Sample Category Title

Daily Technical Analysis: EUR/USD Continues Uptrend After Major Break Above 1.15 Resistance

Currency pair EUR/USD

The EUR/USD uptrend is ready to continue higher now that price has broken above the resistance trend line (dotted red) and 1.15 round level. The bullish breakout confirms the continuation of the wave 3 (green).

The EUR/USD is most likely building a wave 3 (orange) momentum. Within the 3rd wave price seems to be extending the bullish impulse via 5 waves (purple) within the 5th wave (grey). A small retracement could occur now or later as part of the wave 4 (purple) and the Fibonacci levels of wave 4 vs 3 could act as potential support for a new bounce towards the Fibonacci targets of wave 3 vs 1.

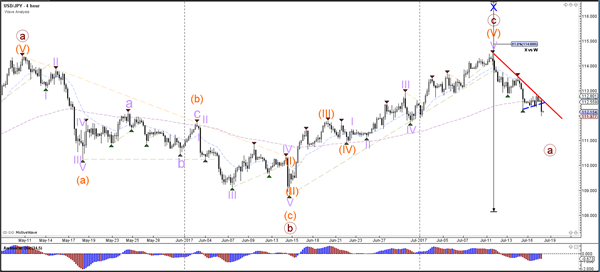

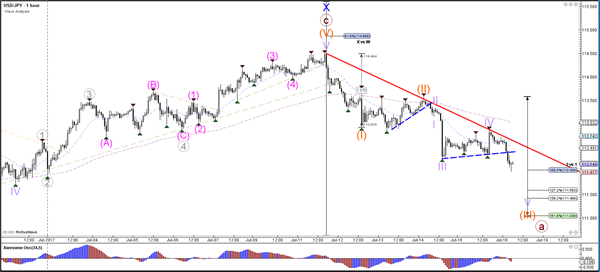

Currency pair USD/JPY

The USD/JPY continuation of the bearish momentum is increasing the chance of a bearish reversal and the completion of a wave X (blue) at the top.

The USD/JPY indeed turned at the resistance trend line (red) which confirmed the wave 4 (purple). The break below the support trend line (dotted blue) could indicate the potential for USD/JPY to move lower towards the Fibonacci targets.

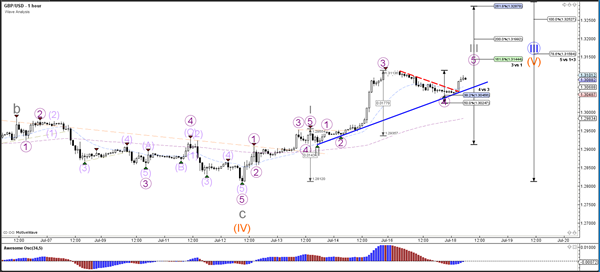

Currency pair GBP/USD

The GBP/USD is continuing with the uptrend after the break above the 1.30 resistance level (dotted red). The Fibonacci levels of wave 5 (orange) are the next targets.

The GBP/USD completed a retracement to the 338.2% Fibonacci support level of wave 4 vs 3 (purple) and used the support for a bullish bounce. The bullish breakout above resistance (dotted red) will probably start the wave 5 (purple) of wave 3 (grey).

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push lower yesterday bottomed at 1.1434 but closed higher at 1.1477 and breaks above 1.1500, hit 1.1532 earlier today in Asian session. The bias remains bullish in nearest term testing 1.1615 region (weekly EMA 200 and 2016 high). Immediate support is seen around 1.1485/65 area. A clear break below that area could lead price to neutral zone in nearest term testing 1.1400 support area but as long as stay above 1.1285 key support I remain bullish and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break above 1.1615 would expose 1.1712 region (2015 high).

GBPUSD

The GBPUSD was corrected lower yesterday but overall still maintain its bullish bias and able to stay above 1.3050 key support so far. The bias remains bullish in nearest term testing 1.3200 area. Immediate support is seen around 1.3050 region. A clear break back below that area could lead price to neutral zone in nearest term testing 1.3000 region. On the upside, a clear break and daily close above 1.3200 would expose 1.3350 area.

USDJPY

The USDJPY was indecisive yesterday but overall still able to maintain its bearish short-term bias and hit 112.15 earlier today in Asian session. The bias remains bearish in nearest term as a part of the bearish scenario after the appearance of the bearish pin bar last week, testing 111.45 region (daily EMA 200). Immediate resistance is seen around 112.75. A clear break above that area could lead price to neutral zone in nearest term testing 113.50 region. On the downside, a clear break and daily close below 111.45 would expose 111.30/00 area. Overall I am neutral on this pair.

