Sample Category Title

Daily Wave Analysis: GBP/USD Breaks Contracting Triangle Pattern In Bearish Channel

Currency pair GBP/USD

The GBP/USD is building lower lows and lower highs which makes a bearish ABC (grey) a bit less likely and a wave 123 (green) more probable, although a bearish breakout below support (blue) is still needed to confirm. The wave 4 (orange) correction is less likely if price breaks above the resistance trend line (yellow). A break below the support trend line (blue) increases the chance of a bearish break within wave 5 (orange).

The GBP/USD broke the support trend lines (dotted blue) of the triangle chart pattern. Price will need to show bearish momentum and bear flag chart patterns to confirm a potential wave 3 impulse. Price would also need to break below the bottom of the bearish channel (blue).

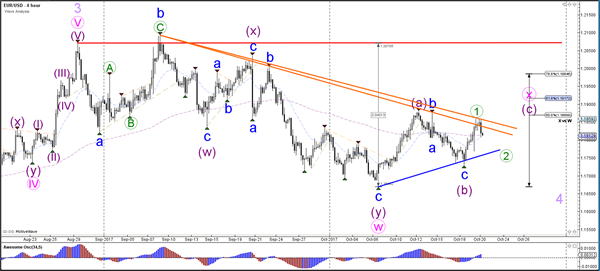

Currency pair EUR/USD

The EUR/USD bounced at resistance trend lines (orange) of the larger triangle chart pattern. A break above resistance would confirm a bullish breakout within wave C of wave X (pink). A break below the support trend line (blue) will probably indicate a larger correction within wave 4 (light purple).

The EUR/USD could be building a wave 1-2 (green) if price stays above the 100% Fibonacci level of wave 2 vs 1.

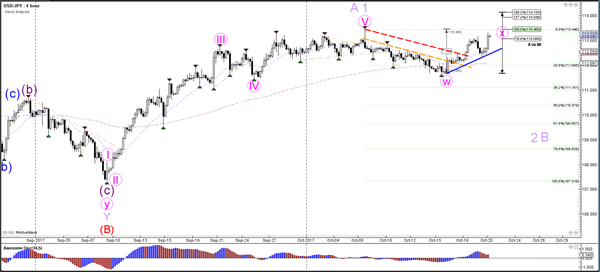

Currency pair USD/JPY

The USD/JPY stopped at the 78.6% Fibonacci resistance level but then failed to break below the support trend line which could either indicate a larger wave X (pink) or an uptrend continuation and an invalidation of the current wave patterns.

The USD/JPY is approaching the resistance from the previous top (red).

US Dollar Eyeing Upside Break Vs Japanese Yen

Key Highlights

- The US Dollar is trading higher and approaching a major resistance at 113.40 against the Japanese Yen.

- There are two bullish trend lines formed with support at 112.70 and 111.80 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending Oct 14, 2017 posted a decline from the last revised reading of 244K to 222K.

- Today in Canada, the Consumer Price Index (CPI) for Sep 2017 will be released, which is forecasted to increase by 1.6% (YoY).

USDJPY Technical Analysis

The US Dollar bounced sharply from 111.65 against the Japanese Yen. The USD/JPY pair is now approaching a crucial resistance near 113.40, which is a breakout point.

The pair is currently well above the 76.4% Fib retracement level of the last decline from the 113.44 high to 111.63 low. Therefore, there are chances of an upside break above 113.40. However, a break won’t be easy since the 113.30-40 region prevented gains on many occasions.

On the downside, there are two bullish trend lines formed with support at 112.70 and 111.80 on the 4-hours chart. As long as the pair is above the 112.50 level, there is a chance of an upside break towards 113.85 in the near term.

US Initial Jobless Claims

Recently in the US, the Initial Jobless Claims report for the week ending Oct 14, 2017 was released by the US Department of Labor. The forecast was slated for a decline from the last reading of 243K to 240K.

The actual result was way above the forecast, as there was a decline to 222K. On the other hand, the last reading was revised up from 243K to 244K. The 4-week moving average was down by 9,500 from the previous week’s revised average of 257,750 to 248,250.

