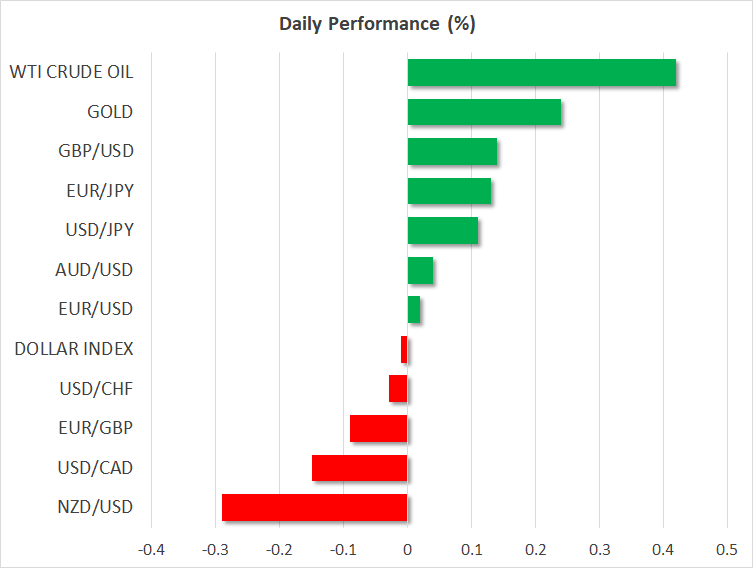

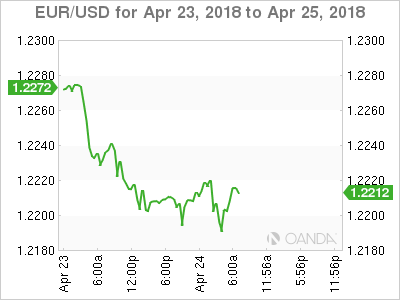

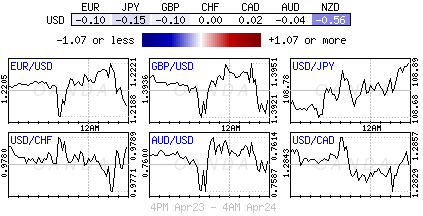

FOREX: The dollar index was consolidating around 91.00 in the early European afternoon, its highest level reached since mid of January despite 10-year US Treasury yields retreating further below the 3.0%. Easing geopolitical and trade tensions were also supportive to the greenback as safe-havens continued to lose attractiveness, with dollar/yen crawling slightly up to a fresh 2 ½-month high of 108.90. On the other hand, euro/dollar was struggling at two-month lows, last seen at 1.2200 (-0.03%), amid expectations that ECB policymakers could hold a cautious stance at the end of their two-day policy meeting on Thursday given recent disappointing PMI and inflation readings. The German Ifo business climate index missed expectations today as well, but the euro did not react much to the figures. Pound/dollar was moving sideways around 1.3945 (+0.01%), unable to deviate above 1½ -month troughs as the Brexit legislation has so far received 3 defeats in the House of Lords, adding further pressure to the UK Prime Minister who wants a clear exit from the EU ahead of a final Brexit bill consideration in May by Parliament members. In antipodean currencies, aussie/dollar was flat at 0.7606 despite CPI figures falling short of expectations earlier in the day, while kiwi/dollar remained the worst performer among major currencies, changing hands at 0.7121 (-0.35%). Dollar/loonie was slightly weaker at 1.2838 (-0.10%) but near three-week highs reached on Monday after the Bank of Canada’s governor signaled no rush to raise interest rates even if inflation is ticking higher.

STOCKS: European stocks were moving upwards at 0800 GMT, strengthening on the back of a weaker euro, with the pan-European STOXX 600 rising by 0.16% above the 10-week highs reached yesterday. The blue-chip Euro STOXX 50 was up by 0.35% driven by gains in the technology sector. The German DAX 30 increased by 0.30%, supported by news that Germany’s SAP – Europe’s largest tech company – was gaining ground against competitors such as Oracle. Britain’s FTSE 100 climbed by 0.30%, the French CAC 40 inched up by 0.09%, while the Spanish IBEX 35 edged down by 0.04%. Indices tracking US stock futures were flashing green, signaling to a positive open.

