Sample Category Title

EURUSD: Rallies On Trend Resumption

EURUSD: The pair resumed its medium term uptrend on Tuesday leaving additional risk on the upside. Resistance comes in at 1.1600 level with a cut through here opening the door for more upside towards the 1.1650 level. Further up, resistance lies at the 1.1700 level where a break will expose the 1.1750 level. Its daily RSI is bullish and pointing higher suggesting further upside pressure. Conversely, support lies at the 1.1500 level where a violation will aim at the 1.1450 level. A break of here will aim at the 1.1400 level. All in all, EURUSD faces further upside pressure.

CAC Slips as Eurozone Investor Confidence Survey Misses Expectations

The CAC index is lower in Tuesday trading. Currently, the index is trading at 5190.50, down 0.81% on the day. In economic news, it's a quiet day. On the release front, Eurozone ZEW Economic Sentiment softened, coming in at 35.6 points. This reading missed the forecast of 37.2 points.

European stock markets are lower on Tuesday, responding to soft investor confidence surveys in Germany and the eurozone. The ZEW Economic Sentiment surveys gauge the optimism of institutional investors and analysts. Both surveys showed weaker optimism in June compared to the May releases. With the eurozone economy continuing to expand and the unemployment picture improving, the dip in investor confidence is likely due to the stronger euro, which has made European exports more expensive.

France has voted for change by electing President Emmanuel Macron, and the new French government is looking to take on a bigger role in Europe and on the international scene. Macron hasn't had to look far, as the messy departure of Britain from the EU could be a golden opportunity for France, both politically and economically. One casualty of Brexit is the City of London, a key financial hub. Many European companies will be downsizing their London operations, and the French are eager to snare a share of the spoils. French officials are actively courting companies to consider moving to Paris, rather than to other locations such as Frankfurt.

There was more bad news for President Trump, as his health care bill, which replaces much of Obamacare, has stalled in the Senate, after two Republicans announced they would not support the bill. The Republican leadership has admitted defeat, saying it will not attempt to advance their health care proposal before Congress takes a recess in August. This decision is a major setback for President Trump, who had made a new health care act a key part of his agenda. Despite Republican control of both houses of Congress and the White House, no major legislation has been passed since Trump took over as president 6 months ago. With this latest defeat, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending.

The US labor remains close to capacity and the unemployment rate is sparkling, at just 4.4%. So why is inflation mired at low levels? Economists are puzzled, and the Federal Reserve is also at a loss, although Fed Chair Janet Yellen insists that it's only a matter of time before inflation moves higher. In testimony before a Senate committee last week, Yellen insisted that it was "premature to conclude that the underlying inflation trend is falling well short of 2 percent", and that with a strong labor market "the conditions are in place for inflation to move up". However, the markets remain skeptical that the Fed will make a move before the end of the year, with the odds of a December hike at just 47%, according to the CME Group.

USD/JPY Additional Drop on the Cards, USD/CAD Sell-off Accelerates, Brent Oil Breakout Still Favored

USD/JPY additional drop on the cards

The currency pair extends the sell-off and looks too heavy to be stopped on the short term, is pressuring an important dynamic support. Is going down as the USD is weakened by the USDX's further drop, the index is trading below the 94.70 level and could most likely will approach and reach the 94.50 psychological level in the upcoming hours.

The Yen could dominate the currency market as the Nikkei stock index decreased and failed to stay above the 20058 major static resistance. JP225 move sideways, but most likely will have a significant move in the upcoming days.

I've said in the previous Market Reports that the Nikkei shows some exhaustion signs as long as continues to stay much below the 20320 previous high. The index could move in range on the short term, only a valid breakdown below the 19700 static support will open the door for more declines.

Is trading in the red and could take out the support from the downtrend line (resistance turned into support) and could hit the next downside targets, represented by the 38.2% retracement level and the 150% Fibonacci line.

A valid breakdown below these levels will attract more sellers on the short term, which will drive the rate towards the 50% retracement level and towards the major confluence formed by the warning line (wl1) of the ascending pitchfork with the second warning line (WL2) of the major descending pitchfork.

The current drop is natural after the false breakout above the 23.6% retracement level and after the failure to reach the third warning line (WL3) of the major descending pitchfork. Continues to move sideways on the Daily chart, but I hope that we'll have a clear direction very soon because the narrow movement can't continue forever.

