Sample Category Title

EUR/USD Losing Momentum, GBP/USD Throwback Expected, Gold Upside Paused

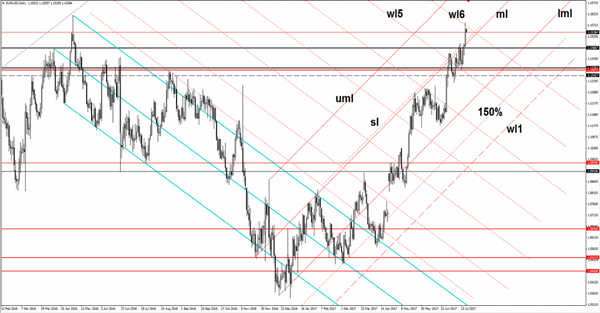

EUR/USD losing momentum

The EUR/USD rallied in the yesterday's trading session and reached the 1.1582 level, the buyers weren't able to keep the price above the 1.1552 closing price and now is going down. The minor decreased could be temporary because is still located in the buyer's territory.

Has found temporary resistance and now could come down to test and retest some support levels before will resume the upside movement.

Technically is expected to climb much higher in the upcoming period after the impressive breakout above the 1.1466 long term resistance. Will turn to the downside only if the USDX will have enough energy to bounce back on the short term.

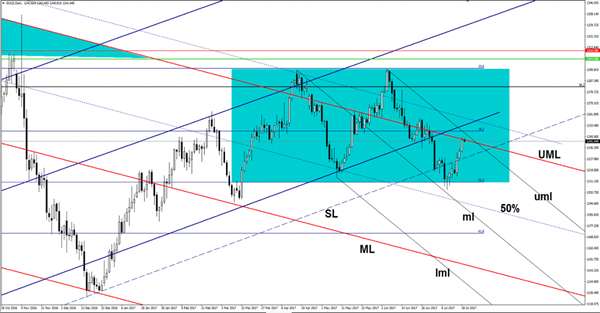

I've added the USDX's daily chart to show you what are the USD's perspectives in the upcoming period, has found temporary support at 94.49 level and now is fighting hard to recover. Has touched the lower median line (lml) of the descending dotted line and closed above this level, signaling an oversold.

USDX is pressuring the broken warning line (WL1) of the major ascending pitchfork, only a false breakout below this level will signal a reversal on the short term. Could increase towards the median line (ml) of the descending pitchfork if will stay above the lower median line (lml).

You can see that the USDX's minor rebound has sent the EUR/USD lower, price failed to close above the sixth warning line (wl6) and now could come to test and retest the median line (ml) of the ascending pitchfork and the sliding line (ascending dotted line).

The perspective remains bullish as long as is trading within the ascending pitchfork's body and most important above the median line (ml). The next major upside target will be at the 1.1615 swing high, I an to remind you that is trading inside of a major resistance area, but as I've said higher, the outlook is bullish.

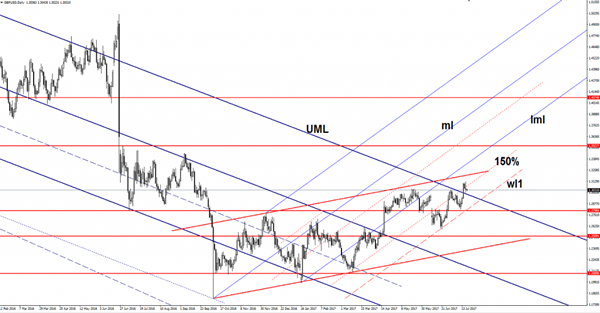

GBP/USD throwback expected

GBP/USD decreased a little in the last two days and could test and retest a former major dynamic resistance (resistance turned into support) before will climb much higher.

Price failed to stay above the 1.3112 level and above the 150% Fibonacci line and now is going down to retest the upper median line (UML) of the major descending pitchfork. A retest followed by an increase will bring us the opportunity to go long again on this pair.