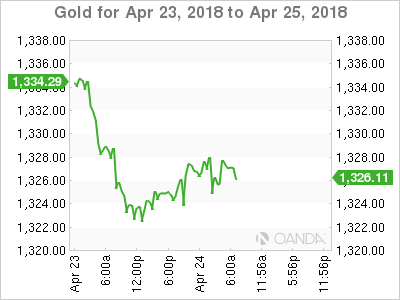

COMMODITIES: Oil prices were on the rise on Tuesday, underpinned by OPEC-led supply cuts and increasing tensions between the US and Iran which could force the US to impose additional sanctions on Iran. WTI crude was up at $69.06 (+0.61%) and Brent was last seen at 74.99 (+0.37%), its highest since November 2014. In precious metals, gold was gaining ground, rising to $1,327.10 (+0.24%) per ounce.

Day Ahead: US consumer confidence & new home sales pending

Tuesday’s calendar is a light one, with the focus possibly remaining on the ECB interest rate decision on Thursday and the GDP flash estimates out of the US and the UK on Friday. Companies releasing earnings will also be attracting interest.

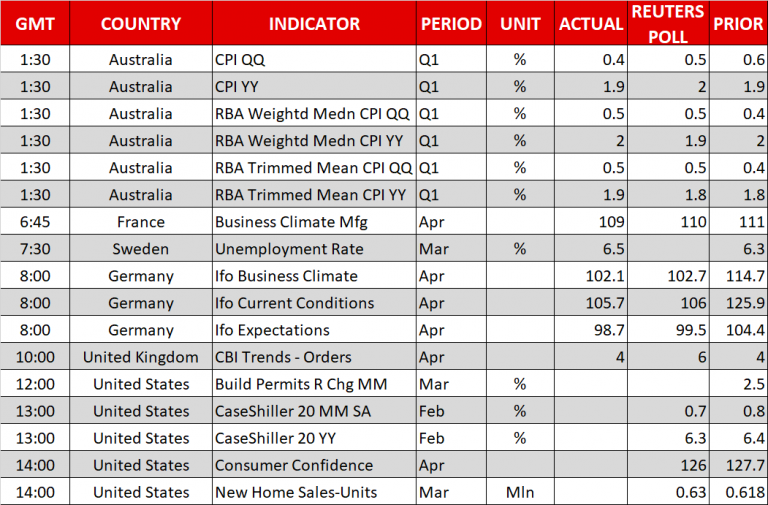

Out of the US, at 1300 GMT, the Case-Shiller indices gauging house prices during the month of February will be made public, while data on consumer confidence for the month of April will be available at 1400 GMT. On a monthly basis, the consumer confidence index is expected to fall to 126.0 versus 127.7 in the prior month. Also, at the same time, new home sales for the month of March are anticipated to edge up by 1.9% m/m following a decline of 0.6% in the preceding month.

In energy markets, investors will be waiting for the API weekly report to indicate the change in US crude oil stocks.

Turning to today’s public appearances, at 1800 GMT Federal Reserve Bank of Philadelphia President Patrick Harker will be participating in a conference, while Bank of England Governor Mark Carney will be giving a speech at the same time.

Dollar Bulls Look For Support Signals

Tuesday April 24: Five things the markets are talking about

U.S dollar bulls seem to have finally found some much needed support from interest rates as U.S bond yields climb toward levels unseen in nearly four-years.

The 'mighty' dollar recorded a three-month high yesterday as 10-year note traded atop of the psychological +3% at +2.998% – a key level that tech analysts believe keeps the door ajar for much higher yields.

Overnight, capital markets have hit the bond pause selloff button that took sovereign rates to key threshold levels. Global equities have traded mixed as earning’s season picks up. The dollar is little changed; sitting atop of New Year high’s while commodity prices ease.

On tap: For today, the market is expecting some more positive data – U.S consumer confidence and new home sales (10:00 am EDT).

1. Stocks mixed results

In Japan, equities hit a two-month closing high overnight with financials leading the gains after U.S yields spiked to four-year highs and, as investors remained optimistic about upcoming earnings. The Nikkei advanced +0.86%, while the broader Topix ended +1.08% higher.

Down-under, Aussie shares rallied on Tuesday, driven by banks as benign inflation data backed expectations interest rates will remain accommodative for some time. However, gains are being capped by losses in materials on an extended slide in aluminum prices. The S&P/ASX 200 index ended up +0.6%. In S. Korea, the Kospi declined -0.4%, its third consecutive decline.

In Hong Kong, shares ended lower, led by tech stocks over trade-spat worries. Both the Hang Seng index and the China Enterprises Index closed -0.5% lower.

