Sample Category Title

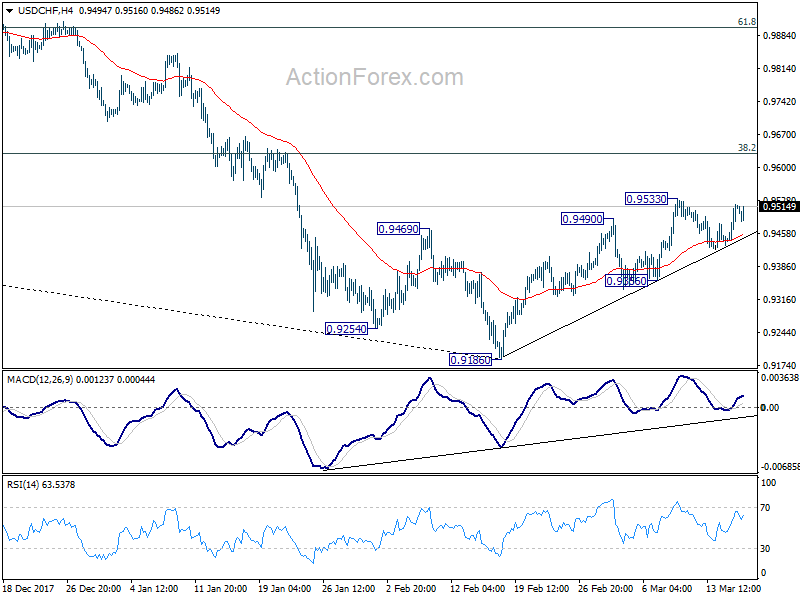

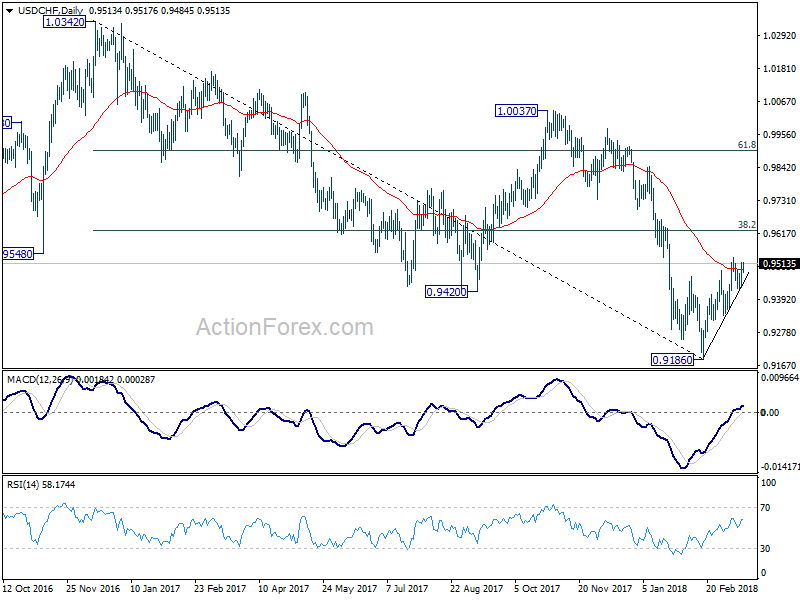

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9458; (P) 0.9488; (R1) 0.9544; More...

USD/CHF is staying below 0.9533 in spite of today's rally. Intraday bias remains neutral at this point. Further rise is in favor as long as 0.9356 support holds. Break of 0.9533 will resume the rebound from 0.9186 and target 0.9626 fibonacci level. However, on the downside, break of 0.9356 will indicate that the rebound has completed. In such case, intraday bias will be turned back to the downside for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

