Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.95; (P) 106.13; (R1) 106.37; More...

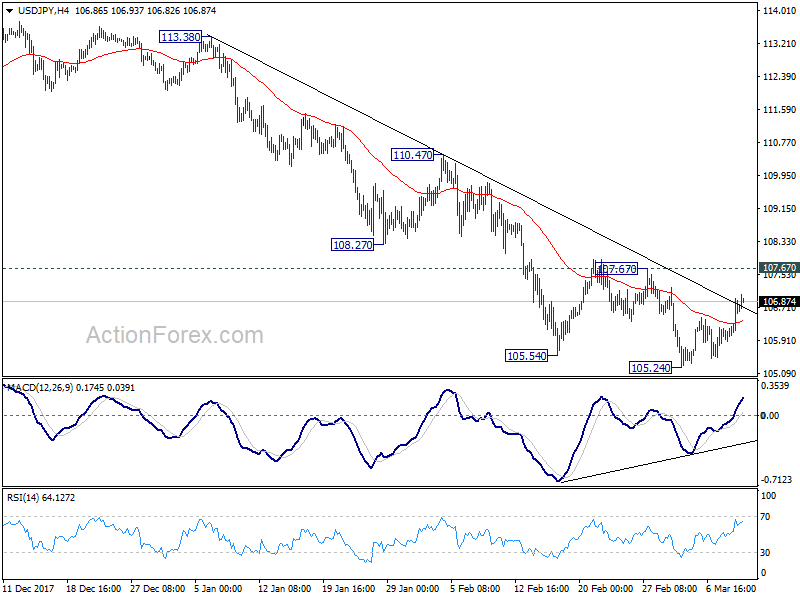

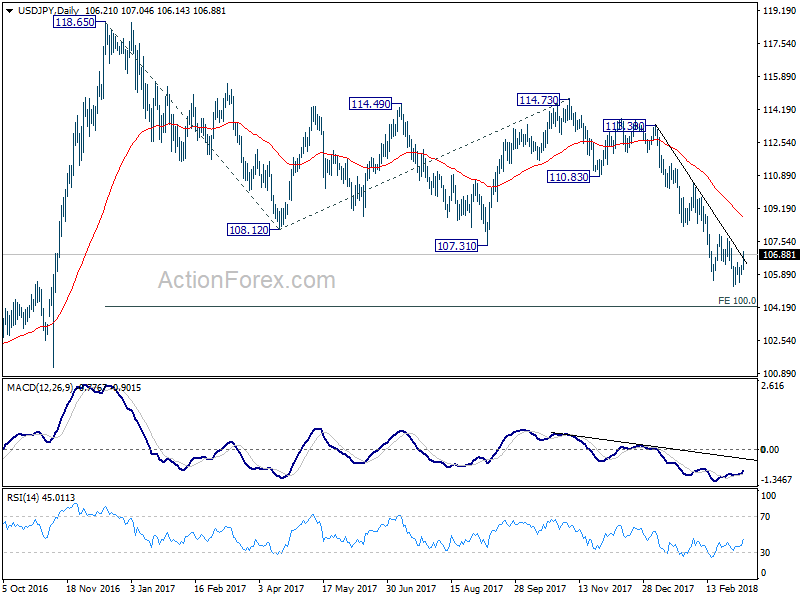

USD/JPY strengthens mildly today but stays well below 107.67 near term resistance. Intraday bias remains neutral first. Considering bullish convergence condition in 4 hour MACD, decisive break 107/67 will indicate near term reversal. In such case, outlook will be turned bullish for 110.47 resistance next. But before that, another decline is still mildly in favor. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