In China, stocks post best gains in two-months as Beijing vows to hit economic targets. The blue-chip CSI300 index and the Shanghai Composite Index climbed +2%.

In Europe, regional indices are trading mostly higher across the board following a plethora os earnings reports – shares of SAP are helping the DAX.

U.S stocks are set to open in the black (+0.4%).

Indices: Stoxx600 +0.2% at 383.8, FTSE +0.4% at 7427, DAX +0.4% at 12621, CAC-40 flat at 5440, IBEX-35 -0.1% at 9914, FTSE MIB -0.1% at 23954, SMI +0.1% at 8814, S&P 500 Futures +0.4%

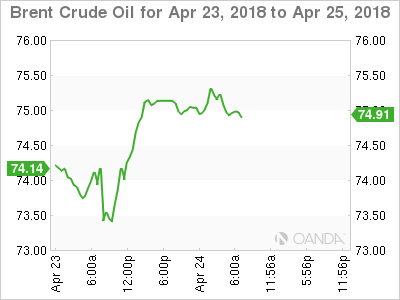

2. Brent hits highest in four-years as supplies tightens, gold up

Crude oil prices have rallied for a sixth day overnight to hit its highest price in four-years, supported by expectations that supplies will tighten just as demand reaches record levels.

Brent crude futures are at +$75.07 a barrel, up +36c, or +0.5% from Monday’s close.

Note: Brent’s six-day rising streak is the longest such string of gains since December, with prices up more than +20% from 2018-lows recorded in February.

U.S West Texas Intermediate (WTI) crude futures are at +$69.17 a barrel, up +53c, or +0.8%.

Markets have been lifted by supply cuts led by the OPEC and the possibility of renewed U.S sanctions against Iran.

Note: The U.S has until May 12 to decide whether it will leave the Iran nuclear deal and re-impose sanctions against OPEC’s third-largest producer.

Market prices are being capped by U.S production – higher crude prices are bringing more U.S producers back “on line.”

Gold prices have edged higher ahead of the U.S open, but the safe-haven demand is beginning to fade. After falling for three previous sessions, spot gold has edged up +0.2% to +$1,327.20 per ounce. That’s not far from Monday’s low of +$1,321.81, its weakest price in three-weeks. U.S gold futures have rallied +0.4% to +$1,329.20 per ounce.

3. Yields remain near four-year highs

The U.S 10-year Treasury yield remains within touching distance of the key psychological +3% handle. The yield on U.S 10’s has eased -1 bps to +2.96%.

Elsewhere, sovereign yields have eased a tad ahead of the U.S open on profit taking.

Nevertheless, higher U.S yields are supporting many regional yields. Germany’s 10-year Bund yield has eased -2 bps to +0.62%, the largest tumble in a week, while the U.K’s 10-year Gilt yield has declined -3 bps to +1.539%.

Note: The last time yields traded atop of current yield levels it hurt investor risk appetite and sent equities tumbling. It also came shortly before crude oil prices plummeted -75%.

The European Central Bank (ECB) guidance later this week (April 26), about the future of its stimulus programme, is the next thing that may cause some yield movement.

Last Friday, ECB’s Draghi said he was confident that the inflation outlook has picked up, but uncertainties “warrant patience, persistence and prudence.”

4. Dollar steadies, looking for clues

Recent commodity price have sparked fears of a stronger rise in inflation and, consequently, a faster rise in interest rates and it’s these higher yields that is supporting the 'big' dollar.

EUR/USD (€1.2202) is holding, trading atop of key support levels ahead of Thursday’s ECB meeting. Euro policy makers have to digest recent economic downside surprises in the various recent economic releases. German Ifo survey (see below) continues to show the recent spat of disappointing numbers.

Elsewhere, USD/JPY is holding below the ¥109 level at ¥108.81, while GBP/USD is at £1.3942 ahead of the U.S open.

5. German Ifo business climate falls

Euro data this morning showed that German business sentiment slipped further this month, as manufacturers cut back their business outlook.

The revamped German Ifo business climate index, which now also includes the service sector, fell to 102.1 points from 103.3 points in March, below market expectations of 102.6 points.

Note: It marks the fifth consecutive decline in the indicator.

The survey follows a string of soft economic data, pointing to a slowdown in economic activity in Q1.

Yesterday’s German PMI data surprised on the upside, as the downtrend in the PMI’s came to a halt this month.

