Sample Category Title

Trade War a Major Theme in Busy Week of Central Banks, Data and Politics

The week open relatively quietly again with Swiss Franc leading the way down, followed by Aussie and Kiwi. Dollar strengthens broadly but it's again out shone by Japanese Yen. Asian markets are mixed with Nikkei trading down -0.8% at the time of writing. But HK HSI, China SSE are mildly up. The economic calendar is quite light today but volatility ahead is ensured with central bank meetings, important economic data and political events. In particular, Jerome Powell will announce the first Fed hike as chairman. US President Donald Trump could ignore all the objections and announce his tariffs on Chinese goods.

45 trade groups warn Trump: Don't do something commercially meaningless and penalize Americans

45 trade groups wrote an open letter to Trump trying to stop him from starting a trade war with China. In a joint open letter, the group urged Trump's administration to take "measured, commercially meaningful actions consistent with international obligations" and warned Trump not to "penalize the American consumer and jeopardize recent gains in American competitiveness." It's clear to the group of businesses what Trump is trying to do regarding tariff on China is not commercially meaningful.

The group also warned of the "chain reaction of negative consequences" of trade war with China by "provoking" retaliation. And Trump should not respond to unfair Chinese practices and policies by measures that will "harm U.S. companies, workers, farmers, ranchers, consumers, and investors."

In particular, it's listed out in the letter that

- Tariffs on consumer goods would raise price for consumers and business and "negating gains for American workers from U.S. tax reform."

- Tariffs will also harm American companies that "sell component pieces of final products exported from China."

- Also, tariffs would harm community services provides including "health care, education, and emergency responders.

- Tariffs on product components would "disrupting existing supply chains" and have "negative impact on American jobs".

- Tariffs will also depress financial markets.

Additionally, the group warned that "imposition of unilateral tariffs by the Administration would only serve to split the United States from its allies".

Here is a copy of the letter. And here is quick glance on the list of trade groups.

German economic minister Altmaier: Americans are "still" our allies"

German Economy Minister Peter Altmaier will meet with US Commerce Secretary Wilbur Ross this week, and "anyone in Washington who is willing to talk." US steel and aluminum tariffs is the main focus on the trip for Altmaier. He warned that "what's dangerous about the current situation is that it threatens a spiral of one-sided measures that contradict the idea of free trade." And, "that would counter what we've done for the past 60 years. Altmaier also emphasized that "Americans are still our allies" and he'd want to prevent a trade war.

German Finance Minister Olaf Scholz will meet US Treasurer Steven Mnuchin at G20 finance head meeting in Buenos Aires. Scholz told the press that "we must think about how we can ensure growth for the future and of course also how we can keep one of the most important resources for future wealth -- the possibility to trade freely -- stable." And, that's why it would be difficult if protectionism played a bigger role now again."

EU published retaliation list, up to EUR 6.4b of US imports

EU published a list of products for retaliation over US steel and trade tariffs last Friday. The total value of US imports to EU could add up to EUR 6.4b in total. There are two parts in the list. Part A includes goods that are worth EUR 2.8b and EU aim to impose 25% tariff. Part B include products that could be tariffed after three years. It's believed that EU will notify the WTO as soon as possible within a 90-day deadline. For the time being, according to WTO rules, EU can only retaliate up to the amount of EU's steel exports to the US, and thus that EUR 2.8b amount. But EU is making itself ready for further action, playing by the WTO book. Here is the list of products in case you're interested.

Weidmann: Good economic developments allows quick end to QE

Bundesbank President Jens Weidmann said in a German newspaper interview that "I personally think that the good economic developments and the inflation forecast would allow a rapid end to the bond purchases." Weidmann is always felt like the lone hawk in ECB board. Recent comments from other ECB officials generally remained cautious. For example, ECB President Mario Draghi just repeated last week that he still need to see further evidence of prices picking up towards target. And repeated that "monetary policy will remain patient, persistent and prudent." Chief economist Peter Praet said last week that he didn't even prefer to revise the ECB's forward guidance too early.

