Sample Category Title

Trumped

Risk sentiment is on the floor this morning after Donald Trump imposed 25% tariff on most Mexican and Canadian imports and 10% tariff on Chinese imports which will take effect from tomorrow – a move, I believe, will certainly backfire and end up in tears for everyone. But it will first add volatility and chaos to the financial markets.

The first market reaction on Monday’s open is a swift move to the US dollar. The Mexican peso gap-opened at the lowest levels since March 2022 and the USDCAD jump-opened and flirted with the 1.48 level with the prospect of melting Canadian exports toward the US and shattered growth outlook which will require a strong support from the Bank of Canada (BoC) in the coming months. Note that, the latest growth numbers from Canada already looked bad, but with Trump’s tariffs, things could snowball toward worse in a short period of time. This being said, the doji candlestick formation on the USDCAD hints at hesitation on whether the pair should travel toward the 1.50 knowing that such tariffs on the country’s two biggest trading partners – that together stand for more than a quarter of the US imports – will boost inevitably US inflation, cut the dream of further Federal Reserve (Fed) cuts short, and could require rate hikes, instead, to deal with a likely price shock. The hawkish shift in Fed expectation and flight to safety explain why the US dollar is widely in demand this morning. But the tariffs will also weigh on the US growth expectations, and the latter should limit the dollar’s upside potential and weigh on equity valuations.

European markets are set to open deeply in the red, the US futures are deeply in the negative as well, provided that the tariffs will severely increase many companies’ costs and hit their profit margins.

And oh, as per Europe, Trump ramped up his tariff threats and the EU said it would retaliate. The EURUSD is also heavily sold at the weekly open, but here as well, the doji candlestick formation hints that the Trump trade can not be one-sided. The US will also suffer from such dramatic tariff increases, the monstruous tariffs will immediately weigh on the US growth outlook as well and prevent the US dollar from fully benefiting from Trump’s America First Policies. Instead, the US could end up in a less appetizing America Alone setting.

Now coming back to the fundamentals, Friday’s PCE numbers from the US came in line with market expectations, while the softer-than-expected German inflation reinforced the dovish European Central Bank (ECB) bets – that are stronger this morning with the fear that Trump would wake up one morning and impose huge tariffs on European imports as well. Overall, the upside pressure in the US dollar will likely remain until the dust settles, but the risk of retaliation, the fact that the tariffs will likely boost US inflation and hit the US growth prospects should quickly build a barrier in front of the US dollar bulls’ path toward the north. And the risk selloff will likely lead to correction in equity markets on both sides of the Atlantic Ocean. Even robust earnings will hardly improve global risk sentiment this week. Big companies including Alphabet, Amazon, AMD, Novo Nordisk and Qualcomm are due to announce their earnings this week.

Inside Oil

Exxon announced better-than-expected earnings and income in Q4 thanks to increased production in the Permian Basin and Guyana. But earnings from the energy products unit dropped significantly with weaker refining margins and reduced global fuel demand, especially from China. Exxon also reduced its share repurchases. Trump’s tariffs will likely further squeeze profit margins and keep risks tilted to the downside. The picture is worse on the Canadian side of the border, of course, as the 25% tariff on Canadian imports will make the European and Asian exports toward the US more competitive. As such, the Canadian Imperial Oil shed more than 6.5% on Friday, other Canadian oil companies were severely pressured as well, while Saudi Arabian oil is 0.18% down in Tadawul this morning.

As per crude oil, the price jumped as a kneejerk reaction to Trump tariffs, as Canadian and Mexican crude oil imports are particularly impactful, given that these countries are among the largest suppliers of crude oil to the US. But the gains remained short-lived above the 200-DMA and the price of crude is back to Friday’s closing level as the shattered prospects of global growth will likely outweigh the geopolitical risks and keep the upside potential limited. Brent on the other hand gives a different reaction to Trump’s tariff threats as Brent is less exposed to the US trade policies. While Brent is expected to follow WTI due to general market sentiment, the effect should be less pronounced because its supply chain is not directly affected by US tariffs.

French Budget Talks Enter Final Stage

In focus today

Today, focus turns to French politics as lawmakers reach the final stage of negotiating a budget agreement. Sources indicate that Bayrou intends to reduce the public deficit to 5.4% of GDP from last year's 6.2%. The budget draft will be debated in the National Assembly today, and Bayrou is likely to pass the bill without a majority.

