Sample Category Title

European Open Briefing: The Bank Of Japan Left Rates

Global Markets:

- Asian stock markets: Nikkei up 0.80 %, Shanghai Composite fell 0.25 %, Hang Seng rose 0.50 %, ASX 200 gained 0.20 %

- Commodities: Gold at $1255 (+0.05 %), Silver at $16.70 (-0.10 %), WTI Oil at $44.50 (+0.05 %), Brent Oil at $46.95 (+0.05 %)

- Rates: US 10-year yield at 2.17, UK 10-year yield at 1.04, German 10-year yield at 0.29

News & Data

- Bank of Japan Interest Rate -0.10 % vs -0.10 % expected

- New Zealand Business NZ PMI 58.5 vs 56.8 previous

- Asia stocks steady after Wall St tech rout, dollar holds gains – RTRS

- BOJ holds policy steady, upgrades view on consumption, global growth – RTRS

- Dollar firms on upbeat data, on track for weekly gains – RTRS

- Oil sits near half-year lows as global supply overhang weighs – RTRS

Markets Update:

The Bank of Japan left rates and their QE programme unchanged, as expected. Traders are now waiting for the BoJ press conference. There has been speculation that BoJ Governor Kuroda could discuss a QE exit plan. This could give the Yen a boost. If Kuroda does not mention it at all, USD/JPY is likely to extend gains to 112 soon.

The US Dollar strengthened slightly against most major currencies. Gains against the Pound were limited though. The Bank of England meeting surprised traders, with only 5 of the 8 MPC members voting to keep rates unchanged. Inflation continues to rise, and so does the pressure on the central bank. The key level to watch in GBP/USD is 1.2830. A clear break above it would signal a recovery for the Pound.

The Euro fell to 1.1130 yesterday, but remains well bid overall. However, a break below 1.11 support would signal that further losses are ahead.

AUD/USD consolidated in a 0.7575-0.76 range overnight. The broad Dollar strength has slowed momentum, but the charts suggest that the AUD/USD could rise towards 0.77 in the near-term.

Upcoming Events:

- 10:00 BST – Euro Zone CPI

- 13:30 BST – US Housing Starts

- 13:30 BST – US Building Permits

- 15:00 BST – US Michigan Consumer Sentiment

Market Morning Briefing: Euro Had Registered A Fresh Low At 1.1132

STOCKS

Dow (21359.90, -0.07%) was almost stable but has the potential to move up towards 21600 by mid of next week. The rise could be eventual and slow but overall near term looks bullish.

Dax (12691.81, -0.89%) has come off sharply and while below the important resistance of 13000, there is some scope of re-testing 12500-12400 in the medium term before possibly stating another leg of an upward rally.

Shanghai (3128.27, -0.13%) is also trading lower and could possibly test 3100 before again trying to move up. Immediate trend looks bearish.

Nikkei (19917.73, +0.43%) has the potential to move up towards 20100 in the next 2-3 sessions. Momentum could be slow but an eventual rise is expected while above 19700.

Nifty (9578.05, -0.42%) could find some support near 9550-9530 today from where it could bounce back to higher levels in the near term. Only on a break below 9530, if seen would force us to change our current bullish view on Nifty.

COMMODITIES

Gold (1255) is trading at lower levels and may test the support zone of 1245. As the dollar index is inching towards 98.30 levels, the bullish momentum is slowly evaporating. In case a break below 1245 takes place in the coming sessions, we may have to consider lower levels of 1230. Thus 1245 could be a level where the price action has to be checked to assess the future price direction.

Similar kind of trading pattern has been seen in silver (16.71) also. The recent trading range could be 16.50-16.95. we think 16.50 would provide good support due to short term oversold condition

Copper (2.57) is hovering around its support at 2.55 of the trading range of 2.55-2.67. Only above 2.66, higher resistances of 2.72-80 can come into consideration. In the medium term 2.55 are going to be a strong support now but a close below that could open up 2.40-35 levels as well.

Taking a look at the energy section, a bounce back could be expected for both Brent (46.93) and WTI (44.45) due to near term oversold condition. Brent could be headed towards 51.25 and WTI towards 47. Immediate supports are poised at 45.42 for Brent and 44 for WTI respectively.

