Sample Category Title

US Health Care Bill Flattened & Risk Off Mode Swings In | CPI and Carney Could Rally For Sterling

- Dollar Weakness Made Aussie Shine

- Carney and CPI Could Make or Break Sterling

- Gold To Break The $1250

The investor sentiment is pessimistic this morning. It is all about the US health care bill and investors have their full focus on this. The Republican health bill has failed to see the daylight and this signifies nothing but a catastrophe for Trump's administration. The profound influence of this disappointment is in the dollar index which plunged to its August lows and the yield on treasuries nudged lower as more senators announced their opposition. Investors are already very dubious in relation to what Trump can deliver or even if he could survive his full term. The fiasco of the health care bill means that the tax reforms or the so-called infrastructure spending plan are in jeopardy.

Dollar Weakness Made Aussie Shine

In the currency market, a number of currencies have rallied against the dollar on the back of this development. The Aussie, yen and the euro rallied overnight and there is still enough momentum there. The Aussie shined the most among other as the central bank confirmed their confidence in the economy. However, they did mention their concern about the outlook for the housing and job industry is still not sturdy.

Carney and CPI Could Make or Break Sterling

As for the British pound, it is the CPI data which would make or break the deal. The forecast is that the prices are probably steady and stayed at 2.9%. But here is an essential bit, even if it stayed as it is, the wage growth is not sufficient to keep up with this. At the same time, you cannot neglect the very fact that the pace of CPI, RPI and PPI has slowed somewhat. Mark Carney, the governor of the Bank of England will be speaking later today and traders are going to watch his comments very closely to see any clues in relation to an upcoming change in the bank's policy. We do not expect him to comment anything meaningful on the monetary policy yet, but it would be arduous to steer clear of this given the hawkish stance of the some MPC members. Therefore, there could be one or two comments buried on this topic.

Gold To Break The $1250

The precious metal, gold is under demand as the risk off mode is in full swing. After suffering some heavy losses mid last week, the rally in the gold price is not losing steam at all. It is highly likely that we could break the resistance of $1250 and target the level of $1300.

DAX Lower As German ZEW Economic Sentiment Slips

The DAX index has posted losses in the Tuesday session. Currently, the DAX is trading at 12,515.00, down 0.57% on the day. On the release front, German ZEW Economic Sentiment dropped to 17.5, short of the estimate of 17.8 points. This marked the key indicator's lowest level in 4 months. The Eurozone ZEW Economic Sentiment also softened, coming in at 35.6 points. This reading missed the forecast of 37.2 points.

The political turmoil continues in the US, as President Trump's troubles are increasing. On Tuesday, the Republicans announced that they will not attempt to advance their health care proposal before Congress takes a recess in August. This decision is a major setback to President Trump, who has tried to pass a health care bill which would replace Obamacare, but opposition from some Republican lawmakers has meant that the White House does not have the votes to pass such a bill. Despite Republican control of both houses of Congress, no major legislation has been passed since Trump took over as president 6 months ago. There is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending.

One of the key stocks on the DAX, Deutsche Bank, is under pressure. Shares dropped 0.91% on Friday and are down 1.8% this week. Germany's largest bank started off the Monday session with losses as well, after the ECB said it was considering implementing ownership-control procedures against the bank's two largest shareholders, Qatar's royal family and HNA, a Chinese conglomerate. The aim of the review is to ensure that an investor is financially stable and untainted by money-laundering or other crimes. If either shareholder fails the test, Deutsche Bank shares would likely fall.

Inflation levels in the US have been stubbornly low, despite a generally strong economy and a tight labor market. Still, the Federal Reserve remains convinced that it's only a matter of time before inflation levels move higher. This stance was reiterated by Fed Chair Janet Yellen last week, as she testified before congressional and senate committees. With the labor market close to capacity and the unemployment rate at just 4.4%, economists are puzzled why this hasn't translated into higher inflation. In her testimony, Yellen admitted that the Fed was at a loss to explain the lack of inflation, but insisted that it was “premature to conclude that the underlying inflation trend is falling well short of 2 percent”, and that with a strong labor market “the conditions are in place for inflation to move up”. Is Yellen's argument just wishful thinking?

US consumer inflation and spending numbers for June were a disappointment. CPI edged up to 0.0%, short of the forecast of 0.1%. There was no relief from Retail Sales, which declined 0.2%, missing the estimate of 0.1%. This marked the third decline in the past four months. Consumer spending accounts for 2/3 of US economic activity, so it's no surprise that weak spending has also meant weak inflation, despite Yellen's claim that low inflation is a temporary phenomenon. The economy had a weak first quarter, with growth of just 1.4%. If the second quarter follows suit, investors could sour on the US dollar.

