Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 104.45; (P) 104.89; (R1) 105.16; More...

Intraday bias in USD/JPY remains on the downside for 104.20 projection level first. Sustained break there will pave the way to 98.97 (2016 low). On the upside, break of 106.63 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

USD/JPY Seems To Have Found A ‘Bottom’ Around The 104-105 Level

Market movers today

There are no significant market movers today. We have a few speeches from Federal Reserve members as well as ECB members.

Focus in the market will continue to be on the risk of a trade war between the US and China.

On top of the tariffs, the US Treasury will sell a record amount of T-bills and Treasury bonds this week as they will sell USD294bn.

Selected market news

The negative sentiment in the equity market continues this morning with a decline in most Asian equity markets. The focus is still on the risk of a possible trade war with China. However, the US and South Korea reached an agreement on trade as well as on the tariffs over the weekend. Hence, US Treasury Secretary Steven Mnuchin said that he was optimistic that an agreement between the US and China could be reached.

In the currency markets, USD/JPY seems to have found a ‘bottom' around the 104-105 level this morning, with the yen trading stronger for most of March.

The USD Libor fixings continued to rise last week. One of the drivers for the increase in the USD Libor has been the increased supply of US T-bills and with the record sale of T-bills and Treasury bonds from the US Treasury department this week, the risk is that the USD Libor will continue to rise this week.

Last Friday, the central bank of Russia (CBR) cut its key rate by 25bp as we expected with the majority of both Bloomberg's and Reuters' consensus. Approximately one third of interbank traders presumed a 50bp cut. In its statement, the CBR emphasised sustainably low inflation (2.2% y/y currently) and decreasing inflation expectations. Yet, the CBR expects inflation to accelerate by end-2018 to 3-4%, anchoring around the desired target of 4% in 2019. The CBR communicated clearly that it will continue to cut rates to achieve the neutral rate in 2018, which is somewhere between 6-7%. Given the current path, we expect the key rate to fall to 6.25% by end-2018. RUB's reaction to the decision was neutral as we expected and the central bank governor's dovish tone at the press conference did not spark any turbulence. Looking forward, we see geopolitical risks being major movers for the RUB in both directions.

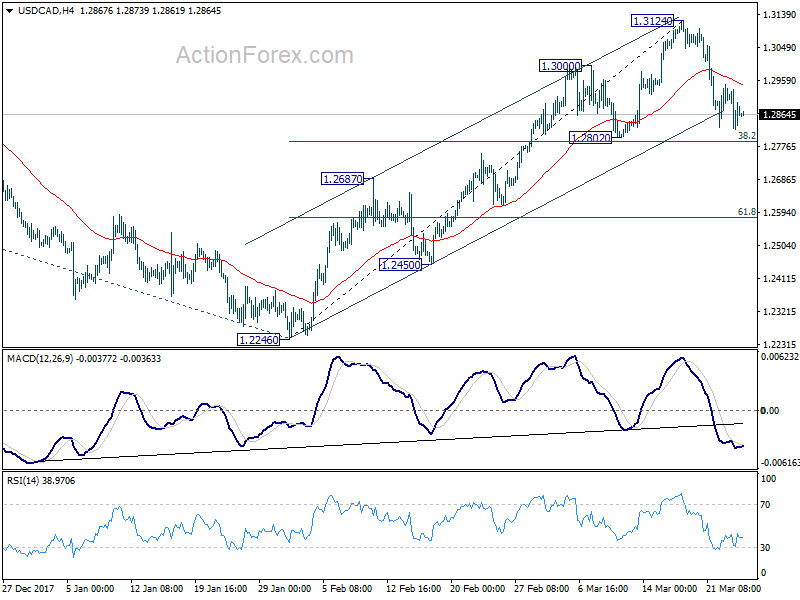

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2833; (P) 1.2885; (R1) 1.2947; More....

No change in USD/CAD's outlook. We'd expect strong support from 1.2802 cluster support zone (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside and bring rebound. Larger rise is expected to resume later. And break of of 1.3124 will target 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629 next. However, firm break of 1.2789/2802 will raise the chance of rejection by 1.3065 medium term fibonacci level and bring deeper fall to 55 day EMA (now at 1.2751) and below.

