Sample Category Title

Bitcoin Slide Continues

Over the weekend, the price of bitcoin and other cryptocurrencies continued to slide. Bitcoin reached a low of $7,840 while ethereum traded below $460.

The continued slide was attributed to the recent regulatory announcements and the policy changes by Google and Facebook.

Early this year, Facebook announced that it would ban ICOs and other crypto-related advertisements from its services. Last week, Google followed suit with a clampdown on crypto advertising across all of its ad platforms. Marketing via Twitter is still allowed, however, a similar policy is perhaps to be expected in the near future.

The news directly affects how cryptocurrency networks and ICOs advertise their products. Before the policy changes, companies could expect maximum outreach by creating a Facebook or Google ad – but things have changed. The revised regulations combined with increased scrutiny from regulators and observers make it difficult to see a silver lining in the cryptocurrency industry.

Euro Trade Data Headlines Slow Monday Session

Economic data, monetary policy and geopolitics will headline the financial markets this week. Monday’s release schedule provides only a small taste of what is to come.

Action begins at 09:00 GMT with a report from Italy on industrial output. Factory-level output in the Eurozone’s third-largest economy is forecast to grow 0.8% in January and 1.9% year-over-year. That follows a monthly gain of 1.6% in December.

The Italian government will also report on its February trade balance at 10:00 GMT. Rome posted a trade surplus of €5.252 billion in December.

The European Commission’s statistical agency will also report on its trade balance at 10:00 GMT. The region’s surplus is forecast to narrow slightly to €23.6 billion in January after coming in at €23.8 billion the month before.

Separately, government economists will release euro-wide construction data at 10:00 GMT. Construction output in the 19-member currency region is projected to rise at a seasonally adjusted 0.6% in January, which translates into an annualized gain of 1.3%.

No major North American data releases are scheduled for Monday. On the monetary policy front, Federal Open Market Committee (FOMC) member Raphael Bostic will deliver a speech at 13:00 GMT. Bostic will join the FOMC for its two-day policy meeting in Washington beginning Tuesday.

The US central bank is widely expected to raise interest rates on Wednesday, with the Fed Fund futures prices implying a 94.4% chance of liftoff. The policy announcement will be handed down alongside a quarterly summary of economic projections covering GDP, unemployment and inflation.

In currencies, the U.S. dollar index (DXY) is trading steady at two-week highs on Monday. The greenback returned more than half a percent between Wednesday and Friday.

EUR/USD

Europe’s common currency edged slightly lower at the start of Asian trading, falling 0.1% to 1.2275. The EUR/USD exchange rate has declined nearly 200 pips since 14 March. Initial support is located between 1.2250 and 1.2270. On the opposite side of the spectrum, immediate resistance is located at 1.2345.

GBP/USD

Cable continued to trade within a narrow band on Monday, extending a period of four straight days that saw prices capped between 1.3900 and 1.400. GBP/USD has attempted to retake 1.4000 several times over the past week but has fallen short every time. Current prices are at 1.3937. That psychological barrier remains the key resistance test.

USD/JPY

Despite its recent upward trajectory, the US dollar has struggled to regain its footing against the yen. The USD/JPY is down more than 1% from the 13 March high of 107.23. The pair is currently trading in the low 106.00s, where it faces initial support of 105.25. Positive momentum north of 107.00 will bring the pair back in range with last week’s high.

Equities Fare Decently In The US Session On Friday And USD Strengthened

Market movers today

On a quiet day on the data front, market focus will be on the signals from the UK and European leaders ahead of the EU summit on Thursday and Friday , when the ambition is to formalise the transition deal. At the summit, the EU leaders are expected to approve the EU's guidelines for the framework of the future relationship. Based on recent news stories, it seems like an agreement on transition is just around the corner, as only a few issues remain outstanding.

Furthermore, financial markets will also be looking for further signs of tension between the West and Russia over the poisoning scandal in the UK . Over the weekend, Russia expelled 23 British diplomats in a tit-for-tat response following the UK's expulsion of Russian diplomats last week. Also, global markets will be focusing on the risk of a full-blown global trade war , as US President Donald Trump is likely to announce protectionist measures against China soon.