The report stated:

The advance number for seasonally adjusted insured unemployment during the week ending October 7 was 1,888,000, a decrease of 16,000 from the previous week’s revised level. This is the lowest level for insured unemployment since December 29, 1973 when it was 1,805,000.

Overall, the USD/JPY pair is gaining pace, and a break above 113.40 would open the doors for more gains, probably towards 113.85.

Elliott Wave View: AUDUSD Short Term

AUDUSD Short Term Elliott Wave view suggests that Primary wave ((W)) ended at 0.7731 on October 6th low. Up from there, Primary wave ((X)) is currently unfolding as a double three Elliott Wave structure. Intermediate Wave (W) of ((X)) ended at 0.7807 and Intermediate wave (X) of ((X)) ended at 0.7815. Near term, while pullbacks stay above 0.7815, but more importantly above 10/6 low at 0.7731, expect pair to extend higher. At this stage, pair still needs to break above Intermediate wave (W) at 0.7815 to give more validity to this view. Until then, we can’t rule out a double correction in Intermediate wave ((X)).

AUDUSD 1 Hour Elliott Wave Chart

Double three ( 7 swings) is one of the most common corrective patterns in Elliott wave’s theory. We often refer to double three structure as a 7-swing structure. It is a great pattern that allows traders to trade with a well-defined level of risk and target areas. Below is the image of a Double Three structure. It has labels of (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

Market Update – Asian Session: US Dollar And Yields Rise As Senate Passes Budget

Asia Summary

Asian equity markets opened the session mixed. S&P 500 and Nasdaq futures have risen after the US Senate gained enough votes to pass the budget, which may help pave the way for tax reforms. The Nikkei 225 opened lower following 13 straight sessions of gains, but has since pared losses.

Nissan has declined by over 1.5%. Following yesterday's close, the company's CEO said it decided to temporarily suspend the production of certain vehicles, as the company continues to grapple with the issue of unauthorized vehicle inspections in Japan. The company is also said to have found improper inspections going as far back as 20 years, according to Japanese media. Coupled with the declines in Nissan, shares of Honda have also traded lower.

In Hong Kong, insurer AIA Group has declined by over 2% on weaker than expected growth in quarterly new business value.

Following yesterday's weakness seen in the technology sector, Taiwan Semi has traded flat after reporting Q3 results and issuing guidance. South Korean chip makers are also trading higher. Hynix has gained over 2%.

South Korean utility services firms, including KEPCO Engineering & Construction, have moved sharply higher following the release of a local public opinion poll, which showed public support for building two new nuclear reactors.

South Korean 3-year bond yields have continued to move higher on today's session. Following the hawkish dissenter at yesterday's BoK meeting, some of the tier 1 brokerage firms have started to move forward their views for rate hikes from 2018. US Treasury yields have moved higher in the Asian session following the Senate's budget vote.

At the same time, USD/JPY has gained over 0.4%, amid broad strength in the US dollar. The Kiwi has traded below 70 cents for the first time since May, as the currency has continued to decline following the move by the NZ First Party to form a coalition with the opposition Labour Party.

Looking ahead, US companies due to report earnings later today include General Electric (GE), Honeywell, Manpower, P&G and Schlumberger. On Sunday (Oct 22nd), Japan is due to hold its general elections. On Thursday (Oct 26th), the ECB is due to hold its monetary policy meeting.

Speakers and Press

China

(CN) China mandates 10 banks for planned US dollar bond denominated issuance (first dollar issuance since 2004); to hold investor meeting in Hong Kong on Oct 25th

(CN) Shanghai said to plan Free-Trade Port – Chinese Press

(CN) China NDRC Head: China 2017 GDP to exceed CNY80T, (vs CNY74T y/y) and the GDP growth rate may exceed the official forecast of around 6.5% - Chinese Press

(CN) China gives sector breakdown for Q3 GDP: Tech +29% y/y, Finance +5.6%, Property +3.9%

Other

(US) Senate has the votes to adopt budget, which is a step toward tax overhaul

(JP) Japan Finance Min Aso: Japan companies' piling up of internal reserves has gone too far; wants corporate reserves to be used for investments and wages

(GE) Germany Chancellor Merkel: UK PM May's Brexit stance insufficient at this point; May offered 'significantly' more on Brexit than before, but presentation did not change stance

(KR) Analysts bring forward Bank of Korea rate hike calls to Nov from 2018 following hawkish dissenter at yesterday's policy meeting

(KR) According to a South Korea public opinion survey, 59% support the building of two new nuclear reactors – financial press

(MY) Malaysia Think Tank MIER said to raise 2017 GDP growth forecast to 5.4% vs. 4.7% July forecast - Malaysian Press; Cites stronger domestic demand and exports.

