Sample Category Title

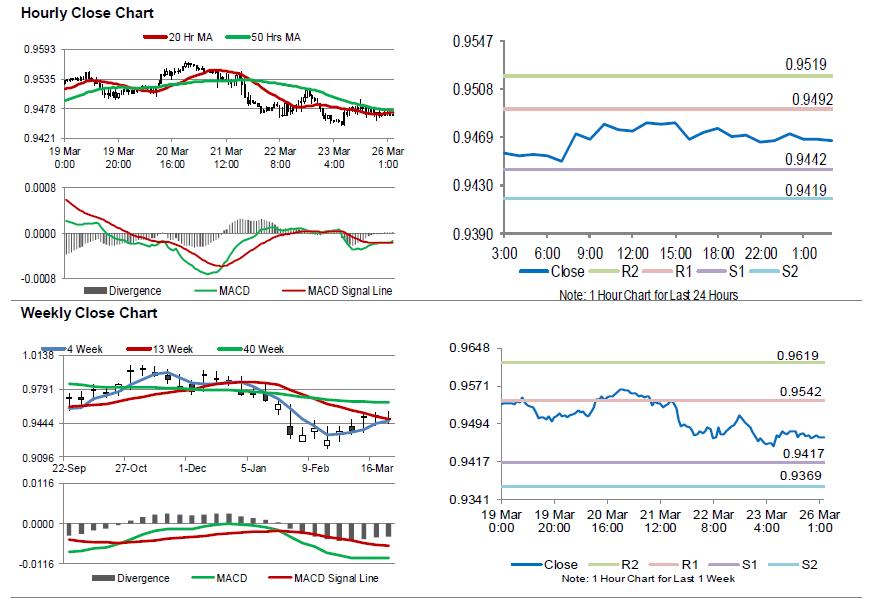

Swiss Franc Trading Marginally Higher This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.06% against the CHF and closed at 0.9470 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9466, with the USD trading slightly lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9442, and a fall through could take it to the next support level of 0.9419. The pair is expected to find its first resistance at 0.9492, and a rise through could take it to the next resistance level of 0.9519.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

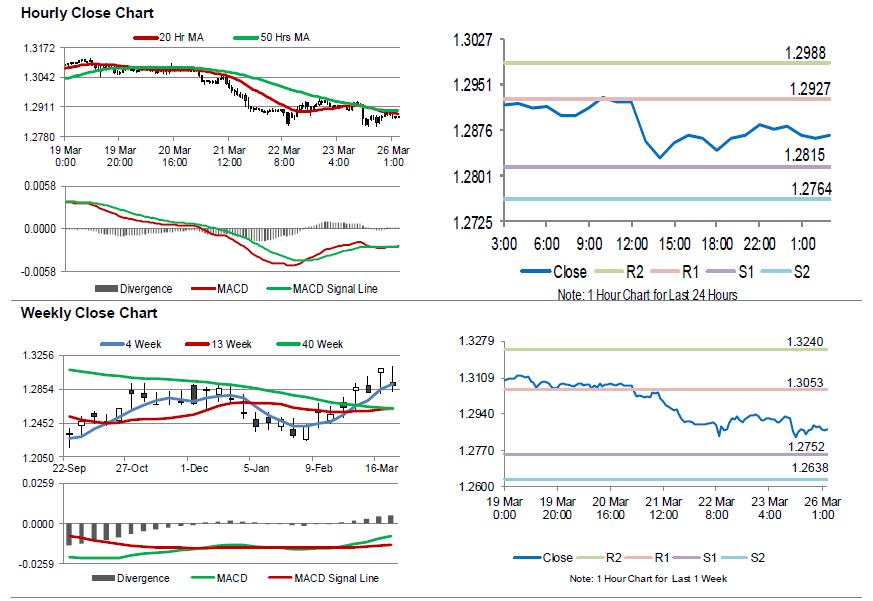

Canada’s Annual Inflation Surged By The Most In 3 Years In February

For the 24 hours to 23:00 GMT, the USD declined 0.33% against the CAD and closed at 1.2868 on Friday.

The Canadian Dollar advanced against the USD on Friday, following better-than-anticipated Canadian inflation figures.

Data revealed that Canada's consumer price index (CPI) advanced 2.2% on an annual basis in February, rising at its fastest pace in 3 years and cementing hopes of a Bank of Canada interest rate hike over the coming months. Market participants had envisaged the CPI to gain 1.9%, after recording a rise of 1.7% in the previous month. Moreover, the nation's retail sales rebounded 0.3% on a monthly basis in January, exceeding market consensus for a rise of 1.1%. Retail sales had registered a revised drop of 0.7% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.2867, with the USD trading marginally lower against the CAD from Friday's close.

