Sample Category Title

Risk Assets Rebound As North Korea Tensions Ease And Hurricane Irma Downgrades

North Korea Refrains from Launching a Missile. The dollar pulled away from last week's lows against its major rivals in early Asian session on Monday, after the weekend passed without any missile tests by North Korea. The dollar index was 0.2 percent higher at 91.524, after falling to a 2-1/2 year low of 91.0 on Friday.

The Yen Edged Lower in Asia This Morning. North Korea marked the 69th anniversary of its founding on Saturday with a celebration honoring the scientists behind the massive nuclear test it conducted last week. The dollar added 0.5 percent against its perceived safe-haven Japanese counterpart to 108.38 yen, moving away from a 10-month low of 107.32 yen touched on Friday.

Euro Falls Against Dollar in Asian Trade. The euro fell 0.15% against the dollar, to $1.2018. Despite the strength of the common currency and prospects for further gains on expectations of a turn in monetary policy, the European Central Bank has signaled it is gearing up to taper its massive stimulus program. Reuters reported on Friday that ECB policymakers agreed at their meeting on Thursday that their next step would be to begin reducing its bond buying. The euro has gained more than 14 percent against the dollar so far in 2017, on track for its best annual performance in 14 years.

Gold Falls as North Korea Tensions Ease and Dollar Gains. Gold retraced while equities and indices had a strong rebound at the Asian open this morning, as North Korea refrained from launching a missile on Saturday and Hurricane Irma made landfall in Florida without catastrophic damage on Sunday.

European Open Briefing: Asian Equity Markets Rose On Monday

Global Markets:

- Asian stock markets: Nikkei up 1.39 %, Shanghai Composite rose 0.13 %, Hang Seng gained 0.97 %, ASX 200 rose 0.77 %

- Commodities: Gold at $1342.02 (-0.68 %), Silver at $17.93 (-1.03 %), WTI Oil at $47.87 (+0.82 %), Brent Oil at $54.03 (+0.46 %)

- Rates: US 10-year yield at 2.08, UK 10-year yield at 0.990, German 10-year yield at 0.309

News & Data:

- (JPY) Tertiary Industry Activity m/m 0.1 % vs 0.1 % expected

- (CNY) CPI y/y 1.8 % vs 1.7 % expected

- (CNY) PPI y/y 6.3 % vs 5.7 % expected

- (GBP) Manufacturing Production m/m 0.5 % vs 0.3 % expected

- (GBP) Goods Trade Balance -11.6 B vs -11.9 B expected

- (CAD) Employment Change 22.2 K vs 17.8 K expected

- (CAD) Unemployment Rate 6.2 % vs 6.3 % expected

- Oil edges up as Saudis discuss extending supply cut- RTRS

CFTC Positioning Data:

- EUR long 96K vs 87K long last week. Longs increased by 9K

- GBP short 54K vs 52K short last week. Shorts increased 2K

- JPY short 73K vs 69K short last week. Shorts increased by 4K

- CHF short 2K vs 2K short last week. Unchanged from prior week.

- CAD long 54K vs 53K long. Longs increased by 1K.

- AUD long 65k vs 67k last week. Longs trimmed by 2K

- NZD long 15K vs 19K long last week. Longs trimmed by 4K

Markets Update:

Asian equity markets rose on Monday as investors piled into risk assets as hurricane Irma’s force waned and the United Nations prepared to vote on tougher North Korean sanctions. Markets also digested headlines concerning developments out of the People's Bank of China and European Central Bank announced at the weekend.