(US) Follow Up: Fed Chair announcement unlikely to come this week as President Trump has yet to make up his mind; Advisers said to favor Taylor or Powell – US financial press

(US) SEMI: North America Sept Billings $2.03B (3-month avg basis), +36% y/y

(NZ) New Zealand Incoming PM Ardern: Will be ‘very pro-active' government

(TW) Zhen Ding Technology: The Apple supplier is said to run factories at full capacity – Taiwan Press

Asian Equity Indices/Futures (00:30ET)

Nikkei flat, Hang Seng +1%, Shanghai Composite flat, ASX200 +0.2%, Kospi +0.5%

Equity Futures: S&P500 +0.3%; Nasdaq +0.3% , Dax +0.3% , FTSE100 +0.3%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1808-1.1858; JPY 112.52-113.31; AUD 0.7829-0.7882; NZD 0.6972-0.7037

Aug Gold -0.3% at 1,286/oz; Aug Crude Oil +0.2% at $51.38/brl; Sept Copper +0.8% at $3.196/lb

GLD SPDR Gold Trust ETF daily holdings flat at 853.1 metric tons

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6092 V 6.6093 PRIOR

PBoC OMO: Injects CNY80B in 7 and 14-day reverse repos v CNY140B injected prior in 7 and 14-day reverse repos; Net daily injection CNY60B, net weekly injection CNY560B v CNY240B drain w/w

(CN) China MOF sells 30-year bonds at 4.28%, bid to cover 2.66x

US markets on close: Dow flat, S&P500 flat, Nasdaq -0.3, Russell -0.2%

Best Sector in S&P500: Utilities +1%

Worst Sector in S&P500: Consumer Staples -0.5%

At the close: VIX 10.05 (-0.02pts); Treasuries: 2-yr 1.535% (-3bps), 10-yr 2.320% (-2.5bps), 30-yr 2.838% (-1bp)

US Market Summary

Stocks moved lower on the open after a wave of risk-off sentiment engulfed markets during the European session, but stock prices along with risk assets recouped most losses into the afternoon. The S&P500 and Dow closed near the day's highs, stretching into positive territory at the end of the session. Before the opening bell in NY, the VIX popped 15% back above 11, but volatility edged off as the day wore on. The Sept Philly business outlook blew through expectations, just as the Empire index did on Monday, while signaling acceleration for the manufacturing jobs market. Treasuries rallied on the risk-off sentiment led by the long end, but ended off their best levels, and gold futures gained for the first time in four sessions. Apple iPhone worries weighed on the tech sector. Consumer staples and energy were also in the red, while healthcare and materials outperformed.

US Afterhours Movers

PYPL Reports Q3 $0.46 v $0.44e, Rev $3.24B v $3.17Be; +3.0% afterhours

SKX Reports Q3 $0.59 v $0.43e, Rev $1.10B v $1.06Be; +18.6% afterhours

Aussie Dollar Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.37% against the USD and closed at 0.7877.

LME Copper prices declined 0.7% or $51.5/MT to $6920.0/MT. Aluminium prices rose 1.0% or $22.0/MT to $2128.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7838, with the AUD trading 0.5% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7817, and a fall through could take it to the next support level of 0.7795. The pair is expected to find its first resistance at 0.7872, and a rise through could take it to the next resistance level of 0.7905.

Going ahead, market participants would keep a close watch on Australia’s consumer price inflation data, the sole important release next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the EUR rose 0.43% against the USD and closed at 1.1847, despite political upheaval in Spain after the Spanish government threatened to suspend Catalonia’s autonomy and take control as the region’s leader, Carles Puigdemont, refused to abandon a push for independence.

