Sample Category Title

XAUUSD Intraday Analysis

XAUUSD (1284.25): Gold prices briefly bounced higher yesterday, but the reversal was strong enough to push prices lower. The downside is now likely to see gold prices falling back to the familiar support level of 1275 - 1274 area. Establishing support here could keep gold prices from posting further declines. However, this cannot be ruled out as a break down below 1274 level could mark further drop in prices. The lower support at 1262 also comes with a horizontal support level as well as the dynamic support from the daily chart's rising trend line.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7852; (P) 0.7867; (R1) 0.7895; More...

Intraday bias in AUD/USD remains neutral at this point. Above 0.7896 will extend the rebound from 0.7732 and target a test on 0.8124 high. But we'd be cautious on strong resistance from there to limit upside and bring another fall to extend recent corrective pattern. On the downside, break of 0.7732 will resume the decline from 0.8124 and target medium term fibonacci level at 0.7628 first.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

USDJPY Intraday Analysis

USDJPY (113.16): The USDJPY remains tightly range bound with price action see testing the upside resistance at 113.00 in the past few sessions. Still, USDJPY has been posting a consolidation that could signal a possible breakout. With the Japanese elections due over the weekend, we could expect to see a breakout emerging by Monday's open. Price action needs to post a convincing close above 113.00 in order to validate any further gains to the upside. Thus, there is a strong chance that USDJPY could push back and close within the range of 113.00 and 112.04.

EURUSD Intraday Analysis

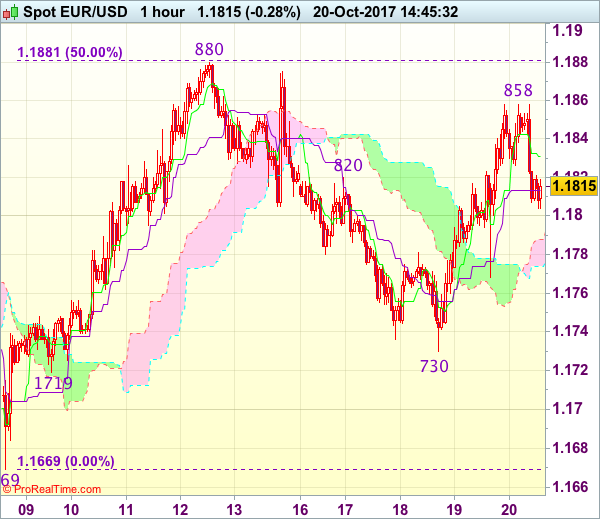

EURUSD (1.1814): After posting strong gains for the second day, the EURUSD was seen pulling back in early trading session today. This comes after price rallied back to the resistance area of 1.1843 - 1.1822. As long as this resistance holds, EURUSD could be seen pushing lower. Support at 1.1720 which was missed previously is likely to be the target to the downside. In the medium term, EURUSD could be seen maintaining the range within these levels. There is also the descending triangle pattern that has formed on the 4-hour chart which also suggests a near-term test to the support level of 1.1720. Although EURUSD could trade sideways, the bias for a downside breakout is increasing.

Trade Idea : EUR/USD – Stand aside

EUR/USD - 1.1815

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1831

Kijun-Sen level : 1.1813

Ichimoku cloud top : 1.1788

Ichimoku cloud bottom : 1.1774

Original strategy :

Exit short entered at 1.1850,

Position : - Short at 1.1850,

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency continued meeting resistance at 1.1858 (like several times) and has retreated today, suggesting consolidation below this level would be seen and pullback to 1.1785-90 cannot be ruled out, however, break of support at 1.1768 is needed to signal the rebound from 1.1730 has ended at 1.1858, bring another fall towards this level later. A drop below this support would prolong consolidation below 1.1880, bring weakness to 1.1700 first.

On the upside, above said resistance at 1.1858 would suggest the correction from 1.1880 has ended, bring retest of this level, break there would signal another leg of erratic upmove from 1.1669 low is underway for gain to 1.1900-10, then towards 1.1940-50 later. As near term outlook is mixed, would be prudent to stand aside for now.

