Sample Category Title

WTI Oil Futures Neutral Near-Term, Downside Risk Below Cloud

WTI oil futures have been rising steadily and making a recovery following a big drop yesterday. On the 4-hour chart, MACD is trading in a bullish direction and has broken above zero while RSI is also rising and attempting to break above 50 into bullish territory.

The move to the upside has encountered resistance provided by the 50-period moving average and also by the 38.2% Fibonacci retracement (47.87) of the decline from 50.19 to 46.43. Immediate support is at the 20-period MA at 47.62. A break of this support area would likely see an acceleration of a fall towards 46.90 (August 18 low) ahead of 46.43 (August 17 low). From here, there would be a resumption of the downtrend that started from the 50.00 region.

For now there is no clear trend for the short-term and the bias is expected to stay neutral between the 20 and 50-period MA. Only a move above 48.85 would weaken downside risk and bring the market above the Ichimoku cloud. The next target would be the key 50.00 level. This is a strong resistance area and a break above it would indicate a shift to a bullish bias.

USD/CAD: Wholesale Sales

The weaker-than-expected report on Canadian wholesale sales was followed by a modest reaction in the market. The Loonie gained against the US Dollar only 4 base points to reach the 1.2582 mark and continue downmove in the Tuesday's morning session.

Statistics Canada reported that the country's wholesale sales fell 0.5%over the course of June, missing expectations for a 0.6% gain after an upwardly revised 1.0% rise in the prior month. Analysts suggested the weak report was unlikely to cause concerns, as only one monthly decline was registered. However, both retail and wholesale sales revealed generally strong growth momentum in previous months, which allowed the Bank of Canada to remain confident about the near-term outlook.

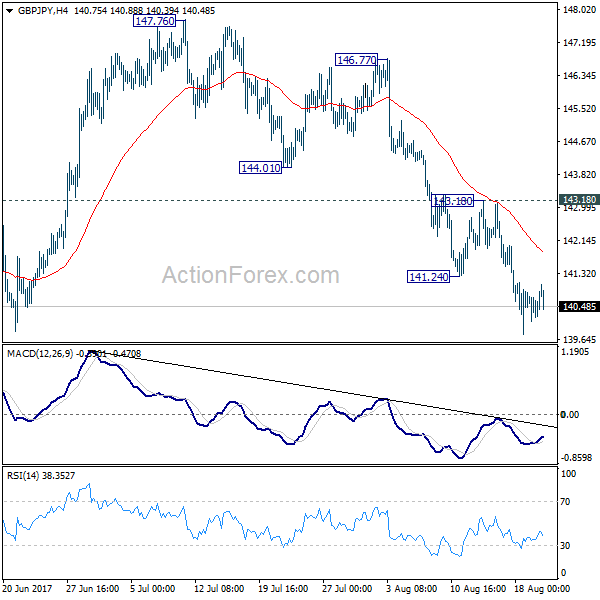

GBP/JPY Daily Outlook

Daily Pivots: (S1) 140.14; (P) 140.49; (R1) 140.89; More

With 143.18 minor resistance intact, fall from 147.76 is still progress for 138.65 support first. Break there will extend the decline to 135.58 key support level. At this point, price actions from 148.42 are seen as a sideway consolidation pattern. Hence, we'll expect strong support from 135.58 to contain downside and bring rebound. Nonetheless, break of 143.18 resistance is needed to indicate short term bottoming first. Otherwise, near term outlook will remain bearish in case of recovery.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. We'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