DAX Higher, Markets Eye ECB Meeting

The DAX index has posted gains in the Tuesday session. Currently, the DAX is trading at 112,614 points, up 0.33% on the day. On the release front, German Ifo Business Climate dropped sharply to 102.1, missing the estimate of 102.7 points.

Is the German locomotive in trouble? German business confidence took a hit in April, as Ifo Business Climate fell to 102.1 points, down from 114.7 points a month earlier. This marks the lowest level since November 2012. German key indicators have softened recently, pointing to a slowdown in economic conditions in the first quarter. We’ll get a look at the mood of consumers, with the release of German GfK Consumer Climate on Thursday.

The US dollar started the week with broad gains and has pushed the euro down to 8-week lows. The catalyst for the greenback rally was higher yields for 10-year US treasury bills, which rose to 2.996% on Monday. Higher yields for US T-bills have made them more attractive than European or Japanese counterparts. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The dollar has also benefitted from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

The markets are keeping a close eye on the ECB, which holds a policy meeting on Thursday. Despite stronger economic conditions in the eurozone, the ECB has been in cautious mode. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The markets are not expecting any change in forward guidance, and concerns over recent trade disputes could mean a dovish statement from ECB President Mario Draghi. Traders shouldn’t expect any dramatic moves this week, as the bank will likely continue to preach patience and prudence.

Euro Under Pressure As US Treasury Yields Spark Dollar

EUR/USD remains under pressure and has posted losses for three straight sessions. The pair is steady in the Tuesday session and is trading at 1.2204, down 0.04% on the day. On the release front, German Ifo Business Climate dropped sharply to 102.1, missing the estimate of 102.7 points. In the US, today’s key event is CB Consumer Confidence, which is expected to dip to 126.0 points. As well, the US releases housing and manufacturing reports.

The US dollar started the week with broad gains and has pushed the euro down to 8-week lows. The catalyst for the greenback rally was higher yields for 10-year US treasury bills, which rose to 2.996% on Monday. Higher yields for US-T bills have made them more attractive than European or Japanese counterparts. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The dollar has also benefitted from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

The markets are keeping a close eye on the ECB, which holds a policy meeting on Thursday. Despite stronger economic conditions in the eurozone, the ECB has been in cautious mode. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The markets are not expecting any change in forward guidance, and concerns over recent trade disputes could mean a dovish statement from ECB President Mario Draghi. Traders shouldn’t expect any dramatic moves next week, as the bank will likely continue to preach patience and prudence.

German IFO Survey Misses Expectations

Notes/Observations

- Continues European economic data shows that regional economy slowing down; gives ECB reasons to hold off on any QE guidance until June

- China stocks react to reports that China had signaled more RRR cuts are possible in the near future to replace maturing MLF (adds to last week's RRR cut which becomes effective on Apr 25th)

Asia:

- Australia remains below RBA’s 2-3% target (Q1 CPI Q/Q: 0.4% v 0.5%e; Y/Y: 1.9% v 2.0%e; Trimmed Mean Q/Q: 0.5% v 0.5%e; Y/Y: 1.9% v 1.8%e). Core CPI has now remained below the target range for 9 straight quarters (record streak)

- China said to have additional room to cut RRR and repay maturing MLF; govt likely to ease liquidity tension in week

Europe:

- UK House of Lords votes 316-245 to add an EU rights charter to UK law, another defeat for PM May

- EU Chief Brexit negotiator Barnier: seeing good progress on orderly UK withdrawal from EU. UK must present a clear plan for its future relationship with the EU if Brexit talks are to move on

Americas:

- Bank of Canada (BOC) Gov Poloz: protectionist trade policies remained the biggest risk to the economic outlook. BoC will stay cautious on rate policy

Economic Data:

- (CH) Swiss Mar Trade Balance (CHF): 1.8B v 3.1B prior; Real Exports M/M: 0.6 v 2.0% prior; Real Imports M/M: +3.9 v -8.8% prior; Watch Exports: 4.8% v 12.9% prior

- (FI) Finland Mar PPI M/M: 0.7% v 0.7% prior; Y/Y: 3.1% v 2.4% prior

- (FI) Finland Mar Unemployment Rate: 8.8% v 8.6% prior

- (DK) Denmark Mar Retail Sales M/M: +0.4% v -0.1% prior; Y/Y: 1.8% v 3.0% prior

- (FR) France Apr Business Confidence: 108 v 108e; Manufacturing Confidence: 109 v 110e; Production Outlook Indicator: 24 v 25e; Own- Company Production Outlook: 15 v 10e