Finally, attention will start to centre on Wednesday's FOMC meeting where the Fed is widely expected to hike rates. However, the tone it strikes at Jerome Powell's first meeting will be interesting. See FOMC Preview: Sticking to three rate hikes signal for 2018 .

No major scheduled events in the Scandi sphere today.

Selected market news

Market focus likely to continue to be on political developments at the start of the week as not only UK-Russian but also US and Japan struggle on that front . In Russia, President Putin secured a 76% win in yesterday's elections, according to the Kremlin, which also hinted at a high voter turnout due to UK allegations against the country.

Adding to recent US political uncertainty, in a range of tweets over the weekend US president Trump attacked both special counsel Robert Mueller and former FBI Director James Comey . The latter was sacked last spring by Trump and speculation has mounted that Trump may try to oust the former from his investigation into Russian meddling with the 2016 election. This comes after a week in which Trump notably expelled Tillerson as Foreign Secretary.

JPY has appreciated after a poll revealed a significant drop in Japanese Prime Minister Shinzo Abe's approval ratings after recent allegations of foul play within his cabinet. Recent scandals question his backing among voters ahead of this autumn's Liberal Democratic Party leadership contest and raises market concerns of whether the current inflation-oriented policy agenda, including the Bank of Japan's yield curve control, will continue to be pursued.

Equities fare decently in the US session on Friday and USD strengthened, not least after Friday's stronger-than-expected industrial-production figures out of the US. Treasury yields ended the day a few bps higher with not least the 5Y point giving in. The stronger yen weighed on Japanese equities overnight. Brent crude oil prices remain just off USD66/bbl even after a rise in the US rig count.

Asian Market Update: Asian Equities Trade Mixed Ahead Of Key Macro Events

Asian equities trade mixed ahead of key macro events; Short interest rates move higher

Singapore's Noble Group declines over 18% ahead of expected debt default on Tuesday

Hong Kong-listed CK Hutchison Holdings declines as Chairman Li Ka-Shing will retire

China nominates new officials including Finance Minister and PBoC Gov

China Feb New Home Prices decline in major cities; Property shares decline in China and HK

China traded Iron Ore declines over 3% in the face of steel demand concerns

AUD/JPY continues to track decline in Nikkei

Australia 3-month bank bill rate fixed higher for 13th straight session; tracks rise in other short rates

BoJ official noted need to distinguish normalization from monetary tightening (March 8-9th Policy Meeting Summary of Opinions)

BoJ JGB holdings hit fresh record high in Q4

Japan Feb Trade Balance below ests amid higher imports and decline in exports to China

US 2-year Treasury yield rises to highest since 2008 amid US data and focus on this week's FOMC meeting and forecasts (March 20-21st)

US Treasury official clarifies remark regarding trade talks with China ahead of upcoming G20 (March 19-20th)

Australia/New Zealand

ASX 200 opened +0.3%; closed +0.2%

ASX 200 Energy Index +1.7%, REIT +1%, Resources +0.7%; Financials -0.2%

(NZ) NZIER: Raises 2017/18 GDP growth forecast to 2.9% v 2.7%; trims 2018/19 forecast to 3.1% v 3.2% prior

Looking ahead: RBA due to release minutes for March meeting on Tuesday

Australia Feb Employment data and Reserve Bank of New Zealand (RBNZ) rate decision due on Thursday, March 22nd

China/Hong Kong

Hang Seng opens -0.4%, Shanghai Composite -0.2%

Hang Seng Materials Index -1.3%, Property/Construction -1%; Services +0.6%

Shanghai Property Index declines over 1%

(CN) China: Confirms current PBoC Dep Gov Yi Gang nominated as PBoC Gov

(CN) China: Nominates former Vice Fin Min Liu Kun as the new Finance Minister; President Xi's Key Economic Adviser Liu He nominated as Vice Premier; Zhong Shan nominated as China Commerce Minister.

