Sample Category Title

Cliff Notes: Continued Labour Market Resilience Constructive for Outlook

Key insights from the week that was.

January’s Westpac-MI Consumer Sentiment survey suggests the Australian consumers’ mood soured over the holiday period. Following a –2.0% dip in December, the headline index fell another 0.7% to 92.1 in January. That said, most of the constituent sub-indexes did not deteriorate during the month, including the one-year outlook for family finances (+1.1%), the one-year and five-year outlook for the economy (0.0% and +0.7%), and ‘time to buy a major household item’ (+1.8%). January’s headline decline instead stemmed from a 7.8% fall in households’ assessment of their finances versus a year ago, reversing December’s gains. Overall, the partial reversal of 2024’s gains over December and January and the indexes’ current sub-par level highlights the enduring impact of cost-of-living pressures, both on current spending and confidence.

It was somewhat surprising to see consumers’ job loss fears worsen in January given the recent strength of official labour market data. December’s Labour Force Survey confirmed our labour market finished the year on a strong footing having remained tight throughout 2024 – measures of slack little changed over the period. Given these developments, the next update for wages will be keenly assessed for risks to inflation. With demand matching the supply of labour, we anticipate wages growth will continue to track lower over 2025 in a manner consistent with inflation returning to target. We view May as the most likely starting point for the 100bps of RBA rate cuts forecast by year end, though risks are tilted towards an earlier start, depending on the strength of the next quarterly inflation print due at month end.

Westpac’s Chief Economist Luci Ellis also investigated some key medium-term issues this week, including how Australia’s floating exchange helps our nation navigate global shocks and productivity.

Offshore, market participants have been kept busy between New Year’s and President Trump’s inauguration – scheduled for next week.

Last Friday, December nonfarm payrolls 256k gain beat the market’s expectation of 165k by a wide margin, even accounting for revisions to the prior two months (-8k). The unemployment rate meanwhile ticked down to 4.1% thanks to a striking 478k rebound in household employment. Note however, over 2024, the monthly gain for household employment averaged just 45k, a fraction of nonfarm payrolls 186k. There remains a significant discrepancy between the two labour market surveys which will only be partly addressed by the annual revision to nonfarm payrolls which will revise history up to March 2024. Helpfully for the FOMC, the wage pulse remains benign, annual growth of 3.9%yr at December at the top of the range historically consistent with consumer inflation at target.

December’s CPI report was also constructive for a continuation of rate cuts through 2025. Core inflation slowed from 0.3% to 0.2% in the month, and the annual rate edged down from 3.3%yr to 3.2%yr. Shelter inflation remains a multiple of the FOMC’s 2.0% target on an annual and annualsed basis; but ex-shelter, headline CPI has now been at or below 2.0% for 16 of the past 20 months – the remaining 4 prints were between 2.0%yr and 2.3%yr.

Still, like the labour market detail, retail sales suggests the FOMC has time on its side as it assesses current and potential inflation risks, headline sales rising 0.4%mth in December and the control group, which feeds into GDP, 0.7%. The control group’s Q4 gain of 1.3% is in line with Q3’s 1.4%, indicating support for aggregate activity from household demand persisted into year end.

Across the pond, the UK CPI also showed promise in December, headline inflation easing to 2.5%yr, in line with the Bank of England’s forecast. Crucially, services inflation decelerated 0.6ppts to 4.4%yr. Bear in mind that a sharp drop in airfares contributed to December’s decrease. Still, while that outcome may reverse, the overall trend in both services and goods inflation seem conducive to additional rate cuts in 2025, aiding activity growth’s recovery.

China’s Q4 GDP and partial data has just been released. As we expected, authorities’ 5.0% target was achieved for the full year, thanks to an acceleration in annual growth from 4.6% to 5.4% Q3 to Q4. Also benefitting the year-to-date result was an upward revision to quarterly growth in Q3 from 0.9% to 1.3%, compared to 1.6% in Q4.

The detail underlying the result is still to come, but December’s partial data was constructive for industrial production (growth accelerated from 5.4%yr to 6.2%yr) and retail sales (from 3.0%yr to 3.7%yr), and suggests a floor is being put in for fixed asset investment (year-to-date growth little changed at 3.2%). Although, on a year-to-date basis, industrial production and retail sales growth was also unchanged from Q3 to Q4 at 5.8%ytd and 3.5%ytd. Focusing on property, policy support is only slowly impacting conditions, home price declines incrementally abating month-on-month towards zero (-0.1% and -0.3% in December for new and existing homes), and new property sales still down 17.6%ytd in December, a slight improvement on November’s -20.0%ytd.

These outcomes point to resilience in China’s economy, but also a need for further significant policy support in coming months. The development of new industry and export markets outside the US are serving China well. But, to sustain growth near 5.0% in coming years and thereby deliver pledged welfare gains over the coming decade, the consumer and non-manufacturing investment must accelerate sustainably. Following lunar new year celebrations at the end of January, look for additional actions by policy makers targeting consumer income and sentiment as well as property and equity markets.

