Sample Category Title

Sterling Rebounds as CPI Hits Four Year High, Canadian Dollar Maintains Gain

Canadian Dollar remains the strongest major currency today as boosted by comments from BoC official. Meanwhile, Sterling follows closely as lifted by stronger than expected consumer inflation data. On the other hand, the Japanese Yen trades as the weakest major currency as risk aversion recedes. Dollar follows as the second weakest as traders are getting cautious ahead of FOMC rate decision tomorrow. In other markets, Gold is suffering steep selling and is back at around 1262. WTI crude oil also stays soft in tight range around 46.

In US, the stock markets have stabilized while FOMC decision is a day away. Focus will temporarily turn to Attorney General Jeff Sessions' public testimony before Senate intelligence committee. Sessions is expected to face sharp questions about his role in the dismissal of former FBI director James Comey and his contacts with Russia during last year's election. In particular, he has contacted Russia Ambassador back then. Released from US, PPI rose 0.0% mom 2.4% yoy in May. Core PPI rose 0.3% mom, 2.1% yoy.

Canadian Dollar jumps on hawkish BoC comments

** Quick update (1450 GMT): Canadian dollar extends gain after BoC Governor Stephen Poloz's comments confirmed the hawkish twist in the central bank's stance. Poloz said a radio interview today that "interest rate cuts we put in place in 2015 have largely done their work". And "we are encouraged by the data".

Canadian Dollar jumped sharply as boosted by comments from a top BoC official that raises prospect of a rate hike. Senior Deputy Governor Carolyn Wilkins said in a speech that adjustment to lower oil prices was "largely behind us" with help of the rate cuts in 2015. And, there are "encouraging signs" of broadening growth across regions and sectors. Meanwhile, there is "significant monetary policy stimulus in the system". And, she noted that "as growth continues and, ideally, broadens further, Governing Council will be assessing whether all of the considerable monetary policy stimulus presently in place is still required." This is seen by the markets as an indication that the door for further rate cut from the current 0.50% is closed. And the next move would be a hike.

Sterling rebounds as CPI hits four year high

Sterling rebounds strongly today as headline CPI unexpectedly rose to 2.9% yoy in May, above expectation of being unchanged at 2.8% yoy. That's highest level since June 2013. Core CPI also accelerated to 2.6% yoy, up from2.4% yoy and beat expectation of 2.3% yoy. RPI rose to 3.7% yoy versus expectation of 3.5% yoy. BoE meeting will be a major focus this week and the central bank is widely expected to keep monetary policies unchanged. Economic projections were already delivered back in May's Inflation Report. So the vote split is the main focus in this meeting. With accelerated inflation, it's highly likely that Kristin Forbes will dissent again and vote for a rate hike. Such expectation would provide some support to the Pound in near term. Also from UK, PPI input dropped -1.3% mom, rose 11.6% yoy. PPI output rose 0.1% mom, 3.6% yoy. PPI output core rose 0.1% mom, 2.8% yoy. House price index rose 5.6% yoy in April.

Chance of softer Brexit and cross party negotiation increases

According to a Reuters survey, 33 out of 49 economists polled this week saying that the chance of a hard Brexit reduced somewhat. Three said that such risk receded significantly. Eight said that there was no change and five said that it increased somewhat. None of the economists said that it increased significantly. It's believed that Tories' lost of majority in the parliament means that there is no longer any mandate for a hard Brexit for Prime Minister Theresa May. Meanwhile, public support for cross party negotiation grew after the election. A poll by YouGov showed that 51% prefer Brexit to be negotiated by a cross party team. 30% preferred it to be down by the Conservatives alone. 19% said they don't know.

German ZEW dropped unexpectedly

German ZEW economic sentiment dropped to 18.6 in June, down from 20.6 and below expectation of 21.8. Current situation gauge, on the other hand, rose to 88.0, up from 83.9 and beat expectation of 85.0. Eurozone ZEW economic sentiment also improved to 37.7, up fro 35.1, beat expectation of 37.2. ZEW President Achim Wambach noted that the prospects for the German economy remain favourable. This is not least due to the positive GDP growth in the European Union in the first quarter of 2017. 70.8 per cent of the financial market experts expect the current situation to remain as favourable as it is at the moment, and 23.9 per cent even expect it to improve in the coming six months."

