Sample Category Title

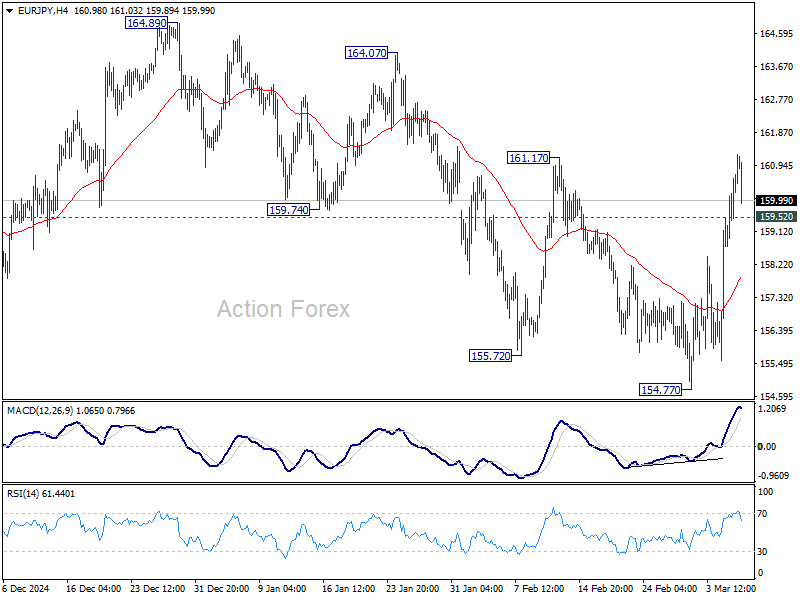

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.32; (P) 160.03; (R1) 161.32; More...

Intraday bias in EUR/JPY stays on the upside for the moment. Rise from 154.77 is seen as another rising leg in the corrective pattern from 154.40. Further rally should be seen towards 164.89 resistance. On the downside, below 159.52 minor support will turn intraday bias neutral first.

