Sample Category Title

Commodities Soar As Allegations Fly

The USD collapses under the weight of allegations overnight, giving a boost to oil and sending gold soaring as investors dump equities and run for safety.

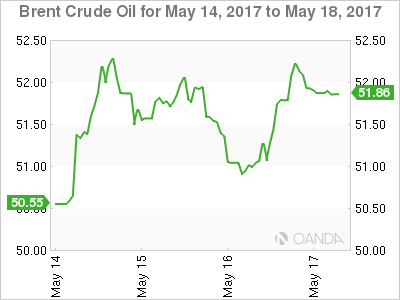

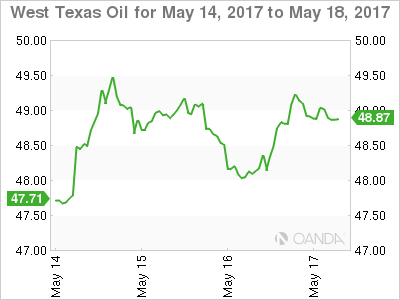

OIL

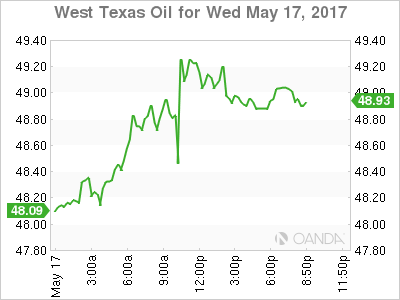

Both Brent and WTI exploded higher overnight buy some 1.80% despite the Crude Inventories showing a lower than expected drawdown. Oil appears to have benefited from a confluence of factors coming together. A weaker U.S. Dollar as President Trump’s travails deepen. The largest OPEC producers are indicating they support a production cut extension ahead of next week’s meeting. And finally, a drawdown for six weeks in a row on crude inventories in the U.S. along with drawdowns also seen on gasoline and distillates.

As ever, late session profit taking saw both crude contracts give back some of their gains with Brent and WTI spot levels opening at 52.00 and 49.00 respectively. However, amongst all the bullish clamours that are sweeping the market this morning we not a divergence between the Brent and WTI contracts. While Brent has comfortably closed above its 22-day average overnight, WTI has failed to do so. It marks the 3rd day in a row that WTI has broken its 200-day average but has failed to close above it to trigger a further bullish technical signal. Our best interpretation is the U.S. shale producers are now back in the market selling futures at these levels to hedge future production.

Brent

This morning Brent spot basis has a double top resistance at 52.40 with a general congestion zone of previous daily highs in this region as well. A break above implies a technical move to the 100-day average at 53.50. Intraday support appears at the 50.80 regions and then 50.50.

WTI

WTI spot basis continues to struggle above its 200-day average which sits at 49.10 this morning. Intra-day resistance appears at 49.55 and then 59.85, just ahead of the psychological 50.00 level. Support lies initially at 48.00 and then 47.20.

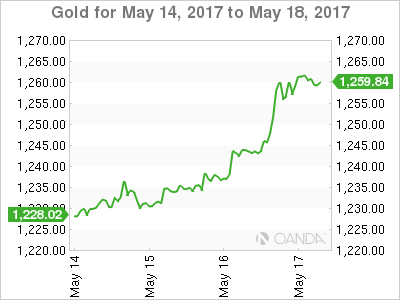

GOLD

Gold rocketed 30 dollars higher overnight to touch 1261 as investors globally flocked to safety as the political turmoil in Washington D.C. ratchets to new highs on the temperature dial. Gold was the primary beneficiary along with U.S. bonds as investors globally rotated out of equities and the U.S. Dollar and fled to safe-havens.

In the process gold has exploded through its 200-day moving average at 1246.60 and trend line resistance at 1257.00 to paint an impressive technical picture this morning in Asia. We do however note, that the move has been driven by “there’s never just once cockroach” approach to political uncertainty, rather than a fundamental investment reassessment structurally of gold itself. Whilst it is evident the investor world does not like cockroaches, gold itself will now trade on headlines rather than fundamentals necessarily.