FOREX

Dollar Index (97.43) made a fresh high at 96.84 before coming back near 97.40. As we had said yesterday that the technical picture hasn’t changed much as the upside reversal chances remain open but requires a break above 97.20-30 to confirm it and a close above 98.10 could be a trend reversal.

Euro (1.1149) had registered a fresh low at 1.1132. It is now trading within the range of 1.1198-1.1120. Yesterday it had faced stiff rejection at the higher levels, imply inherent weakness which would be confirmed on a break below 1.1120 levels.

Dollar-Yen (111.09) was rejected exactly from the support of 109 to a fresh high at 110.97 and the sharp recovery suggests that the Dollar bulls are still at play. The downside looks limited to 108.00 and as we had mentioned yesterday, a break above 110.35 took it to 111.00 already and open up the next resistance of 113.00.

Pound (1.2774) could possibly remain stable today. 1.26/25 is an immediate support for the near term. The currency pair could be ranged within 1.25-1.28 for a couple of sessions before trying to break on either side..

Aussie (0.7592), has been testing levels near 0.7635 for the last 2-sessions but has not been able to sustain above 0.76.Either a fall to 0.7520 is on the card before a ounce to levels above 0.76 or the currency pair may just move up sharply towards 0.7635-0.7650 over the next few sessions.

Dollar-Rupee (64.54) is trading at 64.54 in the NDF right now. Repeat - the support of 64.30-20 is expected to hold and push it back to 64.60-80.

INTEREST RATES

The US yields have moved up and could head higher in the coming sessions. The 5YR, 10YR and 30YR are trading higher and could head towards 1.81%, 2.25% and 2.90% respectively.

The Japanese yields are also moving up and could be headed to higher levels in the near term.

The UK and German yields are almost stable and could initiate some fresh movements next week.

GBPUSD Volatility Increase after BOE Announcement

We have got a more hawkish FOMC and BOE this week. For the former, policymakers raised the policy rate by +25 bps, as expected, and laid out detailed plans to unwind the balance sheet. For the latter, BOE left the Bank rate unchanged at a record low of 0.25%. Yet, the members' division on the monetary policy widened the most in 6 years with Michael Saunders and Ian McCafferty joining Kristin Forbes in support of a rate hike of +25 bps. The tug of war on interest rate differential results in higher volatility in GBPUSD. After BOE's announcement, GBPUSD erased earlier loss from an intra-day low of 1.2688 and rallied to 1.2795, before retreating again. The selloff of EURGBP widened with the pair plunging to a one-week low of 0.8721. ECB earlier this month refrained from talking about tapering and reaffirmed that it would extend QE purchases, if necessary.

FOMC

As widely anticipated, FOME raised the Fed funds rate by +25 bps to 1-1.25%. The latest median dot plot continues to signal one more rate hike 2017. This is followed by three hikes in both 2018 and 2019. On the economic projections, the staff upgraded the GDP growth outlook to +2.2% from +2.1% previously. The staff, however, revised lower the core PCE to +1.7% in 2017, but left those for 2018 and 2019 unchanged at +2%. Meanwhile, the unemployment rate was revised lower to 4.3% in 2017 and 4.2% in 2018-19. The long-run unemployment rate was revised down, by one-tenth, to 4.6%.

What caught the most attention was the release of an addendum to the 'Policy Normalization Principles and Plans' which provides guidelines on the process of balance sheet normalization. The Fed indicated that the process would begin this year 'provided that the economy evolves broadly as expected'. To our, and most market participants', surprise, policymakers have discussed the arrangement, including start size, timing, and the rate of increase and limit) in great details. Initial caps were set at US$ 6B per month for Treasuries and US$ 4B per month for mortgages, increasing in steps of US$ 6B and US$ 4B respectively for Treasuries and mortgages every three months, until the caps reach US$ 30B and US$ 20B, respectively. The Fed expects that, after reaching the maximum runoff rate, 'holdings will continue to decline in a gradual and predictable manner until the Fed judges that the central bank is holding no more securities than necessary to implement monetary policy efficiently and effectively'. The Fed also added that it would be prepared to resume reinvestment of principal payments 'if a material deterioration in the economic outlook were to warrant a sizable reduction in the Committee's target for the federal funds rate'. We expect a formal announcement of the plan would be made in September, followed by implementation in October. We believe the economic developments have to deteriorate very significantly to alter the Fed's plan