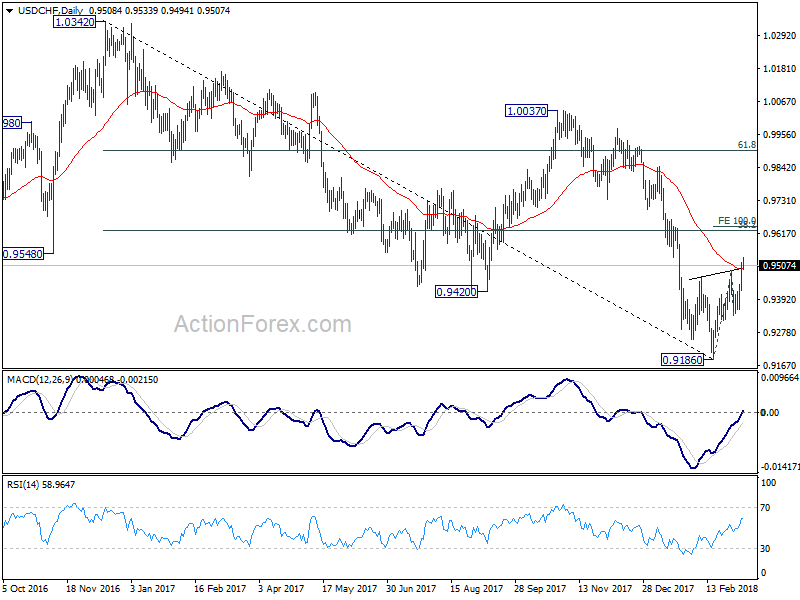

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9448; (P) 0.9484; (R1) 0.9546; More...

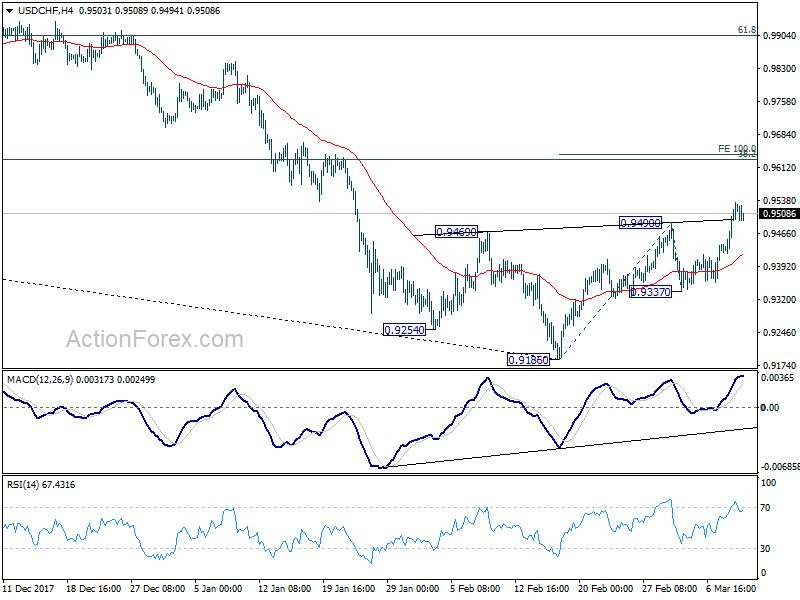

No change in USD/CHF's outlook. Intraday bias stays on the upside for further rally. As noted before, prior break of 0.9490 resistance indicates near term reversal. This is supported by bullish convergence condition in 4 hour MACD. Also, there is a head and shoulder bottom pattern (ls: 0.9254, h: 0.9186, rs: 0.9337). USD/CHF should target 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9641 first. On the downside, break of 0.9337 minor support is needed to indicate completion of the rebound. Otherwise, near term outlook will be cautiously bullish even in case of retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

