Sample Category Title

AUD/USD Tumbles Amid Dovish RBA

RBA backs away from reflation trend

As expected, the Reserve Bank of Australia kept its cash rate unchanged at 1.50%. Despite the widely-held view for no change, there was still a level of disappointment that the RBA refrained from discussing “normalisation” or offering a hawkish lean. We see this meeting as a warning to other central banks normalisation bull, such as those in CAD not to get too far ahead of economic data.

Governor Lowe acknowledged pick-up in external growth dynamics and improvement in domestic economy. The central bank removed the reference to GDP expanding slightly above 3% suggesting that growth forecast could be revised lower. The RBA noted that the inflation rate has fallen in response to weaker crude prices and stagnating wage growth. We see the RBA maintaining a neutral tone for the near-term as increasing household debt without catchup from wage growth could threaten financial stability should the RBA start tightening.

We remain bearish on AUD as believe the market is overpricing the central bank's rush to reflation story and rising funding cost will remove the AUD shine.

Sweden's bellwether of reflation story

Following the RBA failure to change bias, the Riksbanks monetary policy meeting will be closely watched for an expected shift in policy tone. We view this thinking because of recent ECB and BoE language rather than purely the result of improving economic data. While incoming data has been broadly positive, we doubt the time has come to revive the reflation story.

The Riksbanks will play a critical role in rejecting or confirming the monetary policy divergence theme. Recently, a Governing Council member stated that QE was less effective, increasing the likelihood that the central bank removes hints of additional QE measures. While this is a mildly hawkish adjustment, we doubt it will have severe consequences for SEK strength.

Switzerland retail sales declined less than expected

The Swiss franc is still trading below 1.10 against the single currency despite short-term bullish pressures on the pair. We believe that there is at the moment two major reasons that are pushing the euro against the Helvetic currency.

The French Presidential election and the start of the “Brexit” negotiations have removed – at least reducing the political and geopolitical uncertainties - so markets are clearly shifting towards risk-on and this is why we see the EURCHF pair moving up. In addition, Mario Draghi's comments pushed the euro higher by stating the Eurozone recovery is progressing and the ECB monetary policy stance must accompany this recovery. Markets interpreted those declarations from the ECB as hawkish.

The Swiss fundamentals remain correct, even though inflation is clearly not picking up. We nonetheless remain concerned by the FX reserves which continue their massive increase. For the time being, the SNB holds tight to defend the Swiss franc. By the way, the Swiss central bank is now the world's eighth most important investor with $80 billion dollars invested in the US market.

The CHF valuation does not depend on Swiss Economy data. Markets barely reacted on the release of retail sales growth which came in negative for the 2nd month in a row. Swiss political stability is still what attracts investors and we see the EURCHF pair showing a short-term continued bullish move towards 1.1000.

WTI Oil Futures Overbought On 4-Hour Chart, Recent Uptrend Still Intact

WTI oil futures (August 2017 contract) rose to 47.09 today, its highest level since June 7. Near-term upside momentum has weakened as the market reached overbought conditions on the 4-hour chart, which is highlighted by the RSI indicator being above 70.

The rebound from the June 21 low of 42.02 does not look like it is reversing anytime soon and the short-term bullish bias will remain intact as long as the market remains above the 200-period moving average, currently at 46.75. This is now providing immediate support. A break below this would target the next support level at the June 30 low of 45.81 before heading towards further support levels at 44.63 and 43.54. A deeper decline would open the way to target the June 21 low at 42.02, consequently erasing the gains made after rising from this low. Such a move would see a resumption of the longer-term downtrend that started in April.

Due to overbought conditions on the 4-hour chart, the market is expected to consolidate at current levels. Should upside momentum resume, there is scope to target 48.37, the June 6 high, before other resistance levels come into view at 50.25 and 51.97.

While the recent rally is overbought, only a move below 44.50 would indicate a reversal in the recent uptrend.