USD/CAD sell-off accelerates

USD/CAD extends the bearish momentum targeting the 1.2500 psychological level, looks too heavy to be stopped right now. The USD is to release the Import Prices along with the NAHB Housing Market Index and with the TIC Long-Term Purchases reports, only a very good data could save the greenback from downside.

Price plunges after the yesterday's minor retreat, has come higher only to retest the third warning line (wl3) of the minor ascending pitchfork and now is going down towards fresh new lows. The next downside important targets are at the 1.2460 swing low and at the lower median line (lml) of the minor descending pitchfork.

Brent Oil breakout still favored

Brent Oil rallied after the yesterday's drop and is pressuring the 48.88 static resistance, technically, a valid breakout is expected. We may have a buying opportunity if will stabilize above the $48.88 per barrel, the next upside target will be at the outside sliding line (descending dotted line), where he could find temporary resistance again.

Only a valid breakout above the sliding line (sl) will validate a broader rebound in the upcoming weeks.

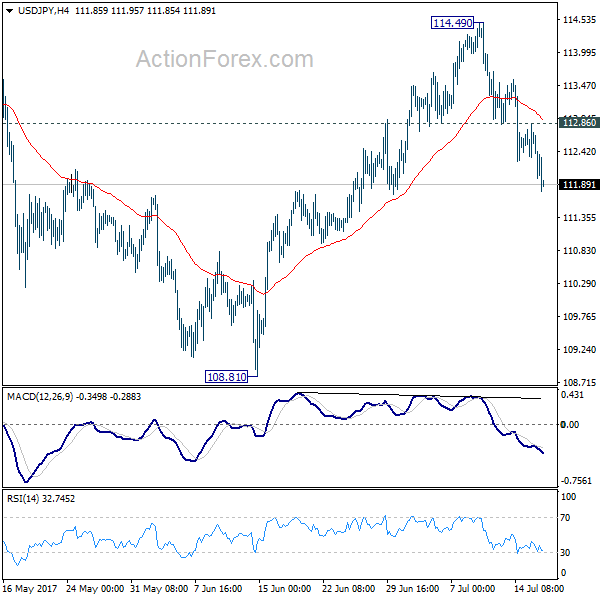

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.35; (P) 112.60; (R1) 112.88; More...

USD/JPY's fall is still in progress and intraday bias remains on the downside. As noted before, the rejection from 114.36 resistance suggests that whole correction from 118.65 is possibly still in progress. Sustained break of 55 day EMA (now at 112.02) will pave the way to 108.12 and below. On the upside, above 112.86 minor resistance will turn intraday bias neutral first.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

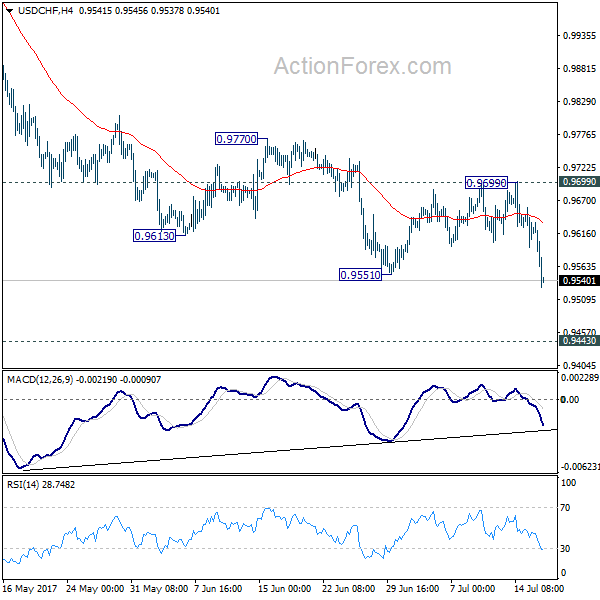

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9593; (P) 0.9625; (R1) 0.9657; More...

