Sample Category Title

Elliott Wave Analysis: EURGBP Looking Down and Oil Up

Good day traders! Today's focus is EURGBP and Crude oil.

On the bearish side of euro the most interesting pair can be EURGBP which is trading nicely lower this month. As such, traders may keep a close eye on corrective pullbacks in three legs before downtrend may resume. We are tracking a fourth wave right now which may rise even to 0.8930/0.8980 zone from where a new drop lower may show up, ideally later this week.

EURGBP, 1H

Crude oil is very interesting, now looking bullish again after recent spike down to 49.60 where energy might have completed a three wave drop within wave four pullback. We think that sooner or later price will break to a new high and extend up to 51.50, maybe even 52.00 by the end of the week.

Crude oil, 1H

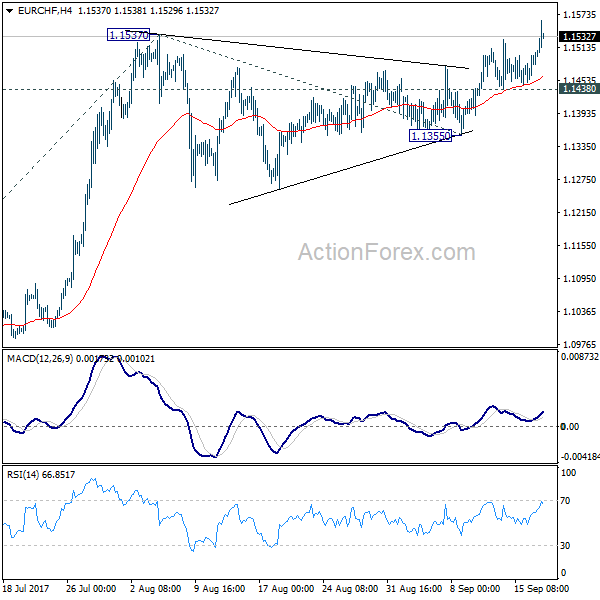

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1463; (P) 1.1481; (R1) 1.1516; More... .

EUR/CHF surges to as high as 1.1562 so far today. The break of 1.1537 resistance indicates resumption of medium term rise. Intraday bias is back to the upside for 61.8% projection of 1.0830 to 1.1537 from 1.1355 at 1.1792 next. However, considering weak upside momentum so far, break of 1.1438 will turn focus back to 1.1355 support instead.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

EUR/CHF Surges to Highest Since 2015, Boosted by ZEW Economic Sentiments

Euro surges to highest level since 2015 against Swiss Franc today as boosted by solid improvement in economic sentiments. But the common currency is overwhelmed by Aussie and Kiwi on strong risk appetite. Meanwhile, Sterling also regained ground after the pull back following BoE Governor Mark Carney's cautious speech yesterday. Dollar is generally softer as markets await FOMC policy decision and press conference tomorrow. In other markets, Gold is gyrating in tight range around 1310 but is vulnerable to another dip to 1300 handle. WTI crude oil is also struggling around 50.

Republicans in last-ditch effort to repeal Obamacare

In US, Senate Republicans are coming back with one last-ditch effort to repeal Obamacare. And they need to act by September 30, using a fast-track procedures. But for the moment, John McCain of Arizona, Rand Paul of Kentucky, Susan Collins of Maine and Lisa Murkowski of Alaska are not offering support yet. Released from US, housing starts dropped to 1.18m annualized rate in August, building permits rose to 1.30m. Import price index rose 0.6% mom. Current account deficit widened to USD -123b in Q2. From Canada, manufacturing shipments dropped -2.6% mom in July.

German ZEW suggests worry of Euro strength has "faded into the background"

German ZEW economic sentiment rose 7 points to 17 in September, well above expectation of 12. While the improvement is notable, it's staying below historical average of 23.8. Current situation gauge also improved to 87.9, up from 86.7 and beat expectation of 86.3. Eurozone ZEW economic sentiment rose to 31.7, up from 29.3 and beat expectation of 32.4. ZEW president Achim Wambach noted in the statement that 'the solid growth figures in the second quarter of 2017 in combination with a steep rise in bank lending and increasing investment activities by both the government and private firms are likely reasons for the financial market experts' significantly more positive outlook compared to that of last month." Also, "the worries about the recent strengthening of the euro have, for now, also faded into the background." Also from Eurozone, Current account surplus widened to EUR 25.1b in July.