BoJ: Needs to explain the difference between normalization and tightening

BoJ summary of opinions at March 8-9 policy meeting showed no change in the board's stance on monetary policy. Generally speaking "powerful monetary easing" will be maintained as it's "still a long way" to meet 2% inflation target. There were concerns of Yen's appreciation and stocks' decline as they would "constrain wages and prices" and risk delaying of meeting price target. CPI is expected to "continue on an uptrend" towards 2%, "mainly on the back of an improvement in the output gap and a rise in medium- to long-term inflation expectations." The board also saw the need to explain the difference between "normalization" and "tightening" even though it's not in the phase to consider normalization. That is, normalization is "gradually reducing the degree of monetary accommodation". On the other hand, tightening " aims at reducing the positive output gap." So we'll likely hear more rhetorics from BoJ Governor Haruhiko Kuroda ahead regarding exit. Yet he'll repeat and repeat that it's not there for exit yet.

Released from Japan, trade balance showed JPY -0.2% deficit in February, versus expectation of JPY -0.1T.

Busy week ahead with central banks, data and politics

The week ahead will likely be an exciting one with central banks, economic data and politics featured.

Three central banks will meet this week. Jerome Powell's first FOMC meeting as Fed chair is the major focus. Fed is widely expected to raise federal funds rate by 25bps to 1.75%. Fed fund futures are pricing in 94.4% chance for that and there shouldn't be any surprise. Focus will be on voting and new economic projections. In particular, known dove Chicago Fed Charles Evans might vote against the hike. The famous dot-plot could also reveal whether Fed officials have shifted their base case from three hikes to four hikes this year. BoE and RBNZ rate decision will likely be none events. In addition to that RBA will release meeting minutes while ECB will release monthly bulletin.

In the politics front, G20 meeting will start today with trade war and protectionism as a hot topic. Trump would possibly announce the tariffs on Chinese goods. Tariff talks between EU and US will likely generate some noises. EU is expected to approve the Brexit transition deal with the UK, with conditions attached.

Here are some highlights for the week ahead:

- Tuesday: RBA minutes, Australia house price index; Swiss trade balance, SECO economic forecasts; UK CPI, PPI; German ZEW; Canada wholesale sales

- Wednesday: UK employment; US current account, existing home sales; FOMC rate decision

- Thursday: RBNZ rate decision; Australia employment; Japan PMI manufacturing, all industry index; Eurozone PMIs, ECB bulletin; German Ifo; UK retail sales, BoE rate decision; US jobless claims, PMIs, house price index

- Friday: BoE quarterly bulletin; Canada CPI, retail sales; US durable goods, new home sales

