Sample Category Title

Dollar Selloff Accelerates as Trump Warns “All Options are on the Table” after North Korea Missile Firing

Risk aversion dominates the global financial markets as geopolitical tension in Korea Peninsula escalates to a tipping point. North Korea fired a missile over Japan to land in the Pacific Ocean. Japan condemned the act as "an unprecedented, serious and significant threat. US warned that "all options are on the table". Nikkei responded by closing down -0.45% at 19362.55. Major European indices are trading deep in red with FTSE down -1.1%, DAX down -1.7% and CAC down -1.3%. US futures also point to sharply lower open. Gold rides on the sentiment and extends this week's rally, accelerating to as high as 1331.9 so far. In the currency markets, Dollar trades as the weakest ones, followed by commodity currencies and Sterling. Swiss Franc is leading the way up, followed by Yen.

US President Trump: All options are on the table

US President Donald Trump said in a statement that "the world has received North Korea's latest message loud and clear: This regime has signaled its contempt for its neighbors, for all members of the United Nations, and for minimum standards of acceptable international behavior." And he warned that "threatening and destabilizing actions only increase the North Korean regime's isolation in the region and among all nations of the world. All options are on the table."

Japan PMI Abe: US and Japan are "totally at one"

Japan Prime Minister Shinzo Abe said after a 40-minute phone call with Trump that the US and Japan "are totally at one" in the position on North Korea. Abe said he and Trump were in "total agreement" that a emergency meeting of the United Nations Security Council should be held. And Abe said that "President Trump expressed his strong commitment to defending Japan, saying he was 100 percent with Japan as an ally." Abe condemned earlier that "this reckless act of firing a missile over our nation is an unprecedented, serious and significant threat, one that seriously diminishes the peace and safety of the region, and as a result we have lodged a firm protest against North Korea."

China: "Tipping point approaching a crisis" but who to blame?

China urged retraint from all parties and warned that situation had reached "a tipping point approaching a crisis". China Foreign ministry spokeswoman Hua Chunying told a daily press briefing in Beijing: "Think hard about it, who do you think should take the blame, if China is urging all parties to calm down while one party holds constant military exercises … and the other is constantly launching missiles?"

EC Juncker: None of UK's Brexit paper "satisfactory"

European Commission President Jean-Claude Juncker criticized that "none" of UK's positions papers on Brexit is "satisfactory. He complained that "the UK government is hesitant in showing all its cards." Juncker also added that "there are still an enormous number of issues that need to be settled. Not only the border problems with Ireland and Northern Ireland, which is a very serious problem to which we have had no definitive response, but also the issue of European citizens living in the UK and UK citizens living on the continent."

Juncker also reiterated and emphasized that "we need to be crystal clear that there will be no negotiations, particular on trade between the UK and the EU, before all these issues, that is to say those under Article 50, are resolved. That is to say the divorce between the EU and the UK." A European Commission spokesperson later told reports in Brussels that "I will not go beyond what president Juncker said this morning. When the president speaks we never interpret or go beyond that."

EU Barnier urged UK to start "negotiating seriously"

Yesterday, EU chief negotiator Michel Barnier urged UK to begin "negotiating seriously" And Barnier emphasized "we need UK positions on all separation issues. This is necessary to make sufficient progress." And, "we need UK papers that are clear in order to have constructive negotiations and the sooner we remove the ambiguity, the sooner we will be in a position to discuss the future relationship and the transitional period."

US President Trump warned of pulling out from NAFTA

In other news, Trump stepped up his rhetorics on the relationships with Canada and Mexico this week. Trump tweeted that "we are in the NAFTA (worst trade deal ever made) renegotiation process with Mexico & Canada". And he told reporters that "I believe that you will probably have to at least start the termination process before a fair deal can be arrived at. In our opinion, the core of NAFTA renegotiation is to narrow US' trade deficit. With US' trade deficit with Canada on the fall, it would put harder pressure on Mexico in the negotiations.