Is trading within an ascending channel, could come to retest also the first warning line (wl1) of the minor ascending pitchfork before will climb towards fresh new highs.

Gold upside paused

We have a rebound in play, which has touched the upper median line (UML) of the major descending pitchfork, this represents a major dynamic resistance, could retest also the upper median line (uml) of the minor descending pitchfork. The bias is somehow bearish as long as is trading under the mentioned resistance levels. Continues to move sideways, between the 23.6% and the 50% retracement levels, we'll have a clear direction after a valid breakout from this range. The bounce back was natural after the false breakdown below the 50% retracement level and after the failure to retest the median line (ml) of the minor descending pitchfork.

EUR/USD Continued The Move Higher

Market Movers Today

It is a very thin calendar today with the only release being US building permits and housing starts in June. Both figures have been on a downward trend for most of this year after being on strong upward trends since 2011. That said, consensus is for an increase in both building permits and housing starts in June.

Before European markets open on Wednesday morning, the Bank of Japan (BoJ) is due to announce its monetary policy decision. We expect the BoJ to keep its 'QQE with yield curve control' policy unchanged, which is widely expected, especially after earlier this month it demonstrated its strong commitment to yield curve control by announcing an unlimited fixed-rate purchase of 10Y JGBs. The announcement should not have any significant impact on price actions. See Bank of Japan preview: BoJ's accommodative policy not about to change, 17 July 2017.

Selected Market News

EUR/USD continued the move higher during yesterday's trading session and rose above 1.158 briefly. The loss of momentum at the end of the day is consistent with positioning, shortterm valuation and technical factors. The next pivotal event for EUR/USD is the ECB meeting on Thursday, when we expect it to deliver only a minor hawkish twist. Despite the break of 1.15, risks for EUR/USD are probably still skewed to the upside in the case of a more hawkish ECB. For more about the recent move higher in EUR/USD and its outlook.

The ECB's staff is currently examining scenarios for the future path of QE including the announcement of a tapering path, an extension of asset purchases at a reduced pace and a combination of strategies, according to Bloomberg. The unnamed sources also said that ECB officials have limited appetite for any significant change in their language for now, which could tighten financial conditions and undermine the ongoing recovery. The recent surge in the effective EUR could spark some concerns among ECB members but, so far, the tapering speculations have not reversed the continued spread tightening in the periphery with 10Y Spain versus Germany decreasing yesterday to below 100bp for the first time since H2 16.

Australia’s Westpac Leading Index Declined Further In June

For the 24 hours to 23:00 GMT, the AUD rose 1.59% against the USD and closed at 0.7920.

LME Copper prices declined 0.4% or $25.0/MT to $5940.5/MT. Aluminium prices declined 0.7% or $14.0/MT to $1887.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7926, with the AUD trading 0.08% higher against the USD from yesterday's close.

Earlier in the session, data showed that Australia's Westpac leading index fell 0.14% in June. In the previous month, the index had dropped by a revised 0.01%.

The pair is expected to find support at 0.7880, and a fall through could take it to the next support level of 0.7834. The pair is expected to find its first resistance at 0.7957, and a rise through could take it to the next resistance level of 0.7988.

Moving ahead, investors will closely monitor Australia's unemployment rate data for June, slated to release in the early hours of tomorrow, to gauge strength in the nation's labour market.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Economic Sentiment Across The Euro-Zone Deteriorated More-Than-Expected In July

For the 24 hours to 23:00 GMT, the EUR rose 0.68% against the USD and closed at 1.1556.

On the data front, the Euro-zone’s ZEW economic sentiment index dropped more-than-expected to a level of 35.6 in July, compared to a level of 37.7 in the previous month, while markets were expecting for a fall to a level of 37.2.

Separately, mood among German investors eased more-than-anticipated to a level of 17.5 in July, compared to market consensus for a drop to a level of 18.0. In the previous month, the index had recorded a level of 18.6.