ECB may keep QE extension open

Reuters reported, quoting unnamed source, that ECB would likely keep the options of prolonging the asset purchase in 2018 open. There are two camps among ECB policymakers. The hawk are already preferring to wind down the EUR 2.3T program. On the other hand, the doves just prefer to slow down from EUR 60b a month purchase. Meanwhile, the strength of Euro is seen as the "number one problem" for one of the sources. Another source noted that US economic policy is another "main source of uncertainty". Also, ECB President Mario Draghi was very careful in his words and used "recalibration" of the program before. Another source noted that "recalibration is not tapering, it's open ended".

BoE Kohn warned of impact of monetary stimulus exit

Donald Kohn, a member of the BoE's Financial Policy Committee, urged global central banks to closely watch the risks of global monetary stimulus exit. Hit said that "macro and micro-prudential policies need to be alert to and anticipate financial stability risks that might arise as rates rise and central bank portfolios stabilize and then decline." He pointed to stress tests" as an "essential tool for spotting risks and building resilience". And that's particularly as "interest rates rise along the yield curve." "The curve itself may even twist in unexpected ways, revealing vulnerabilities in asset prices and portfolio choices."

BoE Carney talked cautious on rate hikes

Yesterday, BoE Governor Mark Carney sounded cautious in his speech at the IMF. He reiterated that interest rates may rise "within months" in reaction to surging prices. But he emphasized that "any prospective increases in Bank Rate would be expected to be at a gradual pace and to a limited extent". Meanwhile, Carney described Brexit as an example of "deglobalization". And "the de-integration effects of Brexit can be expected... to be inflationary." He pointed out that lower immigration to the UK may boost domestic wage growth. Also, new trade barriers would lead to higher prices for goods and services. Meanwhile, the economic impacts of Brexit are subject to "tremendous uncertainty" in terms of scale and timing.

RBA talked jobs, Aussie, iron and household debt in minutes

The RBA minutes for the September meeting contained little news. Four main areas of discussions include employment situation, Australian dollar, iron prices and the balance of household debt and low inflation. Policymakers acknowledged the improvement in the employment market, noting higher participation rate and steady unemployment rate. RBA appeared less worrisome about Aussie's strength. By attributing the appreciation of the Australian dollar to USD's weakness, it appears less likely that RBA would take actions to curb its strength. RBA expected iron ore prices to fall amidst new supply. As the biggest exporter of iron ores, Australian dollar has been affected by the movement in iron ore prices. More in RBA Minutes: More Confident Over Job Market, Less Action Against Rising Aussie.

Also from down under, New Zealand Westpac consumer confidence dropped to 112.4 in Q3. Australia house price index rose 1.9% qoq in Q2.

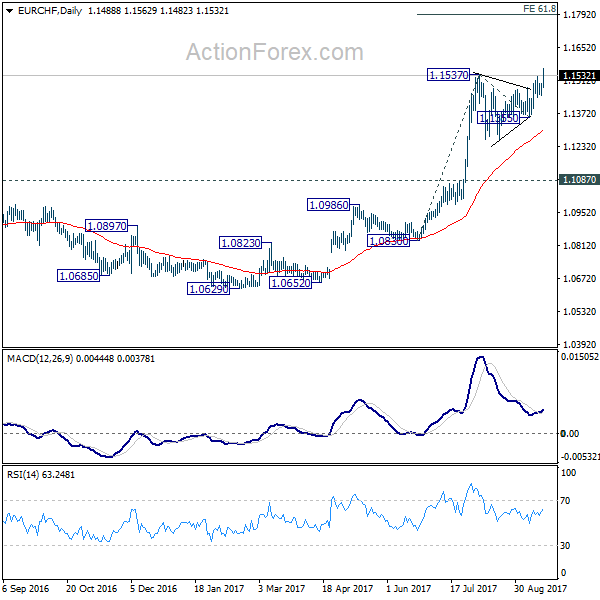

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1463; (P) 1.1481; (R1) 1.1516; More... .

EUR/CHF surges to as high as 1.1562 so far today. The break of 1.1537 resistance indicates resumption of medium term rise. Intraday bias is back to the upside for 61.8% projection of 1.0830 to 1.1537 from 1.1355 at 1.1792 next. However, considering weak upside momentum so far, break of 1.1438 will turn focus back to 1.1355 support instead.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | NZD | Westpac Consumer Confidence Q3 | 112.4 | 113.4 | ||

| 01:30 | AUD | House Price Index Q/Q Q2 | 1.90% | 1.30% | 2.20% | |

| 01:30 | AUD | RBA Meeting Minutes Sep | ||||

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 25.1B | 22.3B | 21.2B | 22.8B |