In the bigger picture, we're favoring the medium term bullish case. That is, larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds. However, rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Asia Market Update: USD/JPY Tests 16-Month Low

Headlines/Economic Data

General Trend: Asian Markets trade generally lower following sharp declines on Friday

- Japan steel companies continue to be weighed down by trade concerns

- Meanwhile, South Korea steelmakers gain on speculation of new trade agreement with US

- Nikkei pares more than 1% loss

- US equity futures trade higher; US financial press reports US and China are aiming to ease trade dispute

- US said to send letter to China about how to reduce trade surplus

- New Zealand adds employment to the RBNZ’s mandate

- Shanghai Yuan-denominated oil futures rise over 6% in first day of trading

- China traded Steel and Iron Ore prices extend declines

Japan

- Nikkei 225 opened -0.9%; closed +0.7%

- TOPIX Iron & Steel Index -1.3%

- Ricoh [7752.JP] declines over 4% after disclosing impairment charge

- (JP) Japan PM Abe Cabinet approval declines to 42%, down 14 pct points from late Feb; comes amid Moritomo land scandal - Nikkei

- (JP) Former head of an education institute confirms PM Abe wife was involved in land sale at center of scandal - Kyodo citing opposition lawmakers who interviewed him at detention center

- (JP) Japan Steel Federation: JPY currency (Yen) appreciation to 104-105 area is a concern

Korea

- Kospi opened -0.1%

- (KR) South Korea Trade Min: South Korea and the United States have reached an agreement “in principle” on renegotiation of their free trade agreement - Korean press

China/Hong Kong

- Hang Seng opened -0.1%, Shanghai Composite -1.1%

- Hang Seng Financials Index -0.9%, Materials -0.7%

- Shanghai Composite Property sub-index declines over 1%

- Footwear company Yue Yuen declines over 6% after reporting drop in FY17 profits

- (CN) China to launch yuan denominated oil futures contract, the "petroyuan", effective today after long awaited approval from China State Council

- (CN) China names Guo Shuqing (current vice Chairman of newly combined banking/insurance regulator) as party secretary of the PBoC – financial press

- (CN) New PBoC Gov Yi Gang reiterated China will steadily reform and further open its financial sector, while putting equal emphasis on risk prevention – China Development Forum in Beijing (update)

- (CN) China researcher says RRR should be cut - Chinese Press

- (US) Treasury Se Mnuchin: Trump administration is pressing ahead with tariffs, but remains hopeful on reaching trade deal with China – Fox

- (US) Trump Administration said to send letter from Treasury Sec and US Trade Rep to China's Liu He seeking reduction of China's tariffs on US autos - US financial press

- (CN) China's former Vice Commerce Min Wei Jianguo says China may seek to add tariffs on US airplanes and computer chips – Chinese

- USD/CNY (CN) China PBoC sets yuan reference rate at 6.3193 v 6.3272 prior

- (CN) PBoC Open Market Operation (OMO): Skips OMO v skips prior; Net drains CNY70B v CNY90B prior (2nd consecutive skip)

- (CN) PBoC auctions 3-month Finance Ministry (MOF) deposits at 4.62%

- (CN) China Minister: 'Made in China 2025' policies apply to foreign companies; reiterates to further open manufacturing sector to foreign capital

- (CN) China targeting US soybean exports would be seen as a serious escalation in tensions - FT

- (CN) China Ambassador to US Tiankai: China is looking at all options in response to US tariffs including reducing purchase of treasuries - financial press

- (HK) HK$ overnight HIBOR +10bps, highest level in March; 12-month +4bps to 1.90193% (highest level since 2008)

Australia/New Zealand

- ASX 200 opened -0.1%; closed -0.5%

- ASX 200 Financials Index -0.8%, Telecom -0.7%

- Gold miners in Australia outperform after recent gain in gold prices

- (NZ) RBNZ incoming Gov Orr and Fin Min Robertson: Issue new RBNZ policy targets; creates monetary policy committee; affirms to retain focus on 2% midpoint of inflation target range and full employment; Adds employment to the RBNZ's mandate