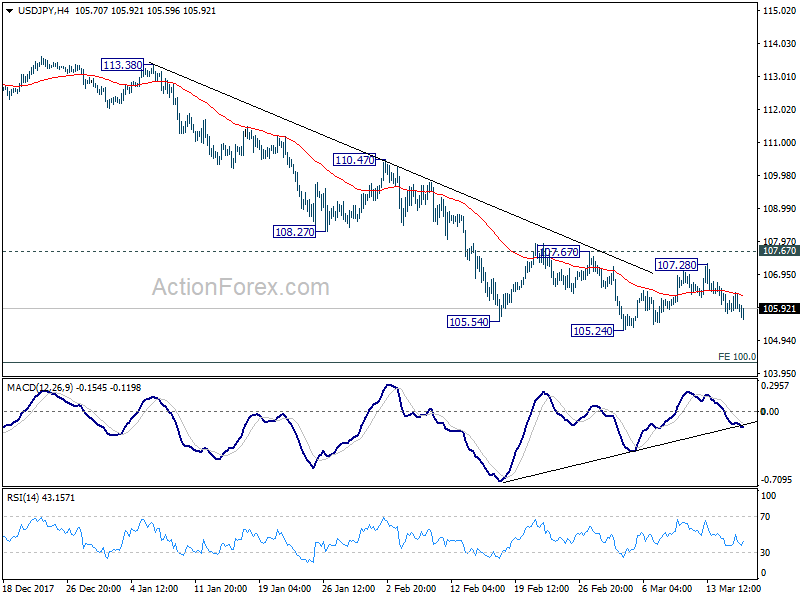

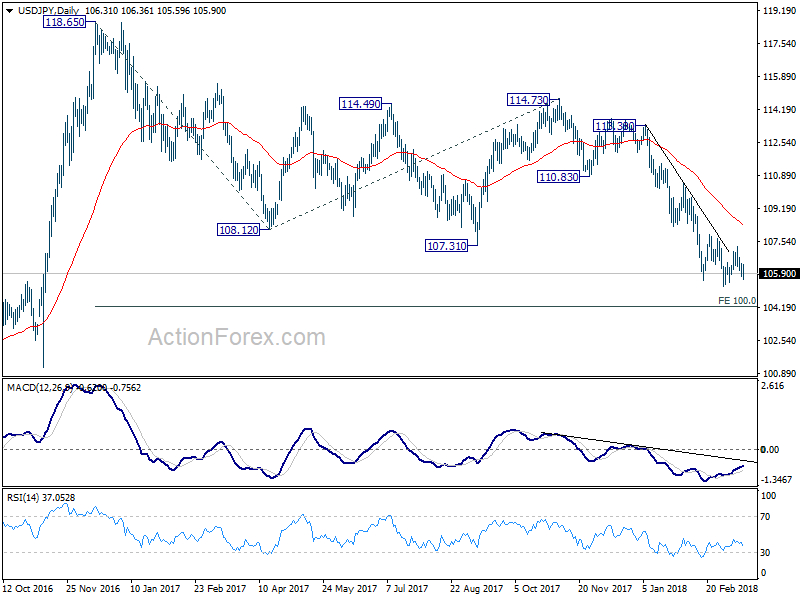

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.94; (P) 106.17; (R1) 106.57; More...

USD/JPY's decline from 107.28 is still in progress but after all, the pair is bounded in range of 105.24/107.67. Intraday bias remains neutral first. Also, Near term outlook remains bearish with 107.67 resistance intact. And deeper decline is in favor. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