- (FR) France Apr Business Survey Overall Demand: 17 v 22 prior

- (CZ) Czech Apr Business Confidence: 17.2 v 16.5 prior; Consumer Confidence: 10.0 v 10.3 prior, Composite (Consumer & Business) Confidence: 15.8 v 15.3 prior

- (ZA) South Africa Feb Leading Indicator: 108.3 v 106.8 prior

- (SE) Sweden Mar Unemployment Rate: 6.5% v 6.6%e; Unemployment Rate (Seasonally Adj): 6.2% v 6.1%e

- (DE) Germany Apr IFO Business Climate: 102.1 v 102.8e; Current Assessment: 105.7 v 106.0e, Expectations Survey: 98.7 v 99.5e

- (IT) Italy Apr Consumer Confidence: 117.1 v 116.9e; Manufacturing Confidence: 107.7 v 108.8e, Economic Sentiment: 105.1 v 106.0 prior

- (UK) Mar Public Finances (PSNCR): £0.5B v £19.1B prior, Public Sector Net Borrowing: -£0.3B v +£1.3Be, Central Government NCR: +£19.9B v -£1.9B prior, PSNB ex Banking Groups: £1.3B v £3.0Be

Fixed Income Issuance:

- (EU) EFSF opened its book to sell €1.0B in 1.375% May 2047 bonds; guidance seen +4bps to mid-swaps

- (ID) Indonesia sold total IDR6.15T vs. IDR target in 3-month, 9-month Bills, 5-year, 10-year and 20-year Bonds

- (CH) Switzerland sold CHF315.0M in 3-month Bills; Yield: -0.853% v -0.853% prior

- (ZA) South Africa sold total ZAR2.4B vs. ZAR2.4B indicated in 2023, 2037 and 2044 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.2% at 383.8, FTSE +0.4% at 7427, DAX +0.4% at 12621, CAC-40 flat at 5440, IBEX-35 -0.1% at 9914, FTSE MIB -0.1% at 23954, SMI +0.1% at 8814, S&P 500 Futures +0.4%]

- Market Focal Points/Key Themes: European Indices trade mostly higher across the board following a raft of earnings out of Europe, with strength in the Dax helped by shares of SAP which reported results and raised guidance. In France PSA Group reported a slight beat in Revs, Michelin reported in line results, with shares slightly lower. AMS following a miss of estimates trades over 10% lower in Switzerland. Randstad and Akzo Nobel fall sharply in the Netherlands after missing on earnings, while Volvo is another notable faller despite a beat on the top and bottom line. In Spain Santander did report a small beat however shares trade lower. In the M&A space Shire trades higher after reportedly nearing an agreement to be acquired by Takeda. Looking ahead notable earners include Verizon, Caterpillar, Eli Lilly and 3M.

Movers

- Materials [Anglo American [AAL.UK] -1.3% (Earnings), Akzo Nobel [AKZA.NL] -3.9% (Earnings) ]

- Industrials [ Michelin [ML.FR] -1.3% (Earnings), Volvo [VOVLA.SE] -3.6% (Earnings), PSA Group [UG.FR] -1.6% (Earnings)]

- Financial [Santander [SAN.ES] -1.8% (Earnings), Randstad [RAND.NL] -4.9% (Earnings), St James Place [STJ.UK] -1.3% (Earnings)]

- Healthcare[Sartorius [SRT.DE] -5.7% (Earnings), Shire [SHP.UK] +4% (Reportedly nearing agreement with Takeda) ]

- Telecoms [Telenor [TEL.NO] -2.6% (Earnings)]

- Technology [SAP [SAP.DE] +3.2% (Earnings), AMS [AMS.CH] -11.3% (Earnings) ]

Speakers

- ECB Bank Lending Survey: Loan growth support by easing credit standards and increasing demand

- EU officials said to believe that the preferred solution on the Irish border may not prevent a hard Brexit. Backstop in its current form could potentially pave the way for a future trade deal that could give the UK many benefits of the single market without membership

- EU's Dombrovskis: Financial companies must continue to prepare for all possible Brexit scenarios

- German IFO Economists noted that id did not view the softer April survey as a change in trend for the economy. Forecasted Q1 GDP at 0.4% vs. 0.6% q/q - UK DMO raised FY18/19 Gilt issuance by £3.1B to £106.0B

- Poland Dep Fin Min Skiba: 2018 GDP growth could exceed 3.8%

- Philippines Central Bank (BSP) Gov Espenilla: Domestic economy is robust and could handle a rate hike if necessary

- Hong Kong Monetary Authority (HKMA): Peg system is stable

- Iran President Rouhani said to warn President Trump to remain in the nuclear deal or face 'severe consequences'

Currencies

- USD continued to hold onto recent gains aide by the recent steepening of the US yield curve

- EUR/USD holding below the 1.22 level ahead of Thursday’s ECB meeting. Dealers noted that ECB would have to digest recent economic downside surprises in various economic releases. German IFO survey continued to show the recent spat of disappoint numbers continued as the German/regional economic shifted into a lower gear.