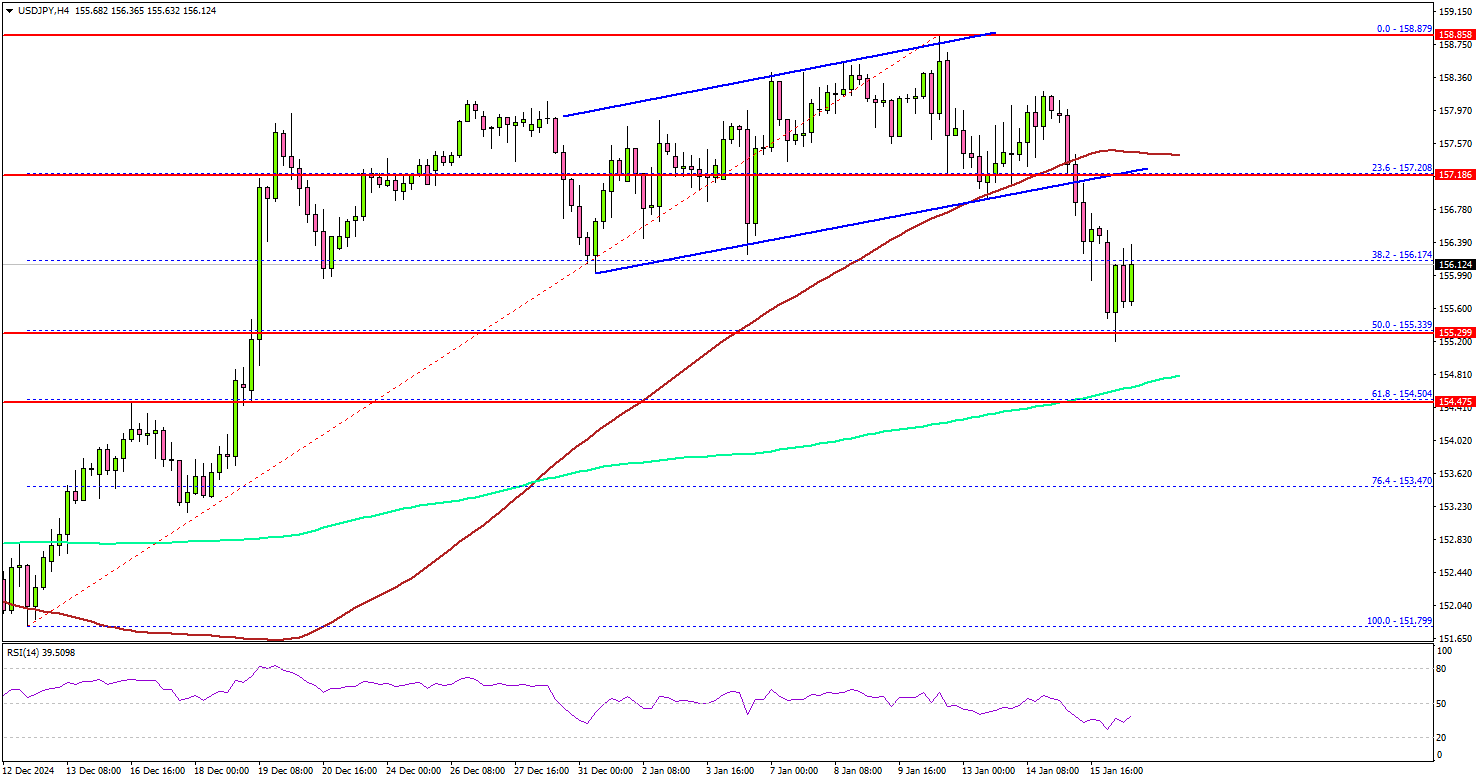

USD/JPY Pulls Back: Is This The Start of Larger Correction?

Key Highlights

- USD/JPY started a downside correction from the 158.85 zone.

- It traded below a key rising channel with support at 157.10 on the 4-hour chart.

- EUR/USD is struggling to recover above the 1.0350 resistance.

- GBP/USD is still trading in the red zone below 1.2350.

USD/JPY Technical Analysis

The US Dollar struggled to rise toward 160.00 against the Japanese Yen. USD/JPY traded as high as 158.87 on TitanFX and recently corrected some gains.

Looking at the 4-hour chart, the pair declined below the 158.00 and 157.50 support levels. It traded below a key rising channel with support at 157.10. There was a move below the 38.2% Fib retracement level of the upward move from the 151.79 swing low to the 158.87 high.

The pair settled below the 100 simple moving average (red, 4-hour), but remained above the 200 simple moving average (green, 4-hour). On the downside, immediate support sits near the 155.35 level.

The 50% Fib retracement level of the upward move from the 151.79 swing low to the 158.87 high is also near 155.35. The next key support sits near the 154.50 level and the 200 simple moving average (green, 4-hour).

Any more losses could send the pair toward the 153.50 level. On the upside, the pair is facing hurdles near the 156.80 level. The first major resistance is near the 157.20 level.