Politics Dominate Trading On Developments From Spain And New Zealand

The political developments in both New Zealand and Spain kept the markets busy on an otherwise calm Thursday. The Spanish government invoked Article 155 of the Spanish constitution in a bid to end the semi-autonomy for Catalonia. This comes amid the Catalonian leader Puigdemont threatened on Thursday to declare independence, in response to the Spanish government seeking clarification.

In New Zealand, the NZ First party announced that it was supporting the Labor party marking a change of government for the first time in nine-years. Although still a minority government, the Green party is also expected to lend support.

The kiwi fell sharply since the morning amid populist measures proposed by the NZ First party leader Peters. Among a number of things, the NZ First party wants to curb immigration and also prefers more central bank intervention and a weaker exchange rate. The RBNZ is also expected to see an additional mandate of full employment coming under its purview besides the current price stability.

On the economic front, UK retail sales fell 0.8% on the month more than expected. The data continued to dampen the outlook for a proposed BOE rate hike later down the line.

Looking ahead, the economic data today is relatively muted. Canada's monthly inflation data is expected to be released alongside the retail sales numbers. The data comes ahead of BoC meeting next week. The Fed Chair, Janet Yellen is expected to speak later in the evening.

Trade Idea : USD/JPY – Buy at 112.80

USD/JPY - 113.22

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.92

Kijun-Sen level : 112.81

Ichimoku cloud top : 112.81

Ichimoku cloud bottom : 112.56

New strategy :

Buy at 112.80, Target: 113.80, Stop: 112.45

Position : -

Target : -

Stop : -

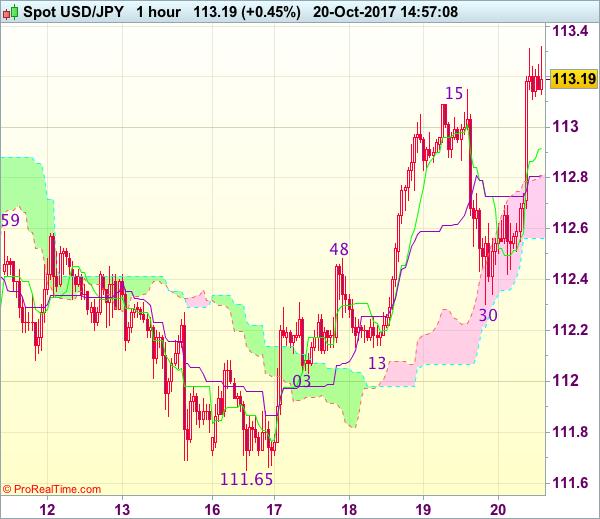

Although the greenback retreated to as low as 112.30 yesterday, dollar found renewed buying interest there and has rallied again, suggesting the rise from 111.65 is still in progress, hence bullishness remains for this move to extend further gain to 113.44 resistance, break of this recent high would provide confirmation and encourage for headway to 113.75-80 but reckon 114.00-10 would hold from here due to oversold condition.

In view of this, we are looking to buy dollar again on pullback as 112.81 (current level of the Kijun-Sen and upper Kumo) should limit downside. Below the lower Kumo (now at 112.56) would defer and risk test of said support at 112.30 but break there is needed to signal top is formed instead, bring test of indicated strong support area at 112.03-13.

Currencies: US Senate Vote ‘Saved’ The Dollar

Sunrise Market Commentary

- Rates: US reflationary spirits in the driving seat?

US Treasuries lost significant ground after the US Senate adopted a budget for the next fiscal year, clearing a crucial hurdle for tax reforms. Reflationary spirits could inflict more losses on US Treasuries given today's eco calendar. European investors might decide to take a wait-and-see attitude with next week's ECB meeting looming on the horizon. - Currencies: US senate vote 'saved' the dollar

The dollar stayed in the defensive yesterday. Interest rate differentials moved against the US currency despite the crisis in Catalonia. A budget vote in the US senate changed fortunes again in favour of the dollar. However, the gain of the dollar against the euro remains modest. EUR/GBP returned to the 0.90 barrier on poor UK eco data and little Brexit progress

The Sunrise Headlines

- US stock markets recovered from opening losses to the tune of 0.5% to end flat. Nasdaq underperformed (-0.25%). Overnight risk sentiment is positive with Japan underperforming .