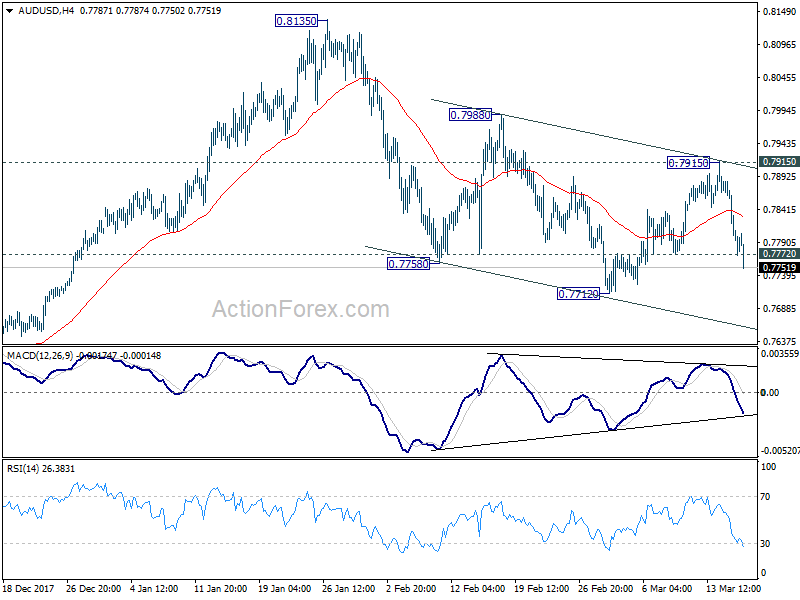

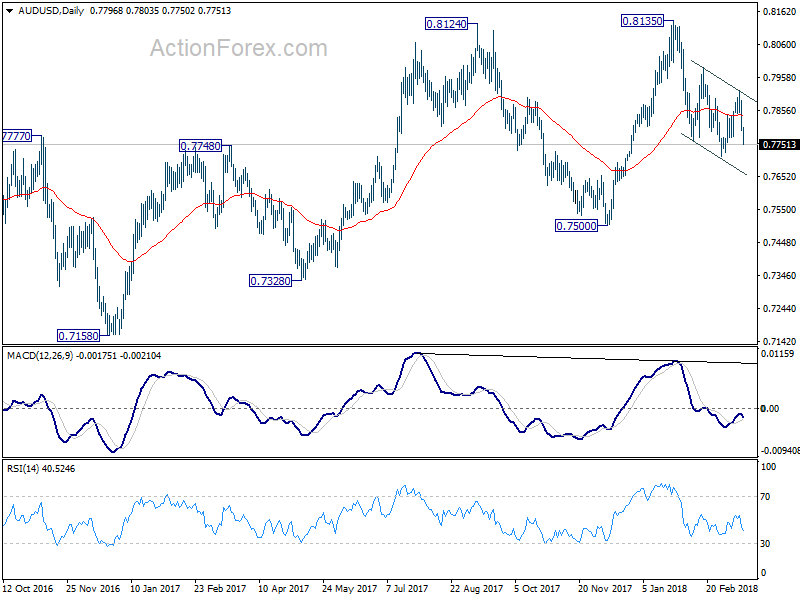

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7766; (P) 0.7825; (R1) 0.7856; More...

AUD/USD's fall from 0.7915 extends to as low as 0.7750 so far in early US session. Break of 0.7772 minor support confirms completion of the rebound from 0.7712. More importantly, fall from 0.8135 is now resuming. Intraday bias is now on the downside for 0.7712 first. Break will pave the way to 0.7500 key support. On the upside, break of 0.7915 is now needed to indicate near term reversal. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Safe Haven Theme Dominates, Yen Strong, Commodity Currencies Weak

Safe haven flows remain the main theme in the forex markets today even though global equities are rather resilient. Yen and to a lesser extend Swiss Franc are trading generally higher. Meanwhile, commodity currencies, Canadian, Australian and New Zealand Dollars suffer most. Fresh selling is indeed seen in early US session on them. Dollar is trading a touch firmer against Euro and Swiss franc. But after all the volatility this week, EUR/USD is holding above 1.2268 minor support well, despite downward revision in Eurozone CPI. GBP/USD is also holding above 1.3873. It's overall, more about selling commodity currencies.

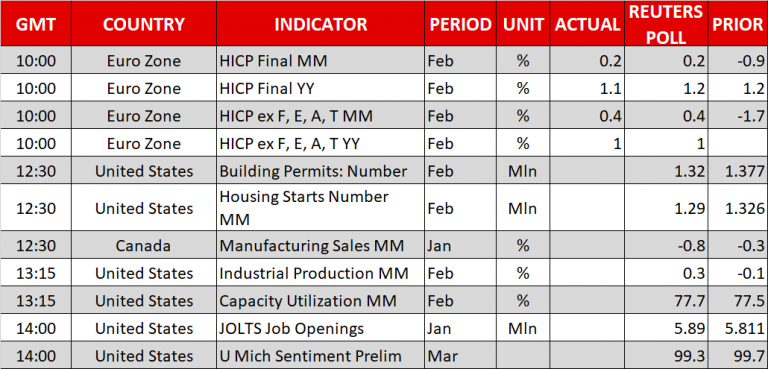

Released from US today, building permits dropped to 1.30m annualized rate in February, housing starts dropped to 1.24m. Industrial production rose 1.1% mom in February while capacity utilization rose to 78.1%. Canada manufacturing sales dropped -1.0% mom in January, international securities transactions rose to CAD 5.68b. Eurozone CPI was revised down to 1.1% yoy in February while core CPI was left unchanged at 1.0% yoy.