The next major resistance is near the 157.50 level. A close above the 157.50 level could set the tone for another increase. In the stated case, the pair could rise toward the 158.80 resistance. The main hurdle could be 160.00.

Looking at EUR/USD, the pair started a short-term recovery wave, but the bears are active near the 1.0350 resistance zone.

Upcoming Economic Events:

- US Housing Starts for Dec 2024 (MoM) – Forecast 1.320M, versus 1.289M previous.

- US Building Permits for Dec 2024 (MoM) – Forecast 1.460M, versus 1.493M previous.

Elliott Wave View Looking for NZDUSD to Extend Lower

Short Term Elliott Wave view in NZDUSD suggests that cycle from 9.30.2024 high is in progress as an impulse. Down from 9.30.2024 high, wave (1) ended at 0.5813 and wave (2) ended at 0.5929. Pair has resumed lower in wave (3) which ended at 0.5583 as the 1 hour chart below shows. Rally in wave (4) unfolded as a zigzag. Up from wave (3), wave A ended at 0.5684 and wave B ended at 0.5628. Wave C higher ended at 0.5692 which completed wave (4) in higher degree.

Pair has resumed lower in wave (5). Down from wave (4), wave ((i)) ended at 0.5568 and wave ((ii)) rally ended at 0.5603. Wave ((iii)) lower ended at 0.5539 and rally in wave ((iv)) ended at 0.5573. Final leg wave ((v)) ended at 0.5538 which completed wave 1. From there, pair bounce in wave 2 with internal subdivision as a zigzag. Up from wave 1, wave ((a)) ended at 0.563 and wave ((b)) ended at 0.558. Wave ((c)) higher ended at 0.565 which completed wave 2 in higher degree. Near term, as far as pivot at 0.569 high remains intact, expect rally to fail in 3, 7, 11 swing for more downside.

NZDUSD 60 Minutes Elliott Wave Chart

NZDUSD Elliott Wave Video

https://www.youtube.com/watch?v=qdF60IkBcTI

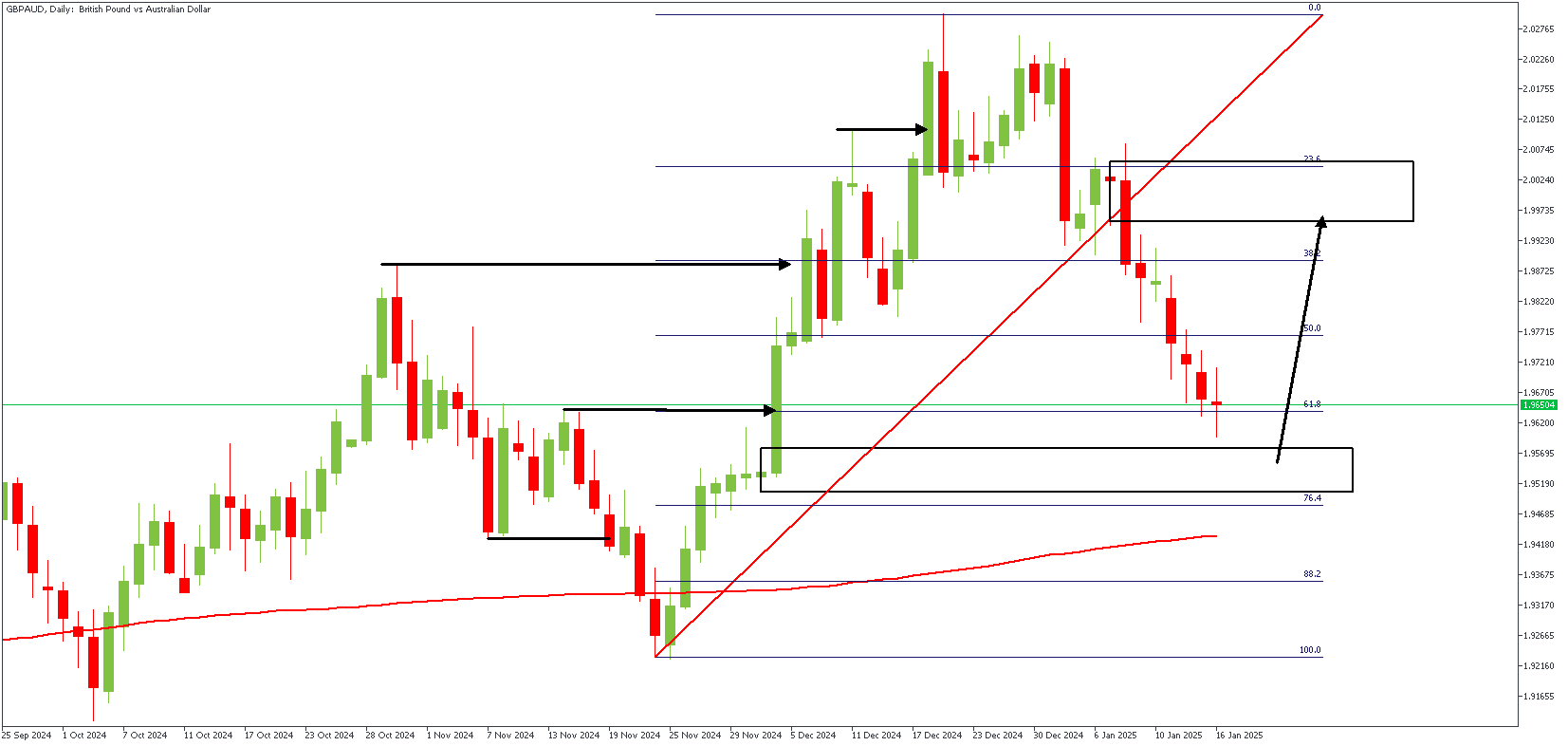

Is GBPAUD Ready for a Rebound?