The pair is expected to find support at 1.2815, and a fall through could take it to the next support level of 1.2764. The pair is expected to find its first resistance at 1.2927, and a rise through could take it to the next resistance level of 1.2988.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Mnuchin in “very productive conversations” with China on trade agreement to avert Section 301 tariffs

US Treasury Secretary Steven Mnuchin said in a Fox News Sunday interview that the US is having "very productive conversations" with China. And he's "cautiously hopeful we can reach an agreement" to avert the tariffs on USD 50-60b announced last week. Mnuchin noted that both countries agreed on reducing the US trade deficit to China. And, they were trying "to see if we can reach an agreement as to what fair trade is for them to open up their markets, reduce their tariffs, stop forced technology transfer."

But Mnuchin emphasized that the US is still on track to impose the Section 301 tariffs unless there is an "acceptable agreement" for Trump to sign off on. He also noted that "we're not afraid of a trade war, but that's not our objective." And, "in a negotiation you have to be prepared to take action."

Separately, the WSJ reported that Mnuchin and US Trade Representative Robert Lighthizer sent a letter to Chinese Vice Premier Liu He last week, detailing the list of specific request for China. And the list is reported to include reduction of Chinese tariffs on US vehicles, purchases of semiconductor products and larger access to China's financial markets.

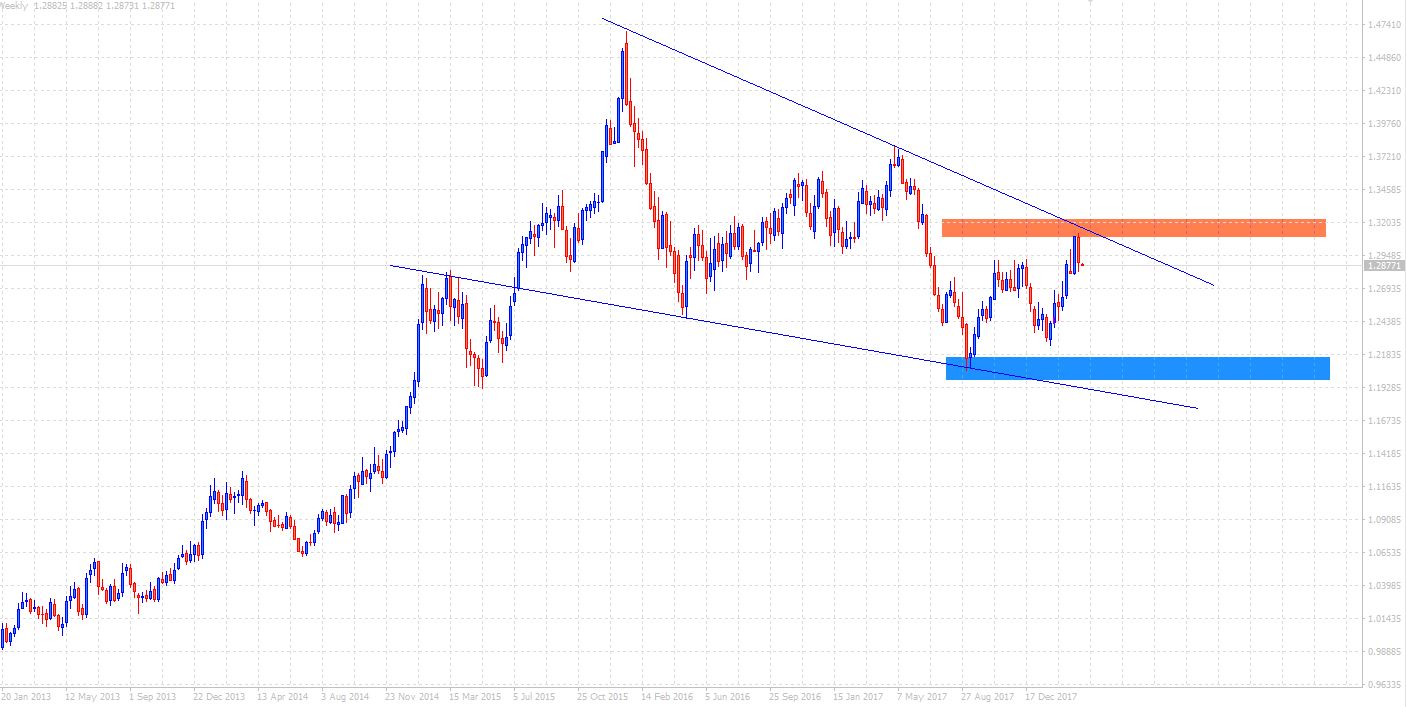

USDCAD At A Strong Downward Trend Line

I hope you had a good weekend. It seems that as traders, we’re perhaps the only people who look forward to Mondays.

