Sample Category Title

USD/CAD Continued Selling Pressures

USD/CAD selling continues. Hourly support is given at a distance at 1.2414 (27/07/2017 low) while resistance is now given at a distance at 1.2778 (15/08/2017 low). Expected to show continued short-term bearish move.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low) before bouncing back. Strong resistance is given at 1.4690 (22/01/2016 high). The pair should head further lower.

USD/CHF Selling Pressures Increase

USD/CHF is heading lower. Strong resistance is given at 0.9771 (15/06/2017 high). Hourly support at 0.9584 (08/11/2017 low) has been broken. Expected to show growing continued bearish pressures.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/JPY Monitoring Strong Support

USD/JPY is now monitoring support at 108.13 (17/04/2017 low). Expected to show another leg lower.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Bouncing Higher

GBP/USD bearish momentum has bounced around support given at 1.2774 (24/08/2017 high). Hourly resistance is given at 1.3031 (11/08/2017 high). Expected to show short-term bullish pressures.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Strong Bullish Trend

EUR/USD bullish pressures are strong. The pair has broken hourly resistance at 1.1910 (02/08/2017 high) while hourly support lies at 1.1662 (17/08/2017 low). Expected to show increasing bullish pressures.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Traders Head For Safety As Japan Sirens Sound

We're seeing significant risk aversion in the markets on Tuesday, with European indices heavily in the red, US futures indicating a similar open on Wall Street, Gold at near-10 month highs and the yen making steady gains.

A ramp up in tensions between North Korea and the US, South Korea and Japan overnight has raised geopolitical risk once again, with Kim Jong Un showing no signs of ceding to international pressures. The missile launch comes as no surprise given proximity to the annual military exercises between the US and South Korea, but the fact that the missile was shot over Northern Japan and prompted warning sirens encouraging people to take cover is a concern.

The distressing impact of Hurricane Harvey in Houston is also weighing heavily on sentiment this morning. From a markets perspective, the uncertainty surrounding the cost and the economic implications of the storm is going to be a concern for investors, although it is difficult to look past the sheer devastation it has caused at the moment.

The dollar is coming under significant pressure in the aftermath of the storm, which has taken the dollar index to its lowest since the start of 2015 and below the 92-93 support zone that has held firmly since then. This move has coincided with the euro trading at its highest against the greenback since the first trading day of 2015, which will be a blow to the ECB which has tried to repeatedly talk down the currency as it prepares to further reduce its quantitative easing program.

Draghi's comments at Jackson Hole did little to halt the charge higher, with the ECB President keen to stress that “a significant degree of monetary accommodation” is still warranted, a statement which doesn't suggest the current level will remain. He's doing his best to talk down the currency but the fact of the matter is that he'd going against the tide, the ECB wants to taper and it looks as though it's going to happen. Traders hear his words and are look past the dovish filler and instead focus on what he isn't saying.

Gold is trading higher again on Tuesday, having finally broken through $1,300 on Monday driven by safe haven demand. The next test for the yellow metal should come around the November high around $1,337.40 but I think further gains could be in store.

Trade Idea: GBP/JPY – Sell at 142.00

GBP/JPY - 140.75

Trend: Near term down

Original strategy:

Sell at 142.00, Target: 140.00, Stop: 142.60

Position: -

Target: -

Stop: -

New strategy :

Sell at 142.00, Target: 140.00, Stop: 142.60

Position: -

Target: -

Stop:-

Although the British pound retreated after marginal rise to 141.40 yesterday, as sterling found good support just above 140.00 level and has rebounded, retaining our view that further consolidation would take place and another bounce to 141.40 is likely, however, still reckon upside would be limited to 141.90-00 and bring another decline later. A break of said support at 140.00-05 would suggest top is possibly formed, break of 139.80-85 would signal the rebound from 139.35 has ended, bring retest of this level, below would extend recent decline to 138.70 (previous support) but loss of downward momentum should prevent sharp fall below 138.30 and 138.00 should hold.

