Sample Category Title

ECB’s Nagel: Should avoid rushing monetary policy normalization

German ECB Governing Council member Joachim Nagel in an interview with Platow Brief, highlighted persistent services inflation and a "high level of uncertainty," referencing concerns about global trade dynamics as Donald Trump prepares to return to the White House next week.

"We should therefore not rush into anything on the path to monetary policy normalization," Nagel stated.

Meanwhile, he defended the ECB’s discussions of a more aggressive 50-basis-point rate cut during its December meeting, noting that such debates are a normal part of policy deliberations.

ECB’s Elderson: Rate setting is a question of speed and magnitude

ECB Executive Board member Frank Elderson emphasized the delicate balance the central bank must strike in setting interest rates during an interview with Het Financieele Dagblad.

He warned, "If we lower the interest rate too quickly, dialling down services inflation sufficiently could become complicated." At the same time, he acknowledged the risks of maintaining rates too high for too long, which could lead to undershooting ECB's inflation target.

"The markets don’t think we’ve finished easing now that we’re at 3% and I don’t think we have, either," he added. "Setting interest rates is ultimately a question of how fast and how much."

Will BoJ Save Yen and Sink GBP/JPY?

- Weak UK retail sales and GDP data has put pressure on the British pound.

- Rumors suggest the Bank of Japan (BoJ) may hike rates next week, which could impact the Yen and GBP/JPY.

- On shorter timeframes (daily and hourly), there’s potential for a bounce and retest of broken trendlines, with resistance levels around 191.50 and 193.00.

The British pound remains under pressure following a surprisingly weak retail sales report this morning. This follows up from a disappointing GDP report for November which fell short of market expectations.

UK retail sales unexpectedly dropped by 0.3% in December 2024, after a small 0.1% rise in November that was revised down. This was worse than the forecasted 0.4% increase. Over the whole of 2024, retail sales grew by 0.7%, recovering from a 2.9% drop in 2023 and a 4.1% fall in 2022.

The data weighed on the pound this morning with GBP/JPY falling some 60-70 pips post data release. However the pair has since recovered the majority of the drop as buying pressure returned.

BOJ To Hike Rates Next Week?

News filtered through via Nikkei this morning that the majority of BoJ board members are set to approve a rate hike next week. Now rhetoric from the BoJ has been notoriously unreliable for the longest time, with the Central Bank using rhetoric and chatter to aid the Yen at times. Could this be another false dawn?

Looking at recent data and comments from BoJ policymakers, it does appear that this might have some substance. Markets are pricing in around an 80% probability of a 25 bps hike next week. As for how this impacts the Yen and GBP/JPY in particular is going to be intriguing.

BoJ Rate Probabilities

Source: LSEG (click to enlarge)

The way GBP/JPY has reacted this morning leaves me to believe that we could be in for a bounce higher ahead of the BoJ meeting next week. The downside is still favored but a short-term pullback may present potential shorts with a better risk to reward opportunity.

Technical Analysis – GBP/JPY

From a technical standpoint, GBP/JPY on a weekly timeframe failed to print a higher high in December which preceded the selloff we have seen since.

GBP/JPY is threatening a break of the ascending trendline on a weekly timeframe with a close below leaving the door open for a deeper correction toward the 100-day MA at 186.239 and potentially the 185.00 handle.

GBP/USD Weekly Chart, January 17, 2025

Source: TradingView.com (click to enlarge)

Dropping down to a daily timeframe and the trendline from the weekly chart has been broken with a daily candle close below yesterday.

There is a possibility of a bounce and retest of the trendline before bearish continuation. Given the rumors about a BoJ rate hike next week, a pullback in the early part of the week toward the 191.50 or 193.00 handle before sellers’ return could materialize.

The RSI period 14 is hovering just above oversold territory though and thus a continuation of the selloff for current price levels cannot be ruled out either.

GBP/JPY Daily Chart, January 17, 2025

Source: TradingView.com (click to enlarge)

Dropping down further to a one-hour timeframe and a one-hour candle close above 190.150 could lead to a rally and retest of the trendline.

On the H1 timeframe the 100-day MA also rests near the trendline at 191.318 and may prove a hurdle too strong to crack. The positive here is that the RSI on the H1 timeframe has broken above the neutral 50 handle, suggesting a shift in momentum from bearish to bullish.

GBP/JPY One-Hour (H1) Chart, January 17, 2025

Source: TradingView.com (click to enlarge)

Support

- 189.349

- 187.628

- 185.000

Resistance

- 190.148

- 191.500

- 193.000

China’s GDP Beats Forecast, Aussie Shrugs

The Australian dollar has edged lower on Friday. In the European session, AUD/USD is trading at 0.6198, down 0.22% at the time of writing.