USDJPY opened up around 50 pips early on Monday. The pair did not fill the gap after finding buyers around 108.15 and is currently seen trading around 108.40 as the Yen lost 0.5 percent against the US Dollar. Similar to the USDJPY all Yen crosses opened higher in very early trade. There had been heightened concerns over a North Korean missile test on the weekend, a test which did not eventuate resulting in a lower Yen

EURUSD is currently seen trading around 1.2010 as the EUR slipped a little losing 0.2 percent against the US Dollar. The Euro had hit a top of $1.2092 on Friday amid speculation the European Central Bank was closer to starting a wind-back of its stimulus program. The dollar index, which tracks the dollar against a basket of currencies rose 0.2 percent and is currently valued at 91.53

AUDUSD is currently seen Trading at 0.8046 as the Australian Dollar lost 0.2 percent against the USD. From a technical perspective, the 0.8100 handle suffered multiple attacks in early trading, but managed to hold ground and eventually push lower. Similar to the Aussie, the New Zealand Dollar has net lost some ground against the USD after having small ranges and is currently seen trading at 0.72443

Upcoming Events:

- 06:00 GMT – (JPY) Prelim Machine Tool Orders y/y

- 07:00 GMT – (EUR) ECB's Coeure Speaks

- 08:00 GMT – (EUR) Italian Industrial Production m/m

- 12:15 GMT – (CAD) Housing Starts

- 13:00 GMT – (RUB) GDP y/y

The Week Ahead:

Tuesday, September 12th

- 01:30 GMT – (AUD) NAB Business Confidence

- 08:30 GMT – (GBP) CPI y/y

- 08:30 GMT – (GBP) PPI Input m/m

- 08:30 GMT – (GBP) RPI y/y

- 14:00 GMT – (USD) JOLTS Job Openings

Wednesday, September 13th

- 07:15 GMT – (CHF) PPI m/m

- 08:30 GMT – (GBP) Average Earnings Index 3m/y

- 08:30 GMT – (GBP) Claimant Count Change

- 08:30 GMT – (GBP) Unemployment Rate

- 12:30 GMT – (USD) PPI m/m

- 12:30 GMT – (USD) Core PPI m/m

- 12:30 GMT – (USD) Crude Oil Inventories

- 14:00 GMT – (AUD) RBA Assist Gov Debelle Speaks

Thursday, September 14th

- 01:30 GMT – (AUD) Employment Change

- 01:30 GMT – (AUD) Unemployment Rate

- 02:00 GMT – (CNY) Industrial Production y/y

- 02:00 GMT – (CNY) Fixed Asset Investment ytd/y

- 07:30 GMT – (CHF) Libor Rate

- 07:30 GMT – (CHF) SNB Monetary Policy Assessment

- 11:00GMT – (GBP) MPC Official Bank Rate Votes

- 11:00GMT – (GBP) Monetary Policy Summary

- 11:00GMT – (GBP) Official Bank Rate

- 12:30 GMT – (USD) CPI m/m

- 12:30 GMT – (USD) Core CPI m/m

- 12:30 GMT – (USD) Unemployment Claims

- 15:30 GMT – (EUR) German Buba President Weidmann Speaks

- 22:30 GMT – (NZD) Business NZ Manufacturing Index

Friday, September 15th

- 08:50 GMT – (GBP) MPC Member Vlieghe Speaks

- 12:30 GMT – (USD) Core Retail Sales m/m

- 12:30 GMT – (USD) Retail Sales m/m

- 12:30 GMT – (USD) Empire State Manufacturing Index

- 13:15 GMT – (USD) Capacity Utilization Rate

- 13:15 GMT – (USD) Industrial Production m/m

- 14:00 GMT – (USD) Prelim UoM Consumer Sentiment

Stock Markets And Bond Yields Moved Higher In Asia Overnight

Market movers today

Norway is due to release inflation for August today where we look for a jump higher in core inflation to 1.5% y/y. Monday also sees parliamentary elections in Norway and it looks to be a very close race. Not only is it unclear which bloc will have a majority, but there is considerable uncertainty about what the governing coalition will look like. For the rest of the week in Scandi focus will be on Swedish CPI, Prospera inflation survey and the regional network survey in Norway.