USD/CHF's decline from 1.0342 resumed by taking out 0.9551 and reaches as low as 0.9528 so far. Intraday bias stays on the downside for 0.9443 key support level next. At this point, we'd expect strong support from there to bring rebound. Nonetheless, break of 0.9699 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

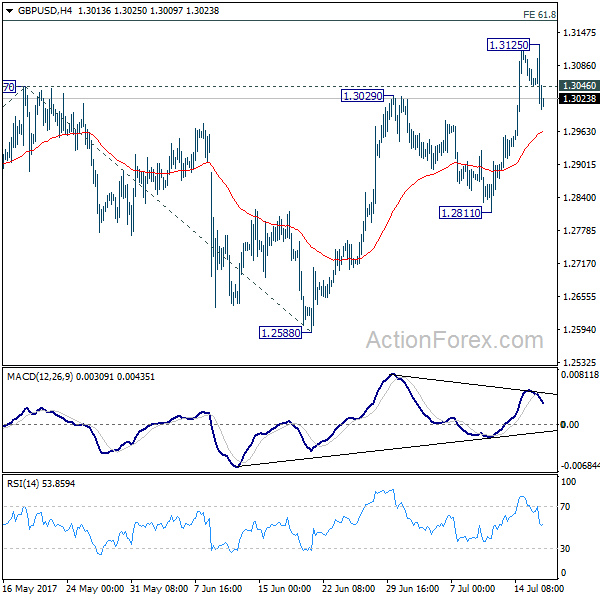

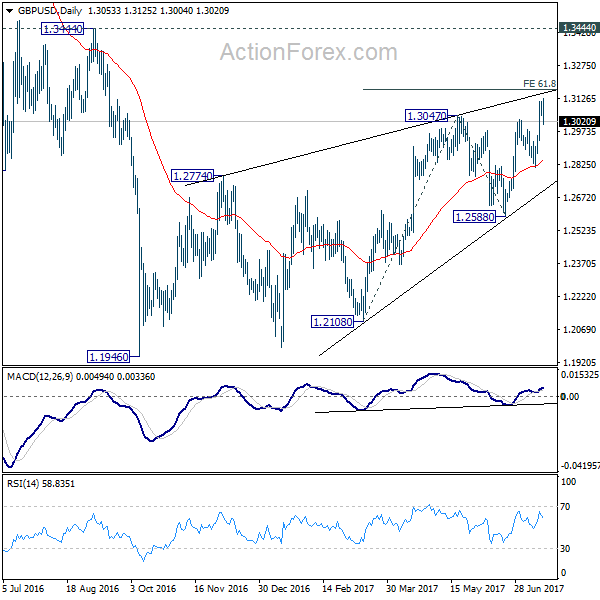

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3028; (P) 1.3070; (R1) 1.3094; More...

GBP/USD's sharp fall suggests that a temporary top is formed at 1.3125 and intraday bias is turned neutral first. Another rise would be seen as long as 1.2811 support holds. Break of 1.3125 will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Overall, choppy rebound from 1.1946 is seen as a corrective pattern, hence, we'd be cautious on strong resistance from 1.3168 to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. Meanwhile, break of 1.2811 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

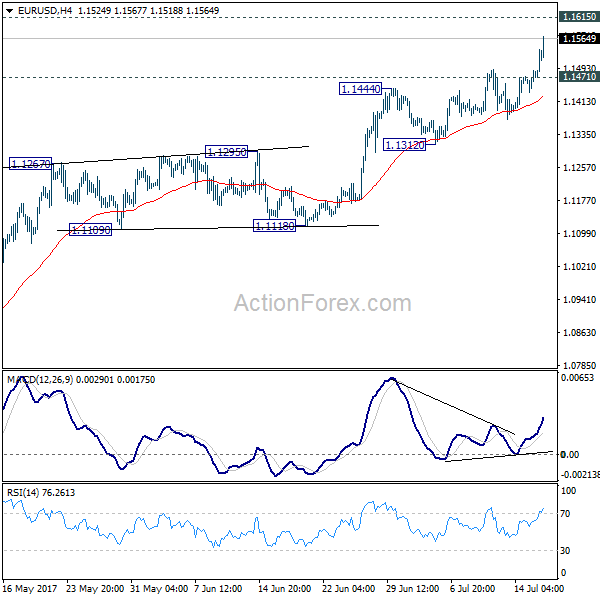

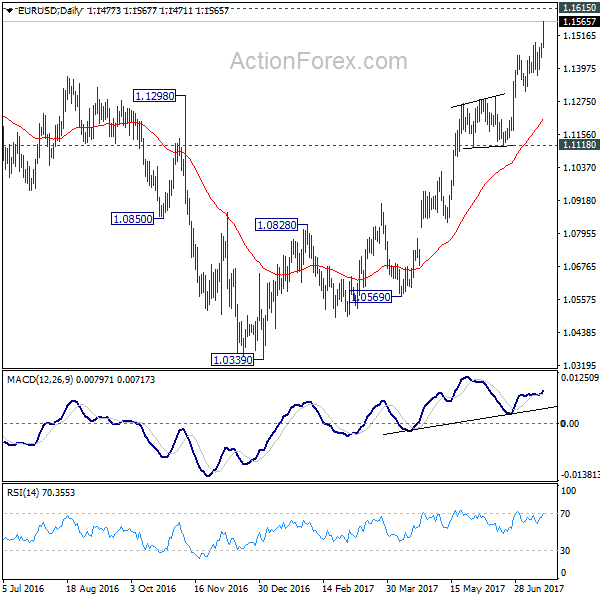

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1446; (P) 1.1466 (R1) 1.1498; More.....