Skimming through some more charts over the weekend and came across a beauty. on the weekly chart of the USDCAD, we’ve got a nice wedge forming. This downward resistance seems to be quite strong as price has sharply rejected it, at least for now, and we’re presented with the potential for some further downside action.

Worthy of note is that we are at previous minor highs which may cause some stalling, however, we can potentially see price reach or breach the 1.24 levels or even further to where our blue support area lies.

Weekly chart below.

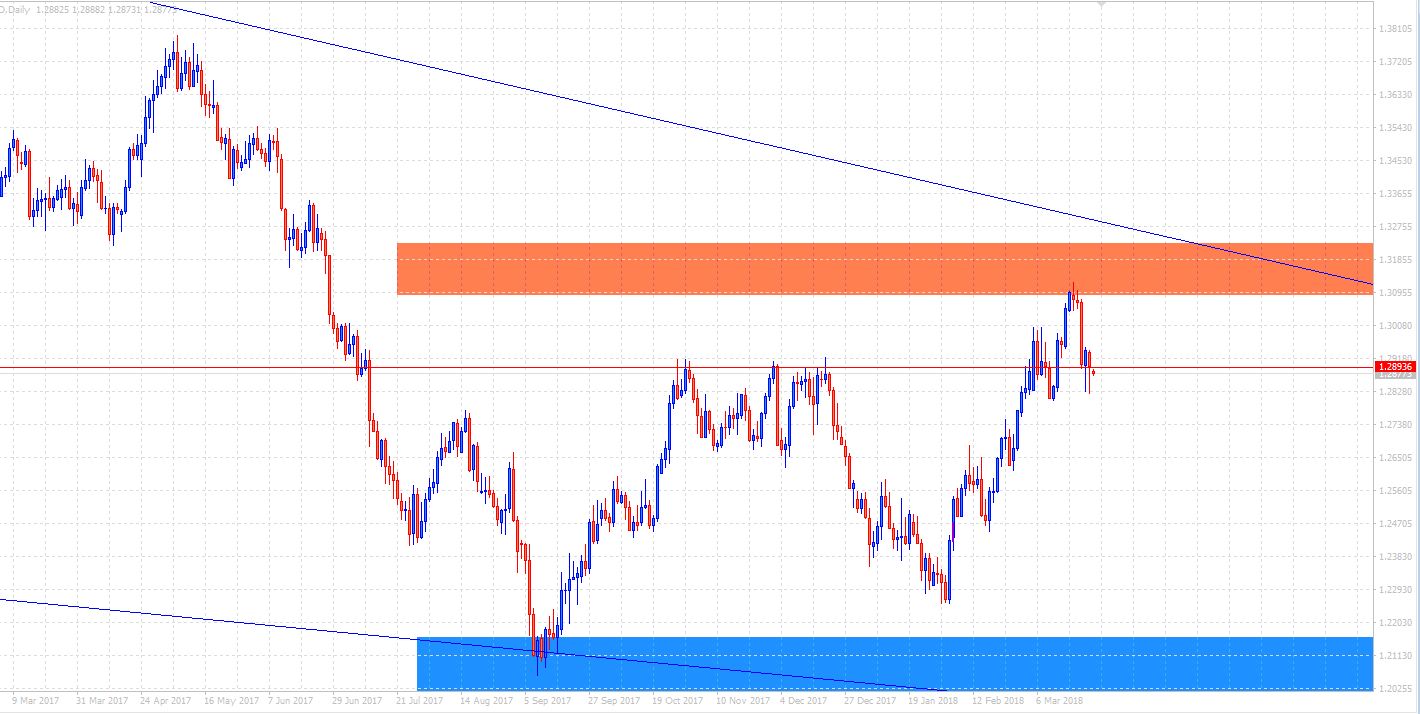

Now, consider the daily chart.

As you can see, price has momentarily stalled at old highs, and whilst there is potential for a bounce, price is still in a medium/long term correction.

Keep an eye for a convincing breach or bounce of these levels and evaluate from there.

EUR/USD Bullish Medium Term Above 1.2250

Key Highlights

- The Euro moved and settled above the 1.2150 and 1.2200 resistance levels against the US Dollar.

- There is a major bullish trend line forming with support at 1.2250 on the daily chart of EUR/USD.