There are no global market movers today but focus continues to be on Hurricane Irma and a new vote on UN sanctions against North Korea taking place today.

Our weekly Strategy on Friday looked closer at the global cycle and the outlook for the Fed next year, see Strategy: Strong cycle while US debt limit is postponed, 8 September 2017.

Selected market news

Stock markets and bond yields moved higher in Asia overnight as the damage from Hurricane Irma is set to be smaller than estimated. The hurricane hit Florida on Sunday and has weakened in strength as it moves up the West coast of Florida.

Markets were also relieved that we did not see another North Korean missile test over the weekend. It was widely anticipated that North Korea would launch another missile on the Founding Day on Saturday. However, North Korea has warned the US on new tough UN sanctions that are set to be voted on today. The state-run news agency cited a statement from the Ministry of Foreign Affairs saying that North Korea is ‘closely following the moves of the US with vigilance' and that the US would make sure the US ‘pays a due price' if it pushes through harsher sanctions. North Korea often comes pit with warnings though, but the regime might respond with a new missile test on the back of new sanctions.

In the UK, Brexit Secretary David Davis warned UK lawmakers of a chaotic departure from the EU if they fail to pass a key bill on domestic legislation.

In Japan, machine orders rose stronger than expected in July by 8.0% m/m (consensus 4.1% m/m) after -1.9% m/m in June. The numbers are very volatile but give a hint of robust investments going into Q3.

Risk Appetite Returns As North Korea Holiday Passes Without Drama

- Safe havens under pressure as geopolitical risk eases a little;

- Gold off its highs but remains elevated;

- UK data and central bank in focus this week.

Risk appetite looks to have returned on Monday, with traders relieved at the inactivity in North Korea over the weekend after reports suggested the country could engage in more provocative testing.

The rogue state celebrated its 69th founding anniversary on Saturday and there had been speculation over the week leading up to it that further tests could be planned. Last year, the occasion was used to carry out its fifth nuclear test and given the ramp up in testing in recent months, it was feared the same would happen again.

Given the market response in recent weeks to such actions, traders were understandably cautious throughout the week but with the day having passed without drama, we’re seeing a move away from the safe havens. Strong gains in Asia overnight are looking to be replicated when the European week gets underway, with indices currently seen around 0.5% higher.

The traditional safe havens are coming under some pressure this morning, a partial unwinding of the sizeable flows seen in recent weeks. Gold has come off its highest levels in more than a year this morning, gapping lower on the open in a sign of relief for traders, but still remains a very elevated levels which is representative of the risk environment we still find ourselves in.

The yen is another safe haven that is seeing some of the recent flows unwound this morning. The dollar is trading back above 108 against the yen this morning, having fallen to its lowest in almost 10 months on Friday, not helped by the greenbacks own difficulties. A combination of political risk, a less hawkish Fed and more hawkish central banks elsewhere has driven the dollar to its lowest since the start of 2015 and the slide doesn’t appear to be easing up yet.

This week the UK will be primarily in focus, with the Bank of England monetary policy decision due on Thursday and coming after jobs and inflation data earlier in the week. Monday is looking a little quieter though, which barring any surprise events could offer some reprieve for markets.