Daily Technical Analysis: USDCAD Bullish Wedge At D L4 Camarilla

The USD/CAD has rejected perfectly, following my previous USD/CAD analysis. However, at this point the pair is hitting the support zone made from the confluence of D L4, ATR Low and Wedge lower trend line. The price might reject from 1.2600 zone towards 1.2700-1.2715 POC (W L5, D H4, EMA89, ATR high). If we see a rejection and another entry within the POC zone the price should reject and break 1.2600 to the downside. However if we see a break below D L4 that will mean the failure of the bullish wedge and price should proceed towards 1.2550 without retracement to POC.

U.S Dollar In Trouble, Bears In Control

Tuesday July 18: Five things the markets are talking about

The U.S dollar, equities and Treasury yields are all under pressure on signs the American health-care reform bill is effectively dead in its current form as two more Republican Senators (Moran and Lee) are set to vote against it.

Where does this leave President Donald Trump's broader economic revitalization agenda? With Congress expected to continue to work on the bill could delay their next action on the debt ceiling and hinder President Trump's broader economic revitalization agenda.

Latest FX positioning data suggest investors are also turning even more 'bearish' on the dollar with the first U.S. dollar future shorts evident in 13-months. However, the 'carry' trade is flourishing with JPY shorts at its highest level in two-years, after last week's U.S inflation data has dampened expectations of another Fed rate hike in coming months.

1. Global equities under pressure

Ahead of the U.S open, European markets have opened lower, while Asian stocks overnight have basically halted a six-day rally that pushed them to the highest in nine-years.

In Japan, the Nikkei share average fell -0.6%, a one-week low, as a stronger yen (having dropped to trade at a two-week low of ¥111.97 vs. ¥114.495 a week ago) hit cyclical stocks and sliding support for PM Abe added to the negative mood. The broader Topix Index dropped -0.3%.

In Hong Kong, stocks rose for a seventh straight session as gains in the technology and energy sectors offset losses in financial stocks. The Hang Seng Index rallied +0.2%, while down-under, Australia's S&P/ASX 200 Index slid -1.2%.

In China, stocks steadied overnight, the blue-chip CSI300 index rose +0.1%, while the Shanghai Composite Index added +0.3% as investors hunted for bargains after an intense sell-off in small-caps in the previous session.

In Europe, indices have rebounded off earlier lows after a flurry of mixed earnings being reported. A fall in U.K CPI (see below) is supporting the FTSE 100, while earnings again will be the dominant theme in the U.S today – (Goldman Sachs and BoA are due to report).

U.S stocks are set to open little changed.

Indices: Stoxx600 -0.3% at 386, FTSE +0.1% at 7414, DAX -0.4% at 12533, CAC-40 -0.1% at 5222, IBEX-35 +0.2% at 10670, FTSE MIB +0.1% at 21503, SMI +0.4% at 9075, S&P 500 Futures +0.1%

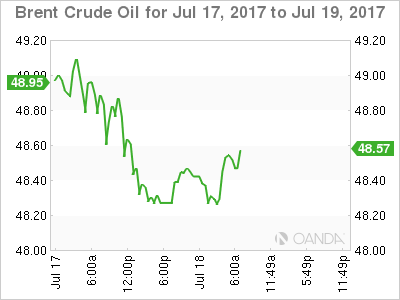

2. Oil steadies as ample supply meets firm demand

Currently, oil markets are trading steady, supported by firm demand, but weighed down by high supplies from OPEC and from shale producers in the U.S.

Benchmark Brent crude is down -10c at +$48.32 a barrel, while U.S. light crude oil (WTI) is -10c lower at +$45.92.

Crude bulls took solace when short-term demand was noted from yesterday's data from China which showed domestic refineries increased crude throughput in June to the second highest on record.

However, with many markets being well supplied, oil for immediate delivery is trading at heavy discounts to forward futures. Net result, crude oil prices are trading at -50% the levels seen three years ago.

Note: Short-term direction will depend on today's U.S API (04:30 pm EDT), and tomorrow's figures from the U.S EIA (10:30 am EDT) and Ecuador's announcement that it will start increasing oil production this month, saying it needs the money.

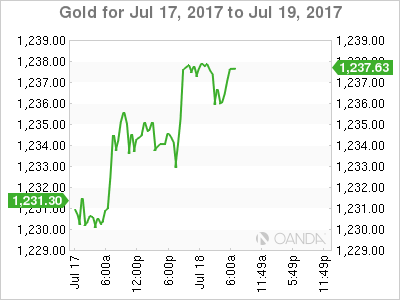

Gold prices have hit a two-week high overnight as the USD falls on fading prospects of an imminent increase to U.S interest rates and expectations of stronger demand from the physical market. Spot gold is up +0.2% at +$1,236.10 an ounce, having touched $1,238.76 in Europe, its highest since July 3.

The price of copper hit a four-month high yesterday after upbeat Chinese economic data dampened fears of a slowdown in the metal's largest market.

Copper for September delivery was up +1.7% at +$2.7355 a pound on the Comex division, the highest level since early March.

