Sample Category Title

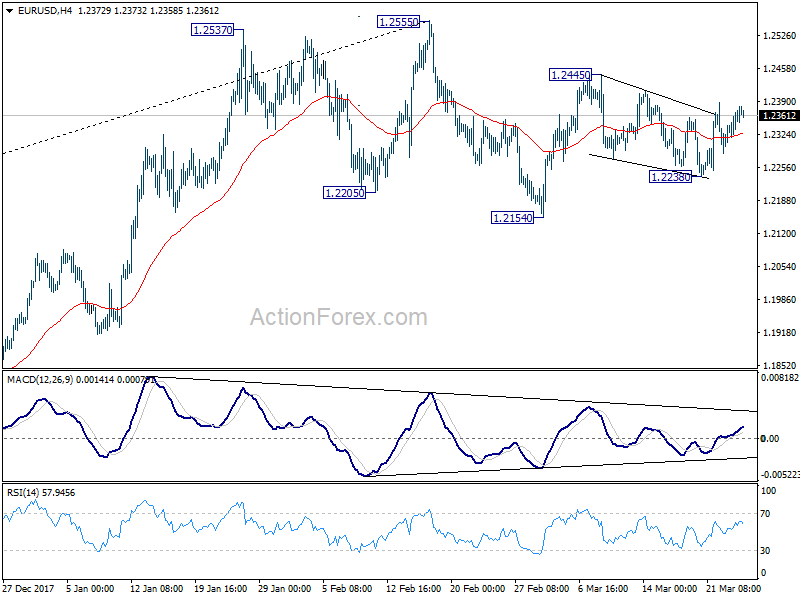

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2308; (P) 1.2341 (R1) 1.2384; More....

Intraday bias in EUR/USD remains neutral first. But we're favoring the bullish case that consolidation from 1.2445 has completed at 1.2238. And, another rise is expected. On the upside, above 1.2445 will target a test on 1.2555 high, which is close to 1.2516 key long term fibonacci level. On the downside, however, firm break of 1.2238 will turn bias back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Major Data Releases For This Week

At 13:30 GMT, US Chicago Fed National Activity Index (Feb) is expected to be 0.19 against the previous 0.12. This number is expected to pick up after falling for the last two months. USD traders will be closely following this data release.

At 18:30 GMT, FOMC Member Dudley is due to participate in a panel discussion about regulatory reform at the United States Chamber of Commerce, in Washington DC. Comments may result in moves in USD crosses.

At 20:30 GMT, FOMC Member Mester is due to speak about the economic outlook and monetary policy at Princeton University, in New Jersey. Audience questions are expected and comments may cause moves in USD crosses.

Major data releases for this week:

On Wednesday at 13:30 GMT, US Gross Domestic Product Annualized (Q4) data will be out, with the headline number expected to be 2.6% from a previous 2.5%. Gross Domestic Product Price Index (Q4) data is expected to be 2.3% from a previous 2.3%.

At 14:30 GMT, Personal Consumption Expenditures (QoQ) (Q4) are expected to be 2.9% v a prior 2.7%. Core Personal Consumption Expenditures (QoQ) (Q4) are expected to be 2.0% v a prior 1.9% reading from Q2.

On Thursday at 13:00 GMT, German Harmonised Index of Consumer Prices (YoY) (Mar) is expected to be 1.5% against a previous 1.2%. German Harmonised Index of Consumer Prices (MoM) (Mar) is expected to be 0.4% against a previous 0.5%.

At 13:30 GMT, US Core Personal Consumption Expenditures – Price Index (YoY) (Feb) is expected to be 1.5% from 1.5% previously. Core Personal Consumption Expenditures – Price Index (MoM) (Jan) is expected to be 0.2% from 0.3% previously.

At 14:00 GMT, Canadian Gross Domestic Product (MoM) (Jan) was 0.1% previously.

On Friday at 00:30 GMT, Japanese Tokyo Consumer Price Index (YoY) (Mar) is expected to be 1.8% v 1.4% previously.

Forex Analysis: South Korea Gets Permanent Exemption On Steel Tariffs After Trade Deal With US

The US and South Korea have reached agreement on a Trade deal that comes with the added bonus for South Korea of a permanent exemption from Steel Tariffs imposed by the US. The arrangement is to allow South Korea to export up to 2.68 million tons of steel to the US each year, equivalent to a 30% reduction on the average figure over the last 3 years. This is a positive development showing a willingness on the part of the US to sign trade deals, following on the progress made on NAFTA last week.