This morning gold trades in Asia at 1260.50 with resistance initially at 1271.00 and then 1295.00. Nearby support sits at 1257.00 followed by 1241.00. Whilst the technical picture looks constructive, traders should monitor their news feeds for near-term direction.

Political Pandemonium

Political Pandemonium

While the markets aggressive risk-off reverberation may well be exaggerated, the fact is dealers never actually believed the Trump impeachment chatter until yesterday when the Comey notes came to light. There is a very high level of uncertainty oozing from the markets but one thing that is crystal clear, investors now believe that at a minimum the rising US political entropy will jeopardise the White House policy agenda, and at the extreme, a Trump impeachment will lead to a flat out market collapse.

What initially started as a risk off narrative turned into a full blow US dollar -off a move that has been intense and unforgiving. But despite the magnitude of the dollar sell-off overnight, we may only be scratching the surface if this storyline has legs.

US political risk will continue to drive sentiment near term which will continue to pressure S&P futures and regional bourses while the traditional havens, Yen, US Treasuries and Gold will provide an umbrella for investors as dark and ominous political thunderheads gather.

Besides the political headline risk, the market is becoming less sure about a June Fed interest rate hike as the pandemonium in Washington and sagging equity markets will not go unnoticed by Dr Yellen and company. It’s a toxic brew for dollar bulls who are getting steamrolled from every possible angle.

US Dollar

Completely engulfed in the Trump Comey story but the key for extending the short USD trade will be how loyal Republican legislators remain to Trump, or will they look to abandon what appears to be a rudderless ship.

Australian dollar

Another solid employment number this morning, and should be supportive but with external US political factors weighing on risk sentiment, it’s unlikely dealers will muster up the courage to make any serious attempt near .7475 level.

Euro

Asset rotation into Europe should continue to provide support while US political decay plays into the Euro as a haven poxy. Any shift in ECB guidance will be a bonus for the EURO bulls

Asia FX

Very deep rooted risk off sentiment with the only bright spot a bounce on oil on the back of inventory decline.Far too much uncertainty in the short term market which will see dealers either keeping inventory light or on the sidelines awaiting the next catalyst

Aggressive Sell Off Sees USDX Back Below Trump’s Election Win Level

As we head into the back-end of the week, the US Dollar has experienced an aggressive sell off.

One interesting line I picked up in my morning reading was:

'The US Dollar has now fully reversed all initial gains following the election victory for President Trump.'

This highlights the lack of confidence in the Trump administration that talked the talk of having the policies to boost economic growth, but so far has failed to walk the walk in delivering anything meaningful.

The latest political developments (which I'm not going to go into for obvious reasons but everyone has access to Twitter and Google), only continue to errode any confidence that markets once had in Trump's election win being some sort of new dawn.

Just take a look at the US Dollar Index chart on your MT4 platform:

USDX Daily:

Thanks to these latest political developments, the USDX trend line break that we had been watching has followed through.

The question we have to now ask ourselves as traders, is will the market remain USD bearish, even if the Fed continues toward interest rate normalisation. That is, do you think that further Fed rate hikes that are definitely coming, will be able to provide any support for the USD?

Bonus Chart!

As long as we're looking at the US Dollar, I thought it'd be worthwhile to also take a look at the S&P 500 chart:

S&P 500 Daily:

As you can see on the daily, at the moment it's all about the gap fill.

Keep an eye on the the level and whether it acts as a magnet to essentially pull price down toward it.

Breaking Point

We learned this year that financial markets can tolerate a great deal of political dysfunction; Tuesday showed this also has a limit. The yen soared while the Canadian dollar lagged as risk aversion hit hard. Japanese GDP and Australian jobs are due up next. The Premium short in the DOW30 hit its final target for 330-pt gain.

The trigger for the meltdown in sentiment Tuesday was a revelation that Trump asked FBI Director Comey to drop his investigation of Mike Flynn. Legal and constitutional circles have been debating on whether it could be obstruction of justice but markets didn't wait for the answer.

USD/JPY fell more than 200 pips in the worst decline since July 2016, US 10-year yields dropped 9 bps and the S&P 500 fell nearly 40 points. The selling was relentless.