3. Yields – 'carry' trades trending

The Reserve Bank of Australia's (RBA) meeting minutes overnight showed that the board spent some time discussing the 'neutral' interest rate, noting that it equated to a neutral nominal cash rate of around +3.5%.

The board also argued that estimates of the neutral real rate suggested that Aussie monetary policy had been clearly 'expansionary' for the preceding five-years. Members also see some probability of an increase in the cash rate by mid-2018. The AUD (A$0.7935) remains better bid on the 'hawkish' view and 'carry' trade.

The market does not expect German Bunds to suffer from bouts of volatility over the rest of the summer, as the ECB is expected to leave policy decisions for September.

Note: The ECB is to meet Thursday (07:45 am EDT) and no change is expected, and no rate hikes before 2019.

Eurozone bond yields have surged since a speech by ECB's Draghi in late June, it was seen as a hint toward QE tapering – 10-year German benchmark is trading at +0.57%.

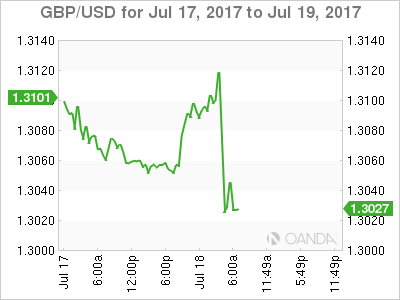

In the U.K, ten-year Gilt yields have slide to +1.24% vs. +1.284%, the lowest in nearly three-weeks after this morning's disappointing CPI data – annual CPI inflation unexpectedly fell to +2.6% in June vs. +2.9% m/m.

Note: It's well above the BoE's +2.0% target, the drop may make policymakers less inclined to hike interest rates, given the squeeze on household incomes as wage growth remains well below inflation.

Ahead of the U.S open, U.S 10-year Treasury yields are down -1 bps to +2.31% after dropping -5 bps last week.

4. U.S dollar in trouble

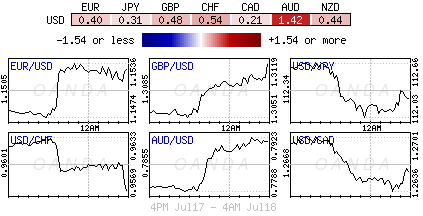

The U.S. dollar is holding at/near 10-month lows outright against some of the majors, while high-yielding currencies such as the AUD (A$0.7934) rallies to two-year peaks as investors pile into leveraged bets.

The pound is under pressure after this morning's lower U.K CPI reading. Sterling is currently trading atop £1.3029 against an otherwise weak dollar, down -0.2% on the day, from around £1.3079 before the data.

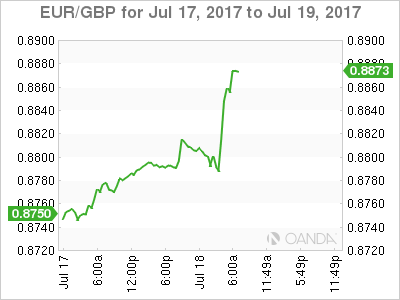

Euro/sterling has rallied +0.6% on the day to €0.8848, up from €0.8811 beforehand. The EUR/USD approached the ¥1.1553 area before consolidating.

Dealers note that ECB chief Draghi faces a difficult challenge of preparing investors/market for a 'gradual' change in the monetary policy while, at the same time, preventing yields from continuing to surge excessively (German yields have moved from +0.25% to +0.58% since Draghi's June speech).

5. German economic sentiment

The ZEW indicator of economic sentiment for Germany fell slightly last month (-1.1 points) and now stands at 17.5 points.

Note: The headline indicator remains below the long-term average of 23.8 points.

The assessment of the current economic situation fell by -1.6 points in July, but remains at a high level of 86.4 points.

This morning's headlines suggest that the medium term outlook for German economic growth continues to be positive.

Technical Outlook: Spot Gold – Strong Barrier At $1239 Holds Bulls For Now

Spot Gold holds firm tone on Tuesday and extends rally into third straight day. Fresh extension of the third wave of five-wave cycle from $1204 (10 July low), broke above its FE100% at $1236 and touched strong resistances at $1239 (double Fibonacci resistance, 38.2% of $1296/$1204 descend and 61.8% of $1258/$1204 bear-leg).

The price may show hesitation here and enter narrow consolidation, ahead of fresh attempts higher. Sustained break above $1239 pivot would open way towards $1246/47 (55 / 100SMA) which formed bear-cross and provide downside pressure.

On the downside, broken 20SMA offers initial support at $1233 (also session low), followed by broken 200SMA / hourly cloud top ($1230), which is expected to contain dips and keep near-term bulls in play.