ECB Praet prefer not to revise forward guidances too early

ECB chief economist Peter Praet sounds cautious as usual. In the latest ECB meeting, the central bank took away the option to expand the asset purchase program again. But going further, Praet said "I would not revise the guidance too early, because that could send wrong signals about the end of our net asset purchases." And, "I wouldn't say there is a date or a deadline" for the program.

He also added that "it is clear that if you believe that the degree of slack is higher, then the process of convergence to below, but close to, 2 percent over the medium term would be drawn out. " And, "other things being equal, it would (mean a) shallower (inflation path)".

Referring to ECB's pledge to keep interest at current level "well past" end of asset purchase, Praet said "markets quantify the 'well past' interval as 'up to next spring'." And he emphasized that "once you stop net asset purchases the signaling aspect of the asset purchase program disappears and you therefore have to be much more precise about the future path of the short term rates."

EU expects Brexit transition deal to be provisional

An unnamed EU official quoted saying that there will be a transition Brexit deal next week. But that would be provisional. He's quoted saying that while there could be a transition agreement next wee, "it would in any case only be a provisional agreement." And, the transition deal "would be completely dependant on what will be the fate of the withdrawal agreement." The official also emphasized that " if there is no withdrawal agreement, there will be no transition."

It's reported earlier that UK Brexit Secretary David Davis is targeting to complete the legal text of the transition deal at the two-day summit from March 22. However, it's unlikely for a resolution on soft Irish border to be reached. EU proposed a fall back option in its own draft published earlier this month. That is, should there be no compromisable solution, Norther Ireland would stay in the customs union along side Republic of Ireland. But UK Prime Minister Theresa May has instantly and bluntly rejected that idea. Intensive talk is now planned between March 26 and April 18 on the issue.

Businesses in UK would definite request a deal with full clarity. Any conditions in the deal attached to the outcome of Irish border issue would dissatisfy UK businesses and markets.

BoE FPC statement talks Brexit, domestic and global risks

In the statement of March 12 FPC meeting, BoE noted that there are risks related to Brexit, domestic, and global vulnerabilities. In particular, the global risks are principally in "debt markets. It pointed out that "Risks stemming from corporate debt in the United States have continued to build." Also, "financial vulnerabilities in China remain elevated."

For UK, current account deficit "remains larger by international standard" And, recent quarter deficit "has been increasingly funded by capital inflows – rather than sales of foreign assets by UK residents". And that increase UK's reliance on "confidence of foreign investors."

Nonetheless, the statement assured that "UK banking system could continue to support the real economy through a disorderly Brexit." And, "Brexit risks did not warrant additional capital buffers for banks".

Fitch predicts 25bps RBA hike in 2018, 50bps hike in 2019

Fitch rating agency predicts RBA to raise cash rate by 25bps this year. It also predicts another 50bps hike next year in 2019.

What Fitch observed is that RBA appears comfortable lagging behind other central banks in tightening policy, allowing exchange rate flexibility to serve as a buffer". This is in-line with what RBA Governor Stephen Lowe has repeated a couple of times. That is, RBA didn't cut as deep as other global central banks. And therefore, it also doesn't need to reverse that cycle as others like Fed and BoC.

But Fitch expects Australia economy to gain further momentum this year with growth holding steady at 2.7% in 2019. That's thanks to "strong terms of trade on income, broadly accommodative financial conditions and buoyant prospects for investment".

RBA Debelle: Markets underpriced risks of global tightening

RBA Deputy Governor Guy Debelle warned that markets are under pricing the risks of global monetary stimulus remove. He pointed to "equity prices embody a view of the future that robust growth can continue without generating a material increase in inflation." And, "there is little priced in for the risk that this may not turn out to be true." Meanwhile, to him, the market volatility back in February, with sudden selloff in stocks, was just "a small example of what could happen following a larger and more sustained shift upwards in the rate structure." He admitted before wrong in predicting higher volatility before, but added "I think there is a higher probability of being proven correct this time."