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 31 Jul 2017

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 2 Aug 2017

• Trend bias: Up

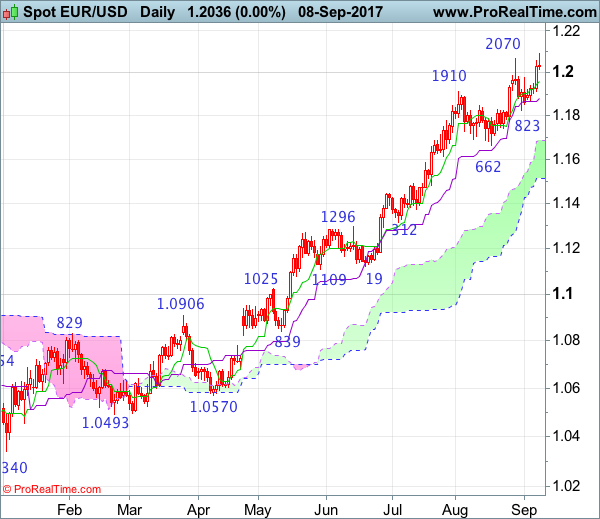

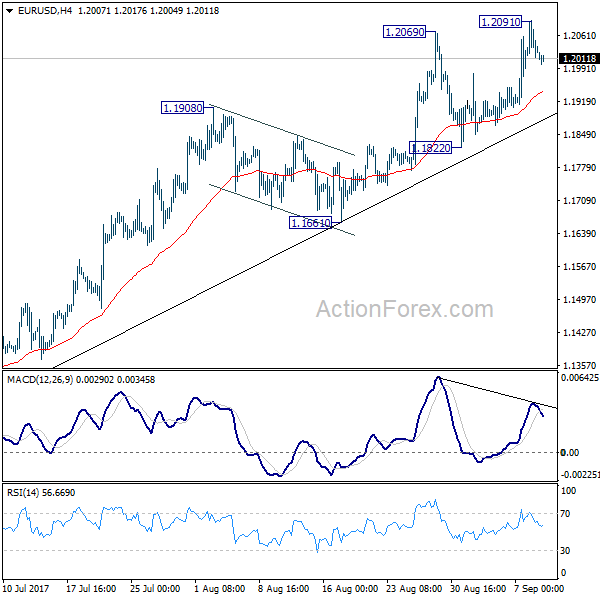

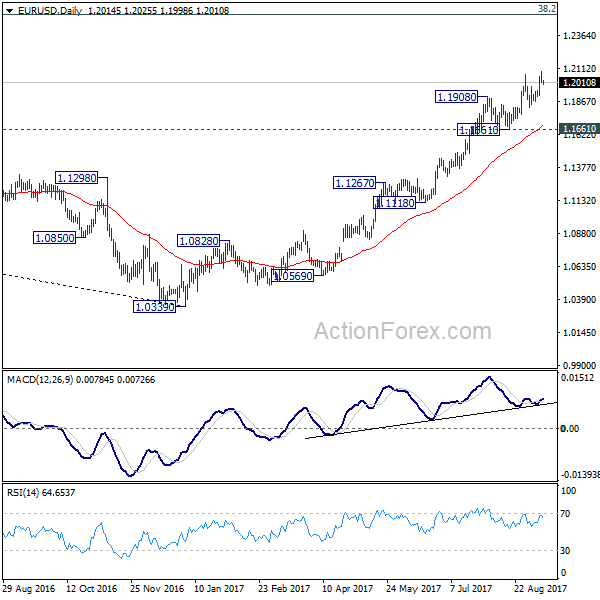

EUR/USD – 1.2015

Although the single currency resumed recent upmove after finding renewed buying interest at 1.1823 and rose to as high as 1.2093, the subsequent retreat formed a shooting star alike pattern on the daily chart and if a long black candlestick is formed today, this would signal a potential bearish reversal pattern is finished and further consolidation below said resistance would be seen with mild downside bias for test of the Tenkan-Sen (now at 1.1958), then towards the Kijun-Sen (now at 1.1878), however, reckon said support at 1.1823 would hold from here and bring rebound later. Looking ahead, only a drop below this level would signal a temporary top has been formed and bring retracement of recent rise to 1.1770-75, then 1.1740 but reckon support at 1.1662 would remain intact.

On the upside, above said resistance at 1.2093 would signal recent upmove is still in progress and may extend headway to dynamic resistance at 1.2165-70 (50% Fibonacci retracement of 1.3993-1.0340) and later towards 1.2200-10, however, loss of upward momentum should prevent sharp move beyond 1.2250-60 and reckon 1.2300-10 would hold from here, risk from there is seen for another retreat to take place later this month.