In view of this, we are looking to sell sterling on subsequent recovery as 141.90-00 should limit upside and bring such a decline. A firm break above resistance at 142.05 would suggest low is possibly formed instead, bring a stronger rebound to 142.50-60 but resistance at 143.20 should remain intact and bring another decline later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Tensions Flare Amid Missile Launch

Rush for safe-haven as North Korea fires missiles

Investors piled into safe havens on Tuesday morning amid rising global uncertainties. Firstly, last week comments from Donald Trump have heightened concerned about a potential government shutdown should the Congress keeps refusing to fund the wall along the southern border with Mexico. Even the arrival of Hurricane Harvey in Texas wasn’t enough to make Trump back off on his threat. Against such a backdrop, the US dollar extended losses with the dollar index breaking the 91.91 support (low from May 2016) to the downside. Normally, the greenback is considered as a “light” safe haven asset meaning that when uncertainty rises, the dollar depreciates against the Japanese yen and the Swiss franc at most. It seems now that Trump punches its weights on the USD.

The launching of ballistic missiles over Japan by North Korea also helped the CHF and the JPY to rise across the board. So far investors wrongly assumed that the North Korean situation was under control and that some negotiations were taking place behind closed door. The Swiss franc and the Japanese yen rose 0.90% and 0.75% against the USD. The yellow metal was also better bid as it climbed to $1,325 per ounce, up 1.15% on the day.

Despite the fact that the Trump and Kim Jong-un are keeping investors on their toes for longer than expected, we maintain our view that the USD is oversold. The question now is to determine how long this spike in uncertainty will last. Therefore investors will need to have patience and let the storm go by.

Gold bounces back

For the first time this year, gold has broken the strong resistance at $1300 and the precious metal is now standing around 1317$, its highest level since 2016. The summer was quiet but volatility is back due to the escalating tensions between the US and North Korea. We also believe that those tensions are not the only reasons for the gold surge. Economic reasons are also important. The US S&P 500 index went from 2480 to 2440 and it seems that investors become more reluctant to buy stocks at those elevated prices.

On top of that, we consider that the Fed made a clear U-turn by raising rates twice this year before stating that it was almost done with rate hikes. The US central bank went from hawkish to dovish. We recall that the Fed was expected to raise rates at least 3-4 times this year. Markets are now ruling out a rate hike before year-end.

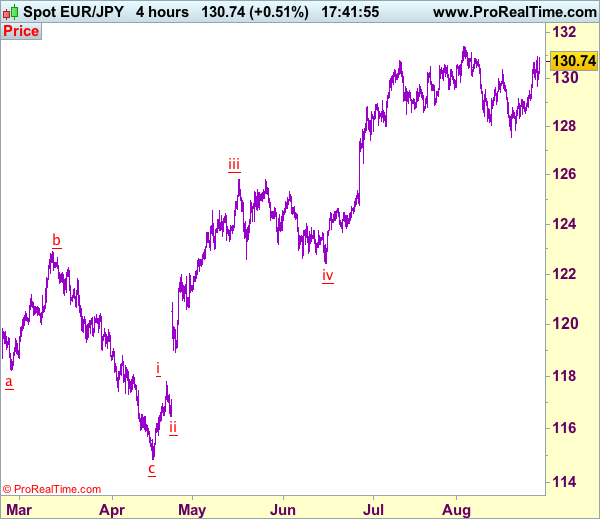

Trade Idea: EUR/JPY – Hold long entered at 129.70

EUR/JPY - 130.75

Original strategy:

Bought at 129.70, Target: 131.70, Stop: 129.10

Position: - Long at 129.70

Target: - 131.70

Stop: - 129.10

New strategy :

Hold long entered at 129.70, Target: 131.70, Stop: 130.00

Position: - Long at 129.70

Target: - 131.70

Stop:- 130.00

Although the single currency retreated after rising to 130.97 yesterday, as euro found renewed buying interest at 129.66 and has rebounded in line with our bullish expectation (we recommended to buy at 129.70 and a long position was entered), adding credence to our bullish view that the rise from 127.56 low is still in progress, hence further gain to recent high at 131.40 would be seen, once this level is penetrated, this would extend early upmove to 131.90-00 but near term overbought condition should prevent sharp move beyond 132.50-60.