EUR/USD's rally continues today and reaches as high as 1.1567 so far. Intraday bias remains on the upside for 1.1615 key resistance. Decisive break there will pave the way to 1.2 handle next. On the downside, below 1.1471 minor support will turn intraday bias neutral and bring consolidations. But downside of retreat should be contained above 1.1312 support and bring rise resumption.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1756). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Sterling Punished by CPI Miss, Dollar Selloff Continues on Trumpcare Failure

Sterling is sold off sharply after slowdown in inflation reading dents hope of a near term BoE hike. The violent move in the Pound makes it the weakest currency today, overtaking Dollar and Kiwi. The greenback tumbles broadly after another failure of Trump care and stays generally weak as traders pare back expectations of another Fed hike this year. Kiwi was sold off sharply earlier as CPI miss suggests that RBNZ was right not to turn hawkish. Meanwhile, Australian Dollar remains the strongest one today as RBA minutes raised hope of a hawkish turn in the central bank. Trading in other currencies are mixed. In other markets, Gold again rides on Dollar weakness and is back pressing 1240. WTI crude oil also firms up mildly and is back above 46.

Dollar sold off on another Trumpcare failure

Dollar is under much selling pressure on the news of the collapse of health care bill of US President Donald Trump and Republicans to replace ObamaCare. Senate Majority Leader Mitch Connell accepted defeat after a total of four Senate Republicans openly announced opposition to the bill, that leaves it two vote short of advancing. McConnell said in a statement that "regretfully, it is now apparent that the effort to repeal and immediately replace the failure of Obamacare will not be successful". Senate Democratic leader Chuck Schumer urged the Republicans to "start from scratch and work with Democrats" on a bill to fix problems with Obamacare. And, he criticized that "this second failure of Trumpcare is proof positive that the core of this bill is unworkable."

According to a Reuters poll of over 100 economists, the consensus is that Fed will hike federal funds rates by 25 to 1.25-1.50% by the end of the year. Meanwhile, two-thirds of the respondents expected Fed to announce the plan to unwind the USD 4T balance sheet in September. Fed fund futures are pricing in only 8.4% chance of a Fed hike in September.

Released from US, import price index dropped -0.2% mom in June.

UK CPI miss lifted pressure on BoE to hike

Sterling drops broadly as inflation data comes in much lower than expected. Headline CPI in UK slowed to 2.6% yoy in June, down from 2.9% yoy and missed expectation of 2.9% yoy. Core CPI slowed to 3.4% yoy, down from 2.6% yoy and missed expectation of 2.6% yoy. RPI also slowed to 3.5% yoy, down from 3.7% yoy and missed expectation of 3.6% yoy. The data should have eased much pressure for BoE to hike interest rate in near term. Back in June, the MPC decided to keep bank rate unchanged at 0.25% with 5-3 vote. Kristin Forbes has left the committee already and has returned to MIT's Sloan School of Management. And it's unlikely that other MPC members will rush to vote for a hike in August.

Also from UK, PPI input slowed to 9.9% yoy, PPI output slowed to 3.3% yoy, PPI output core rose to 2.9% yoy. House price index rose 4.7% yoy in May.

While the markets are pricing in full chance of 25bps hike by May 2018, a Reuters poll suggests that rates will not be raised until 2019. Meanwhile, there is on average a 1/3 chance of a rate hike this year. Only two of the 80 economists surveyed expected a hike in August. And four others expected a hike by the end of December.

German ZEW dropped by outlook remains positive

German ZEW economic sentiment dropped to 17.5 in July, down from 18.6 and missed expectation of 18.0. Current situation gauge dropped to 86.4, down from 88.0 and missed expectation of 88.0. Eurozone ZEW economic sentiment dropped to 35.6, down fro 37.7 and missed expectation of 37.2. ZEW president Achim Wambach noted in the statement the "overall assessment of the economic development it Germany Remains unchanged compared to the previous month. And, "the outlook for the German economic growth in the coming six months continues to be positive. This is now also reflected in the survey results for the eurozone."