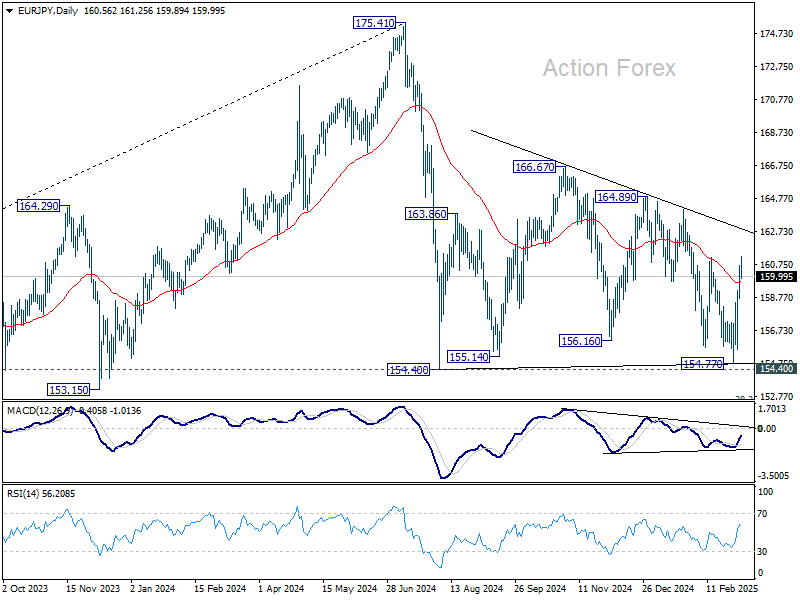

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

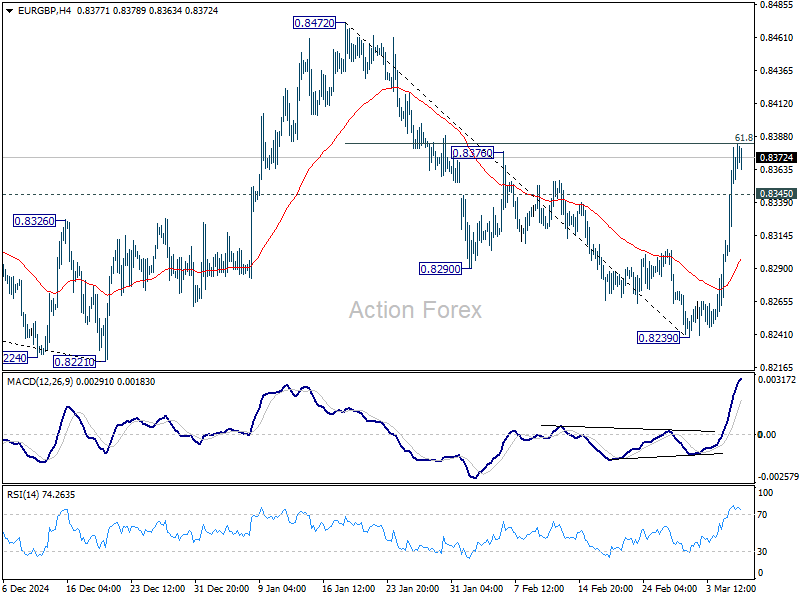

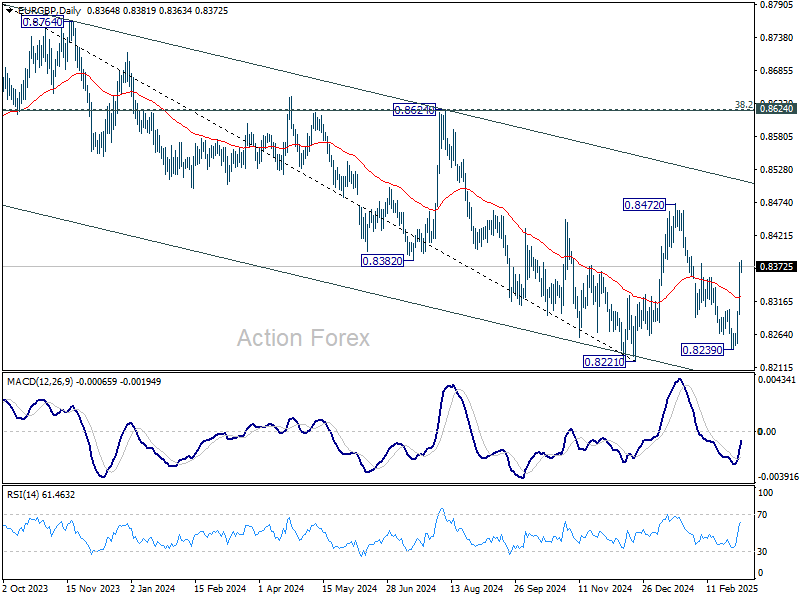

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8316; (P) 0.8349; (R1) 0.8398; More...

Intraday bias in EUR/GBP stays on the upside for the moment. Rise from 0.8239 is seen as the third leg of the pattern from 0.82210. Sustained break of 1.8% retracement of 0.8472 to 0.8239 at 0.8383 will target 0.8472 resistance next. On the downside, below 0.8345 minor support will turn intraday bias neutral first.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8511).

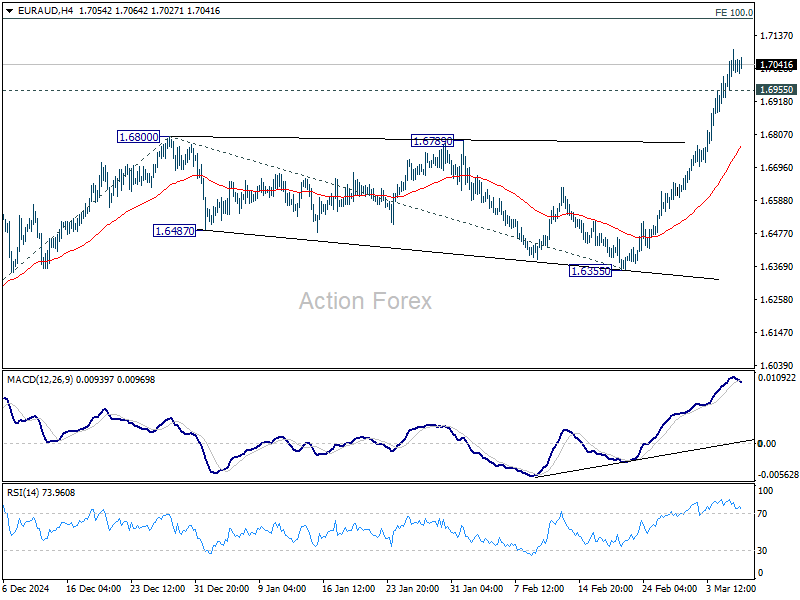

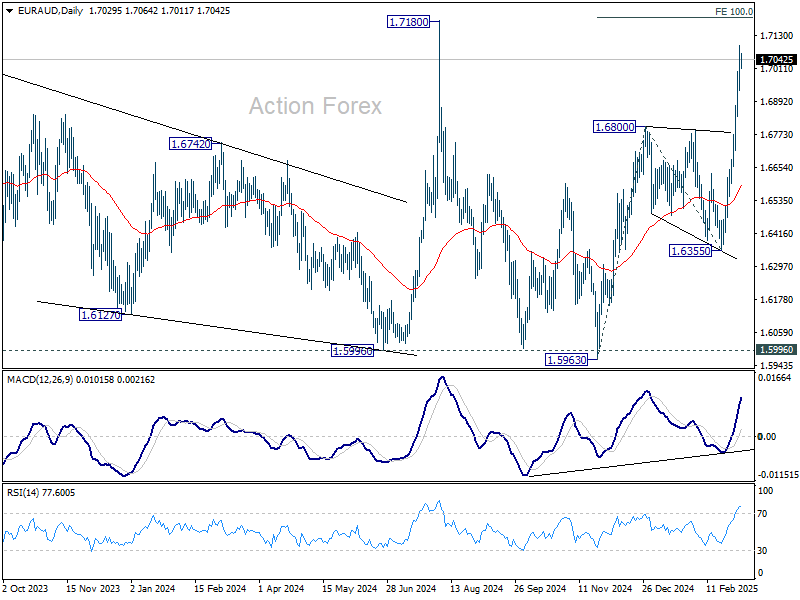

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6944; (P) 1.7019; (R1) 1.7106; More...