NZ PMI suggests Q1 manufacturing GDP similar to Q4's

New Zealand Business NZ manufacturing PMI dropped to 53.4 in February, down from 54.4. Among the sub-indices, production rose 0.4 to 53.9, employment rose 3.3 to 54.8, new orders rose 5.1 to 54.8, deliveries rose 2.9 to 52.7. But finished stocks dropped -1 to 51.1. Bank of New Zealand economist Doug Steel noted in the release that "Q1 manufacturing GDP wouldn't be much different from Q4's based on the "generally slower PMI". Business NZ manufacturing executive director Catherine Beard said pace of expansion had levelled off in recent months and "noted the sluggish start to the year with a dip in new orders being a common message."

IMF Lagarde: Fix economic imbalances with fiscal means, not trade obstacles

IMF Managing Director Christine Lagarde urged politicians to "resolve trade disagreements without resort to exceptional measures". She warned that "trade wars not only hurt global growth, but they are also unwinnable". And, "self-inflicted harm of import tariffs can be substantial even when trade partners do not retaliate with tariffs of their own." She added that " protectionism is pernicious, because it puts the biggest strain on the poorest consumers who buy relatively more low-priced imports." And "harming trade is bad for the economy and bad for people."

She emphasized "the way to address global economic imbalances is not to raise new obstacles to trade." That is, by "using fiscal means to address global imbalances is critical", including "lowering deficits in the US to bring public debt towards a sustainable path, and stronger infrastructure investment and education spending in Germany," At the same time, " those who are adversely affected by globalization and technological progress should receive more support to ensure that they can invest in their skills and transition to higher-quality jobs."

The IMF's Global Prospects and Policy Challenges report also noted that "the global expansion is gaining strength from the pick-up in international trade, and it should not be put at risk by the adoption of inward-looking policies." "The modernization of the rules-based multilateral trade system should continue, anchored in the World Trade Organization, with well-enforced rules that promote competition and a level playing field. Co-operation is also needed to tackle excess global imbalances." The report also warned "the re-emergence of unilateral trade restrictions may escalate tensions and fuel global protectionism, disrupting worldwide supply chains and affecting long-term productivity."

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7766; (P) 0.7825; (R1) 0.7856; More...

AUD/USD's fall from 0.7915 extends to as low as 0.7750 so far in early US session. Break of 0.7772 minor support confirms completion of the rebound from 0.7712. More importantly, fall from 0.8135 is now resuming. Intraday bias is now on the downside for 0.7712 first. Break will pave the way to 0.7500 key support. On the upside, break of 0.7915 is now needed to indicate near term reversal. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Feb | 53.4 | 55.6 | 54.4 | |

| 04:30 | JPY | Industrial Production M/M Jan F | -6.80% | -6.60% | -6.60% | |

| 10:00 | EUR | Eurozone CPI M/M Feb | -0.30% | 0.20% | -0.90% | |

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 1.10% | 1.20% | 1.30% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | 1.00% | 1.00% | 1.00% | |

| 12:30 | CAD | Manufacturing Sales M/M Jan | -1.00% | -0.90% | -0.30% | -0.10% |

| 12:30 | CAD | International Securities Transactions (CAD) Jan | 5.68B | 9.11B | -1.97B | -1.54B |

| 12:30 | USD | Housing Starts Feb | 1.24M | 1.30M | 1.33M | |

| 12:30 | USD | Building Permits Feb | 1.30M | 1.33M | 1.38M | |

| 13:15 | USD | Industrial Production M/M Feb | 1.10% | 0.30% | -0.10% | -0.30% |

| 13:15 | USD | Capacity Utilization Feb | 78.10% | 77.70% | 77.50% | 77.40% |

| 14:00 | USD | U. of Mich. Sentiment (Mar P) | 99.3 | 99.7 |

Merkel criticized Trump’s tariffs as against the WTO principles

German Chancellor Angela Merkel criticized that US President Donald Trump's steel and aluminum tariffs are against the principles of the WTO. And "we want to change or solve these problems via discussions if possible."

At the same occasion, Swiedish Prims Minsiter Stefan Lofven said the tariffs are worrying and regrettable.

AUDUSD – Bears Extend Below 100SMA; Focus 0.7712 Low

The Australian dollar remains in red on Friday and extends strong fall of the previous day, which broke and closed below thick daily cloud, as the Aussie remains under pressure on concerns of trade war.

Friday’s extension lower was sparked risk fresh risk aversion on new turmoil in the US politics.