Recommendation: Stand aside for this week.

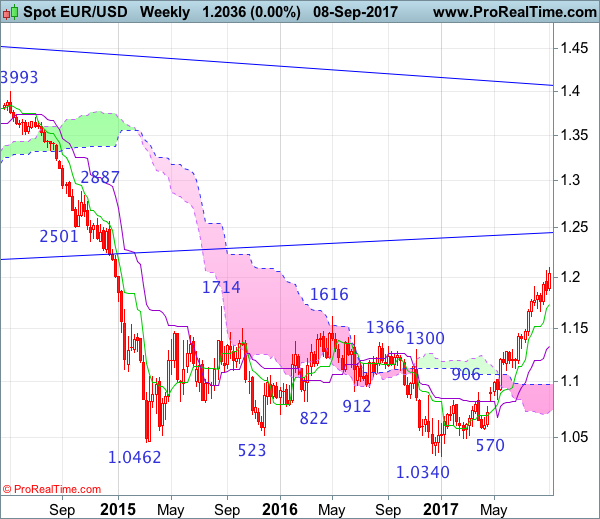

On the weekly chart, the single currency has continued moving higher after brief pullback, suggesting recent upmove from 1.0340 low is still in progress and mild upside bias remains for further gain to 1.2100 and possibly towards 1.2160-70 (50% Fibonacci retracement of 1.3993-1.0340) but loss of upward momentum should limit upside to 1.2220-30 and reckon 1.2300-10 would hold from here, price should falter well below 1.2390-00, bring another retreat later.

On the downside, whilst initial pullback to 1.1950-55 is likely, reckon downside would be limited to 1.1925-30 and support at 1.1i868 would hold, bring another rise later. A drop below support at 1.1823 (last week’s low) would suggest a temporary top is possibly formed, bring test of the Tenkan-Sen (now at 1.1764) , break there would add credence to this view, then correction of recent upmove would commence for retracement to 1.1662 support and later towards 1.1600 but downside should be limited to 1.1500-05, bring rebound.