The market reaction towards NAFTA renegotiation has been muted, overshadowed by other events including North Korean peninsula tensions, US debt ceiling, and central banks' monetary policy outlook. Indeed, we do not expect to see material developments for the rest of the year. However, the parties, especially the US and Mexico, would be eager to complete a deal by mid-2018, ahead of and Mexican election in July and US mid-term election in November." More in Second Round of NAFTA Renegotiation to Begin...

On the data front

Canada IPPI dropped -1.5% mom in July, RMPI dropped -0.6% mom. French GDP grew 0.5% qoq in Q2. German Gfk consumer sentiment rose 0.1 to 10.9 in September. UK nationwide house price dropped -0.1% mom in August. Japan unemployment rate was unchanged at 2.8% in July, household spending dropped -0.2% yoy.

*Quick update: US Case Shiller 20 cities house price rose 5.7% yoy in Jun. Consumer confidence rose to 122.9 in August.

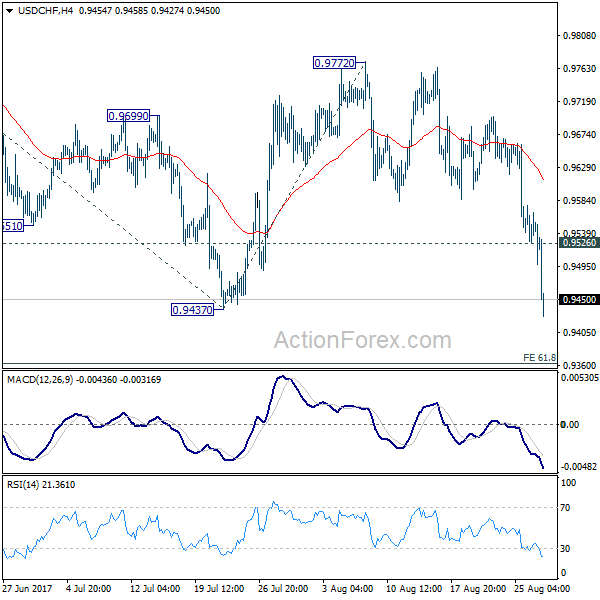

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9526; (P) 0.9552; (R1) 0.9577; More....

USD/CHF's decline accelerates to as low as 0.9427 so far today. The break of 0.9437 key support level suggests that whole down trend from 1.0342 is resuming. Intraday bias remains on the downside and current fall will now target 61.8% projection of 1.0099 to 0.9437 to 0.9772 at 0.9363. On the upside, above 0.9526 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 0.9772 resistance holds.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Jul | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Jul | -0.20% | 0.70% | 2.30% | |

| 06:00 | GBP | Nationwide House Prices M/M Aug | -0.10% | 0.00% | 0.30% | 0.20% |

| 06:00 | EUR | German GfK Consumer Confidence Sep | 10.9 | 10.8 | 10.8 | |

| 06:45 | EUR | French GDP Q/Q Q2 P | 0.50% | 0.50% | 0.50% | |

| 12:30 | CAD | Industrial Product Price M/M Jul | -1.50% | -0.50% | -1.00% | -1.10% |

| 12:30 | CAD | Raw Materials Price Index M/M Jul | -0.60% | -0.30% | -3.70% | -3.60% |

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Jun | 5.70% | 5.60% | 5.69% | |

| 14:00 | USD | Consumer Confidence Aug | 122.9 | 120.4 | 121.1 |

CAC Slides as Euro Climbs, Korea Jitters

The CAC index has posted strong losses in the Tuesday session. Currently, the index is at 5,079.75, down 1.23% on the day. On the release front, French Consumer Spending came in at 0.7%, matching the forecast. French Preliminary GDP improved to 0.5%, also matching the forecast. On Wednesday, the US releases Preliminary GDP, which is expected to post a strong gain of 2.7%.

Geopolitical tensions are back in the headlines this week, as North Korea fired a missile over Japanese territory on Tuesday. Japan and the US have sharply condemned the missile launch, and with tensions once again climbing in the Korean peninsula, investors are bracing for more stock market losses, and both gold and the Japanese yen, which are safe-haven assets, have posted strong gains this week.