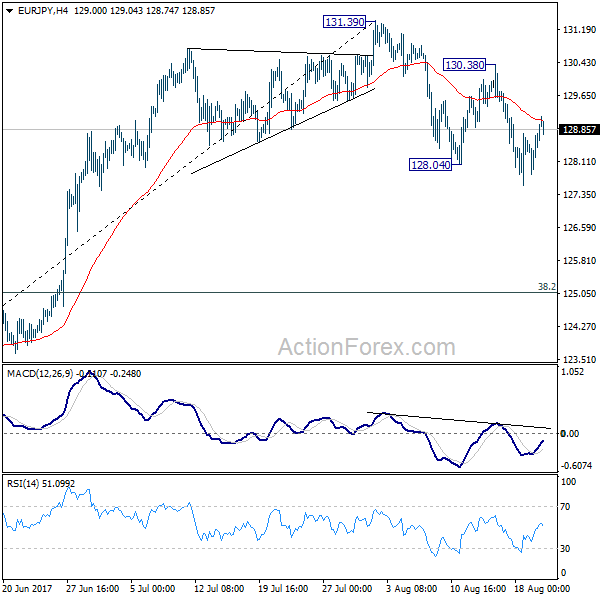

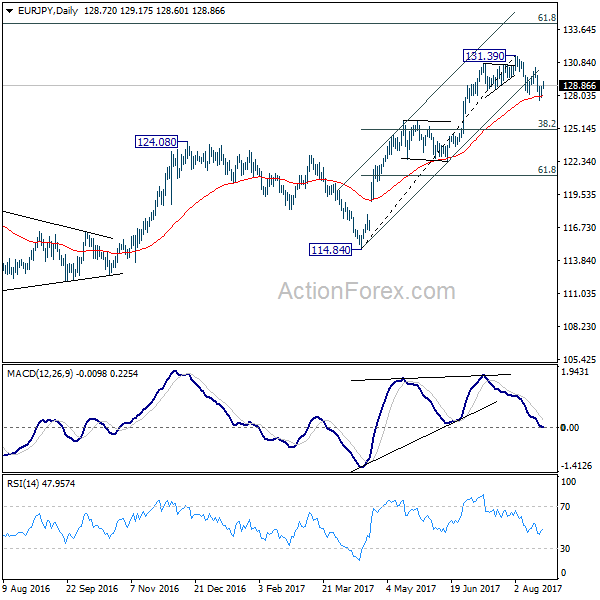

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.11; (P) 128.44; (R1) 129.06; More...

No change in EUR/JPY's outlook as fall from 131.39 is still in progress. Such decline is seen as correcting whole rise from 141.84 with break of channel support. Deeper decline would be seen to 38.2% retracement of 114.84 to 131.39 at 125.05 before completion. On the upside, break of 130.38 resistance is needed to confirm completion of the pull back. Otherwise, deeper decline is expected even in case of recovery.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds. However, firm break of 124.08 will argue that rise from 109.03 is completed and turn outlook bearish.

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 16 Jan 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 18 Apr 2017

• Trend bias: Near term up

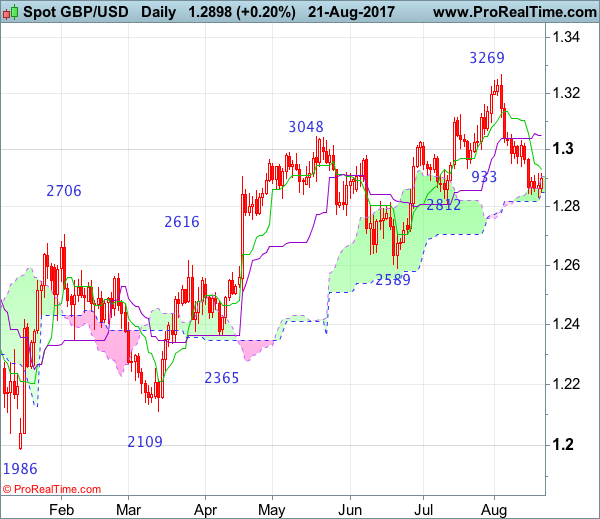

GBP/USD – 1.2857

Cable has remained under pressure after recent selloff below indicated support at 1.2933, adding credence to our view that a temporary top has been formed earlier at 1.3269 and further consolidation below this level would take place with mild downside bias for at least a strong retracement of recent upmove to support at 1.2812, then 1.2775-80 (38.2% Fibonacci retracement of 1.1986-1.3269), however, near term oversold condition should prevent sharp fall below 1.2700 and reckon 1.2620-30 (50% Fibonacci retracement) would hold from here and price should stay above previous chart support at 1.2589.