The Russian Interest Rate Decision was for the rate to be cut to 7.25% against the current 7.50%. The Bank of Russia said that it would continue key rate cuts and will end the shift to neutral stance this year. GDP is expected to be 1.5% to 2.0% from 2018 to 2020. Annual CPI is expected to be between 3% and 4% by year end and 4% in 2019.

FOMC Member Bostic is due to speak about the economic outlook at the Knoxville Economics Forum. Comments made were: Further gradual rate hikes over next couple of years ‘appropriate’. He is confident the US is at or near the Fed’s inflation goal. This week’s interest-rate hike made sense and there is a need to move rates toward ‘neutral’. If economy develops as he expects, will likely support more rate hikes this year. Labour markets ‘not yet overheated’, sees upside risks to labour costs. Inflation calm to persist but risks are to the upside. He sees potential for inflation to run somewhat above Fed’s 2% target.

US Durable Goods Orders ex Transportation (Feb) was 1.2% v an expected 0.5% from -0.3% previously which was revised up to -0.2%. Durable Goods Orders (Feb) was 3.1% v an expected at 1.5%% v -3.7% previously which was revised up to -3.5%. This data series missed to the downside last time out but it has recovered and exceeded expectations. EURUSD fell on the announcement from 1.23555 to 1.23337.

Canadian Consumer Price Index (MoM) (Feb) was 0.6% v an expected 0.5% against 0.7% previously. BOC Consumer Price Index Core (YoY) (Feb) was 1.5% v an expected 1.4% against 1.2% previously. BOC Consumer Price Index Core (MoM) (Feb) was 0.7% v an expected 0.5% v a prior 0.5%. Consumer Price Index (YoY) (Feb) was 2.2% v an expected 2.0% against 1.7% previously. Consumer Price Index – Core (MoM) (Feb) was 0.2% v an expected 0.5% against 0.2% previously which was revised up to 0.3%. Canadian Retail Sales ex Autos (MoM) (Jan) was 0.9% v an expected 0.9% against -1.8% previously which was revised up to -1.7%. Retail Sales (MoM) (Jan) was 0.3% v an expected 1.1% against -0.8% previously which was revised up to -0.7%. Inflation showed an expected rise after a beat last month, with gasoline, autos and mortgages all contributing to the increase. Retail sales were expected to be stronger and have missed for the second month in a row. Autos were largely the culprit for this miss with building materials also a drag. USDCAD fell sharply from 1.29069 to 1.28345 after the data deviated from expectations.

UK MPC Member Vlieghe is due to speak at the Birmingham Chamber of Commerce. He made headlines by saying that recent data adds to warranting removal of monetary stimulus. He also said that the current outlook is consistent with 1 or 2 0.25% rate hikes per year in forecast period and rates will need to rise over forecast period if the current balance of global risk vs Brexit headwinds persists. The tight labour market continues to increase domestic inflationary pressures. EURGBP fell from 0.87401 to 0.87114.

US New Home Sales (MoM) (Feb) was 0.618M v an expected 0.623M from 0.593M previously which was revised up to 0.622M. New Home Sales Change (MoM) (Feb) was -0.6% v an expected 4.4% v -7.8% previously which was revised up to -4.7%. On the back of strong HPI data Thursday, Sales improved as expected after falling for three months. However they fell short of the expected level. GBPUSD moved higher from 1.41483 to 1.41717 as a result of this data.

Baker Hughes US Rig Count numbers was released and came in at 804. The prior number last Friday showed that there were 800 Oil rigs in operation. WTI traders will be paying close attention to this number as they look to the week ahead.

EURUSD is up 0.10% overnight, trading around 1.23654.

USDJPY is down 0.14% in the early session, trading at around 104.992

GBPUSD is up 0.12% this morning trading around 1.41525.

USDCAD is unchanged in early trade at around 1.28718

Gold is down -0.12% in early morning trading at around $1,345.30

WTI is down -0.50% this morning, trading around $65.56

Currencies: Trade Tensions Block Any USD Upside Attempts, At Least For Now

Rates: Risk sentiment set to improve, downward bias for core bonds

Risk sentiment is set to improve as weekend comments suggest that common sense could avoid an escalation in the trade disputes. Core bonds could lose some ground with the US Note future underperforming the Bund ahead of supply and after the test of 2.80% support in the US 10-yr yield last week.

