Sample Category Title

Trade Idea: EUR/GBP – Buy at 0.9000

EUR/GBP - 0.9129

Original strategy :

Buy at 0.9000, Target: 0.9130, Stop: 0.8960

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9000, Target: 0.9130, Stop: 0.8960

Position : -

Target : -

Stop : -

As the single currency has maintained a firm undertone, suggesting recent upmove is still in progress and bullishness remains for further gain to 0.9160, however, weakening of near term upward momentum should prevent sharp move beyond 0.9180-85 and price should falter below 0.9200, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy euro on subsequent pullback as 0.9000-05 would limit downside. Below 0.8960-70 would defer and suggest a temporary top is possibly formed, bring correction to 0.8922 support which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Hold short entered at 1.2690

USD/CAD - 1.2599

Trend: Down

Original strategy :

Sold at 1.2690, Target: 1.2490, Stop: 1.2750

Position: - Short at 1.2690

Target: - 1.2490

Stop: - 1.2750

New strategy :

Hold short entered at 1.2690, Target: 1.2490, Stop: 1.2700

Position: - Short at 1.2690

Target: - 1.2490

Stop:- 1.2700

As the greenback met renewed selling interest at 1.2691 and has retreated as suggested (we recommended to sell at 1.2690 and a short position was entered), suggesting the decline from 1.2778 top is still in progress for retracement of recent rise, hence weakness to 1.2540-50 would be seen, however, a sustained breach below there is needed to signal the wave iv correction from 1.2414 (wave iii trough) has ended at 1.2778, brig further fall to 1.2490-00 but support at 1.2451 should hold on first testing. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii possibly ended at 1.2414, hence wave iv correction is underway.

In view of this, we are holding on to our short position entered at 1.2690. Above 1.2700 would risk a stronger rebound to 1.2740-50, however, said resistance at 1.2778 should hold. Only break of said resistance at 1.2778 would abort and signal the rebound from 1.2414 is still in progress for retracement of recent decline to 1.2825-30 but still reckon upside would be limited to 1.2880-85 (50% Fibonacci retracement of wave iii) and price should falter well below 1.2990-95 (61.8% Fibonacci retracement), bring retreat later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

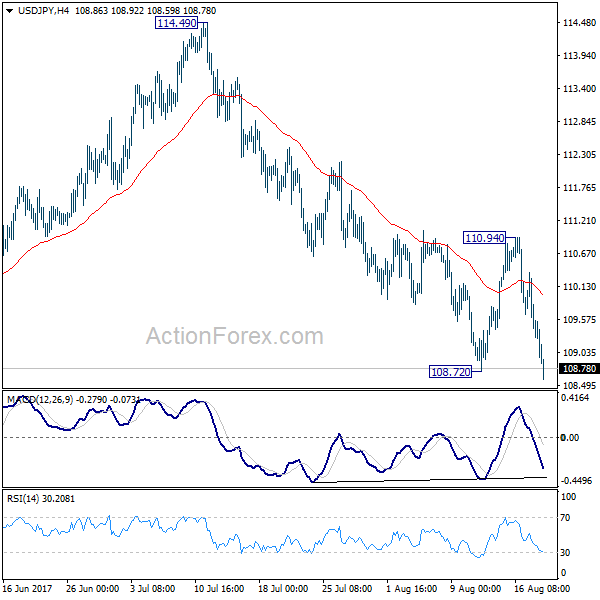

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.21; (P) 109.79; (R1) 110.13; More...

USD/JPY's fall continues today and breaks 108.72 support. The development argues that whole decline from 118. 65 is resuming. Intraday bias stays on the downside for 108.12 first, and then next medium term fibonacci level at 106.48.On the upside, break of 110.94 is needed to indicate short term bottoming. Otherwise, outlook remains bearish in case of recovery.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