- (NZ) NEW ZEALAND FEB TRADE BALANCE (NZ$): +217M V -100ME; 12-MONTH YTD: -3.0B V -3.2BE; Exports: 4.5B v 4.6Be, Imports: 4.2B v 4.6Be

North America

- (US) Trump Administration said to send letter from Treasury Sec and US Trade Rep to China President Xi's top economic advisor Liu He seeking reduction of China's tariffs on US autos - US financial press

- (US) Reportedly San Francisco Fed Pres John Williams is the leading candidate to become next president of the New York Fed - press

- (US) Gun manufacturer Remington Outdoor has filed for bankruptcy

- UBER.IPO Sells southeast Asia operations to Grab in exchange for 27.5% stake in Grab; Uber CEO to have seat on board

Europe

- (ES) S&P raises Spain sovereign debt rating one notch to A- from BBB+; outlook Positive (from Friday, March 23rd)

- (ES) On Sunday, former Catalonia leader Carles Puigdemont was detained by police officials in Germany – US financial press

- (IT) Italy's 5-star and League parties said to reach agreement on election of parliamentary speakers - financial press

Levels as of 01:00ET

- Hang Seng -0.5%; Shanghai Composite -1.7%; Kospi +0.5%

- Equity Futures: S&P500 +0.8%; Nasdaq100 +1.0%, Dax +1.0%; FTSE100 +0.7%

- EUR 1.2382-1.2343; JPY 105.06-104.57; AUD 0.7731-0.7696;NZD 0.7277-0.7231

- Apr Gold -0.2% at $1,346/oz; May Crude Oil -0.5% at $65.55/brl; May Copper -0.5% at $2.96/lb