BOE

As expected, BOE left its Bank rate unchanged at 0.25% in June, at a 5-3 vote. Michael Saunders and Ian McCafferty joined Kristin Forbes in voting for an immediate interest rate rise to fight against rising inflation. the central bank unanimously decided to leave the bond purchase program at 435B pound for UK gilts and 10B pound for non-financial GBP investment-grade corporate bonds. Concerns over rising inflation were evidence in the minutes. Policymakers acknowledged that CPI inflation has been 'pushed above the 2% target by the impact of last year's sterling depreciation'. It 'reached 2.9% in May, above the MPC's expectation'. Policymakers noted that 'inflation could rise above 3% by the autumn, and is likely to remain above the target for an extended period as sterling's depreciation continues to feed through into the prices of consumer goods and services'. The members also raised concerns over currency depreciation on inflation. They noted that '2.5% fall in the exchange rate since the May Inflation Report, if sustained, will add to that imported inflationary impetus'.

Sterling rallied against US dollar and the euro shortly after the announcement. Rate hike speculations heightened as three members, compared with one previously, voted for a 25bp rate increase. Meanwhile, the statement mentioned that 'the continued growth of employment could suggest that spare capacity is being eroded, lessening the trade-off that the MPC is required to balance and, all else equal, reducing the MPC's tolerance for above-target inflation'.

Despite heightened expectations, we expect the central bank to leave the interest rates unchanged for the rest of the year. Conservatives' loss of majority in the general election and the hung parliament have increased uncertainty in the Brexit negotiations between the UK and the EU. Policymakers would have to be more cautious in their moves.

NZD/USD Halted By Daily Trend Line Resistance

It really wasn't that long ago that we were talking about NZD/USD breaking support!

The daily swing lows from December had broken back in May on the back of the RBNZ holding interest rates steady and the intraday price action was conducive to day trading.

Fast forward back into the present day and take a look at the NZD/USD daily chart we've featured below:

NZD/USD Daily:

Price ripped off support and 4500 pips later, has been halted by trend line resistance. A nice higher time frame resistance point.

Zoom into an intraday 15 minute chart and lets have a look at the price action:

NZD/USD 15 Minute:

After a higher time frame level holds, we want to trade in that direction. In this case short.

Take a look at how price has reacted to each short term support level and cleanly held it as resistance.

Will this trend continue?

Draining The Punch Bowl

Draining the Punch Bowl

The markets continue to digest the latest signals from the Federal Reserve Board who are now actively discussing how and when to pare back the balance sheet. But just as significantly the investors are now coming to grips with the notion that perpetual global central bank gravy train may be coming to an end in the wake of policy pivots from both the BoC and BoE and the overly hawkish musings from the Federal Reserve Board

The Central Bank's money printing machines and bloated balance sheet have not had the inflationary effects anticipated, and perhaps it's time to err on the side of caution as concerns over possible financial market distortions driven by easy money policy come to the fore. Market distortions ultimately lead to market failures, so perhaps the Federal Reserves and other global CB's are growing concerned with investors hubris and signalling it's time to reign in risk.

Not too unexpectedly in the wake of the surprising policy pivots from BoC and BoE, the market is now wondering which central bank will be next to drain the punch bowl. BoJ??

Japanese Yen

Very aggressive dollar buying across all three sessions yesterday has propelled USDJPY above the 111 level but it was the profusion of strong US economic data released yesterday, that corroborated the Fed's view, that was the primary catalyst. BoJ is not expected to shift guidance today, so the markets will focus on whether the bank maintains its JPY 80 turn QE backstop.

Euro

The markets remain in FOMC post-mortem as a dovish ECB and Hawkish Fed has Euro longs squirming but with few catalysts and little to glean from cross asset price action, buying EURUSD on dips gave way to paring back risk.