- Other USD-related pairs were little change with USD/JPY holding below the 109 level and GBP/USD at 1.3930 just ahead of the NY morning.

Fixed Income

- Bund Futures trade 5 ticks higher at 157.88 as European markets eye Thursday’s ECB meeting. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 121.30 higher by 14 ticks, tentatively finding support from the 121 handle. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Tuesday’s liquidity report showed Wednesday's excess liquidity fell to €1.846T from €1.848T prior. Use of the marginal lending facility fell from €92M to €85M.

- Corporate issuance saw 6 issuers raise $8B in the primary market last week

Looking Ahead

- NAFTA talks resume

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender

- 05:30 (DE) Germany to sell €4.0B in 0% Mar 2020 Schatz

- 05:30 (UK) DMO to sell £750M of 0.125% Inflation -Linked 2048 Gilts (UKTei)

- 05:30 (ZA) South Africa to sell combined ZAR2.4B in 2023, 2037 and 2044 bonds

- 06:00 (UK) Apr CBI Industrial Trends Total Orders: 4e v 4 prior, Selling Prices: No est v 18 prior, Business Optimism: No est v 13 prior

- 06:00 (FI) Finland to sell €1.0B in 0.5% Sept 2027 RFGB bonds

- 06:45 (US) Daily Libor Fixing - 07:00 (RU) Russia announces upcoming OFZ bond auction (held on Wed)

- 07:00 (BR) Brazil Apr FGV Consumer Confidence: No est v 92 prior

- 07:30 (TR) Turkey Apr Capacity Utilization: No est v 77.8% prior

- 07:30 (TR) Turkey Apr Real Sector Confidence (seasonally adj): No est v 109.5 prior; Real Sector Confidence (unadj): No est v 111.9 prior

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central Bank (MNB) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

- 08:00 (PL) Poland Mar M3 Money Supply M/M: 0.3%e v 0.4% prior; Y/Y: 5.3%e v 4.9% prior

- 08:00 (CL) Chile Mar PPI M/M: No est v -0.8% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:55 (US) Weekly Redbook Sales

- 09:00 (US) Feb FHFA House Price Index M/M: 0.6%e v 0.8% prior

- 09:00 (US) Feb S&P/ Case-Shiller 20-City M/M: 0.68%e v 0.75% prior; Y/Y: 6.35%e v 6.40% prior; House Price Index (HPI): No est v 205.10 prior

- 09:00 (US) Feb S&P Case-Shiller (overall) HPI Y/Y: No est v 6.18% prior, Overall HPI Index: No est v 196.31 prior

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:00 (BE) Belgium Apr Business Confidence: -0.5e v +0.1 prior

- 09:00 (HU) Hungary Central Bank (MNB) Gov Matolcsy policy statement

- 10:00 (US) Apr Consumer Confidence: 126.0e v 127.7 prior

- 10:00 (US) Mar New Home Sales: 630Ke v 618K prior

- 10:00 (US) Apr Richmond Fed Manufacturing Index: 16e v 15 prior

- 11:30 (US) Treasury to sell 4-Week and 52-Week Bills

- 13:00 (US) Treasury to sell $32B in 2-Year Notes

- 15:00 (AR) Argentina Feb Economic Activity Index (Monthly GDP) M/M: No est v 0.6% prior; Y/Y: 4.3%e v 4.1% prior