Intraday bias in EUR/AUD stays on the upside for the moment. Current rise from 1.5963 should target 100% projection of 1.5963 to 1.6800 from 1.6355 at 1.7192, which is close to 1.7180 high. On the downside, below 1.6955 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

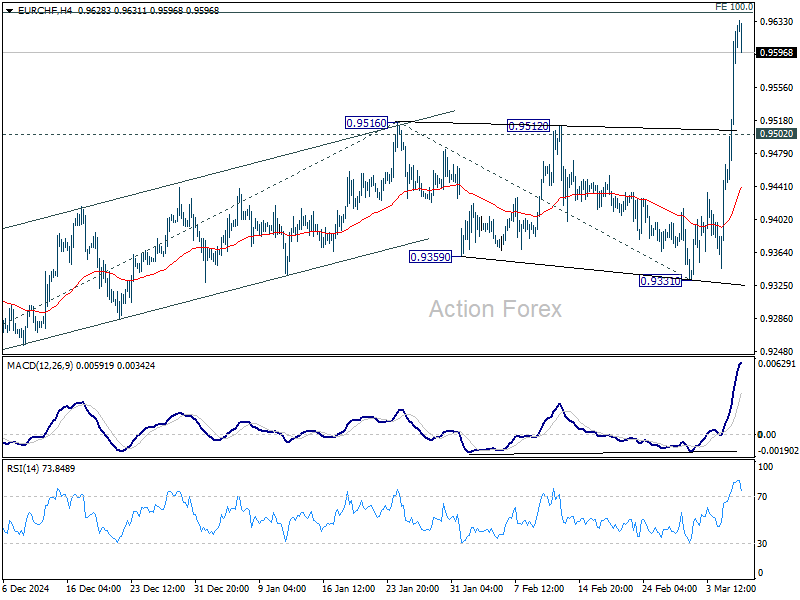

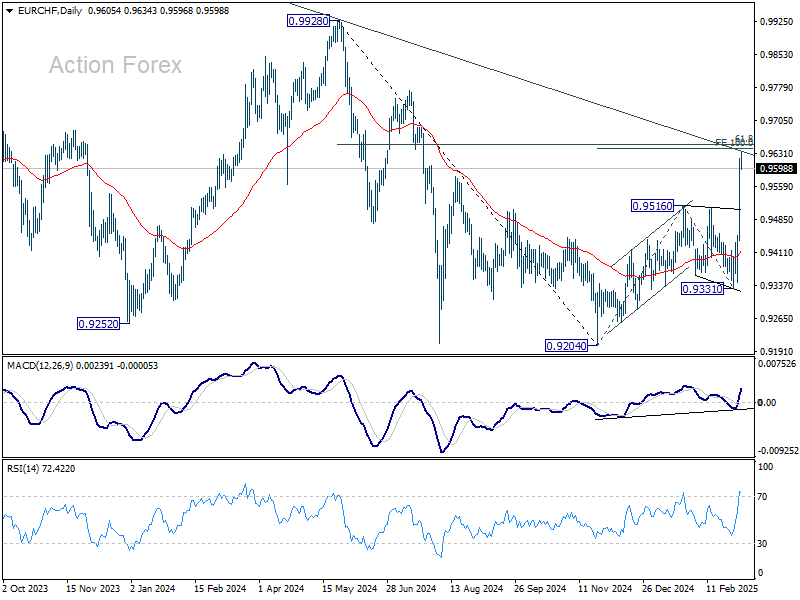

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9491; (P) 0.9557; (R1) 0.9677; More....

Intraday bias in EUR/CHF stays on the upside for the moment. Firm break of 100% projection of 0.8204 to 0.9516 from 0.9331 at 0.9643 will extend the rise from 0.9204 to retest 0.9928 key structural resistance. For now, further rally will remain in favor as long as 0.9516 resistance turned support holds, in case of retreat.

In the bigger picture, the strong break of 55 W EMA (now at 0.9484) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9620) would suggest that the downtrend from 1.2004 (2018 high) has finally bottomed at 0.9204. Further break of 0.9928 will solidify this bullish case, and bring stronger medium term rise even still as a corrective move.

Dollar Declines Ahead of Employment Report Release

The US currency continues to test new lows amid slowing economic growth in the United States and the introduction of new tariffs on China and Canada. Investor disappointment with Trump’s initial executive orders has led to broad-based dollar sell-offs.