Attention also shifts to the euro area inflation data for January. HICP inflation rates in Germany, France, and Spain were broadly unchanged compared to last month. We also forecast that euro area HICP inflation will remain at 2.4% y/y. Core inflation is projected to slightly decrease to 2.6% y/y (prior: 2.7%) due to lower services inflation. Additionally, the final release of manufacturing PMI for January should confirm the flash release that rose more than expected.

For the US, we get the ISM manufacturing index for January. Its preliminary PMI counterpart released earlier pointed towards recovering activity at the beginning of the year.

At 8.30am CET, the Swedish manufacturing PMI will be released. Recent PMIs have consistently exceeded the 50-mark (last print 52.4) outperforming France and Germany. Although the NIER manufacturing survey fell in January, we still expect a solid print above the 50-mark.

The week is packed with US data releases, including key events such as the ISM service index, JOLTs and the jobs report. On Thursday, the Bank of England will announce its rate decision.

New feature from the Danske Bank Global Research team: Personal customers in Denmark, Sweden and Finland now have access to a selection of research articles in Danske Bank's Mobile App. You will find the new feature under Investments.

Economic and market news

What happened during the weekend and overnight

Overnight in China, Caixin's early January PMI were released, mirroring last week's weak official PMI. It fell short of expectations at 50.1 (cons: 50.5, prior: 50.5), indicating slowed factory activity growth. The decline in foreign orders and average selling prices highlights pressure from rising competition and global uncertainties. However, manufacturers' sentiment has improved due to signs of increasing domestic demand and anticipated government support measures.

Over the weekend, Trump imposed new tariffs on Canada, Mexico and China, initiating a trade war with three of the US's largest trading partners. The executive order enforces a 25% tariff on imports from Canada and Mexico, excluding Canadian oil and energy products, which faces a 10% levy. Chinese imports are hit with an additional 10% tariff. The changes apply to all goods imports from countries that together account for around 45% of all US imports. In retaliation, Canada announced 25% tariffs on US goods like alcohol, clothing, household appliances and lumber, while Mexico's President Sheinbaum said the country would also launch retaliatory tariffs and other measures.

What happened Friday

In France, inflation was slightly below expectations in January, with the HICP inflation index remaining at 1.8% y/y (cons: 1.9%, prior: 1.8%). The monthly increase in seasonally adjusted services inflation was 0.0%, reinforcing the argument for further ECB rate cuts.

In Germany, CPI inflation was lower than expected in January, although the details on core services and HICP were not as weak as indicated by regional data, CPI inflation declined to 2.3% y/y (cons: 2.6%, prior: 2.6%) while HICP inflation, the measure prioritised by the ECB, remained unchanged at 2.8% y/y as expected.

In the US, the Employment Cost Index was slightly above expectations, exceeding levels that would be comfortable for the Fed if productivity growth returns to its typical pre-pandemic pace. The impact on firms' unit labour costs will be clearer this week with the release of Q4 growth productivity data. December PCE inflation aligned closely with expectations, as indicated by Thursday's Q4 figures. The EUR/USD fell slightly lower on the ECI data.

Equities: Global equities ended lower on Friday, dragged down by the US and news of US trade tariffs. Last week's and Friday's performances are somewhat secondary, as the tariffs are shifting focus and having a significant impact on markets this morning. However, let's be clear: these tariffs are being introduced at a time when we have strong macroeconomic conditions, loosening monetary policy, solid earnings and with global equities at an all-time high. Hence, the markets will be more resilient than if we were facing macroeconomic, monetary, and earnings headwinds. Nonetheless, as we are close to all-time highs after a solid January, markets will naturally get hit by the negative effects of the tariff announcements. In the US on Friday: Dow -0.8%, S&P 500 -0.5%, Nasdaq -0.3%, and Russell 2000 -0.9%.

Unsurprisingly, most Asian markets are lower this morning, including Japan, South Korea, and Taiwan, which are down by approximately 3%, despite not being the direct targets of the tariffs. However, we believe this is logical, as the tariffs should be seen through the lens of their effects on global growth. European and US futures are down 1.5-3% this morning.

FI: European rates dropped sharply on the German inflation data missing expectations. 2y German yields were down 4bp on the release, as markets may have to rethink the inflationary profile for the euro area this year. That said, with new weights and menu price adjustments it is too early to make firm conclusions. The weekend confirmation that the US is imposing 10/25/25% tariff on China/Canada/ Mexico is set to impact trading appetite this morning. While this is less than the worst-case scenarios, the announcement confirmed the tariff induced volatility on Friday. That trading sessions will continue to be vigilant on potential tariff headlines. Canada and Mexico have already said they will retaliate, while China will do "corresponding countermeasures". UST futures are up, thus 10y UST is down about 5bp in the overnight session.