Macroeconomic data released in the US showed that first time claims for the US unemployment benefits dropped to a level of 222.0K in the week ended 14 October, hitting its lowest level since March 1973, thus pointing to a strong labour market growth that would allow the Federal Reserve to hike interest rate again in December. Markets had expected initial jobless claims to fall to a level of 240.0K, after recording a revised level of 244.0K in the previous week. Further, the nation’s Philadelphia Fed manufacturing index unexpectedly climbed to a five-month high level of 27.9 in October, compared to a level of 23.8 in the prior month, while markets were expecting the index to ease to a level of 22.0.

On the other hand, the nation’s leading indicators unexpectedly retreated 0.2% in September, defying market consensus for a gain of 0.1% and following an advance of 0.4% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1809, with the EUR trading 0.32% lower against the USD from yesterday’s close, as the greenback strengthened after the US Senate voted to approve a budget blueprint that will allow the Republicans to pursue a tax-cut package without Democratic support.

The pair is expected to find support at 1.1765, and a fall through could take it to the next support level of 1.1722. The pair is expected to find its first resistance at 1.1855, and a rise through could take it to the next resistance level of 1.1902.

Going ahead, investors would eye the Euro-zone’s current account balance data for August, slated to release in a few hours. Moreover, the US existing home sales data for September, slated to release later in the day, would keep investors on their toes.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

UK’s Retail Sales Plunged In September

For the 24 hours to 23:00 GMT, the GBP declined 0.41% against the USD and closed at 1.3155, following weaker-than-expected UK retail sales figures.

Data showed that Britain's retail sales declined more-than-expected by 0.7% on a monthly basis in September, suggesting that accelerating inflation is squeezing household incomes and holding back the growth of retail sector. Retail sales had registered a revised advance of 0.9% in the prior month, while investors had envisaged for a drop of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.3101, with the GBP trading 0.41% lower against the USD from yesterday's close.

The pair is expected to find support at 1.3060, and a fall through could take it to the next support level of 1.3019. The pair is expected to find its first resistance at 1.3182, and a rise through could take it to the next resistance level of 1.3263.

Moving ahead, traders would direct their attention to the UK's public sector net borrowing data for September, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.42% against the JPY and closed at 112.56.

On the data front, Japan’s final machine tool orders climbed 45.0% YoY in September, and revised lower from a preliminary print indicating a gain of 45.3%. Machine tool orders had risen 36.2% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 113.21, with the USD trading 0.58% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.57, and a fall through could take it to the next support level of 111.93. The pair is expected to find its first resistance at 113.58, and a rise through could take it to the next resistance level of 113.95.

Looking ahead, a speech by the BoJ Governor, Haruhiko Kuroda, due in a few hours, will be eyed by traders. Also, market participants will closely monitor Japanese general election, due over the weekend, wherein the Japanese Prime Minister, Shinzo Abe’s ruling party is expected to secure a majority.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Switzerland’s Trade Surplus Rose In September

For the 24 hours to 23:00 GMT, the USD declined 0.51% against the CHF and closed at 0.9762.

In economic news, Switzerland's trade surplus widened to CHF2.9 billion in September, after recording a revised surplus of CHF2.2 billion in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9822, with the USD trading 0.61% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9757, and a fall through could take it to the next support level of 0.9691. The pair is expected to find its first resistance at 0.9868, and a rise through could take it to the next resistance level of 0.9913.

Going ahead, Switzerland's ZEW expectations index and the UBS consumption indicator, due to release next week, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading Lower, Ahead Of Canada’s Inflation And Retail Sales Data

.

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CAD and closed at 1.2485.

In the Asian session, at GMT0300, the pair is trading at 1.2518, with the USD trading 0.26% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2473, and a fall through could take it to the next support level of 1.2428. The pair is expected to find its first resistance at 1.2541, and a rise through could take it to the next resistance level of 1.2564.

This afternoon will bring two crucial Canadian releases, namely the consumer price index for September and retail sales figures for August.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.