USD/JPY

At the start of the week, USD/JPY sellers managed to break a key support level at 149.00–148.60. The price had not fallen below this range since November last year. The downward breakout was followed by a rebound and a retest of the psychological level at 150.00.

Technical analysis of USD/JPY suggests a potential continuation of the downtrend towards 147.00–146.80, as a bearish engulfing pattern is forming on the daily timeframe. To negate the bearish correction scenario, the pair must consolidate above 150.60–150.00.

In the coming trading sessions, the following events could influence USD/JPY pricing:

- Today at 16:30 (GMT+2): US initial jobless claims

- Today at 16:30 (GMT+2): US non-farm productivity

- Today at 21:00 (GMT+2): GDPNow indicator from the Federal Reserve Bank of Atlanta

- Today at 23:30 (GMT+2): Speech by FOMC member C. Waller

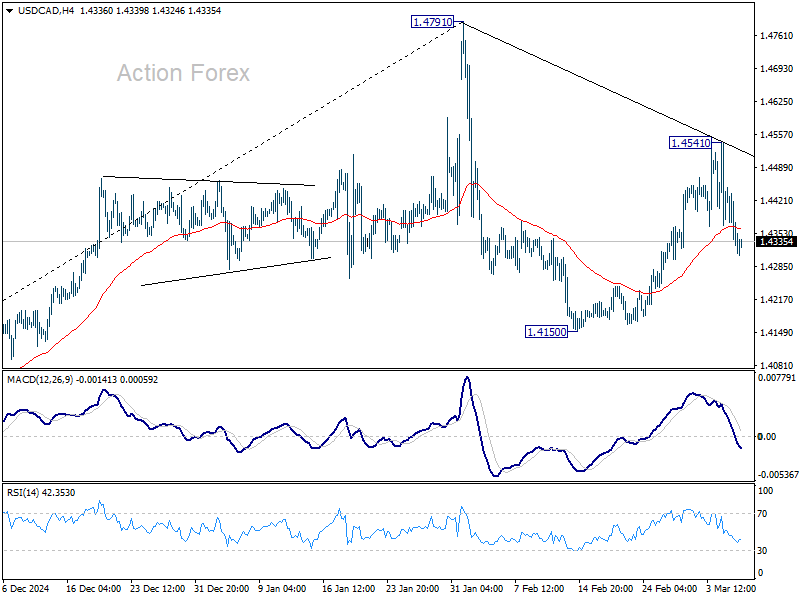

USD/CAD

New tariffs on Canadian goods, introduced two days ago, have driven USD/CAD back towards the 1.4550–1.4500 range. Dollar buyers failed to break above this level, and a subsequent pullback from 1.4550 led to the formation of a bearish engulfing pattern. Technical analysis of USD/CAD indicates a possible downward correction towards 1.4230–1.4170. A resumption of the uptrend is possible if the pair consolidates firmly above 1.4480.

Key events to watch until the end of the week:

- Today at 16:30 (GMT+2): Canada’s trade balance

- Today at 17:00 (GMT+2): Ivey Purchasing Managers’ Index for Canada

- Tomorrow at 16:30 (GMT+2): US average hourly earnings

- Tomorrow at 16:30 (GMT+2): Canada’s employment change

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB Lagarde Will Incorporate Views of Hawkish Wing

Markets

German chancellor-to-be Merz’s fiscal whatever it takes triggered the biggest one-day move in the German 10-yr yield (+29.8 bps) since the reunification in 1990. It tells you something about both the importance of Germany letting go of its longtime devotion to the Schwarz Null and about how forceful they turn the ship in the other direction with a blank cheque for defense spending, a €500bn infrastructure fund and looser debt rules on a state level. German yields on a daily basis rose by 21.6 bps (2-yr) to 30.2 bps (5-yr) with the belly of the curve underperforming the wings. From a technical point of view, the German 10-yr yield took out both the previous 2025 top (2.65%) and the 2024 top (2.71%) with the 2023 top at 3.03% being the next target. The German 10y ASW spread hit a positive 15 bps with more widening (Bund underperformance) to come. The German 30-yr yield (3.08%) moved back above 3%. Apart from a brief spell in Q3 2022, this last happened back in 2011. We stick to the view that yesterday’s move in the Bund market wasn’t a one-off repositioning. The move at the front end of the European curves shows anticipation of the overflow from a looser fiscal policy (pro-growth, inflationary) to a more restrictive monetary policy, given that inflation is still stuck above the ECB’s 2% inflation target. We expect the ECB to lower its deposit rate by another 25 bps today, to 2.5%, while dropping the statement reference that those settings are considered “restrictive” policy. We don’t expect a lot of changes to the GDP & CPI outlook. At the press conference, we think that ECB Lagarde will incorporate the views of the hawkish wing inside the ECB calling for a pause in the current cutting cycle at the April policy meeting, our preferred scenario. Doing so would cause more repositioning in EUR money markets. The expected bottom in the ECB policy rate is currently back around 2%, coming from lower levels at the start of the week. We expect this week’s events to eventually raise it further towards 2.25%. European fiscal events this week served as a catalyst to propel the euro against as US-recession vulnerable USD. EUR/USD started the week at 1.0372 and closed yesterday at 1.0789, rocketing through 1.0533/51 resistance, to currently already test 1.0804 (62% retracement on Sep24-Feb25 decline). We position for a full retracement (1.1214) with a “hawkish ECB cut” likely accompanied by a more dovish tone by Fed chair Powell if he discusses the economic outlook tomorrow evening (payrolls also due with downside risks). Apart from the ECB meeting, there’s the EU Council on defense today which will specify the amounts Europe pledges to Re-Arm and to support Ukraine, but also the way they want to raise them. Expect more muscle flexing here. On the US side, weekly jobless claims and a Fed Waller speech could add to negative US vibes. The White House exempting car makers for tariffs on Mexico and Canada for one month is likely to be insufficient to change that US sentiment. More carveouts could be coming for certain agricultural products. It highlights that the US administration is walking a tightrope between getting what it wants through tariffs and the negative boomerang effect on the US economy.