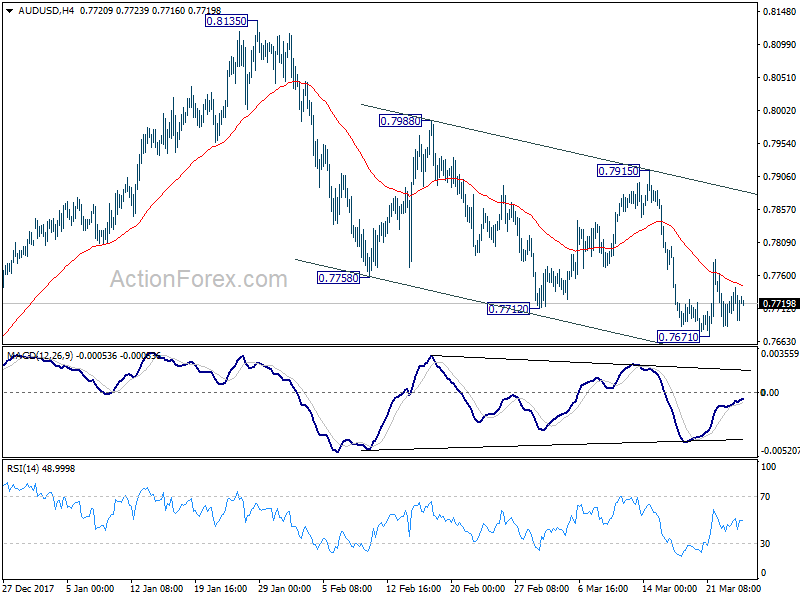

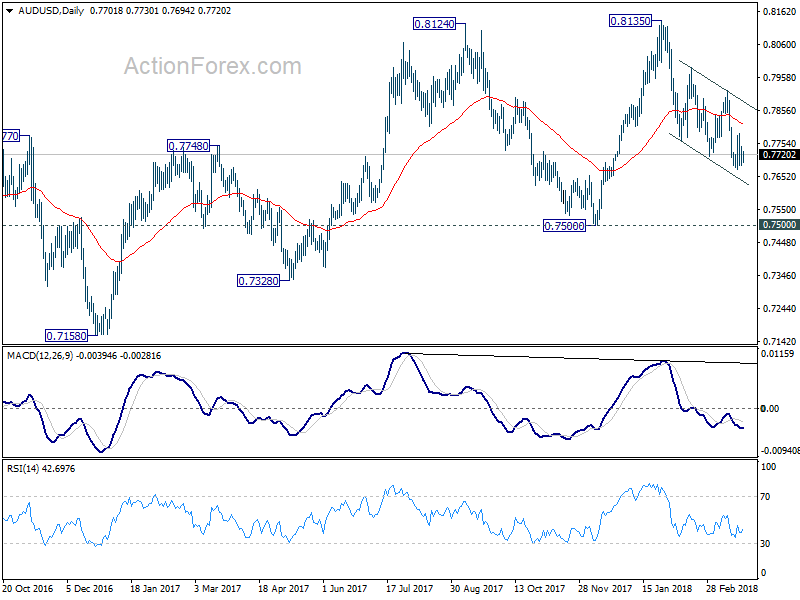

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7672; (P) 0.7708; (R1) 0.7729; More...

AUD/USD continues to stay in consolidation above 0.7671 temporary low and intraday bias remains neutral. Near term outlook stays bearish with 0.7915 resistance intact and fall from 0.8135 is expected to extend. Break of 0.7671 will turn bias to the downside for 0.7500 key support level next. However, break of 0.7915 resistance will indicate near term reversal and turn focus back to 0.8135 high instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

US Treasury Mnuchin in Trade Talk with China, But No One is Cheering Yet

The financial markets opened the week rather quietly. Nikkei and KOSPI opened lower and turned black as the session went on. But other major Asian indices stayed slightly in red. US is apparent in talk with China on trade agreement. But no one in the markets is cheering for it at this stage. In the currency markets, commodity currencies are generally higher. New Zealand dollar is leading the way on solid trade performance in February. Yen is paring its recent gains broadly as risk aversion is not intensifying. Markets could turn more quiet in a holiday shortened week.

The financial markets opened the week rather quietly. Nikkei and KOSPI opened lower and turned black as the session went on. But other major Asian indices stayed slightly in red. US is apparent in talk with China on trade agreement. But no one in the markets is cheering for it at this stage. In the currency markets, commodity currencies are generally higher. New Zealand dollar is leading the way on solid trade performance in February. Yen is paring its recent gains broadly as risk aversion is not intensifying. Markets could turn more quiet in a holiday shortened week.

Mnuchin in "very productive conversations" with China on trade agreement to avert Section 301 tariffs

US Treasury Secretary Steven Mnuchin said in a Fox News Sunday interview that the US is having "very productive conversations" with China. And he's "cautiously hopeful we can reach an agreement" to avert the tariffs on USD 50-60b announced last week. Mnuchin noted that both countries agreed on reducing the US trade deficit to China. And, they were trying "to see if we can reach an agreement as to what fair trade is for them to open up their markets, reduce their tariffs, stop forced technology transfer."

But Mnuchin emphasized that the US is still on track to impose the Section 301 tariffs unless there is an "acceptable agreement" for Trump to sign off on. He also noted that "we're not afraid of a trade war, but that's not our objective." And, "in a negotiation you have to be prepared to take action."

Separately, the WSJ reported that Mnuchin and US Trade Representative Robert Lighthizer sent a letter to Chinese Vice Premier Liu He last week, detailing the list of specific request for China. And the list is reported to include reduction of Chinese tariffs on US vehicles, purchases of semiconductor products and larger access to China's financial markets.

South Korea the first that got indefinite exemption on US steel tariffs

The South Korea's Ministry of Trade said today that is' exempted from the US steel and aluminum tariffs. However, South Korea now received a quota of around 2.68m tonnes of steel exports. And that is 70% of the annual average of Korean steel exports to the US between 2015-2017. South Korean contributed to 9.7% of US steel imports in 2017. In the mean time, Both countries also agreed on 20-year extension of Korean pickup trucks, until 2041. US automakers could also bring in 50000 vehicles to South Korean annually, doubling from prior amount of 25000.

That is the first of many US allies to receive an indefinite exemption on the steel and aluminum tariffs. Other six, Argentina, Australia, Brazil, Canada, Mexico and EU are just having the tariffs temporarily suspended. At this point, there is no news regarding the exemption on Japan and Taiwan, two other major US allies in Asia, yet.

