Sample Category Title

Summary 2/3 – 2/7

Monday, Feb 3, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Dec | -0.70% | 0.80% |

| 00:30 | AUD | Building Permits M/M Dec | 1.00% | -3.60% |

| 00:30 | JPY | Manufacturing PMI Jan F | 48.8 | 48.8 |

| 01:45 | CNY | Caixin Manufacturing PMI Jan | 50.5 | 50.5 |

| 08:30 | CHF | Manufacturing PMI Jan | 48.4 | |

| 08:50 | EUR | France Manufacturing PMI Jan F | 45.3 | 45.3 |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 44.1 | 44.1 |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 46.1 | 46.1 |

| 09:30 | GBP | Manufacturing PMI Jan F | 48.2 | 48.2 |

| 10:00 | EUR | Eurozone CPI Y/Y Jan P | 2.40% | 2.40% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan P | 2.60% | 2.70% |

| 14:30 | CAD | Manufacturing PMI Jan | 52.2 | |

| 14:45 | USD | Manufacturing PMI Jan F | 50.1 | 50.1 |

| 15:00 | USD | ISM Manufacturing PMI Jan | 49.3 | 49.3 |

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 52.6 | 52.5 |

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 45.3 | |

| 15:00 | USD | Construction Spending M/M Dec | 0.30% | 0.00% |

| 21:45 | NZD | Building Permits M/M Dec | 5.30% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | -0.50% | -1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Dec | |

| Forecast: -0.70% | Previous: 0.80% | ||

| 00:30 | AUD | Building Permits M/M Dec | |

| Forecast: 1.00% | Previous: -3.60% | ||

| 00:30 | JPY | Manufacturing PMI Jan F | |

| Forecast: 48.8 | Previous: 48.8 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jan | |

| Forecast: 50.5 | Previous: 50.5 | ||

| 08:30 | CHF | Manufacturing PMI Jan | |

| Forecast: | Previous: 48.4 | ||

| 08:50 | EUR | France Manufacturing PMI Jan F | |

| Forecast: 45.3 | Previous: 45.3 | ||

| 08:55 | EUR | Germany Manufacturing PMI Jan F | |

| Forecast: 44.1 | Previous: 44.1 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | |

| Forecast: 46.1 | Previous: 46.1 | ||

| 09:30 | GBP | Manufacturing PMI Jan F | |

| Forecast: 48.2 | Previous: 48.2 | ||

| 10:00 | EUR | Eurozone CPI Y/Y Jan P | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan P | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 14:30 | CAD | Manufacturing PMI Jan | |

| Forecast: | Previous: 52.2 | ||

| 14:45 | USD | Manufacturing PMI Jan F | |

| Forecast: 50.1 | Previous: 50.1 | ||

| 15:00 | USD | ISM Manufacturing PMI Jan | |

| Forecast: 49.3 | Previous: 49.3 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | |

| Forecast: 52.6 | Previous: 52.5 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Jan | |

| Forecast: | Previous: 45.3 | ||

| 15:00 | USD | Construction Spending M/M Dec | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 21:45 | NZD | Building Permits M/M Dec | |

| Forecast: | Previous: 5.30% | ||

| 23:50 | JPY | Monetary Base Y/Y Jan | |

| Forecast: -0.50% | Previous: -1.00% | ||

Tuesday, Feb 4, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 15:00 | USD | Factory Orders M/M Dec | -0.70% | -0.40% |

| 21:45 | NZD | Employment Change Q4 | -0.20% | -0.50% |

| 21:45 | NZD | Unemployment Rate Q4 | 5.10% | 4.80% |

| 21:45 | NZD | Labour Cost Index Q/Q Q4 | 0.60% | 0.60% |

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | 3.80% | 3.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 15:00 | USD | Factory Orders M/M Dec | |

| Forecast: -0.70% | Previous: -0.40% | ||

| 21:45 | NZD | Employment Change Q4 | |

| Forecast: -0.20% | Previous: -0.50% | ||

| 21:45 | NZD | Unemployment Rate Q4 | |

| Forecast: 5.10% | Previous: 4.80% | ||

| 21:45 | NZD | Labour Cost Index Q/Q Q4 | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | |

| Forecast: 3.80% | Previous: 3.00% | ||

Wednesday, Feb 5, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Services PMI Jan F | 52.7 | 52.7 |

| 01:45 | CNY | Caixin Services PMI Jan | 52.3 | 52.2 |

| 07:45 | EUR | France Industrial Output M/M Dec | -0.10% | 0.20% |

| 08:50 | EUR | France Services PMI Jan F | 48.9 | 48.9 |

| 08:55 | EUR | Germany Services PMI Jan F | 52.5 | 52.5 |

| 09:00 | EUR | Eurozone Services PMI Jan F | 51.4 | 51.4 |

| 09:30 | GBP | Services PMI Jan F | 51.2 | 51.2 |

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.50% | 1.60% |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | -1.20% | |

| 13:15 | USD | ADP Employment Change Jan | 149K | 122K |

| 13:30 | USD | Trade Balance (USD) Dec | -97.1B | -78.2B |

| 13:30 | CAD | Trade Balance (CAD) Dec | 0.4B | -0.3B |

| 14:45 | USD | Services PMI Jan F | 52.8 | 52.8 |

| 15:00 | USD | ISM Services PMI Jan | 54.2 | 54.1 |

| 15:30 | USD | Crude Oil Inventories | 3.5M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Services PMI Jan F | |

| Forecast: 52.7 | Previous: 52.7 | ||

| 01:45 | CNY | Caixin Services PMI Jan | |

| Forecast: 52.3 | Previous: 52.2 | ||

| 07:45 | EUR | France Industrial Output M/M Dec | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 08:50 | EUR | France Services PMI Jan F | |

| Forecast: 48.9 | Previous: 48.9 | ||

| 08:55 | EUR | Germany Services PMI Jan F | |

| Forecast: 52.5 | Previous: 52.5 | ||

| 09:00 | EUR | Eurozone Services PMI Jan F | |

| Forecast: 51.4 | Previous: 51.4 | ||

| 09:30 | GBP | Services PMI Jan F | |

| Forecast: 51.2 | Previous: 51.2 | ||

| 10:00 | EUR | Eurozone PPI M/M Dec | |

| Forecast: 0.50% | Previous: 1.60% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Dec | |

| Forecast: | Previous: -1.20% | ||

| 13:15 | USD | ADP Employment Change Jan | |

| Forecast: 149K | Previous: 122K | ||

| 13:30 | USD | Trade Balance (USD) Dec | |

| Forecast: -97.1B | Previous: -78.2B | ||

| 13:30 | CAD | Trade Balance (CAD) Dec | |

| Forecast: 0.4B | Previous: -0.3B | ||

| 14:45 | USD | Services PMI Jan F | |

| Forecast: 52.8 | Previous: 52.8 | ||

| 15:00 | USD | ISM Services PMI Jan | |

| Forecast: 54.2 | Previous: 54.1 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 3.5M | ||

Thursday, Feb 6, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | -6 | |

| 00:30 | USD | Fed's Jefferson speech | ||

| 00:30 | AUD | Trade Balance M/M Dec | 6.73B | 7.08B |

| 06:45 | CHF | Unemployment Rate M/M Jan | 2.70% | 2.60% |

| 07:00 | EUR | Germany Factory Orders M/M Dec | 1.70% | -5.40% |

| 09:30 | GBP | Construction PMI Jan | 53.7 | 53.3 |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -0.10% | 0.10% |

| 12:00 | GBP | BoE Interest Rate Decision | 4.50% | 4.75% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--8--1 | 0--3--6 |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | 11.40% | |

| 13:30 | USD | Initial Jobless Claims (Jan 31) | 214K | 207K |

| 13:30 | USD | Nonfarm Productivity Q4 P | 1.80% | 2.20% |

| 13:30 | USD | Unit Labor Costs Q4 P | 3.30% | 0.80% |

| 15:00 | CAD | Ivey PMI Jan | 54.7 | |

| 15:30 | USD | Natural Gas Storage | -321B | |

| 23:30 | JPY | Household Spending Y/Y Dec | 0.30% | -0.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | |

| Forecast: | Previous: -6 | ||

| 00:30 | USD | Fed's Jefferson speech | |

| Forecast: | Previous: | ||

| 00:30 | AUD | Trade Balance M/M Dec | |

| Forecast: 6.73B | Previous: 7.08B | ||

| 06:45 | CHF | Unemployment Rate M/M Jan | |

| Forecast: 2.70% | Previous: 2.60% | ||

| 07:00 | EUR | Germany Factory Orders M/M Dec | |

| Forecast: 1.70% | Previous: -5.40% | ||

| 09:30 | GBP | Construction PMI Jan | |

| Forecast: 53.7 | Previous: 53.3 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.75% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--8--1 | Previous: 0--3--6 | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | |

| Forecast: | Previous: 11.40% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 31) | |

| Forecast: 214K | Previous: 207K | ||

| 13:30 | USD | Nonfarm Productivity Q4 P | |

| Forecast: 1.80% | Previous: 2.20% | ||

| 13:30 | USD | Unit Labor Costs Q4 P | |

| Forecast: 3.30% | Previous: 0.80% | ||

| 15:00 | CAD | Ivey PMI Jan | |

| Forecast: | Previous: 54.7 | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -321B | ||

| 23:30 | JPY | Household Spending Y/Y Dec | |

| Forecast: 0.30% | Previous: -0.40% | ||

Friday, Feb 7, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Dec P | 108.1 | 107.5 |

| 07:00 | EUR | Germany Industrial Production M/M Dec | -0.70% | 1.50% |

| 07:00 | EUR | Germany Trade Balance (EUR) Dec | 17.1B | 19.7B |

| 07:45 | EUR | France Trade Balance (EUR) Dec | -5.3B | -7.1B |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Jan | 731B | |

| 13:30 | USD | Nonfarm Payrolls Jan | 154K | 256K |

| 13:30 | USD | Unemployment Rate Jan | 4.10% | 4.10% |

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.30% |

| 13:30 | CAD | Net Change in Employment Jan | 26.5K | 90.9K |

| 13:30 | CAD | Unemployment Rate Jan | 6.80% | 6.70% |

| 15:00 | USD | Wholesale Inventories Dec F | -0.50% | -0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Dec P | |

| Forecast: 108.1 | Previous: 107.5 | ||

| 07:00 | EUR | Germany Industrial Production M/M Dec | |

| Forecast: -0.70% | Previous: 1.50% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Dec | |

| Forecast: 17.1B | Previous: 19.7B | ||

| 07:45 | EUR | France Trade Balance (EUR) Dec | |

| Forecast: -5.3B | Previous: -7.1B | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Jan | |

| Forecast: | Previous: 731B | ||

| 13:30 | USD | Nonfarm Payrolls Jan | |

| Forecast: 154K | Previous: 256K | ||

| 13:30 | USD | Unemployment Rate Jan | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 13:30 | USD | Average Hourly Earnings M/M Jan | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | CAD | Net Change in Employment Jan | |

| Forecast: 26.5K | Previous: 90.9K | ||

| 13:30 | CAD | Unemployment Rate Jan | |

| Forecast: 6.80% | Previous: 6.70% | ||

| 15:00 | USD | Wholesale Inventories Dec F | |

| Forecast: -0.50% | Previous: -0.50% | ||

A U.S.-Canada Trade Shock Now in Play: First Economic Takeaways

Canada has been hit with its largest trade shock in nearly 100 years. RBC Economics now finds itself balancing the desire to produce a clear analysis with the recognition that the evolution of trade policies, and policymakers’ responses to them, still remains highly uncertain. Still, we now have a growing list of “knowns” compared to a week ago, allowing us to analyze this shock with greater confidence. As the landscape continues to evolve, RBC Economics will provide updates to our outlook, helping to build a deeper understanding of this major economic event. We continue to lean heavily on the RBC Economics Playbook To Measure A Tariff Shock as a model for assessing the outlook amid these uncertainties.

- This is the most significant trade shock since the Smoot-Hawley tariffs of the 1930s, which are widely blamed for exacerbating and prolonging the Great Depression. This shock far surpasses the 2018 tariffs in magnitude, diminishing the value of that period as a helpful guide for the economic impact ahead. For context, in 2018, the U.S. average import tariff rose from 1.5% to roughly 3%. Under the new policy, the U.S. average tariff rate to nearly 11%, the highest average ratio since the 1940s. More importantly, this policy signifies a fundamental shift in a trade order that has endured for nearly a century, challenging the core economic principle that frictionless trade is a superior model.

- A persistent tariff of this magnitude is recessionary for Canada. If sustained, our initial analysis suggests that tariffs of this size (based on many assumptions) could wipe out Canadian growth for up to three years, with the largest impacts in the first and second years. Our estimates align to the Bank of Canada’s findings which simulate that a 25% increase in tariffs across the board (U.S. and global) would reduce Canadian GDP ranging from -3.4 to -4.2 percentage points, compared to the baseline forecast. Similarly, an earlier model from the Bank of Canada estimated that GDP could drop by as much as 6 percentage points. By our calculations, such reductions could push Canadian unemployment rates up by between 2 to 3 percentage points. While the precise impact depend on a variety of assumptions – including monetary and fiscal policy responses – this is a significant negative shock to Canadian growth and poses a serious risks of unemployment rate increases.

- Canadian retaliatory measures (25% on $155bn CAD, phased in) appear designed to asymmetrically challenge the U.S economy more than the Canadian economy. However, they will still function like tariffs do for any imposing country – by lowering growth and raising inflation on targeted goods. In the days ahead, we will focus on identifying where Canadians are most likely to experience inflationary pressures from these measures.

- Canada’s manufacturing sector is most exposed, but the knock-on effects will also matter in many other indirectly exposed industries. As we’ve covered before, Canada’s manufacturing sector – which accounts for approximately 9% of Canada’s GDP and 70% of total trade with the U.S. – is particularly vulnerable to tariff impacts. Canada’s top 15 industries by trade with the United States, most of which are manufacturing based, represent nearly 3.1% of the country’s total workforce. A key area of concern is Canada’s motor vehicles sector, which is exceptionally integrated with the United States and Mexico. Parts can cross the border multiple times, meaning an end-product like a car may incur several rounds of tariffs.

Notably, Canadian raw commodity exports are less likely to see a drop in U.S. demand as Americans lack substitutes for these goods. This likely encouraged a lower 10% tariff on energy products for Americans, as this particular imported good is one of the most likely to create a larger and more immediate inflationary burden for American producers and consumers.

As outlined in our tariff playbook, we are mindful that secondary industries in the services sector, for example, are also likely to feel knock-on effects. Consider an auto plant that experiences reduced demand and is forced to lay off workers. These workers, in turn, are less likely to then go to restaurants, movie theatres or engage in other “discretionary” spending. This ripple effect leaves a variety of non-tariffed industries exposed to the broader economic shock, and are also somewhat challenging to model as they can be exacerbated by confidence and sentiment channels.

- Tariffs are hitting the Canadian economy at a moment during which it is already struggling. Canada is still recovering from a major interest rate shock, and even as the Bank of Canada has cut interest rates by 200bps, the unemployment rate continues to rise, with the country is still operating with excess supply and below full capacity. GDP per capita has declined for eight of the past nine quarters, and business investment has been stagnant. Both cyclically and structurally, Canada’s economy is not well positioned to absorb a shock of this scale.

- Tariffs will also be damaging to the U.S. economy. While the U.S. economy is starting from a relative place of strength (and is far less reliant on trade), it will face a shock large enough to adjust most forecasts downward on growth and upwards on inflation. Additional retaliatory policies from Canada and/or Mexico will likely exacerbate these impacts.

Like in Canada, certain American regions and sectors will be more exposed. The U.S. manufacturing sector, in particular, has already been underperforming. Industrial production is little changed from a year ago and the sector has on aggregate shrunk since 2017. Washington’s tariffs are likely to hurt U.S. manufacturing competitiveness further and, worse, as we have argued before will not lead to significant re-shoring of manufacturing capacity.

Moreover, comparisons to 2018 tariffs imposed upon China understate the economic impact for Americans. Canada and Mexico account for a combined 29% of U.S. imports as of 2023 (13.6% from Canada, 15.4% from Mexico) – more than twice the share combined compared to China (13.8%). In 2023, Canada was the top import source for 23 U.S. states and second largest for 11. Canada was also the top export destination for 36 states, and the second most important for another 8.