Currencies: Trade tensions block any USD upside attempts, at least for now

Global FX remains less affected than equities and bonds by the uncertainty on the US foreign trade policy. The dollar remains slightly in the defensive. Investors apparently want more clarity on the trade issue before considering to engage in additional USD long positions.

The Sunrise Headlines

- US stock markets closed lost 1.75% (Dow) to 2.5% (Nasdaq) after US President Trump threatened to veto a huge spending bill (which he eventually didn't). Losses on Asian stock markets are smaller overnight.

- China and the US have quietly started negotiating to improve US access to Chinese markets, after a week filled with harsh words from both sides over Washington's threat to use tariffs to address trade imbalances. (WSJ)

- The Federal Reserve is set to elevate SF Fed President Williams to the presidency of the New York Fed, one of the central bank's most important positions, just as it faces a potential turning point for setting interest-rate policy.

- Italy's anti-establishment 5SM and the far-right Lega Nord struck a deal to elect the speakers of the country's parliament, increasing chances that they could join forces to form a populist-led government in the coming weeks. (FT)

- S&P raised Spain's rating from BBB+ to A- (positive outlook). Spain's overall economic and budgetary performance has not been hampered by political tensions in Catalonia and GDP will outperform EMU average over 2018-2021.

- Britain's opposition Labour Party will demand that parliament has the final say on the government's Brexit deal, including an option to send ministers back to the negotiating table rather than leave without an exit agreement.

- Today's eco calendar contains only contains second tier eco data. ECB Weidmann, Fed Dudley and Fed Mester speak. The US and Italy tap the market

Currencies: Trade Tensions Block Any USD Upside Attempts, At Least For Now

Trade debate remains a (modest) USD negative

On Friday, global trade tensions had again less impact on FX compared to bonds or equities. The dollar came under moderate pressure as risk sentiment in the US deteriorated going into the weekend. USD/JPY dropped below 105, but the decline remained modest given the steep losses on US equity markets. EUR/USD closed higher on a daily basis (1.2353 from 1.2302), but held within the established ranges.

Asian equities are mostly in negative territory this morning, but the losses are moderate given the sell-off in the US on Friday. South Korea outperforms. The country received an exemption on the US steel tariffs and the two countries are working to revise an existing free trade pact. Markets are pondering whether this could be some kind of blueprint to solve other bilateral issues between the US and its trading patterns. For now, the tentative easing of tensions (US equity futures are trading in positive territory) doesn't help the dollar much. EUR/USD trades in the 1.2370 area. USD/JPY struggles to regain the 105 barrier.

There are only second tier eco data in the US and Europe today. Several Fed and ECB members (including Dudley, Mester, Quarles & Weidmann) speak. Tensions between the US and its trading patterns and the impact of the issue on global sentiment remains the dominant driver for FX trading.US equity futures suggest that markets might shift to a more neutral wait-and-see attitude. This is unlikely to be enough to trigger a sustained USD rebound, especially if there is no other USD supportive news. EUR/USD is holding more or less in the middle of the 1.2155/1.2555 range. USD/JPY remains more vulnerable. The pair is holding near the lowest level since November 2016.

Sterling rebounded temporary on Friday. Comments from the EU summit suggested that talks between the EU and the UK developed in a rather constructive way. BoE's Vlieghe, seen as a dove, confirmed that a scenario of one or two rate hikes this year is possible. However, the deterioration in global risk sentiment didn't help sterling, especially not against the euro. EUR/GBP closed the session at 0.8742. UK housing loans will probably only be of intraday significance for sterling trading today. EUR/GBP is holding north of the 0.8668/52 support. We don't see a trigger for a sustained break at this stage