Res: 1239, 1242, 1244, 1246

Sup: 1233, 1230, 1225, 1221

Kiwi Tumbles As Inflation In New Zealand Comes Weaker Than Forecast

After a robust pace in the first quarter of the year, inflation in New Zealand lost steam in the second quarter, rising less than expected. Since the newly released data indicated that consumer prices are not going to pick up soon, the Reserve Bank of New Zealand will be in no rush to raise interest rates in the short-term. Meanwhile, the kiwi fell below the $0.7300 key level in the Asian session following the CPI figures but managed to recover immediately.

Based on calculations from the Statistics New Zealand, consumer prices of goods and services in the country remained unchanged within the second quarter, missing the forecast of 0.2% growth. In the first quarter, inflation grew by 1%, the highest percentage increase since 2011. Despite food prices continuing to rise, lower transport costs offset this increase. On a yearly basis, prices slowed from 2.2% to 1.7% in the second quarter and were below expectations of 1.9%.

Eyes will now focus on the next RBNZ meeting on August 10, where policymakers will gather to decide on the cash rate. In their last meeting in May, the RBNZ kept rates steady at 1.75% and showed no intention to hike rates in the upcoming months as they characterized the recent steep increase in inflation as temporary due to volatility in energy and food prices. Although headline inflation was within the RBNZ’s target of 1-3%, the latest CPI numbers are expected to give fewer incentives to policymakers to adjust their accommodative monetary policy.

The release of the data sent the kiwi against the greenback immediately down by 0.80%, near to a one-week low of $0.7262, from $0.7320 traded earlier in the Asian session. However, the currency bounced back, recouping all its losses before the end of the session on the back of a weaker US dollar.

Market Update – European Session: UK Inflation Pulls Back In The Wake Of Sterling’s Recent Rebound

Notes/Observations

UK Jun CPI comes in below expectations (YoY: 2.6% v 2.9%e) but still above BOE target for 5th straight month

Reform momentum of the Trump administration has received another blow as 4 GOP Senators have rejected the recent proposal of the Obamacare Repeal Act

Broad based USD weakness taken hold in wake of US health care bill problems; means a delay to dealing with debt ceiling, Art of the Deal' has not worked so far in US politics (Six months in office and with no major legislation signed into law)

Overnight

Asia:

New Zealand Q2 CPI Q/Q: 0.0% v 0.2%e; Y/Y: 1.7% v 1.9%e

Reserve Bank of Australia (RBA) July Policy Meeting Minutes: current economic conditions in Australia, and the outlook for growth and inflation, meant that developments in the labor and housing markets continued to warrant careful monitoring. Steady policy stance consistent with growth/inflation targets

China PBOC affirms monetary policy to be prudent and neutral; to strengthen macro-prudential management and counter cycle adjustments; Vows to prevent systemic financial risks

Bank of Japan (BOJ) sustainability of exchange-traded funds (ETFs) said to raise concerns among some officials but saw no need for immediate action

Americas:

Two Republican senators join opposition to revised healthcare bill and delivering a serious blow to the legislation

McCain's surgery may be more serious than thought, sparking fears among Republicans over fate of Trumpcare

Energy:

Ecuador Oil Min Perez: Will be unable to honor its OPEC pledge to cut output by 26k b/d through March; planning a gradual production increase

Economic Data

(ES) Bank of Spain: May non-performing loans Ratio at 8.7% v 8.9% m/m

(UK) Jun CPI M/M: 0.0% v 0.2%e; Y/Y: 2.6% v 2.9%e; CPI Core Y/Y: 2.4% v 2.6%e; CPIH Y/Y: 2.6% v 2.7%e

(UK) Jun RPI M/M: 0.2% v 0.4%e; Y/Y: 3.5% v 3.6%e; RPI Ex Mortgage Interest Payments (RPIX) Y/Y: 3.8% v 3.8%e prior, Retail Price Index: 272.3 v 272.7e

(UK) Jun PPI Input M/M: -0.4% v -0.9%e; Y/Y: 9.9% v 9.4%e

(UK) Jun PPI Output M/M: 0.0% v 0.1%e; Y/Y: 3.3% v 3.4%e

(UK) Jun PPI Output Core M/M: 0.2% v 0.1%; Y/Y: 2.9% v 2.8%e

(UK) May ONS House Price Index Y/Y: 4.7% v 3.0%e

(HK) Hong Kong Jun Unemployment Rate: 3.1% v 3.2%e

(DE) July Zew Current Situation Survey: 86.4 v 88.0e; Expectation Survey: 17.5 v 18.0e

(EU) Euro Zone July Zew Expectations Survey: 35.6 v 37.7 prior

Fixed Income Issuance:

(EU) EFSF opened book to sell EUR-denominated 2027 and 2056 bonds

(SE) Sweden opened its book to sell $2.75B in 2-year notes; guidance seen -6bps to mid-swaps

(ES) Spain Debt Agency (Tesoro) sold total €2.985 vs. €2.5-3.5B indicated rangein 3-month and 9-month Bills

(ID) Indonesia sold total IDR7.12T vs. IDR target in 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 386, FTSE +0.1% at 7414, DAX -0.4% at 12533, CAC-40 -0.1% at 5222, IBEX-35 +0.2% at 10670, FTSE MIB +0.1% at 21503, SMI +0.4% at 9075, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European Indices have rebounded off earlier lows after a flurry of earnings notably from Ericsson which reported results which fell short of estimates. Lufthansa, Puma, Software Ag reported preliminary results, whilst Novartis beat on both the top and bottom line helping the Swiss SMI outperform. Earnings will continue to be the dominant them in the US morning with Goldman Sachs, JNJ and Bank of America all due to report.