The euro is enjoying a solid rally, and has climbed an impressive 2.1% since Friday. Earlier on Tuesday, the euro pushed above the 1.20 line, for the first time since January 2015. A stronger euro has weighed on exporters, and the CAC dipped below the 5,000 level earlier on Tuesday. On Friday, ECB President Mario Draghi took a page out of Janet Yellen's page book, opting to steer away from any discussion about ECB monetary policy in a speech at a meeting of central bankers in Jackson Hole. Draghi seems to have learned a lesson from a meeting of central bankers in Portugal in June, when the markets seized on his comments that the euro zone was undergoing a broad recovery, and the euro soared. With the euro zone enjoying solid growth in 2017, analysts expect the ECB to address its plans for its asset purchases program (QE), which is expected to terminate in December. The ECB is widely expected to taper its QE program early next year, and the euro has jumped 14% against the dollar in 2017.

At the Jackson Hole meeting, Yellen did not discuss interest rate policy, choosing instead to emphasize that the financial regulations put in place since the financial crisis in 2008 should not be undermined. Her message appeared aim at Donald Trump, who has expressed his intention to relax banking and financial regulations which he has argued are hampering business. The markets remain skeptical about a third and final rate hike this year, as the odds of an increase in December have been falling – currently, the odds a December hike are at 35%, down from 42% a month ago.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD continued its bullish momentum yesterday topped at 1.1983. The bias remains bullish in nearest term testing 1.2000 – 1.2050 region as a part of the bullish continuation scenario after broke above the bullish flag formation as you can see on my daily chart below. Immediate support is seen around 1.1910. A clear break below that area could lead price to neutral zone in nearest term but as long as stay above 1.1830 the overall bullish bias should remain strong and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break and daily close above 1.2050 would expose 1.2100 – 1.2175 region.

GBPUSD

The GBPUSD printed a bullish pin bar formation on daily chart after a rejection to move below the daily EMA 200 as you can see on my daily chart below and closed above 1.2915 key resistance. Overall I remain neutral but the bias is bullish in nearest term testing 1.3000 – 1.3030 resistance area. Immediate support is seen around 1.2870 (daily EMA 200). A clear break below that area could lead price to neutral zone in nearest term as direction would become unclear.

USDJPY

The USDJPY was indecisive yesterday. Price attempted to push lower earlier today in Asian session, slipped below 108.70 key support, hit 108.33 but traded higher and struggling around 108.70 at the time I wrote this comment. Overall I still prefer a bearish scenario but need a clear break and daily close below 108.70 to confirm the bearish continuation scenario testing 108.00 – 107.50 area as nearest bearish target. Immediate resistance is seen around 109.25 (current high). A clear break and daily close back above that area could trigger further bullish pressure retesting 109.85 key resistance.

USDCHF

The USDCHF was indecisive yesterday but overall still able to maintain its bearish bias and hit 0.9498 earlier today in Asian session. The bias remains bearish in nearest term testing 0.9450 key support which remains a good place to buy with a tight stop loss. Immediate resistance is seen around 0.9580. A clear break and daily close above that area could trigger further bullish pressure testing 0.9650 – 0.9700 region. On the downside, a clear break and daily close below 0.9450 would expose 0.9350 – 0.9250 region.

Technical Outlook: WTI OIL Is Holding Below Broken Cloud Top, Fresh Bearish Signal Seen On Close Below $46.44 Pivot

WTI oil stays in red on Tuesday and holds below daily cloud top, former strong support which was taken out on yesterday's strong fall. Today's action is holding within narrower range compared to yesterday's span, with upside attempts being capped under daily cloud top (now acting as resistance at $47.01) but also holding above yesterday's low at $46.14. Bearish signal was generated after break below triangle support line as well as break and close below daily cloud top. Bears need the final negative signal on close below cracked support at $46.44 (17 Aug trough) to confirm continuation of downmove from $50.41 (01 Aug peak). Bearish extension below $46.44 would target $45.39/24 (24 July trough/Fibo 61.8% of $42.04/$50.41 rally).