- 15:00 (AR) Argentina Mar Trade Balance: -$1.1Be v -$0.9B prior

- 16:30 (US) Weekly API Oil Inventories

- (AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 27.25%

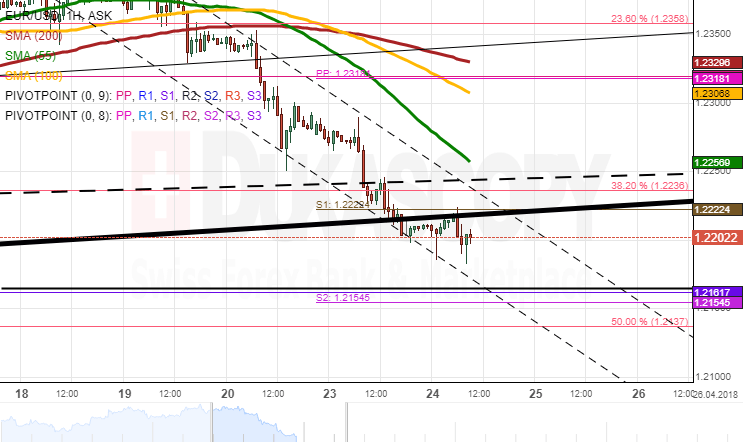

EUR/USD Analysis: Tests 1.22

The Euro remained under the bearish pressure on Monday. Downside risks accelerated early in the session when sluggish Euro zone's Manufacturing PMI dragged the pair down to the dashed trend-line and the 38.20% Fibonacci retracement at 1.2235. The pair subsequently edged even lower just to end the day below the weekly S1.

Technical indicators suggest that this psychological 1.22 level is likely to surrender today. However, the comparably strong support formed by the weekly S2 and the monthly S1 that should hold strong is located nearby at 1.2170.

On the other hand, the 1.22 could stop the pair's three-day decline, especially when the 100-day SMA is likewise supporting this level. In case of an upward movement, the Euro should target the senior channel and the 55-hour SMA at 1.2270.

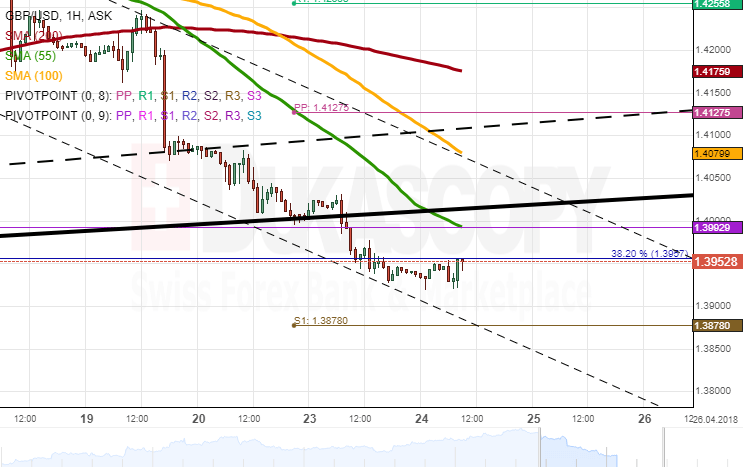

GBP/USD Analysis: Breaches Senior Channel

Despite flashing bullish signals on Monday morning, the Sterling managed to maintain its downward-sloping movement throughout the day. As a result, it breached the senior channel, the monthly PP and the 38.20% Fibonacci retracement along the way. The pair had remained near the latter by the time of this analysis.

It is expected that the 1.39 mark is not surpassed today, as bulls might want to re-gain some of their lost positions after the massive 3.19% plunge that started last Tuesday. In addition, technical indicators are likewise starting to converge.

The Sterling could find strong resistance at 1.4050 where the 55-hour SMA and the senior channel are located. This level should eventually be breached just to push the pair towards the 100-hour SMA and the weekly PP at 1.4150.

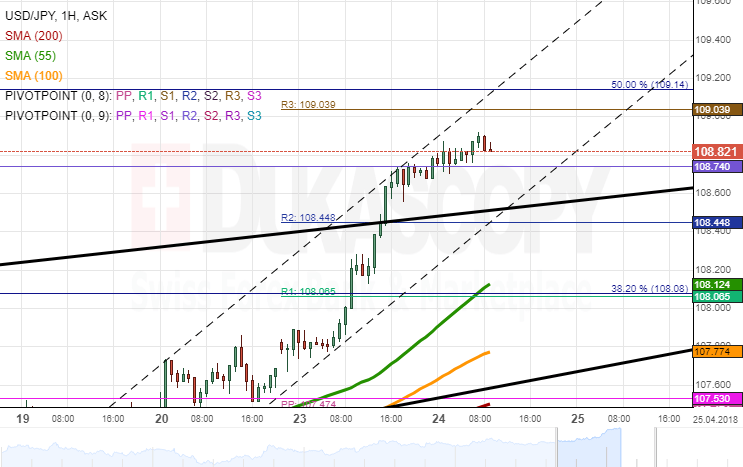

USD/JPY Analysis: Allays After Surge

The US Dollar accelerated significantly against the Japanese Yen on Monday, thus closing the session with a 93-pip gain. This strong upside momentum prevailed mid-day as a result of which several significant resistance areas were breached, including the weekly R2 and a trend-line at 108.45.