Bears took out former key support at 0.7773 (100SMA) and Fibo 76.4% of 0.7712/0.7916 upleg at 0.7760, opening way towards 0.7712 (01 Mar low).

Today’s action is capped by broken 20SMA (0.7800) former strong support, turned to resistance and guarding cloud base (0.7817), which should cap extended upticks.

Res: 0.7773; 0.7800; 0.7817; 0.7836

Sup: 0.7725; 0.7712; 0.7664; 0.7634

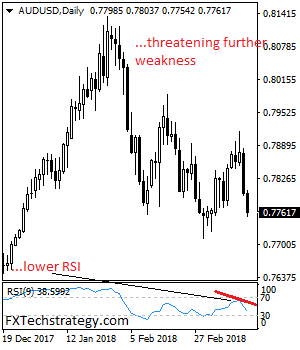

AUDUSD: Bearish, Retains Downside Pressure

AUDUSD. The pair extended its weakness on Friday following its sell off on Thursday. On the downside, support resides at the 0.7700 level where a breach will aim at the 0.7650 level. Below that level will set the stage for a run at the 0.7600 level with a cut through here targeting further downside pressure towards the 0.7550 level. On the upside, resistance lies at the 0.7800 level. A cut through here will turn attention to the 0.7850 level and then the 0.7900 level where a violation will set the stage for a retarget of the 0.7950 level. On the whole, AUDUSD faces further bear threats.

Safe Havens Advance on Political Risks; European Equities Inch Up

Here are the latest developments in global markets:

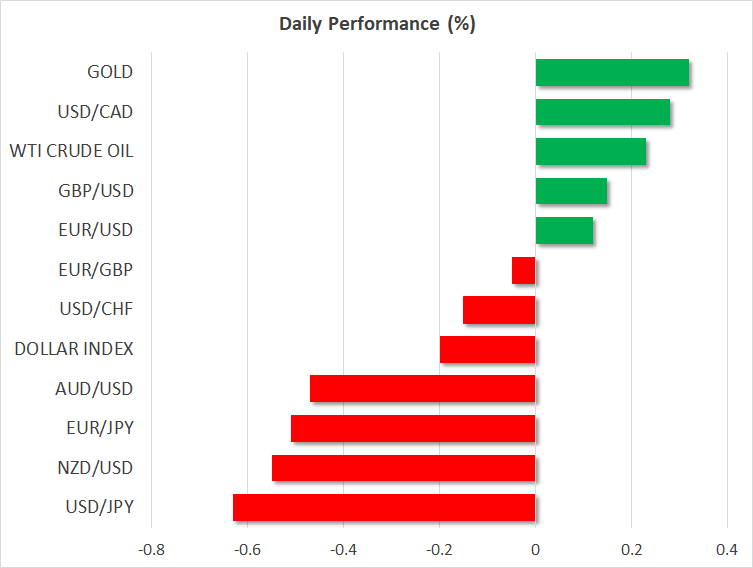

FOREX: Safe-haven currencies continued to benefit from risk aversion, with dollar/yen diving below the 106 key level near one-week lows, last trading at 105.64 (-0.65%). From the one hand, political turmoil in the US was pressuring the dollar after the Washington Post newspaper reported yesterday that the US President has decided to fire his national security adviser, H.R McMaster and was discussing further potential replacements. On the other hand, demand for the yen was also rising on the back of suspicions surrounding the Japanese Finance Minister over his complicity in a state-owned land sale affair. The Swiss franc, another safe asset, was also increasing its positive momentum driving dollar/swissie down to an intraday low of 0.9484 (-0.16%). Euro/dollar crawled up to a high of 1.2335 (+0.13%), in the wake of headlines stating that the US was planning to scrap its punitive import tariffs against Europe. Pound/dollar jumped to 1.3980 (+0.23%) with investors being optimistic that the EU and the UK would strike a deal on the transitional period at next week’s summit in Brussels. Remarks by the rating agency Moody’s regarding the UK economy, however, were not so encouraging as the agency argued that the country will struggle to deliver the public spending cuts it has promised in order to bring down its overload budget deficit. Dollar/loonie reached a fresh 8 ½ -month peak of 1.3090 (+0.09%), underpinned by Trump’s strict views that the US has a trade deficit with Canada. In antipodean currencies, aussie/dollar and kiwi/dollar were struggling and were unable to gain from the dollar’s weakness as any escalation in US-China trade tensions could have a negative influence on the currencies given the country’s heavy export reliance on China. Aussie/dollar and kiwi/dollar were last trading at 0.7760 (-0.50%) and 0.7240 (-0.51%) respectively.

