Sample Category Title

ECB’s Vujcic: Gradual rate cuts justified amid elevated uncertainty

Croatian ECB Governing Council member Boris Vujcic emphasized a cautious and deliberate approach to monetary policy adjustments during comments to Econostream Media.

Vujcic stated that any acceleration in the pace of rate cuts would require a "significant departure" from the current economic projections, which he noted were being met by ongoing developments.

"In circumstances where uncertainties are still elevated," Vujcic explained, "it’s better to move gradually, and this is what we’re doing."

Vujcic also highlighted the ECB's independence from other central banks, including the Fed. "We are not dependent on the Fed or any other central bank," he remarked.

His comments lent support to current market expectations for ECB’s policy path, which he described as "justified" in the near term.

ECB’s Rehn: Restrictive monetary policy to end latest by mid-summer

Finnish ECB Governing Council member Olli Rehn reaffirmed the central bank's commitment to easing monetary policy as disinflation remains on track and the region faces a weakening growth outlook. Speaking with Bloomberg TV, Rehn stated that it "makes sense to continue rate cuts."

Rehn projected that ECB is likely to exit restrictive monetary territory "sometime in the spring-winter," a timeline he clarified could range from January to June in Finland's seasonal context.

He added, "I would say at the latest by midsummer, we should have left restrictive territory."

Rehn also emphasized ECB's independence in policy decisions, distancing it from the Fed's approach.

"The ECB is not the 13th federal district of the Federal Reserve System," he noted, reinforcing that the bank's decisions are guided solely by its mandate to maintain price stability within the Eurozone.

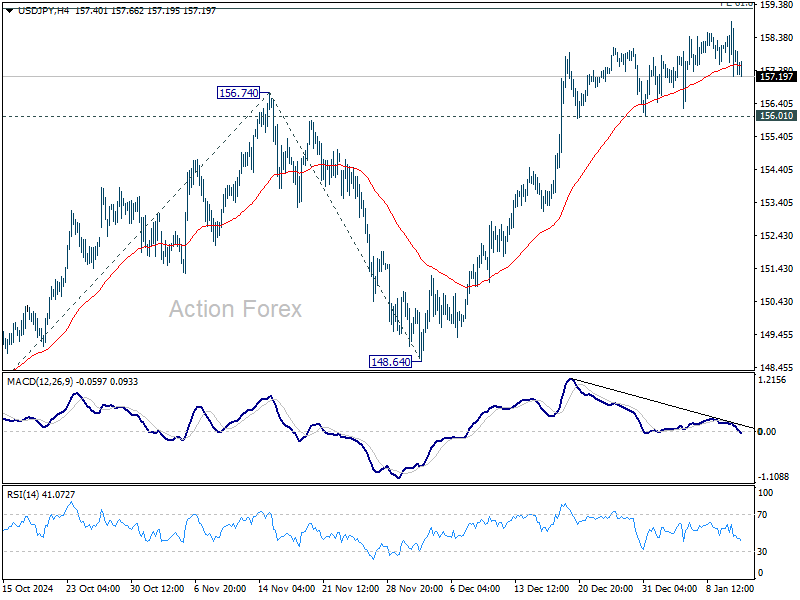

Serious Divergence Between USD/JPY and US Yields Explains the Strength of JPY Due to Risk-off

USDJPY moved slightly to the upside on Friday, but it was mostly just a spike, despite higher US yields which raises the question of whether the pair is starting to lose momentum. The price action clearly shows a potential five-wave move up from the December lows, which could now be ready to complete its recovery. If US yields would also hit some resistance this week, then it would likely have a bearish impact on the US dollar, and in that case, USDJPY could fall sharply, especially considering the Japanese yen is currently stronger compared to other currencies. However, this strength of JPY could also be driven by risk-off flows.