| 09:00 | EUR | German ZEW (Economic Sentiment) Sep | 17 | 12 | 10 | |

| 09:00 | EUR | German ZEW (Current Situation) Sep | 87.9 | 86.3 | 86.7 | |

| 09:00 | EUR | Eurozone ZEW (Economic Sentiment) Sep | 31.7 | 32.4 | 29.3 | |

| 12:30 | CAD | Manufacturing Shipments M/M Jul | -2.60% | -0.70% | -1.80% | -1.90% |

| 12:30 | USD | Current Account Balance (USD) Q2 | -123B | -113B | -117B | |

| 12:30 | USD | Housing Starts Aug | 1.18M | 1.18M | 1.16M | 1.19M |

| 12:30 | USD | Building Permits Aug | 1.30M | 1.22M | 1.23M | |

| 12:30 | USD | Import Price Index M/M Aug | 0.60% | 0.40% | 0.10% | -0.10% |

DAX Yawns as German ZEW Beats Expectations

The DAX index has edged higher in the Tuesday session. Currently, the DAX is trading at 12,543.00, down 0.11% on the day. On the release front, German ZEW Economic Sentiment climbed to 17.0 points, crushing the forecast of 12.3 points. Eurozone ZEW Economic Sentiment improved to 31.7, but fell short of the estimate of 32.4 points.

Institutional investors and analysts gave a thumbs-up to the German economy on Tuesday, as the September ZEW Economic Sentiment jumped to 17.1 points, rebounding from a weak reading of 10.0 in August. The ZEW report noted that Germany's growth in the second quarter remained strong, and both the public and private sectors were marked by increased investment. As well, global demand remained steady, and a stronger euro had not had a negative impact on the German economy. The Eurozone ZEW Economic Sentiment also improved in September, climbing to 31.7 points, up from 29.3 in the August release.

Germans head to the polls on Sunday, and Angela Merkel is widely expected to win her fourth term as prime minister. Merkel's CDU conservative party is enjoying a 14 percent lead over the center-left SPD, its current coalition partner. Still, the CDU is not expected to win a majority, meaning that Merkel will have to hammer out a coalition agreement with either the SPD or the FDP. The pro-business FDP is against Germany transferring funds to other EU members and wants to take a tougher stance against laggards, such as Greece. The FDP has also taken a hard line on immigration, which Merkel may not be comfortable with.

The eurozone economy has rebounded in 2017, and much of the credit goes to Germany, the largest economy in the bloc. At the same time, inflation levels have been stubbornly low. This has complicated the ECB's plans to reduce its quantitative easing scheme (QE), although ECB President Mario Draghi has said that the ECB will announce its plans to reduce QE at the October policy meeting. QE is scheduled to end in December, and policymakers will have to balance opposing interests as to what happens next. Germany, with its robust economy, would like to remove stimulus entirely, while less affluent eurozone members want to retain an accommodative monetary policy. We're likely to see some compromise, in which stimulus is extended into 2018, but will be tapered from its current level of EUR 60 billion/month.

CADJPY Elliott Wave Sequence Still Bullish

CADJPY Elliott Wave Sequence is bullish and incomplete to the upside due to which we have been telling clients not to sell the pair and use the dips as an opportunity to get long for higher prices. Our Live Trading Room was able to catch a long in CADJPY for a profit of +197 pips recently and in this blog, we will take a look at CADJPY daily chart to show that the rally is not over yet and any pull backs should still be viewed as a buying opportunity in the sequence of 3, 7 or 11 swings.

CADJPY Elliott Wave Sequence from 11.9.2016

Daily chart of CADJPY shows the pair rallied in 3 waves from 11.9.2016 low to 12.15.2016 high. Then, the pair pulled back to 50 - 61.8 Fibonacci retracement area of the rally from 11.9.2016 low and made a new high above 12.15.2016 peak. As soon as pair broke above 12.15.2016 peak, it created a bullish Elliott wave sequence with a target of 94.57 - 97.91 area. We know that market doesn't move in a straight line and always does pull backs. Since the pair broke above 12.15.2016 peak, we have been telling clients to use pull backs as a buying opportunity in 3, 7 or 11 swings. As far as dips hold above 8.11.2017 low i.e blue (X) low, pair should remain supported and see more upside towards 94.57 - 97.91 area.

CADJPY 8 Hour Elliott Wave Analysis

Pair is showing 5 swings up from 4.19.2017 low which makes Elliott wave sequence incomplete and bullish against 8.11.2017 low in this time frame. Pair has reached 0.618 - 0.764 Fibonacci extension area of (W)-(X). This is the area which will typically end 5th swing in a 7 swing sequence. Therefore, we don't like chasing the longs here as a pull back can be seen soon in wave X. We don't like selling the pair and expect wave X pull back to find buyers in 3, 7 or 11 swings as far as pivot at 8.11.2017 i.e. blue (X) at 85.44 low remains intact.