What We Are Watching For Next

The scope of economic impacts for Canada (and the U.S.) remains significant and, even with robust economic models, requires a consideration number of assumptions. As we continue to adjust our outlook based on new developments, the following elements will be critical variables:

Items that will worsen the impact

- Duration of the tariffs: Tariffs removed within a matter of weeks are likely to create a temporary stall for Canada. However, if they extend over a matter months (e.g. 3-6 months), Canada’s recessionary risks increase rapidly. The duration of the tariff isn’t just about the immediate shock (or recession) – the longer the tariffs last, the greater the structural damage (i.e. permanent) on the economy. For example, Canada’s manufacturing sector (the most trade sensitive) accounts for more than 10% of total Canadian business investment, and almost a quarter of total Canadian machinery and equipment investment. A prolonged slowdown in investment in this sector will further reduce Canadian economic potential in the longer-run and require an even larger long-term adjustment.

- Evolution of retaliatory measures or escalation of U.S. tariffs. Canada’s retaliatory measures appear aimed at reducing the duration of U.S. tariffs. However, additional adjustments in Canada (and Mexico) could further alter forecasts. Moreover, if the U.S. follows through on its threats to escalate tariffs in response to retaliation, we will need to make further additional adjustments in our analysis.

Items that can soften the impact

- A weaker Canadian dollar (stronger U.S dollar): The Canadian dollar has already weakened by 7% in the past 12 months and a further full offset equivalent to the 25% tariff/price increase seems unlikely. That said, any additional weakness in the Canadian dollar will buffer the price shock for Americans and reduce the expected drop in demand for Canadian tariffed goods.

- An appropriate fiscal policy response: Beyond the decisions around retaliatory measures, governments will have to make a series of choices and trade-offs around how they support Canadians through a recessionary-type environment, going above and beyond traditional “automatic” stabilizers. A tariff shock differs from a pandemic shock – it represents a structural shift in two countries’ most important trading relationship. There is no ‘unpause’ button on a trade conflict, even after the tariffs are potentially removed, and thus fiscal policy will not simply act as a bridge from one side to another, but also the investment in Canada’s next economic chapter. In that context, Canadian governments will now need to navigate:

- The right amount of support. Unlike the global pandemic or Great Financial Crisis, Canada is experiencing (along with Mexico) an economic shock that is mostly unique to its economy – it won’t be expanding its deficit or debt level along with its global peers and thus benefit from “relative” comparisons by global bond markets. With federal finances already pushing up closely to so-called “fiscal anchors”, the rainy day fund isn’t as flush as some would have hoped. Meanwhile, excess spending should the length of the trade conflict be (hopefully) short, could exacerbate inflationary pressures that Canada is only now overcoming, complicating the job of the Bank of Canada. Given the length of the conflict is likely more determined in Washington than Ottawa, this represents a particular challenge.

- The right targets for support: The tariff shock is, likely to flow through both the goods and services side of the economy, but it will absolutely hit some areas much more than others. Broad-based support, as we saw in the pandemic, is likely to be less effective than appropriately targeted support that stops the bleed from tariffed sectors to non-tariffed sectors. Decoding which sectors need the urgent support will be a critical first step. We will write more on this in the coming weeks.

- The balance of short-term vs. long-term support: the longer the tariff shock, the more Canada will have to spend to re-orient its economy towards a shifting trade order. That will have to happen in parallel with near-term support to soften the depths of a possible recession. Unlike the pandemic, we suspect that even a reversal of U.S. tariff policy would not eliminate a growing thirst for Canadian trade diversity and economic independence will grow in the years ahead.

- A supportive monetary policy response: Our base case expectation has been that the BoC was already on its way to cutting interest rates to about 2% by year-end 2025 and we suspect a tariff shock that produces a recession (even if it has inflationary elements) would put the BoC on an even more dovish track. All central banks are challenged by tariff shocks because they tend to raise prices but also lower growth. Further, the monetary policy response will need to be calibrated with the fiscal response ahead (more fiscal implies less need for monetary and vice versa). Our expectation is that, based on what we know now, the risks of additional easing over the baseline expectations for 2025 is growing. Regardless, we’ll be monitoring for commentary (and/or) action from the BoC that would ameliorate interest rate burdens (and indirectly help support further weakening of the Canadian dollar).

What Next: US Job Market and BoE Rate Decision

The new week will focus on the US labour market and the UK rate decision.

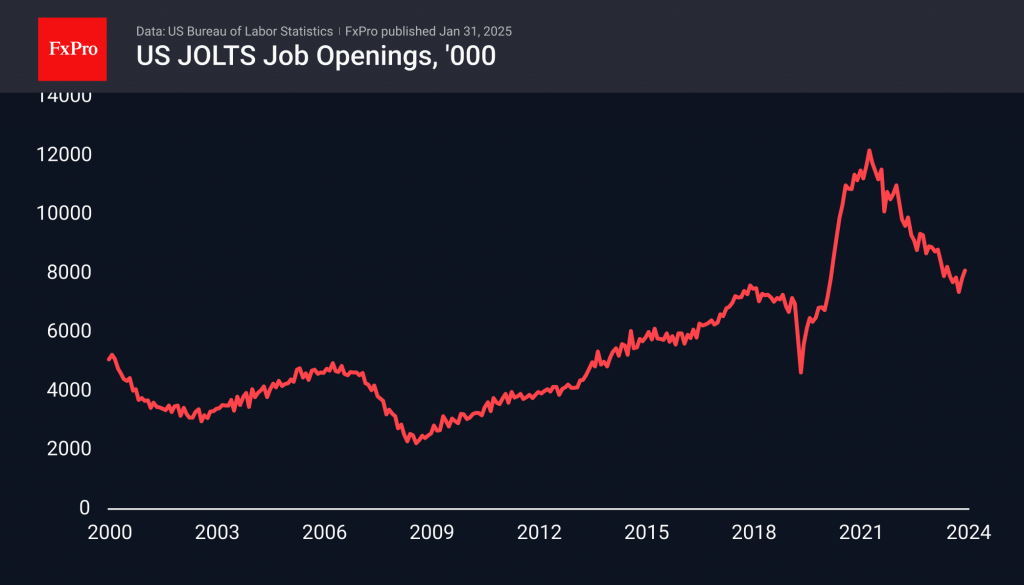

On Tuesday, 4 February, the focus is on the new US job opening statistics. The indicator’s fall over the past two years was viewed with alarm, but the figure has stabilised in the region of the 2019 highs. A rise would be a strong positive signal.

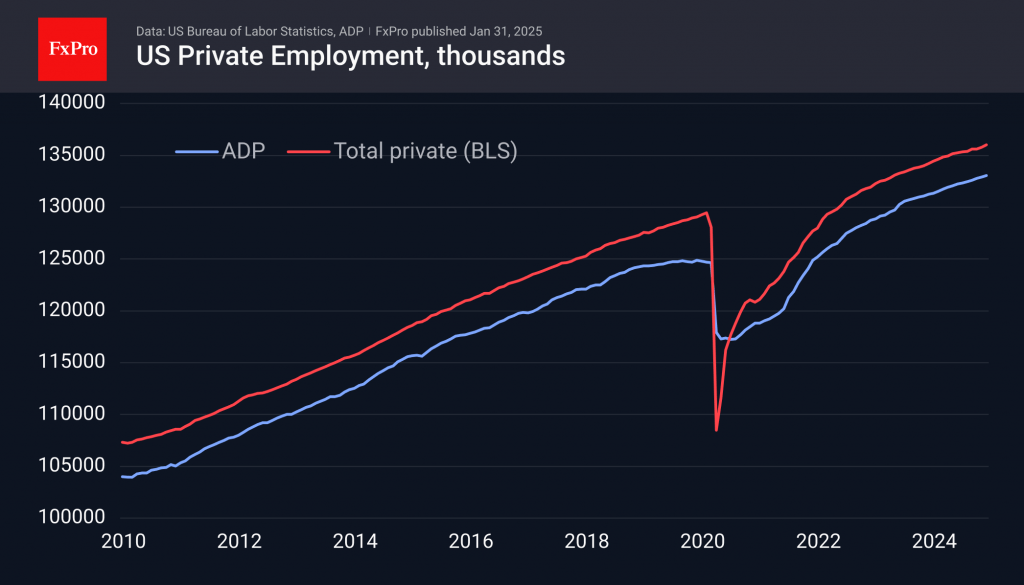

Wednesday, 5 February, sees the release of ADP private sector employment data. This is the closest indicator to Friday’s NFP. The indicator has been adding at a slightly below-trend pace in recent months, but so far, the labour market as a whole has not turned around. Surprises can’t be ruled out here, though.