(CN) CHINA FEB PROPERTY PRICES M/M: RISE IN 44 OUT OF 70 CITIES V 52 PRIOR; Y/Y RISE IN 59 OUT OF 70 CITIES v 59 PRIOR

(CN) China Housing Min: Property market remains stable overall, overly fast property price trend 'curbed'; to stick to property control measures

HNA Group said to be planning to sell $2.2B in properties across China - US financial press

(CN) PBoC sets yuan reference rate at 6.3320 v 6.3340 prior

(CN) China PBoC Open Market Operation (OMO): To inject CNY50B in 7 and 14-day reverse repos v skipped prior; Net injection: nil

USD/HKD: Hong Kong (HKD) hits new 33-year low

Japan

Nikkei 225 opened -0.6%: closed -0.9%

TOPIX Securities Index -1.8%, Electric Appliances -1.7%, Real Estate -1.6%, Iron & Steel -1%

Megabanks and Automakers trade generally lower

(JP) Bank of Japan (BoJ) Summary of Opinions for March 8-9th Policy Meeting: One member noted need to distinguish normalization from monetary tightening

(JP) Japan Feb Trade Balance: ¥3.4B v ¥89.1Be; Adjusted Trade Balance: -¥201.5B v -¥90.8Be; Exports to China -9.7% y/y

(JP) Support for PM Abe's Cabinet declines amid Moritomo scandal - Japanese Press Polls

Korea

Kospi opened -0.1%

Hyundai Motor [005380.KR]: Declines over 4% amid reports US officials are probing certain airbag failure related deaths.

(KR) South Korea Finance Ministry sells KRW1.8T in 10-year bonds: avg yield 2.73%

North America

(US) US Treasury Official Malpass said there has been no decision on formal economy talks with China, says he was wrong to say the US ended formal economic dialogue with China – financial press (clarifies earlier comment) [Note: Malpass is originally said to have noted that the Treasury had discontinued the US China Comprehensive Economic Dialogue (CED)]

(US) Trade bodies said to ask the US government to halt planned tariffs against China - US financial press

CSRA Inc [CSRA]: CACI confirms $44/share cash and stock offer (~8% premium to prior close), above $40.75/share cash bid from General Dynamics

Apple [AAPL]: Said to develop displays to replace screens from Samsung; The company is said to have a facility in California which could be used to produce microled screens, which could weigh on suppliers such as Sharp and LG Display - US financial press [Reminder: In June of 2017, it was reported in the Japanese press that Apple was reportedly planning micro-LED displays for its upcoming wearables products]

Europe

(EU) ECB's Weidmann (Germany): Personally thinks that the good economic developments would allow a rapid end to the bond purchases –financial press

(RU) Russia President Putin re-elected for another 6-year term ; received 76% of the vote with most of the ballots counted – Press

(RU) Russia Energy Min: Affirms pledge to see OPEC output cuts deal through to the end; Reiterates willing to prolong cuts if necessary.

Hammerson [HMSO.UK]: Klepierre said to make £5.0B offer - UK Press

Levels as of 01:00ET

Hang Seng +0.1%; Shanghai Composite +0.1%; Kospi -0.7%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.6%, Dax -0.2%; FTSE100 -0.1%

EUR 1.2264 to 1.2292 ; JPY 105.67 to 106.17; AUD 0.7687 to 0.7721 ;NZD 0.7198-0.7229

Feb Gold -0.1% at $1,311/oz; Feb Crude Oil -0.5% at $62.09/brl; Mar Copper -1.1% at $3.079/lb