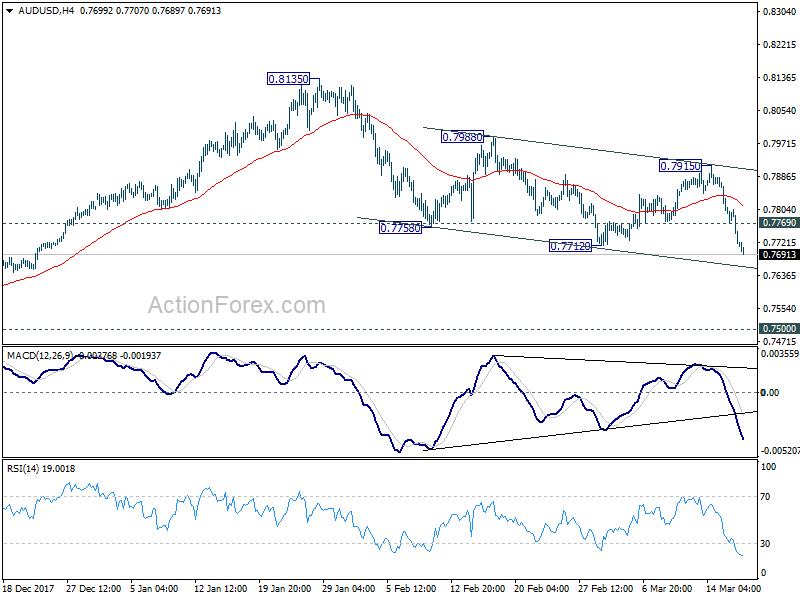

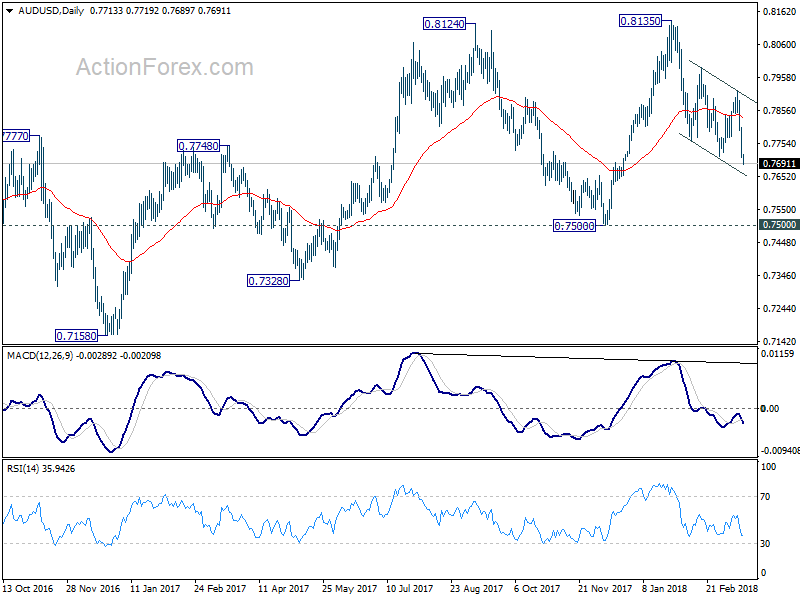

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7678; (P) 0.7740; (R1) 0.7773; More...

AUD/USD's decline continues today and reaches as low as 0.7689 so far. Intraday bias remains on the downside for a test on 0.7500 key support next. We'll keep an eye on sign of downside acceleration to gauge the chance of breaking 0.7500. On the upside, above 0.7769 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 0.7915 resistance holds.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 23:50 | JPY | Trade Balance (JPY) Feb | -0.20T | -0.10T | 0.37T | 0.35T |

| 00:01 | GBP | Rightmove House Prices M/M Mar | 1.50% | 0.80% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 22.6B | 23.8B |

Market Morning Briefing: Euro Yen Is Testing Crucial Support Near 129.75

STOCKS

Dow (24946.51, +0.29%) is stuck near important levels. While there is a medium term resistance just above current levels, there is also a near term support along which the price has been trading for the last 3-sessions. In case the support breaks on the daily candles, the index could be bearish for this week targeting levels near 24500-24000.

Dax (12389.58, +0.36%) is trading below immediate resistance near 12500 and while that holds, the index could be pushed back towards 12000 or lower in the near term. A sustained break above 12500 is needed to indicate an upmove in the medium term.

Nikkei (21465.91, -0.97%) is trading above the 3-day candle support near 21400 and while that holds, medium term looks bullish for Nikkei towards 22600.

Shanghai (3272.80, +0.09%) looks bearish while below 3350. Narrow trade region of 3250-3350 could keep the index stable for the next couple of sessions.

Nifty (10195.15, -1.59%) and Sensex (33176, -1.51%) are trading just near immediate suport levels near 10130 and 32750 respectively and may bounce back in the near term. Note that overall the medium term view is bearish and the indices may resume downtrend after a few sessions.

COMMODITIES

Commodities are trading near import ant levels and could try to move up in the next few sessions.

Brent (65.87) is likely to move up towards 68 gradually while above the 64 support. Whereas the Nymex WTI (62.11) could try an attempt towards 63-64 levels.

Gold (1311.60) broke below the support on the daily candles and while the price continues to trade lower, there could be chances of testing 1300 on the downside.

Copper (3.0790) is trading just near the support of 3.0750 and if that breaks on the downside, the price may move towards 3.05-3.00 in the near term. Thereafter a bounce from there could take it higher towards 3.15-3.17 again.

FOREX

Dollar index (90.282) is close to immediate resistance on daily candles near 90.25-90.30. There is resistance near 90.5 on weekly candles as well which we expect should hold and produce a dip. A lot could depend on the US Fed meeting this week, where a rate hike is expected. Whether a rate hike and a possible rise in US yields subsequently are positive for Dollar strength or not would have to be seen –the usually positive correlation between bond yields and currency strength has not worked for the Dollar in the past 3-4 months and whether this particular rate hike can reinstate the previous correlation would be something to watch out for in the coming weeks. Our preference is for the negative correlation to continue ie for the Dollar to see a dip.