FX: Tariffs shook the markets on Friday with a volatile session in FX. At the end of the day, US equity indexes closed in negative territory and the USD gained vs its G10 peers. President Trump confirmed over the weekend that steep tariffs on Canada, Mexico and China will apply from Tuesday alongside threats that EU will be targeted as well. Canada immediately responded by setting tariffs on US goods, while other counterparties indicate that they are ready to retaliate. EUR/USD has dropped further to around 1.02 from Friday's close at 1.0362, USD/CAD has traded a multi-year high just shy of 1.48 and the MXN is being hit as well. Equity futures are firmly in red indicating a sour opening. While the correlation between equities and EUR/Scandies has been poor recently, the risk in EUR/SEK and EUR/NOK is probably skewed to the upside if markets stay sour although the fundamental impact would also depend on the design of any possibly tariffs directed toward Europe. Besides tariff jitters, focus is on today's EA CPI and the global batch of confidence numbers.

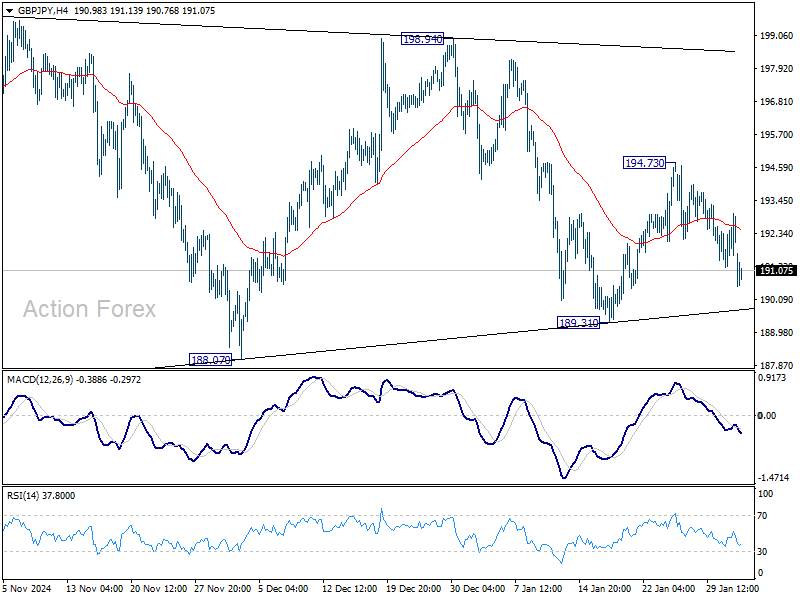

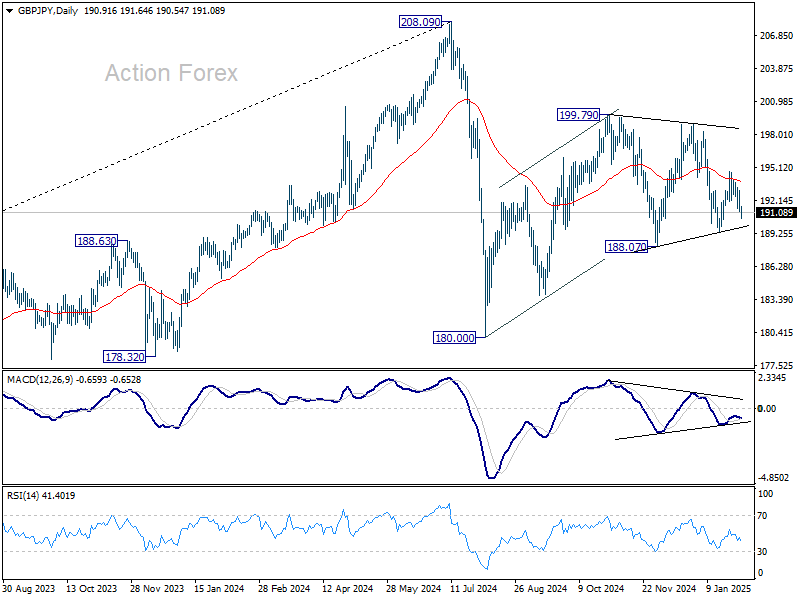

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.32; (P) 192.18; (R1) 193.17; More...