Equities

Consumer discretionary [Lufthansa [LHA.DE] -2.0% (Prelim results), Puma [PUM.DE] +1.2% (prelim results), Royal Mail [EMG.UK] +2.9% (Q1 update), Zalando [ZALG.DE] -7% (prelim Q2)]

Materials: [Rio tinto [RIO.UK] -1.2% (Cuts outlook)]

Financials: [ IG Group [IGG.UK] +9.0% (Trading update), Gecina [GFC.FR] -1.2% (rights issue)]

Technology: [Software Ag [SOW.DE] flat (prelim Q2)]

Telecom: [Ericsson [ERICB.SE] -10% (Earnings, cost cuts)]

Healthcare: [Novartis [NOVN.CH] +2.2% (Earnings)]

Speakers

Sweden Central Bank (Riksbank) July Minutes: Several members stress that important that inflation was sustained close to 2%. International developments had improved (in-line with expectations). Government bond purchases to continue during H2

Gov Ingves: Important that future rate hikes were not pre-empted. Inflation just touching 2% short-term was not stable enough

Member Skingsley: Still signs that inflation to remain low

Member AF Jochnick: Likelihood of further cuts has decreased

German ZEW Economists noted that the outlook for German economic growth continued to be positive

ECB Bank Lending Survey: Net demand for business loans expected to increase in Q3. Banks expected easing of credit standards for business loans in Q3

Japan Chief Cabinet Sec Suga: Strong economic growth more important than a temporary deficit cut; reiterates govt view that strive for primary balance

Currencies

The European session began with broad based USD weakness in wake of US health care bill problems. Reform momentum of the Trump administration had received another blow as 4 GOP Senators have rejected the recent proposal of the Obamacare Repeal Act. EUR/USD approached the 1.1540 area before consolidating. Dealers noted that ECB chief Draghi faced the challenge of preparing markets for a gradual change in the monetary policy while, at the same time, preventing yields from continuing to surge excessively

The GBP saw its early advance dissipate after UK Jun CPI came in below expectations (YoY: 2.6% v 2.9%e). UK inflation pulled back" in the wake of sterling's recent rebound. Although the data remained above BOE target for 5th straight month dealers took note that it might have seen its peak in May. GBP/USD holding around 1.3030 after testing 1.3120 earlier in the session.

Fixed Income

Bund futures trade at 161.55 up 17 ticks and back towards the middle of July's trading range. Resistance lies near the 162.10 level followed by 162.75. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 125.87 higher by 45 ticks following softer inflation data. Price finds key support at the 125.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.00 region, followed by 126.72.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.656T a drop of €13B from €1.669T prior. Use of the marginal lending facility fell to €60M from €192M prior.

Corporate issuance saw $18.55B come to market via 8 issuers headlined by Citigroup $5.75B 3-part senior unsecured offering and JP Morgan $4B 2-part senior unsecured note offering

Looking Ahead

05:30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

06:00 (TR) Turkey to sell 2022, 2027 bonds (3 tranches)

06:30 (EU) ESM to sell €1.5B in 6-Month Bills

06:45 (US) Daily Libor Fixing

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (HU) Hungary Central Bank (NBH) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

08:00 (PL) Poland Jun Employment M/M: 0.2%e v 0.0% prior; Y/Y: 4.3%e v 4.5% prior

08:00 (PL) Poland Jun Average Gross Wages M/M: +1.6%e v -2.2% prior; Y/Y: 5.0%e v 5.4% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) May Import Price Index M/M: -0.2%e v -0.3% prior; Y/Y: 1.3.%e v 2.1% prior; Import Price Index (ex-petroleum) M/M: 0.2%e v 0.0% prior

08:30 (US) May Export Price M/M: 0.1%e v -0.7% prior; Y/Y: No est v 1.4% prior

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves:

09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement

09:30 (UK) BOE Gov Carney introduces new 10 pound note

10:00 (US) July NAHB Housing Market Index: 67e v 67 prior

11:30 (US) Treasury to sell 4-Week and 52-week Bills

16:00 (US) May Total Net Tic Flows: No est v $65.8B prior; Long-Term Tic Flows: No est v $1.8B prior

16:30 (US) Weekly API Oil Inventories

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

Majors started the week in slow motion, as a holiday in Japan, combined with a scarce macroeconomic calendar, sent investors to the sidelines ahead of first tied data to be released later this week, including among others, the ECB monetary policy decision. The American dollar closed mixed, although not far from its Friday's closing levels and looking vulnerable across the board. The EUR/USD pair fell to a daily low of 1.1434, but recovered towards its recent highs near 1.1490, ending the day a few pips below this last. In the data front, EU June inflation was confirmed at 1.3% yearly basis, down from 1.4% in May, remaining unchanged in the month. In the US, the Empire State manufacturing survey showed that business activity grew by less than expected in July, with the index down to 9.8 from 19.8 in July and the expected 15.0.