- The US Durable Goods Orders in Feb 2018 increased 3.1%, more than the forecast of +1.5%.

- Today, the Chicago Fed National Activity Index (CFNAI) for Feb 2018 will be released, which is forecasted to increase from 0.12 to 0.19.

EURUSD Technical Analysis

During the past few weeks, the Euro traded nicely, broke a few hurdles, and settled above the 1.2150 and 1.2200 resistance levels against the US Dollar. The EUR/USD pair is currently consolidating above 1.2200 and remains supported on the downside.

The pair traded as high as 1.2559 recently before starting a downside correction. It declined and moved below the 50% Fib retracement level of the last wave from the 1.1915 low to 1.2559 high.

However, the downside move was protected by the 1.2150-1.2200 support area. There is also a major bullish trend line forming with support at 1.2250 on the daily chart. Moreover, the 61.8% Fib retracement level of the last wave from the 1.1915 low to 1.2559 high also served as a support.

The pair is currently trading well above the trend line and 1.2200 on the daily chart. It seems like the pair is consolidating above 1.2200 and is preparing for the next move.

On the upside, a break above the 1.2450 resistance could open the gates for more gains above 1.2500. On the downside, the pair remains supported above the 1.2200 and 1.2150 levels.

This past week in the US, the Durable Goods Orders for Feb 2018 was released by the US Census Bureau. The market was looking for a rise of 1.5% compared with the last reading of -3.7%.

The real outcome was positive as there was an increase of 3.1% in orders. The last reading was revised up from -3.7% to -3.5%. Overall, the result was better than the forecast and helped the US Dollar in the short term.

South Korea the first that got indefinite exemption on US steel tariffs

The South Korea's Ministry of Trade said today that is' exempted from the US steel and aluminum tariffs. However, South Korea now received a quota of around 2.68m tonnes of steel exports. And that is 70% of the annual average of Korean steel exports to the US between 2015-2017. South Korean contributed to 9.7% of US steel imports in 2017.

In the mean time, Both countries also agreed on 20-year extension of Korean pickup trucks, until 2041. US automakers could also bring in 50000 vehicles to South Korean annually, doubling from prior amount of 25000.

That is the first of many US allies to receive an indefinite exemption on the steel and aluminum tariffs. Other six, Argentina, Australia, Brazil, Canada, Mexico and EU are just having the tariffs temporarily suspended.

At this point, there is no news regarding the expemption on Japan and Taiwan, two other major US allies in Asia, yet.

Market Morning Briefing: Dow Looks Weak Below 24000

STOCKS

Dow (23533.20, -1.77%) looks weak below 24000. There could be some slight recovery towards 24000-24500 but overall the downside scope towards 22500 remains open for the longer term. A sustained rise above 24500 could negate immediate downside taking the index back towards a possible upmove. Watch price action near 24000.

Dax (11886.31, -1.77%) is almost headed to test immediate support near 11700 and could then bounce back a bit from there.

Nikkei (20513.63, -0.51%) could get some immediate support near 20200 but it has broken below long term support on the weekly candles and while the index trades lower, there could be chances of a further fall towards 19500 in the longer run. The fall could sustain if Dollar Yen (104.94) does not recover from current levels.

Shanghai (3119.08, -1.07%) fell sharply last week testing weekly support near 3100. Note that this is an important level and a bounce back from here or a break below this would indicate the course of direction for the medium term.

Nifty (9998.05, -1.15%) and Sensex (32596.54, -1.24%) may see some bounce from current levels. Some more scope on the downside is possible towards 9900 and 32250 respectively.

COMMODITIES

Brent (70.25) is headed towards the Jan’18 high of 71.28 and while that holds, the price could see a short term dip towards 69.0-68.50

Nymex WTI (65.54) is also near the Jan-high of 66.65 and could come off from there to levels near 64 in the coming sessions.

A break on the upside is needed for the Crude prices to start a fresh upward rally from here on.

Gold (1348) has been rising for the past 3-sessions and is headed to test resistance near 1354. A break above 1354, if seen immediately would take it higher towards 1360/70 levels; else a fall from 1354 could bring it back to 1330 by end of the week.

Copper (2.9685) is testing important support on the 3-day candle and if that holds, an immediate bounce from here is likely. Else a break below 2.96 could prove to be bearish for the medium term towards 2.90. Recovery in Copper price could come from some recovery in the Chinese stock index.

FOREX

Dollar index (89.43) is trading near crucial support on daily candles and on weekly line chart near 89.3-89.5. It has not been able to break below 89.40 in the last 4 weeks. After Trump’s trade war announcement last week, we could see the Dollar weaken more this week, in which case, the next downside target would be support near 88.5 on daily candles.