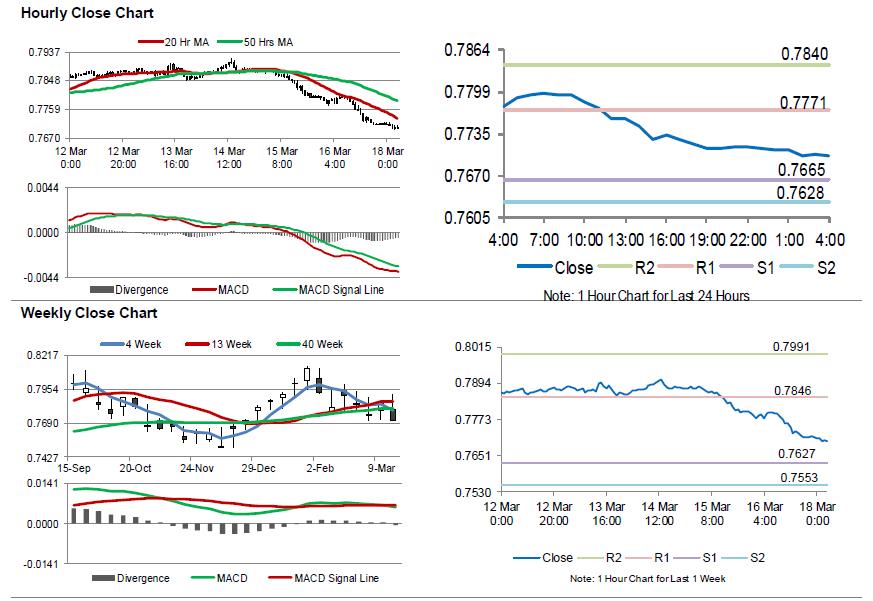

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.98% against the USD and closed at 0.7712 on Friday.

LME Copper prices rose 0.5% or $37.5/MT to $6923.0/MT. Aluminium prices rose 0.3% or $6.5/MT to $2069.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7701, with the AUD trading 0.14% lower against the USD from Friday’s close.

The pair is expected to find support at 0.7665, and a fall through could take it to the next support level of 0.7628. The pair is expected to find its first resistance at 0.7771, and a rise through could take it to the next resistance level of 0.7840.

Going ahead, traders would eye the Reserve Bank of Australia’s (RBA) March meeting minutes, due to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

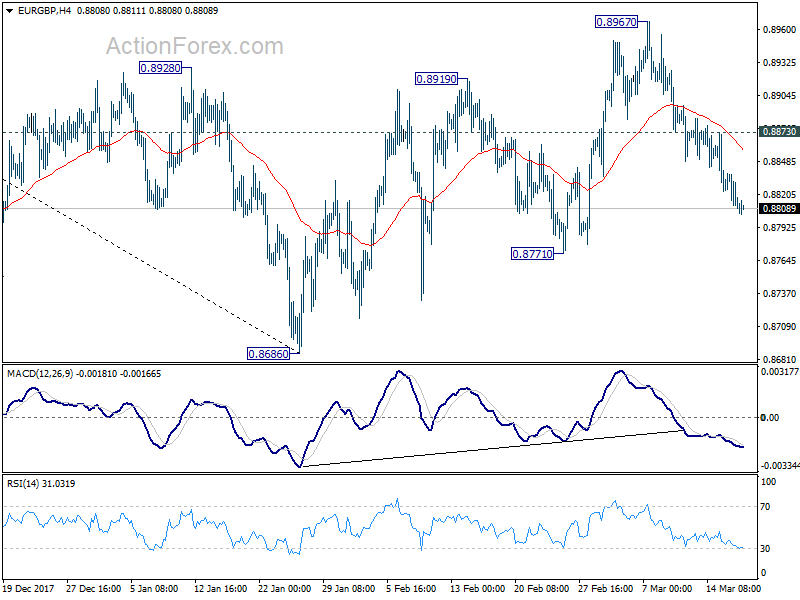

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8797; (P) 0.8817; (R1) 0.8828; More...

Intraday bias in EUR/GBP remains on the downside for 0.8771 support. Firm break there will confirm completion of rebound from 0.8686 and target a retest of this low. On the upside, above 0.8896 minor resistance will turn bias neutral first. Further break of 0.8967 will resume the rebound from 0.8686 to 61.8% retracement of 0.9305 to 0.8686 at 0.9069.