Intraday bias in GBP/JPY remain son the downside as fall from 194.73 continues. Firm break of 189.31 support will suggest that corrective pattern from 180.00 has completed. But before that, the pattern could still extend. Break of 194.73 will bring stronger rebound instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

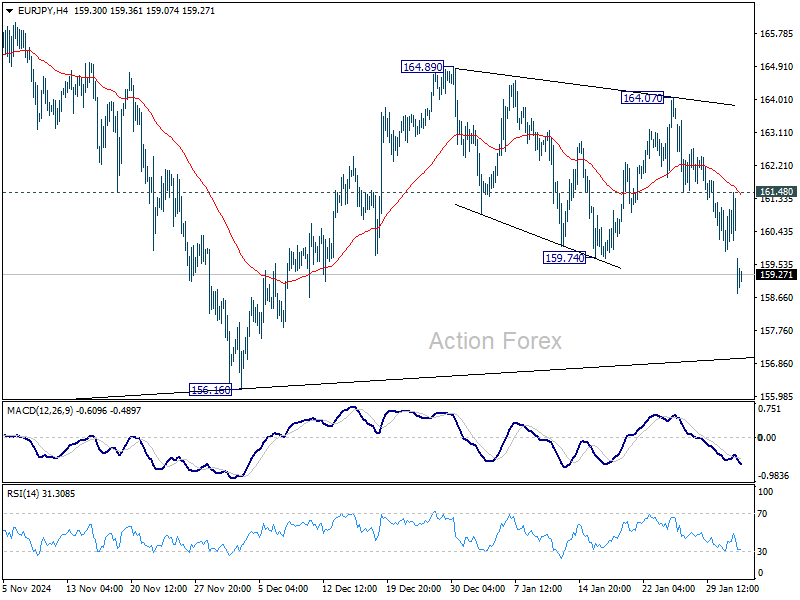

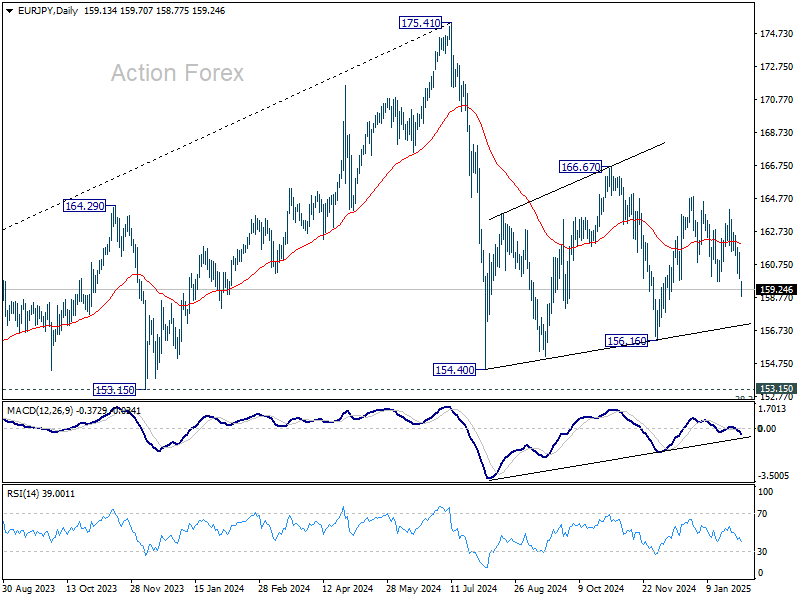

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.94; (P) 160.72; (R1) 161.54; More...

EUR/JPY's strong break of 159.74 support confirms resumption of whole fall from 164.89. Intraday bias is back on the downside for 156.16 support next. Overall, consolidation pattern from 154.40 could still extend. Above 161.48 minor resistance will turn bias back to the upside for 164.07 resistance.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