News & Views

Portugal could have its third early election in less than four years in May. The country’s president put that timing forward yesterday in anticipation of a confidence vote next Wednesday. As things stand now, current prime minister Montenegro’s center-right minority government does not have enough support to survive the motion. The premier is haunted by and failed to quell speculation about potential conflicts of interest related to a company owned by his family. Some opposition parties have tabled a censure motion as recently as February. The biggest of them, the Socialist Party, helped the ruling AD (Democratic Alliance) coalition to defeat it. This time around, though, the socialists have already said they would vote against the government. The AD (30.4%) has 2.4 ppt lead over the socialists in recent polls. The far-right Chega party is third with 18%.

The UK’s Institute for Fiscal Studies, a leading think tank, said chancellor Reeves may soon have to choose which promise she’ll have to break and either raise taxes or return to austerity. The UK presents an update to the budget in its spring forecast on March 26. Since outlining the first Labour budget last October, however, borrowing costs rose sharply (including yesterday’s 15 bps) while the economic outlook deteriorated. This will be reflected in the budget watchdog’s (OBR) new forecasts and will all but certain wipe out the £10bn in fiscal headroom Reeves had projected in order to still comply with the self-imposed budget rules. One of these rules imply that day-to-day spending must be met by revenues.

Rising European Growth Expectations Favour Euro, European Assets

US President Donald Trump said that the tariffs that concern the North American car industry will be delayed by a month... a day after he imposed 25% levies on all Mexican and Canadian imports. Global markets welcomed Trump’s move to turn a threat into reality and then roll it back—arguably a better outcome than imposing and sticking to 25% tariffs. However, the uncertainty and lack of seriousness in these decisions will undoubtedly have a sizeable impact on US growth.

In the markets, the car stocks rebounded yesterday on delayed tariffs. The Mexican and Canadian investors were relieved, mood in Europe was significantly better, as well. The Stoxx 600 recovered 0.91% while the DAX jumped 3.38%. Even though the tariffs haven’t reached the European coast of the Atlantic Ocean, the European investors are extremely sensitive to the trade news, and that leads to big sized moves – rising volatility. The market conditions are getting appetizing for traders that are looking for interesting short-term opportunities, but it’s important to have a clear playbook and determine what factors influence the market moves? Is it the data, is the central bank expectations, is it politics, geopolitics?

Major market movers change

Over the past two years for example, the main trading themes in the West were AI and the central bank decisions. Market prices were very sensitive to these factors. The incoming data was digested in the context of the impact that it would have for the central bank decisions. As such, weak economic data – especially weak inflation data - was perceived as good news by investors as weakness would lead to lower rates and lower rates would boost economic growth and company valuations.

Today, growth expectations prime, while the importance of the inflation outlook is no longer the same for all markets. For the Federal Reserve (Fed), the inflation outlook is crucial because the tariffs are expected to have a direct impact in boosting US inflation and limiting the Fed’s ability to cut the interest rates to boost growth. In this scenario, the weak economic data is bad news. In Europe, however, the inflation outlook is important but growth outlook has become more important: the European countries are obliged to boost their military budgets today no matter how fast inflation is growing. This no choice situation is reflected in the way Germany is acting today. The country is literally throwing the spending speedbumps out of the window to allow boosting spending in defense and security. They now want to create a EUR 500 billion infrastructure fund to get the continent back to its feet.

In short, US growth expectations remain closely linked to inflation and Fed policy, while European growth forecasts are getting a lift from higher spending prospects and become less dependent on the European Central Bank (ECB) monetary decisions. Weakening US growth expectations and strengthening European growth prospects continue to favour European assets.