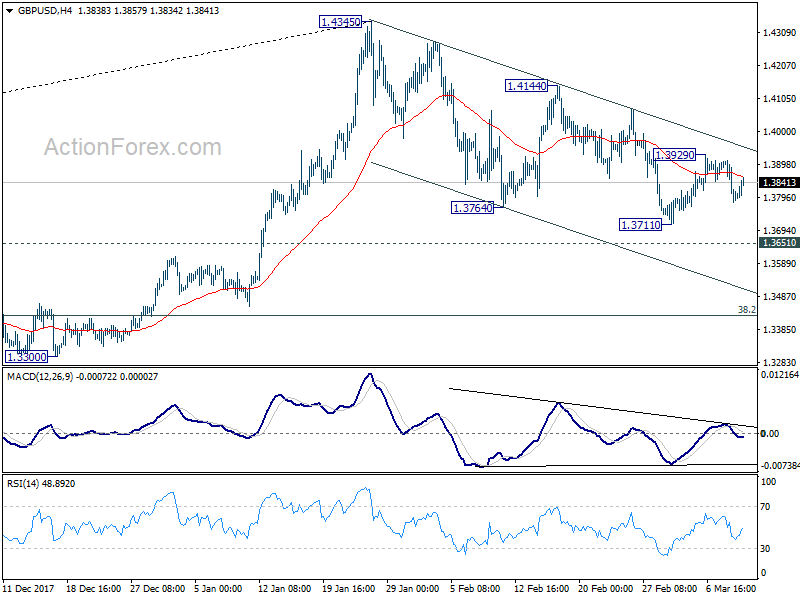

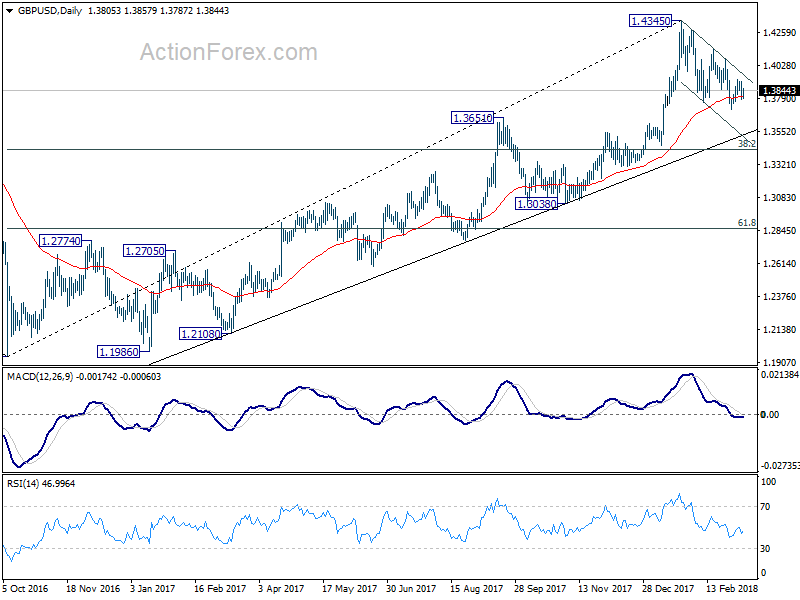

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3757; (P) 1.3833; (R1) 1.3888; More....

GBP/USD recovers today as sideway trading between 1.3711/3929 continues. Intraday bias remains neutral first. Fall from 1.4345 is in favor to extend and break of 1.3711 will target 1.3651 resistance turned support and below. At this point, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound. This will be the favored case as long as 1.3929 holds.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

U.S and Canada Payrolls Strong

Non-farm payroll (NFP)

U.S payrolls rose a seasonally adjusted +313k last month, while the unemployment rate held steady atop of its five month consecutive low of +4.1%.

Note: Market expectations were looking for a +205k headline print and a +4% unemployment rate.

Digging deeper, construction firms’ added +61k, the biggest increase in nearly 11 years for the sector. Hiring also picked up at retailers, manufacturers and local governments, including schools.

The share of Americans participating in the labor force rose by +0.3% to +63.0% m/m.

Revised figures show employers added +239k jobs in January and +175k in December, a net upward revision of +54k.

A tad disappointing were wages – average hourly earnings increased +4c to $26.75. Wages rose +2.6% from a year earlier in February. The annual wage gain in January was revised down to +2.8% increase.

Canada Jobs

Canada Jobs

Canada added a net +15.4k jobs in February on a seasonally adjusted basis, following a net loss of -88k in January. Market expectations were looking for a net gain of +21k. The unemployment rate fell to +5.8% m/m from January’s +5.9%.

Average hourly wages also advanced at a +3% y/y for the second consecutive month.

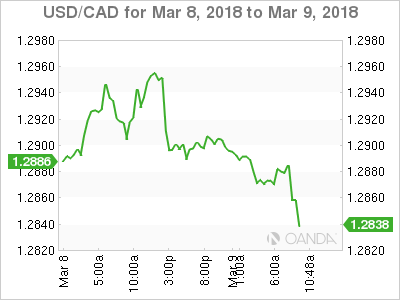

The loonie is off its highs but still up +0.22% at C$1.2866.

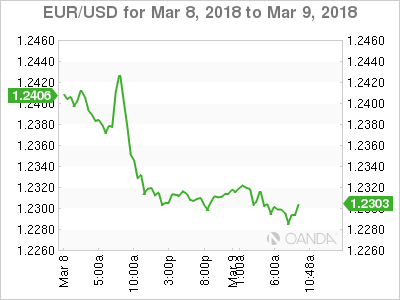

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2257; (P) 1.2351 (R1) 1.2406; More....