BoJ official said slower bond purchase due to falling yields

In Japan, BoJ's executive director on monetary policy told the Parliament that the pace of bond purchases slowed since US yields have fallen. Masayoshi Amamiya said that "the slowdown came as a result of our policy of guiding yields at appropriate levels:. And BoJ will "continue to take necessary steps to stabilize prices, while keeping an eye on how they affect its financial health". BoJ will announce monetary policy decision on Friday and it's widely expected to keep everything unchanged.

Australia business confidence dropped

Australia NAB business confidence dropped sharply by 6 points to 7 in May. Business conditions also dropped 1 point to 12. But NAB chief economist Alan Oster noted that "the business sector is looking quite upbeat, maintaining the apparent disconnect with a rather melancholy household sector." And, "it is good to see that the strength has been quite broad-based, and even at the state level we have seen some significant improvements in Western Australia, which signals that the worst of the mining sector drag is probably behind us."

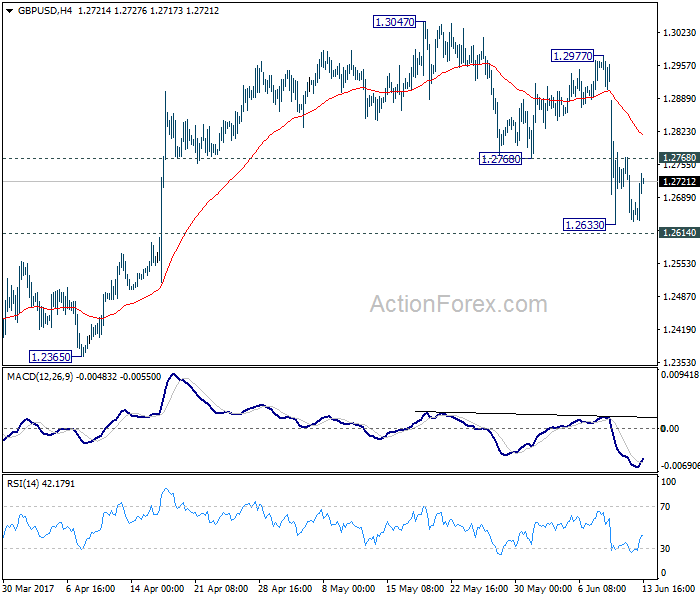

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2608; (P) 1.2689; (R1) 1.2739; More...

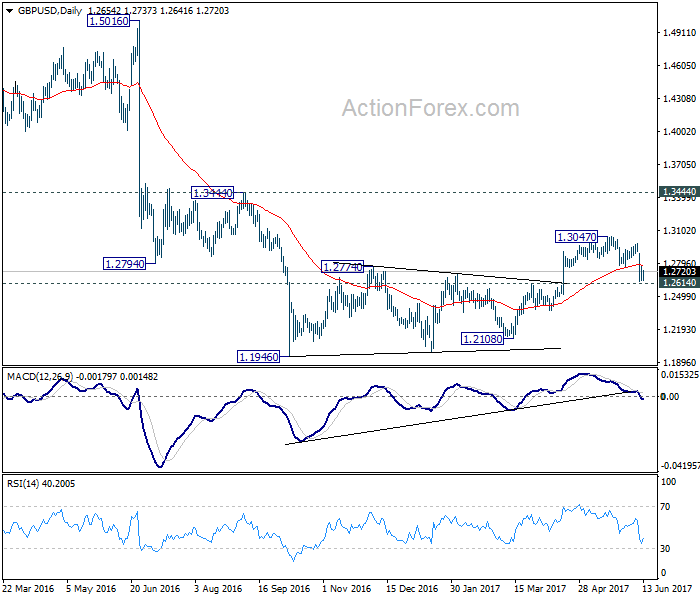

A temporary low is in place at 1.2633 and intraday bias in GBP/USD is turned neutral for consolidation. While stronger recovery might be seen, upside should be limited below 1.2977 resistance to bring fall resumption. At this point, we're favoring the case that consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 resistance turned support would confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2977 will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large All Industry Q/Q Q2 | -2.9 | 1.5 | 1.3 | |