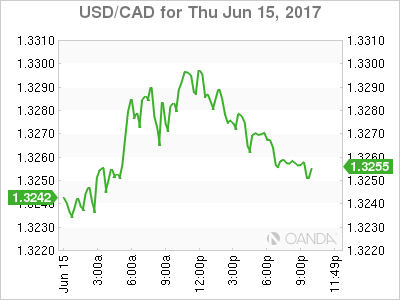

USD/CAD Canadian Dollar Lower As USD Stronger After Fed Hike

The Canadian dollar is weakening versus the US dollar on Thursday. The loonie had a dream start to the week when the one-two punch of hawkish comments from Bank of Canada (BoC) Deputy Governor Carolyn Wilkins on Monday and a day later Governor Stephen Poloz repeated similar comments during a radio interview in Winnipeg. The positive assessment from both BoC officials on the state of the economy helped the currency appreciate against the USD but the CAD rally ended on Wednesday when the U.S. Federal Reserve hiked rates as expected and delivered its own hawkish rhetoric supercharging the greenback.

Oil prices offered no support to the Canadian dollar with prices once again dropping following a weekly inventory report in the US showing a buildup, this time of gasoline stocks. Last week there was a massive unexpected buildup of crude, and now although the report from the Energy Information Administration (EIA) showed crude inventories contracted they did it by less than expected. So with higher than expected drawdown in crude and a buildup in gasoline stocks oil has lost 2.5 percent in the last five days.

Economic data in Canada were scarce with manufacturing sales growing by more than anticipated with a 1.1 percent gain in April. Oil and coal sales lead the rebound with an 8.9 percent rise. Housing has been gaining priority as an economic indicator with Canadian house resales dropping in May by 6.2 percent. Toronto housing alone plunged 25.3 percent as there are less inventory while prices climbed 17.9 percent nationally. With the slowdown in the number of houses sold there is a forecast prices will stabilize after speculators are driven off the market. Low rates will continue to make that goal difficult to achieve, but this is where the words of the central bank officials with a promise to reduce stimulus could end up with higher rates sooner than later.

The USD/CAD gained 0.099 percent in the last 24 hours. The currency is trading at 1.3272 after the decision by the U.S. Federal Reserve to hike the US benchmark rate by 25 basis points to a 100–125 range. The press conference by Chair Yellen made it clear that the Fed is maintaining its 3 go 4 rate hikes a year and is not worried about slowing inflation, cataloguing it as a temporary issue.

The CAD had gained earlier in the week as the BoC officials had given a hawkish view on the economy and hinted at a possible rate hike sooner than originally expected. With two rate cuts in 2015 to minimize the impact of dropping oil prices the BoC had stood on the sidelines awaiting the effects of fiscal stimulus that was introduced in 2016. Canadian economic indicators have been mixed but still tell a positive trend with the biggest concern being the high levels of household debt. Poloz has openly addressed that hiking too much too soon could have terrible consequences for Canadian debtors, but the fact that they are considering a hike at all did boost the loonie earlier in the week.

Market events to watch this week:

Thursday, June 15

3:30 am CHF Libor Rate

3:30 am CHF SNB Monetary Policy Assessment

3:30 am CHF SNB Press Conference

4:30 am GBP Retail Sales m/m

7:00 am GBP MPC Official Bank Rate Votes

GBP Monetary Policy Summary

GBP Official Bank Rate

8:30 am USD Unemployment Claims

Tentative JPY Monetary Policy Statement

Friday, June 16

Tentative JPY BOJ Policy Rate

2:30 am JPY BOJ Press Conference

8:30 am CAD Core Retail Sales m/m

8:30 am USD Building Permits

BOJ Falling Behind Other Central Banks

Japanese yen drops ahead of the BOJ Decision

The Bank of Japan (BOJ) will release its monetary policy statement around midnight EDT of Thursday, June 15. BOJ Governor Haruhiko Kuroda will host a press conference on Friday, June 16 at 2:30 am EDT. The Japanese central bank is not expected to change its current monetary policy despite the economy showing signs of life. The BOJ will maintain its negative interest rate and massive quantitative and qualitative easing programs unchanged. Earlier in the week the U.S. Federal Reserve has hiked rates as anticipated by 25 basis points and is looking to add another hike in 2017, while the Bank of England (BoE) kept rates at record low but minutes showed there were three votes for a hike.