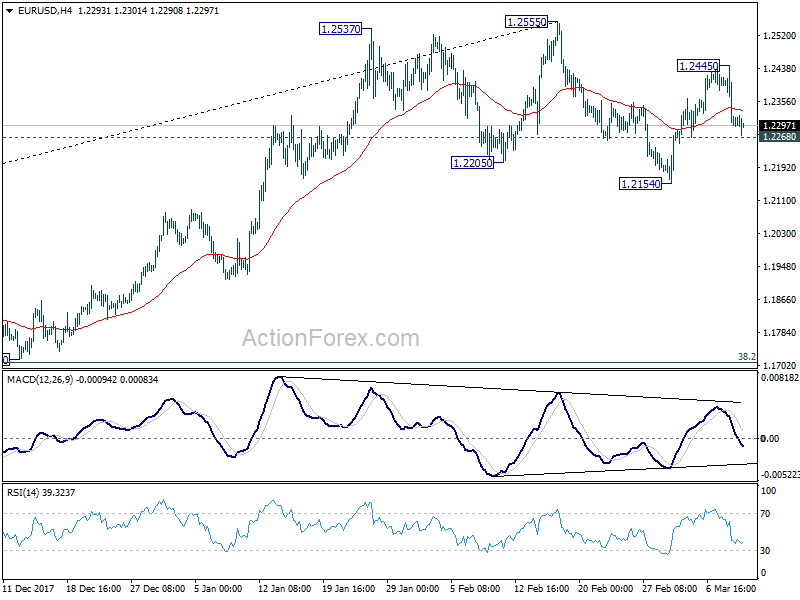

EUR/USD dips in early US session but is still staying above 1.2268 minor support. Intraday bias remains neutral at this point. On the downside, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below. Om the upside, above 1.24455 will turn bias to the upside for retesting 1.2555 key resistance.

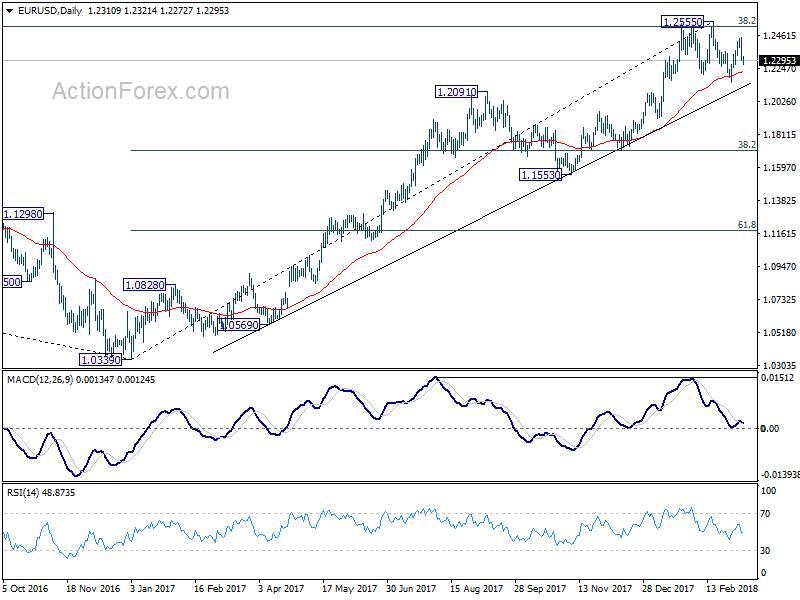

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Fails to Ride on Stellar 313k NFP Growth, Sluggish Wage Drags

Despite stellar report of job growth, Dollar fails to secure upside momentum so far due to sluggish wage growth. Non-farm payrolls report showed 313k growth in February, much better than expectation of 205k. Prior month's figure was also revised up from 200k to 239k. Unemployment rate was unchanged at 4.1%, above expectation 4.0%. Most disappointingly, average hourly earnings rose 0.1% mom only, below expectation of 0.2% mom, slowed from prior months 0.3% mom. The set of data is a repeat of the mystery that many Fed officials have pointed out. That is, strong job growth exists without wage pressure. The report does nothing to secure the chance of a fourth hike by Fed this year.

Released from Canada, the economy added 15.4k jobs in February, below expectation of 21.0k. But unemployment rate dropped to 5.8%, versus expectation of 5.9%.