The Pound Sterling weakened on Thursday after reports showed the UK economy grew less than expected in November, while factory activity continued to decline. The UK’s GDP grew by 0.1% after shrinking in October, falling short of the 0.2% growth economists had predicted. Additionally, manufacturing and industrial production dropped in November, signaling ongoing challenges for UK factories as demand remains weak.

Traders increasingly bet that the Bank of England (BoE) may cut interest rates at its February meeting, especially after recent inflation data showed slowing price growth. Lower inflation has also eased pressure on UK government bond yields, which had been rising due to economic concerns, but the Pound remains under selling pressure amid economic uncertainty.

GBPAUD – D1 Timeframe

The probability of price reacting from an Order Block increases significantly when such an OB occurs immediately after an FVG (Fair Value Gap). Regarding the price action on the daily timeframe chart of GBPAUD, we can see the highlighted demand zone, acknowledging that it occurs right after an FVG area. In addition, the highlighted OB enjoys further confluence from the Fibonacci retracement level and the 200-day moving average.

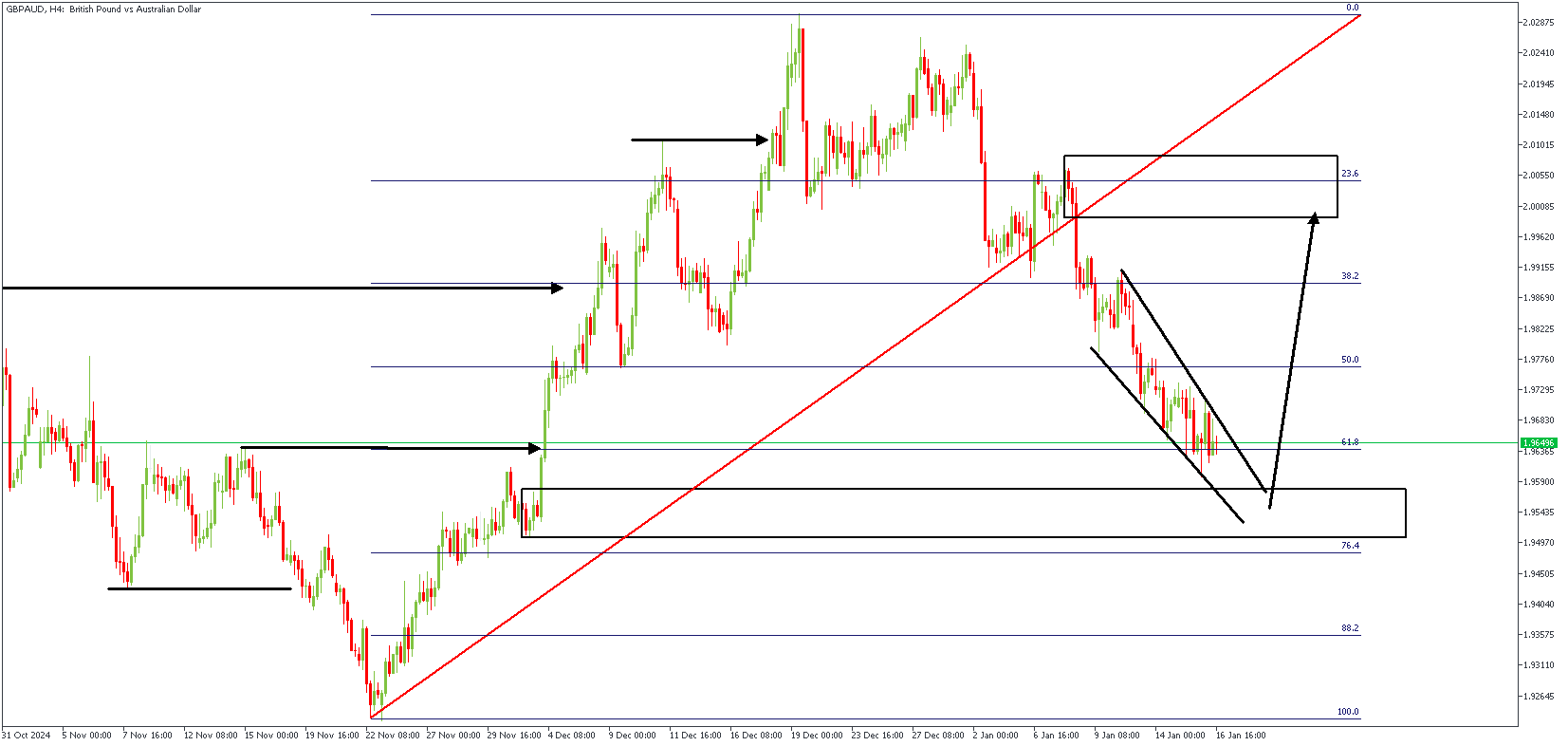

GBPAUD – H4 Timeframe

The 4-hour timeframe chart shows that GBPAUD prices are currently contracting within the boundaries of a descending wedge whilst approaching a key area of demand. Considering this aligns with all the aforementioned confluences, it is easy to conclude with a bullish bounce from the highlighted region.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.99879