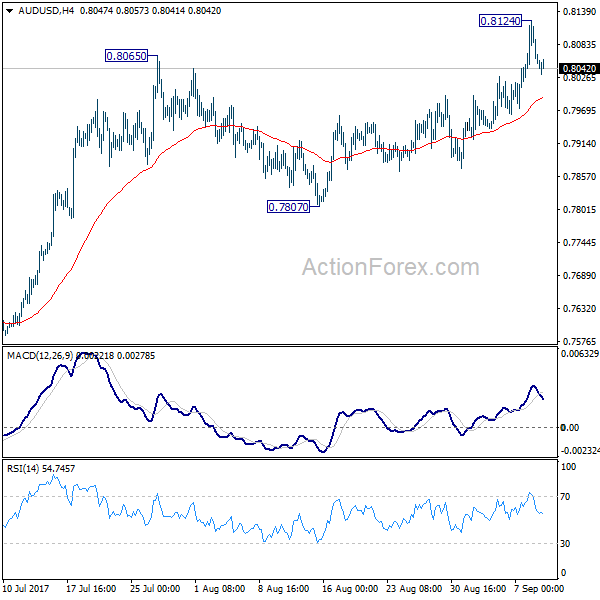

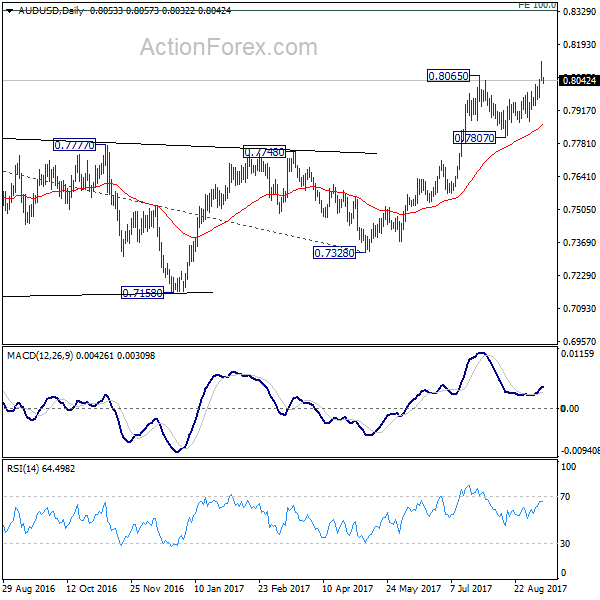

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.8022; (P) 0.8073; (R1) 0.8104; More...

A temporary top is formed at 0.8124 with today's retreat in AUD/USD. Intraday bias is turned neutral for consolidations first. As long as 0.7807 support holds, near term outlook remains bullish for further rally. Above 0.8124 will target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335 next.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8090) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7807 support is needed to to be the first sign of completion of the rebound. Otherwise, further rise is now in favor.

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Dark cloud cover

• Time of formation: 10 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Evening doji

• Time of formation: 7 Aug 2017

• Trend bias: Down

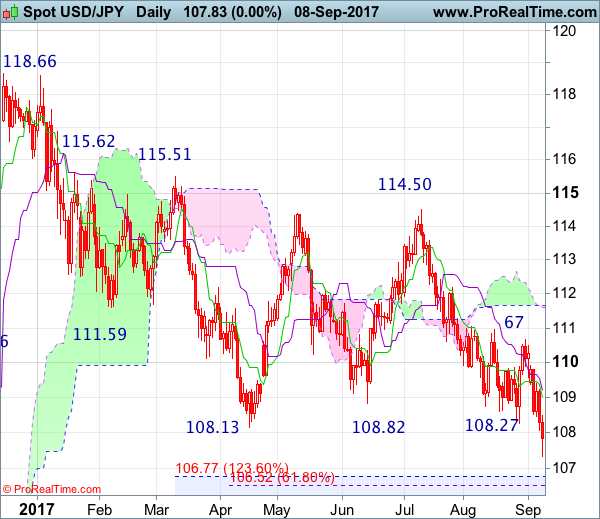

USD/JPY – 108.39

The greenback did meet renewed selling interest at 110.67 and dropped again (we recommended to sell at 110.55 and a short position was entered), adding credence to our bearish expectation for a resumption of recent decline, price finally penetrated support at 108.13, confirming the medium term fall from 118.66 top has resumed and downside bias remains for further weakness to 107.30-35, then 107.00, however, near term oversold condition should limit downside to 106.50-55 (61.8% Fibonacci retracement of 99.01-118.66) and 105.90-00 should hold, bring rebound later.

On the upside, whilst initial recovery to the Tenkan-Sen (now at 109.00) cannot be ruled out, reckon upside would be limited to 109.35-40 and bring another decline later. Above 109.90-95 would risk another test of said resistance at 110.67 but only a daily close above there would signal low is formed instead, bring retracement of recent decline to 110.95-05 resistance and later towards the Ichimoku cloud (now at 111.60-66).

Recommendation : Short entered at 110.55 met target at 108.55 with 200 points profit and would sell again at 110.00 for 107.00 with stop above 111.00.