| 01:30 | AUD | NAB Business Confidence May | 7 | 13 | ||

| 08:30 | GBP | CPI M/M May | 0.30% | 0.20% | 0.50% | |

| 08:30 | GBP | CPI Y/Y May | 2.90% | 2.70% | 2.70% | |

| 08:30 | GBP | Core CPI Y/Y May | 2.60% | 2.30% | 2.40% | |

| 08:30 | GBP | RPI M/M May | 0.40% | 0.30% | 0.50% | |

| 08:30 | GBP | RPI Y/Y May | 3.70% | 3.50% | 3.50% | |

| 08:30 | GBP | PPI Input M/M May | -1.30% | -0.40% | 0.10% | |

| 08:30 | GBP | PPI Input Y/Y May | 11.60% | 13.40% | 16.60% | 15.60% |

| 08:30 | GBP | PPI Output M/M May | 0.10% | 0.10% | 0.40% | |

| 08:30 | GBP | PPI Output Y/Y May | 3.60% | 3.60% | 3.60% | |

| 08:30 | GBP | PPI Output Core M/M May | 0.10% | 0.20% | 0.50% | |

| 08:30 | GBP | PPI Output Core Y/Y May | 2.80% | 2.90% | 2.80% | |

| 08:30 | GBP | House Price Index Y/Y Apr | 5.60% | 3.70% | 4.10% | |

| 09:00 | EUR | German ZEW (Economic Sentiment) Jun | 18.6 | 21.8 | 20.6 | |

| 09:00 | EUR | German ZEW (Current Situation) Jun | 88 | 85 | 83.9 | |

| 09:00 | EUR | Eurozone ZEW (Economic Sentiment) Jun | 37.7 | 37.2 | 35.1 | |

| 12:30 | USD | PPI M/M May | 0.00% | 0.00% | 0.50% | |

| 12:30 | USD | PPI Y/Y May | 2.40% | 2.50% | 2.50% | |

| 12:30 | USD | PPI Core M/M May | 0.30% | 0.20% | 0.40% | |

| 12:30 | USD | PPI Core Y/Y May | 2.10% | 2.00% | 1.90% |

Trade Idea: EUR/GBP – Buy at 0.8690

EUR/GBP - 0.8808

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Buy at 0.8750, Target: 0.8880, Stop: 0.8710

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8690, Target: 0.8880, Stop: 0.8650

Position : -

Target : -

Stop : -

As The single currency has retreated after marginal rise to 0.8866, suggesting consolidation below this level would be seen and pullback to 0.8745-50 cannot be ruled out, however, reckon 0.8690-00 would attract renewed buying interest and bring another rise later, above said resistance would extend recent erratic upmove from 0.8304 low to 0.8880, then 0.8900, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000, bring retreat later this week.

In view of this, we are looking to buy euro on subsequent pullback but one should exit on such rise. Below 0.8680 would defer and risk test of 0.8650-55 support but break there is needed to signal top is formed instead, bring further fall to 0.8620, then 0.8600 which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Target met and sell at 1.3330

USD/CAD - 1.3245

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sold at 1.3500, met target at 1.3330

Position: - Short at 1.3500

Target: - 1.3330

Stop: -

New strategy :

Sell at 1.3330, Target: 1.3130, Stop: 1.3390

Position: -

Target: -

Stop:-

The greenback finally dropped in line with our bearish expectation, our short position entered at 1.3500 met downside target at 1.3330 with 170 points profit, this anticipated selloff adds credence to our view that top has been formed at 1.3794 earlier and downside bias remains for the decline from there to extend weakness to 1.3200, then towards 1.3130-40, however, near term oversold condition should limit downside to 1.3100 and previous support at 1.3078 should remain intact.