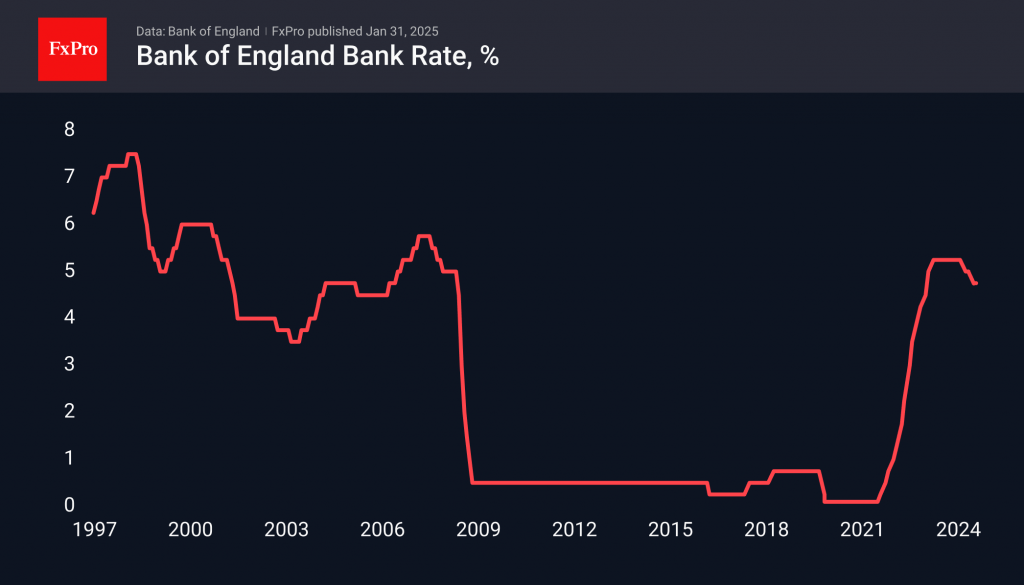

On Thursday, 6 February, the focus is on the Bank of England’s key rate decision. Markets are expecting a 25-point cut. The central forecast is for two more cuts within a year. Signalling a change in this expected trajectory will be the main driver of UK markets. More declines will increase pressure on the pound.

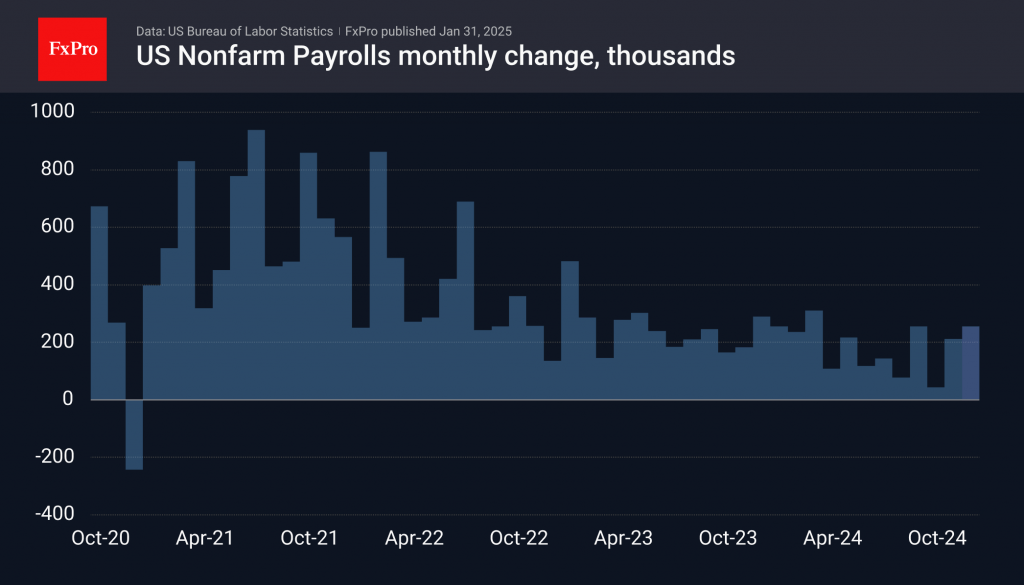

On Friday, 7 February, all eyes are on Nonfarm Payrolls. Often, markets are quiet, going into a waiting mode a day before the release. The last couple of months have seen growth rates above the trend of 200K, also working to strengthen the dollar. However, strong data can also trigger a sell-off in stocks.

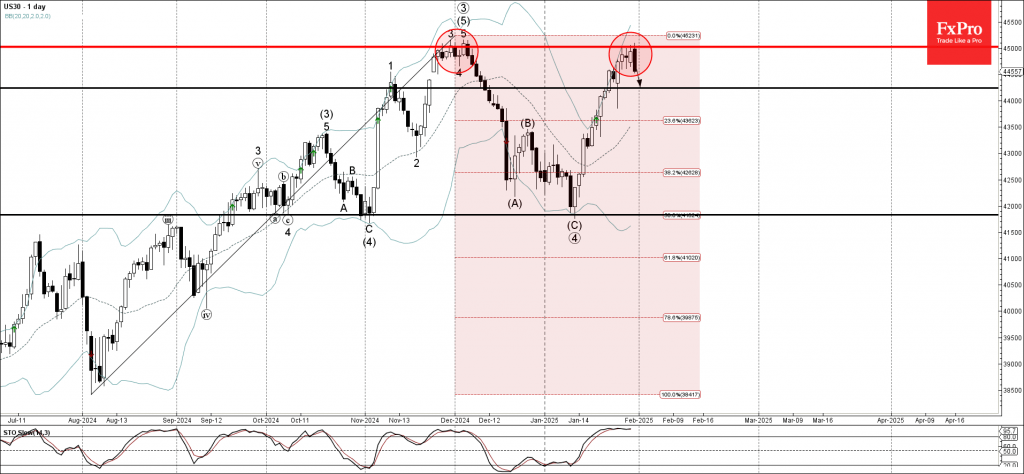

Dow Jones index Wave Analysis

- Dow Jones reversed from strong resistance level 45000.00

- Likely to fall to support level 44235.00

Dow Jones index today reversed down from the resistance area located between the strong resistance level 45000.00 (which stopped the previous multi-month uptrend in November) and the upper daily Bollinger Band.

The downward reversal from this resistance area will most likely form the daily Bearish Engulfing – if the price closes today near the current levels.

Given the strength of the resistance level 45000.00 and the overbought daily Stochastic, Dow Jones index can be expected to fall to the next support level 44235.00.