EUR/USD: Trade tensions prevent USD rebound

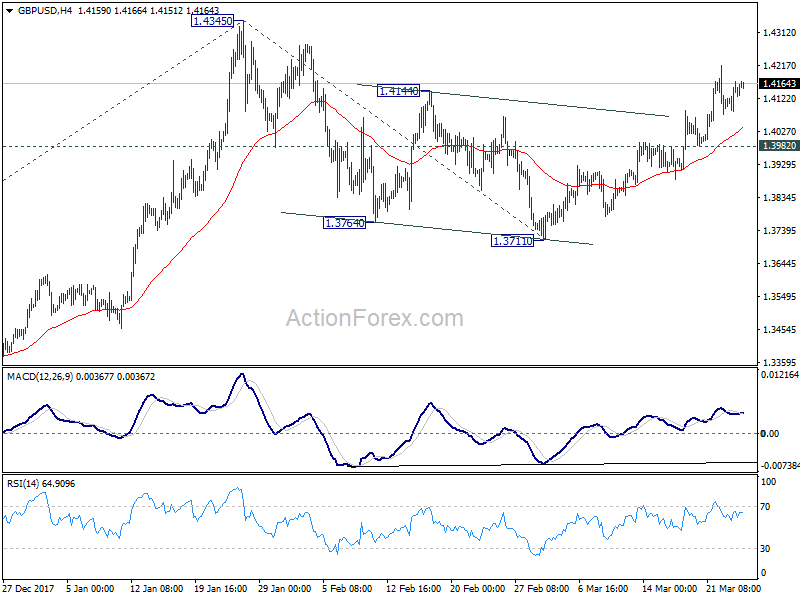

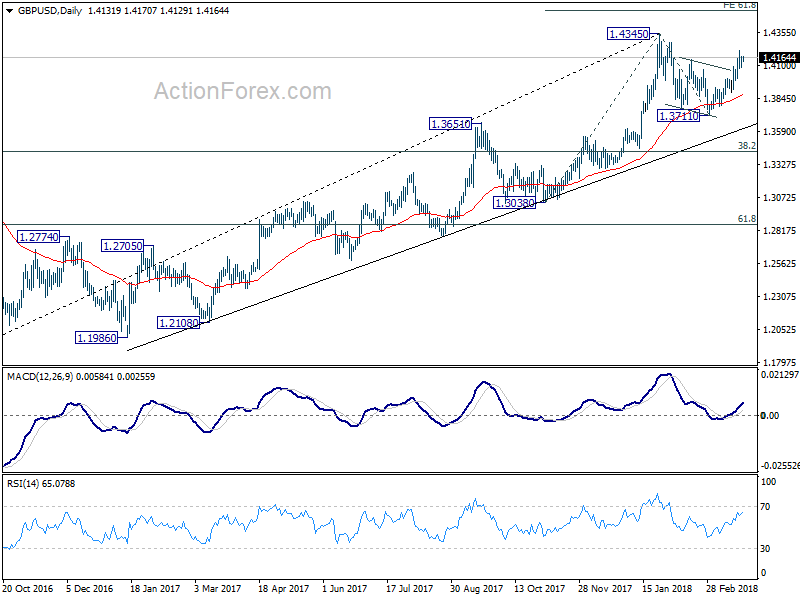

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4085; (P) 1.4128; (R1) 1.4173; More....

With 1.3982 minor support intact, further rise is expected in GBP/USD to retest 1.4345 resistance first. Firm break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, , break of 1.3982 will argue that rebound from 1.3711 has completed. And, intraday bias will be turned back to the downside for 1.3711 support and possibly below, to extend the corrective pattern from 1.4345.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