This is why, the 30bps jump in German 10-year yield and the higher-than-expected PPI data in the Eurozone didn’t prevent the German DAX index from gaining more than 3% yesterday. The Stoxx 600 index is set for its biggest quarterly outperformance against the S&P500 in a decade and the EURUSD recorded its best three-day session in a decade. The ECB is widely expected to cut its rates by 25bp at today’s meeting. The press conference will be particularly interesting as it marks Lagarde’s first remarks since the US decided to withdraw military support for Europe.

Across the Atlantic, the major indices were better bid yesterday, but the tariff talks, actions, decision reversals and uncertainty make the US markets a riskier place to be. The ADP report showed that the US economy added around 77K new nonfarm jobs last month, almost half of the number expected by analysts. The growing number of job cuts at companies including federal contractors, policy uncertainty and slowdown in consumer spending explained the weakness. Happily, the ISM data came in better-than-expected to prevent a further selloff of the S&P500 below the 200-DMA, but it’s probably just a matter of time before we see the index return below that level.

All Eyes on ECB as Markets Brace for 25bp Cut

In focus today

In the euro area, the ECB meeting today is expected to end with yet another 25bp rate cut, bringing the policy rate to 2.50%, 150bp lower than the peak last year. While the cut decision is relatively straight forward, divergences in the ECB's GC members assessment of the policy stance is starting to show, thus a key question will be whether ECB will already now start to soften is assessment on the monetary policy restrictiveness. Markets are pricing another 59bp worth of rate cuts this year, following today's 25bp rate cut. We expect ECB to cut more than this to end with a terminal rate of 1.50% in H2 this year, albeit risks are slightly skewed to the upside. See more in ECB preview - A cut is the easy part, 28 February.

In the US, initial claims data released in the afternoon will provide some flavour on the impact of the public sector layoffs initiated by the DOGE initiative. So far, the public sector layoffs have only been visible in the claims data at a regional level (e.g. District of Columbia), but the numbers will likely increase as terminations are being effectuated.

In Denmark, January's industrial production figures are due, following a 4% increase in December, resulting in 8.6% annual growth in 2024. Unlike the broader European trend, Danish manufacturing remains strong, even excluding pharmaceuticals. February's bankruptcy statistics are also expected, with January showing a 3.5% rise from December. However, in 2024 we saw a 17.5% decrease in bankruptcies from 2023. Currently, the number of bankruptcies is only slightly above the levels we observed in the years before the pandemic, thus not ringing the alarm bells.

In Sweden, preliminary February inflation will be in the spotlight. Despite January underlying inflation printing an unusually high monthly increase (+0.2%), we have taken a cautious stance assuming a normal increase in February, +0.6 % mom. Energy will contribute net positively to CPIF this month, as increasing electricity prices usually outweigh a decline in fuel prices. Finally, the Riksbank's rate cuts are now pulling mortgage costs lower, contributing about -0.3 p.p. on the month. Compared to the Riksbank's forecast (CPIF 2.2%, and CPIF excl. energy 2.4%), we anticipate both CPIF and CPIF excl. energy at 2.7%.

Economic and market news

What happened yesterday

In the US, data painted a mixed picture on the labour market dynamics in February ahead of the NFP release tomorrow. The ADP report showed a weaker-than-expected increase in private-sector payrolls of 77,000 (consensus: 140,000), the lowest print since July 2024. On the other hand, yesterday's ISM data provided some relief in terms of the worries related to the state of the US services sector. The composite activity measure recorded a rise from 52.8 to 53.5 (consensus: 52.5), standing in strong contrast to the very weak reading in the comparable PMI survey, while the employment measure rose to a 3-year high of 53.5 (consensus: 52.5). Although the ISM measure has been volatile recently, the persistently improving employment signals does suggest that labour demand remains decent despite the recent signs of slowing economic growth.

In the euro area, the final PMIs confirmed the slightly disappointing flash release, as the composite PMI remained unchanged at 50.2. In the services sector the PMI dropped to 50.6 from 51.3, mainly due to France. With the composite PMI above 50 for the second consecutive month, it suggests that the euro area economy experienced marginal growth in Q1.

In Germany, the upcoming German government has proposed a significant easing of fiscal policy through increased public investment, higher defence spending, and a change to the debt brake. We expect these three proposals to be approved in parliament next week with support from the Greens. If passed, the proposals will positively impact the German economy, though we expect to see the effect on GDP next year, with most of the impact in 2027-2028. Financial markets have reacted strongly by driving up yields on German government debt and widening the Bund-ASW spread. We expect the Bund-ASW spread to fall towards 15 basis points in the short term. This will also support Danish government bonds, where we expect the 10-year spread to move towards minus 25 basis points.

In Sweden, services PMI came out a little bit stronger than January at 50.8 (50.2) and looking at the sub-components the employment index rose from 46 to 47.6, so a healthy increase albeit the index remains below the 50-mark. Business volumes and new orders rose marginally as well.

In Norway, house prices rose 0.9% m/m (SA) in February. As such, it was another very strong month for Norwegian house prices which still very much remains a "lack of supply"-story. The message in January from Norges Bank was that the housing market has no impact on the near-term policy setting at this stage and although this is another strong report it does seem like other factors are more important for the number of rate cuts that Norges Bank will deliver this year. We have 4x25bp as base case. Markets price 68bp worth of cuts by the December 2025 Norges Bank meeting.