The next move is to take a step back and search for perspective. It seems highly unlikely this is enough to impeach a President. This isn't Watergate. The Republican agenda also probably isn't in peril. If anything, Congressional Republicans will want to get to work and accomplish something in order to help change the conversation.

But maybe the message from markets isn't about impeachment or the Republican agenda. Maybe it's about governance. The breaking point might be that the market has determined that the new administration is so gaffe prone and the President so impulsive that he will never be able to lead effectively. That's the kind of instability that grates on business and sentiment.

It doesn't mean this is the start of a bear market or a recession but it could dial back expectations. The odds of a June 14 Fed hike are down to 66% from 88%, according to the CME's Fedwatch tool. That's not just about politics, it's also a reflection of sluggish economic data.

What's also instructive is that troubles in the present always seem bigger than they are, especially with geopolitics. The market freaked out about Ebola, Russia's incursion into Ukraine, dozens of things that will never appear in history books. There's a good chance that's what will happen next.

Ultimately, the economy is what will guide markets so we look next to key data from Japan and Australia. Up first at 2350 GMT, Japanese Q1 preliminary GDP data is due. The market is expecting 0.5% y/y growth, or 1.7% annualized.

For Australia, the jobs report is at 0130 GMT and forecast to show 5.0K new jobs and 5.9% unemployment. Given the negative rumblings from China, we will be watching Australian data closely in the coming months.

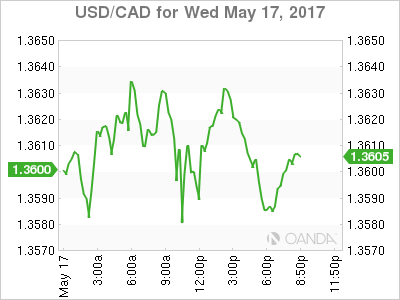

USD/CAD Canadian Dollar Lower After Trump Turmoil Triggers Risk Aversion

The Canadian dollar is trading lower even as the price of oil is close to 1 percent higher on Wednesday.Safe havens such as gold, the Japanese yen and the Swiss franc trade higher against the US dollar after the crisis engulfing the Trump administration. The loonie could not capitalize on USD weakness as the newly appointed US Trade representative set the groundwork for the NAFTA renegotiation. Robert Lighthizer, briefed a Senate Finance Committee on the trade agreement overhaul. The renegotiation talks are expected in late August with representatives of Canada and Mexico. The Trump administration needs to present a letter before congress 90 days before starting trade talks. Senator Ron Wyden mentioned that the US is seeking a currency manipulation clause to be used in future trade agreements the United States enters into.

A Reuters survey that took in the opinions of economists was caught off guard as much as the rest of the market when back in February there were no reasons to be concerned about a NAFTA renegotiation. The same panel of economists is now warning that the trade talks could have material impact on Canada as it exports three quarters of its exports south of the border.

Canadian manufacturing sales rose 1 percent in March but the February data was revised downward to a 0.6 contraction. Canadian retail sales will be released on Friday, May 19 at 8:30 am alongside inflation data.

The USD/CAD gained 0.416 percent in the last 24 hours. The currency pair is trading at 1.3632 near daily highs after the turmoil surrounding the White House has triggered a wave of risk aversion that has pulled investors away from the Canadian dollar in search of safe havens.

The rise of oil prices could not offset the pressure on the Canadian dollar as the White House regardless the current drama with Trump’s disclosure of classified information in the aftermath of the dismissal of FBI Director James Comey.

Crude is 0.952 percent higher on Wednesday. The price of West Texas Intermediate is trading at $49.08 after US crude inventories confirmed the forecast of 1.8 million barrels drawdown last week. The softness in the US dollar following the political turmoil in Washington has also helped WTI climb towards the $50 price level.

US inventories recorded their sixth straight drawdown a day after Organization of the Petroleum Exporting Countries (OPEC) members were voicing their support for the extension to their production cut agreement. Russia and Saudi Arabia issued a joint statement on Monday almost guaranteeing an extension to be announced on the scheduled meeting May 25.