In view of this, we are holding on to our long position entered at 129.70. Below 130.00 would risk test of said support at 129.66 but only break there would signal top is formed instead, risk correction to 129.10-15, break there would confirm and correction to 128.75-80 would follow but still reckon 128.30-35 support would remain intact and bring another rise later this week.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Risk Aversion Prevails As North Korea Fires Missile Over Japan

Overnight, North Korea fired a missile that violated Japanese airspace and fell approximately 1180km east of Japan’s Hokkaido Island. According to media reports, this act may have been intended to show that an attack on the US territory of Guam is possible. North Korea has conducted several missile tests lately, but a rocket has not flown over Japan since 2009. This marks a clear escalation of the latest geopolitical tensions in the region, and likely comes as a response to the military drill that the US and South Korea have been conducting recently.

The market response was a classic risk-off reaction, with investors immediately turning to safe haven assets. Gold, JPY, and CHF all rallied on the news, while riskier assets such as the AUD and Japanese stocks tumbled. We believe that this negative sentiment may spill over into European and US equity markets, the indices of which could open with negative gaps today.

Moving forward, we expect market action to be very much headline-driven. A lot may depend on how the US, Japan and South Korea respond to this aggression. Japanese PM Abe already stated that 'We must immediately hold an emergency meeting at the United Nations, and further strengthen pressure against North Korea'. Such a diplomatic response would likely be the 'soft' approach, and may thus carry little market impact. On the other hand, if we see an escalation in rhetoric, such as more 'fire and fury' comments or some form of action from the NATO countries, this risk-off sentiment could linger and we may see the overnight price action continue.

USD/JPY traded lower overnight following the news. The pair dipped briefly below 108.70 (S1), but quickly rebounded to trade fractionally above it. The rate is back within the range between 108.70 (S1) and 111.00 and thus, the short-term outlook remains flat in our view. If the situation escalates further, we expect the bears to drive the battle back below 108.70 (S1), a move that could turn the bias to the downside this time, and initially aim for the 108.00 (S2) support.

Switching to the daily chart, we see that the pair is trading within a broader range between 108.70 (S1) and 114.40. This keeps the medium-term outlook flat as well, but a clear dip below 108.70 (S1) could be the first sign for larger downside extensions, perhaps towards the long-term upside support line, taken from the low of the 24th of June 2016.

Gold surged yesterday, breaking above the key psychological barrier of 1300 (S2). Subsequently, the metal gapped further up after North Korea fired a missile over Japan, to hit resistance at 1325 (R1) before retreating somewhat. The 1300 (S2) zone acted as the upper bound of the wide range the metal has been trading within since the 31st of January, between that hurdle and the 1200 territory. As such, its clearing make us confident that the outlook may have turned somewhat positive. We would expect a move above 1325 (R1) to set the stage for extensions toward our next resistance of 1340 (R2). Having said that, given that the latest rally appears overextended, we would stay careful of a possible retreat before the bulls decide to take charge again. A dip below 1313 (S1) may confirm the case and is possible to open the way for a test near the 1300 (S2) zone as a support this time.

The economic calendar is light today:

We only get second-tier economic indicators: The UK nationwide house price index for August, Canada’s PPI for July, the US S&P/Case-Shiller house price index for June, and the nation’s Conference Board consumer confidence index for August are all due out. We have only one speaker on the agenda: Chicago Fed President Charles Evans. He is a voting FOMC member this year, and usually maintains a cautious stance on policy matters. Speaking in early August, Evans said that inflation would have to accelerate for him to support an interest-rate hike at the end of the year. Given that the latest US CPI prints were disappointing, we doubt he will deviate much from his latest dovish remarks.

USD/JPY

Support: 108.70 (S1), 108.00 (S2), 107.40 (S3)

Resistance: 109.00 (R1), 109.40 (R2), 109.75 (R3)

Gold

Support: 1313 (S1), 1300 (S2), 1292 (S3)

Resistance: 1325 (R1), 1340 (R2), 1352 (R3)