As we have taken profit on our short position entered at 1.3500, would not chase this fall here and would be prudent to sell again on subsequent recovery as 1.3330-40 should limit upside. Above previous support at 1.3387 (now resistance) would defer and suggest low is possibly formed, bring a stronger rebound to 1.3420-25 but break there is needed to provide confirmation.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

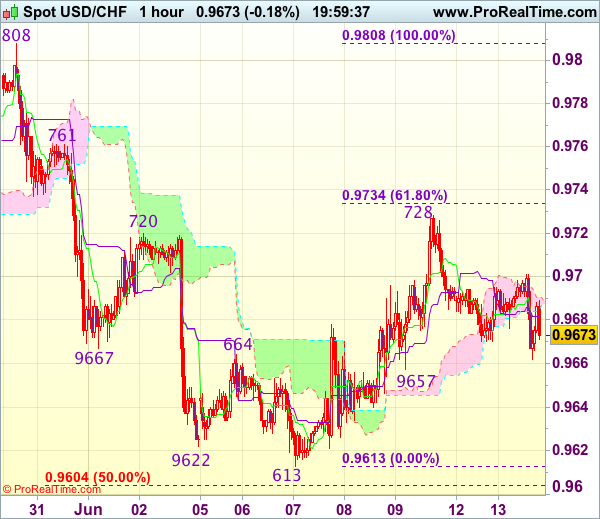

Trade Idea Update: USD/CHF – Hold short entered at 0.9720

USD/CHF - 0.9672

Original strategy :

Sold at 0.9720, Target: 0.9620, Stop: 0.9720

Position : - Short at 0.9720

Target : - 0.9620

Stop : - 0.9720

New strategy :

Hold short entered at 0.9720, Target: 0.9620, Stop: 0.9720

Position : - Short at 0.9720

Target : - 0.9620

Stop : - 0.9720

The greenback met resistance at 0.9728 late last week and has retreated, retaining our bearishness and consolidation with mild downside bias remains for weakness to 0.9657 support, however, break of 0.9640 is needed to signal the rebound from 0.9613 has ended, bring retest of this level first. A break below this level would extend recent decline to 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808) later.

In view of this, we are holding on to our short position entered at 0.9720. Above said resistance at 0.9728 would abort and signal a temporary low has been formed at 0.9613 last week instead, bring a stronger rebound to 0.9761 resistance but price should falter below resistance at 0.9808.

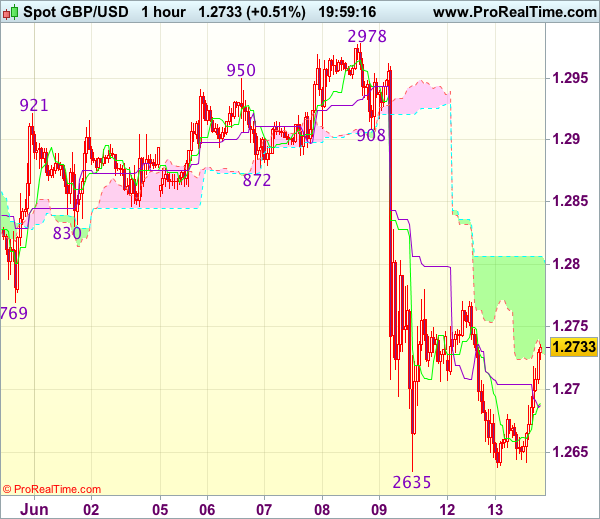

Trade Idea Update: GBP/USD – Look to sell again higher

GBP/USD - 1.2736

New strategy :

Look to sell again higher

Position : -

Target : -

Stop : -

As the British pound has recovered after holding above indicated support at 1.2635, retaining our view that further consolidation would be seen and gain to 1.2750-60 cannot be ruled out, however, still reckon upside would be limited to 1.2780 and price should falter below 1.2805-10, bring another decline later.