RBNZ added employment to its mandate. But won't change Governor Orr's policy bias

RBNZ jointly announced the policy target agreements with Ministry of Finance today. Employment is now formally added to its mandate. The statement retained price stability as a target. RBNZ should target to keep annual CPI inflation between 1-3% over medium term. And focus is to keep inflation near to the 2% mid-point. Additionally, the with stable general price level maintained, the monetary would "contribute to supporting maximum sustainable employment within the economy." Overall, the announce is widely expected as a result of the new government's RBNZ review. And, there wouldn't be any change to the neutral to slightly dovish bias of RBNZ as Adrian Orr just take over as the governor.

New Zealand trade surplus at NZD 217m in Feb, import hits Feb record high

NZD trades generally higher in Asian session after trade balance data. Accord to Stats NZ Tatauranga Aotearoa, for February 2018 compared with February 2017, goods exports rose NZD 446 million or 11% yoy to NZD 4.5 billion. Goods imports rose NZD 187 million or 4.6% to NZD 4.2 billion. Import was a new high a new high for total imports in a February month. The previous high was NZD 4.1 billion, in February 2017. The monthly trade balance was a surplus of NZD 217 million. That equals to 4.9% of exports.

The week ahead

The economic calendar ahead is not too busy, in a holiday shortened week. There are some economic data that could be market moving. And they include US personal income and spending, consumer confidence and Canada GDP. But traders will probably look through to next week for the more important data like non-farm payrolls and ISM indices instead.

- Monday: UK BBA mortgage approvals

- Tuesday: Japan corporate service price; Eurozone M3; US S&P Case-Shiller house price, consumer confidence

- Wednesday: New Zealand business confidence; German Gfk consumer sentiment; UK CBI realized sales; US Q4 GDP final, trade balance, wholesale inventories, pending home sales

- Thursday: UK Gfk consumer confidence; Japan retail sales; German CPI, unemployment; Swiss KOF; UK Q4 GDP final, M4, mortgage approval, current account; Canada GDP, RMPI and IPPI; US personal income and spending, Chicago PMI, jobless claims;

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, housing starts

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7672; (P) 0.7708; (R1) 0.7729; More...

AUD/USD continues to stay in consolidation above 0.7671 temporary low and intraday bias remains neutral. Near term outlook stays bearish with 0.7915 resistance intact and fall from 0.8135 is expected to extend. Break of 0.7671 will turn bias to the downside for 0.7500 key support level next. However, break of 0.7915 resistance will indicate near term reversal and turn focus back to 0.8135 high instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Feb | 217M | -100M | -566M | -655M |

| 08:30 | GBP | BBA Loans for House Purchase Feb | 39.2K | 40.1K |

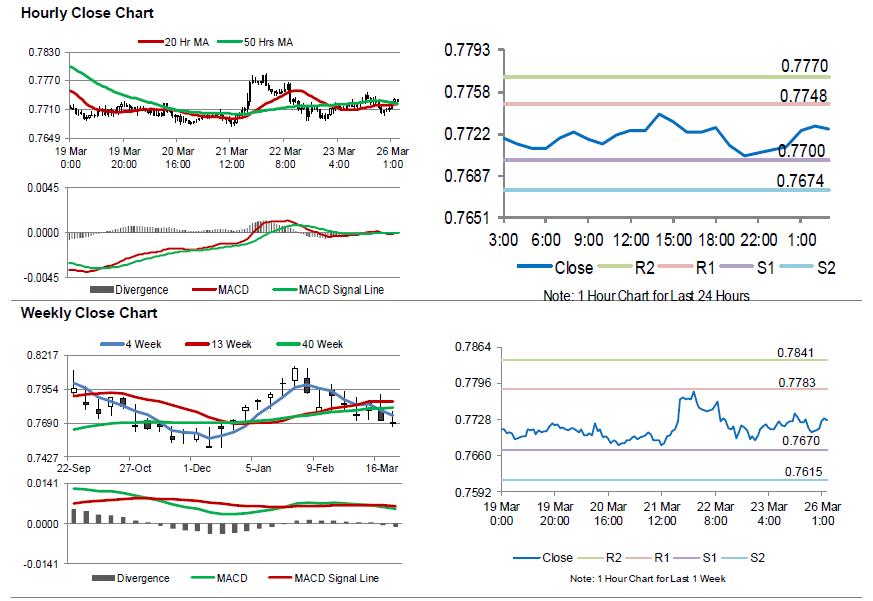

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.16% against the USD and closed at 0.7703 on Friday.