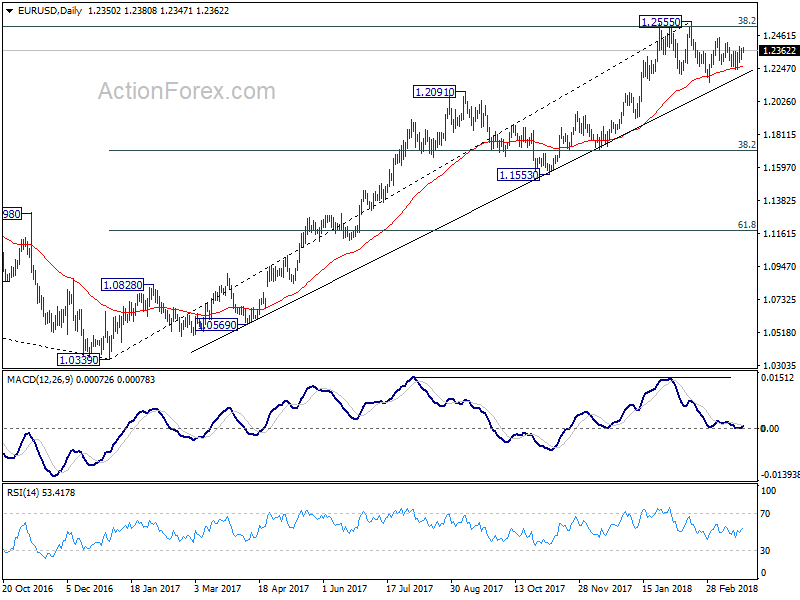

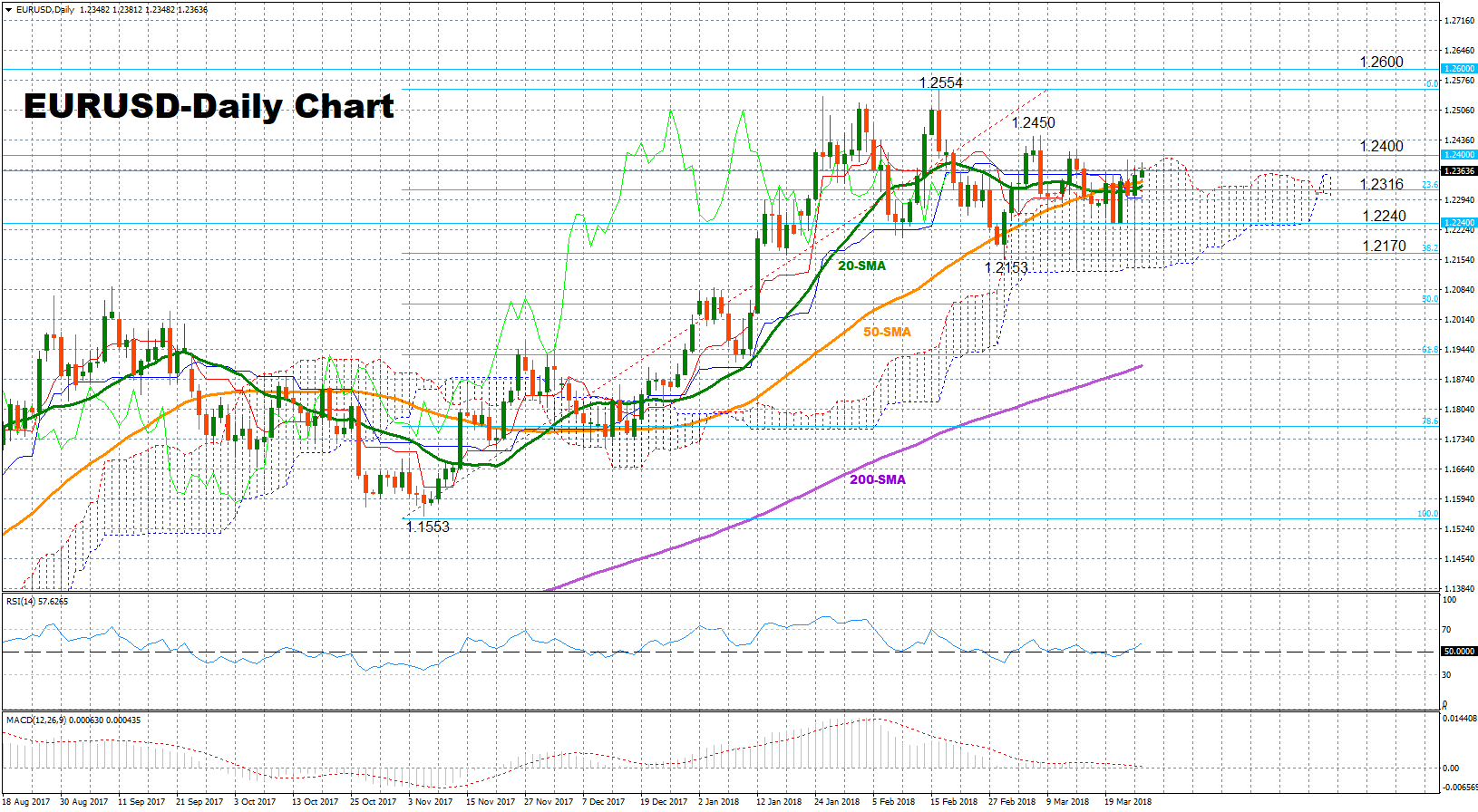

EURUSD Stretches Range-Bound Trading

EURUSD closed higher in Friday's trading but maintained in a range between 1.2150-1.2450 started at the end of February, with technical indicators suggesting that the sideways pattern might continue for a while.