On the upside, whilst initial recovery to 1.2932-33 (current level of the Tenkan-Sen and previous support turned resistance) cannot be ruled out, reckon upside would be limited to 1.2970-80 and resistance at 1.3032 should remain intact, bring another decline later. A daily close above said resistance at 1.3032 would would defer and suggest first leg of decline from 1.3269 has ended instead, risk a stronger rebound to 1.3100 and then 1.3150 but still reckon upside would be limited to 1.3200, bring another leg of corrective decline later. A daily close above 1.3200 would risk another test of said resistance at 1.3269 but break there is needed to confirm recent upmove has resumed and extend gain to 1.3300-10, having said that, loss of upward momentum should prevent sharp move beyond resistance at 1.3425 and price should falter well below 1.3500-05 (50% Fibonacci retracement of 1.5018-1.1986).

Recommendation: Sell at 1.3050 for 1.2850 with stop above 1.3150.

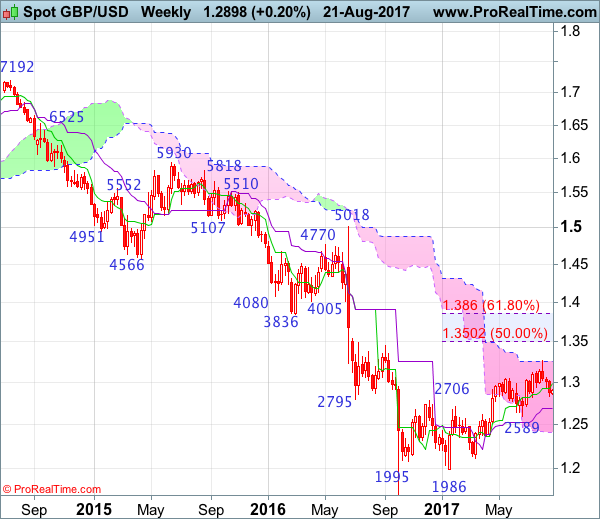

On the weekly chart, cable’s retreat from 1.3269 (with a shooting star) has kept price under pressure, adding credence to our view that a temporary top is possibly formed there and consolidation with mild downside bias is seen for test of 1.2812 support, break there would extend weakness to 1.2775-80 (38.2% Fibonacci retracement of 1.1986-1.3269), then towards 1.2705-10, however, reckon downside would be limited to the Kijun-Sen (now at 1.2689) and previous support at 1.2589 should hold from here. Looking ahead, only a sustained breach below 1.2589 would signal the entire correction from 1.1986 has ended at 1.3269, bring further decline to 1.2500, then towards support at 1.2365.

On the upside, expect recovery to be limited to 1.2930-40 and 1.2980 should hold, bring another decline. Above 1.3032 would defer and suggest the retreat from 1.3269 has ended, risk a strong rebound to 1.3100 but upside should be capped at resistance at 1.3165, bring another decline. Break of 1.3165 resistance would defer and risk retest of 1.3269 but only break there would shift risk back to upside and extend the erratic rise from 1.1986 low for retracement of early downtrend to 1.3300-10 and 1.3350-60, however, upside should be limited to previous resistance at 1.3425 and reckon 1.3500-05 (50% Fibonacci retracement of 1.5018-1.1986) would hold, price should falter below 1.3670-75, bring another decline in Q4.