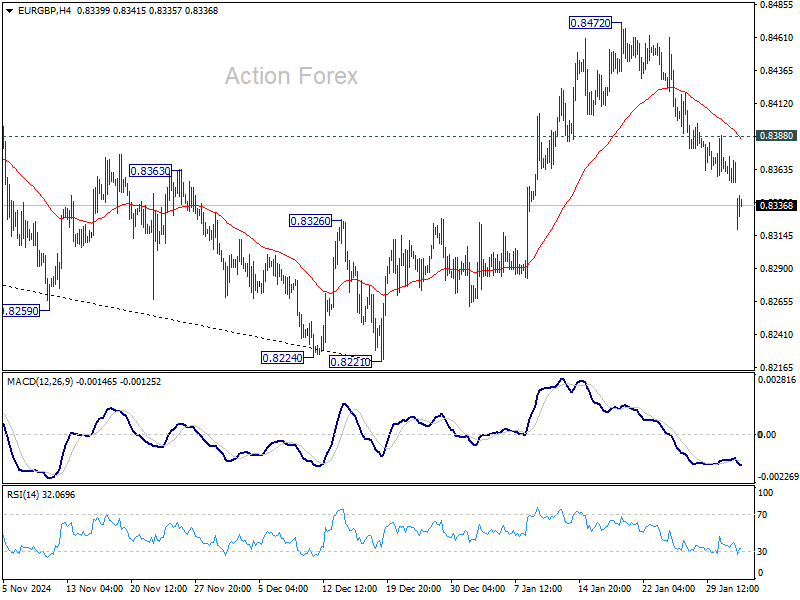

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8346; (P) 0.8367; (R1) 0.8379; More...

EUR/GBP's strong break of 55 D EMA (now at 0.8355) suggests that rebound from 0.8221 has completed at 0.8472 as a corrective move. Intraday bias stays on the downside for retesting 0.8221 low. On the upside, above 0.8388 minor resistance will turn intraday bias neutral first.

In the bigger picture, a medium term bottom should be in place at 0.8221, just ahead of 0.8201 key support (2022 low). Sustained trading above 55 W EMA (now at 0.8442) will pave the way to 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621), even just as a correction to the down trend from 0.9267 (2022 high). But still, medium term outlook will be neutral at best as long as 0.8621/4 holds.

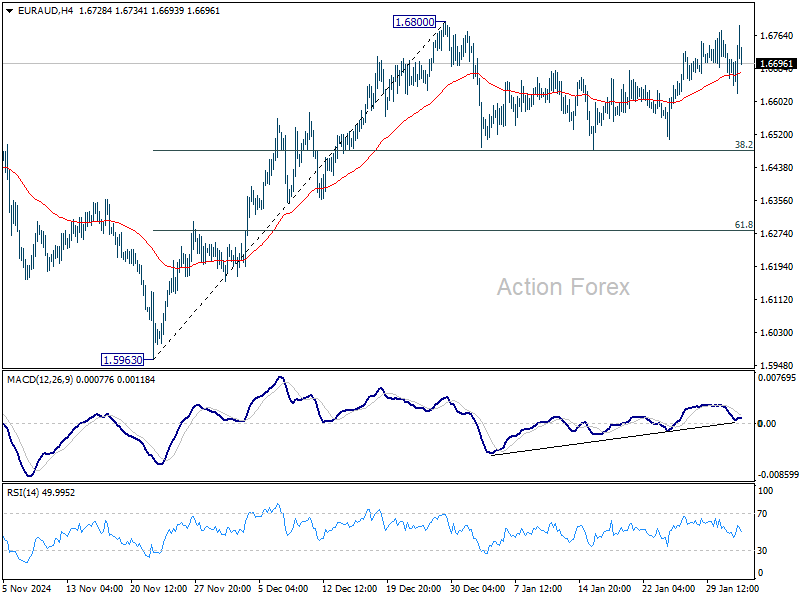

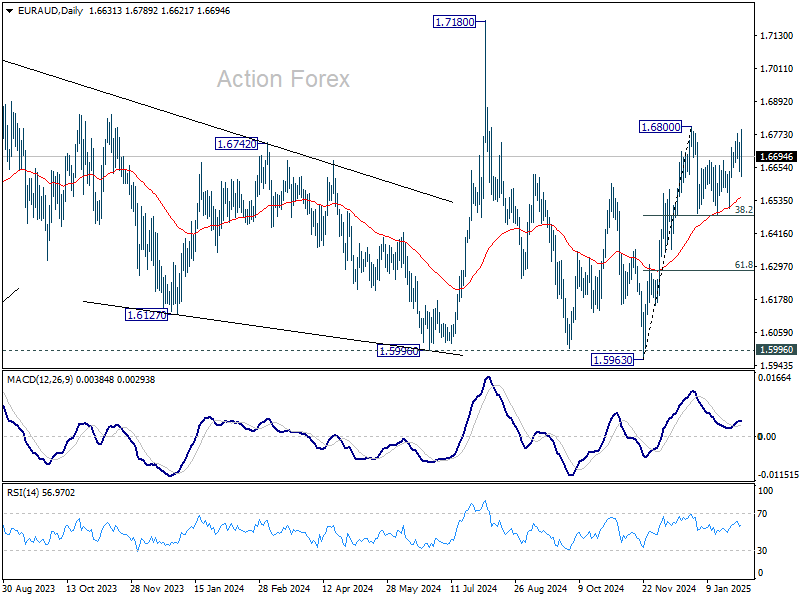

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6631; (P) 1.6690; (R1) 1.6738; More...