Euro (1.2369) has again breached immediate resistance on daily candles near 1.235. If the Dollar weakens this week, it might imply Euro moving towards higher resistance level on 3 day candles near 1.255-1.260.

Dollar Yen (104.95) dipped to a 17 months low last week and is currently trading just above support on daily and 3 day candles near 104.5-104.8. A further break of this support (which is less preferred for this week) would lead to the next downside target being near support on weekly and daily line chart near 103.75.

Euro Yen (129.81) is moving in a downward channel on daily candles. It tested support near 129 on Friday and might again move towards 130.0-130.5 in the next couple of sessions before moving down again. The next crucial downside target would be near 127.5-128.0 which was last seen in Aug ’17 and a break of which, could imply sustained bearishness.

Pound (1.4160) is moving up in a channel on daily candles and might attempt a test of resistance near 1.43 this week. If 1.43 is breached, it could move further up towards 1.46, which is seen as a crucial long term resistance.

Dollar Rupee (65.01) –Let’s watch whether Support at 64.90 holds today or not.

INTEREST RATES

We repeat Friday’s comment: “After the US Fed didn’t put up a sufficiently hawkish stance for US yields to move up, Trump’s announcement of import curbs on China has made investors move away from stocks towards safer bonds, thereby pushing yields down even further.”

Our Treasury report for Mar’18 (available on demand) had predicted a decline in yields after an initial upmove in the days post the rate hike. The decline is currently happening without the initial upmove and might just continue through Apr-May.

US 10 Yr Yield (2.8263%), 30 Yr (3.075%), 5 Yr (2.61%), 2 Yr (2.27%) :

On the short term chart, the 10 Yr yield might rise this week from channel support near 2.8% towards channel resistance near 2.88%-2.90%.

The 30 yr yield should move up further towards 3.10-3.15% in this week from support near 3.04%-3.05%.

The 5 year yield is near support at 2.6% and could see a rise to 2.7% by end of the week.

US yields have been seeing a decline post the Fed rate hike, which could continue in the medium term.

Japan 10 year yield (0.028) broke crucial support near 0.0375-0.0400 on short term charts last week and is currently near horizontal support near 0.03%. We are expecting it to rise back up from these levels towards 0.05% in the next 1-2 weeks.

RBNZ added employment to its mandate. But won’t change Governor Orr’s policy bias

RBNZ jointly announced the policy target agreements with Ministry of Finance today. Employment is now formally added to its mandate. The statement retained price stability as a target. RBNZ should target to keep annual CPI inflation between 1-3% over medium term. And focus is to keep inflation near to the 2% mid-point. Additionally, the with stable general price level maintained, the monetary would "contribute to supporting maximum sustainable employment within the economy."

Overall, the announce is widely expected as a result of the new government's RBNZ review. And, there wouldn't be any change to the neutral to slightly dovish bias of RBNZ as Adrian Orr just take over as the governor.

Here is the full announcement:

Policy Targets Agreement 2018

The Government's economic objective is to improve the wellbeing and living standards of New Zealanders through a sustainable, productive and inclusive economy. Our priority is to move towards a low carbon economy, with a strong diversified export base, that delivers decent jobs with higher wages and reduces inequality and poverty.

Monetary policy plays an important role in supporting the Government's economic objective. The Government expects monetary policy to be directed at achieving and maintaining stability in the general level of prices over the medium term and supporting maximum sustainable employment.

This agreement between the Minister of Finance and the Governor of the Reserve Bank of New Zealand (the Bank) is made under section 9 of the Reserve Bank of New Zealand Act 1989 (the Act). The Minister and the Governor agree as follows:

1. Monetary policy objective

a) Under Section 8 of the Act the Reserve Bank is required to conduct monetary policy with the goal of maintaining a stable general level of prices.

b) The conduct of monetary policy will maintain a stable general level of prices, and contribute to supporting maximum sustainable employment within the economy.

2. Policy target

a) The price stability target will be defined in terms of the All Groups Consumers Price Index (CPI), as published by Statistics New Zealand.

b) For the purpose of this agreement, the policy target shall be to keep future annual CPI inflation between 1 and 3 percent over the medium-term, with a focus on keeping future inflation near the 2 percent mid-point.

c) The Bank will implement a flexible inflation targeting regime. In particular the Bank shall, in pursuing the policy target:

- have regard to the efficiency and soundness of the financial system;

- seek to avoid unnecessary instability in output, employment, interest rates, and the exchange rate; and

- respond to events whose impact on inflation is expected to be temporary in a manner consistent with meeting the medium-term target.