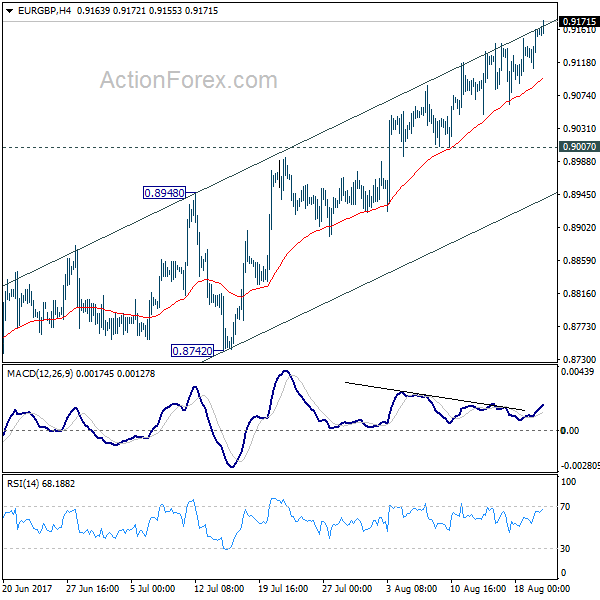

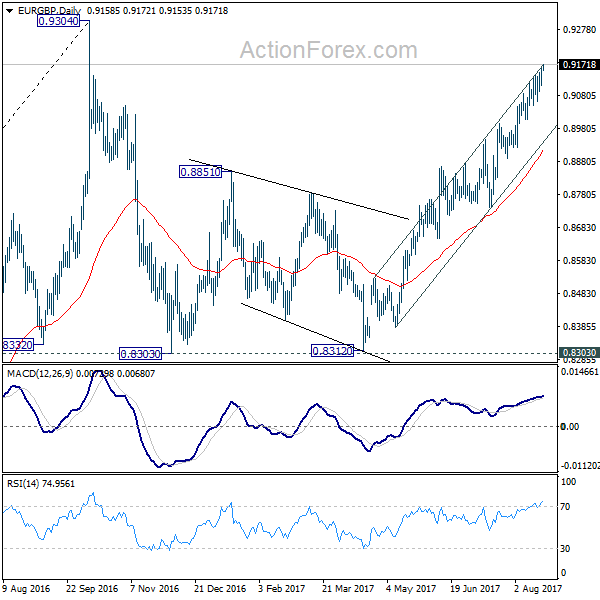

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9126; (P) 0.9144; (R1) 0.9176; More

No change in EUR/GBP's outlook and current rise is in progress for 0.9304 high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. On the downside, break of 0.9007 support will indicate short term topping. Intraday bias will then be turned back to the downside for 0.8742/8948 support zone.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