- Invalidation: 1.94573

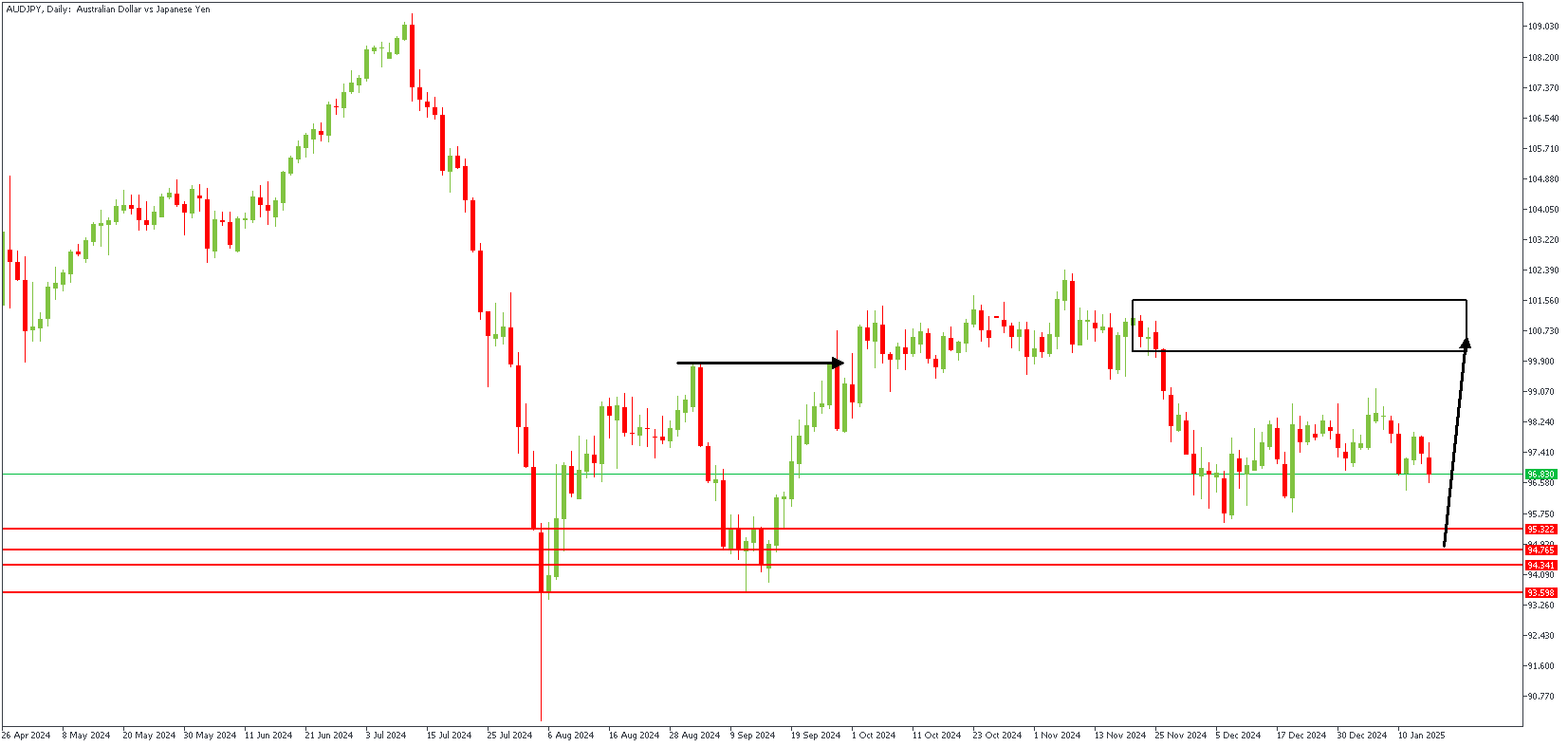

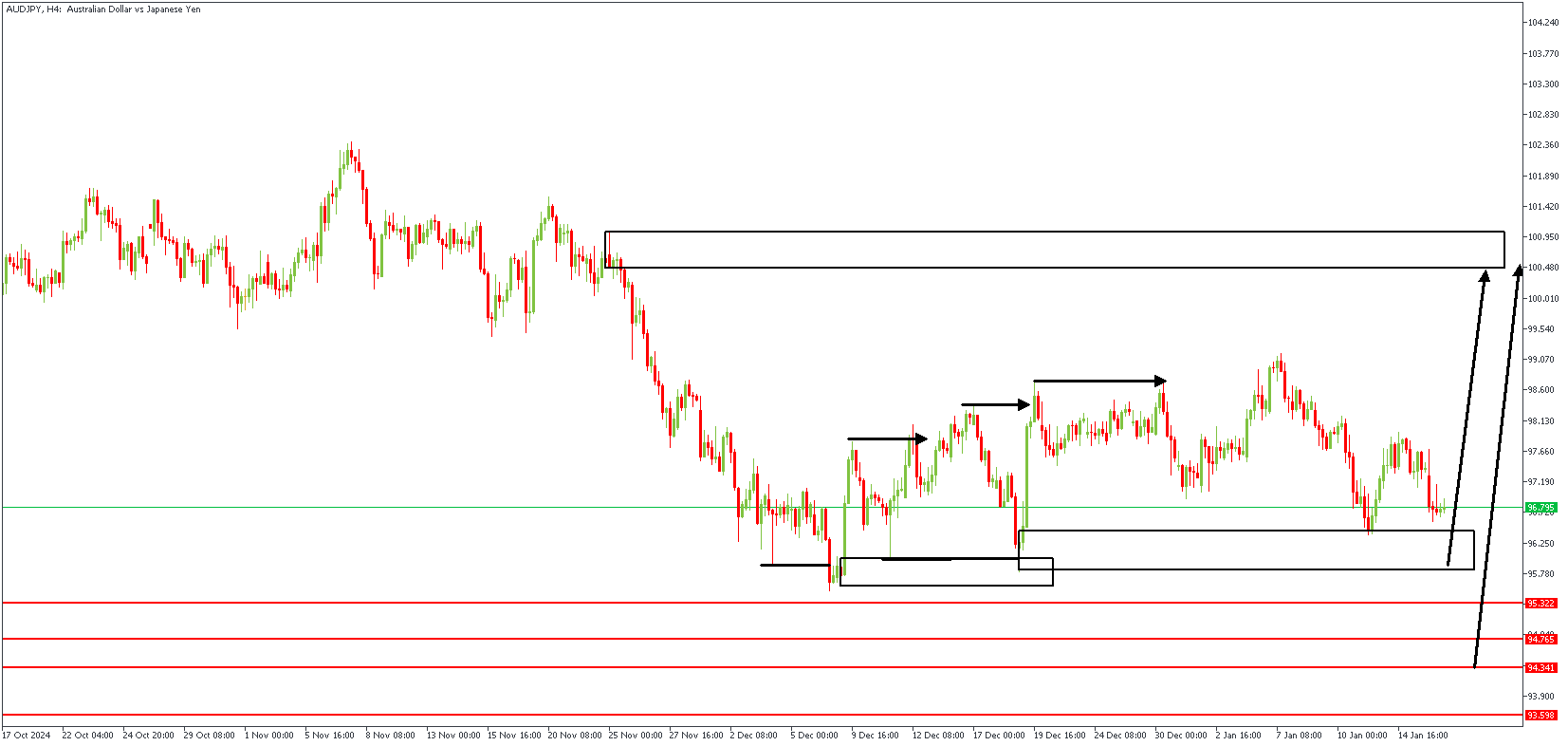

AUDJPY Preps for a Bullish Rally

The Japanese Yen (JPY) strengthened against the US dollar (USD), according to reports that the Bank of Japan (BoJ) is likely to raise interest rates next week as long as there are no significant disruptions with Trump's presidency. Markets are pricing in a 0.2% rate hike for the January 24th meeting, which has boosted confidence in the Yen. Meanwhile, steady US bond yields have also supported Yen's performance.

The British Pound (GBP) weakened after disappointing UK growth data, lowering UK bond yields. In the US, upcoming data releases, including retail sales and housing market updates, are expected to show a solid economy as consumers try to make purchases before potential tariffs are introduced. Later, China will release important economic figures like GDP and retail sales, which could influence global markets.

AUDJPY – D1 Timeframe

At the recent high on the daily timeframe chart of AUDJPY, we see an FVG (Fair Value Gap) with a supply zone behind it. This often attracts price movement, as the FVG usually seeks to be mitigated. On this ground, we can scan the lower timeframe for factors that cause bullish momentum.

AUDJPY – H4 Timeframe

Breaking down the price action on the 4-hour timeframe chart of AUDJPY, we see an SBR pattern emerging from the bearish sweep below the previous low, followed immediately by a bullish break of structure. The rectangular shape highlights the initial entry zone, whilst a secondary entry may present itself at the pivot region marked by the red horizontal lines.