DOW to take on 25000 again on improved sentiments

There were talks that market sentiments were boosted by breakthrough in tension between the US and North Korea. Politically, the agreement on meeting between US President Donald Trump and North Korean leader Kim Jong-un is welcomed globally. But Nikkei gained a mere 0.47% today. European index are mixed with FTSE trading up 0.25%, DAX Up 0.15% and CAC up 0.42% at the time of writing. Nonetheless, US futures point to higher open and DOW might have another go at 25000 handle.

NAFTA collapse could cost Canada 0.5% reduction in growth in first year

The Conference Board of Canada warned that failure to resolve the difference with the US and ending NAFTA could cost -0.5% reduction in real GDP growth in the first year. And that's even taken a lower exchange rate and easing in monetary policy into consideration. The Canadian economy could also lose as many as 85k jobs the first year.

In case of a NAFTA collapse, Conference Board predicts CAD 3.3b drop in real business spending in the first year. Real exports and imports will decline by -1.8%. Tariffs are predicted to revert to WTO most-favored nation rates. That is, Canadian exports to US would face 2.0% tariff. US exports to Canada would face 2.1% tariff.

Little reaction to European economic data

Markets have little reaction to economic data released in the European session. Released in European session, UK trade deficit narrowed to GBP -12.3b in January, slightly larger than expectation of GBP -12.0b. UK industrial production rose 1.3% mom, 1.6% yoy, vs expectation of 1.5% mom, 1.8% yoy. Manufacturing production rose 0.1% mom, 2.7% yoy, versus expectation of 0.2% mom, 2.8% yoy. UK construction output dropped -3.4% mom in January versus expectation of -0.5% mom. NIESR GDP estimate rose 0.3% in February versus expectation of 0.4%. German trade surplus narrowed slightly to EUR 21.3b in January. German industrial production dropped -0.1% mom in January.

BoJ stands pat. Moderate economic expansion to continue

BoJ left monetary policy unchanged today as widely expected. Short term policy rate is kept at -0.1%. BoJ will continue to purchase assets at a pace of JPY 80T per annum to keep 10 year JGB yields at around 0%. Goushi Kataoka dissented again, continued his push to lower yields on JGBs with maturities longer than 10 years. In the statement, BoJ noted that the economy is "expanding moderately, with a virtuous cycle from income to spending operating". And it expects such "moderate expansion" to continue. Core CPI is expected to "continue on an uptrend and increase toward 2percent". Risks to the outlook include US policies, outcome and Brexit negotiation and geopolitical risks. BoJ maintained the pledge on "continuing expanding the monetary base." until core CPI exceeds 2% and stays above in a "stable manner.

Japan household spending rose 2.0% yoy in January versus expectation of -0.8% yoy. M2 rose 3.3% yoy in February. Labor cash earnings rose 0.7% yoy versus expectation of 0.6% yoy.

From China, CPI jumped sharply to 2.9% yoy in February, up from 1.5% yoy and beat expectation of 2.4% yoy. PPI slowed to 3.7% yoy, down from 4.3% yoy and below expectation of 3.8% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2257; (P) 1.2351 (R1) 1.2406; More....

EUR/USD dips in early US session but is still staying above 1.2268 minor support. Intraday bias remains neutral at this point. On the downside, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below. Om the upside, above 1.24455 will turn bias to the upside for retesting 1.2555 key resistance.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BOJ Monetary Policy Statement | |||||

| 23:30 | JPY | Overall Household Spending Y/Y Jan | 2.00% | -0.80% | -0.10% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Feb | 3.30% | 3.30% | 3.40% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Jan | 0.70% | 0.60% | 0.70% | |

| 01:30 | CNY | CPI Y/Y Feb | 2.90% | 2.40% | 1.50% | |

| 01:30 | CNY | PPI Y/Y Feb | 3.70% | 3.80% | 4.30% | |

| 07:00 | EUR | German Trade Balance Jan | 21.3B | 21.1B | 21.4B | |

| 07:00 | EUR | German Industrial Production M/M Jan | -0.10% | 0.60% | -0.60% | |