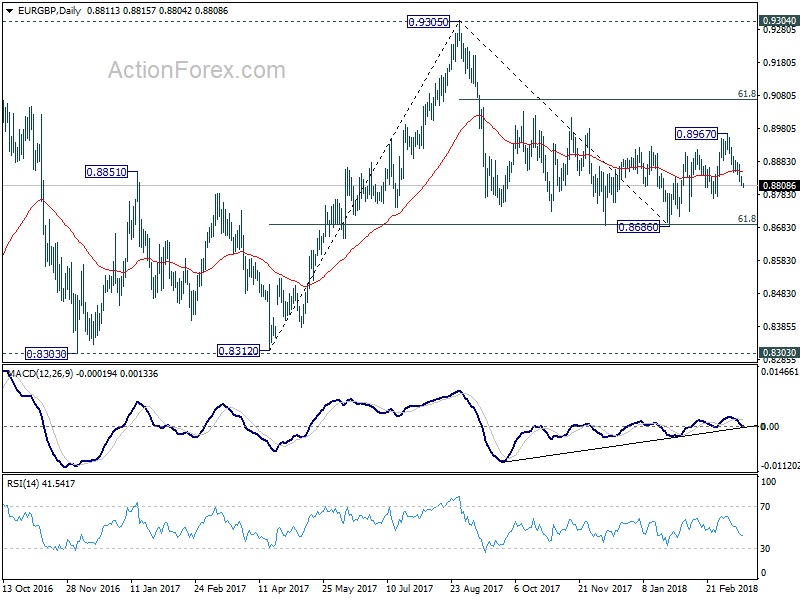

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

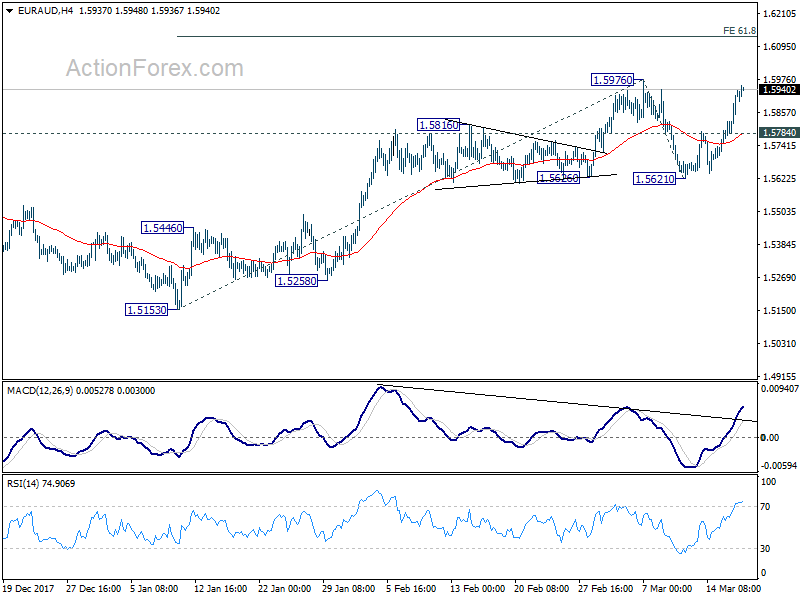

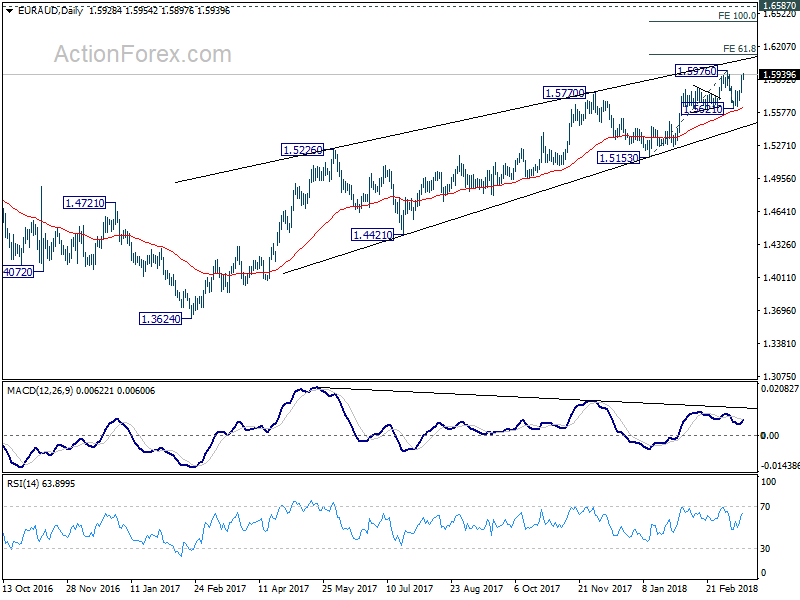

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5816; (P) 1.5876; (R1) 1.5982; More....

Intraday bias in EUR/AUD remains on the upside for 1.5976 resistance first. Decisive break will resume the up trend from 1.3624 and target 61.8% projection of 1.5130 to 1.5976 from 1.5621 at 1.6130 first. On the downside, below 1.5784 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, current development suggests that rise from 1.3624 is not completed yet. And it's still in progress for 1.6587 key resistance level. We'd be cautious on strong resistance from there to limit