Euro (1.2270) – has immediate support on daily, 3 day and weekly candles in the 1.225-1.230 region from where a bounce should take place. The Euro has been seeing sideways movement in the broad 1.215-1.255 zone for the last 8 weeks. A decisive breakout on the upside beyond 1.255 could be on the cards within the next couple of weeks. For now, we see Euro dipping till 1.225 and then bouncing back up.

Dollar Yen (105.85) seems to be continuing its down move with possible downside target being crucial support near 105.00-104.75 on daily candles. However a testing of the same would imply a break of 105.5, which is a crucial level since the Dollar Yen hasn’t been able to move below it. On the daily line charts, the 13 day and 21 day moving average lines are pushing down the Dollar Yen further.

Euro Yen (129.87) is testing crucial support near 129.75 on 3 day and weekly candles and also on the daily line chart. This support should hold if the Euro continues its sideways movement of the last 8 weeks in this week by bouncing from immediate support levels as mentioned above.

As mentioned on Friday as well, Pound (1.3934) had dipped from resistance near 1.4 on the daily candles and is now moving towards support near 1.39 on 3 day candles. This support is also seen on daily line chart and is likely to hold, thereby producing a bounce.

Dollar Rupee (64.935) was stable on Friday. Support near 64.75/80 is likely to continue holding and the currency pair may head towards 65 or higher this week.

INTEREST RATES

US 10 Yr Yield (2.85), 30 Yr (3.08), 5 Yr (2.65), 2 Yr (2.295) : The US 2 Year Yield had risen to a 9 year high on Friday on the back of positive data on unemployment claims and import prices (which had indicated higher employment and rising prices respectively). Moreover, the Friday data releases showed industrial production rising as well as Capacity Utilization (while Housing Starts saw a decline). However, from the Fed minutes of the last meeting, it would be obvious that capacity utilization is considered as an important variable in one of the inflation models which the Fed considers before arriving at its decision on rates. A growth in Capacity Utilization only provides impetus to the possibility of a rate hike combined with hawkishness from the new Fed chairman in the press conference that follows. Lets wait and watch. US 2 year yield has continued to rise to record highs while longer term yields have seen a 3 basis points increase on average.

Japan 10 Yr Yield (0.038) has fallen slightly below important support on the short term chart around 0.035%. It seems to be moving up again which implies that the support might hold and the yields might again rise.

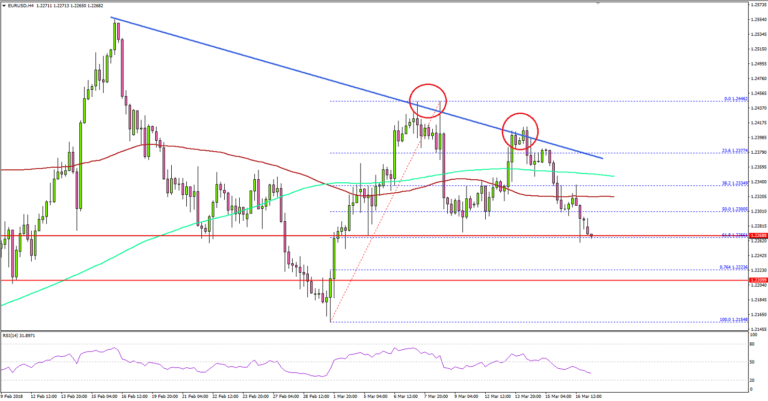

EUR/USD Remains At Risk Of More Downsides

Key Highlights

- The Euro struggled to move above 1.2370 against the US Dollar and declined this past week.

- There is a major bearish trend line forming with resistance at 1.2375 on the 4-hours chart of EUR/USD.

- The US Industrial Production increased 1.1% in Feb 2018 compared with the +0.3% forecast.

- Today, the Euro Zone Trade Balance figure for Jan 2018 will be released, which is forecasted to post a surplus of €23.6B.

EURUSD Technical Analysis

The Euro moved down this past week after it failed to move above the 1.2370 resistance against the US Dollar. The EUR/USD is now trading well below 1.2350 and it remains at a risk of more losses.

There was an upside move this past week from the 1.2285 swing low. However, the pair failed to move above the 1.2380-90 levels and started a downside move. There was a break below the 38.2% Fib retracement level of the last wave from the 1.2154 low to 1.2446 high.

The pair is now trading well below 1.2350 and the 200 simple moving average (green, 4-hour). On the downside, the pair must stay above the 1.2260 support to avoid further declines.