Will strong China numbers boost the Aussie?

There was good news out of China on Friday, highlighted by GDP which was stronger than expected. The economy expanded by 5.4% y/y in the fourth quarter, up from 4.6% in Q3 and above the market estimate of 5.0%. This was the strongest pace of growth since Q2 2023. Industrial production jumped 6.2% in December, up from 5.4% in November and above the forecast of 5.4%. Finally, retail sales climbed 3.7% in December, compared to 3.0% a month earlier and blowing past the forecast of 3.0%.

The solid numbers out of China are a result of the government’s aggressive stimulus measures to kick-start the economy and no less important, boost business and consumer confidence. One strong month does not mean that China’s economic problems are over but the positive data is clearly a step in the right direction.

China’s exports rose in December jumped 10.7% which was higher than expected. Much of the gain was due to manufacturers rushing to fill orders ahead of Donald Trump taking office next week. Trump has threatened to slap China with tariffs and demonstrated in his first presidential term that he was willing to engage in a nasty trade war with China.

The improvement in China’s economy is good news for Australia, as China is its largest trading partner. China’s bumpy recovery since the Covid pandemic has led to lower demand for imports and Australia’s crucial export sector has felt the pinch. If China has turned the corner, it will be good news for Australian exporters and should provide a boost to the ailing Australian dollar, which has plunged 10.5% against the US dollar since October 1.