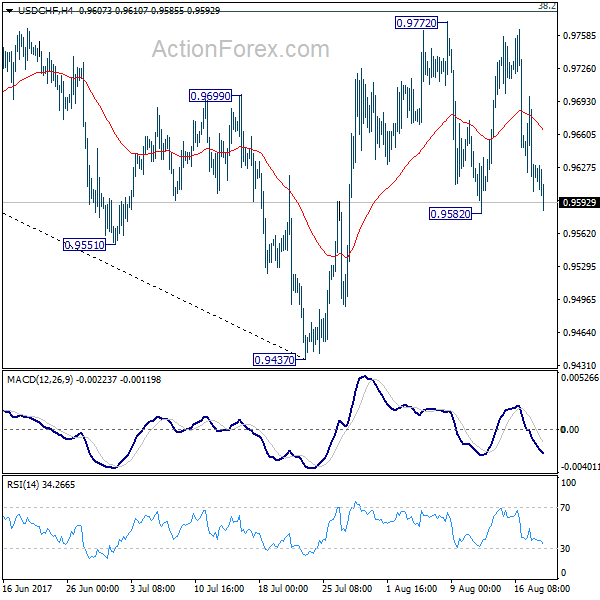

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9590; (P) 0.9644; (R1) 0.9683; More...

USD/CHF is still staying in range of 0.9582/9772 and intraday bias remains neutral for the moment. On the upside, decisive break of 0.9772 resistance will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9862) next. Meanwhile, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

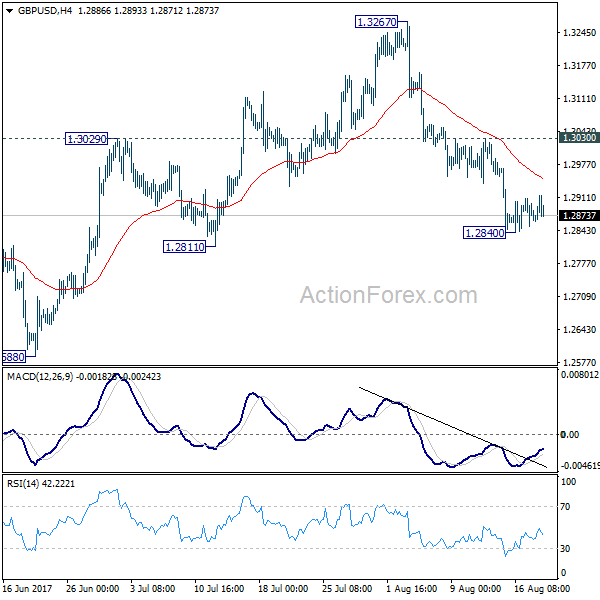

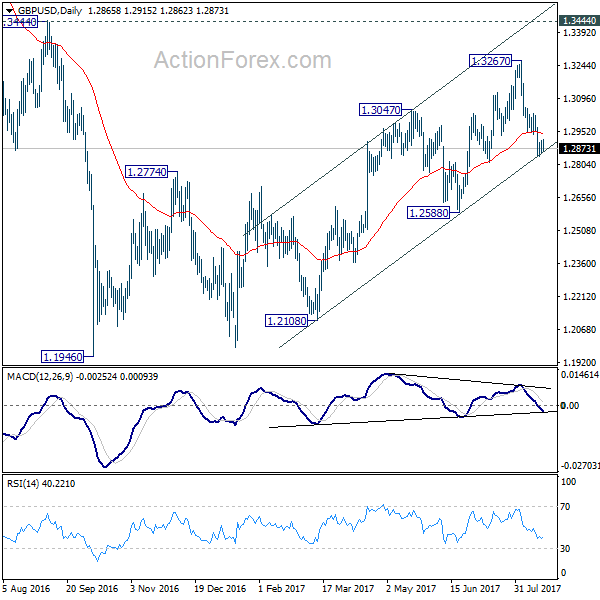

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2843; (P) 1.2876; (R1) 1.2899; More...