Res: 46.94, 47.01, 47.43, 47.67

Sup: 46.14, 45.80, 45.39, 45.24

Gold Surges, Dollar And Stocks Tumble On Latest North Korea Missile Strike

Geopolitical tensions came back to haunt markets today after North Korea fired an unidentified ballistic missile over Japan. The missile flew over the northern Japanese island of Hokkaido before falling into the Pacific. This was the first missile to pass over Japanese territory since 2009 and comes after North Korea recently backed down from its threat to strike the US military installation in Guam in the Pacific Ocean earlier this month.

The latest provocation has reignited fears of a serious escalation of tensions between the United States and North Korea, raising the stakes to a new level. Although some reaction from the North was expected to the recent UN sanctions and joint military drill currently underway between the US and South Korea, today's actions could prompt a tougher response by President Trump. Military action seems unlikely at this point but not totally improbable. The Japanese government would likely be supportive of a US-led military response, though the new South Korean President is seen as favouring dialogue as long as that remained an option.

Gold was the biggest gainer from the latest flight to safety caused by today's strike. The precious metal jumped more than 1%, reaching a 9½-year high of $1325.94 an ounce in European trading. Exasperating gold's gains has been broad dollar weakness on fading expectations of a third rate hike by the Fed this year. The combined effect has pushed gold into oversold territory according to many technical indicators, so further gains in the near term may be limited.

In forex markets, the dollar fell to a 4-month low of 108.25 yen, while its broader measure, the dollar index, slid to its lowest since January 2015, tumbling to 91.62. The possibility of conflict involving Japan failed to deter the safe-haven yen (although it did hurt the Korean won). The Japanese currency was also up sharply against the Australian dollar and the pound, rising by around 0.5% to 86.51 and 140.54 respectively. The Swiss franc posted even larger gains versus the greenback, surging by more than 1% to a two-year high. The dollar was last trading at 0.9435 francs, not far from its session low of 0.9428 francs.

Stocks were also hit by the latest bout of risk aversion, with European bourses following their Asian counterparts in negative territory. The pan-European Stoxx 600 index was last trading 1.4% lower at 367.22

Japanese Consumption Disappoints But Labor Conditions Remain Robust, Yen Surges On Rising Geopolitical Tensions

Japanese data showed on Tuesday that the labor market continued strengthening in July in line with expectations, remaining near full employment conditions. However, other data on household spending indicated that better labor conditions did not support consumption in the aforementioned period. The yen overall experienced substantial demand today, hitting a 4 ½ – month high as heightened geopolitical tensions in the Korean peninsula came into the spotlight.

During early Asian trading hours, the Japan Institute for Labour Policy and Training released figures on the jobs to application ratio and the unemployment rate for the month of July. According to the numbers, each applicant was assigned to 1.52 available positions as expected, compared to 1.51 positions in the previous month. This was the highest jobs to application ratio recorded since February 1974, when the Japanese economy was booming.

Regarding the unemployment rate, this matched expectations, remaining steady at June’s mark of 2.8% in July and indicating that the Japanese labor market was operating near full employment conditions. Note that, this level was last seen back at the end of the 1980s and early 1990s when the unemployment rate was fluctuating around 2.0%.

While the labor environment seems to be improving, consumers surprisingly held back from purchases. Based on Statistics Bureau, household spending turned negative after three months of rising, falling by 1.90% month-on-month. Analysts anticipated that consumers’ spending would decline moderately by 0.50% following 1.50% growth in June. On a yearly basis, household spending dropped by 0.20% compared to a rise of 0.70% forecasted and a 2.30% growth seen in June.