upside, on bearish divergence condition in daily MACD. But for now, break of 1.5153 support is needed to indicate medium term reversal. Otherwise, outlook will stays bullish even in case of deep pull back.

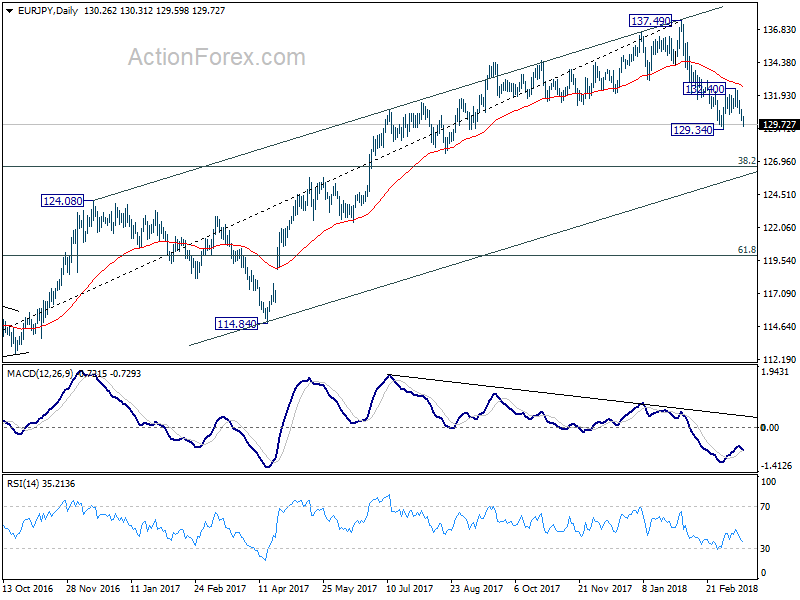

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.88; (P) 130.39; (R1) 130.71; More....

Intraday bias in EUR/JPY remains on the downside for 129.34 low. Decisive break there will confirm resumption of whole fall 137.49 and target 126.61 medium term fibonacci level. In case the corrective pattern from 129.34 extends with one more rise. we'd continue to expect strong resistance from 38.2% retracement of 137.49 to 129.34 at 132.45 to limit upside.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