The consolidation from 1.2840 temporary low is still in progress and intraday bias remains neutral first. Outlook will stay bearish as long as 1.3030 resistance holds. We're preferring the case that correction from 1.1946 is completed at 1.3267. Below 1.2840 will target 1.2588 key support to confirm our bearish view. Nonetheless, break of 1.3030 will dampen our view and turn bias back to the upside for retesting 1.3267.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

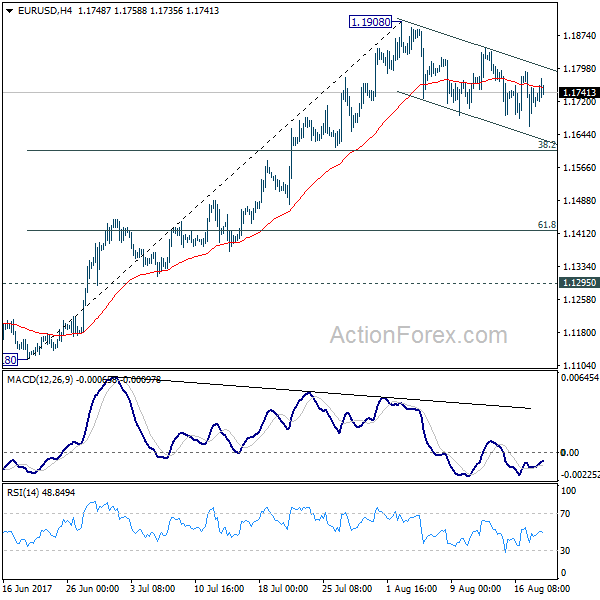

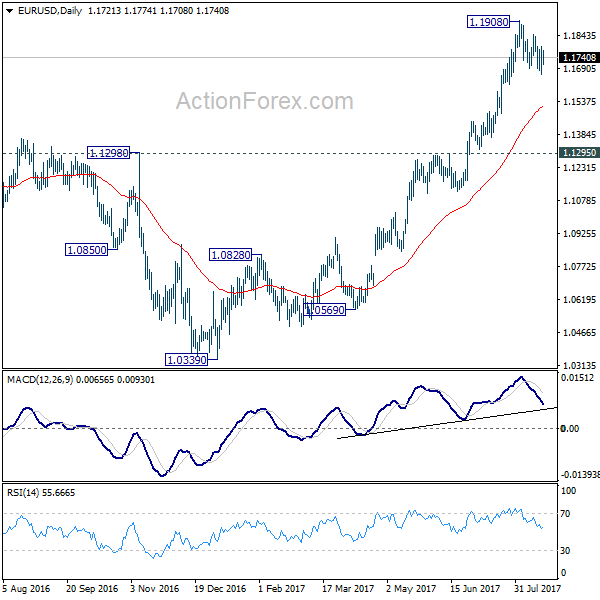

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1659; (P) 1.1725 (R1) 1.1788; More...

No change in EUR/USD's outlook as correction from 1.1908 is still in progress. While deeper pull back could be seen, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

USDCAD Fell to Two-Week Low Below 1.2600 Handle

The USDCAD fell to two-week low below 1.2600 handle despite Canadian inflation fell below expectations (July CPI 0.0% m/m vs 0.1% f/c / core CPI -0.1% in July vs 0.1% f/c) that may cool down expectations of BoC hiking rates soon. Loonie benefits from reduced risk appetite and may advance further on weak daily technicals as the latest acceleration broke through 20SMA (1.2603) after yesterday's probe below 1.2600 handle was short-lived. The pair eyes next support at 1.2552 (Fibo 61.8% of 1.2413/1.2778 upleg) violation of which is needed to signal an end of 1.2413/1.2778 corrective phase. The pair is also on track for bearish weekly close after two consecutive bullish week, with strong bearish signal being generated from bearish weekly candle with long upper shadow that signals strong upside rejection. Broken 10 SMA at 1.2681 which caps today's action, marks significant barrier.

Res: 1.2600; 1.2644; 1.2681; 1.2700

Sup: 1.2574; 1.2552; 1.2531; 1.2500

Canadian Inflation Remained Modest in July

Consumer price inflation ticked up slightly in July to a still-modest 1.2% year-on-year pace (June: 1.0%). On a month-on-month, seasonally adjusted basis, prices rose 0.2%.

In a reversal from June, goods price inflation ticked up a bit, albeit to barely above 0%, on the back of swings in energy prices. Conversely, services inflation, at 2.1% year-on-year, remains the driver of overall price growth, but decelerated somewhat from June's 2.4% reading.