EUR/AUD is still bounded in range trading below 1.6800 and intraday bias remains neutral. In case of another dip, strong support is expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. On the upside, firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support (2024 low) despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

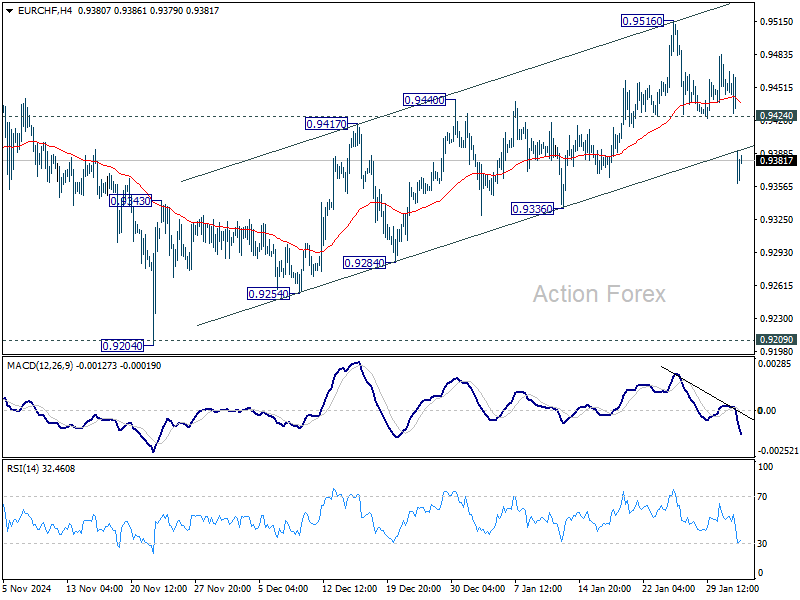

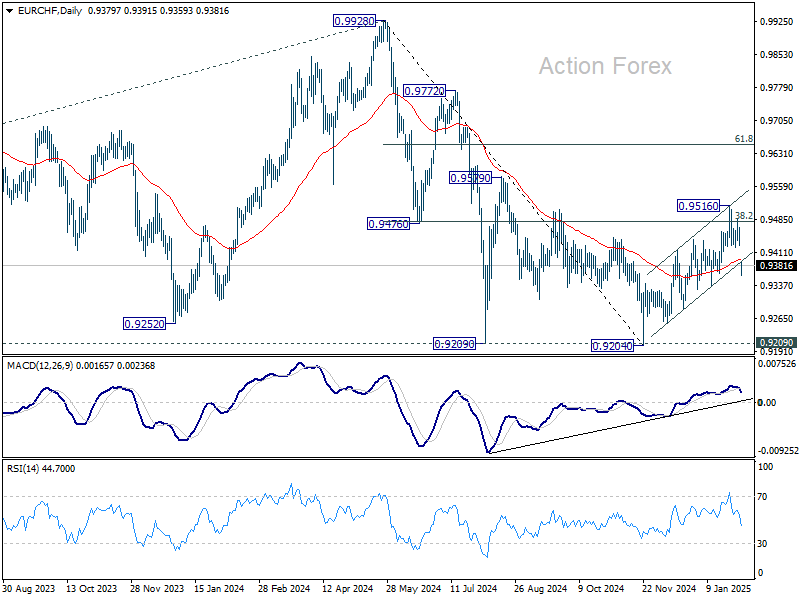

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9420; (P) 0.9448; (R1) 0.9469; More....

EUR/CHF's steep decline and break of near term channel support argues that corrective rebound from 0.9204 has completed at 0.9516 already. Intraday bias is back on the downside for 0.9336 support first. Firm break there will solidify this bearish case and target a retest on 0.9204 low. On the upside, though, above 0.9424 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, current development argues that rebound from 0.9204 has completed as a corrective move after failing to sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Firm break of 0.9204/9 support zone will confirm larger down trend resumption.