From a technical point of view, the pair retains its long-term positive tone, but remains unable to confirm a bullish breakout, still struggling around 1.1460, from where the pair retreated multiple times since January 2015. In the 4 hours chart, the pair met buying interest on an approach to a flat 20 SMA, while the RSI indicator aims higher, currently around 63, but the Momentum lost upward strength, holding anyway within positive territory. An upward acceleration through 1.1490 should see an upward extension towards 1.1615 May 2016 high, while beyond this last the next level to watch is 1.1713, August 2015 high.

Support levels: 1.1420 1.1380 1.1340

Resistance levels: 1.1490 1.1525 1.1560

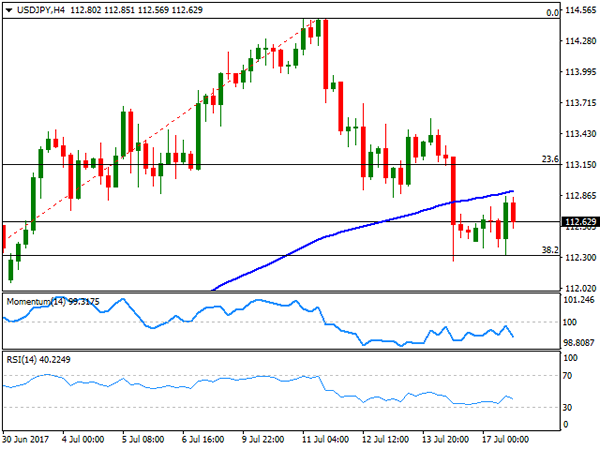

USD/JPY

The USD/JPY pair posted a modest advance this Monday, ending the day at 112.63, and having met selling on an advance up to its 200 DMA, around 112.90. The JPY saw little action at the beginning of the week as Japan banks were closed on a local holiday, with the main event scheduled for this week being the BOJ's monetary policy meeting early Thursday, but no big surprise is expected from Kuroda this time. US Treasury yields traded marginally lower daily basis, indicating a possible yen recovery for the upcoming sessions. In the meantime, the pair continues finding support around 112.30, the 38.2% retracement of the latest bullish run, and below the mentioned 200 DMA, with the scale lean towards the downside. In the 4 hours chart, the early advance was unable to surpass a still bullish 20 SMA, while technical indicators have retreated from their mid-lines, supporting a bearish extension on a break below the mentioned Fibonacci support and with scope then to test the 111.60 region.

Support levels: 112.30 111.90 111.60

Resistance levels: 112.90 113.20 113.50

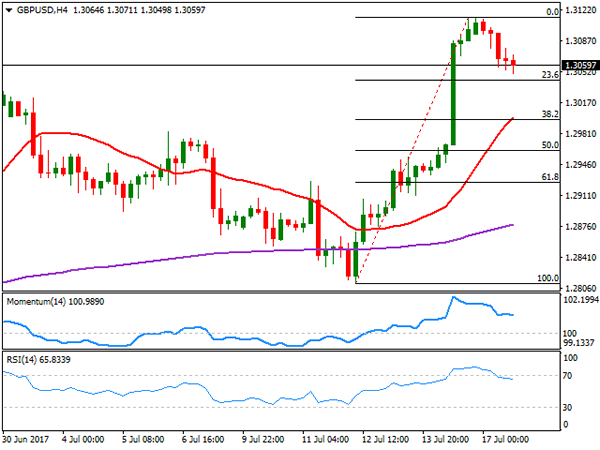

GBP/USD

The GBP/USD pair gave back some of its Friday's gains, but closed anyway well above the 1.3000 level. There were no relevant macroeconomic releases in the UK, but things will get more interesting in that front this Wednesday, with the release of inflation at consumer and factory levels for June. Additionally, BOE's Governor Mark Carney is due to unveil the new £10 note featuring Jane Austen, in Hampshire, and while he will probably offer a speech, seems unlikely he will discuss monetary policies in such event. From a technical point of view, the intraday decline remains as corrective, as price remains above the 23.6% retracement of its latest bullish run from 1.2811 to 1.3113 at 1.3040, the immediate support and the level to break to confirm further declines during the upcoming sessions. In the 4 hours chart, technical indicators have corrected extreme overbought conditions, heading modestly lower within positive territory, whilst the 20 SMA maintains its bullish slope below the current level, converging with the 38.2% retracement of the mentioned rally at 1.2295, a probable bearish target in the case of further Pound's weakness.