The greenback declined against a basket of major currencies, after the collapse of a Republican healthcare bill in the Senate added to worries that the US President, Donald Trump may be losing control of his legislative agenda.

On the macro front, the US NAHB housing market index unexpectedly eased to a level of 64.0 in July, hitting its lowest in 8 months, dragged down by concerns over rising costs for materials, particularly lumber. The index had registered a revised reading of 66.0 in the prior month, while market participants had expected it to climb to a level of 67.0. Moreover, the nation’s export price index surprisingly fell 0.2% on a monthly basis in June, compared to a revised drop of 0.5% in the prior month. Also, the nation’s import price index declined 0.2% MoM in June, after recording a revised drop of 0.1% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1539, with the EUR trading 0.15% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1506, and a fall through could take it to the next support level of 1.1472. The pair is expected to find its first resistance at 1.1578, and a rise through could take it to the next resistance level of 1.1616.

Moving ahead, market participants will focus on the Euro-zone’s construction output data for May, slated to release in a few hours. Additionally, in the US, housing starts and building permits data, both for June, scheduled to release later in the day, would pique investor attention.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

British Inflation Unexpectedly Slowed For The First Time Since October 2016 In June

For the 24 hours to 23:00 GMT, the GBP declined 0.08% against the USD and closed at 1.3044, following softer inflation figures in the UK.

Data indicated that Britain's consumer price index (CPI) climbed 2.6% on an annual basis in June, easing for the first time since October 2016 and diminishing the likelihood of an interest rate hike by the Bank of England (BoE) in the upcoming months. The CPI had advanced 2.9% in the previous month, while markets had anticipated for a gain of 2.9%.

In the Asian session, at GMT0300, the pair is trading at 1.3028, with the GBP trading 0.12% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2980, and a fall through could take it to the next support level of 1.2932. The pair is expected to find its first resistance at 1.3101, and a rise through could take it to the next resistance level of 1.3174.

With no major economic releases in the UK today, investor sentiment would be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Trading Marginally Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.54% against the JPY and closed at 112.01.

In the Asian session, at GMT0300, the pair is trading at 112.06, with the USD trading a tad higher against the JPY from yesterday's close.

The pair is expected to find support at 111.71, and a fall through could take it to the next support level of 111.35. The pair is expected to find its first resistance at 112.40, and a rise through could take it to the next resistance level of 112.73.

Moving ahead, the Bank of Japan's (BoJ) interest rate decision, scheduled to be announced tomorrow, will grab a lot of market attention. Markets widely anticipate the central bank to stand pat on monetary policy.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.81% against the CHF and closed at 0.9549.

In the Asian session, at GMT0300, the pair is trading at 0.9556, with the USD trading 0.07% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9519, and a fall through could take it to the next support level of 0.9481. The pair is expected to find its first resistance at 0.9599, and a rise through could take it to the next resistance level of 0.9641.

In absence of any economic releases in Switzerland today, trading trend in the CHF is expected to be determined by global macroeconomic news.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average

Loonie Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.58% against the CAD and closed at 1.2623.

In the Asian session, at GMT0300, the pair is trading at 1.2638, with the USD trading 0.12% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2588, and a fall through could take it to the next support level of 1.2538. The pair is expected to find its first resistance at 1.2681, and a rise through could take it to the next resistance level of 1.2724.

Ahead in the day, market participants will look forward to Canada's manufacturing shipments data for May.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