A close below the 1.2260 and 1.2250 support levels could ignite more losses toward the 1.2200 level. On the upside, the pair has to break a major bearish trend line forming with resistance at 1.2375 on the 4-hours chart to gain upside momentum.

This past week, the US Industrial Production report for Feb 2018 was released by the Board of Governors of the Federal Reserve. The market was looking for a 0.3% rise in Feb 2018 compared with the previous month.

The real outcome was better as there was a rise of 1.1% in the Industrial Production, which was also better than the last decline of 0.3%. The report added that:

Manufacturing production increased 1.2 percent in February, its largest gain since October. Mining output jumped 4.3 percent, mostly reflecting strong gains in oil and gas extraction.

The overall market sentiment is favoring the US Dollar and EUR/USD could break the 1.2260 support level in the near term.

Economic Releases to Watch Today

- Euro Zone Trade Balance Jan 2018 – Forecast €23.6B versus €23.8B previous.

- Euro Zone Construction Output Jan 2018 (YoY) – Forecast +1.3%, versus +0.5% previous.

- Euro Zone Construction Output Jan 2018 (MoM) – Forecast +0.6%, versus +0.1% previous.

45 trade groups warn Trump: Don’t do something commercially meaningless and penalize Americans

45 trade groups wrote an open letter to Trump trying to stop him from starting a trade war with China. In a joint open letter: -

The group urged Trump's administration to take "measured, commercially meaningful actions consistent with international obligations" and warned Trump not to "penalize the American consumer and jeopardize recent gains in American competitiveness." It's clear to the group of businesses what Trump is trying to do regarding tariff on China is not commercially meaningful.

The group also warned of the "chain reaction of negative consequences" of trade war with China by "provoking" retaliation. And Trump should not respond to unfair Chinese practices and policies by measures that will "harm U.S. companies, workers, farmers, ranchers, consumers, and investors."

In particular, it's listed out in the letter that

- Tariffs on consumer goods would raise price for consumers and business and "negating gains for American workers from U.S. tax reform." T

- Tariffs will also harm American companies that "sell component pieces of final products exported from China."

- Also, tariffs would harm community services provides including "health care, education, and emergency responders.

- Tariffs on product components would "disrupting existing supply chains" and have "negative impact on American jobs".

- Tariffs will also depress financial markets.

Additionally, the group warned that "imposition of unilateral tariffs by the Administration would only serve to split the United States from its allies".

And below is the list of trade groups:

- Agriculture Transportation Coalition

- Airforwarders Association

- Allied for Startups

- American Apparel & Footwear Association

- AutoCare Association

- CAWA Auto Parts

- Coalition of New England Companies for Trade

- Columbia River Customs & Forwarders

- CompTIA

- Computer and Communications Industry Association

- Consumer Technology Association (CTA)

- Customs Brokers and Forwarders Association of Northern California

- Developers Alliance

- Fashion Accessory Shippers (FASA)

- Gemini Shippers Association

- Grocery Manufacturers Association

- Home Furnishings Association

- Information Technology Industry Council (ITI)

- International Wood Products Association

- Internet Association

- Los Angeles Customs Brokers

- National Customs Brokers and Forwarders Association of America

- National Foreign Trade Council

- National Retail Federation

- NY/NJ Forwarders and Brokers Association

- North American Meat Institute

- Outdoor Industry Association

- Pacific Northwest Asia Shippers Association

- Promotional Products Association International

- Retail Industry Leaders Association (RILA)

- Snowsports Industries America

- Specialty Crop Trade Council

- Sports and Fitness Industry

- Tea Association of the U.S.A., Inc.

- TechNet

- Telecommunications Industry Association (TIA)

- The APP Association (ACT)

- The Pacific Coast Council of Customs Brokers and Freight Forwarders

- The Toy Association

- Travel Goods Association (TGA)

- U.S. Chamber of Commerce

- U.S. Council for International Business

- U.S. Fashion Industry Association

- U.S. Hide, Skin, and Leather Association

- Wine and Spirits Shippers Association

EU published retaliation list, up to EUR 6.4b of US imports

EU published a list of products for retaliation over US steel and trade tariffs last Friday. The total value of US imports to EU could add up to EUR 6.4b in total. There are two parts in the list. Part A includes goods that are worth EUR 2.8b and EU aim to impose 25% tariff. Part B include products that could be tariffed after three years. It's believed that EU will notify the WTO as soon as possible within a 90-day deadline. For the time being, according to WTO rules, EU can only retaliate up to the amount of EU's steel exports to the US, and thus that EUR 2.8b amount. But EU is making itself ready for further action, playing by the WTO book.