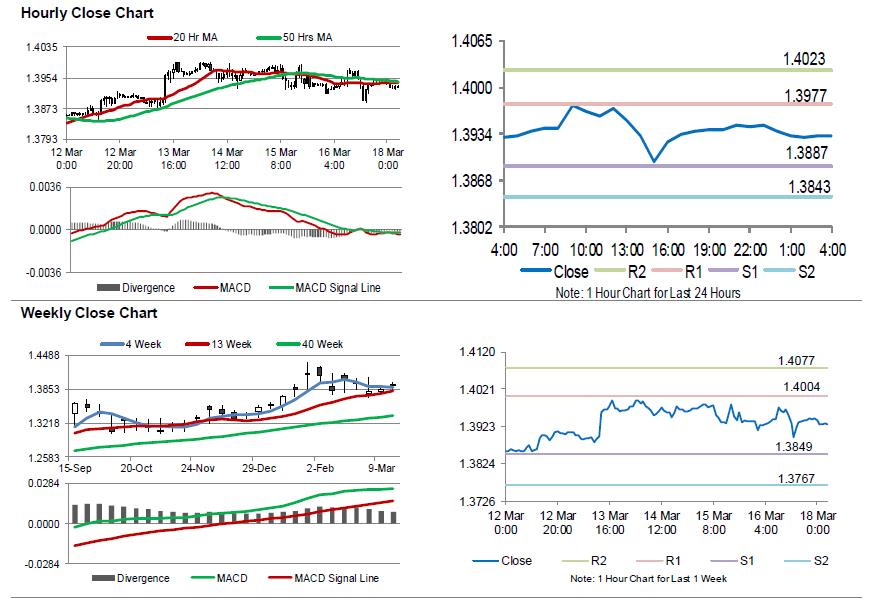

UK’s Rightmove House Prices Advanced In March

For the 24 hours to 23:00 GMT, the GBP rose 0.11% against the USD and closed at 1.3940 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.3930, with the GBP trading 0.07% lower against the USD from Friday’s close.

Overnight data showed that UK’s Rightmove house price index climbed 1.5% on a monthly basis in March, following a gain of 0.8% in the prior month.

The pair is expected to find support at 1.3887, and a fall through could take it to the next support level of 1.3843. The pair is expected to find its first resistance at 1.3977, and a rise through could take it to the next resistance level of 1.4023.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

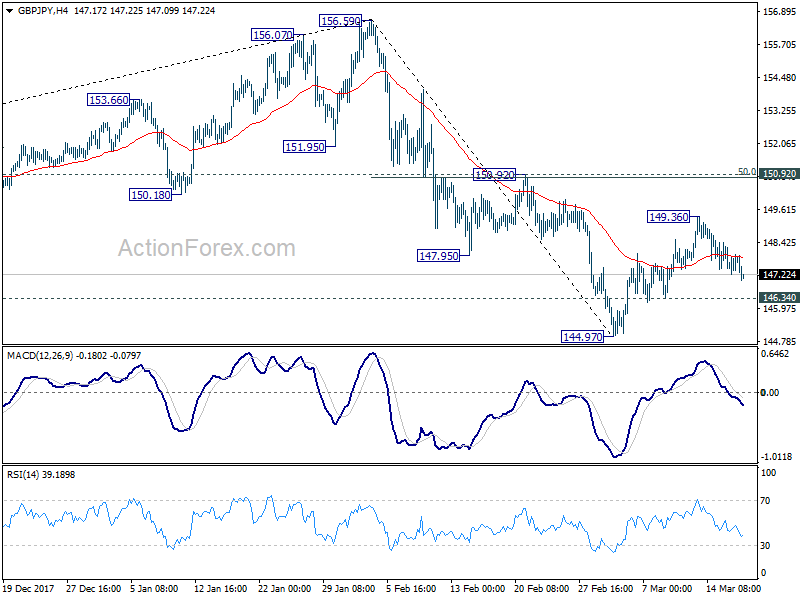

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.23; (P) 147.73; (R1) 148.22; More....

Intraday bias in GBP/JPY remains neutral for the moment. Corrective rise from 144.97 might extend. But in that case, upside should be limited by 150.92 (50% retracement of 156.59 to 144.97 at 150.78 to bring fall resumption. On the downside, below 146.34 minor support will suggest that the recovery has completed. Intraday bias will then be turned back to the downside for 144.97 first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.