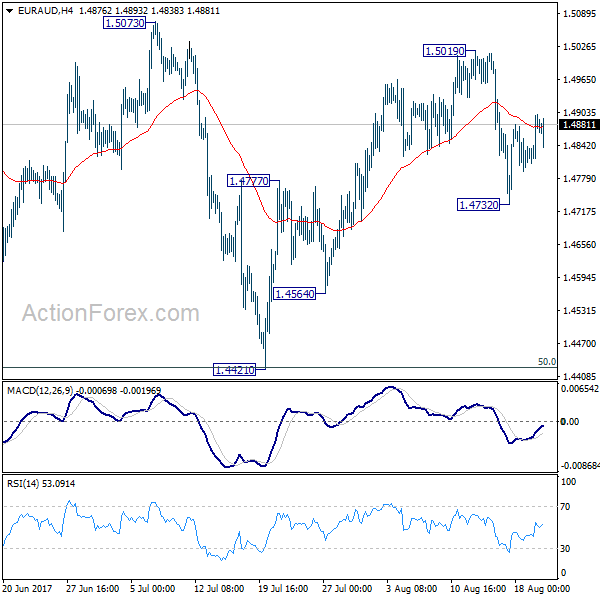

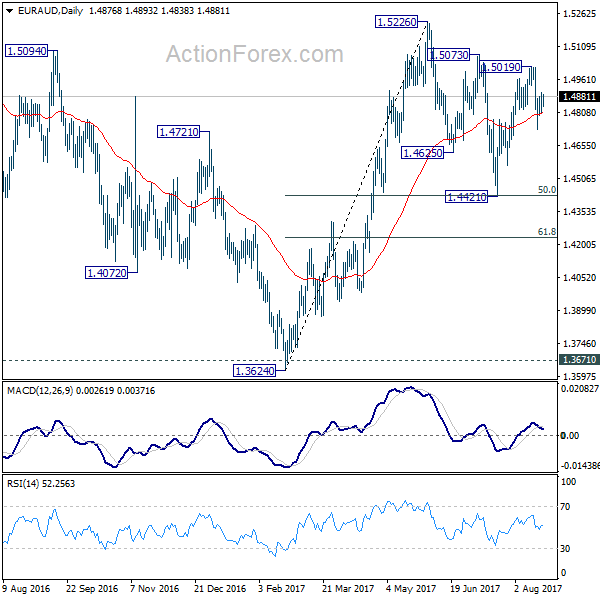

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4824; (P) 1.4862; (R1) 1.4915; More...

Intraday bias in EUR/AUD remains neutral for the moment. Consolidation pattern from 1.5226 is possibly still in progress. Below 1.4732 will bring another fall. But we'd expect 1.4421 cluster support (50% retracement of 1.3624 to 1.5226 at 1.4427) to hold and bring rebound. On the upside, above 1.5019 will target a test on 1.5226 high instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Technical Outlook: Cable – Fresh Weakness Pressures Daily Cloud Base

Cable was lower in Asian session after daily cloud top capped upside attempts and fresh strength of the US dollar increased pressure on Sterling. Fresh weakness is eyeing key supports at 1.2851/48 (daily cloud base/Fibo 61.8% of 1.2588/1.3268 rally), break of which is expected to generate stronger bearish signal for resumption of broader downtrend from 1.3268 (03 Aug peak) which has been paused for 1.2917/1.2831 consolidation in recent days.

Res: 1.2877, 1.2908, 1.2917, 1.2928

Sup: 1.2850, 1.2831, 1.2811, 1.2749

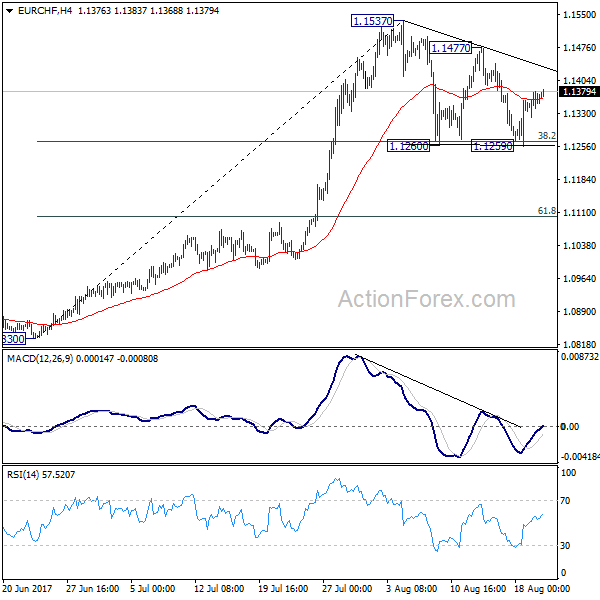

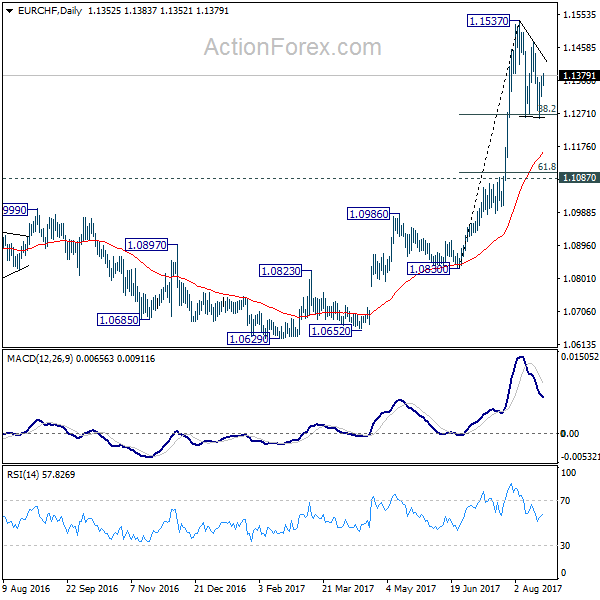

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1330; (P) 1.1354; (R1) 1.1387; More...