GOLD Targets Further Weakness, Eyes 1,298.23 Zone

GOLD: The commodity followed through lower the past week to open the door for more on Tuesday, opening the door for additional weakness. On the downside, support comes in at the 1,300.00 level where a break will turn attention to the 1,290.00 level. Further down, a cut through here will open the door for a move lower towards the 1,280.00 level. Below here if seen could trigger further downside pressure targeting the 1,270.00 level. Conversely, resistance resides at the 1,320.00 level where a break will aim at the 1,330.00 level. A turn above there will expose the 1,340.00 level. Further out, resistance stands at the 1,350.00 level. All in all, GOLD looks to weaken further on bear pressure.

The Pound is Regaining Positions. What’s Next?

The GBP/USD is back to the highs it reached in June 2016. It was achieved with the help of the macroeconomic statistics, which turned out to be better than before. However, in these circumstances the Pound could have rising slower, with an eye to the Brexit and the debates surrounding it. The major contribution to the quick growth was made by the Bank of England, which said it might increase the key rate in the months to come.

During the September meeting, the Bank of England made a decision to keep the key rate unchanged at 0.25% along with the QE program at 435B Pounds. This time the regulator, which is usually very careful and conservative, was more energetic. In the comments, it announced that there might be reasons to increase the key rate in the next several months.

Most likely, it's all about the inflation. The inflationary pressure on the country's economy is increasing and it's much easier to force the CPI into the required range by means of changing the rate. As a rule, the Bank of England has no problems to "accelerate" the CPI as it finds fit, but later the indicator has to be kept within bounds. This is the way the British regulator has been operating for the last 8 years: controlling the inflation by means of monetary tools. And one should admit, it runs smoothly.

For the Pound, the rate increase in the nearest future will stabilize the country's economy and eliminate real dangers from both the Brexit and events outside the United Kingdom. Using the rate increase as a basis, the British currency may continue rising, especially if the statistics continues to confirm the economic stability.

Also, this week the currency market is waiting for the results of the September meeting of the US Federal Reserve. So far, the USD is very vulnerable (including the GBP pair), but market trends may change depending on the Fed's comments and decisions.

It's better to analyze the technical picture of the British Pound using the GBP/USD pair charts. If one takes a look at the weekly timeframe, it can be seen that the instrument has been moving inside the uptrend for about a year.

More details can be seen at the daily timeframe. The chart not just shows the ascending movement, but one can see that this movement "boosted" after the price broke the resistance level of the short-term ascending channel. Later, the instrument may start a short-term correction to the broken resistance level, which now provides support. However, the future outlook remains "bullish". The main upside target is close to the upside border of the mid-term channel at 1.4000.

German Elections And DAX | Fed’s Uncharted Territory | Wild Cards For Market Meltdown

Parade To Uncharted Territory

Wild Cards For Market Meltdown

DAX Showing No Sign of Vulnerability; VDAX Plunged

EURO ZEW Sentiment Knocked Euro

Parade To Uncharted Territory

The Fed would kick off their two-day monetary policy and the parade towards the uncharted territory would begin soon. Shrinking the size of the balance sheet is something which is untested and no back test records exist for such scale. However, the Fed has prepared the market for this event by telegraphing their message consistently, and no forthwith wild moves are expected immediately when they will take this course. But the fact is that the Fed doesn’t know the actual implications of this and they have made it clear that they will be learning about it as it goes.

The important thing when it comes to the Fed’s balance sheet is not so much the timing, but the equilibrium level. We do not know what that level is and this remains the wild question. However, the Fed is going to make sure that the process would stay as smooth as possible and this would likely push them to hold their gradual approach in hiking the interest rates. The odds of a December rate hike are standing at 40 percent but a hawkish tone by the Fed could strengthen the dollar index.

Wild Cards For Market Meltdown

We do think that Trump’s speech to the U.N, the counter-reaction from North Korea, and Trump’s decision on the Iranian nuclear deal are the wild cards which have the potential to trigger a full-blown market meltdown scenario.

One could say that geopolitical tensions have eased off and are no longer at the boiling point given that there have been no more missile tests from North Korea. However, we do think that it would be naive to underestimate them and ignore the facts which have the ability to propel them to their climax level. The issues with North Korea were clearly directed to the U.N by President Donald Trump. In his speech yesterday, he has made it very clear that the expenses for the U.N have gone up, while the US makes a meaningful contribution to this bill, and the mismanagement has surged too.