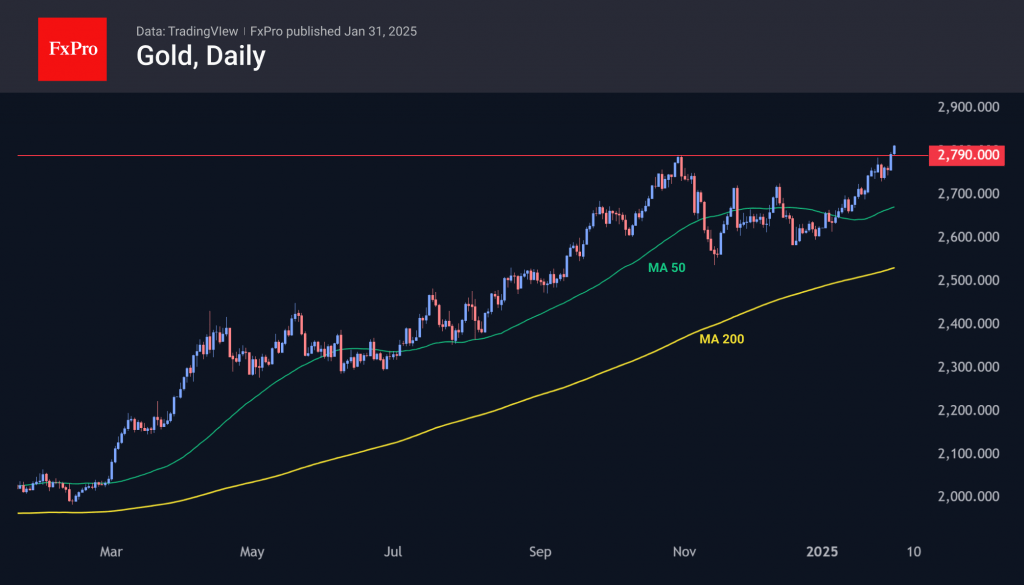

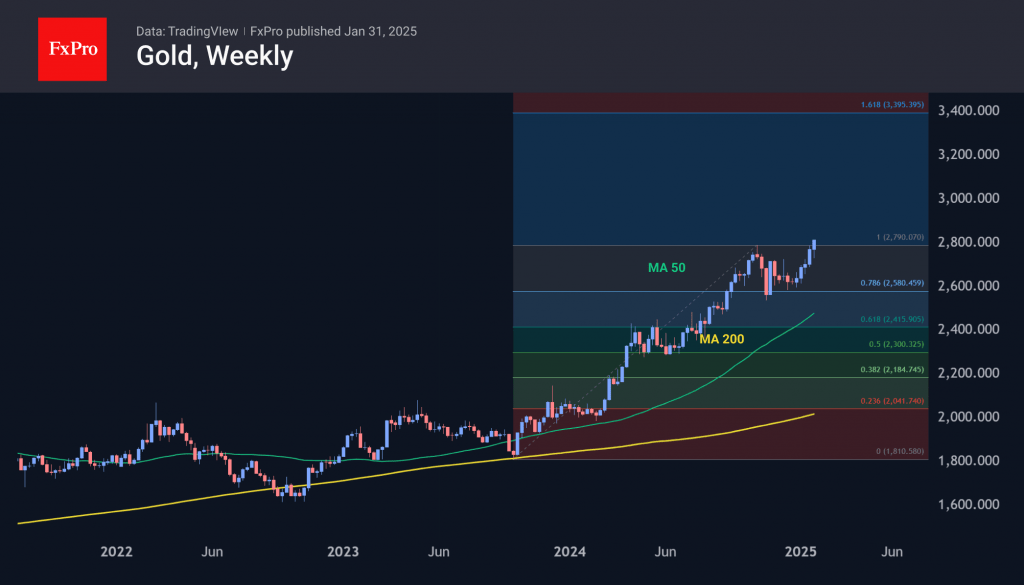

Gold on the Upswing

Gold has hit record highs, moving into territory above 2800. Strong buying following the November-December correction suggests the end of the correction phase and the beginning of a new growth cycle.

A breakout to new highs activates a Fibonacci expansion pattern. The fundamental upside momentum in gold started in October 2023 and formed a peak at the end of October 2024. This was followed by a correction to 76.4% of the initial rally, which is typical of strong bull markets. The formal technical target now looks to be the $3,400 per troy ounce area. This is more than 20% above current levels but is achievable in the two- to four-quarter timeframe.

The Weekly Bottom Line: Tariffying

Canadian Highlights

- President Trump continues to threaten Canada with a 25% tariff on its U.S. exports as early as Saturday. A prolonged U.S.-Canada trade skirmish could dampen growth significantly and lift inflation.

- The Bank of Canada cut its policy rate by 25 basis points this week, bringing it to 3.0%. A trade battle would likely warrant more rate cuts than we built into our December baseline.

- The November GDP report suggests that Canada’s economy performed well in Q4, indicating solid momentum heading into the potential trade shock.

U.S. Highlights

- The U.S. economy ended 2024 on solid footing, expanding at a 2.3% annualized pace. The consumer did the heavy lifting, with spending accelerating in the fourth quarter.

- The Fed’s preferred inflation gauge, the core PCE deflator, continued to hover somewhat above target in December, growing at 2.8% year-on-year. But trends over the past few months suggest further cooling ahead.

- Major action may come on the trade policy front as early as this weekend, with President Trump reiterating his intentions to impose tariffs on Canada and Mexico – America’s largest trading partners.

Canada – Tariffying

On Thursday President Trump reiterated his threat of a 25% tariff on Canadian imports as early as Saturday. This opens the strong possibility that Canada will retaliate with tariffs of its own, although the dollar amount of U.S. imports targeted by these tariffs isn’t yet public news. There is still some time left for lawmakers in both countries to negotiate a deal to avoid this outcome, but it seems increasingly likely that tariffs are imminent. The Canadian dollar sagged a bit on the news but is holding at around 0.69 U.S. cents as of writing. There could be even more downside if the tariffs do indeed hit.

Amid this swirling uncertainty, the Bank of Canada (BoC) cut its policy rate by 25 basis points this week, bringing it to 3.0%. This reflected the Bank’s desire to soak up excess supply in the economy. It also made sense from a risk management perspective given the potential for a significant trade shock. Because of the uncertainty on the level and extent of any imposed tariffs, the Bank’s accompanying economic forecast didn’t explicitly build them in. In this “optimistic” scenario, GDP was seen as expanding by 1.8% both in 2025 and 2026. Inflation, meanwhile, was seen as hitting 2.1% by 2025 Q4, capping off what was a solid outlook. Alas, this goldilocks outcome is now under heavy threat, and may end up being a reminder of what could have been.

Ultimately, the damage to the Canadian economy from this skirmish will be determined by how long it lasts. To get a sense of potential impacts, it’s helpful to highlight a BoC study accompanying its interest rate decision which analyzed 25% across-the-board tariffs permanently applied by the U.S. on all its trading partners, with Canada retaliating with 25% tariffs of its own. In this scenario, GDP growth was about 2 percentage points (ppts) lower than a no-tariff situation and inflation was about 0.3 ppts higher, on average, in the first two years (Chart 1). This implies that 2025 GDP growth would flip from being firmly positive, to slightly negative, using the Bank’s baseline forecast.

The Bank didn’t have to wait long for fresh news on the state of the economy. This morning’s GDP report showed a 0.2% monthly decline in November. However, GDP looks to have picked up by the same amount in December, according to Statcan’s preliminary estimate. All told, these dynamics suggest that 2024 Q4 growth was firm at around 2% (Chart 2). At least the economy had decent momentum heading into this potentially damaging trade skirmish.

How will monetary policy respond in this backdrop? According to the BoC, the answer is complicated by the fact that tariffs will negatively impact growth and lift inflation. At a minimum, tariffs would cause a one-time increase in price levels, with a potential to morph into a more sustained problem if inflation expectations are impacted. Our initial thought is that a prolonged trade battle would bolster the case for the Bank’s policy rate fall by more than what we’d imbedded in our December projection.

U.S. – Stock Market Rowdy, Economy Steady

The last week of January began on a soft note for stock markets. As it became apparent that a low-cost Chinese artificial intelligence start-up (DeepSeek) could threaten the dominance of American rivals, the valuations of several large tech firms took a hit, weighing on major indexes. Some recovery ensued later in the week, with the S&P 500 and tech-heavy NASDAQ nearly erasing the losses from last week’s close (at the time of writing). In contrast to the rowdiness of the stock market, signals out of the economy continued to point to steadiness.

The first read on fourth quarter GDP showed that the U.S. economy ended last year on a solid footing as it grew at 2.3% quarter-on-quarter annualized. The consumer did the heavy lifting, offsetting a notable drag from gross fixed private investment (Chart 1). Goods spending carried the torch once again, propelled forward by a double-digit increase in durable goods, but services also notched a mild acceleration. Meanwhile, within the softness of the broad private investment category, residential investment was a bright spot for a change, lifted by a double-digit gain in housing starts last quarter. Looking at the big picture, the fact that the economy essentially sustained 2023’s pace through 2024, despite the still elevated interest rate environment, is an impressive accomplishment.

Friday morning’s monthly PCE report provided some more detail with respect to consumption and inflation trends at the turn of the year. The handoff to the start of 2025 is solid, as real spending growth remained robust in December, growing at nearly 5% annualized. This, as strength in services helped offset some cooldown in goods spending from the double-digit gain in the month prior. Additionally, the Fed’s preferred inflation gauge – core PCE – held at 2.8% in year-on-year terms. The fact that the 3-month and 6-month annualized rate of change in core PCE inflation gravitated lower toward the target, was a welcome development (Chart 2).

With inflation still somewhat elevated (though appearing to head in the right direction) and the economy remaining on solid footing, the Fed can afford to take a cautious approach to further loosening monetary policy. The FOMC left the policy rate unchanged at this week’s meeting – a move that was widely anticipated. Fed Chair Powell acknowledged that “we don’t need to be in a hurry to adjust our policy stance”, while nodding to the uncertainties and the risks related to major policy changes out of Washington, such as on trade policy. Powell reiterated a wait-and-see approach, stating that they’d need any new policy changes to be articulated first, before assessing their impacts on the economy.