LME Copper prices declined 1.3% or $88.5/MT to $6658.0/MT. Aluminium prices declined 0.5% or $10.0/MT to $2049.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7726, with the AUD trading 0.30% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7700, and a fall through could take it to the next support level of 0.7674. The pair is expected to find its first resistance at 0.7748, and a rise through could take it to the next resistance level of 0.7770.

With no macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

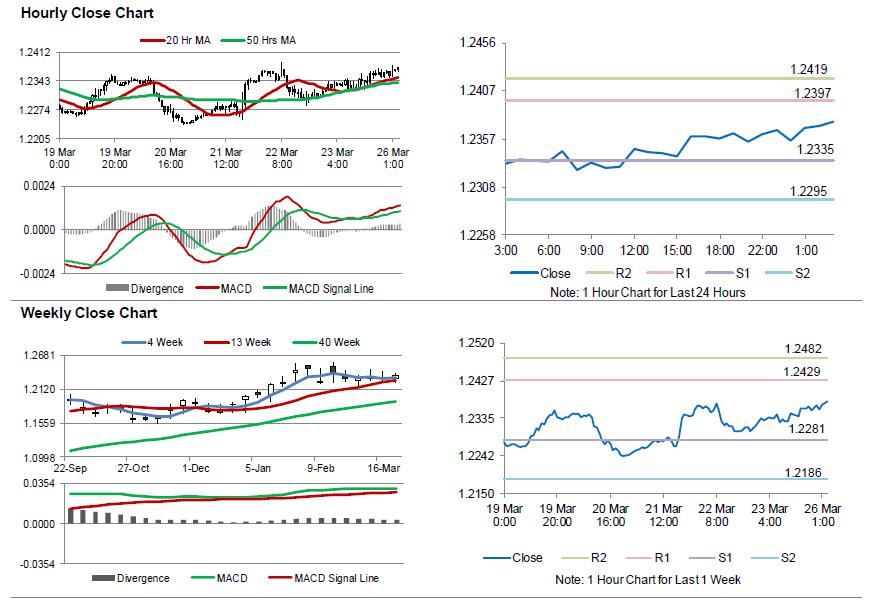

Euro Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the EUR rose 0.20% against the USD and closed at 1.2354 on Friday.

The US Dollar plummeted against a basket of major currencies on Friday, as fears over the impact of a trade war on global economic growth continued to dampen investor sentiment.

On the macro front, the US flash durable goods orders rebounded more-than-expected by 3.1% on a monthly basis in February, rising at its fastest pace since June 2017. In the previous month, durable goods orders had registered a fall of 3.6%, while markets were anticipating for a gain of 1.6%.

On the other hand, the nation’s new home sales surprisingly declined 0.6% on a monthly basis, to a level of 618.0K in February, dropping for the third straight month. New home sales had registered a revised reading of 622.0K in the prior month, while investors had envisaged for a rise to a level of 623.0K.

In the Asian session, at GMT0300, the pair is trading at 1.2375, with the EUR trading 0.17% higher against the USD from Friday’s close.

The pair is expected to find support at 1.2335, and a fall through could take it to the next support level of 1.2295. The pair is expected to find its first resistance at 1.2397, and a rise through could take it to the next resistance level of 1.2419.