| 09:30 | GBP | Visible Trade Balance (GBP) Jan | -12.3B | -12.0B | -13.6B | |

| 09:30 | GBP | Industrial Production M/M Jan | 1.30% | 1.50% | -1.30% | |

| 09:30 | GBP | Industrial Production Y/Y Jan | 1.60% | 1.80% | 0.00% | |

| 09:30 | GBP | Manufacturing Production M/M Jan | 0.10% | 0.20% | 0.30% | |

| 09:30 | GBP | Manufacturing Production Y/Y Jan | 2.70% | 2.80% | 1.40% | |

| 09:30 | GBP | Construction Output M/M Jan | -3.40% | -0.50% | 1.60% | |

| 12:00 | GBP | NIESR GDP Estimate Feb | 0.30% | 0.40% | 0.50% | 0.40% |

| 13:30 | CAD | Net Change in Employment Feb | 15.4K | 21.0K | -88.0K | |

| 13:30 | CAD | Unemployment Rate Feb | 5.80% | 5.90% | 5.90% | |

| 13:30 | USD | Change in Non-farm Payrolls Feb | 313K | 205K | 200K | 239K |

| 13:30 | USD | Unemployment Rate Feb | 4.10% | 4.00% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.10% | 0.20% | 0.30% | |

| 15:00 | USD | Wholesale Inventories M/M (JAN F) | 0.70% | 0.70% |

NAFTA collapse could cost Canada 0.5% reduction in growth in first year

The Conference Board of Canada warned that failure to resolve the difference with the US and ending NAFTA could cost -0.5% reduction in real GDP growth in the first year. And that's even taken a lower exchange rate and easing in monetary policy into consideration. The Canadian economy could also lose as many as 85k jobs the first year.

In case of a NAFTA collapse, Conference Board predicts CAD 3.3b drop in real business spending in the first year. Real exports and imports will decline by -1.8%. Tariffs are predicted to revert to WTO most-favored nation rates. That is, Canadian exports to US would face 2.0% tariff. US exports to Canada would face 2.1% tariff.

Dollar spikes higher on stellar 313k NFP, back down on sluggish wage growth

Dollar spikes higher after stellar 313k NFP growth in Feb. But traders quickly realize that wage growth disappoints. Dollar then reverses the gains. On the other hand, strong buying is seen in CAD as unemployment rate unexpectedly fell.

US job data:-

- NFP Feb: 313k vs exp 205k vs prior 239k (revised up from 200k)

- Unemployment rate Feb: 4.1% vs exp 4.0% vs prior 4.1%

- Average hourly earnings Feb: 0.1% mom vs exp 0.2% mom vs prior 0.3% mom

Canada job data:-

- Employment change: 15.4k vs exp 21.0k vs prior -88.0k

- Unemployment rate Feb: 5.9% vs exp 5.9% vs prior 5.9%

Canadian Dollar Ticks Higher, Key Job Reports Loom

USD/CAD is showing slight losses in the Friday session. In the North American session, USD/CAD is trading at 1.2878, down 0.15% on the day. On Friday, employment data will be in focus on both sides of the border. Canada releases employment change, and the US publishes wage growth and nonfarm payrolls.

Is President Trump baiting his trading partners into an all-out global trade war? After declaring that trade wars are a “good thing”, Trump made good on his tariff threat on Thursday, and signed an order imposing 25% tariffs on steel imports. Canada is the largest exporter of steel to the US, accounting for some 16% of US steel imports. The move could have severely impacted on the Canadian steel industry, but Trump has exempted Canada and Mexico from the tariffs, at least temporarily, drawing a huge sigh of relief from Ottawa. Still fears of an all-out global trade war remain a serious concern for Canada and the resignation of Gary Cohn, a senior economist in the White House who opposed the tariffs, will only dampen investor risk appetite.

The Federal Reserve is widely expected to raise rate four times in 2018, but the Bank of Canada will likely be unable to compete with that kind of pace. The BoC is concerned with economic growth, which slowed in the fourth quarter, as well as uncertainty over NAFTA, which could fall apart if the Trump administration makes good on its threat to withdraw if its demands for more favorable treatment for US goods is not met. The Bank is not expected to raise rates before May, and if the Fed outpaces the BoC on the rate front, the Canadian dollar could lose ground to a more attractive US currency.