Major action on the trade front may come as early as this weekend, with President Trump reiterating his intention to impose 25% tariffs on Mexico and Canada on February 1st. There’s still a possibility that cooler heads will prevail, as President Trump’s top pick for commerce secretary suggested that tariffs could be avoided if swift action was taken on the border issues. Still, the deadline is fast approaching and any trade skirmishes with its neighbors will be problematic – the two countries are America’s largest trading partners and are deeply integrated in supply chains.

Weekly Economic & Financial Commentary: In Little Hurry to Cut Further

Summary

United States: Economic Momentum Holding, for Now

- The economy ended 2024 on a solid note with a 2.3% Q4 increase in real GDP. Volatile inventory swings lowered the headline, but real final sales to domestic private purchasers rose by a robust 3.2%. Fervent consumer spending continues to drive economic activity, while inflation is receding at a snail’s pace. That said, trends in the Employment Cost Index suggest that the labor market is no longer a meaningful source of price pressures.

- Next week: ISM Manufacturing & Services (Mon. & Wed.), Employment (Fri.)

International: Foreign Central Bank Bonanza!

- It was a busy week for foreign central banks, with several institutions offering their first monetary policy assessments of 2025. The European Central Bank lowered its Deposit Rate by 25 bps to 2.75% and delivered commentary that was, in our view, consistent with further easing at upcoming meetings. The Bank of Canada and Sweden's Riksbank also lowered their policy rates by 25 bps, and we have updated our forecast to look for an earlier start to Reserve Bank of Australia policy easing. In the emerging economies, Brazil's central bank delivered a hawkish-leaning 100 bps rate hike, and China's PMI data disappointed.

- Next week: Eurozone CPI (Mon.), Bank of England Policy Rate (Thu.), Banxico Policy Rate (Thu.)

Interest Rate Watch: In Little Hurry to Cut Further

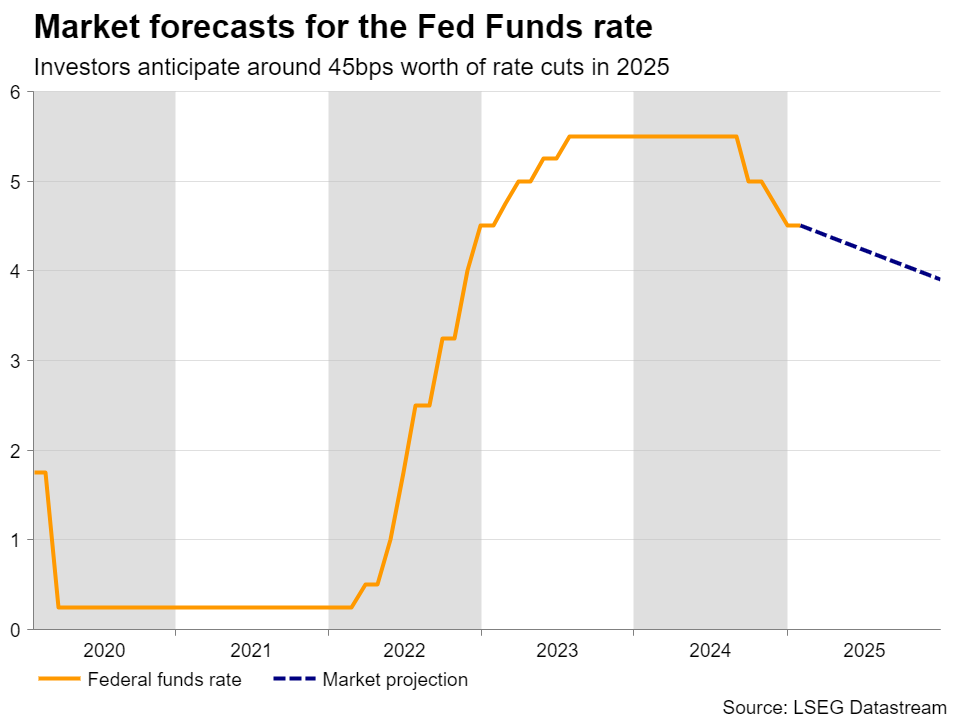

- As universally expected, the Federal Open Market Committee (FOMC) left its target range for the federal funds rate unchanged at 4.25%-4.50% on Wednesday. With inflation remaining stubbornly above target and real economic activity holding up reasonably well, we see little reason for the FOMC to cut rates in the near term.

Topic of the Week: Nobody Puts ASI in the Corner...Except Tariffs

- The Animal Spirits Index (ASI) finished out 2024 on a soft note, hitting its lowest level since November 2023. The index dropped 0.44 points in December to 0.31—the largest monthly decrease in over a year. Though the ASI remained in positive territory for all of 2024, it has softened considerably from a five-year high of 0.96 in March.

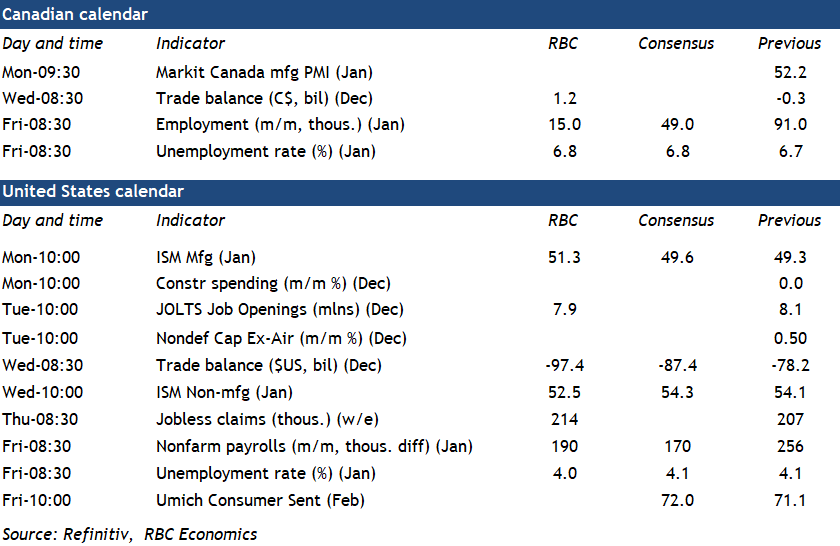

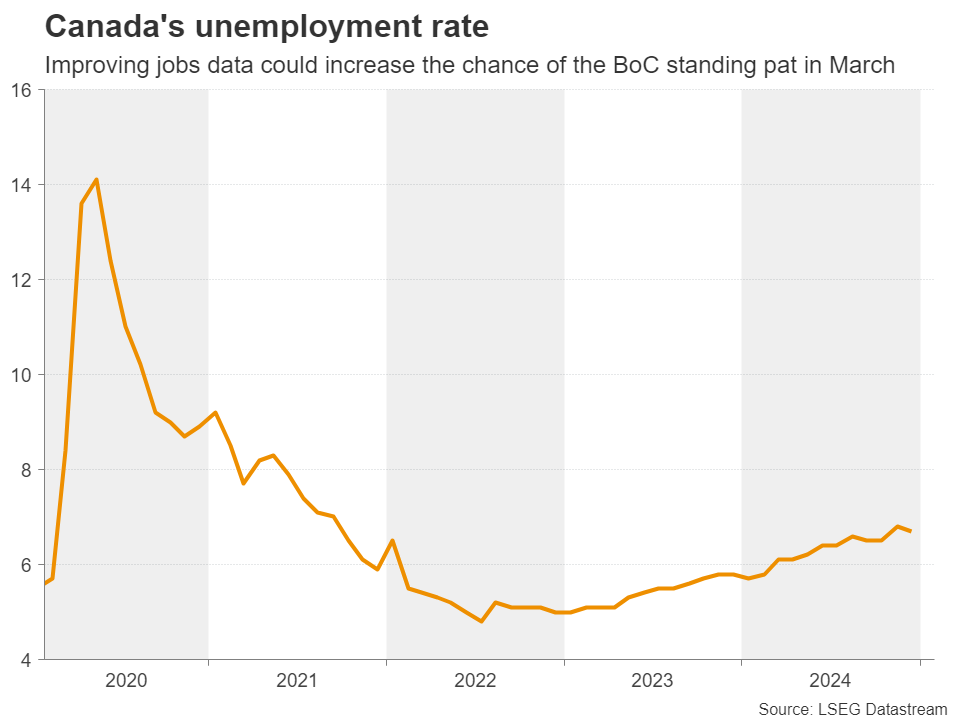

Canada’s Labour Market Still Gradually Softening Ahead of Looming Tariff Threat

Canada’s labour market likely continued to underperform in January as it has consistently shown a more pronounced deterioration than the U.S. job market.