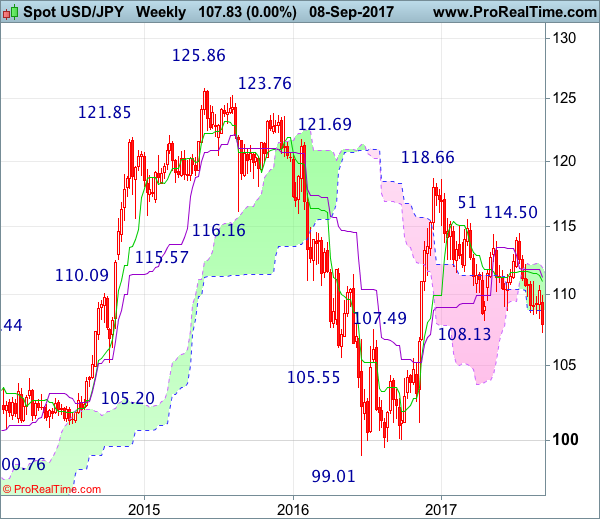

On the weekly chart, despite rebounding to 110.67 the week before, dollar met renewed selling interest there and dropped last week, a black candlestick was formed and the breach of this year’s low at 108.13 adds credence to our bearish view for the resumption of recent decline from 118.66 top, hence bearishness remains for this fall to extend weakness to 117.00, then 106.50-55 (61.8% Fibonacci retracement of 99.01-118.66), however, near term oversold condition should limit downside to previous resistance at 105.53 (now support) and price should stay above 105.00, bring rebound later.

On the upside, although initial recovery to 108.90-00 cannot be ruled out, reckon upside would be limited to the Tenkan-Sen (now at 110.10) and bring another decline later. A weekly close above the Kijun-Sen (now at 110.91) would defer and suggest a temporary low is formed instead, risk rebound to the upper Kumo (now at 111.49), however, reckon resistance at 112.20 would limit upside and price should falter below 112.90-00, bring another decline later.

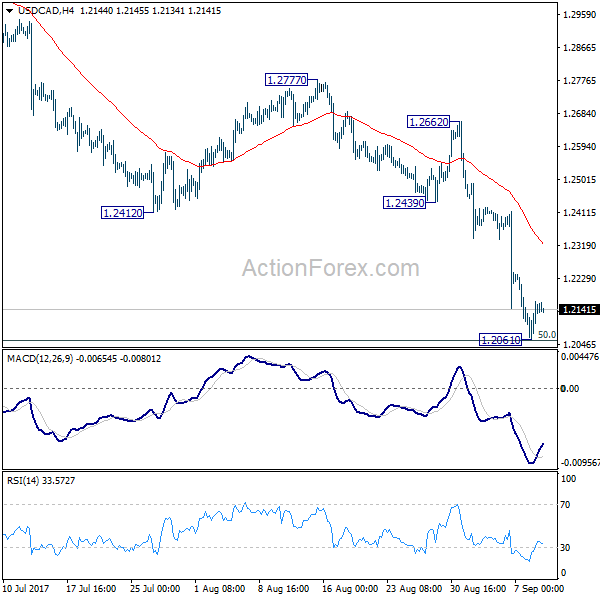

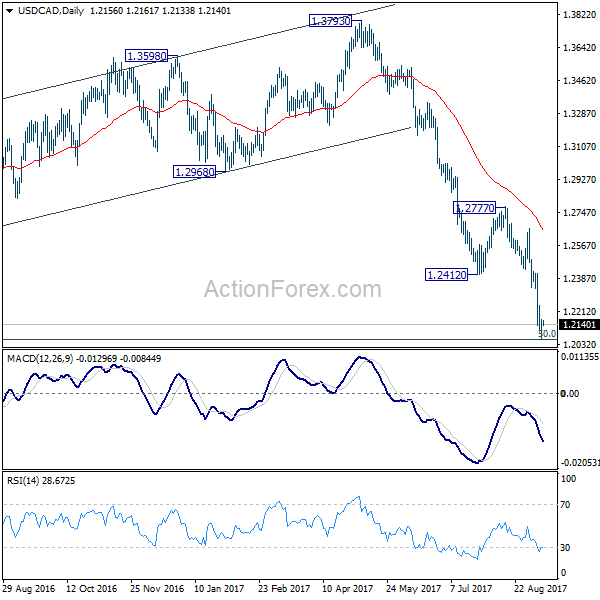

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2088; (P) 1.2126; (R1) 1.2192; More....