Two of three Bank of Canada core inflation measures ticked up in July. CPI-median rose to 1.7% from 1.6% previously, while CPI-trim was also a tick higher, at 1.5%. The CPI-common measure of inflation was at an unchanged pace of 1.4% in July.

Key Implications

Canadian inflation may still be modest, but is showing some signs of moving in the "right" direction vis-à-vis the Bank of Canada's 2% inflation target. After months of deceleration, tick-ups in energy costs (on a year-on-year basis) helped deliver a small gain in price inflation in July. One month is hardly a trend, but the modest increases in the Bank of Canada's core measures provides some hope that inflation may have turned a corner.

The Bank of Canada has indicated that it will continue to monitor inflation data closely, but given that today's report is more or less in line with their expectations for soft (but rising) inflation in the back half of 2017, no change in Governor Poloz's thinking is likely to result. The Bank views the recent inflationary weakness as temporary, and expects recent economic strength to translate into inflationary pressures next year.

Monetary policy is not set for the inflation you have now, but for the inflation you expect to have down the road. Absent a significant economic shock or a significant change in thinking (and communication), it thus remains likely that the Bank of Canada will follow through with another 25bp increase in their overnight policy interest rate this fall.

Loonie Takes Flight After Inflation Report

- Canada Jul CPI-Common +1.4% y/y

- Canada Jul CPI-Median +1.7% y/y

- Canada Jul CPI-Trim +1.3% y/y

- Canada Jul Total CPI +1.2% y/y

- Canada Jul Total CPI Forecast at +1.2%

- Canada Jul Total CPI +0.0% from Jun

Data this morning showed that Canada's annual inflation rate picked up steam last month after slowing to a near two-year low in June, as it cost more to purchase gasoline and maintain a residence.

The all-items consumer-price index in July rose +1.2% from a year earlier, following a +1% advance in the previous month. The headline print matched market expectations.

On a month-over-month basis, CPI was unchanged in July. Meanwhile, the average annual rate of core-inflation rose +1.5% in July vs. June's gain of +1.4%.

The loonie has gathered steam outright, rallying +0.4% to C$1.2714 from C$1.2768 immediately after the data release. Major support remains intact just below the psychological C$1.27 handle at C$1.2685.

Canadian Inflation Edged Higher in July But Remained Well Short of 2%

Highlights:

- The year-over-year rate of headline CPI inflation rose to 1.2% in July from 1.0% in June.

- Two of the Bank of Canada's three preferred core measures ticked higher, lifting the average from 1.4% to 1.5% after rounding. Ex food and energy inflation similarly edged up to 1.5%.

- Another round of electricity price rebates in Ontario left national electricity prices 9% below year-ago levels. That represents a 0.2 percentage point drag on headline inflation.

Our Take:

Canadian inflation showed further signs of stabilization in July after having trended lower since the start of the year. The annual increase in most core measures edged higher and the all items index rose as expected following five months of below-consensus readings. There is still a ways to go, however, with headline inflation near the bottom of the Bank of Canada's 1-3% target range and most core indices around 1.5%. Some temporary factors are at play—the central bank has attributed part of the recent decline to lower energy prices and less auto price inflation. The former was once again a factor in July amid another round of electricity price rebates in Ontario. Nonetheless, our diffusion index shows less than 40% of the CPI basket is growing at 2% year-over-year, indicating below-target inflation doesn't simply reflect a few items.

So while it is encouraging to see the recent downward trend in the annual rate coming to an end, today's data doesn't really change the narrative on inflation. When they meet next month, the BoC's Governing Council will once again be weighing sub-target inflation against further strengthening in activity (we expect Q2 GDP +3.7% vs. the BoC's 3.0% forecast from July) and robust job growth. Faced with that same tradeoff in July, policymakers opted to raise the overnight rate, anticipating that tighter economic conditions will eventually put upward pressure on prices. They are likely to maintain that view, particularly as stronger Q2 GDP growth points to remaining economic slack being absorbed sooner than expected. But until there are clear signs of inflationary pressure emerging, we think the central bank will be fairly cautious in removing accommodation. A September rate hike can't be totally ruled out, but we think a move in October is more likely when the bank refreshes their economic projections.