3. Transparency and accountability

a) The Bank shall implement monetary policy in a transparent manner. In addition to the requirements of section 15 of the Act the Bank shall in its Monetary Policy Statement (MPS):

- explain what measures it has taken into account in respect of meeting the requirements of section 2(c) and explain how these matters have been taken into account in its implementation of monetary policy; and

- when inflation outcomes, and/or expected inflation outcomes, are outside of the target range explain the reasons for this; and

- explain how current monetary policy decisions contribute to supporting maximum levels of sustainable employment within the economy.

b) The Bank shall be fully accountable for its judgements and actions in implementing monetary policy.

Hon Grant Robertson

Minister of Finance

Adrian Orr

Governor Designate

Reserve Bank of New Zealand

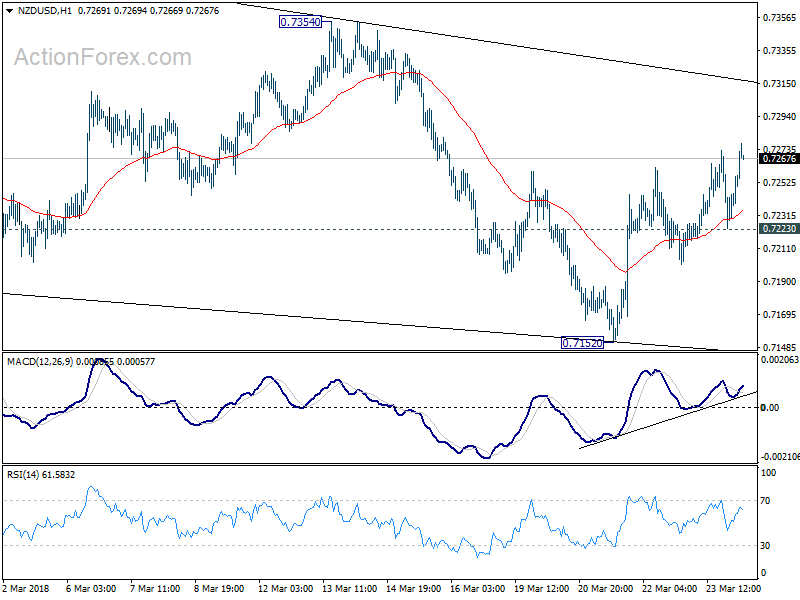

New Zealand trade surplus at NZD 217m in Feb, import hits Feb record high, NZD broadly higher

NZD trades generally higher in Asian session after trade balance data.

Accord to Stats NZ Tatauranga Aotearoa, for February 2018 compared with February 2017:

- Goods exports rose NZD 446 million (11%) to NZD 4.5 billion.

- Goods imports rose NZD 187 million (4.6%) to NZD 4.2 billion, a new high for total imports in a February month. The previous high was NZD 4.1 billion, in February 2017.

- The monthly trade balance was a surplus of NZD 217 million (4.9% of exports).

NZD is trading higher together with commodity currencies in general, as seen in daily heatmap.

Against Dollar, NZD/USD extends the rebound from 0.7152 and reaches as high as 0.7276 so far. Further rise is now mildly in favor to 0.7354 resistance.

Against Dollar, NZD/USD extends the rebound from 0.7152 and reaches as high as 0.7276 so far. Further rise is now mildly in favor to 0.7354 resistance.