AUD/USD Technical

- 0.6217 is a weak line of resistance, followed by resistance at 0.6243

- 0.6188 and 0.6162 are providing support

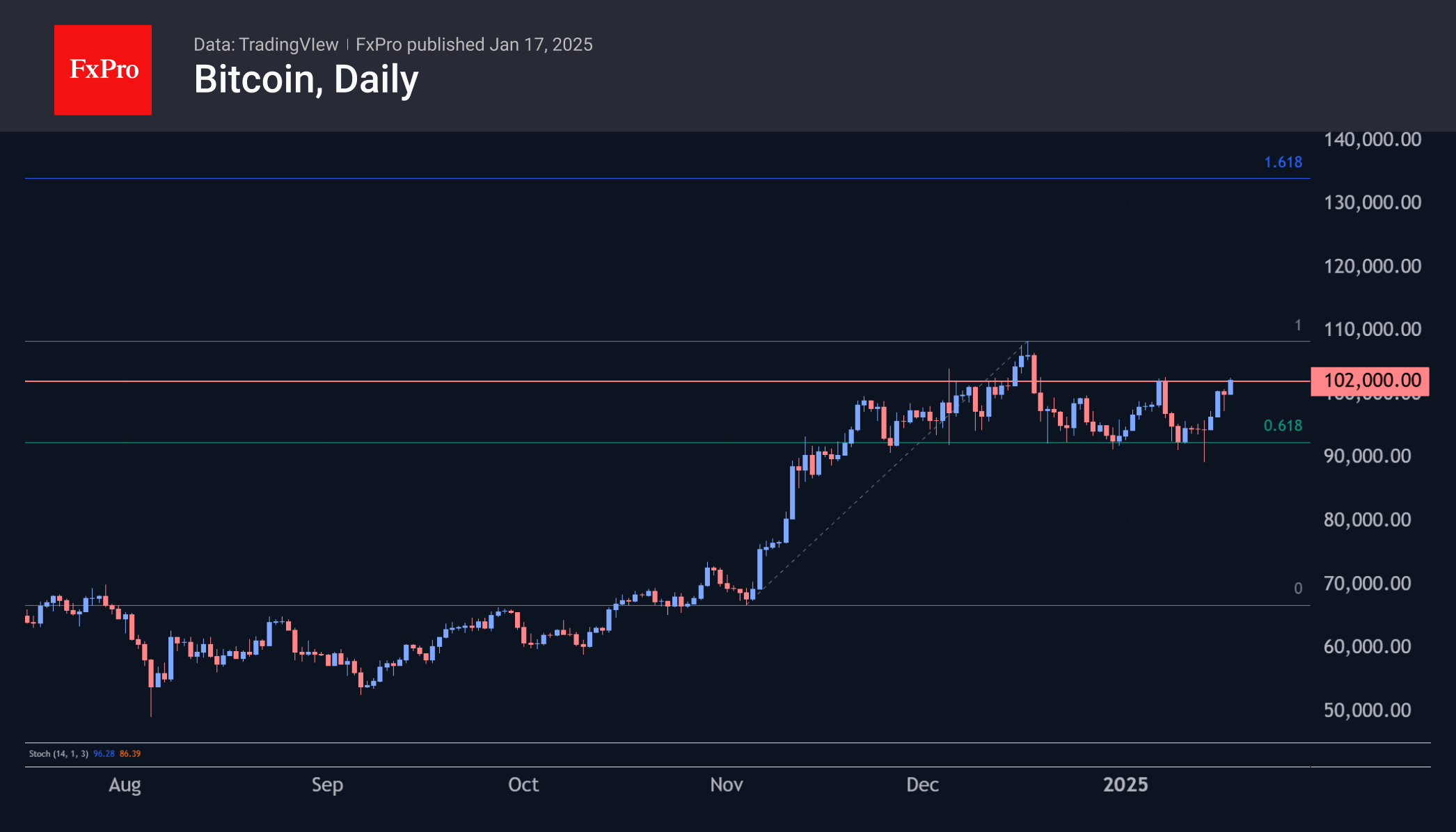

Crypto Market Keeps Its Pace

Market picture

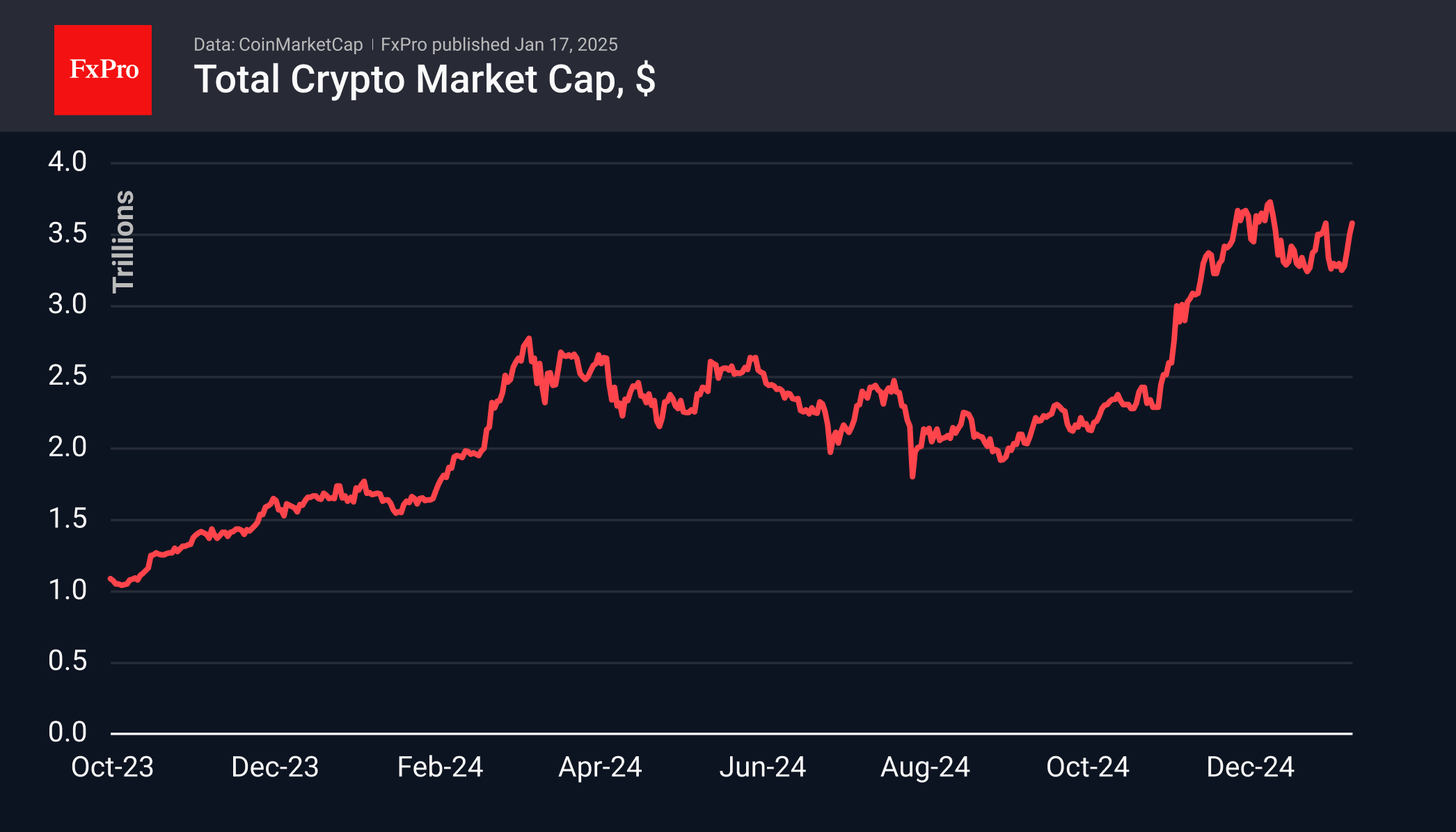

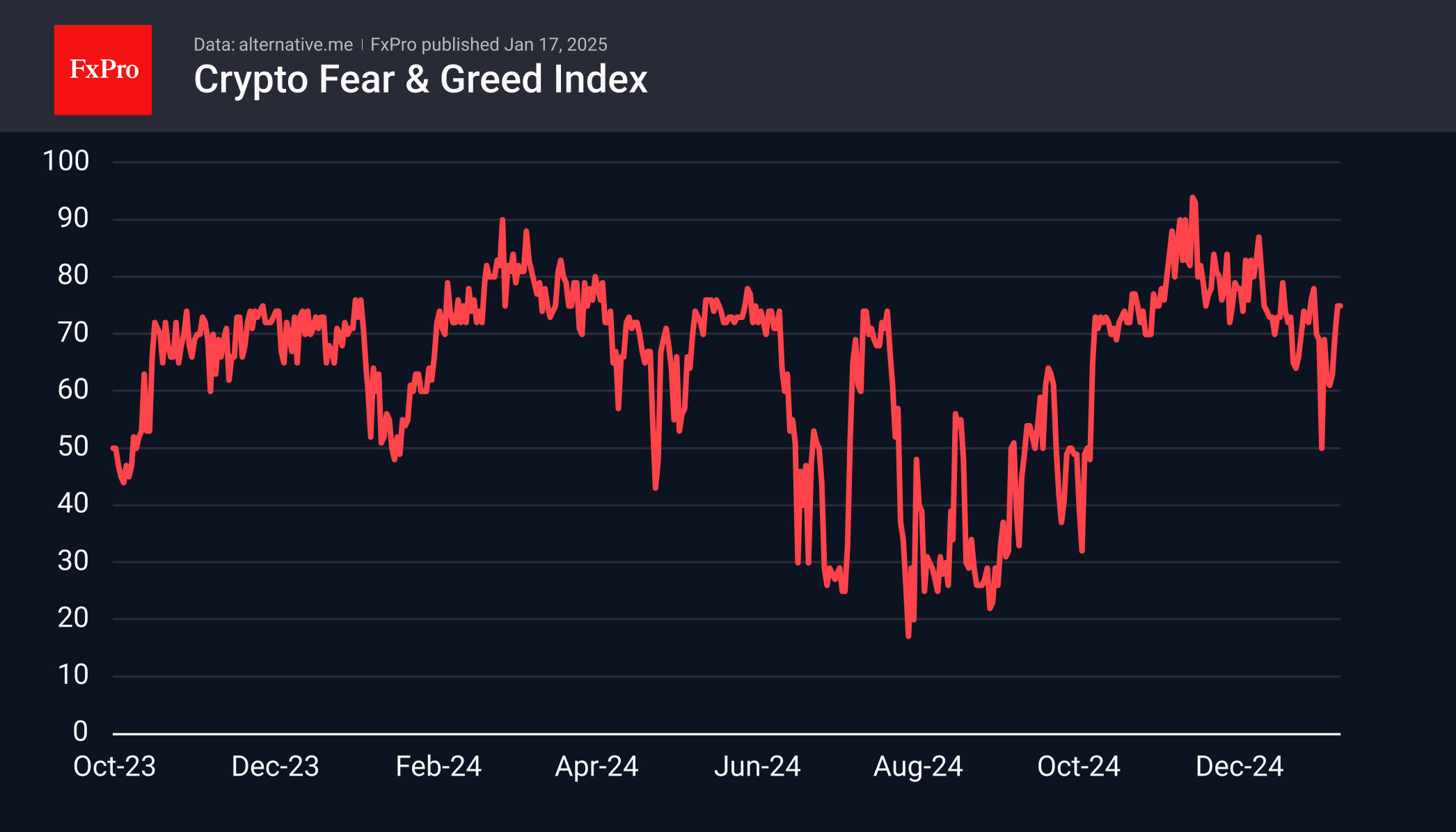

The cryptocurrency market increased by 2.7% in the past 24 hours, reaching $3.6 trillion. It is returning to levels seen on January 7th and has been maintaining steady growth since the beginning of the week. Successful consolidation at these levels could pave the way to historical highs observed in December, effectively ending the period of corrective pullback and consolidation.