Amid no key macroeconomic releases in the Euro-zone today, investors would shift their attention to the US Dallas Fed manufacturing activity index for March and the Chicago Fed national activity index for February, both slated to release later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

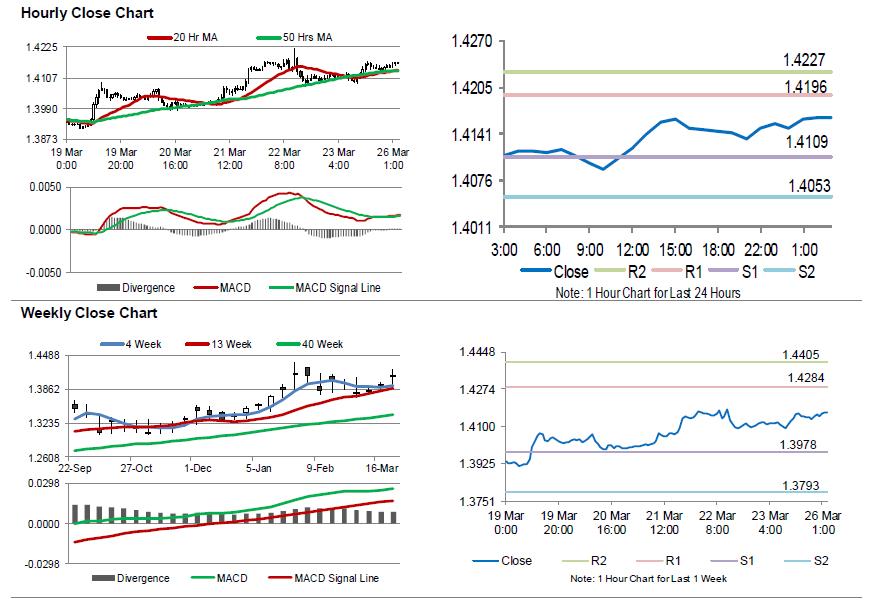

Pound Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.10% against the USD and closed at 1.4133 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.4164, with the GBP trading 0.22% higher against the USD from Friday’s close.

The pair is expected to find support at 1.4109, and a fall through could take it to the next support level of 1.4053. The pair is expected to find its first resistance at 1.4196, and a rise through could take it to the next resistance level of 1.4227.

Moving ahead, traders would eye UK’s BBA mortgage approvals data for February, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

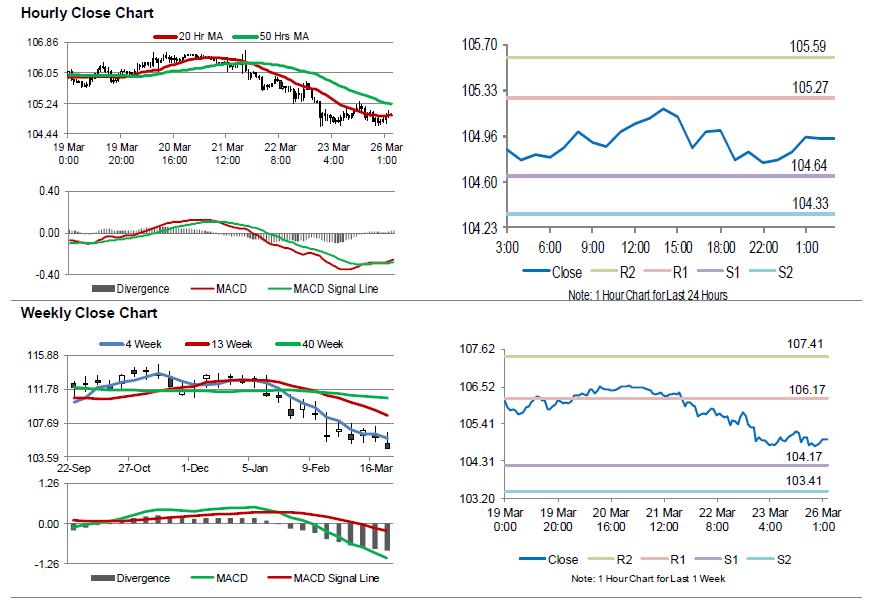

Japanese Yen Reverses Its Gains This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.08% against the JPY and closed at 104.84 on Friday.

In the Asian session, at GMT0300, the pair is trading at 104.94, with the USD trading 0.10% higher against the JPY from Friday’s close.

The pair is expected to find support at 104.64, and a fall through could take it to the next support level of 104.33. The pair is expected to find its first resistance at 105.27, and a rise through could take it to the next resistance level of 105.59.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.