- The US Senate's passage of the budget blueprint for the next fiscal year, in a 51-49 vote primarily along party lines, helps unlock a procedure that Republicans plan to use to rewrite the tax code with just GOP votes.

- European leaders rebuffed British PM May's pitch to revive stalled Brexit talks, but German Chancellorl Merkel said she was confident negotiations would advance by December.

- CIA director Pompeo warned that North Korea could be just 'months away' from developing the ability to strike America with a nuclear-armed ballistic missile.

- Separatist campaign group the Catalan National Assembly is calling on its supporters to pull cash from lenders including CaixaBank SA and Banco Sabadell SA between 8 am and 9 am today.

- President Trump will support a bipartisan bill of health care only if it includes a series of conservative measures that Republicans sought in their failed effort to repeal the Affordable Care Act.

- Today's eco calendar is extremely thin with only US existing home sales. The Q3 earnings season continues with GE, P&G,…

Currencies: US Senate Vote 'Saved' The Dollar

Dollar saved by US Senate vote

All eyes were on Spain yesterday. EUR/USD spiked lower as the Spanish government initiated the process of suspending the regional powers of the Catalan government. However, the euro decline was almost immediately reversed. EUR/USD even moved in positive territory. A tentative global risk-off sentiment caused US Treasuries to outperform German bunds, reducing the interest rate differential in favour of the euro. EUR/USD finished the session at 1.1852 (from 1.1787). USD/JPY closed the day at 112.54.

Overnight, the US Senate adopted a fiscal 2018 resolution which is an important step for a tax overhaul further down the road. The approval triggered a rebound in US bond yields and supported the dollar. USD/JPY jumped north of 113. EUR/USD returned to the 1.18 area. The hope on a US tax reform also propelled US equity futures. The impact on Asian equity markets is diffuse and modest. The Hong Kong market reverses part of yesterday's late session decline. Japanese indices are little changed despite the rise of USD/JPY. Investors look forward to the outcome of the Japanese parliamentary elections to be held this weekend. The Kiwi dollar declined further below 0.70 after the formation of a government with Labour and the New Zealand first party.

The eco calendar is extremely thin today. There are no important data in EMU. US the existing homes sales (September) will only be of intraday significance for USD trading, at best. Fed's Yellen will give a lecture on 'Monetary policy since the Financial crisis' after the US close. We don't expect the Fed chair to change her view on the Fed's policy action in the near future.

A global risk off context, partially inspired by tensions in Catalonia weighed more on the dollar than on the euro yesterday as interest rates in the US declined more than in EMU. Overnight fortunes changed again in favour of the dollar as US yields jumped higher on the approval of a 2018 budget resolution in the US Senate. The rise in US yields and a constructive risk sentiment support the dollar overnight. The gains of the dollar against the euro remain modest. EUR/USD still trades north of 1.18. We see room for some further USD gains today. However, the price action earlier this week indicated that it wasn't that easy for the dollar to gain ground against the euro even if the move was supported by a favourable interest rate differential. The day-to-day picture of USD/JPY is improving and the pair is nearing the recent highs. Investors will look out for the outcome of the Japanese elections. The prospect of the continuation of Abenomics (including an easy monetary policy) might be a slightly negative for the yen.

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern, but no real test of the 1.1662 support occurred. Last week, the pair even returned (temporary?) above the 1.1823 previous range bottom, which was disappointing for EUR/USD bears. We maintain a cautious sell-on upticks bias. However, the pair needs to drop below 1.1670/62 support to really give comfort to EUR/USD bears. The USD/JPY momentum was constructive in September. The pair regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. Sentiment improved again this week, but we still assume that a break beyond 114.49 will be difficult.

EUR/USD: Holding tight ranges, despite plenty of 'event risk

EUR/GBP

EUR/GBP returns to 0.90 barrier

UK retail sales fell by 0.8% M/M in September, reversing a rise of 0.9% the previous month. The report suggested that there is little room for the BoE to raise its policy rate beyond a sole rate hike in November. This prospect of little additional interest rate support weighed further on sterling yesterday. EUR/GBP spiked to the 0.8990 area and held close to that level for the remainder of the session. At the EU summit, German Chancellor Merkel indicated that both parties in the EU-Brexit talks should move so that a deal on the divorce can be reached by the end of the year. However, there were no concrete steps. The statement didn't help sterling much. EUR/GBP even closed the session north of 0.90 (0.9006). Cable finished the day at 1.3159.