USDCHF

The USDCHF was indecisive yesterday but traded lower earlier today in Asian session hit 0.9589. The bias remains bearish in nearest term testing 0.9550 – 0.9450 area which remains a key support and good place to buy with a tight stop loss below 0.9450. Immediate resistance is seen around 0.9635. A clear break above that area could lead price to neutral zone in nearest term retesting 0.9700 region. As you can see on my daily chart below, price is still moving below the daily EMA 200 suggests a bearish view with key resistance seen at 0.9700 – 0.9765 region. On the downside, a clear break below 0.9450 would expose 0.9250 area.

USDJPY Bearishness Set To Extend

Key Points:

- The Dollar-Yen should sink below the 100 day EMA this week.

- Numerous technical readings support further losses.

- Downsides should be limited to the 110.00 handle.

Further losses are looking more and more likely for the Dollar-Yen this week as its technical outlook remains stubbornly bearish. Indeed, we expect the pair to sink through the 100 day moving average to test support around the 110.00 handle within the next week or so. This being said, the greenback has been anything but predictable recently which could mean a reversal is not altogether improbable.

Nevertheless, on the balance of things, the argument for such a reversal is fairly flimsy. The main thing one might point out is the fact that the EMA bias is highly bullish and that the 100 day moving average can often prove to be a source of dynamic support. Unfortunately for the bulls out there, the USDJPY has been oscillating around the 100 day EMA rather comfortably and ignoring any potential support or resistance that it could be generating. Moreover, the pair has yet to move into oversold territory and the next potential zone of support is the 50.0% Fibonacci level – often one of the softer retracements.

Conversely, the evidence for ongoing losses is actually fairly compelling and suggests that the pair could depreciate by as much as 1.50% in the near term. Specifically, the parabolic SAR is notably bearish and in little danger of inverting in the absence of a major fundamental upset. Meanwhile, the recent crossover of the MACD and the signal line tends to indicate that momentum has shifted which could put heightened pressure on the pair.

Nevertheless, whilst losses are expected moving forward, they are likely to be somewhat limited. More precisely, we can't ignore the presence of the broader pennant structure which should prevent the pair from pushing below the 110.00 handle. This view is only reinforced by the fact that the 78.6% Fibonacci level exists just above this handle at the 110.28 mark which severely limits the chances of us seeing a downside breakout from the USDJPY.

Overall, keep an eye on this pair as even though it remains within a consolidation phase, it has plenty of movement left. For now, the movement looks predisposed to the downside for the reasons discussed above. However, don't forget to keep half an eye on the fundamental side of things as this still has the ability to disrupt the so far orderly decline of the Dollar-Yen.

Is A Higher Aussie Dollar Complicating Rebalancing?

Key Points:

- AUDUSD continues to appreciate thereby complicating economic rebalancing.

- Nominal real interest rates have continued to decline towards 1.00%.

- RBA unlikely to undertake monetary policy action in the near term.

The Australian Dollar has seen a stunning run over the past few weeks as the currency pair has been buoyed by a range of increasingly negative U.S. economic data. In particular, a softening in the Fed’s position regarding rate hikes has seen capital flowing into the AUD and, subsequently, price action has risen to presently trade around the 0.7843 mark. However, this could be complicating the path of rebalancing for the economy and might trouble the Reserve Bank in the coming months.

The fact is that the Australian economy is still somewhat reeling from the impact of the end of the commodity super cycle. In fact, the rebalancing process from mining to service based industries is still ongoing and reduced trade competition, based on an appreciating currency, is likely the last thing that the reserve bank needs to deal with right now.

However, it isn’t all bad news for the central bank with the latest round of minutes suggesting that the recent rises in employment are likely to support an improvement in the household income and spending. This is most certainly n economic silver lining, despite the appreciating Australian Dollar, especially given that the RBA is estimating that the neutral real interest rate has fallen to 1.00%. Additionally, Unemployment continued to trend lower and the latest projections seem to suggest that the rate will move towards 5.0% over the next 18 months.

However, despite ongoing tightening within the labour markets, along with increasing inflationary pressures, the RBA is unlikely to take anything in the way of monetary policy action in the coming months. Although there is a broad trend of various central banks moving towards a tightening phase, Australia is unlikely to be one of them in the remainder of 2017. In fact, the coming year is likely to bring with it renewed expansionary fiscal policy which would likely cancel out any tightening. Subsequently, the RBA is likely to sit on the side lines in the coming month especially if they believe that the government will undertake a fiscal expansion in the near future.

However, the Australian economy is continuing to do relatively well considering the sharp domestic shock the end of the mining boom posed. Regardless, the RBA is unable to retain rates at the presently low level for too long lest they worsen much of the capital and lending issues within the banking sector whilst also encouraging further risky leveraging. Ultimately, the time will come for the central bank to take action and this can only occur after a significant rebalancing within the economy.