Even though core inflation showed signs of building momentum, rising slowly for four consecutive months to 0.40% in August, the recent downturn in household spending is less likely to provide support to inflation in the upcoming months. Moreover, most companies’ attitude of refusing to increase prices in order to avoid losing clients, as wage growth remains subdued, restricts inflation from approaching the BOJ’s target of 2.0% anytime soon. Nevertheless, the Japanese government expressed yesterday its persistent optimism on the economy’s outlook, stating that that business spending, exports, and output were “picking up” while it also said that private consumption was growing moderately, signaling a solid recovery.

Turning to the reaction in the forex markets, dollar/yen reacted little to the data as geopolitical risks heightened substantially on Tuesday after Japan announced earlier today that a ballistic missile weapon, launched by North Korea, flew across the Japanese island of Hokkaido before it fell into the Pacific Ocean. The pair dipped by 0.55% to a 4 ½ -month low of 108.32 as investors were selling riskier assets to buy safe haven ones including the yen. However, the pair managed to climb to a session high of 108.93 immediately after the data release but its gains were short-lived as it pulled back to 108.39 afterwards.

WTI Oil Futures Under Pressure, Bias Tilted To Downside

WTI oil futures are giving a bearish picture on the 4-hour chart. Prices are on a downwards trajectory as they have been making lower highs since the August 10 peak of 50.19. The 20-period moving average (MA) crossed below the 50-period MA earlier today giving a bearish signal.

Following a neutral phase between August 21 until 28, prices came under severe pressure after breaking below the key 47.00 level. This is now expected to act as strong resistance to the upside. Downward momentum has clearly picked up based on the falling MACD. But the flat RSI suggests some consolidation in the near term. A move below 46.13 would open the way to target the next major low at 45.38 (July 24 low). Such a move would strengthen the bearish scenario.

Only a sustained move above 47.00 would indicate that the near-term downward pressure has eased. Trading above this support level brings the market back to neutral until prices rise towards the next major top at 48.87 (August 18 high). From here, a push higher to reclaim the key 50.00 level cannot be ruled out.

For now, the bias is tilted to the downside based on the bearish technicals, which are diminishing the odds for a sustained rebound in the short-term.

Euro Jumps Above 1.20 As German Consumer Climate Picks Up

EUR/USD has posted considerable gains in the Tuesday session. Currently the pair is trading at 1.2046, up 0.57% on the day. On the release front, French Consumer Spending came in at 0.7%, matching the forecast. French Preliminary GDP improved to 0.5%, also matching the forecast. In the US, today’s key event is CB Consumer Confidence, which is expected to dip to 120.9 points. On Wednesday, Germany releases Preliminary CPI, and the US publishes ADP Nonfarm Payrolls and Preliminary GDP.

The euro continues to push higher, and has climbed an impressive 2.1% since Friday. Earlier on Tuesday, the euro punched above the 1.20 line, for the first time since January 2015. On Friday, ECB President Mario Draghi took a page out of Janet Yellen’s page book, opting to steer away from any discussion about ECB monetary policy in a speech at a meeting of central bankers in Jackson Hole. Draghi seems to have learned a lesson from a meeting of central bankers in Portugal in June, when the markets seized on his comments that the euro zone was undergoing a broad recovery, and the euro soared. With the euro zone enjoying solid growth in 2017, analysts expect the ECB to address its plans for its asset purchases program (QE), which is expected to terminate in December. The ECB is widely expected to taper its QE program early next year, and the euro has jumped 14% against the dollar in 2017.

At the Jackson Hole meeting, Yellen did not discuss interest rate policy, choosing instead to emphasize that the financial regulations put in place since the financial crisis in 2008 should not be undermined. Her message appeared aim at Donald Trump, who has expressed his intention to relax banking and financial regulations which he has argued are hampering business. The markets remain skeptical about a third and final rate hike this year, as the odds of an increase in December have been falling – currently, the odds a December hike are at 35%, down from 42% a month ago.