STOCKS: European stocks edged up on Friday supported by positive corporate news but were on track to finish the week in the red as investors were cautious on risk asset purchases amid heightened trade tensions. The pan-European STOXX 600 was up by 0.08% at 1050 GMT, with energy and telecommunications leading the index. Among companies included in the index, the exchange operator NEX Group was the best performer, with its shares rallying at the time of writing by 31.62% after its US-based counterpart CME Group offered to take over the company. The blue-chip Euro 50 increased by 0.39% with all sectors being in the green. The German DAX 30 climbed by 0.53%, the French CAC 40 climbed by 0.07% and the Italian FTSE MIB picked up by 0.09%. UK’s FTSE 100 improved by 0.21% and the US stock futures were mixed.

COMMODITIES:Oil prices extended today’s uptrend but headed for a negative weekly close as worries about the US rising oil production and whether this could hamper OPEC’s efforts to curb oil supply remained a drag on the markets. WTI crude and Brent stood at $61.35 (+0.26%) and $65.18 (+0.09%) per barrel. In precious metals, risk-off sentiment gave a lift to gold, sending the yellow metal to $1321.31 (+0.42%) per ounce.

Day ahead: US data flow continues; US politics in the spotlight

US data will continue to dominate the calendar today ahead of a relatively quiet week for economic releases out of the US. However, today’s numbers are expected to have a little impact on the FOMC rate decision announced on Wednesday, while any updates on the trade story could give another round of volatility for the dollar before a crucial G20 meeting kicks off between March 17-20.

At 1230 GMT, February’s building permits are expected to ease to 1.320 million contracts after reaching a multi-year high of 1.377 million in the previous month. Housing starts, delivered at the same time are also estimated to come in lower in the aforementioned month. On the other hand, readings on industrial production which slowed down by 0.1% in January are now anticipated to grow by 0.3% in monthly terms. Finally, JOLTs job openings for the month of January and the University of Michigan consumer sentiment index for the month of March (preliminary) will inform on the US new vacancies and consumer confidence at 1400 GMT.

While encouraging numbers could bode well for the dollar, positions on the currency could be on the defensive since concerns over a global trade war continue to hang in the background. The recent staff changes in the White House, including the resignation of the economic adviser, Gary Cohn, and the firing of the Secretary of State, Rex Tillerson, and now whispers of a potential departure of the national security adviser, Herbert McMaster, left investors scratching their heads about how serious Trump is about taking a punitive trade stance against the rest of the world. Therefore, any political news that could worsen the already negative sentiment, could offset any gains arising from potentially positive data.

Next week, it will be interesting to see how FOMC members, who will meet to decide on monetary policy between March 20-21, will respond to the trade turbulence. Note that the markets are widely expecting the Fed to pick up rates next week, however, considering the chaos in the White House, we wonder whether the FOMC board will adopt a dovish stance on the country’s economic outlook.

Meanwhile in Canada, January’s manufacturing sales will attract attention at 1230 GMT, while in energy markets, traders will be waiting for Baker Hughes to report on the US oil rig count at 1700 GMT.

Yen broadly higher into US session, CAD/JPY increasing downside bias

Yen staying strongest entering into US session. Commodity currencies are under pressure.

CAD/JPY in down trend across time frame. With increasing intraday downside bias.

CAD/JPY in down trend across time frame. With increasing intraday downside bias.

EU expects Brexit transition deal to be provisional

An unnamed EU official quoted saying that there will be a transition Brexit deal next week. But that would be provisional. He's quoted:

- "There could be an agreement on transition, but it would in any case only be a provisional agreement,"

- "It would be completely dependant on what will be the fate of the withdrawal agreement. Of course, if there is no withdrawal agreement, there will be no transition."

It's reported earlier that UK Brexit Secretary David Davis is targeting to complete the legal text of the transition deal at the two-day summit from March 22.

However, it's unlikely for a resolution on soft Irish border to be reached.

Intensive talk is now planned between March 26 and April 18 on the issue.

So, yes, the best transition deal will be provisional.