Economic Outlook Remains Positive: RBA July Meeting Minutes

For the 24 hours to 23:00 GMT, the AUD declined 0.27% against the USD and closed at 0.7801.

LME Copper prices rose 1.8% or $107.5/MT to $5965.5/MT. Aluminium prices declined 0.2% or $3.0/MT to $1901.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7885, with the AUD trading 1.08% higher against the USD from yesterday’s close, after minutes of the Reserve Bank of Australia’s (RBA) July meeting indicated officials offered an optimistic assessment of the Australian economy.

Minutes noted that policymakers remained upbeat over the health of the Australian economy, as the nation’s labour market, public investment and retails sales showed signs of gradual improvement. Further, it revealed that officials now expect a cash rate of 3.5% to keep inflation in check and growth at reasonable levels.

The pair is expected to find support at 0.7816, and a fall through could take it to the next support level of 0.7746. The pair is expected to find its first resistance at 0.7925, and a rise through could take it to the next resistance level of 0.7964.

Going ahead, Australia’s Westpac leading index for June, due to release in the early hours’ tomorrow, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Growth Slowed To A 6-Month Low In June

For the 24 hours to 23:00 GMT, the EUR rose 0.19% against the USD and closed at 1.1483.

On the macro front, the Euro-zone's final consumer price index (CPI) advanced 1.3% on an annual basis in June, confirming the preliminary print indicating the slowest increase in six months. The CPI had registered a gain of 1.4% in the prior month.

In the US, data showed that the New York Empire State manufacturing index fell more-than-expected to a level of 9.8 in July, after recording a two-year high level of 19.8 in the prior month, while market participants were expecting a drop to a level of 15.0.

In the Asian session, at GMT0300, the pair is trading at 1.1530, with the EUR trading 0.41% higher against the USD from yesterday's close, after two more Republican senators expressed their disagreement to repeal and replace Obamacare with Republican health-care bill, raising fresh questions about the US President, Donald Trump's ability to fulfil his policies.

The pair is expected to find support at 1.1464, and a fall through could take it to the next support level of 1.1398. The pair is expected to find its first resistance at 1.1567, and a rise through could take it to the next resistance level of 1.1604.

Moving ahead, investors will focus on the release of ZEW survey of economic sentiment for July across the Euro-zone, slated to release in a few hours. Moreover, the US NAHB housing market index for July, set to be released later in the day, will also grab market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Second Round Of Formal Brexit Talks Begun

For the 24 hours to 23:00 GMT, the GBP declined 0.35% against the USD and closed at 1.3056, after reports of political quarrels in the British government sparked concerns that discord within the government could make it difficult to secure a good deal with the European Union (EU).

Meanwhile, the Brexit Secretary, David Davis and EU’s chief negotiator, Michel Barnier, kicked off four days of talks to settle Brexit terms.

In the Asian session, at GMT0300, the pair is trading at 1.3087, with the GBP trading 0.24% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3054, and a fall through could take it to the next support level of 1.3022. The pair is expected to find its first resistance at 1.3112, and a rise through could take it to the next resistance level of 1.3138.

Trading trend in the Pound today will be determined by the release of Britain’s crucial inflation data for June, set to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD slightly declined against the JPY and closed at 112.60.

In the Asian session, at GMT0300, the pair is trading at 112.15, with the USD trading 0.4% lower against the JPY from yesterday's close.

The pair is expected to find support at 111.86, and a fall through could take it to the next support level of 111.58. The pair is expected to find its first resistance at 112.65, and a rise through could take it to the next resistance level of 113.16.

Amid a lack of major economic releases in Japan today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.24% against the CHF and closed at 0.9620.

In economic news, Switzerland’s total sight deposits inched up to a level of CHF578.9 billion in the week ended 14 July, from CHF578.7 billion reported in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9597, with the USD trading 0.24% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.957, and a fall through could take it to the next support level of 0.9544. The pair is expected to find its first resistance at 0.9641, and a rise through could take it to the next resistance level of 0.9686.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Existing Home Sales Declined By The Most Since 2010 In June

For the 24 hours to 23:00 GMT, the USD rose 0.26% against the CAD and closed at 1.2688.

The Canadian Dollar fell against the USD, after data showed that Canada's existing home sales dropped 6.7% on a monthly basis in June, posting its largest monthly drop since 2010 and following a decline of 6.2% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2655, with the USD trading 0.26% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2622, and a fall through could take it to the next support level of 1.2588. The pair is expected to find its first resistance at 1.2695, and a rise through could take it to the next resistance level of 1.2734.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.