EUR/CHF is staying in consolidation pattern from 1.1537 and intraday bias remains neutral. On the upside, break of 1.1477 resistance will argue that the consolidation from 1.1537 has completed and larger rise is resuming. However, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

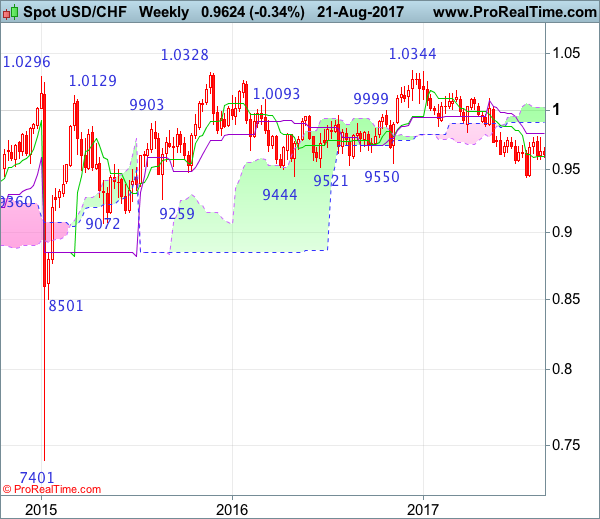

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

USD/CHF – 0.9650

Despite last week’s initial rise to 0.9766, as the greenback has retreated again after faltering below recent high at 0.9773, suggesting the rise from 0.9438 low is not ready to resume yet and further consolidation would be seen, hence weakness to 0.9583 support cannot be ruled out, however, if our view that low has been formed at 0.9438 is correct, downside should be limited to 0.9540-50 and bring another rebound later. Above 0.9700 would bring another test of 0.9773 but only break there would revive bullishness and extend the rise form 0.9438 low to resistance at 0.9808. Looking ahead, a break above this level is needed to retain bullishness and encourage for subsequent rise to 0.9845-50 (61.8% Fibonacci retracement of 1.0100-0.9438).

On the downside, whilst initial pullback to 0.9583 cannot be ruled out, reckon downside would be limited to 0.9540-50 and bring another rebound later. Only a daily close below support at 0.9490 would abort and signal the rebound from 0.9438 has ended instead, risk retest of this level, once this support is penetrated, this would indicate recent decline from 1.0344 (2016 high) has resumed and extend weakness to 0.9390-00, then towards 0.9330-40.

Recommendation: Long entered at 0.9600 stopped profit at 0.9640 and would stand aside for this week.

On the weekly chart, dollar’s retreat after faltering below resistance at 0.9773 formed a candlestick with a long upper shadow, suggesting further consolidation below 0.9773 would be seen and although weakness to 0.9583 and possibly 0.9540-50 cannot be ruled out, as long as said support at 0.9438 holds, prospect of another rebound remains, above 0.9773 resistance would add credence to our view that a temporary low is possibly formed at 0.9438 last month, bring retracement of recent selloff to 0.9805-08 (current level of the Kijun-Sen and previous resistance), above there would provide confirmation, bring subsequent gain to 0.9845-50 (61.8% Fibonacci retracement of 1.0100-0.9438) and possibly test of the lower Kumo (now at 0.9894) but price should falter below psychological resistance at 1.0000, bring another decline later.

On the downside, expect pullback to be limited to 0.9583 and 0.9540-50 should attract buying interest, bring another rise later. Only a drop below support at 0.9490 would abort and suggest the rebound from 0.9438 has ended, bring retest of this level later. Once this recent low is penetrated, this would signal the decline from 1.0344 (2016 high) is still in progress and may extend weakness to 0.9350, then towards 0.9290-00, however, loss of near term downward momentum should prevent sharp fall below 0.9250 and reckon 0.9200-10 would hold from here, risk from there has increased for a rebound later.