Euro Edges Lower, US Markets Closed For Fourth Of July Holiday

The euro has ticked lower in the Tuesday session. Currently, the pair is trading at 1.1350. On the release front, there are no US events, as markets are off for Independence Day. There are no major events in the eurozone, so traders can expect a quiet day. On the schedule, Spanish Unemployment Change dropped sharply to -98.3 thousand, well below the estimate of -120.3 thousand. Later in the day, we'll get a look at Eurozone PPI. On Wednesday, the Federal Reserve will publish the minutes of its June policy meeting.

Analysts would be hard pressed to recall a European forum of note, but this year's gathering of central bankers won't be forgotten anytime soon. Last week's meeting in Portugal triggered sharp rises from the euro and British pound, following hawkish remarks from Mario Draghi and Mark Carney. The euro jumped 2.0% last week, surprising the ECB. The bank tried to dampen market speculation about any imminent moves to withdraw stimulus, but the euro remains at high levels. Last week's stampede to snap up euros has forced ECB policymakers to reassess whether what moves, if any to announce at the July 20 policy meeting. In June, the ECB removed an easing bias regarding interest rates, effectively closing the door to further rate cuts. However, after the Draghi rally last week, policymakers may be wary about removing a second easing bias regarding the asset-purchase program, to avoid another run on the euro. The ECB has repeated loud and clear that it will not remove QE until inflation levels are closer to the bank's target of 2.0%, but Draghi may have learned the hard way at the ECB forum that the market is picking up a different message than what the ECB thinks it is sending. This could result in the ECB playing it safe and avoiding any meaningful discussion about QE at the July meeting, especially if the euro remains at high levels.

The Federal Reserve has all but signed in writing that it would raise interest rates three times in 2017, but the markets are becoming more skeptical. The odds of a rate hike in December have fallen to 47%, down from 53% last week, according to the CME Group. With the US economy giving a mediocre performance in the first quarter, and inflation levels remains low, there are Fed policymakers who are currently lukewarm to the idea of raising rates again this year. Key economic indicators have not looked particularly sharp in the second quarter, notably housing and consumer spending numbers. If inflation numbers do not improve and GDP reports for Q2 remain soft, the odds of a December hike will drop even further, which could translate into broad losses for the US dollar.

Technical Outlook: GBPUSD Pressures Daily Cloud Top Support, Techs Favor Further Downside

Cable extends pullback from 1.3029 and pressures strong support at 1.2910 (daily cloud top). Strong close in red on Monday confirmed reversal on completion of Hanging Man reversal pattern. Deeper correction could be expected on penetration into daily cloud as slow stochastic is reversing from overbought zone and generating bearish signal. Dips could extend towards 1.2861 (Fibo 38.2% of 1.2588/1.3029 upleg, reinforced by 55SMA) and 1.2833 (10/30 SMA bull-cross). Psychological 1.3000 barrier is expected to ideally cap upside attempts for now.

Res: 1.2958, 1.3000, 1.3029, 1.3047

Sup: 1.2910, 1.2861, 1.2841, 1.2833

Technical Outlook: EURUSD – Biased Lower And Pressures 1.1320 Support, Quiet Trading Expected As US Is Closed Today

The Euro remains at the back foot on Tuesday and extends weakness into third consecutive day. Monday's strong close in red signaled reversal after double upside rejection at 1.1445. Slow stochastic reversed from overbought territory and shows room for deeper correction. Pivotal support at 1.1320 (Fibo 38.2% of 1.1118/1.1445) is under pressure and break here would generate stronger bearish signal. Extension towards next pivot at 1.1243 (20SMA/Fibo 61.8%) seen on break below 1.1320/00. Tops at 1.1445 now mark strong offers. US is closed today for Independence Day and quiet trading is expected.