On the geopolitical front, the U.S. has paused intelligence-sharing with Ukraine in yet another effort at pressuring Zelenskiy towards peace talks with Russia. This step follows the decision on Monday by President Trump to suspend military aid to Ukraine.

Meanwhile, Trump has issued a stern warning to Hamas, demanding the release of hostages in Gaza and pledging unwavering support for Israel. The U.S. has entered direct talks with Hamas for the first time, aiming to secure American hostages' release amid stalled ceasefire negotiations.

In economic developments, Trump is giving automakers complying with the USMCA rules a one-month exemption from the 25% tariffs on Canada and Mexico, allowing automakers time to move production to the US. This provided temporary relief to the auto industry, boosting stocks like GM and Ford.

Concurrently, oil prices fell to new lows yesterday despite rising equities and a falling USD, which normally pushes oil prices higher. OPEC+'s decision to start hiking oil output along with trade concerns might be dominating the former. It will be interesting to see if the US will use the recent price drop to resume buying of crude for its strategic reserves. That could provide some much-needed support for the market near-term.

Equities: Global equities were higher yesterday, once again driven largely by political developments, despite the release of valuable macroeconomic data that adds more pieces to the puzzle. As mentioned yesterday, there was very encouraging political news from China, Germany, and the EU, particularly on Tuesday. Yesterday, Trump made a small concession regarding the Canada-Mexico tariff, but this does not change the fact that regional political news remains more negative in the US compared to elsewhere.

Here are some equity return numbers to provide context:

- The MSCI World Index is down nearly 4% from its peak but remains 1% higher year-to-date.

- The German DAX is 16%(!) higher year-to-date and is close to reaching an all-time high.

- The Hang Seng Index reached its high for the year this morning, marking a 50% increase over the past year. This serves as a good reminder not to become overly focused on US exceptionalism and the MAG 7 as we exit 2024.

It is also valuable to examine the European sector rotation from yesterday. While the Stoxx 600 rose, led by a more than 3% increase in the DAX, ten industries within the Stoxx 600 fell, resulting in a very split sector and industry performance. This is logical given the potential for significant shifts in German/EU spending. Therefore, review the performance table from yesterday and exercise caution in opposing these trends, especially as long as we have tailwinds from spending negotiations and positive key figures in Europe, led by the manufacturing sector. In the US yesterday, the Dow rose by 1.1%, the S&P 500 by 1.1%, the Nasdaq by 1.5%, and the Russell 2000 by 1.0%. Asian markets are higher this morning, led by China. Futures in the Western world are mixed, with European indices pushing higher and the US being marginally lower.

FI: Wednesday was one for the history books with 10Y Germany yields rising by 30bp, while US rates were basically flat throughout the day. This was a fundamental relative repricing, reflecting that the EU now seems ready to act on the building geopolitical risks. Germany suggesting a loosening of the EU fiscal rules after being the fiscal hawk 'par excellence' the past decade is telling of the rapidly changing narrative in Europe right now. Whether the 30bp repricing is adequate or excessive remains uncertain, and we advise caution regarding the short-term outlook, as various political and legal factors in Germany could dilute some policy signals. The aggressive movement in Bunds was mirrored across Europe, with long-end inflation swap rates closing approximately 15bp higher. Markets adjusted by removing 15bp of cuts previously anticipated for the ECB by the end of 2025, bringing the total to 70bp.

FX: It was an eventful session across asset classes yesterday. EUR/USD broke above 1.07 for the first time since the US election, with EUR optimism continuing in yesterday's session. This move has been fuelled by what appears to be a regime shift in euro area - particularly German - fiscal policy, with large-scale investments in infrastructure and, most notably, defence spending. Akin to the USD, CHF weakened considerably despite Swiss inflation for February coming in stronger than expected. EUR/GBP moved higher on the broad-based EUR optimism and combined with the high-volatility environment, it was a poor cocktail for GBP. SEK remained fairly unscathed and is eying the release of February inflation this morning.