RBA minutes: 3.5% could be the appropriate neutral rate

RBA minutes for the July meeting suggested that policymakers acknowledged the economic growth and the improvement in the labor market recently. The members also discussed the appropriate neutral rate which they believed should be at 3.5%, well above the current cash rate of 1.5%. This heightened market expectations of a potential rate hike in the near-term. As such, Aussie jumped to a 2-year high after the release of the minutes. More in Speculations Of RBA Rate Hike Heightened, As Members Discussed Neutral Rate.

Kiwi plummets as CPI affirmed RBNZ's neutral stance

New Zealand Dollar tumbles sharply after weaker than expected inflation data. Over the quarter, CPI rose 0.0% qoq, down from prior quarter's 1.0% qoq and missed expectation of 0.2% qoq. Annually, CPI slowed to 1.7% yoy, down from 2.2% yoy and missed expectation of 1.9% yoy. The reading now clearly support RBNZ's neutral stance. There were some questions and disappointment as RBNZ didn't turn hawkish after CPI shoot to 2.2% yoy back in Q1. But now it's obvious that the central bank has made the correct decision.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1446; (P) 1.1466 (R1) 1.1498; More.....

EUR/USD's rally continues today and reaches as high as 1.1567 so far. Intraday bias remains on the upside for 1.1615 key resistance. Decisive break there will pave the way to 1.2 handle next. On the downside, below 1.1471 minor support will turn intraday bias neutral and bring consolidations. But downside of retreat should be contained above 1.1312 support and bring rise resumption.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1756). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | 0.00% | 0.20% | 1.00% | |

| 22:45 | NZD | CPI Y/Y Q2 | 1.70% | 1.90% | 2.20% | |

| 01:30 | AUD | RBA Minutes July | ||||

| 03:00 | NZD | Non Resident Bond Holdings Jun | 61.50% | 61.40% | ||

| 08:30 | GBP | CPI M/M Jun | 0.00% | 0.20% | 0.30% | |

| 08:30 | GBP | CPI Y/Y Jun | 2.60% | 2.90% | 2.90% | |

| 08:30 | GBP | Core CPI Y/Y Jun | 2.40% | 2.60% | 2.60% | |

| 08:30 | GBP | RPI M/M Jun | 0.20% | 0.40% | 0.40% | |

| 08:30 | GBP | RPI Y/Y Jun | 3.50% | 3.60% | 3.70% | |

| 08:30 | GBP | PPI Input M/M Jun | -0.40% | -0.90% | -1.30% | -0.70% |

| 08:30 | GBP | PPI Input Y/Y Jun | 9.90% | 9.30% | 11.60% | 12.10% |

| 08:30 | GBP | PPI Output M/M Jun | 0.00% | 0.10% | 0.10% | |

| 08:30 | GBP | PPI Output Y/Y Jun | 3.30% | 3.40% | 3.60% | |

| 08:30 | GBP | PPI Output Core M/M Jun | 0.20% | 0.10% | 0.10% | |

| 08:30 | GBP | PPI Output Core Y/Y Jun | 2.90% | 2.80% | 2.80% | |

| 08:30 | GBP | House Price Index Y/Y May | 4.70% | 3.00% | 5.60% | 5.30% |

| 09:00 | EUR | German ZEW (Economic Sentiment) Jul | 17.5 | 18 | 18.6 | |

| 09:00 | EUR | German ZEW (Current Situation) Jul | 86.4 | 88 | 88 | |

| 09:00 | EUR | Eurozone ZEW (Economic Sentiment) Jul | 35.6 | 37.2 | 37.7 | |

| 12:30 | USD | Import Price Index M/M Jun | -0.20% | -0.20% | -0.30% | -0.10% |

| 14:00 | USD | NAHB Housing Market Index Jul | 67 | 67 | ||

| 20:00 | USD | Net Long-term TIC Flows May | 20.3B | 1.8B |

Unexpected Fall in Inflation Punishes Sterling

The fact that Sterling sharply depreciated across the board on Tuesday, after British inflation rates unexpectedly dropped to 2.6% in June, continues to highlight how the currency has become increasingly sensitive to monetary policy speculation. Price action suggests that those who were heavily reliant on the possibility that higher rates would support Sterling further were left empty-handed, as deceleration in inflation eroded expectations of a UK rate increase in 2017. Although the Bank of England has adopted a hawkish tone in recent weeks, today's fall in inflation is likely to ease pressure on the Bank of England taking action, consequently keeping hawks at bay.