Crypto market sentiment remains in the ‘Greed’ territory, with values recording 75 for the second consecutive day. These figures indicate significant buyer interest but are not yet indicative of an overbought market.

Bitcoin’s price has exceeded $102K, entering the range it occupied ten days ago. Similar to the broader market, BTC is on the brink of reaching the December highs. Additionally, overcoming downward momentum intraday on Thursday has demonstrated buyer strength. If risk appetite in equities persists, an advance into the $108K-$110K range could materialize within a few days. Continued upward movement might trigger FOMO, potentially driving the price to $130K by the end of January.

News background

According to Bloomberg analyst Eric Balchunas, a Litecoin-based exchange-traded fund is anticipated to be the next spot cryptocurrency ETF in the U.S., which recently led to a 30% increase in LTC prices. There are currently five applications for Solana-based ETFs and two applications for XRP-based funds pending with the SEC.

Investment firm VanEck has applied to the SEC to launch an exchange-traded fund named Onchain Economy ETF. The fund will target companies involved in digital transformation and/or digital asset-based instruments.

Caution prevails in the BTC options market, as bets on increased volatility intensify with the approach of Donald Trump’s inauguration as U.S. President on January 20th, The Block reports.

New York-based Burwick Law has announced plans to sue the Pump.fun platform on behalf of meme-coin investors who have incurred substantial losses.

Scam Sniffer warns that Telegram malware scams targeting crypto investors have now outpaced traditional phishing attacks. Since November, the number of fraudulent incidents on Telegram has surged 20-fold.

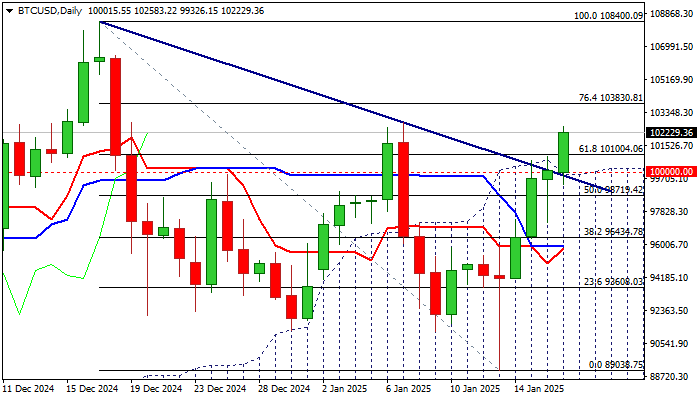

Bitcoin Establishes Above 100K as Markets Expect Fast Action from Trump’s Pro-crypto Administration

BTCUSD continues to trend higher for the fourth consecutive day and is on track to register a firm break above 100K level (psychological barrier reinforced by daily Ichimoku cloud top and bear trendline off new record high).

Fresh strength reflects overall bullish sentiment, which is primarily fueled by expectations that pro-crypto Trump’s administration may start easing current crypto market regulations and possibly declare a Bitcoin Reserve in the first days of the term.

Recent crack of strong 90K support zone raised fears among traders, but dip proved to be short-lived and strong bids at this area quickly lifted the price out of bearish formation and generated positive signal on formation of bear-trap pattern on daily chart.

Converging daily Tenkan/Kijun-sen are about to form a bull-cross, which will further strengthen near-term structure, as the price is likely to register a weekly close above 100K (for the first time in five weeks) and eyeing next targets at 102770 (Jan 7 lower top) and 103830 (Fibo 76.4% of 108400/89038).

Large weekly bullish candle with long tail contributes to positive signals as BTCUSD retraced over 61.8% of 108400/89038 pullback during this week.

As mentioned in the previous report, the rise in bitcoin’s price will be directly proportional to the pace of Trump’s action in the crypto market.

Bitcoin may retest the all-time high (108400) if things go in line with expectations but may accelerate further on potential euphoria in the market if the administration gives top priority to their task in crypto’s.

Break of 108400 pivot to expose psychological 110K barrier, violation of which to open way towards 120K, with a number of Fibo projections seen as intermediary barriers (111260, 113260; 116500).

Broken Fibo 61.8% (101000) marks initial support, with potential extended dips (daily studies are overbought) expected to hold above 100K and keep near term bulls in play.