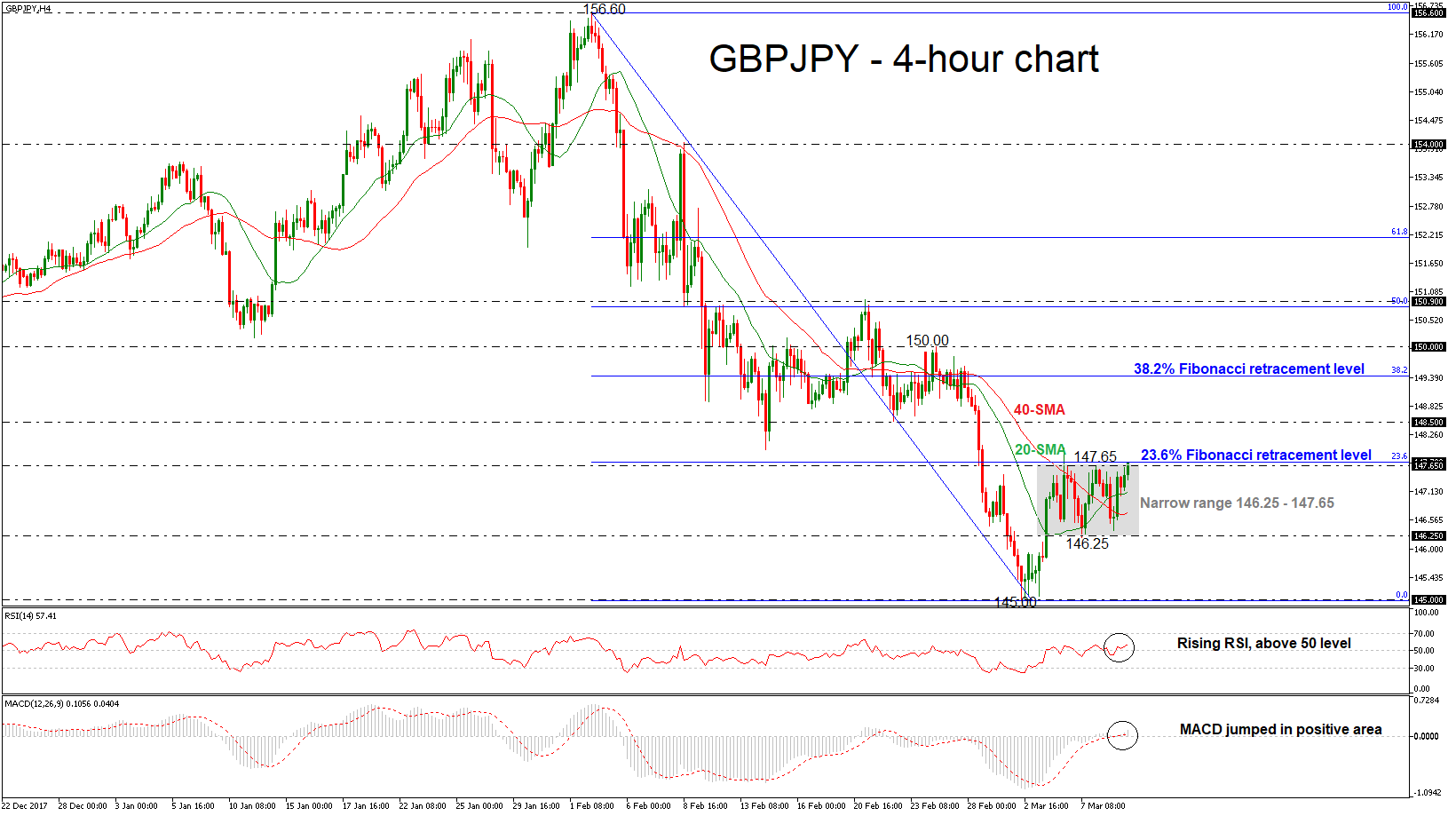

GBPJPY Trades in Narrow Range; Bullish Move is Expected Yntil 148.50

GBPJPY is creating a bullish recovery over the last sessions after it hit a 6-month low near the 145.00 psychological level. The prices jumped above the 20 and 40 simple moving averages in the 4-hour chart and are standing below the 148.00 handle. As a side note, the pair has been holding within a narrow range of 146.25 – 147.65 since March 5 and is trying to jump above this area at the time of writing.

From the technical point of view, the market could increase positive momentum in short-term. The Relative Strength Index (RSI) is sloping up in the bullish territory, while the MACD oscillator entered the positive zone and climbed above its trigger line.

If price action remains positive and rises above the 23.6% Fibonacci retracement level near 147.65 of the downleg from 156.60 to 145.00, the next major resistance to watch is the 148.50 barrier. Further gains could push GBPJPY towards the 38.2% Fibonacci level of 149.40.

Conversely, if the price creates a bearish movement again, then the focus could shift to the downside until the lower boundary of the range at 156.25. If this level is breached, it could increase bearish pressure until the price hits 145.00.