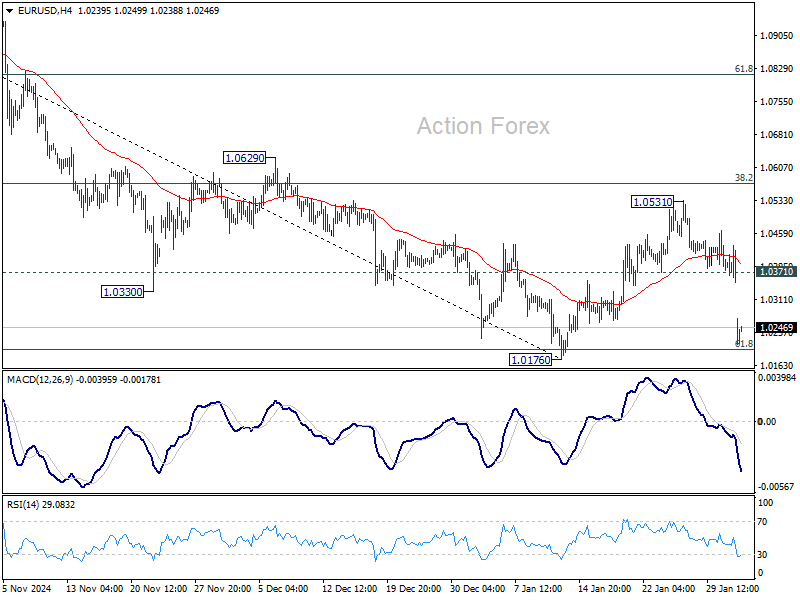

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0328; (P) 1.0381; (R1) 1.0412; More...

EUR/USD's steep decline and strong break of 1.0371 minor support suggests that corrective recovery from 1.0176 has completed at 1.0531 already. Intraday bias is back on the downside for 1.0176 support. Firm break there will resume whole fall from 1.1274. For now, outlook will remain bearish as long as y 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds, in case consolidation from 1.0176 extends with another rebound.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0693) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

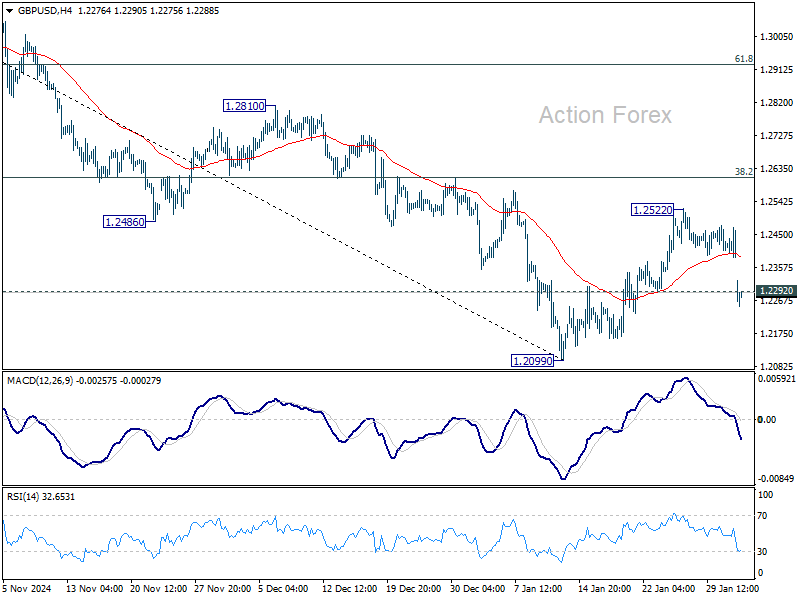

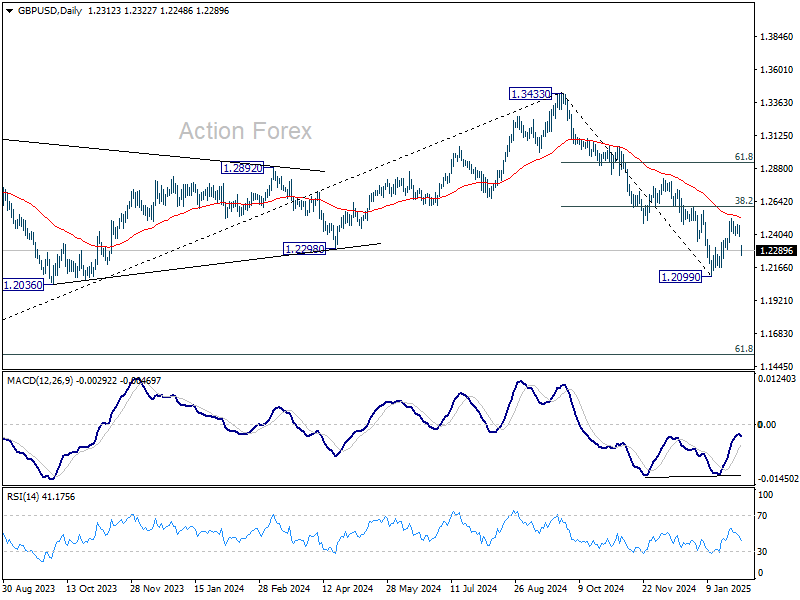

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2361; (P) 1.2416; (R1) 1.2447; More...