From an Elliott Wave perspective, I see the potential for a wedge formation on the USJDPY hourly chart that could push the pair back toward the 156 area.

https://www.youtube.com/watch?v=rY-bLohZlhE

S&P 500 Index Drops to 2-Month Low

On Friday, the US unemployment data was released, as reported by ForexFactory:

→ The unemployment rate dropped from 4.2% to 4.1%;

→ The number of new jobs (Non-Farm Employment Change) increased by 256,000 over the month, although analysts had forecast an increase of 164,000 (previous value = 212,000).

According to Reuters, the strong labour market data strengthened the market participants' view that the Federal Reserve will be cautious in cutting interest rates in 2025.

Based on CME Group’s FedWatch tool, traders expect the Fed to reduce borrowing costs for the first time in June and then keep it at that level for the remainder of the year.

Expectations that tight monetary policy will persist longer than usual have led to bearish sentiment. As a result, the S&P 500 index (US SPX 500 mini on FXOpen) dropped below the 5,800 mark this morning, its lowest point since early November.

Technical analysis of the S&P 500 index (US SPX 500 mini on FXOpen) shows:

→ A bearish Head and Shoulders (SHS) pattern is visible on the chart;

→ The price has broken below the median of the ascending channel (marked in blue).

The strengthening bearish sentiment may lead to:

→ The price fluctuating within the descending channel, the boundaries of which are already visible (marked in red);

→ The median of this red channel currently acting as support.

It is possible that the intensification of bearish sentiment will result in the S&P 500 index (US SPX 500 mini on FXOpen) declining towards the 5,700 level, which may be reinforced by the proximity of the lower boundary of the ascending channel.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

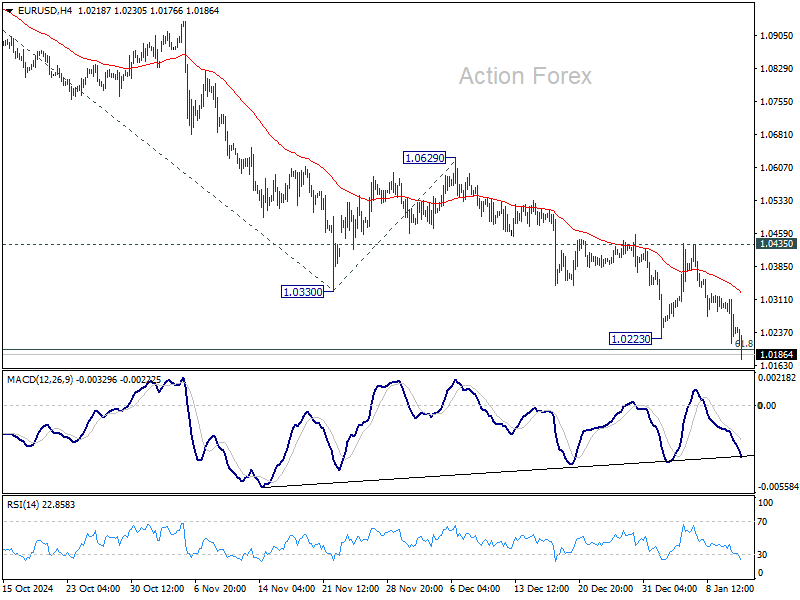

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0201; (P) 1.0257; (R1) 1.0301; More...

EUR/USD's decline from 1.1213 is extending today and intraday bias is back on the downside. Next near term target is 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. For now, outlook will stay bearish as long as 1.0435 resistance holds, in case of recovery.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