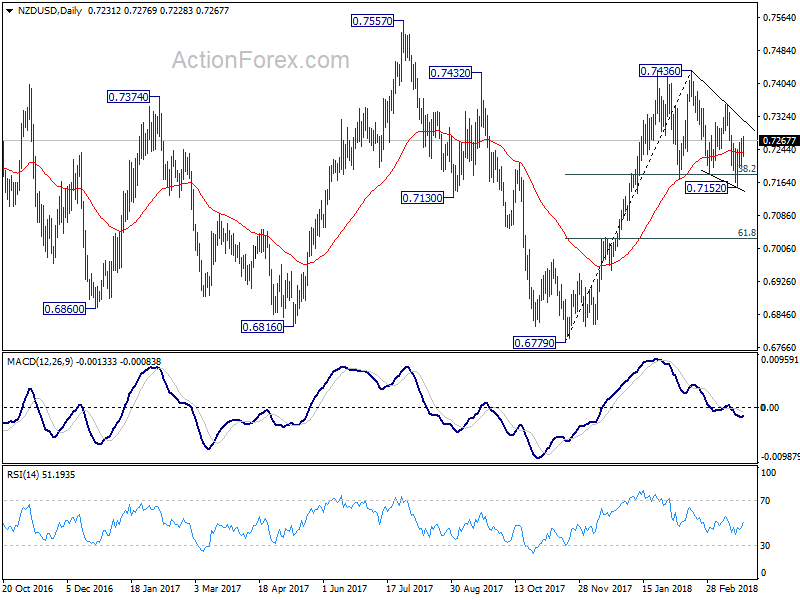

From the daily chart, NZD/USD has been in consolidation since hitting 0.7436. Firm break of 0.7354 will now be a strong signal of resumption of medium term rise from 0.6779.

From the daily chart, NZD/USD has been in consolidation since hitting 0.7436. Firm break of 0.7354 will now be a strong signal of resumption of medium term rise from 0.6779.

Manic Monday Or Just Singing The Stock Market Blues?

Manic Monday or Just Singing the Stock Market Blues?

One thing is for sure: markets are in for a bumpy ride this week as, between the continued trade noise, possible warmongering, month and quarter end rebalancing flow all within a holiday-shortened week, something is bound to go upside down. However, after last week tumult, there's a semblance of calm gripping the market this morning, but price action is more characteristic of the calm before the storm than anything else.

While, it should be quiet on the G-10 central bank and data fronts given the sparse economic calendar, but the proclivity for headline risk remains enormous, and it should make for an exciting week none the less.

On the trade war front, how China escalates will determine the pace of play, but Chinese retaliation so far has been more genial than initially thought, and they have made efforts for a diplomatic solution. Although China is willing to negotiate and is likely to offer compromises, uncertainty and the fear of escalation will likely hold back market sentiment in the short run.

Beyond the apparent quid pro quo, China's ambassador to the US Cui Tiankai did not rule out the possibility of scaling back purchases of Treasuries in response to Trump's tariffs. “We are looking at all options,” he said when asked whether China would consider reduced purchases of Treasuries. “That's why we believe any unilateral and protectionist move would hurt everybody, including the United States itself. It would certainly hurt the daily life of American middle-class people, and the American companies, and the financial markets.”

However, considering the US Bond market is the only game in the town for China, and while they may threaten to reduce US bond purchases as leverage in a possible trade war escalation, it's implausible they will follow through for fear of irreparably eroding the values of their enormous US Bond holdings.Let's face it no one who is watching China intently, thinks China is about to sell a boatload of Treasuries. But as we saw back in January when China reportedly wanted to slow its Treasury purchases, it briefly generated a lot of attention, so something to keep an eye on regardless.

In addition to tariff headlines, having a ” neo-con”( John Bolton) back in the Whitehouse will take the geopolitical risk monitor to another level. With the war drums likely to start beating in Washington again, friend or foe, no one will be immune from his bombastic ideologue and extreme policy views. And as the US is about to enter critical negotiations with North Korea and Iran( once dubbed the Axis of evil when Bolton was working for “Dubbya Bush”), It too appears Trump is taking a no holds barred approach to diplomacy as well.

Backend yields rallied as the probabilities of Trade War with China and a genuine war with North Korea, or Iran has intensified as the foreign affairs policy hawks gain power in the US administration. But historically when you have tanking equity markets and falling bond yields, nothing good ever comes from this type of scenario. Complete risk-off mode!!

With many markets on holiday this Friday, expect liquidity conditions to deteriorate but complicating matters, March's month end also coincides with the quarter end so we could see some non-correlated or complicatedly confusing currency moves. Looking at various Quant models heading into this period, the month-end rebalance act suggests USD buying and selling of all other currencies, primarily the EUR.

Oil Markets

Riyhad came under ballistic missle attack this morning that fortunately, the Army has intercepted. But this is an outright Yemeni escalation which could lead to a massive global supply disruption if Saudi Oil fields are successfully targetting. Oil prices have jumped higher on this escalation in early trade. It's undoubtedly a much more dangerous world we woke up to this morning with the geopolitical warning lights blinking red.

In general, Crude oil prices are on the ups driven by rising geopolitical risk in the Middle East which is threatening global oil supplies. President Donald Trump continues to suggest the US will pull out from Iran nuclear deal which raises the spectre of bringing back sanctions on the country and severely limiting Tehran's ability to export crude oil. But with the appointment of John Bolton as his national security advisor is very bullish for oil markets, it suggests President Trump is now looking to pursue a more hard-line approach with Bolton fanning the flames of the discontent.