Iran’s nuclear deal is something which investors should watch very closely as President Trump stated yesterday that he will be letting the world know about his decision very soon. We know that he has never been happy with the Iranian deal and given that there are also warnings from Iran that if the US back outs from the deal, it would have serious consequences, which provides us an indication about the upcoming events and how they will unfold.

Therefore, we do think that it is immensely important not to neglect the importance of hedging the risk. The record high headlines could easily deviate the attention.

Trump’s speech to the U.N today could spark some new concerns and that could trigger a fresh demand for gold.

DAX Showing No Sign of Vulnerability; VDAX Plunged

Macron’s victory crushed the anti-euro parties over in Europe and investors are no longer as worried about this as before. The fresh evidence of this can be seen by looking at the performance of the DAX index. The German elections are due on Sunday and if you look at the equity market, there are no signs of anxiety. The index is on track to log September as the best month within the developed world. This is also evident in the DAX volatility index which has plunged the most prior to the German election. The situation was not the same before the French Election, when we experienced a number of large bets coming to the market looking to hedge their bets.

EURO ZEW Sentiment Knocked Euro

The Eurozone ZEW sentiment took the wind out of the euro-dollar pair which broke the 1.20 mark earlier. The weaker number tells us that the economic growth or the sentiment are not necessarily at the same boiling point across the Eurozone. The German ZEW number showed that neither businesses nor consumers have any concerns about the upcoming elections (confirming our earlier argument).

Daily Technical Analysis: NZD/USD Correction Seems Over

The USD/JPY is being pushed towards next resistance by the backwind of risk on sentiment that is currently dominating the Forex market. When risk on sentiment is prevailing Gold goes down, Commodities are up, Equities are up and Yen weakens as a result. Adding to that is a Bullish SHS (head and shoulders) pattern that signifies now moment buyers. 110.45-70 is the POC zone and if the price retraces we might see another bounce to the upside towards 111.40. A spike above or 4h close above 111.40 could make a breakout on the price towards 111.70 and 112.05. A daily close above 112.00 could push the pair up to 112.58-74. The bullish sentiment might weaken if the pair drops and closes below the low of SHS pattern 109.54.

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

EUR/USD – Sharp German ZEW Economic Sentiment Pushes Euro Above 1.20

The euro has posted slight gains in the Tuesday session. Currently, EUR/USD is trading at 1.1993, up 0.32% on the day. Earlier in the day, the pair punched above the symbolic 1.20 level. On the release front, German ZEW Economic Sentiment climbed to 17.0 points, easily beating the forecast of 12.3 points. Eurozone ZEW Economic Sentiment improved to 31.7, but fell short of the estimate of 32.4 points. The US will release two key housing events – Building Permits and Housing Starts. On Wednesday, the Federal Reserve winds up its policy meeting and will release a rate statement.

The German economy continues to look strong, and institutional investors and analysts like what they see. German ZEW Economic Sentiment, jumped to 17.1 points in September, rebounding from a weak reading of 10.0 in August. The ZEW report noted that growth in the second quarter remained strong, and both the public and private sectors were marked by increased investment. As well, global demand remained steady, and a stronger euro had not had a negative impact on the German economy.

The eurozone economy has rebounded in 2017, and much of the credit goes to Germany, the largest economy in the bloc. At the same time, inflation levels have been stubbornly low. This has complicated the ECB’s plans to reduce its quantitative easing scheme (QE), although ECB President Mario Draghi has said that the ECB will announce its plans to reduce QE at the October policy meeting. QE is scheduled to end in December, and policymakers will have to balance opposing interests as to what happens next. Germany, with its robust economy, would like to remove stimulus entirely, while less affluent eurozone members want to retain an accommodative monetary policy. We’re likely to see some compromise, in which stimulus is extended into 2018, but will be tapered from its current level of EUR 60 billion/month.

The Federal Reserve will be back in the spotlight on Wednesday. There is virtually no chance that the benchmark rate of 1.25% will change, so the markets are focusing on the Fed’s bloated balance sheet, which currently stands at $4.2 trillion. Earlier in the year, the Fed outlined plans to reduce the balance sheet by not replacing some maturing bonds, starting at $10 billion/month, and gradually moving higher. This move can be viewed as a mini-rate hike, and could provide a boost for the US dollar against major rivals, such as the euro. The Fed is still debating whether it will raise rates in December, as persistently low inflation has hampered plans for a third rate hike in 2017. However, the odds of a December increase have been moving higher in September, and are currently at 56%.