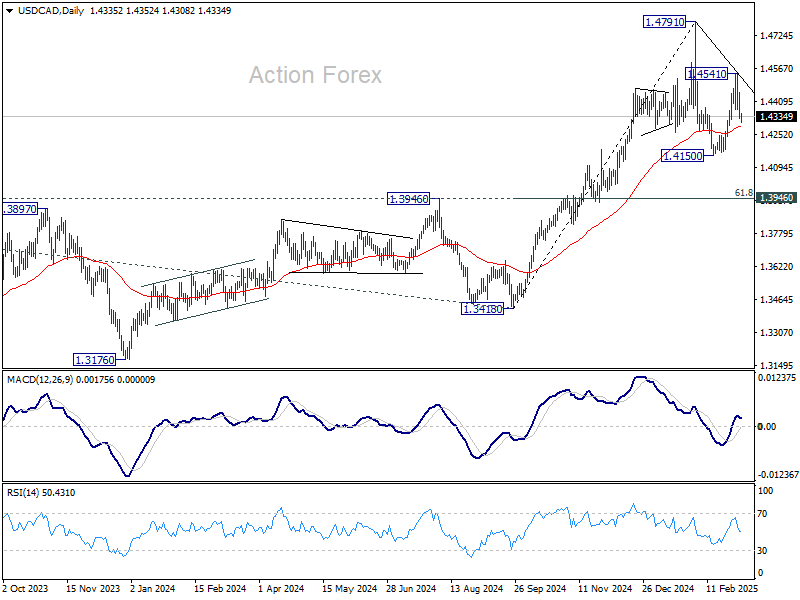

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4300; (P) 1.4300; (R1) 1.4419; More...

USD/CAD's firm break of 55 4H EMA (now at 1.4362) suggests that rebound from 1.4150 has completed at 1.4541 already. Fall from there is seen as the third leg of the corrective pattern from 1.4791. Intraday bias is back on the downside for 1.4150 support first. On the upside, though, above 1.4541 will resume the rebound from 1.4150 to retest 1.4791 high.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

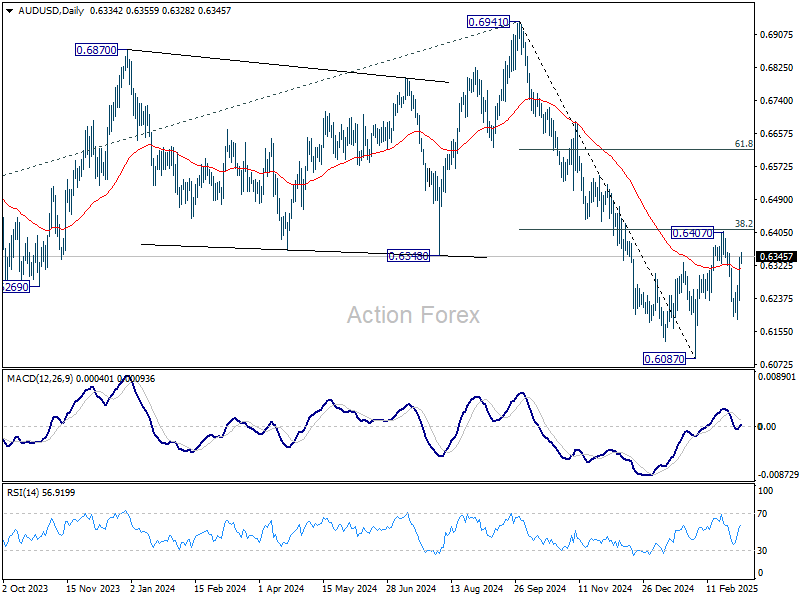

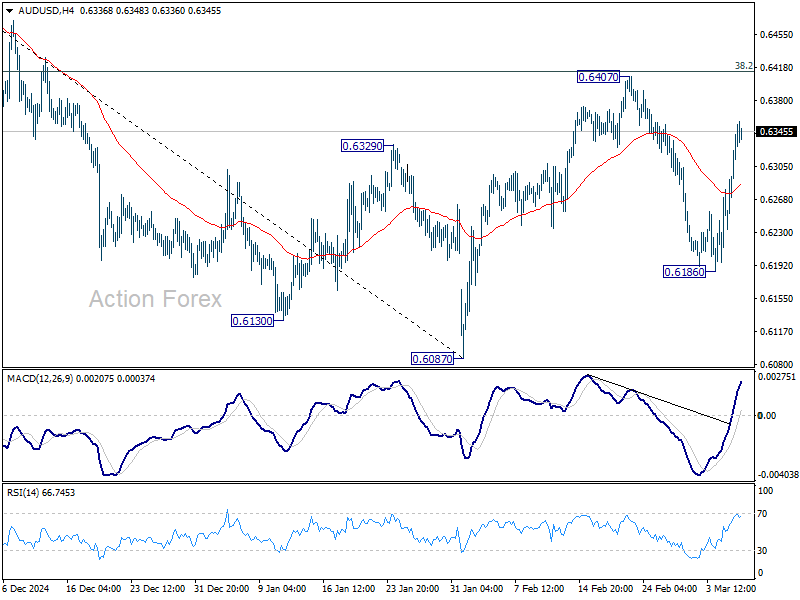

AUD/USD Daily Report

Daily Pivots: (S1) 0.6265; (P) 0.6304; (R1) 0.6374; More...

Intraday bias in AUD/USD remains neutral as range trading continues. On the downside, below 0.6186 will resume the fall from 0.6407 to retest 0.6087 low. However, sustained trading above 38.2% retracement of 0.6941 to 0.6087 at 0.6413 will raise the chance of near term bullish reversal, and target 61.8% retracement at 0.6615 next.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6494) holds.