Below 1.2680-85 would bring weakness to 1.2650 but break of said support at 1.2635 is needed to confirm recent decline has resumed for weakness to 1.2616 (previous resistance turned support) and possibly towards 1.2575-80, however, reckon downside would be limited to 1.2550. As near term outlook is mixed, would be prudent to stand aside for now.

Gold Tests Major Support Ahead of US Data and FOMC

Spot gold hit a high of $1295.96 on June 6th, last seen on November 9th.

However, it has seen a substantial 2.2% retracement since June 7th, due to profit-taking and the release of the UK general election outcome which has eased markets' risk-off sentiment.

The price has been consolidating since Friday evening, holding above the near term major support line at $1260.

On the 4-hourly chart the price is still trading below the 10-SMA indicating the upside pressure remains heavy.

The crucial US retail sales and inflation figures for May will be released at 13:30 BST on Wednesday June 14th it will be followed by the long-awaited FOMC June rate decision 19:00 BST and the press conference at 19:30 BST.

The data performance and the tone of the Fed's statement will be the key to affect gold strength this week.

If the FOMC makes a dovish outlook we will likely see a rebound of gold prices. Conversely, if the FOMC makes a hawkish outlook it will likely weigh on gold prices and test supports.

The current price is likely to be held temporarily above the level at 1260 ahead of the release of US data and the FOMC.

The 4-hourly RSI indicator reading is around 30 suggesting a rebound.

The resistance level is at $1265.00 followed by $1270.

The support line is at $1260 followed by $1255.

GOLD: Retains Downside Pressure, Eyes 1,253.06 Level

GOLD: The commodity continues to target downside pressure leaving risk of more downside pressure. On the downside, support comes in at the 1,260.00 level where a break will turn attention to the 1,250.00 level. Further down, a cut through here will open the door for a move lower towards the 1,240.00 level. Below here if seen could trigger further downside pressure targeting the 1,230.00 level. Its daily RSI is bearish and pointing lower suggesting further weakness. Conversely, resistance resides at the 1,270.00 level where a break will aim at the 1,280.00 level. A turn above there will expose the 1,290.00 level. Further out, resistance stands at the 1,300.00 level. All in all, GOLD looks to strengthen further.

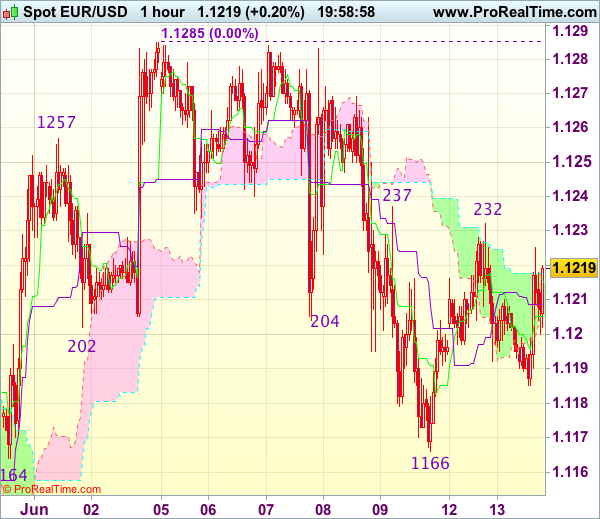

Trade Idea Update: EUR/USD – Hold short entered at 1.1230

EUR/USD - 1.1219

Original strategy :

Sold at 1.1230, Target: 1.1130, Stop: 1.1240

Position : - Short at 1.1230

Target : - 1.1130

Stop : - 1.1240

New strategy :

Hold short entered at 1.1230, Target: 1.1130, Stop: 1.1240

Position : - Short at 1.1230

Target : - 1.1130

Stop : - 1.1240

As the single currency retreated after faltering below indicated resistance at 1.1237, retaining our view that consolidation below this level would be seen and as long as said resistance holds, bearishness remains for weakness to 1.1180, break there would signal the rebound from 1.1166 has ended, bring retest of this level but below there is needed to extend the fall from 1.1285 top for retracement of early upmove to 1.1145-50 and then towards 1.1120, however, support at 1.1109 should hold from here.