Res: 102770; 103830; 104030; 106520

Sup: 101000; 100000; 99326; 98719

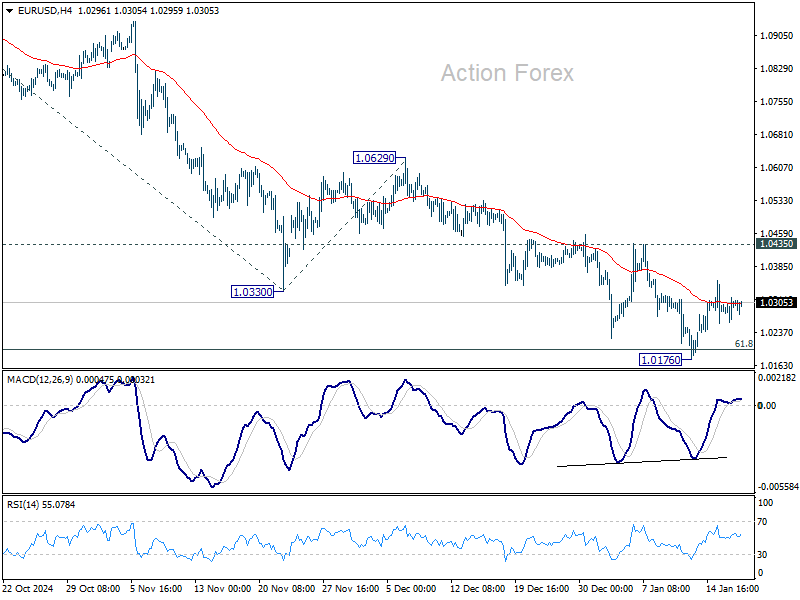

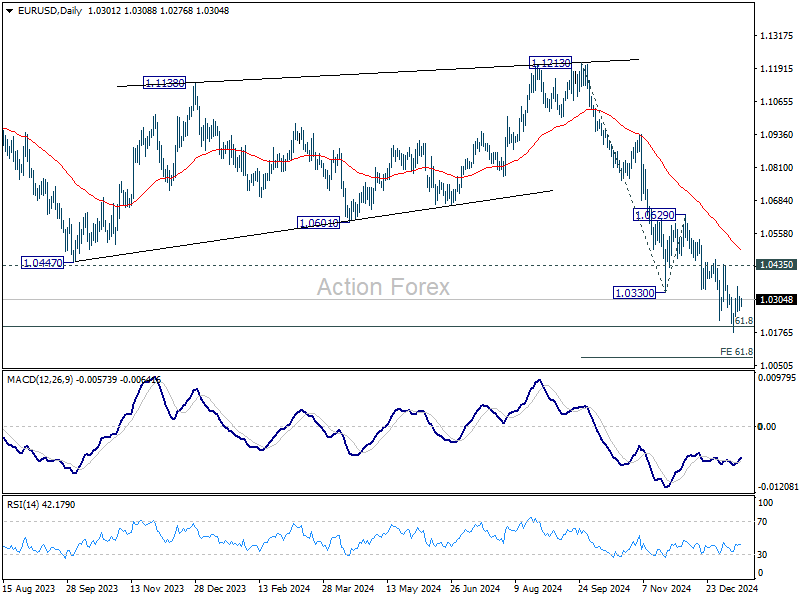

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0270; (P) 1.0293; (R1) 1.0324; More...

EUR/USD is staying in consolidation above 1.0176 and intraday bias stays neutral. With 1.0435 resistance intact, outlook remains bearish and further decline is expected. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, considering bullish convergence condition in 4H MACD, firm break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