Support levels: 1.3050 1.3010 1.2965

Resistance levels: 1.3120 1.3160 1.3200

GOLD

Gold prices continued advancing this Monday, with spot surging to $1,234.52, its highest since June 3rd, still backed by speculation that the US Federal Reserve will likely have to pause its rising rate policy after one more hike this year. Despite the US released just a minor manufacturing reading, the NY Empire State index, the disappointing number was enough to feed demand for the base metal. The daily chart shows that the price advanced above a still bearish 20 DMA, while holding well below the 100 DMA, this last around 1,258.00, while technical indicators have advanced within negative territory, nearing their mid-lines, suggesting that the commodity may extend its advance on Tuesday. In the 4 hours chart, the price has advanced above its 20 and 100 SMAs, with the shortest advancing below the largest, whilst technical indicators have turned flat after entering overbought territory, maintaining the risk towards the upside.

Support levels: 1,228.30 1,216.60 1,208.30

Resistance levels: 1,236.50 1,242.50 1,251.90

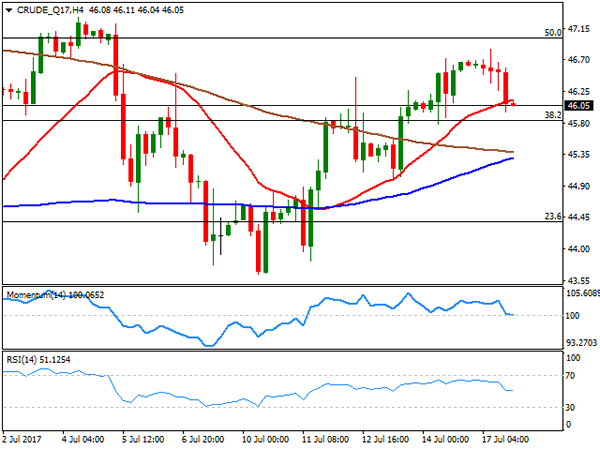

WTI CRUDE OIL

West Texas Intermediate crude oil futures trimmed all of its Friday's gains, closing the day at $46.05 a barrel, undermined by speculation of a monthly raise in US shale-oil production. The black gold advanced up 46.85 intraday, stalling short of the 50% retracement of its latest decline between 51.98 and 42.04 at 47.00, now nearing the 38.2% retracement of the same rally at 45.90, the immediate support. In the daily chart, the 20 DMA maintains its bullish slope below the current level, but technical indicators turned lower and are currently crossing their mid-lines towards the downside, indicating a possible bearish extension ahead, particularly on a break below the mentioned support. In the 4 hours chart, he price is a few cents below its 20 SMA, whilst technical indicators also retreated from near overbought readings towards their mid-lines where they lost bearish strength, also indicating that a bearish extension is likely on a break below the mentioned key support.

Support levels: 45.90 45.20 44.60

Resistance levels: 46.60 47.20 47.70

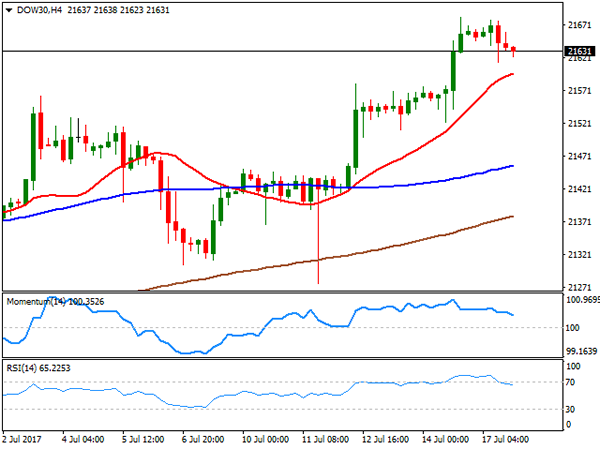

DJIA

US indexes closed mixed, but little changed this Monday, with only the Nasdaq Composite posting a modest advance of 2 points, to close at 6,314.43. The Dow Jones Industrial Average closed at 21,629.72, down by 8 points, whist the S&P ended at 2,459.14, down 0.01%. Ahead of big earnings reports releases later this week, the indexes hold near record highs, boosted by hopes that the US Federal Reserve will have to slow its tightening pace. Within the Dow, Microsoft led advancers with a 0.78% gain, while the worst performer was JP Morgan that closed down 0.98%. The daily chart shows that the index remains far above all of its moving averages that maintain their bullish slopes, whilst technical indicators have retreated modestly, holding anyway near overbought readings. In the 4 hours chart, the 20 SMA heads north around 21,596 while technical indicators corrected overbought readings, but remain well above their mid-lines, suggesting the index may correct lower short-term, within a dominant bullish trend.