GBP/USD's break of 1.2292 minor support suggests that corrective recovery from 1.2099 has completed at 1.2522. Intraday bias is back on the downside for retesting 1.2099 first. Firm break there will resume whole decline from 1.3433. In case of another rise as corrective move from 1.2099 extends, upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

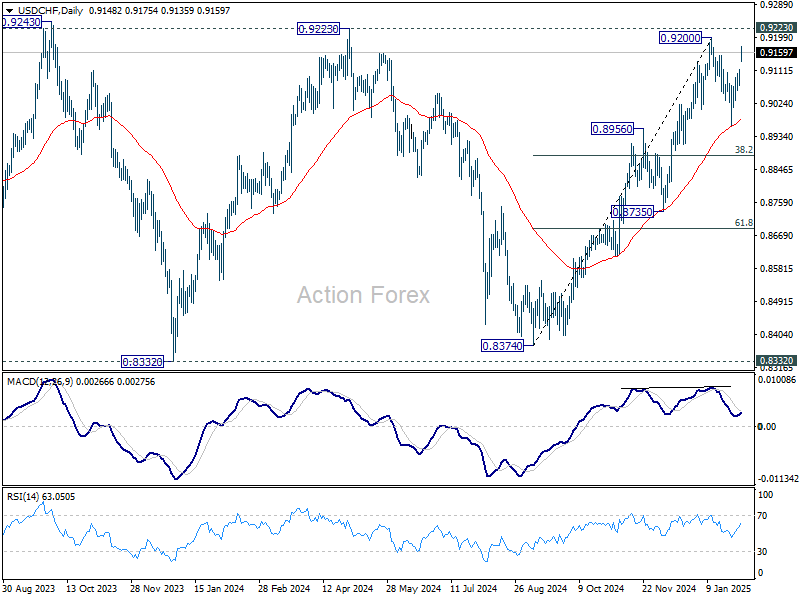

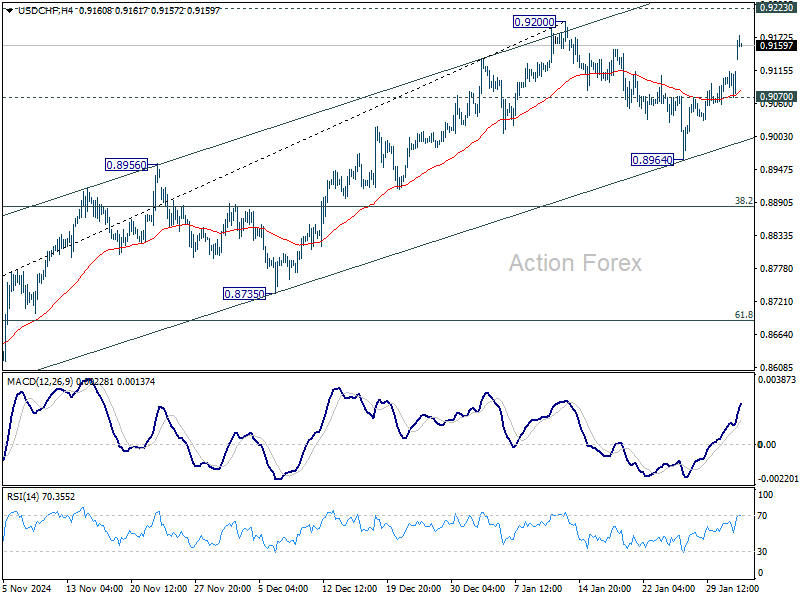

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9083; (P) 0.9099; (R1) 0.9129; More…

Intraday bias in USD/CHF stays on the upside for the moment. Break of 0.9200 will resume the whole rise from 0.8374. Further decisive break of 0.9223 key resistance will carry larger bullish implications. On the downside, below 0.9070 minor support will turn intraday bias neutral first. But outlook will now stay bullish as long as 0.8964 support holds.

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.