Looking at momentum indicators, the RSI is pointing to the upside, giving some positive signals for the short-term, though, the index has not deviated much above its neutral threshold of 50. Therefore, we expect the pair to improve moderately in the short-term, remaining overall in a range. MACD barely holds in positive territory and is still capped by its red signal line, painting a neutral picture as well.

Should the pair make a step higher, the area between 1.2400-1.2450, which includes February's highs, could offer nearby resistance before the focus shifts to the three-year peak of 1.2554. A close above this top could see prices rallying towards the 1.26 handle, while a more decisive upside move could open the door to the 1.2700 psychological level as well.

To the downside, if the market weakens, support could come around the area between 1.2336-1.2316 where the 23.6% Fibonacci of the upleg from 1.1553 to 1.2554, and the 50- and the 20-day simple moving average lines are currently located. A leg below this mark could target 1.2240, a frequently congested area since the beginning of the year, while steeper decreases could also revisit the 38.2% Fibonacci of 1.2170. However, only a break below the March low of 1.2153 could trigger bearish extensions, resuming the downtrend from 1.2554.

In the medium-term, the market looks bullish, given that the market maintains its uptrend recorded over the last three months and the bullish cross between the 50-day and the 200-day SMA remains intact. However, the bullish signals could be stronger if prices manage to increase their distance from the 50-day SMA.

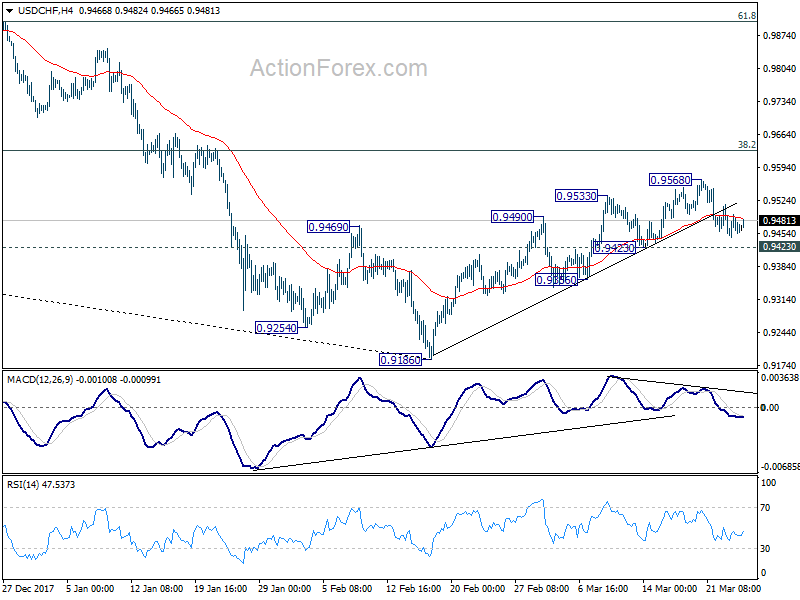

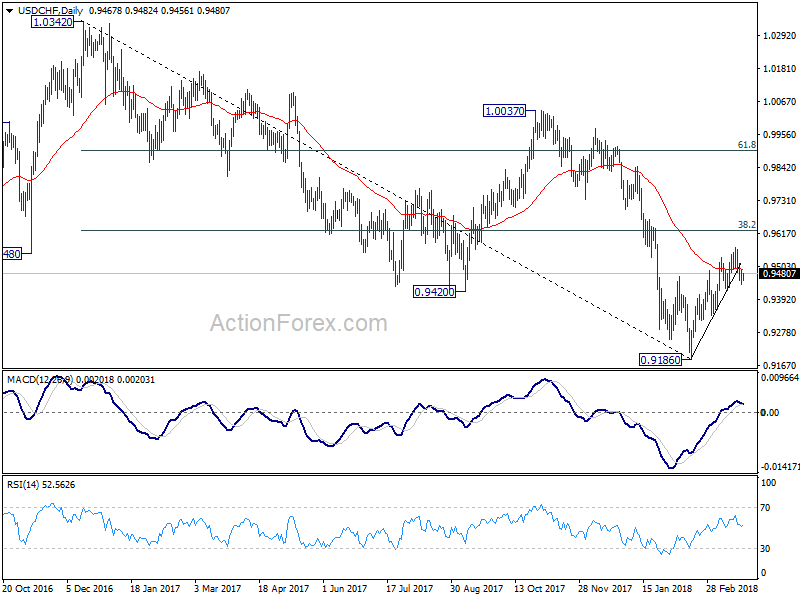

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9442; (P) 0.9469; (R1) 0.9493; More...