Market Update – European Session: Risk Aversion Sentiment Back On Front Burner

Notes/Observations

Risk aversion sentiment was the theme in the session after the latest North Korean missile threat revived geopolitical tensions

British and EU negotiators resumed Brexit talks but officials played down the prospect of breakthroughs

Tropical Storm Harvey poised to re-enter the Gulf of Mexico and make another landfall closer to Houston

Overnight

Asia:

North Korea launched missile that passed over Northern Japan and landed into the sea

Japan PM Abe: North Korea missile is an unprecedented serious and grave threat to Japan. Spoke with President Trump for 40 minutes, agreed to strengthen pressure on North Korea, Trump gave "strong commitment" to Japanese security

Japan Chief Cabinet Sec Suga:Missile flying over Japan is a new and serious development, no objects did fall on Japan territory. Will take appropriate steps as needed regarding North Korea missile

Japan Foreign Min Kono: Discussed further sanctions on North Korea with US

South Korea President Moon orders show of force in response with 4 f-15k fighters conducting bomb dropping exercise

Japan July Jobless Rate matched its lowest rate since Jun 1994 ( 2.8% v 2.8%e)

Europe:

EU Chief Brexit Negotiator Barnier said to have expressed concern about progress so far in Brexit talks. UK needs positions on all issues and must start negotiating seriously

Germany Fin Min Schaeuble reiterates debt cut for Greece not currently on the agenda. Greece must press ahead with reform-for-aid program

Americas:

President Trump: Mexico has been very difficult in NAFTA talks, why wouldn't they, they had a sweetheart deal for so long. One way or another Mexico will pay for the border wal

Energy:

Saudi Arabia and Russia are pushing to extend their deal to limit crude oil production for another three months

Economic data

(DE) Germany Sept GfK Consumer Confidence: 10.9 v 10.8e (highest since Oct 2001)

(UK) Aug Nationwide House Price Index M/M: -0.1% v 0.0%e ; Y/Y: 2.1% v 2.5%e

(NO) Norway Q2 Manufacturing Wage Index Q/Q: 0.4% v 0.7% prior

(FR) France Q2 Preliminary GDP Q/Q: 0.5% v 0.5%e; Y/Y: 1.7% v 1.8%e

(FR) France July Consumer Spending M/M: 0.7% v 0.7%e; Y/Y: 2.1% v 1.8%e

(TR) Turkey Aug Economic Confidence: 106.0 v 103.4 prior

(TR) Turkey July Trade Balance: -$8.8B v -$8.8Be

Fixed Income Issuance:

(ID) Indonesia sold total IDR7.0T in 6-month Bills & 2-year,4-year,7-year and 15-Year Project-based Sukuk (PBS)

(IT) Italy Debt Agency (Tesoro) sold €6.0B vs. €6.0B indicated in 6-month Bills; Avg Yield: -0.356% v -0.362% prior; Bid-to-cover: 1.72x v 1.62x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -1.7% at 3,365, FTSE -1.5% at 7,292, DAX -2.0% at 11,877, CAC-40 -1.6% at 5,000, IBEX-35 -1.4% at 10,146, FTSE MIB -1.5% at 21,397, SMI -1.2% at 8,759, S&P 500 Futures -0.7%]

Market Focal Points/Key Themes: European indices opened down and continued lower; geopolitical concerns driving negative risk sentiment; all sectors move lower; Prosiebensat cuts outlook, dragging on broadcasters; insurers still under pressure pending evaluation of impact from Hurricane Harvey;commodity strength did not translate into support for materials stocks; upcoming earnings in US session include Best Buy and H&R Block

Equities

Consumer discretionary: Prosiebensat PSM.DE -10.0% (cuts outlook, analyst action), Mitie MTO.UK -0.4% (FCA opens investigation)

Materials: Avocet Mining AVM.UK 11.4% (standstill extension agreement)

Industrials: Hapag-Lloyd HLAG.DE % (earnings)

Financials: Wendel MF.FR +2.8% (analyst action), Sydbank SYDB.DK -3.8% (earnings), Van Lanschot LANS.NL +1.7% (results), Banca Generali BGN.IT 2.9% (analyst action)