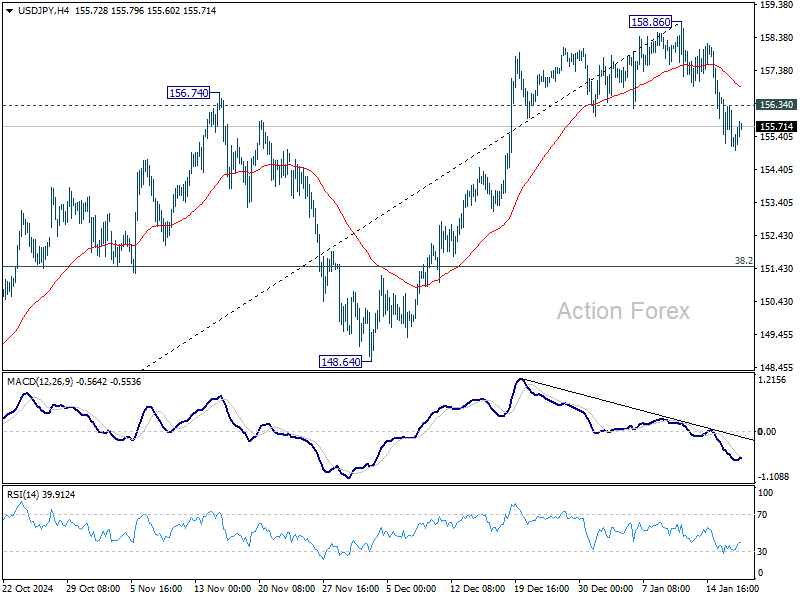

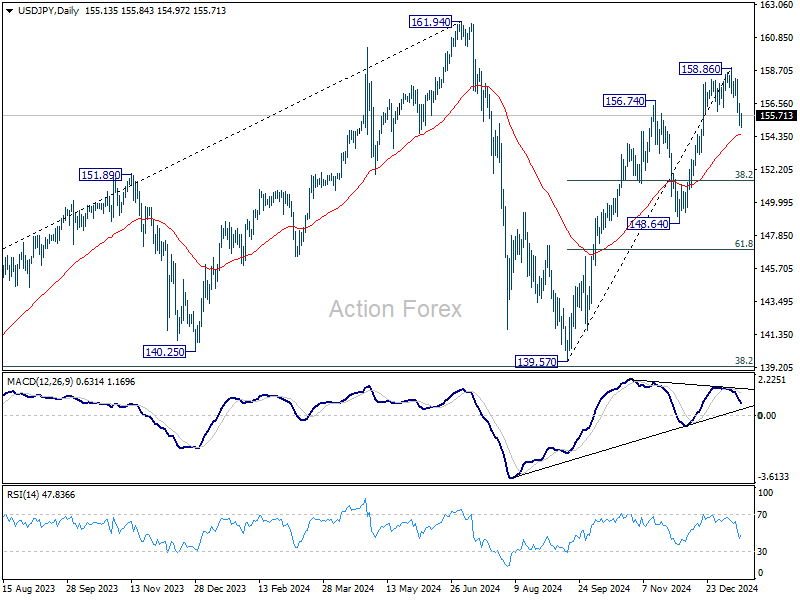

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.59; (P) 155.63; (R1) 156.15; More...

USD/JPY's fall from 158.86 short term top is in progress and intraday bias stays on the downside for 55 D EMA (now at 154.51). Firm break there will target 38.2% retracement of 139.57 to 158.86 at 151.49 next. On the upside, above 156.34 minor resistance will turn intraday bias neutral again first. But risk will stay on the downside as long as 158.86 resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