Analyst's Expectations:

- Direction: Bullish

- Target: 100.353

- Invalidation: 93.405

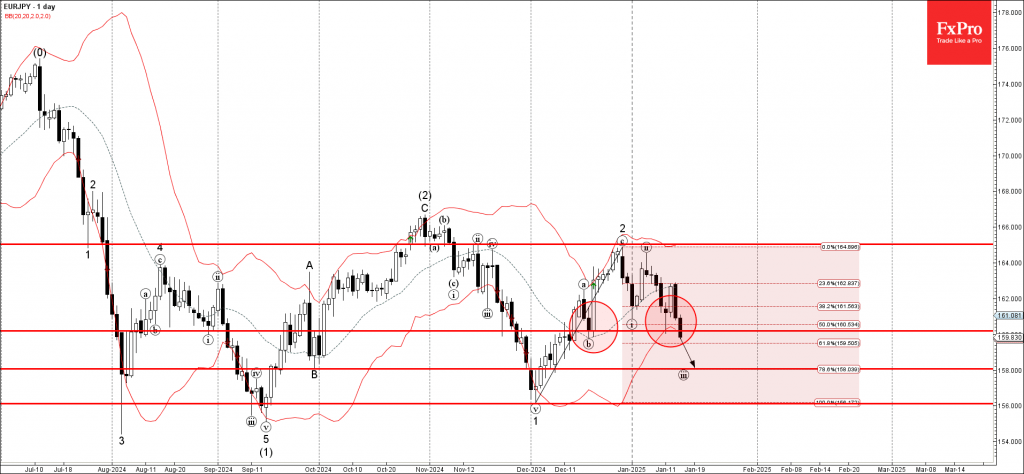

EURJPY Wave Analysis

- EURJPY broke support zone

- Likely to fall to support level 158.00

EURJPY currency pair recently broke the support zone located between the key support level 160.200, (which has been reversing the pair from December) and the 50% Fibonacci correction of the upward ABC correction 2 from last month.

The breakout of this support zone accelerated the active short-term impulse wave iii of the higher impulse waves 3 and (3).

Given the strong bullish yen sentiment, EURJPY currency pair can be expected to fall to the next support level 158.00, the target price for the completion of the active impulse wave iii.

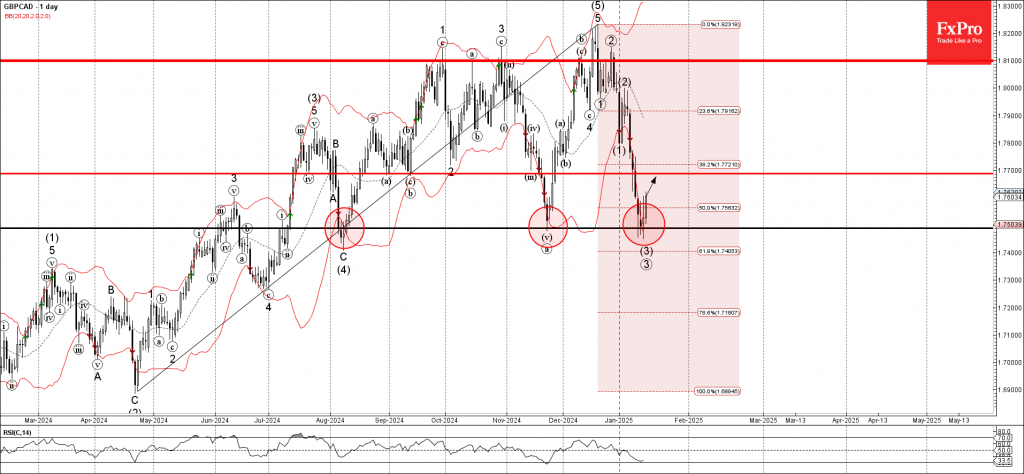

GBPCAD Wave Analysis

- GBPCAD reversed from strong support level 1.7490

- Likely to rise to resistance level 1.7700

GBPCAD currency pair recently reversed up with the daily Japanese candlesticks reversal pattern Hammer from the strong support level 1.7490, which has been steadily reversing this currency pair from the start of August.

The support level 1.7490 was strengthened by the lower daily Bollinger Band and by the 61.8% Fibonacci correction of the upward impulse from last April.

Given the strong daily uptrend, GBPCAD currency pair can be expected to rise to the next resistance level 1.7700.

Fed’s Waller suggests rate cuts possible in H1 if inflation trend holds

Fed Governor Christopher Waller expressed optimism about the US inflation outlook during an interview with CNBC, signaling that rate cuts may be on the table sooner than previously anticipated.

Waller highlighted the positive inflation data released yesterday, describing it as “very good.” He suggested that, if this trend continues, “it’s reasonable to think rate cuts could happen in the first half of the year.”

Waller noted that Fed's median estimate of the neutral policy rate indicates the potential for three or four rate cuts in 2025, contingent on the evolution of economic data.

However, he tempered this with caution, stating, “If the data doesn’t cooperate, then you’re going to be back to two, maybe even one if we just get a lot of sticky inflation.”

On the labor market, Waller described conditions as stable rather than overheated. He pointed out that indicators like hiring rates, quit rates, and wage growth remain restrained, which aligns with Fed's restrictive policy stance.