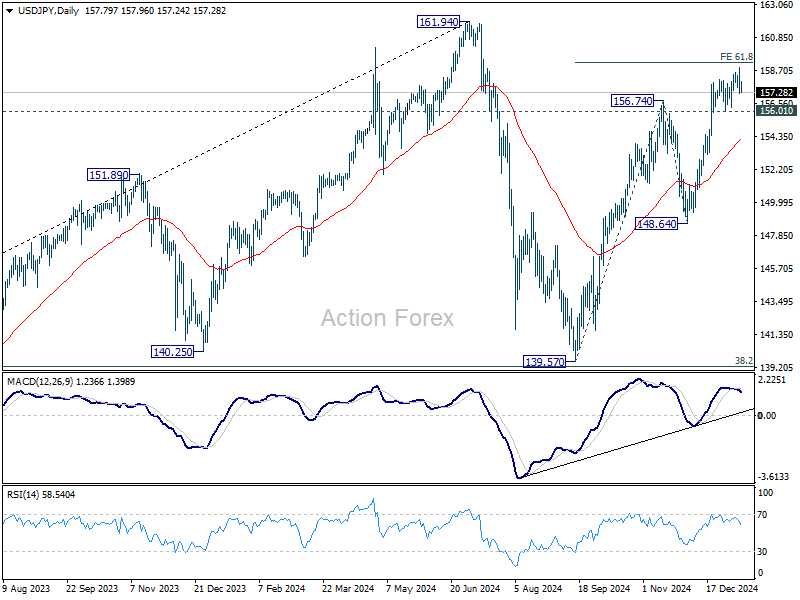

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.98; (P) 157.94; (R1) 158.64; More...

Intraday bias in USD/JPY remains neutral for the moment and some consolidations would be seen first. Further rally is in favor as long as 156.0 support holds. ON the upside, decisive break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will indicate short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 154.13) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

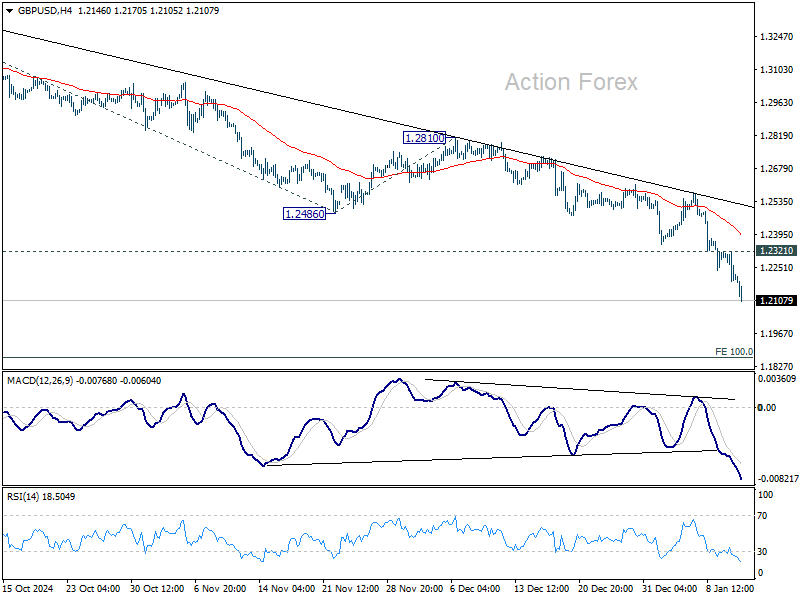

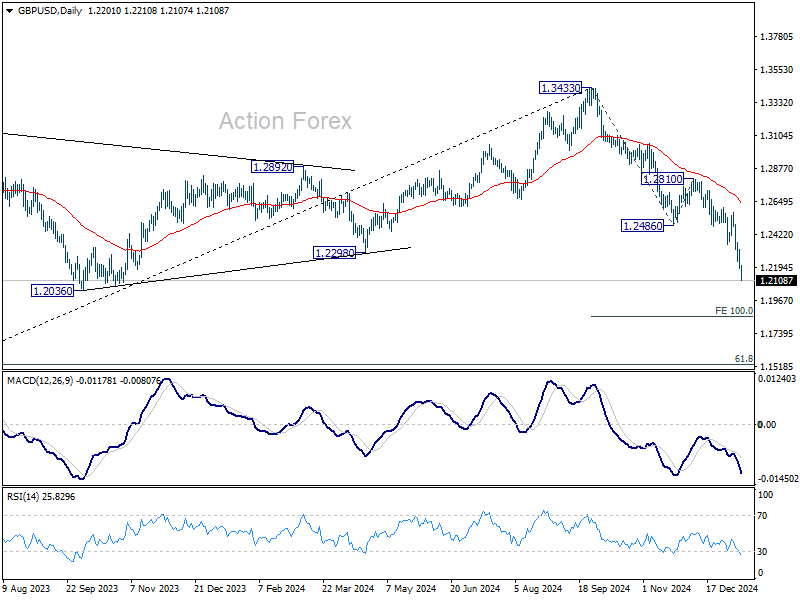

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2160; (P) 1.2241; (R1) 1.2291; More...

GBP/USD's decline from 1.3433 continues today and intraday bias stays on the downside. Deeper fall should be seen to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863. On the upside, break of 1.2321 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.2486 support turned resistance holds.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

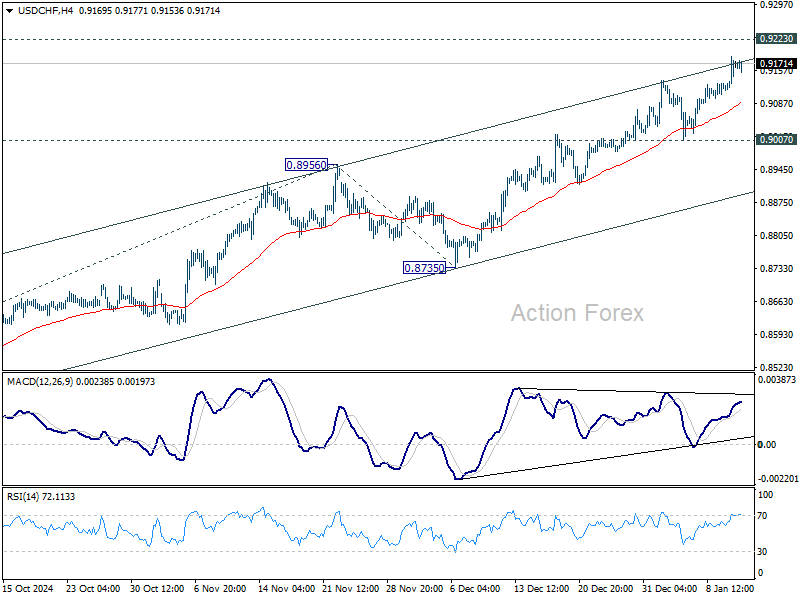

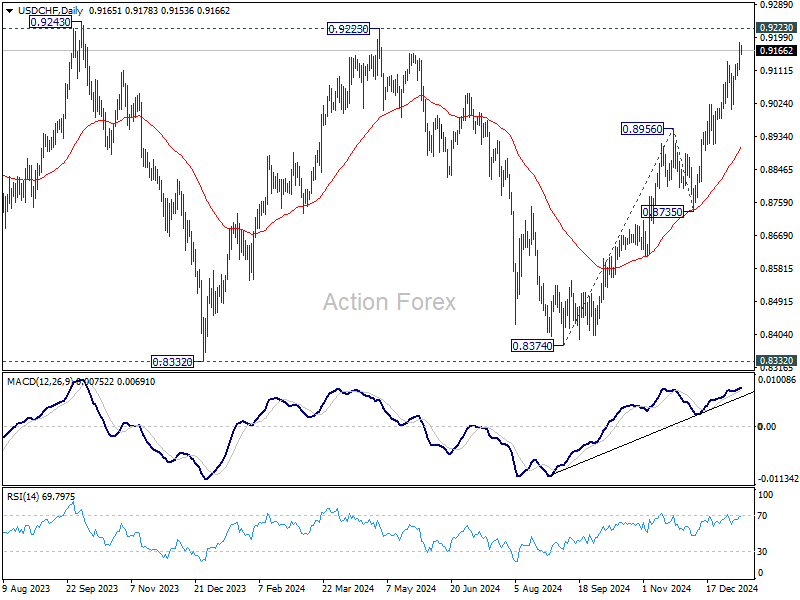

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9120; (P) 0.9154; (R1) 0.9200; More…

Intraday bias in USD/CHF remains on the upside for the moment. Current rally from 0.8374 is in progress for 0.9223 key resistance next. Decisive break there will carry larger bullish implications. For now, near term outlook will stay bullish as long as 0.9007 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

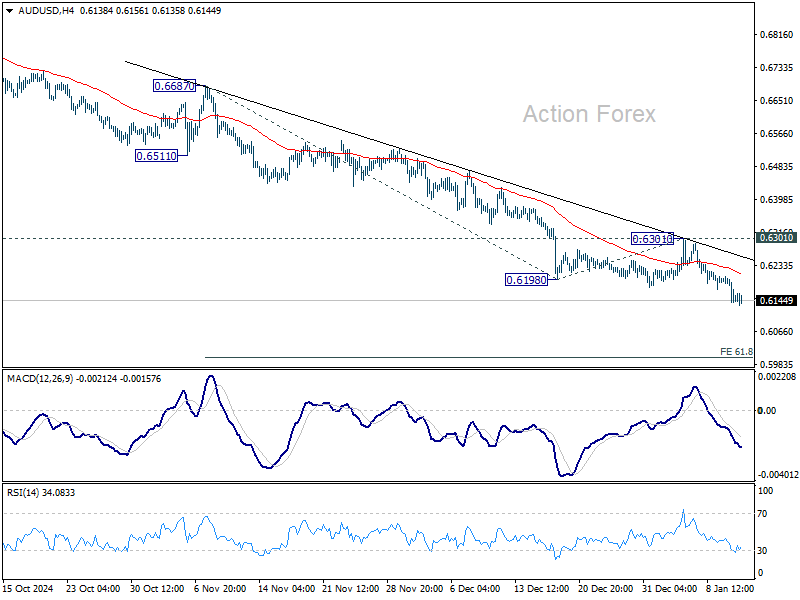

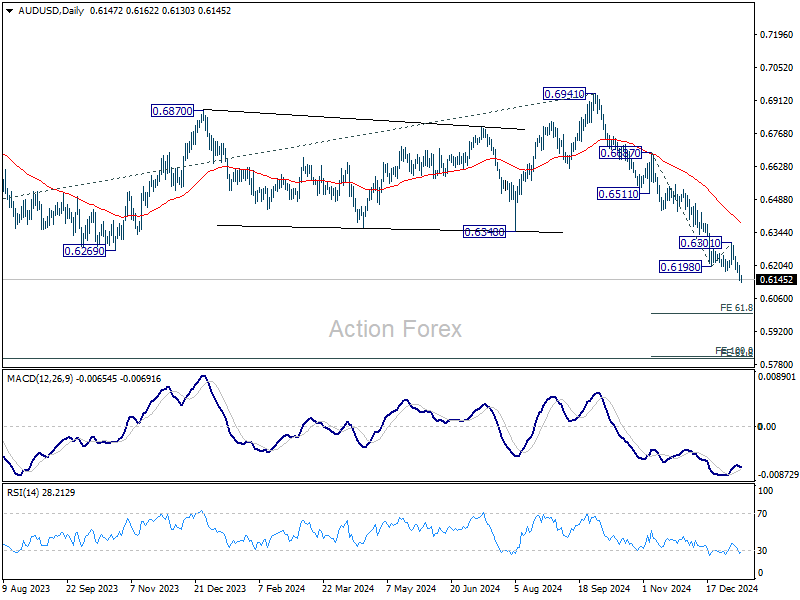

AUD/USD Daily Report

Daily Pivots: (S1) 0.6121; (P) 0.6163; (R1) 0.6188; More...

Intraday bias in AUD/USD stays on the downside for the moment. Current down trend should target next near term target at 61.8% projection of 0.6687 to 0.6198 from 0.6301 at 0.5999. For now, outlook will stay bearish as long as 0.6301 resistance holds, in case of recovery.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

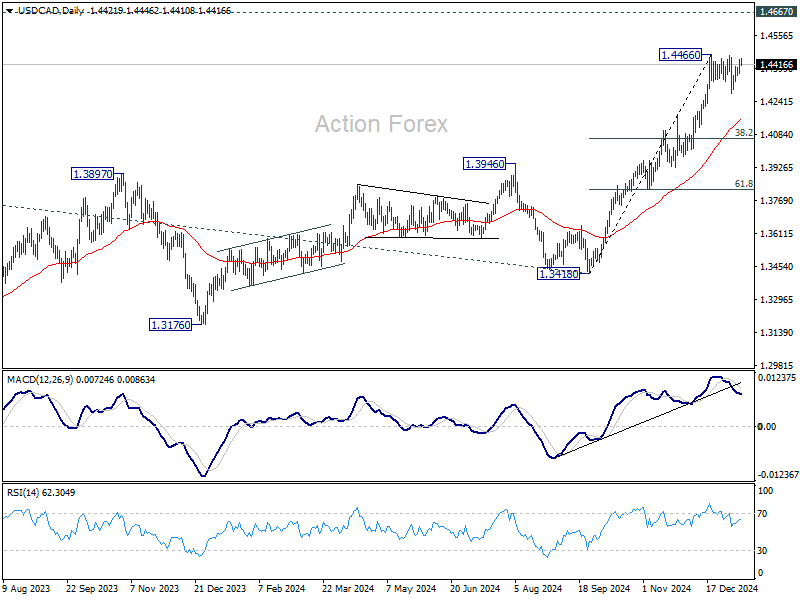

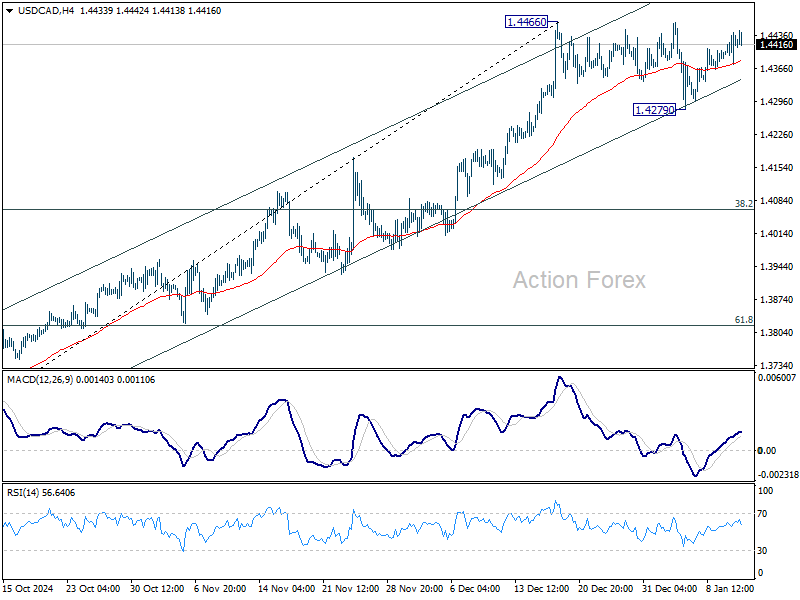

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4388; (P) 1.4416; (R1) 1.4455; More...

Intraday bias in USD/CAD remains neutral for the moment. On the upside, break of 1.4466 will resume larger up trend to 1.4667/89 long term resistance zone. However, break of 1.4279 will extend the corrective pattern from 1.4466 with another falling leg.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.