Support levels: 21,628 21,576 21,531

Resistance levels: 21,682 21,735 21,780

FTSE100

The FTSE 100 closed 25 points higher at 7,404.13, lifted by gains in the mining sector and a weaker Pound. Mining-related equities got a boost from positive news coming from China, with most big names, as Anglo American, Glencore, and BHP Billiton adding over 1%. The best performer, anyway, was Ashtead Group that added 3.42%. Imperial Brands was the worst performer, down 1.63%, followed by Experian that lost 1.51%. In the meantime, over 40% of businesses in the UK said that fears over the UK's future relationship with the EU after the Brexit has affected their investment decisions, according to a CBI survey, somehow anticipating that the latest recovery won't see follow through during the upcoming sessions. In the daily chart, the index has closed the day around a bearish 20 DMA, while technical indicators maintain a neutral stance, hovering directionless around their mid-lines. In the 4 hours chart, the outlook is also neutral, as the index is a few points above a bullish 20 SMA, while technical indicators turned lower around their mid-lines, with no clear directional strength.

Support levels: 7,362 7,333 7,304

Resistance levels: 7,413 7,439 7,482

DAX

European equities closed mixed, with the German DAX down 44 points or 0.35%, to 12,587.16. Most sectors closed lower, with only eight members up, led by Deutsche Lufthansa that added 2.28%, after the company reported earnings before interest and taxes of €1,042 million in the first half of 2017. Deutsche Boerse was the worst performer, ending the day 1.53% lower, followed by Merck that lost 1.50%. The daily chart for the index shows that it retreated towards its 20 DMA that presents a modest bearish slope, while the 100 and 200 DMAs remain well below the shortest, whilst technical indicators hover around their mid-lines, with no clear directional strength. In the 4 hours chart, the index settled above all of its moving averages, now a few points below a bullish 20 SMA, whilst technical indicator extended their slides, with the Momentum indicator having entered negative territory and the RSI indicator around 52. The index could extend its decline on a break below 12,542, Friday's low, and a strong static support area, as it presents multiple intraday highs and lows around the level in the past few weeks.

Support levels: 12,541 12,488 12,432

Resistance levels: 12,621 12,665 12,710

GOLD Short-Term Bullish Momentum Continues, SILVER Consolidating After Strong Increase, CRUDE OIL Upside Pressures Are Growing

GOLD Short-term bullish momentum continues.

Gold's is trading higher after the precious metal reached the $1200 level. Hourly support is now given at $1204 (10/07/2017 high). Hourly resistance lies at 1238 (18/07/2017 high). Expected to show further strengthening.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

SILVER Consolidating after strong increase.

Silver is consolidating after the bounce still bouncing from hourly support given at 15.18 (10/07/2017 low). Key resistance is given at a distance at 17.75 (06/06/2017 high). The road seems wide open for renewed weakness in case the commodity remains around $16.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Upside pressures are growing.

Crude Oil is trading higher. Hourly support is given at 43.65 (10/07/2017 low). Expected to monitor resistance given at 47.32 (04/07/2017).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

Euro Punches Above 1.15 On Trump Troubles

The euro has posted gains in the Tuesday session. Currently, EUR/USD is trading at 1.1560. On the release front, German ZEW Economic Sentiment dropped to 17.5, short of the estimate of 17.8 points. The Eurozone ZEW Economic Sentiment also softened, coming in at 35.6 points. This reading missed the forecast of 37.2 points. There are no major US events on the schedule. On Wednesday, the focus will be on construction data, with the release of Building Permits and Housing Starts.

The euro has pushed above the 1.15 line and is trading at its highest levels since May 2016. The currency received a boost on Tuesday, following the news that the Republicans will not attempt to advance their health care proposal before Congress takes a recess in August. This decision is a major setback to President Trump, who has tried to pass a health care bill which would replace Obamacare, but opposition from some Republican lawmakers has meant that the White House does not have the votes to pass such a bill. Despite Republican control of both houses of Congress, no major legislation has been passed since Trump took over as president 6 months ago. There is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending.

Inflation levels in the US have been stubbornly low, despite a generally strong economy and a tight labor market. Still, the Federal Reserve remains convinced that it’s only a matter of time before inflation levels move higher. This stance was reiterated by Fed Chair Janet Yellen last week, as she testified before congressional and senate committees. With the labor market close to capacity and the unemployment rate at just 4.4%, economists are puzzled why this hasn’t translated into higher inflation. In her testimony, Yellen admitted that the Fed was at a loss to explain the lack of inflation, but insisted that it was “premature to conclude that the underlying inflation trend is falling well short of 2 percent”, and that with a strong labor market “the conditions are in place for inflation to move up”. Is Yellen’s argument just wishful thinking? The markets aren’t buying in, with a rate hike considered extremely unlikely in September. As for a December increase, the odds are currently at just 47%, according to the CME Group. Consumer spending and inflation numbers were soft in June, and the disappointing numbers will do little to improve market skepticism about one last rate hike this year.