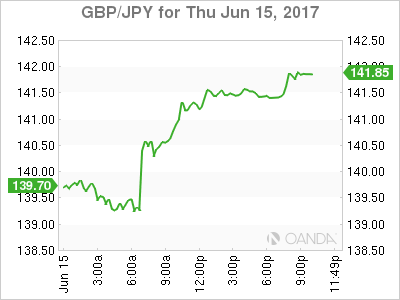

The rate hike by the Fed and the words by Chair Janet Yellen have boosted the dollar across the board. The USD/JPY is trading at 110.76, a gain of 1.4 percent in the last 24 hours. The yen has also fallen against the pound; with the GBP/JPY rising 1.036 after the more hawkish statement form the BoE. In April the BOJ upgraded its assessment of the economy to a “moderate expansion” but low inflation persists despite all the efforts from the central bank. As many monetary policy makers before them they might employ rhetoric about a strong economy, yet not quite reducing the stimulus as it is still needed. Given the change in economic fundamentals the Bank of Japan could be left further behind by other G7 central banks.

The USD/JPY gained 1.70 percent on Thursday. The currency pair is trading at 110.93 continuing a dollar rally that was started by the U.S. Federal Reserve raised the benchmark US interest rate by 25 basis points as expected. The Fed also outlined the plans to gradually reduce its massive balance sheet later this year. The American central bank Chair was not concerned with inflation remaining weak and attributed current levels to temporary effects such as cellphone bills and drug prices.

The monetary policy divergence between the Fed and the BOJ will keep growing as the American central bank has already signalled it will continue to raise its rates and reduce the balance sheet it amassed as part of its QE program. The Japanese central bank is in no position to follow that lead. The improving economy is a factor, but so is the sluggish inflation that has failed to reach the 2 percent goal set by Prime Minister Shinzo Abe.

The GBP/JPY gained 1.397 in the last 24 horus. The currency pair is trading at 141.51 after the Bank of England (BoE) held rates but released the minutes of its monetary policy meeting where 3 out of 8 members voted for a rate hike. Rising inflation and the concerns of a bad Brexit deal will keep the BoE vigilant. The snap election resulted in a hung parliament which will put more pressure on Conservatives to push for a hard Brexit that the central bank has already warned could do great damage to the economy. In that sense a Conservative costly victory is good for the pound as it could extend the timeline and soften the leverage of the Uk negotiators.

Market events to watch this week:

Thursday, June 15

3:30 am CHF Libor Rate

3:30 am CHF SNB Monetary Policy Assessment

3:30 am CHF SNB Press Conference

4:30 am GBP Retail Sales m/m

7:00 am GBP MPC Official Bank Rate Votes

GBP Monetary Policy Summary

GBP Official Bank Rate

8:30 am USD Unemployment Claims

Tentative JPY Monetary Policy Statement

Friday, June 16

Tentative JPY BOJ Policy Rate

2:30 am JPY BOJ Press Conference

8:30 am CAD Core Retail Sales m/m

8:30 am USD Building Permits

BoE Hawks Touch Down, Japan Next?

The Bank of England became the third central bank this week to send a surprisingly hawkish message. The pound edged out the dollar as the top performer while the yen lagged. The BOJ decision is up next.

The MPC held rates unchanged as anticipated but the vote was a surprising 5-3 instead of the widely expected 7-1, with Saunders and McCafferty joining Forbes in calling for a rate hike. There was also some effectively pro-pound jawboning in the statement as it said continued weakness in the currency would push CPI further above 3%.

Cable traders were caught off guard and the pair jumped to 1.2795 from 1.2700. One caveat is that this was Forbes' last meeting so all else equal there will only be two dissenters next month, thereby, helping to cap GBP strength. The market was hoping for more clarity from Carney at the Mansion House speech but it was cancelled due to the London fire tragedy. The text may be released on Friday but no time has yet been specified.

Aside from the GBP move, the US dollar remained the performer as the FOMC momentum continued. USD/JPY was especially buoyant as it climbed more than a cent to 110.98 in New York trade. The gains were barely slowed by soft US reports on the import price index, NAHB housing market index and industrial production. Better news for the dollar was once again confined to soft data surveys as the Philly and Empire Fed beat.