There was a suspicion that bulls were relying on a weak foundation to propel the GBPUSD above 1.3000 last week, with the current selloff almost validating this observation. Investors should keep in mind that the fundamentals behind Sterling's woes remain intact, with sellers potentially exploiting rate hike speculations and Dollar weakness to install fresh rounds of selling. From a technical standpoint, a decisive breakdown and daily close below 1.3000 should encourage a further decline towards 1.2850.

Will the upcoming OPEC meeting support oil?

It has certainly been an eventful second trading quarter for the oil markets, with the commodity still under intense pressure as the oversupply woes remained a dominant theme. As the third quarter of the year gets under way, investors will be paying very close attention to see whether OPEC moves forward with deeper cuts in an effort to stabilize the markets. The recent string of events involving OPEC and oil price action in general raise questions over whether the cartel has lost its grip on the global oil markets. For instance, the supply cut exemptions for some OPEC members have come back to bite the cartel, with reports circulating over the possibility that OPEC will request Nigeria and Libya to cut production. I believe the threat of increased production from Nigeria and Libya which would obstruct efforts made by the rest of the group to rebalance the markets may prompt OPEC to request for production caps from both nations at the upcoming OPEC meeting on 24 July.

Commodity Spotlight - Gold

Gold bulls received support in the form of Dollar weakness during Tuesday's trading session, while concerns over Donald Trump failing to deliver on his controversial healthcare reforms complimented the upside as investors sought safe-haven safety. Although further upside could be on the cards in the short term amidst the cautious atmosphere, the rising prospects of tighter global monetary policy may dampen the metal's allure this quarter. From a technical standpoint, bulls need a breakout and daily close above $1240 for a further incline higher towards $1260. In an alternative scenario, repeated weakness below the $1240 resistance level may encourage sellers to drag Gold back towards $1225.

UK Inflation Slows in June; Sterling Takes a Hit on Falling Rate Rise Prospects

UK CPI data for the month of June showed inflation slowing during the month. The decline in annual inflation marks the first slowdown since October of last year and led sterling to record losses relative to other major currencies. Market participants interpreted the figures as easing pressure on the Bank of England to raise rates as it convenes to set monetary policy in the beginning of August.

Turning to the actual numbers, the annual inflation rate stood at 2.6% in June, below the expected 2.9% which also coincided with the near four-year high from the previous month. Month-on-month, the inflation rate recorded zero growth, falling short of forecasts for a rate of 0.2% and below May's reading of 0.3%. Core inflation, which excludes volatile energy and food products, fell to 2.4% year-on-year from 2.6% in May.

Delving into the details underpinning the numbers, the fall was in large part attributed to the decline in global oil prices. Despite forex market participants pushing sterling lower on reduced prospects for a rate rise by the BoE, the numbers could provide some relief to British consumers who have been witnessing their purchasing power decline as a result of elevated inflation after last year's Brexit referendum. Many economists though, expressed their conviction that inflation will reenter a rising path soon. Adding to this, the BoE, which correctly predicted inflation would stand at 2.6% in June, anticipates inflation to peak at 2.8% later in the year. Therefore, the relief on British households, if any, is expected to be short-lived.

Looking at the market's reaction, the pound experienced losses relative to majors including the dollar and the euro upon immediate release of the data. Pound/dollar last traded at 1.3025, down two-tenths of a percent. Before the release of the numbers the pair was trading at 1.3071, while earlier in the day it hit a fresh ten-month high of 1.3125. Euro/pound was last up more than nine-tenths of a percent and close to the day's high of 0.8877. It traded at 0.8815 before the news hit the markets, while it opened below the 0.87 handle.

The BoE's upcoming monetary policy meeting will take place on August 3. During the last meeting in June, three out of eight Monetary Policy Committee members voted for a rate rise. One of them, Kristin Forbes, has since retired from her position as an MPC voting member, but there have been growing voices for a rate hike as of late – including BoE Chief Economist Andrew Haldane, an otherwise known dove, while even Mark Carney, the Bank's Governor made some hawkish comments. Today's data are weakening the case for a rate hike next month, especially if one takes into account the fact that the BoE has so far taken a cautious stance ahead of Brexit negotiations. Economists expect that the British central bank will maintain its official cash rate at the record low of 0.25% throughout the rest of the year.