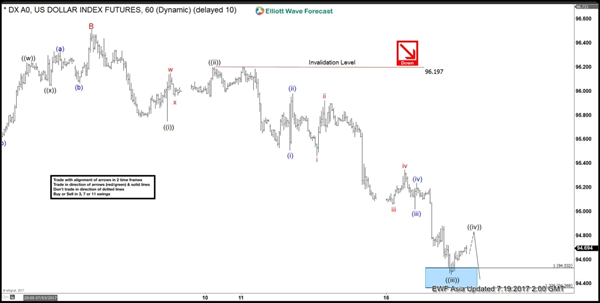

Elliott Wave View: DXY

Short term DXY (USD Index) Elliott Wave view suggests the decline from 6/20 peak (97.87) is unfolding as a Zigzag Elliott Wave structure. Down from 97.87 high, decline to 95.47 ended Minor wave A, and bounce to 96.51 high ended Minor wave B. Wave C is unfolding as an Elliott wave Impulse structure with extension where Minute wave ((i)) ended at 95.75, Minute wave ((ii)) ended at 96.2, and Minute wave ((iii)) ended at 94.47. Minute wave ((iii)) is subdivided into another impulsive wave of a smaller degree. Minutte wave (i) ended at 95.51, Minutte wave (ii) ended at 95.98, Minutte wave (iii) ended at 95.01, Minutte wave (iv) ended at 95.24, and Minutte wave (v) of ((iii)) ended at 94.47.

Currently Minutte wave ((iv)) is in progress to correct cycle from 7/10 high, and while pivot at 7/10 high holds, expect Index to turn lower again. We don’t like buying the Index and expect bounces to find offer in 3, 7, or 11 swing for more downside.

DXY 1 Hour Elliott Wave Chart

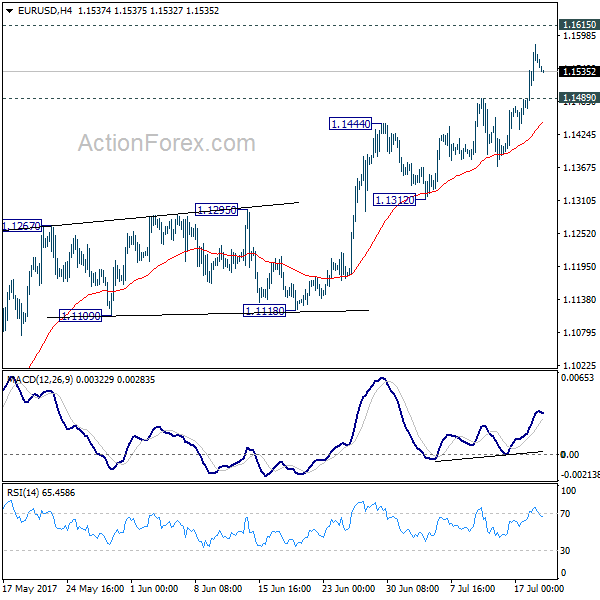

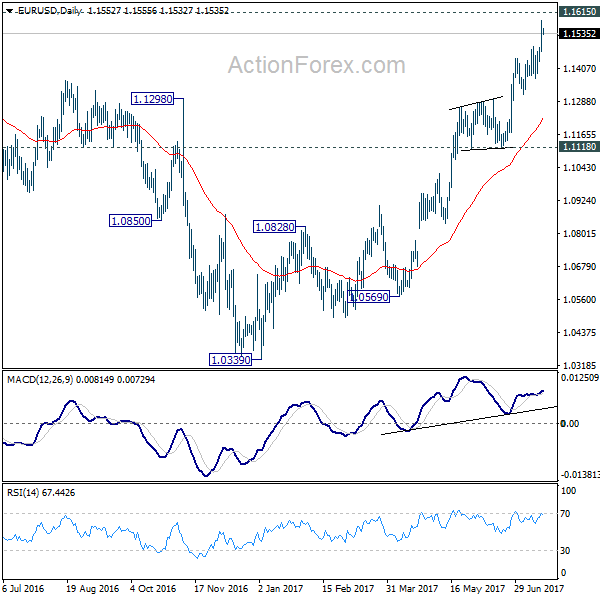

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1536 (R1) 1.1600; More.....

Intraday bias in EUR/USD remains on the upside for 1.1615 key resistance. Decisive break there will pave the way to 1.2 handle next. On the downside, below 1.1489 minor support will turn intraday bias neutral and bring consolidations. But near term outlook will remain bullish as long as 1.1312 support holds.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1756). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.