Here is the list of products in case you're interested.

German Economy Minister Altmaier: Americans are “still” our allies

German Economy Minister Peter Altmaier will meet with US Commerce Secretary Wilbur Ross this week, and "anyone in Washington who is willing to talk." US steel and aluminum tariffs is the main focus on the trip for Altmaier. He warned that "what's dangerous about the current situation is that it threatens a spiral of one-sided measures that contradict the idea of free trade." And, "that would counter what we've done for the past 60 years. Altmaier also emphasized that "Americans are still our allies" and he'd want to prevent a trade war.

German Finance Minister Olaf Scholz will meet US Treasurer Steven Mnuchin at G20 finance head meeting in Buenos Aires. Scholz told the press that "we must think about how we can ensure growth for the future and of course also how we can keep one of the most important resources for future wealth -- the possibility to trade freely -- stable." And, that's why it would be difficult if protectionism played a bigger role now again."

Bundesbank Weidmann: Good economic developments and inflation forecast allows quick end to asset purchase

Bundesbank President Jens Weidmann said in a German newspaper interview:-

- "I personally think that the good economic developments and the inflation forecast would allow a rapid end to the bond purchases."

Weidmann is always felt like the lone hawk in ECB board. Recent comments from other ECB officials generally remained cautious.

For example, ECB President Mario Draghi just repeated last week that he still need to see further evidence of prices picking up towards target. And repeated that "monetary policy will remain patient, persistent and prudent." Chief economist Peter Praet said last week that he didn't even prefer to revise the ECB's forward guidance too early.

BoJ summary of opinions at March meeting: Need to explain the difference between normalization and tightening

BoJ summary of opinions at March 8-9 policy meeting showed no change in the board's stance on monetary policy. Generally speaking "powerful monetary easing" will be maintained as it's "still a long way" to meet 2% inflation target. There were concerns of Yen's appreciation and stocks' decline as they would "constrain wages and prices" and risk delaying of meeting price target. the board also saw the need to explain the difference between "normalization" and "tightening" even though it's not in the phase to consider normalization. So we'll likely hear more rhetorics from BoJ Governor Haruhiko Kuroda ahead regarding exit. Yet he'll repeat and repeat that it's not there for exit yet.

Some quote highlights:-

- If the current trends of the appreciation of the yen and the decline in stock prices become prolonged, business fixed investment and consumption will be restrained due to negative wealth effects and a deterioration of households' and firms' balance sheets, and the profits of export industries will decrease due to the adverse effects on exports. As these will constrain wages and prices, there will be a risk of a delay in achieving the price stability target.

- The year-on-year rate of change in the consumer price index (CPI) is likely to continue on an uptrend and increase toward 2 percent, mainly on the back of an improvement in the output gap and a rise in medium- to long-term inflation expectations.

- In terms of projecting price developments, the key is to what extent wage developments after the annual spring labor-management wage negotiations will improve individual firms' price-setting stance and consumers' acceptance of price rises.

- Considering that there is still a long way to go to achieve the price stability target of 2 percent, it is appropriate to pursue powerful monetary easing with persistence under the current guideline for market operations in order to firmly maintain the momentum toward achieving the price stability target

- This is not the phase in which the Bank should consider "normalization" -- that is, gradually reducing the degree of monetary accommodation -- in a concrete manner. However, the Bank needs to explain to market participants so that they can fully understand that "normalization" is still in the process of monetary accommodation and completely different from monetary tightening, which aims at reducing the positive output gap. Such explanation will also be beneficial in smoothly proceeding with "normalization" in the future.

- If there is a heightened risk that achieving the price stability target will be delayed, additional monetary easing will be needed

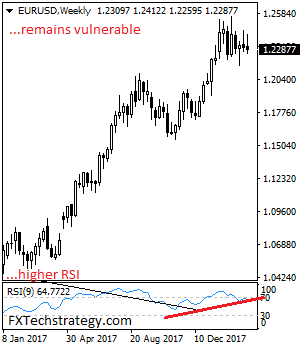

EURUSD – Vulnerable, Threatens Further Weakness

EURUSD - The pair faces further weakness in the new week. On the upside, resistance comes in at 1.2350 level with a cut through here opening the door for more upside towards the 1.2400 level. Further up, resistance lies at the 1.2450 level where a break will expose the 1.2500 level. Conversely, support lies at the 1.2250 level where a violation will aim at the 1.2200 level. A break of here will aim at the 1.2150 level. Below here will open the door for more weakness towards the 1.2100. All in all, EURUSD faces further bear threats.