In the bigger picture, the BOC, Fed and BOE all delivered hawkish surprises this week -- a trend that can't be ignored. It speaks to the confidence that central banks have that growth is really coming this time. Markets were burned by the reflation trade at the start of the year but the old saying that 'you can't fight the Fed' still rings true.

A final twist this week would be if another central bank adds to the chorus. The BOJ gets the chance with today's decision on interest rates. A hike is out of the question but even a subtle shift to something less dovish would be a surprise.

As we noted earlier this week, numbers from Japan have been solid. Exports have picked up and industry has some momentum. Kuroda has signaled in the past that he will be very patient but Poloz sounded the same way until this week.

If there is a shift, the bottom will fall out of yen crosses and it would send a broader hawkish signal that would seriously threaten equities and risk assets.There is no set time for the decision but it's usually around 0300 GMT.

Gold Slightly Lower as Fed Surprises With Upbeat Rate Statement

Gold has dipped in the Thursday session. In North American trade, XAU/USD is down 0.40%, with spot gold trading at $1254.00 per ounce. On the release front, unemployment claims dipped to 237 thousand, marking a 3-week low. The Empire State Manufacturing Index rebounded with a strong gain of 19.8, crushing the estimate of 5.2 points. The Philly Fed Manufacturing Index dropped sharply to 27.6, but still beat the estimate of 25.5 points.

The markets had priced in a rate hike at almost 100%, and the Federal Reserve did not disappoint. After weeks of broad hints that a rate hike was coming, the Federal Reserve made a move at the June meeting, marking its second rate hike in 2017. The Fed increased rates by 25 basis points, to a target range of 1.00 percent to 1.25 percent. Fed policymakers sounded upbeat in the rate statement, which that was more hawkish than expected. The statement portrayed an optimistic picture, noting that the economy was growing and the labor market remained strong. Concerns over low inflation were brushed aside, as the statement noted that although inflation remains below the Fed's target of 2.0%, it expected that target to be reached in the "medium term". The Fed projected one more rate hike in 2017, and analysts were quick to circle December meeting as the most likely date. However, the markets don't appear to share the Fed's optimism as far as another rate hike this year. The odds for a September increase are at 18%, compared to 23% a week ago, according to the CME Group. As for a December increase, the odds stand at just 38%.

Although the rate hike was practically a non-event, the Fed still managed to surprise the markets. Earlier in the year, the Fed mentioned its goal of reducing its $4.2 billion balance sheet (comprised of Treasury bonds and mortgage-backed securities). Fed Chair Janet Yellen revisited this issue at her follow-up press conference on Wednesday. Yellen was short on specifics, saying that the goal was to begin the normalization "relatively soon". The Fed balance sheet ballooned after the financial crisis in 2008, as the Fed implemented a massive quantitative easing program as part of its accommodative monetary policy, together with interest rates of zero. The gradual reduction in the purchase of these assets is significant for the markets, as signifies a vote of confidence in the strength of the US economy.

Trade Idea : USD/CHF – Buy at 0.9705

USD/CHF - 0.9750

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9719

Kijun-Sen level : 0.9689

Ichimoku cloud top : 0.9683

Ichimoku cloud bottom : 0.9682

Original strategy :

Buy at 0.9710, Target: 0.9810, Stop: 0.9675

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9705, Target: 0.9805, Stop: 0.9670

Position : -

Target : -

Stop : -

Although the greenback slipped to 0.9641, lack of follow through selling and the subsequent rally on dollar’s broad-based strength suggest low has been formed at 0.9613 last week and mild upside bias is seen for the erratic rise from there to extend gain towards resistance at 0.9808, however, reckon previous resistance at 0.9825 would hold from here due to near term overbought condition, bring retreat later.

In view of this, we re looking to buy dollar on pullback as 0.9705-10 should limit downside. Below 0.9680 would defer and risk weakness towards said support at 0.9641 but only break there would abort and revive bearishness, this would also suggest the rebound from 0.9613 has ended instead, bring retest of this level later.