Intraday bias in USD/CAD remains neutral for consolidation above 1.2061 temporary low. At this point, we'd remain cautious on strong support from 1.2048 long term fibonacci level to bring sustainable rebound. But still, break of 1.2439 support turned resistance is needed to be the first sign of trend reversal. Otherwise, outlook will remain bearish. Firm break of 1.2048 will pave the way to next fibonacci level at 1.1424.

In the bigger picture, current downside acceleration is raising the chance that whole long term rise from 0.9406 (2011 low), and that from 0.9056 (2007 low) is completed at 1.4689. Focus is now on 50% retracement of 0.9406 to 1.4869 at 1.2048. As long as this level holds, we'd still favor that case that fall from 1.4689 is a correction. However, firm break of 1.2048 will indicate that fall fro 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2001; (P) 1.2046 (R1) 1.2079; More...

A temporary top is in place at 1.2091 in EUR/USD with today's retreat. Intraday bias is turned neutral first. But outlook remains bullish as long as 1.1822 support holds. Above 1.2091 will extend larger rise fro 1.0339 and target next key fibonacci level at 1.2516.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall fro 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

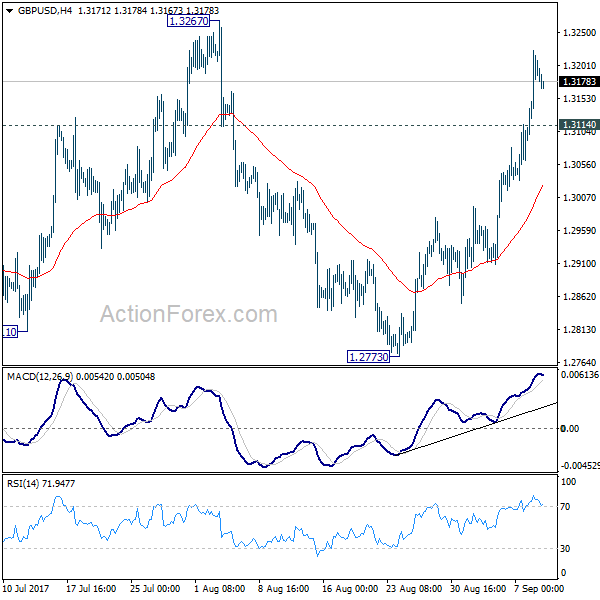

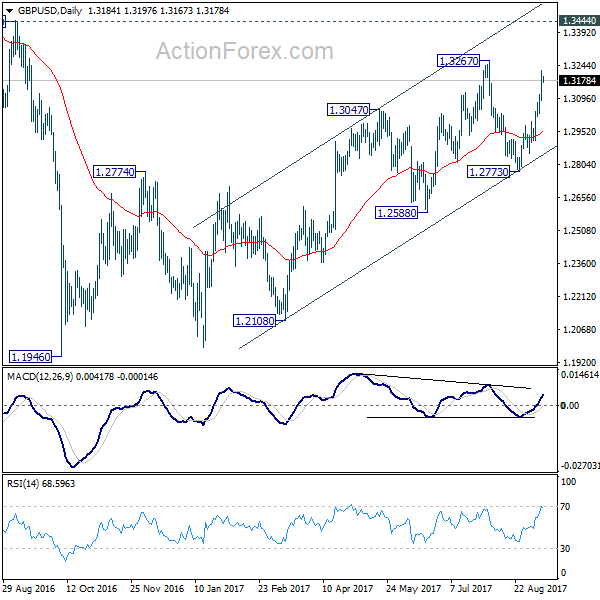

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3113; (P) 1.3168; (R1) 1.3245; More...

Intraday bias in GBP/USD remain son the upside for 1.3267 resistance. Break there will resume whole rise from 1.1946 and target 1.3444 key resistance next. But again, price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside, below 1.3114 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming.