Sample Category Title

AUD/USD Rejected by Dynamic Resistance

Price increased sharply after the FOMC and jumped much above the first warning line (wl1) of the minor ascending pitchfork, but found strong resistance at the 150% Fibonacci line (ascending dotted line). Is pressuring the wl1, a retest of this level followed by a decrease will open the door for a decline towards the upper median line (uml) of the ascending pitchfork. Support can be found also at the 0.7989 level and much lower at 0.7874 static downside obstacle.

USD/JPY Undecided

Price has posted important gains in the last hours and is trying to stay higher as the USDX has managed to erase the morning gains and to recover after the morning sell-off. The dollar index is trading in the green ahead of the US data release, remains to see how will react after the reports will be published, another disappointment will send the dollar tumbling.

The US Unemployment Claims are expected to increase again, from 233K to 240K in the previous week, while the Core Durable Goods Orders may increase by 0.4% and could beat the 0.3% growth in the former reading period. The Durable Goods Orders are expected to increase by 3.5% in June, more after the 0.8% drop in the former reporting period, while the Goods Trade Balance is forecasted to increase from -65.9B to -65.0B in the last month. Prelim Wholesale Inventories could increase by 0.3%, less compared to the 0.4% in May.

USD/JPY continues to move sideways on the short term, has tried to increase, but was stopped by the 112.19 level. Now is trading below the 38.2% retracement level and much below the 150% Fibonacci line (ascending dotted line), a drop towards the 50% retracement level and towards the warning line (wl1) is favored. Will decrease only if the USDX will slide further and if the Nikkie stock index will stay below the 20058 major static resistance.

Is trapped between the 23.6% and the 50% retracement levels, that's why I've said that will approach the downside line of this range. A buying opportunity will appear only if will come down to retest the confluence area formed between the 50% retracement level and the warning line (wl1), or if will manage to breakout above the third warning line (WL3) of the descending pitchfork.

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.1698

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency rallied on dollar’s broad-based weakness after Fed, the breach of previous resistance at 1.1712 confirms recent upmove has resumed, hence gain to 1.1780-85 (50% projection of 1.1370-1.1712 measuring from 1.1613) cannot be ruled out, however, loss of near term upward momentum should prevent sharp move beyond 1.1820-25 (61.8% projection), risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.1680 would suggest an intra-day top is formed, bring test of the lower Kumo (now at 1.1648) but break there is needed to bring correction of recent rise towards support at 1.1613 first.

Trade Idea Update: USD/JPY – Hold short entered at 111.45

USD/JPY - 111.51

Original strategy :

Sold at 111.45, Target: 110.45, Stop: 111.80

Position : - Short at 111.45

Target : - 110.45

Stop : - 111.80

New strategy :

Hold short entered at 111.45, Target: 110.45, Stop: 111.80

Position : - Short at 111.45

Target : - 110.45

Stop : - 111.80

The greenback found support at 110.78 and has rebounded, suggesting further consolidation above this week’s low at 110.62 would be seen and marginal gain from here cannot be ruled out, however, reckon the upper Kumo (now at 111.78) would hold and bring retreat later, below said support at 110.78 would signal decline has resumed for retest of 110.62, break there would extend recent fall to 110.30-35.

In view of this, we are holding on to our short position entered at 111.45. Above 111.75-80 would defer and prolong choppy trading, however, price should still falter below said resistance at 112.20, bring retreat later.

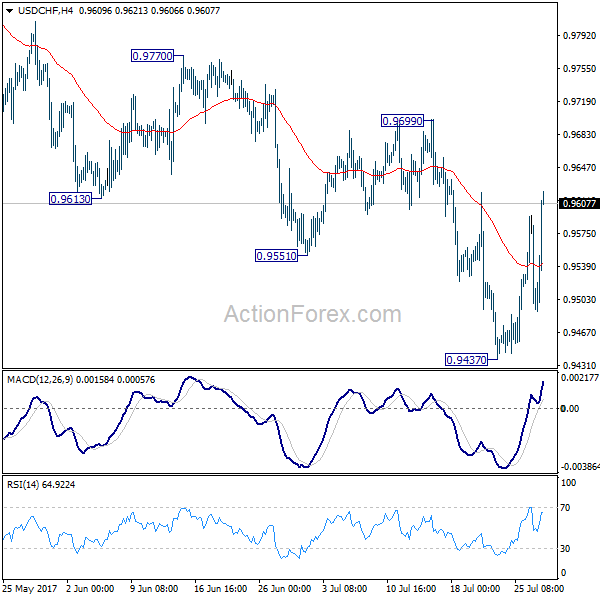

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9472; (P) 0.9533; (R1) 0.9569; More...

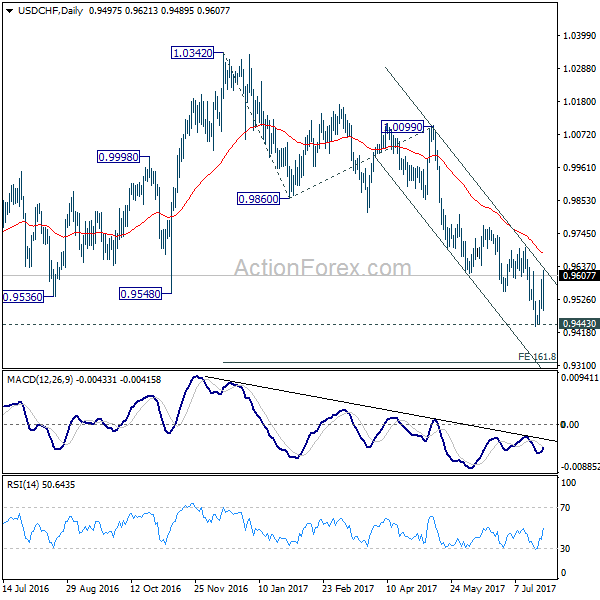

USD/CHF's rebound from 0.9437 resumed after deep but brief retreat. But still, it's staying in range of 0.9437/9699. Intraday bias remains neutral first. At this point, we remain cautious on strong support from 0.9443 key support to bring reversal. Decisive break of 0.9699 will confirm and turn outlook bullish. Meanwhile, sustained trading below 0.9443 will extend the down trend from 1.0342 to 161.8% projection of 1.0342 to 0.9860 from 1.0099 at 0.9319.

In the bigger picture, focus is now back 0.9443 key support level. Sustained break there indicate underlying bearish momentum and would target 0.9 handle and possibly below. Meanwhile, strong rebound from current level and break 0.9699 resistance will extend long term range trading between 0.9443/1.0342.

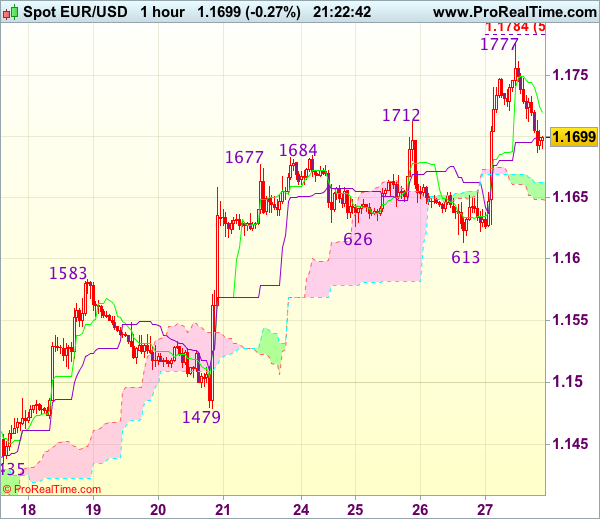

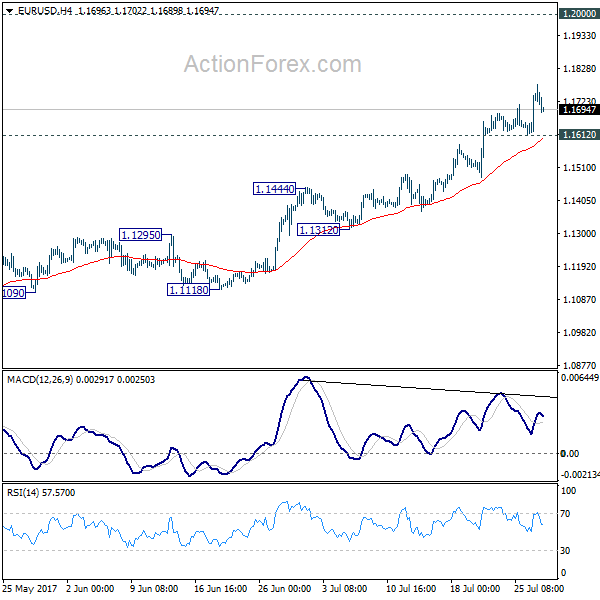

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1649; (P) 1.1695 (R1) 1.1777; More...

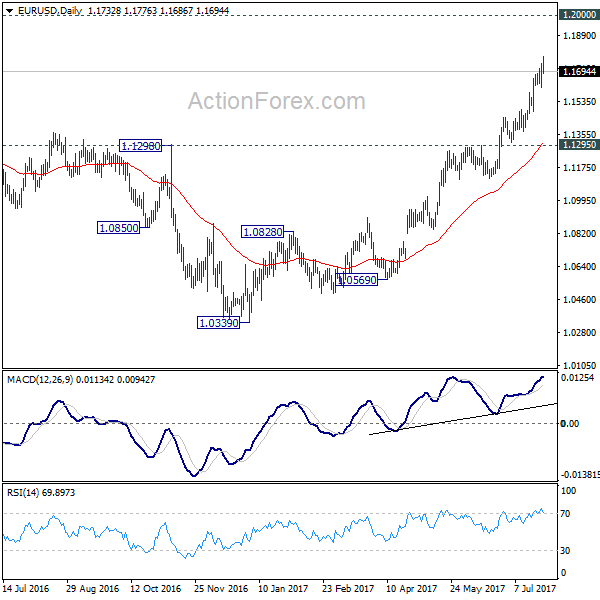

EUR/USD retreats mildly after hitting as high as 1.1776. But still, with 1.1612 minor support intact, intraday bias remains on the upside for further rise. Current medium term rally is expected to target 1.2 handle next. Nonetheless, considering bearish divergence condition in 4 hour MACD, break of 1.1612 will indicate short term topping and bring lengthier consolidation first.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained break of 55 month EMA (now at 1.1760) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

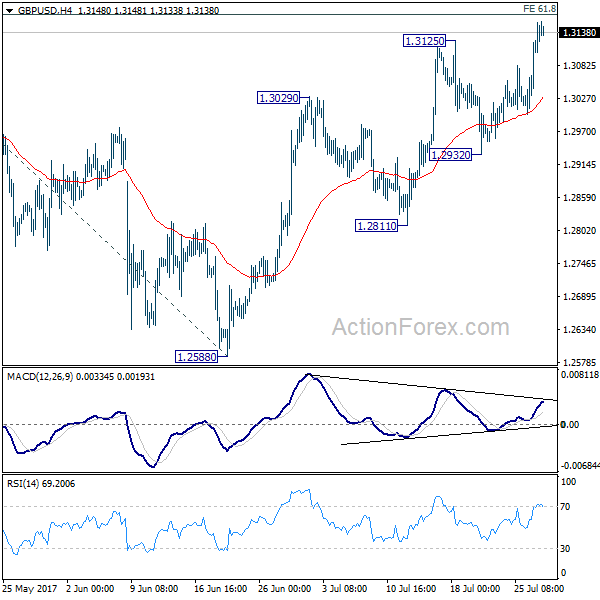

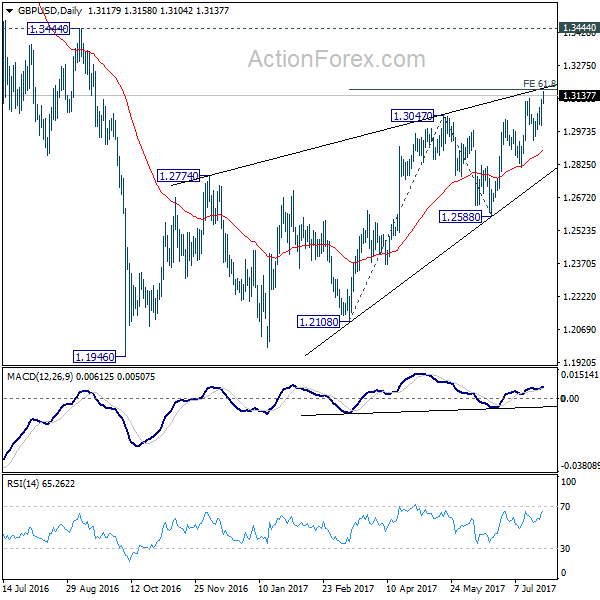

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3037; (P) 1.3080; (R1) 1.3161; More...

Intraday bias in GBP/USD remains on the upside for 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Considering bearish divergence condition in 4 hour MACD, we'd stay cautious on strong resistance from 1.3168 to limit upside. However, sustained break there could extend recent rebound towards 1.3444 key resistance. But still, price actions from 1.1946 is seen as a corrective pattern and GBP/USD should feel heavy approaching 1.3444. On the downside, break of 1.2932 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

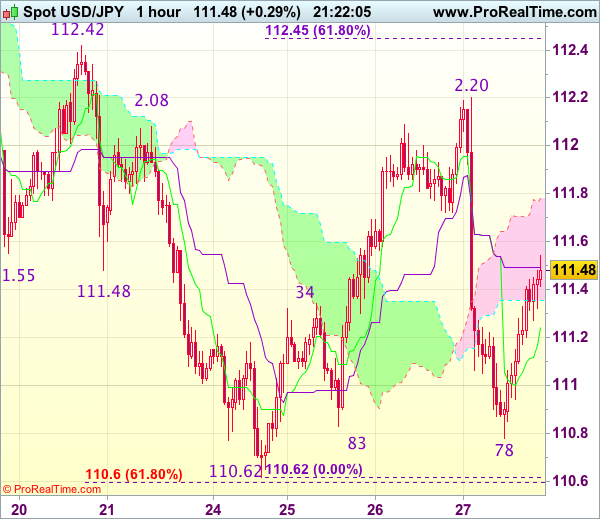

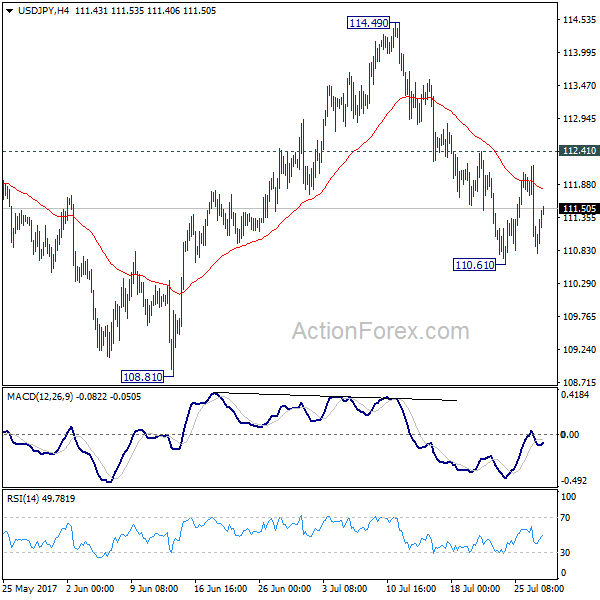

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.76; (P) 111.47; (R1) 111.89; More...

USD/JPY recovered ahead of 110.61 temporary low and stays in range below 112.41. Intraday bias remains neutral first. With 112.41 intact, further decline is expected. Below 110.61 will target 108.81. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.41 will dampen this bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

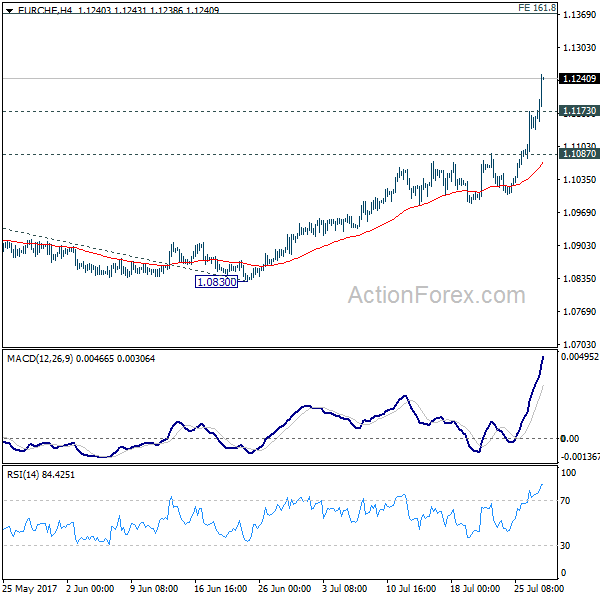

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1099; (P) 1.1136; (R1) 1.1194; More...

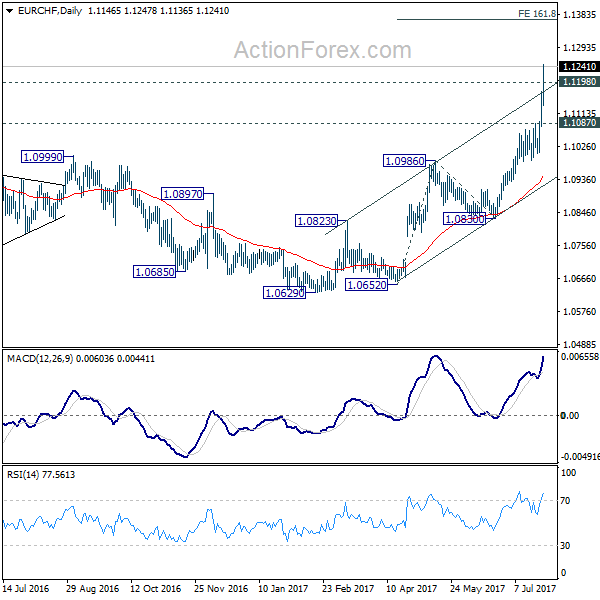

EUR/CHF's rally accelerates further today and reaches as high as 1.1247 so far. 1.1198 key resistance level is seen as taken out decisively. And there is no sign of topping yet. Intraday bias remains on the upside for 161.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1370. On the downside, below 1.1173 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well by 1.1087 resistance turned support and bring rise resumption.

In the bigger picture, sustained break of 1.1198 key resistance will confirm resumption of the long term rise from SNB spike low back in 2015. In such case, EUR/CHF could eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.0986 resistance turned support holds.

Spotlights Back on Swiss Franc as EUR/CHF Surges Past 1.12 Key Resistance

The spotlight moves back to the Swiss Franc today as EUR/CHF surges past 1.12 key resistance level. The cross is now setting up the momentum to regain 1.2 handle in medium term, which is the prior SNB imposed floor. Back in January 2015, SNB shocked the market by removing the floor and EUR/CHF dived to as low as 0.86, depending that what chart you read. With all the improvements in Eurozone, fundamentally, politically and system-wise, it now looks like there is no longer the need of safe haven parking in the Franc, with negative interest rates. The surge in commodity and energy prices would also help lift Eurozone inflation which keep ECB on course for stimulus exits.

Also regarding Swiss, the SNB's Libor will be discontinued in 2021, after being adopted as monetary policy target since 2000. An SNB spokesman said that the central bank will announce an alternative to franc Libor "in good time" And he emphasized that "The expected end of the franc Libor won't have an effect on the monetary policy orientation and monetary conditions." Some analysts pointed out that the Libor was mainly for the interbank market. SNB would need to rethink their approach. The secured Swiss Average Rate Overnight, SARON, could be an alternative.

Dollar paring back some post FOMC loss

Dollar is trying to recover today after the sharp post FOMC selloff. Some additional support is provided by solid economic data release. Meanwhile, it should be noted again that for the week as a whole, the Swiss Franc and Yen are indeed the weakest ones, not the greenback. Durable goods orders jumped 6.5% in June, well above expectation of 3.5%. But ex-transport orders rose only 0.2%, below expectation of 0.4%. Whole sale inventories rose 0.6% in June, above expectation of 0.3%. Initial jobless claims rose 10k to 244k in the week ended July 22, above expectation of 240k. It's nonetheless still the 125 straight week of sub 300k reading, the best streak since early 1970s. Continuing claims dropped 13k to 1.96m and stayed below 2m for 16 straight week, best since 1973.

Yesterday, Fed left its monetary policy unchanged, maintaining the federal funds rate target at 1-1.25%. The Fed made two tweak in the statement, though. First, it noted that balance sheet reduction would begin 'relatively soon', signaling that the official announcement would come in September. Second, policymakers revised lower the outlook on core inflation. US dollar plunged, with the weighted index falling to a 13-month low as the market interpreted the inflation assessment as dovish.

More on FOMC:

- FOMC Signaled To Begin Balance Sheet Normalization 'Relatively Soon', Downgraded Core Inflation Assessment

- Dollar Resumes The Unwind As Fed Fail To Impress

- FOMC Review: Smidgen Dovish But It Does Not Alter The Overall Picture

- FOMC: Steady As She Goes

- Little-Changed FOMC Statement Maintains Dovish Uncertainty, Weighs Further On Dollar

- Fed Stands Pat as Expected, Signals Coming Balance Sheet Normalization

- Fed Acknowledges the Inflation Miss, But Sticks to Balance Sheet Plans

EU officials warned of delay in Brexit negotiations

EU chief Brexit negotiator Michel Barnier briefed the 27 EU ambassadors yesterday regarding the July talks with UK. An EU official was quoted by Reuters saying that the chance of starting "future relationship talks" with UK in October "appeared to be decreasing". Progress on financial settlement, or the so called divorce-bill, was little to none. And EU officials believed that the problem lies in the lack of position of UK on many issues. The EU officials sounded a bit worried as the more time the first phrase drags on , the less time is left for the second phase, in particular on trade agreements.

UK Immigration Minister Brandon Lewis said today that "free movement of labor ends when we leave the European Union in the spring of 2019. I'll be very clear about that." While there is a period of negotiation with EU, Lewis emphasized that "we're very clear that free movement ends – it's part of the four key principles of the European Union – when we leave." That is seen as a response to recent reports that the UK government could allow a "transitional" period of three or four years regarding the issue.

Also released today, UK CBI realized sales rose to 22 in June. Eurozone M3 money supply rose 5.0% yoy in June. German Gfk consumer sentiment rose to 10.8 in August.

RBA Lowe warned of prolonged weak wage growth

In Australia, RBA governor Philip Lowe warned that prolonged weakness in wage growth could hurt the economy. He said that "if workers are getting no real wage increase year after year after year that's insidious." And, he emphasized that high wage growth "would help get inflation back to target and I think people would feel a bit better as well, and the fact that many of us have lowered our expectations of future income growth means we're less inclined to spend."

Regarding monetary policy, Lowe noted that "the main effect of lower interest rates is that more people have jobs". And "that's why I'm very comfortable with the current setting of monetary policy, it's helped people get jobs." Regarding the exchange rate, Lowe said that "it would be better if the exchange rate were a bit lower than it currently is. It would help generate more jobs, push inflation a bit closer to our target -- so that's the solution to a competitiveness problem."

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1099; (P) 1.1136; (R1) 1.1194; More...

EUR/CHF's rally accelerates further today and reaches as high as 1.1247 so far. 1.1198 key resistance level is seen as taken out decisively. And there is no sign of topping yet. Intraday bias remains on the upside for 161.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1370. On the downside, below 1.1173 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well by 1.1087 resistance turned support and bring rise resumption.

In the bigger picture, sustained break of 1.1198 key resistance will confirm resumption of the long term rise from SNB spike low back in 2015. In such case, EUR/CHF could eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.0986 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Import Price Index Q/Q Q2 | -0.10% | 0.70% | 1.20% | |

| 06:00 | EUR | German GfK Consumer Confidence AUG | 10.8 | 10.6 | 10.6 | |

| 08:00 | EUR | Eurozone M3 Y/Y Jun | 5.00% | 5.00% | 5.00% | |

| 10:00 | GBP | CBI Realized Sales Jul | 22 | 10 | 12 | |

| 12:30 | USD | Initial Jobless Claims (Jul 22) | 244K | 240k | 233k | 234K |

| 12:30 | USD | Durable Goods Orders Jun P | 6.50% | 3.50% | -0.80% | |

| 12:30 | USD | Durables Ex Transportation Jun P | 0.20% | 0.40% | 0.30% | |

| 12:30 | USD | Advance Goods Trade Balance Jun | -63.9B | -65.0B | -65.9B | |

| 12:30 | USD | Wholesale Inventories Jun P | 0.60% | 0.30% | 0.40% | |

| 14:30 | USD | Natural Gas Storage | 28B |