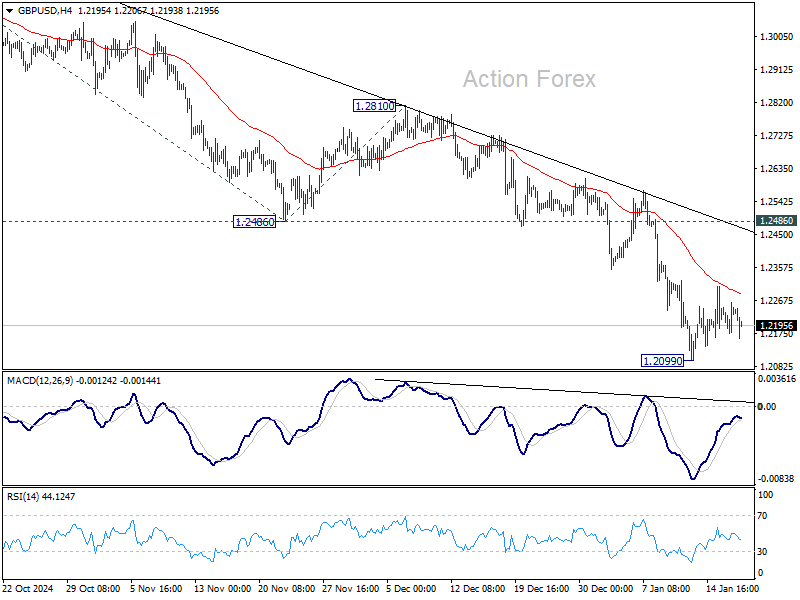

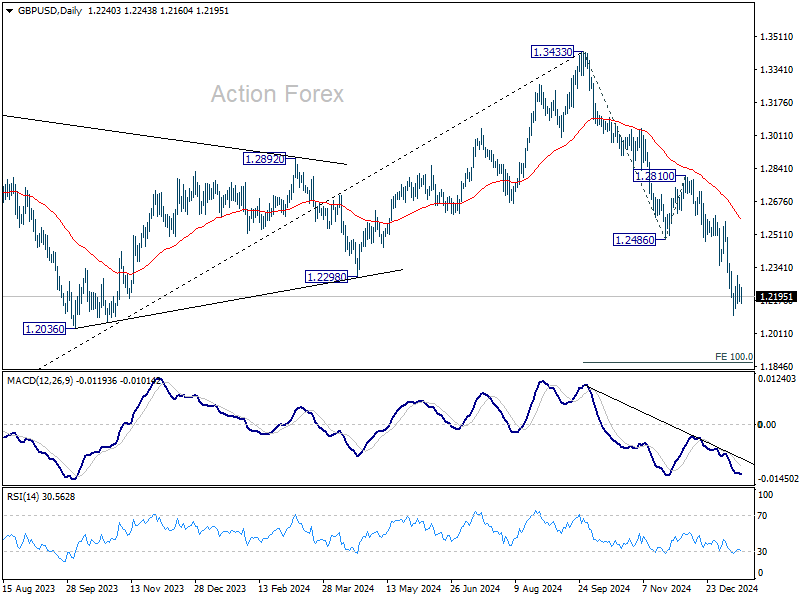

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2188; (P) 1.2225; (R1) 1.2274; More...

Intraday bias in GBP/USD remains neutral as consolidation continues above 1.2099. Outlook remains bearish with 1.2486 support turned resistance intact. Larger fall from 1.3433 is still expected to continue. On the downside, break of 1.2099 will resume the decline to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

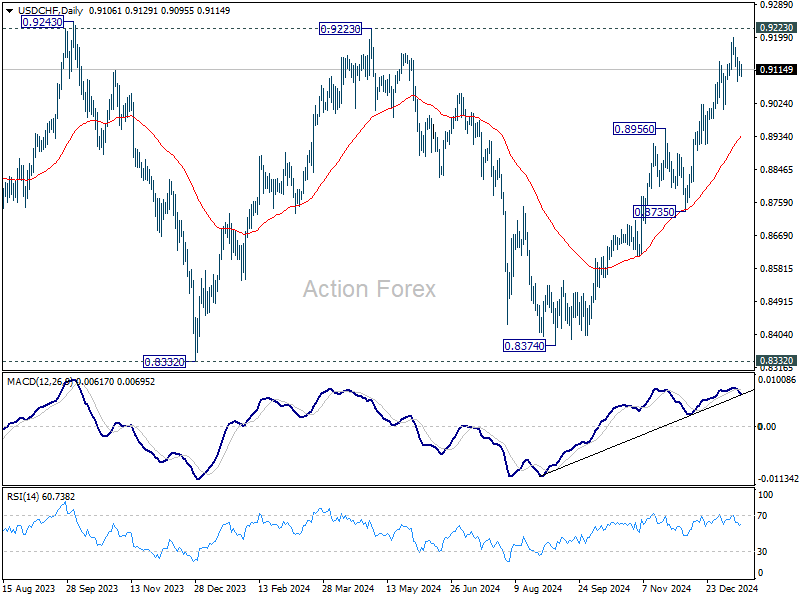

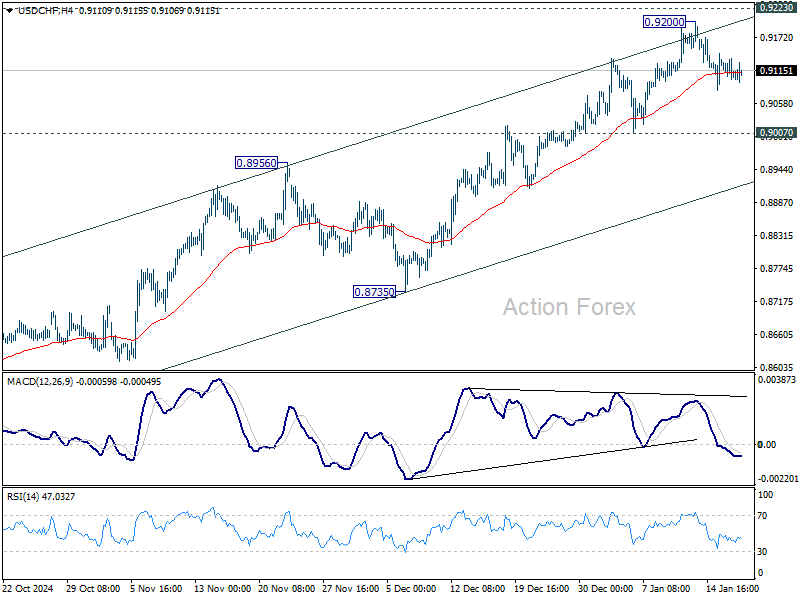

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9092; (P) 0.9116; (R1) 0.9132; More…

USD/CHF is staying in consolidation below 0.9200 and intraday bias remains neutral. As long as 0.9007 support holds, near term outlook remains bullish. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.8936).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.