Technology: Adva Optical ADV.DE -22.3% (cuts outlook)

Utilities: Findel FDL.UK +9.6% (trading update)

Energy: CGG CGG.FR -10.8% (analyst action), Statoil STL.NO -1.7% (Korpfjell exploration doesn't find oil), Lundin Petroleum LUPE.SE -6.7% (Korpfjell exploration doesn't find oil)

Speakers

German Chancellor Merkel: Seeing positive economic data in Europe; improving employment a good sign

South Africa Central Bank (SARB): Rate cut cycle likely to be modest

Denmark Finance Ministry presented its tax proposal; to cut taxes by DKK23B on cars, income and pensions. Cuts to be phased in through 2025 and apply to all income groups

Greece PM Tsipras: Conditions were appearing for a steady return to growth. 2017 GDP growth seen near 2.0%

Italy Business industry lobby Confindustria: Strong EUR currency to significantly affect the Italian economy

Poland Central Bank's Kokoszczynski: Interest rate hike unlikely ahead of 2019 Presidential election -

China Foreign Ministry spokesperson Chunying: Urged relevant countries from provoking each other. Threats and sanctions could not solve the North Korea issue

Currencies

Risk aversion sentiment was the theme in the session after the latest North Korean missile threat revived geopolitical tensions - USD Index remained at 2 1/2 lows and did not participate in any safe-haven flows,

EUR/USD tested above the 1.20 level for its highest reading since Jan 2015. The pair has been moving higher ever since ECB chief Draghi did not comment or show any concern over its recent appreciation.

USD/JPY hovering around the 108.50 as the JPY currency (yen) benefited from risk-aversion sentiment .

Fixed Income

Bund futures trades at 165.58 up 79 ticks as the latest North Korean missile threat revives geopolitical tensions. Downside targets 164.50 followed by 163.75. To the upside the 165.75 to 166.00 remains key resistance.

Gilt futures trades at 128.73 up 67 ticks following other haven assets on the broad risk-off move. A resumption to the upside could eye 129.25 then 130.10. A move back below 128.25 targets 126.51

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.700T from €1.701T and use of the marginal lending facility rose to €634M from €310M.

Corporateissuance no deals price in high grade primary

Looking Ahead

(BR) Brazil July Central Govt Budget Balance (BRL): No est v -19.8B prior

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (EU) ECB alotment in 7-day Main Financing Tender (MRO) vs. €7.0Be

05:30 (DE) Germany to sell €5.0B in new 0% coupon Sept 2019 Schatz

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Aug FGV Inflation IGPM M/M: +0.1%e v -0.7% prior; Y/Y: -1.7%e v -1.7% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (BR) Brazil July PPI Manufacturing M/M: No est v 0.0% prior; Y/Y: No est v 1.5% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada July Industrial Product Price M/M: -0.5%e v -1.0% prior; Raw Materials Price Index M/M: -0.3%e v -3.7% prior

08:55 (US) Weekly Redbook Sales

09:00 (US) Jun S&P/Case-Shiller 20-City M/M: 0.10%e v 0.1% prior; Y/Y: 5.60%e v 5.7% prior; House Price Index (HPI): No est v 198.97 prior

09:00 (US) Jun S&P/Shiller Case-Shiller (overall) HPI Y/Y: No est v 5.6% prior, House Price Index (HPI): No est v 190.61 prior

09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

09:00 (EU) Weekly ECB Forex Reserves

09:00 (RU) Russia announces weekly OFZ bond auction

10:00 (US) Aug Consumer Confidence: 120.4e v 121.1 prior

11:00 (US) Fed Evans (dove, voter)

11:30 (US) Treasury to sell 4-Week Bills

13:00 (US) Treasury to sell 7-Year Notes

16:30 (US) Weekly API Oil Inventories

CRUDE OIL Short-Term Bearish

Crude oil is trading lower. Hourly support is given at 45.40 (17/08/2017 high). Strong resistance can be found at 50.41 (31/07/2017). Expected to show continued short-term bearish move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).