Res: 1.1376, 1.1400, 1.1426, 1.1445

Sup: 1.1336, 1.1320, 1.1300, 1.1243

Elliott Wave Analysis: AUDUSD Undergoing A Bearish Movement, More Weakness In View

AUDUSD is displaying a strong bearish structure away from 0.7711 level where a high has been found. Current structure we can count as a bigger three wave move in the making, with blue waves one and two already completed, which means current sharp fall is part of blue wave three. Ideally we will see more weakness develop this week.

AUDUSD, 1H

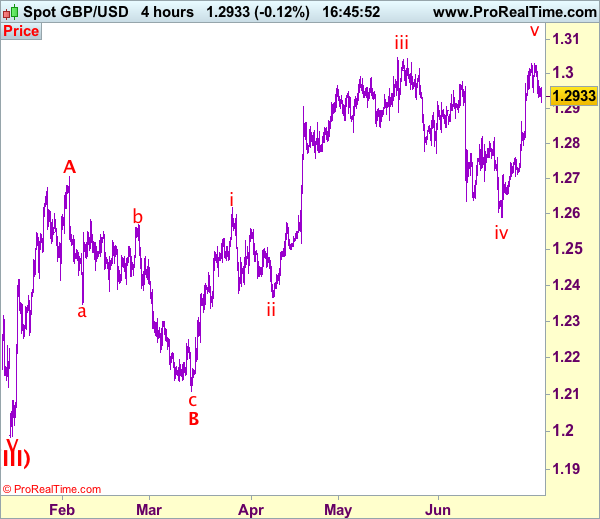

Trade Idea: GBP/USD – Buy at 1.2870

GBP/USD – 1.2927

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Buy at 1.2870, Target: 1.3020, Stop: 1.2810

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2870, Target: 1.3020, Stop: 1.2810

Position: -

Target: -

Stop:-

Sterling’s retreat after faltering below last week’s high at 1.3030 has retained our view that minor consolidation below this level would be seen and pullback to support at 1.2916 is likely, however, reckon previous resistance at 1.2861 would turn into support and limit cable’s downside, bring another rise later, above said resistance at 1.3030 would extend the rise from 1.2589 low towards recent high at 1.3048 but break there is needed to retain bullishness and bring subsequent headway towards 1.3090-00.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst initial pullback to 1.2900 is likely, reckon 1.2861 (previous resistance turned support) and bring such a rise. Below support at 1.2794 would abort and signal top is formed instead, risk further fall to 1.2750, then towards 1.2706 support.

RBA Remains On Hold, Not As Upbeat As Expected

The Reserve Bank of Australia left its cash rate unchanged at +1.50% today. In the statement accompanying the decision, the Bank stated that indicators of the labor market remain mixed. It acknowledged that employment growth has been stronger over recent months, but it expressed concerns with regards to wage growth.

AUD/USD came under selling interest at the time of the release as the bank was not as upbeat as expected following the latest two stellar employment reports. The pair fell after it hit resistance at 0.7680 (R2), to break below the support (now turned into resistance) of 0.7635 (R1). Nevertheless, the slide was stopped by the short-term uptrend line taken from the low of the 2nd of June. In our view, a clear break below that line is needed before we get confident on further downside extensions. Something like that is possible to pave the way for our next support obstacle of 0.7580 (S1).

Looking forward, we expect the Bank to maintain a balanced tone in the months to come and try not to tip the scale in any direction. Given that the quick cuts in 2016 reignited the housing market, we believe that officials will be reluctant to lower rates in coming months as concerns of potential financial stability risks may prevail again. On the other hand, the prospect of an extended period of labor market slack and inflation weakness are far from favoring a hike.

Overall, bearing in mind the latest hawkish signals from several G10 central banks, like the ECB, the BoE, and the BoC, we expect the Aussie to underperform against their respective currencies. We would avoid to exploit any further Aussie weakness against the US dollar, given investors’ expectations that the Fed may not proceed with another rate increase this year. We see EUR/AUD as a better proxy, given that the common currency has been supported by the latest ECB hints that the era of ultra-loose monetary policy is probably behind us.