Monthly UK budget data will be published today. However, we don't expect this data series to have a lasting impact on sterling trading. The UK currency remains in the defensive this morning, both against the euro and the dollar. Recent eco data reinforced investors' feeling that any interest rate support for sterling in the near future will be very limited. At the same time, there is no noticeable progress in the Brexit talks. We hold on to the view that any upside of sterling will be difficult. We look to buy EUR/GBP on dips.

EUR/GBP staged a strong uptrend from April till late August to set a top at 0.9307. Rising UK inflation data and hawkish BoE comments reinforced a sterling rebound, but this rebound has run its course. EUR/GBP supports at 0.8743 and 0.8652 proved difficult to break. The recent rebound above 0.89 improved the ST technical picture of EUR/GBP, but for now there were no convincing followthrough gains. EUR/GBP 0.9026 is 50% retracement of the recent countermove

EUR/GBP: Poor UK eco data and little progress in Brexit talks propel EUR/GBP back to 0.90

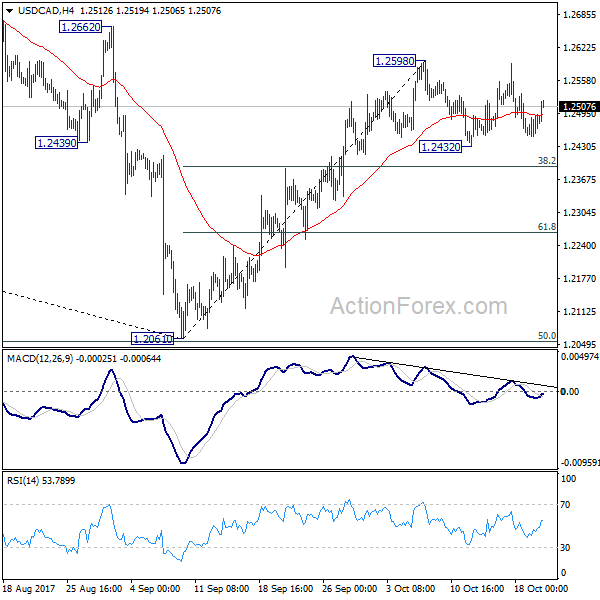

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2476; (R1) 1.2502; More....

At this point, USD/CAD is staying in consolidation from 1.2598 and intraday bias remains neutral for the moment. In case of deeper fall, downside should be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption. On the upside, break of 1.2598 will extend the rebound from 1.2061 to 1.2777 resistance next.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Dollar Regains Ground as Boosted by Tax Hope

Dollar regains much ground overnight as boosted by revived hopes on tax reform in the US. A critical hurdle was cleared after the Senate approved a budget blueprint for fiscal 2018. That was narrowly passed by 51-49 after marathon debate. Nonetheless, the passing of the blueprint includes instruction that would help Republicans avoid a Democrat filibuster. Senate Majority Leader Mitch McConnell said that "passing this budget is critical to getting tax reform done, so we can strengthen our economy after years of stagnation under the previous administration." Senator Bob Corker, who's in feud with President Donald Trump, voted the for the budget. Meanwhile, Senator John McCain also voted yes.

Trump concluded Fed chair interviews, leans towards Powell

Separately, it's reported that Trump has concluded all interviews on the five candidates for next Fed chair. A decision could be announced as soon as next week. The interview with current Fed chair Janet Yellen "went well" according to unnamed source. But it's also reported that Trump is leaning towards current Fed Governor Jerome Powell for the job. And important factor is that Powell is known to be heavily favored by Treasury secretary Steven Mnuchin. The other three candidates include former Fed Governor Kevin Warsh, Stanford economist John Taylor and National Economic Council Director Gary Cohn. The formal response on the issue from White House spokeswoman Natalie Storm is that "they're all at the same level of consideration at this time. The president said himself on Tuesday, he likes all of the candidates and has great respect for them all."