We expect Canada added 15K jobs in January, but with a larger increase in the labour force nudging the unemployment rate higher. We expect it will rise to 6.8%, partially retracing a pullback to 6.7% in November from 6.9% in October but still up more than a percentage point from a year ago. Canadian household spending has shown signs of life, but sentiment among businesses remains lethargic as firms continue to face challenges with spare capacity after a prolonged string of slow demand growth. Companies reported limited hiring intentions for the year ahead in the Q4 Bank of Canada Business Outlook Survey.

Hiring demand has fallen sharply – job openings were still running 23% below year-ago levels in November. Wage growth has shown signs of slowing and smaller increases in wages in job postings argue for further slowing ahead. The rise in the unemployment rate to-date has been driven more than usual by students and new job seekers, but layoffs have still accounted for almost 40% of the increase in the unemployment rate over the last two and a half years.

Over the past year, job gains have been largely concentrated in the services sector – almost half from public sector education and healthcare jobs. We expect this will continue as the manufacturing sector faces weaker demand and threats of disruption from tariffs. With weaker population growth expected from reduced immigration targets, the pace of job creation is expected to continue to slow throughout 2025.

U.S. labour markets, however, continue to look solid by comparison. We expect January payroll numbers to show the U.S. added 190K jobs on Friday, and for the unemployment rate to tick down to 4.0%. We continue to expect resilience in the U.S. jobs market through 2025 but hiring rates continue to fall, indicating tight conditions have eased. The pace of job creation will be challenged over the medium term by an ageing population and slower population growth (made worse if mass deportations of migrants materializes).

Week ahead data watch

We expect the U.S. trade deficits to widen to $97.4B in December. According to the advance economic indicator report, the goods deficit widened by $18.6B from last month, mainly driven by higher imports and weaker exports.

We expect Canadian exports expanded by 1.9% in December, in line with stronger rail carloading data. We expect imports to dip slightly given motor vehicle shipments weakened.

Week ahead – Nonfarm Payrolls and BoE Decision in the Spotlight

- Dollar continues to be driven by tariff headlines.

- Nonfarm Payrolls to reshape Fed expectations.

- BoE to cut by 25bps; focus to fall on forward guidance.

- Canadian jobs report key for BoC’s next move.

In the mercy of tariffs

The US dollar has staged a recovery this week, corroborating the notion that the latest pullback on news that Trump may adopt a softer stance on tariffs than his pre-inauguration rhetoric suggested, was just a corrective phase.

Tariffs remained the main driver, with Wednesday’s Fed decision adding some extra fuel to the rebound. After Colombia succumbed to Trump’s threats, investors’ concerns were amplified again, with many perhaps thinking that the US President may harden his rhetoric to get what he wants from the rest of the world. And indeed, Trump himself confirmed that view after he rejected reports that US Treasury secretary Scott Bessent is pushing for only 2.5% tariffs that would be gradually lifted to 20%, saying that tariffs would be “much bigger.”

In the shadows of the first imposition of 25% tariffs on Canadian and Mexican imports on February 1, the Fed decided on Wednesday to keep interest rates unchanged. At the press conference following the decision, Fed Chair Powell acknowledged signs of progress in reducing inflation, adding though that “non-market” prices remain stubbornly high and stressing that they are in no hurry to make further adjustments. They will wait for more clarity on the economic front as well as on government policy.

From around 50bps worth of rate reductions for this year, Fed fund futures are now pointing to 45bps as investors lifted only slightly the implied rate path. The next quarter-point reduction is still nearly fully priced in by June.

Nonfarm Payrolls enter the limelight

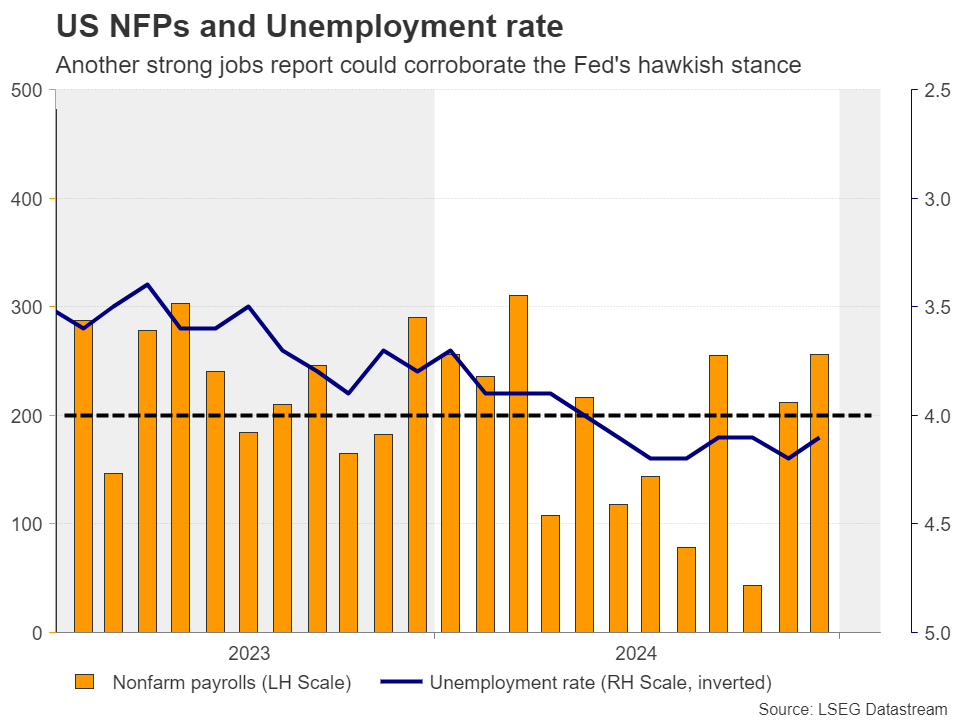

With all that in mind, attention next week is likely to fall on the NFP employment report for January. Powell noted that further labor market weakening is not needed for the inflation target to be met as the path for continued disinflation remains intact. However, he did not mention what will happen in the case of unexpected labor market tightening.

In December, the economy added 256k jobs, with average hourly earnings ticking down, but remaining elevated close to 4.0% y/y. Another round of strong employment and wage growth could intensify concerns about a resurgence of inflation in the months to come, especially if Trump kicks off the tariff game on February 1. Market participants are likely to start doubting again whether two rate cuts will be needed this year, which could allow the US dollar to extend its latest recovery.

The ISM manufacturing and non-manufacturing PMIs on Monday and Wednesday, as well as the ADP private employment report on Wednesday will also be closely monitored ahead of Friday’s NFP data.

Will the BoE opt for a hawkish cut?

After the BoJ, the Fed, the ECB and the BoC, it will be the BoE’s turn to hold its first policy decision for 2025. Following the concerns over the sustainability of the new government’s fiscal plans, where UK bonds and the pound tumbled on fears of a Truss 2.0 budget crisis, investors became more convinced that a rate cut would be appropriate at this gathering.