Riksbank may appear more optimistic this time

During the European day, the central bank torch will be past to the Riksbank. The forecast is for the world’s oldest central bank to remain on hold. At its latest gathering back in April, the Bank extended the duration of its QE program by 6 months to December 2017 and pushed somewhat further out the timing for its first planned rate hike.

A few weeks after that meeting, the Bank announced plans to move away from its strict 2% inflation target and to introduce a target range of 1% from 2%. This implies that policymakers may be more tolerant of subdued inflation, which reduces the likelihood for any further easing measures. What’s more, European political risks have dissipated notably following the French election, something that could be reflected in the meeting statement. The combination of these factors makes us believe that the Bank is likely to appear more optimistic this time. In fact, we would not rule out the prospect that the Riksbank follows in the recent footsteps of the Norges Bank and the ECB, by also removing its interest rate easing bias.

USD/SEK edged north yesterday after it hit support fractionally above 8.4000 (S1). Nevertheless, following the break below 8.6200 (R3), which has been the lower bound of the short-term sideways range that contained the price action from 16th of May until the 27th of June, we see a negative short-term picture. A more-sanguine-than-previously Riksbank today may prove the trigger for another leg down and the continuation of the newborn near-term downtrend. If the Riksbank does not disappoint market expectations, we expect the bears to take charge and aim for another test near 8.4000 (S1). A break below that barrier could set the stage for extensions towards our next support of 8.3370 (S2).

As for the rest of today’s events:

In the UK, the construction PMI for June is due out. Expectations are for the index to have slid to 55.0 from 56.0 in May. The manufacturing PMI for the month fell by more than anticipated, enhancing the case for the construction index to follow suit and perhaps decline by more than it is forecasted. Something like that could pour some cold water on expectations regarding a BoE rate hike at one of the upcoming meetings. From Eurozone, we get PPI data for May and expectations are for the rate to have declined.

Besides the RBA and Riksbank Governors Philip Lowe and Stefan Ingves, we have two more speakers scheduled during the day: ECB Executive Board members Peter Praet and Yves Mersch.

AUD/USD

Support: 0.7580 (S1), 0.7535 (S2), 0.7515 (S3)

Resistance: 0.7635 (R1), 0.7680 (R2), 0.7710 (R3)

USD/SEK

Support: 8.4000 (S1), 8.3370 (S2), 8.2800 (S3)

Resistance: 8.5000 (R1), 8.5500 (R2), 8.6200 (R3)

Trade Idea: GBP/JPY – Buy at 145.15

GBP/JPY - 146.40

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Buy at 144.30, Target: 146.30, Stop: 143.70e

Position: -

Target: -

Stop: -

New strategy :

Buy at 145.15, Target: 147.15, Stop: 144.55

Position: -

Target: -

Stop:-

As sterling has eased after rising marginally to 146.90, suggesting minor consolidation below this level would be seen and pullback to 145.65-70 cannot be ruled out, however, reckon previous support at 145.15 would limit downside and bring another rise later to 147.10 (previous resistance), having said that, loss of near term upward momentum should prevent sharp move beyond 147.50-60 and price should falter below recent high at 148.10, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy sterling on subsequent pullback as support at 145.15 should limit downside. Below 144.60-70 would defer and risk test of previous resistance at 144.20, break there would abort and signal a temporary top is formed, bring correction of recent rise to 143.90-00 but support at 143.30 should remain intact.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

XAU/USD Analysis: Reaches 1,220 Level

As it was expected, the bullion's price continued to plummet during Monday's trading ssession. However, the situation changed on Tuesday morning. The commodity price found support at the first monthly support level, which is located at the 1,220.50 mark. For this reason, the metal seems to have a rather larger range for the consolidation period, which seems to be beginning. Meanwhile, the 55- and 100-hour SMAs are moving in from the upside at 1,235.38 and 1,241.65, respectively. The SMAs are too distant to be considered a notable resistance on Tuesday. However, additional clues in regards to closer resistance levels could be observed on the daily chart.