And let's not forget those surprising US inventory drawdowns that caught everyone by surprise. Indeed, the confluence of a middle east geopolitical noise with supportive short-term fundamentals has oil traders putting US shale supply concerns on the back burner for now, though the current fundamentals are still set to soften later on this year.

Watershed day for China's oil traders as mainland Oil futures commences trading today.It will be a viable hub given that China has become the most significant global consumer and will eventually provide China with higher weight in pricing Crude distributed in Asia. However, oil habits die hard, and it's doubtful there will be a massive shift of liquidity from traditional exchanges given the fact the contract is priced in Yuan.

The mainland exchange will accept USD as collateral for potentially attracting participation from non-Chinese Oil hedgers and speculators. But unless there is a natural two-way need for Yuan, the futures exchange is more likely to attract local speculator and arbitrage traders rather than anything else at this stage But make no mistake this is China spreading their financial reach, but the petrodollar is under little threat at this stage.

Gold Markets

The spectre of a heated trade war between the U.S. and China has the marketplace unnerved as the accompanying equity market sell-off has increased haven demand exponentially. AS well, having a war-happy neoconservative ( John Bolton) back in the White House brings back memories of the Iraq war and just how quickly a war of words turned into bombs away is an unnerving thought. But even at these elevated price levels, it's hard not to stay long gold with geopolitical risk now registering in the danger zone as an escalation of a trade war and John Bolton's appointment unambiguously raised short-term market risks to a whole new level.

Currency Markets

On the trade war front, currency markets continue to iron themselves out. It's not a case of currency markets taking things in stride, but more a function that longer-term currency e implications aren't so obvious.But the current go-to trades should be abundantly clear by now, Long Gold and Bonds, Short Equities and USDJPY seem to be the favourite cross-asset shelters.

Although Kashkari said on Friday that ” we're not sure why the dollar has been weakening ” I have a few conjectures to add the brewing cauldron of despair. Besides the obvious USDJPY haven appeal; currently, the markets cannot see the forest for the trees. I've been around trading desks long enough to realise that the continuation of easy money policy and the Fed turtling on 2018 monetary policy adjustments is a nasty cocktail for the USD and should lead to the resumption of more widespread dollar weakness over the short term. And, lets not even start about the burgeoning US budget deficit.

G-10

The US Dollar

With the Fed unwilling to move ahead of the curve nor validate the markets hawkish suspicions, the USD should remain in the back foot as they little more than buying some time to ensure they were not walking head first into fatal policy error. But going forward, and considering just how spooky these markets are we could be entering an endless loop of lather, rinse, repeat when it comes to Fed policy

The Japanese Yen

The Yen stands to gain the most from USD weakness and any contraction in global risk appetite. The verbal interventions will be sidestepped and will only provide a better level to by Yen. that is if anyone falls for it. This week we should expect more intense Japanese exporter selling who are underhedged and have been hoping for a dollar rebound ahead of Japan fiscal year end. Also, they're starting forward hedges for the next fiscal year after eventually setting the new budget rate at around 105. Within the context of the Uber risk off the narrative, we should expect more downside on the pair.

The Euro

The market is completely underpricing the EURO. Trade war aside, as s the Fed policy matures, the ECB is only entering the early stages of policy debate. With the USD support capped from policy divergence perspective, the opportunity to ride the shifting ECB policy wave should come back in vogue.

$Asia X Japan

Regardless that the initial size of the tariffs which are much smaller than expected, the fear of escalation is what is driving risk sentiment batty.

The currencies that remain vulnerable on a trade war escalations are KRW and TWD. But with risk aversion taking hold, regional equity market will stay out of favour, and this could envelop the entire regional currency basket in a swarm of negativity.From a current account deficit perspective, IDR and PHP remain incredibly prone why the THB and MYR should remain relatively sheltered form trade war pressures given the stronger current accounts and less vulnerable US trade exposures.

The Malaysian Ringgit

Trade war rhetoric was a major theme over the weekend again and will continue to weigh like an anvil on local equity markets. But the USD continues to trade with a weaker, not against the JPY and EUR and OIL markets remain extremely firm which is providing background support but with traders trying to iron out the actual Trade War implications on FX markets, its unlikely the Ringgit will move off its defensive posture.

The Chinese Yaun

Everyone including their pet dog is focusing on the RMB complex which has fortunately been tracking the USD woes suggesting Chinese authorities are not looking to use the currency to retaliate.But it's more likely given the small economic impact from the US tariffs; the Pboc could reintroduce the counter-cyclical factor to contain RMB bearishness and prevent renewed outflow pressure after all the Trade War rhetoric is a poor eye test for mainland investors.