Euro resilient despite Catalonia turmoil

Euro is trading as the second strongest one for the week so far, just next to Dollar. The turmoil regarding Catalonia doesn't have much lasting impact on the common currency so far. Spain has called for a special cabinet meeting on Saturday. It's believed that officials would trigger the so call Article 155 process to suspend Catalonia autonomy and take away lower powers. At the EU summit, German Chancellor Angela Merkel said they will watch the developments closely. But she leaned towards the Spanish government and said that "we hope that there will be solutions that can be found on the basis of the Spanish constitution." French President Emmanuel Macron also called for "unity".

UK PM May seeks dynamic in Brexit negotiations

UK Prime minister Theresa May also attended the working dinner of EU official sin Brussels. She urged EU leaders to create a "dynamic" in Brexit negotiations" that "enables us to move forward together". And she acknowledged that the process was progressing "step by step" and "from my side there are no indications at all that we won't succeed." Meanwhile, Merkel said there were "encouraging" signs but progress was "no sufficient" to start trade talks.

On the data front

German PPI rose 0.3% mom, 3.1% in September, above expectation of 0.1% mom, 2.9% yoy. Eurozone current account and UK public sector net borrowing will be featured in European session. But main focus of the day will be Canadian Dollar, including CPI and retail sales. US will release existing home sales.

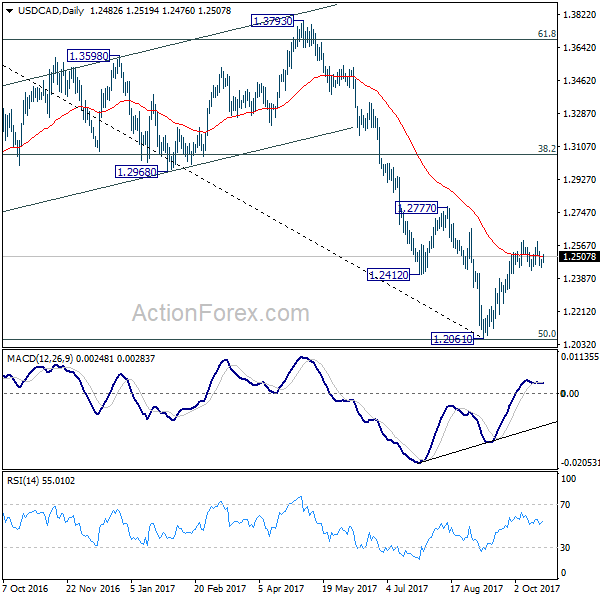

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2476; (R1) 1.2502; More....

At this point, USD/CAD is staying in consolidation from 1.2598 and intraday bias remains neutral for the moment. In case of deeper fall, downside should be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption. On the upside, break of 1.2598 will extend the rebound from 1.2061 to 1.2777 resistance next.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 6:00 | EUR | German PPI M/M Sep | 0.30% | 0.10% | 0.20% | |

| 6:00 | EUR | German PPI Y/Y Sep | 3.10% | 2.90% | 2.60% | |

| 8:00 | EUR | Eurozone Current Account (EUR) Aug | 26.2B | 25.1B | ||

| 8:30 | GBP | Public Sector Net Borrowing (GBP) Sep | 5.7B | 5.1B | ||

| 12:30 | CAD | CPI M/M Sep | 0.40% | 0.10% | ||

| 12:30 | CAD | CPI Y/Y Sep | 1.70% | 1.40% | ||

| 12:30 | CAD | CPI Core - Common Y/Y Sep | 1.50% | |||

| 12:30 | CAD | CPI Core - Trim Y/Y Sep | 1.40% | |||

| 12:30 | CAD | CPI Core - Median Y/Y Sep | 1.70% | |||

| 12:30 | CAD | Retail Sales M/M Aug | 0.40% | 0.40% | ||

| 12:30 | CAD | Retail Sales Less Autos M/M Aug | 0.30% | 0.20% | ||

| 14:00 | USD | Existing Home Sales Sep | 5.32M | 5.35M |