Struggling To Stay Positive

Struggling to Stay Positive

Markets are struggling to stay positive given the torrents of potential headwinds. Whether it’s the Whitehouse revolving door, an escalation of a global trade war or Japans brewing political scandal, markets are grappling to find an equilibrium.But when you toss in the prospect of a more hawkish Fed, it’s not surprising risk sentiment continues to trade poorly.

Global Foreign Exchange markets are headed for a significant litmus test as traders set sights on Jerome ” Jay” Powell’s first live FOMC decision. .Consensus suggests the hurdle is high for the Fed to shift to four dots, but markets are on guard and with good reason. While a March rate hike is a foregone conclusion, many Fed policymakers have upgraded their growth outlook for 2018, and even Federal Reserve Governor Lael Brainard, one of the central bank’s most fervent doves, sounded optimistic about the U.S. economy’s outlook and suggested the pace of monetary policy tightening may need to accelerate. Given this more hawkish Fed tone, many investors are acknowledging the risk heading into Wednesday’s meeting and reducing interest rate sensitive exposures.

Mind you, this meeting all about forwards guidance. Traders usually will take cues from recent Fedspeak while factoring in the latest growth and inflation metrics as that lays the groundwork typically for an altered official messaging. As for the current disappointing data, especially average hourly earnings, and retail sales, coupled with a tepid core CPI than remains tepid, so therein lies the issues and why gradualism and staying course may frame Jay Powell post FOMC statement. But, he is still an unknown even though his policy views are believed to be close to those of Janet Yellen, Chair Powell could shake things up if he wants to stamp a hawkish lean on this sitting FOMC board.

Currency markets

Outside of Dollar-Yen, the US dollar has been showing a bit of moxy, despite the fact most traders believe it will soon run out of puff post FOMC.

Most are pointing to pre FOMC position reduction for the US dollar unusual amount of stamina.

But this week brings no less than 12 other central bank meetings, various speakers, and critical CPI & jobs reports globally which will keep FX traders hoping, regardless.

The Japanese Yen

The JPY continues to be the beneficiary of the wobbly risk sentiment while the Abe scandal continues to cast a dark cloud over USDJPY, but given that the market is trading as if everyone is short USDJPY we could see some offensive position squeezes higher in this environment. Keep in mind that while risk is trading exceptionally poorly, there is a growing sense that most of the current headwinds will not transpire as severely as feared so this too may factor into some of the pre FOMC position squaring mentality.

The Malaysian Ringgit

The Ringgit struggled last week on repatriation outflows but there increasing acknowledgement and even acceptance for strengthening regional currencies with the Malaysian PM saying USD-MYR could well go to 3.80 in the near-term.

However, this week the local unit will be challenged by a possible move in the FED dots to signal four hikes this year. While the bar remains high for this outcome, investors continue to respect the possibility, but beyond this unlikely outcome and possible repricing of risk, the picture remains positive for the MYR.

Oil prices continue to trade with a firmer bias, and robust demand for MGS bond yield carry suggests the market appetite for Ringgit remains solid.

Gold Prices

For gold prices this week It all boils down to a dovish or hawkish FOMC hike, and on a hawkish lean, most certainly gold will test essential levels of support due to the stronger US dollar implications. But potential market headwinds from the underlying susceptibleness to risk appetite, heightened ( geo) political tensions, inflation concerns Russia tensions, to name a few, could help keep the floor on gold prices in check.

On the physical side of the equation, Asian investors remain incredibly wary of a possible shift in the Fed forward guidance, so demand continues low.

Oil Prices

While inventories continue to see-saw, the oil markets moved higher into the Friday close driven by short covering as the fear of weekend headline risk looms.Despite all the bearish US shale supply headlines, oil prices remain firm as an in the wake of Rex Tillerson’s departure the odds are that the US will pull out for the Iran nuclear agreement continue to run very high.