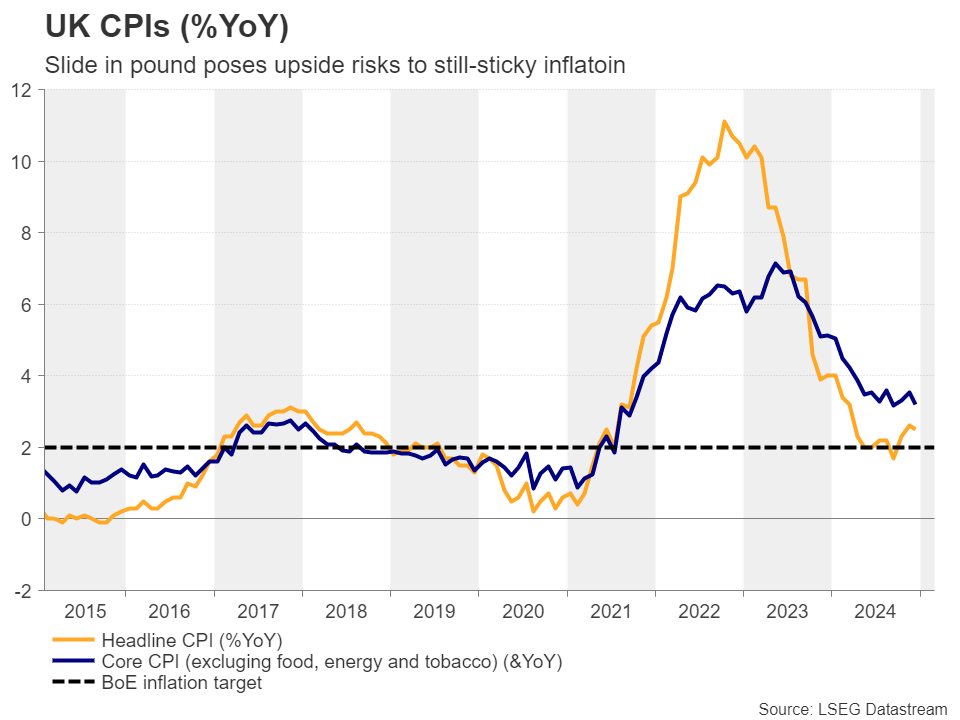

Taking also into account the cooler-than-expected CPI numbers for December and the sluggish UK growth, investors are now penciling in around a 90% chance of a quarter-point rate cut at this gathering, while anticipating nearly another two by the end of the year.

That said, both the headline and the core inflation rates remain above the Bank’s objective of 2%, with the latter standing at 3.2% y/y. What’s more, although the surge in bold yields was largely reversed, the pound recovered only a portion of its losses. It is actually the worst performing major currency so far this year, posing upside risks to UK inflation.

Therefore, even if the well-anticipated rate cut is delivered, it may be a hawkish cut, with the Bank revising up its inflation projections, especially with rent inflation remaining stagnant at 7.6% y/y and services inflation still above 4.0% y/y. Officials may signal that they will take their decisions meeting by meeting, avoiding to pre-commit to any future rate cuts. This may disappoint those expecting another two reductions this year and thereby allow the pound to gain some more ground.

Will the jobs data allow the BoC to take the sidelines?

At the same time with the US jobs data, Canada releases its own employment report for January. This week, the Bank of Canada trimmed interest rates by another 25bps and revised down its growth forecasts, noting that they are concerned about US tariffs.

However, they also added that tariffs could also stoke persistently high inflation, which led market participants to pencil in around a 50% probability for policymakers to take the sidelines at the next policy gathering in March.

In other words, the BoC will find itself between a rock and a hard place and Friday’s jobs report may help tilt the scale towards a pause or another rate cut, depending on whether it will come in strong or soft.

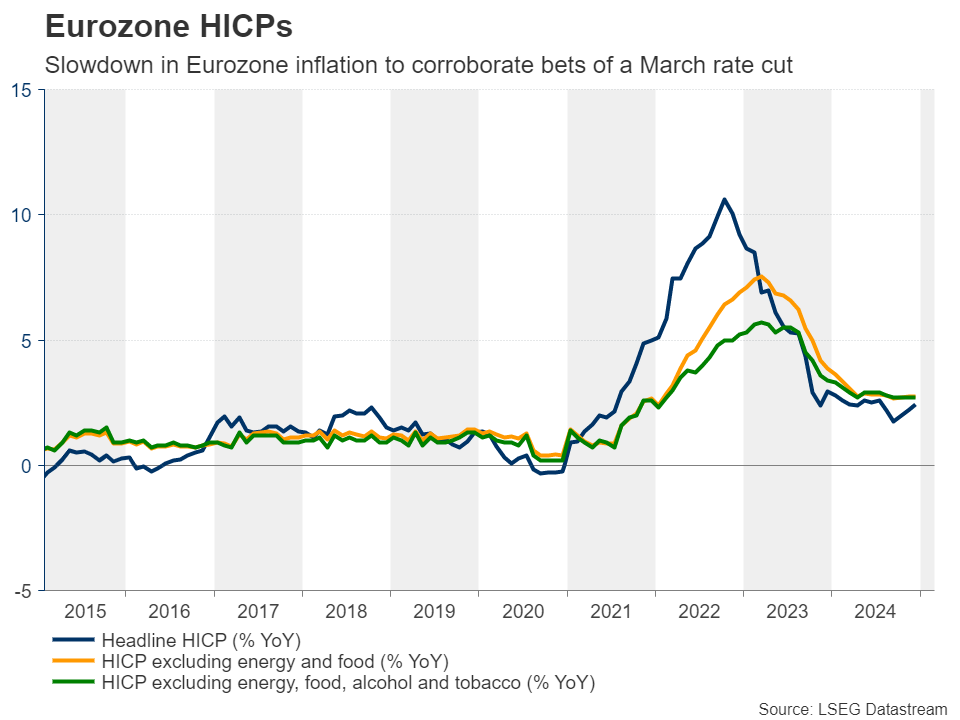

Eurozone CPIs, NZ employment and Japan’s wages

Flying from Canada to the Eurozone, the ECB also decided to reduce interest rates this week, noting that the disinflationary process is well on track and that the economy is still facing headwinds. In the statement, it was noted that the Bank is still not pre-committing to a particular rate path. At the post-decision conference, President Lagarde said that interest rates are still in restrictive territory and that there was no discussion on whether it's time to stop reducing rates.

The market was quick to price in around an 85% chance for another quarter-point cut in March and should Monday’s flash CPI data reveal cooling inflation, that probability could go even higher, thereby weighing on the euro. Eurozone’s retail sales are also on next week’s agenda.

Elsewhere, during Tuesday’s Asian session, New Zealand’s employment report for Q4 could prove crucial on whether the RBNZ will cut by 25 or 50bps, while the following day, Japan’s wage data for December could shape expectations about the BoJ’s next rate increase.

On the earnings front, the tech-related reporting continues with Alphabet and AMD on Tuesday, and Amazon on Thursday.

Weekly Focus – Uneventful Cut, Uneventful Keep

Soft US and euro area data weighed slightly on rates, which largely did not move much through the week, at least until German inflation unexpectedly declined significantly in several of the big Bundesländer, which drove 2Y Bund yields 10bpslower. This puts the spotlight on the euro area total released Monday. January is always a special month setting the stage for the year, because many prices are adjusted only at new year.

After a long period of some serious zigzagging the dollar has been steadier this week. The fallout of US tariff plans will continue to be a key driver of volatility in FX markets, though. European equities outperformed US in a week when the Chinese AI start-up DeepSeek took the spotlight as it poses a challenge to US AI developers to compete without relying on the most advanced chips.

The ECB cut its key interest rates by 25bp in a unanimous decision as widely expected. Despite several attempts from journalists, we did not get much colour on the final destination for this cutting cycle.

The decision followed data showing that the euro area stalled in Q4 with shrinking French and German economies still weighing down. The new year has started off a bit stronger as the current situation index from the IFO data supported the better-than-expected German PMI data for January. Expectations declined further to the lowest level in a year though, and we continue to expect the economy to stagnate in the first half of this year.

The FOMC meeting was as uneventful as the one in Frankfurt. The Fed kept rates unchanged, and Powell delivered a balanced message to markets while steering clear of toxic political questions. He noted that the committee is in no hurry to adjust the policy stance. Data out of the US ticked in a bit weaker than expected, with q/q Q4 GDP growth of 0.6%, slightly below expectations and softer vibes from the labour market with the "jobs plentiful"-index declining to the lowest level since September.

The calendar is packed with interesting highlights next week. Besides inflation data, on Monday French lawmakers will discuss the 2025 budget, and likely adopt it without a majority. Later in the week, we will see if PM Bayrou survives a no-confidence vote. On Friday, the ECB publishes a new paper on the neutral rate of interest, which might give us some further insight into where we should expect the cutting cycle to end up.

In the US, the first tariffs should take effect over the weekend. On the data front, we have a packed schedule with ISM data, JOLTs and jobs report as the key highlights. After a long period of solid job market data, it will be interesting to see if it continues. We expect nonfarm payrolls growth to slow down to +150k. We expect the Bank of England to cut the policy rate by 25bp to 4.50% on Thursday. We expect a cautious message, focusing on a gradual cutting cycle.