GBP Struggles Amid Weak Data and BoE Bets

Fundamental Analysis

The British Pound faces bearish pressure against the Dollar and Euro, driven by weak UK economic data and expectations of looser monetary policy from the Bank of England (BoE). UK GDP rose only 0.1% in November, below the 0.2% forecast, while industrial and manufacturing production contracted.

This economic weakness has fueled bets on a 25-basis-point rate cut in February, with up to four cuts expected in 2024, according to a Reuters poll. Meanwhile, UK gilt yields have eased from recent highs, further reducing the Pound's appeal.

Upcoming U.S. employment and retail sales data will play a key role in shaping the Dollar's trajectory, while BoE expectations remain the primary driver for Sterling.

Technical Analysis

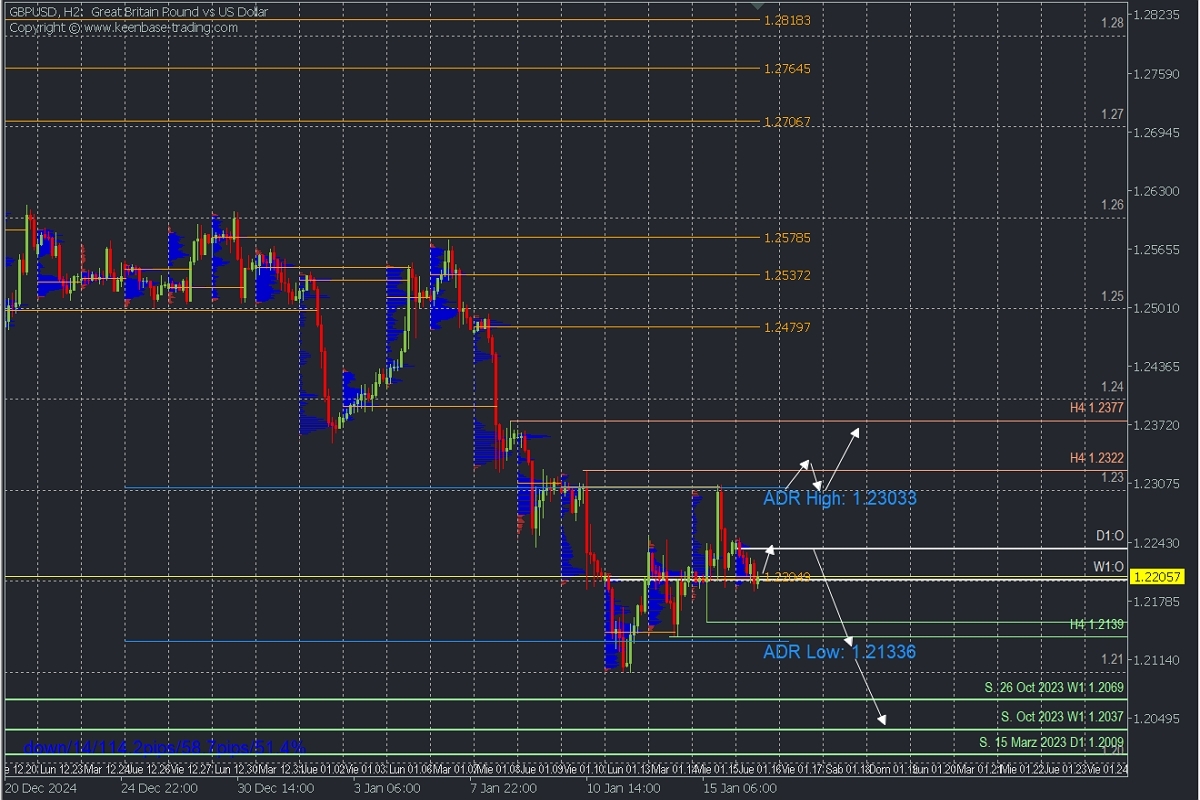

GBPUSD, H2

Supply Zone (Sell): 1.23

Demand Zone (Buy): 1.2140

The intraday bullish correction is consolidating, with volume clustering around 1.22, aligning with yesterday’s POC (Point of Control). This demand zone could support buying toward the daily open at 1.2235, or even attempt a broader rally toward 1.23.

The last validated intraday resistance of the bearish trend is at 1.2322. As long as this level holds, the trend remains intact. A moderate rally below the daily open may pave the way for another drop toward the key correction support at 1.2155, yesterday’s low. A break of this level would signal further downside toward 1.2133, 1.21, and October/March 2023 supports in the coming days.

Technical Summary:

Bearish Scenario: Sell below 1.2235 or earlier at 1.2190, targeting 1.2155, 1.2133, 1.21, and 1.2070 in the short term.

Bullish Scenario: Buy above 1.2245, targeting 1.23, with extended targets at 1.2360 and 1.2370 only after a decisive break above 1.2322.

Always wait for a *Reversal/Exhaustion Pattern (REP) on M5 as taught here https://t.me/spanishfbs/2258 before entering trades in the key zones indicated.

*POC Explained: The Point of Control (POC) is the level or zone with the highest volume concentration. If followed by a bearish move, it acts as a resistance zone. If followed by a bullish move, it acts as a support zone, often near lows.