The pair might still edge higher during the early hours of the European session towards the weekly R3 and the 50.0% Fibonacci retracement near 109.10. However, this strong up-move should not be sustainable for long, thus allowing bears to lead the second part of the session.

A significant support cluster is formed by the 55-hour SMA, the weekly R1 and the 38.20% Fibonacci retracement at 108.10. The 100– and 200-hour SMAs are likewise located nearby.

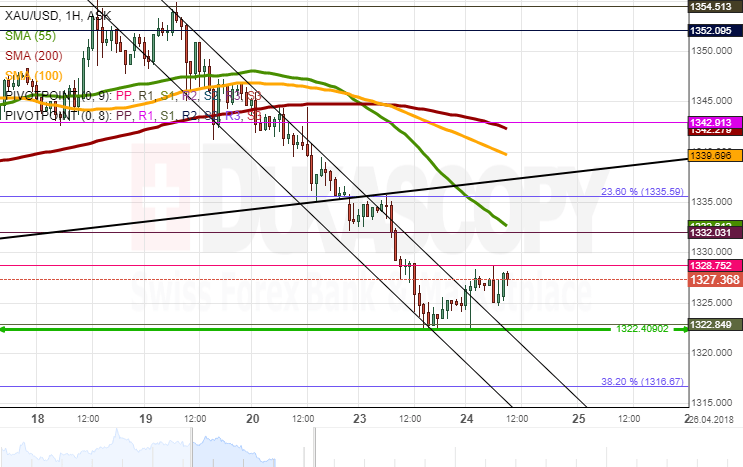

Gold Analysis: Reverses From April Support

The overall strength of the US Dollar put downward pressure on XAU/USD on Monday, thus allowing to extend the pair's losses for the third consecutive session. This fall halted at 1,322.40—a level which has provided an unbreakable support for the last five weeks.

It seems that the yellow metal might be reluctant to push significantly lower in this session, given that the 100-day SMA is strengthening the 1,320.00 area. Thus, it is more likely that bulls take the upper hand and push Gold closer to 1,350.00.

The nearest resistance that could hinder rapid appreciation is the 55-hour SMA and the 23.60% Fibonacci retracement at 1,335.00. Even if this level is surpassed, further gains should be limited due to the 100– and 200-hour moving averages being located slightly higher.

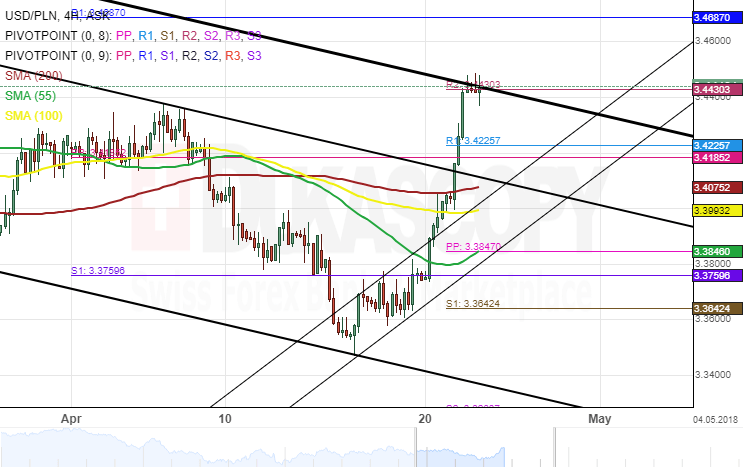

USD/PLN 4H Chart: Breaking Most Resistance

The US Dollar has mapped a massive surge against the Polish currency. Dukascopy analysts had hypothesized a surge. However, the expectations have been beaten in more than one way.

Namely, the drawn junior ascending pattern was broken to the upside on April 20. Secondly, the pair continued the surge only being slowed down by the 200-SMA for a short period. The following surge broke past the medium scale pattern's upper trend line.

On Tuesday morning Dukascopy analytics saw that the pair had stopped during the last 16 hours at the combined resistance of the most dominant pattern and the weekly R2. It was expected that the stalemate would end soon and the pair would break free soon.