In view of this, we are holding on to our short position entered at 1.1230. Only above 1.1265-70 would abort and bring retest of 1.1285, only break there would revive bullishness and confirm recent upmove has resumed and extend further gain to previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 and later towards chart point at 1.1366.

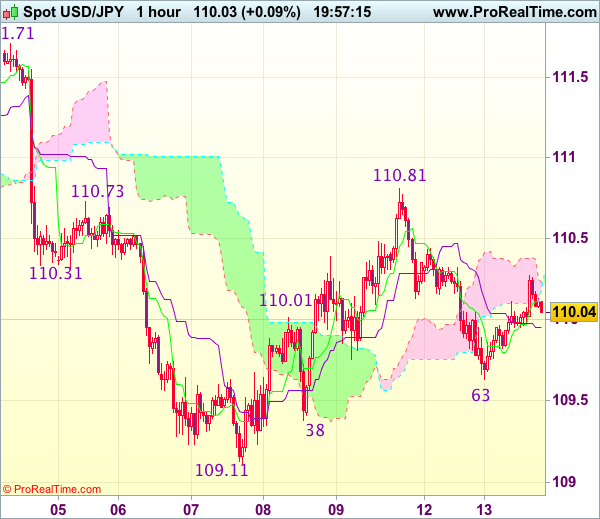

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 110.03

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback slipped to 109.63 yesterday, dollar needs to penetrate previous support at 109.38 to signal the rebound from last week’s low of 109.11 has ended at 110.81 and bring retest of this level. A drop below there would confirm recent decline has resumed for further fall to 109.00, then 108.75-80, however, near term oversold condition would limit downside and reckon 108.50 would hold.

If said support at 109.38 continues to hold, then further consolidation is in store and another bounce to 110.35-40 cannot be ruled out, however, upside should be limited to 110.60 and price should falter below 110.81. Only break of this resistance would signal the erratic rise from 109.11 low is still in progress for further gain to 111.00 and possibly 111.20-30 but price should falter well below resistance at 111.71, bring retreat later. As near term outlook is mixed, would be prudent to stand aside in the meantime.

GBP Buoyed by Inflation Data ahead of BoE

- Markets cautious ahead of Fed meeting while tech sell-off pauses;

- Yield curve flattening on delayed delivery of Trump stimulus;

- GBP buoyed by inflation data ahead of BoE.

US futures are pointing to a slightly higher open on Wall Street on Thursday, with the sell-off in tech over the last couple of days possibly abating and providing relief for indices.

There is an element of caution in the markets ahead of tomorrow's Federal Reserve meeting, with a rate hike now almost fully priced in and traders keen to find out what the path of rate hikes will be going forward. Policy makers had previously alluded to another hike this year but markets remain unconvinced given the data we've seen, particularly on inflation which has actually been trending lower in recent months and remains below target.

Just to complicate matters further, the Fed has discussed reducing the balance sheet, probably starting later this year which would likely slow the pace of rate hikes over the next couple of years. The flattening of the yield curve, which can signal an expected recession, is more likely a reflection of markets losing faith in Donald Trump's ability to deliver on his growth agenda and provide the boost to inflation and interest rates that was priced in after the election in November.

After two woeful sessions, sterling is making decent gains this morning, buoyed by UK inflation data for May which showed prices once again rising faster than markets were expecting. Headline inflation rose to 2.9% last month while core rose to 2.6%, both now well above the Bank of England's 2% target and continuing their upward trajectory. With the BoE meeting this week it will be interesting to get immediate reaction to the moves and perhaps see just how much more policy makers are willing to tolerate.

It will also be interesting to see whether the election has complicated matters. Policy makers will be reluctant to rock the boat at a time when there is already so much uncertainty and fragility and may therefore be willing to tolerate slightly higher inflation if they are convinced its only temporary. The economy is already showing signs of slowing, particularly in the consumer sector as negative real wage growth begins to drag, which would make it the worst time to be raising interest rates.