Intraday bias in USD/CHF remains neutral for the moment. Rebound from 0.9186 might not be finished yet. But considering divergence condition in 4 hour MACD, even in case of another rise, upside should be limited by 0.9626 key fibonacci level. Break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will carry larger bullish implications.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

USDJPY Still Bearish Below 105.24 Level

The U.S dollar continues to suffer from risk-off trading sentiment against the Japanese yen, as U.S trade tariffs on China pressure global stocks and the greenback lower. The USDJPY pair finished the previous trading week at a sixteen-month trading low, with price-action closing firmly below the key 105.24 support level. Downside pressures on the pair are likely to remain, as financial markets await China’s retaliation to the latest round of U.S trade tariffs.

The USDJPY pair is bearish while trading below the 105.24 support level, further selling towards 104.00 and 103.60 remains possible.

If the USDJPY pair can maintain price-action above the 105.24 level, a correction towards the 105.50 and 106.00 level cannot be ruled out.

Furhter EURUSD Gains Above 1.2382 Level

The euro retains a bullish bias against the U.S dollar as the new trading week gets underway, with buyers now needing to keep price-action anchored above the key 1.2382 level for further gains. Medium term MACD and Stochastic indicators are also supporting EURUSD upside, with key intraday technical support found at the 1.2305 level. Movements in stocks and the U.S dollar index seem likely to drive today’s action in the pair, with U.S trade tariffs still capturing financial markets attention.

The EURUSD pair is likely to likely to see further buying interest once clearly above the 1.2382 level, key weekly resistance is found at the 1.2430 and 1.2555 levels.

Should the EURUSD start to trade below the 1.2305 support level for a sustained period, price-action will turn bearish. Key weekly support is then found at 1.2238 and 1.2160.

Fed Officials Members Chime In On Monetary Policy Monday

US economic data and monetary policy will once again take centre stage on Monday. On the policy front, two officials at the Federal Reserve will shine the spotlight back on the central bank's decision to raise interest rates last week.

Action begins in Europe at 06:00 GMT with a report on German import prices. Just 45 minutes later, the French government will deliver its quarterly report on GDP.

At 09:00 GMT, the Italian government will update the market on its trade balance with non-European Union countries.

In the United Kingdom, the British Bankers Association will deliver its monthly report on mortgage approvals at 09:30 GMT.

Shifting gears to the United States, the Federal Reserve Bank of Chicago will release the national activity index at 12:30 GMT. The monthly report is expected to show a slight uptick in national economic activity with a reading of +0.19.

Meanwhile, the Dallas Fed will release the manufacturing business index at 14:30 GMT. The monthly reading is expected to fall to 33.4 from 33.7 in February.

Federal Reserve Bank of New York President William Dudley is scheduled to speak at 17:30 GMT. Three hours later, Federal Open Market Committee (FOMC) member Loretta Mester is also scheduled to deliver a speech. Mester was on the policy board that voted to raise interest rates by a quarter point last Wednesday.

The Fed's official rate statement left the door open to further policy tightening in the months ahead. The official dot plot summary of interest rate expectations also pointed to gradual rate hikes in the near future.

EUR/USD

The euro is coming off a strong Friday session that was triggered by fresh losses in the US dollar. EUR/USD extended its gains on Monday, with prices climbing toward 1.2370. The pair has moved above initial resistance and is now poised to re-test 1.2413, which is the high from 14 March. On the opposite side of the ledger, immediate support is located at 1.2330.

GBP/USD

Cable's bullish upside continued last week, as investors reacted positively to Brexit developments. GBP/USD rose 0.2% on Monday to 1.4160. The bulls are looking at the 1.4218 level as the next major resistance test. A clean break above this level would lead to a re-test of the 1 February high of 1.4278.

GOLD

Global risk aversion tied to last week's epic stock market collapse sent gold prices to yearly highs on Friday. The yellow metal was little changed at the start of Asian trade but remains well supported around $1,346. With European and Asian stocks expected to fall hard on Monday, gold could be poised to extend its recent rally. A sharp reversal in the US dollar could also provide the catalyst for gold's continued growth.