Gold has gained 1.656 percent in the last 24 hours. The price of the yellow metal is trading at $1,259.21 continuing to climb higher as the political situation in the United States has given way to a rise in risk aversion by investors. The difficulties facing the Trump administration raise serious doubts about the pro-growth policies that were promised last year being enacted this year. Tax reform and infrastructure spending were behind the USD rally earlier as Trump took office, but as immigration, trade and health battles took their toll in the President’s political capital. The US economic data has also been mixed of late adding more uncertainty into the next meeting of the U.S. Federal Reserve in June. The CME FedWatch tool has reduced the probability of a rate hit to 64.6 percent after reaching 87.7 percent a week ago.

Market events to watch this week:

Thursday, May 18

4:30 am GBP Retail Sales m/m

8:30 am USD Unemployment Claims

Friday, May 19

8:30 am CAD CPI m/m

8:30 am CAD Core Retail Sales m/m

Trump Troubles Boost Gold Prices

Gold has posted strong gains in the Wednesday session, as the metal trades at 2-week highs. Currently, spot gold is trading at $1256.32 in the North American session. On the release front, there was only one US release, as Crude Oil Inventories declined 1.8 million barrels, compared to the estimate of a decline of 2.5 million barrels. On Thursday, there are two key events – unemployment claims and the Philly Fed Manufacturing Index.

Gold has been a big winner from the ongoing political turmoil in Washington, as the Trump administration lurches from crisis to crisis. President Trump and his aides have preoccupied with damage control, as the fallout from Trump's dismissal of FBI director James Comey continues. On Tuesday, reports swirled that Trump had asked Comey to close an investigation into ties between Russia and Trump's former security adviser, Michael Flynn. The Democrats have been quick to attack, with some lawmakers claiming that Trump may have committed obstruction of justice. Another brewing controversy is Trump's passing of classified intelligence to the Russian foreign minister earlier this week. Trump initially denied the claim, but has since backtracked, admitting that he did share intel with the Russians, but that he had full authority to do so. With the Trump administration busy putting out political fires, investors are growing increasingly nervous that the president's agenda for a stimulus package and tax reform will stall, and gold, a safe-haven asset, is shining brighter as market jitters intensify.

Weak US numbers since last week have also contributed to higher gold prices, as the US economy has slowed in 2017. On Tuesday, construction data was softer than expected. Building Permits dropped to 1.23 million, short of the forecast of 1.26 million. The news wasn't any better from Housing Starts, which slipped to 1.17 million, compared to the estimate of 1.26 million. This marked the smallest number of housing starts since November 2016. Despite the weak numbers, demand for housing remains high, fueled by a labor market that is close to capacity and an unemployment of just 4.4 percent.

Will Falling Real Incomes Affect the UK Consumer?

Consumer Revival Needed After Disappointing First Quarter

As cracks start to appear in the economic data, the Bank of England downgrades its growth and inflation forecasts and the country heads to the polls to vote for the government that will lead the Brexit negotiations with the EU, it's clear that an interesting period lies ahead for the UK.

For almost a year now - since the EU referendum - we've heard a lot about the surprisingly resilience of the UK economy, while the BoE and other experts have been berated for their gloomy outlook for Brexit Britain. And while many of those will accept that the country has performed better than they anticipated, the cracks are starting to appear and the data so far this week has clearly highlighted where.

The retail sales report on Thursday should offer further insight into the consumer following a dire start to the year for spending and at a time when real incomes are now officially falling. The data released earlier in the week showed inflation hit 2.7% in April - albeit largely driven by the timing of Easter this year - while earnings rose by only 2.4%, or 2.1% excluding bonuses.

With at least the near-term outlook for real wage growth looking bleak - as the weaker pound keeps inflation elevated and the uncertainty surrounding Brexit weighs on wage growth - the coming months may be quite challenging for retailers. While the UK consumer is not particularly averse to spending on credit, which at times is what's kept the economy ticking along, there is a clear correlation between real wage growth and spending and it doesn't look good. The chart below shows real wage growth (earnings growth minus inflation) in orange and retail sales in purple, compared to a year ago.

Given how valuable the consumer is to the UK economy and the trend over the last few months, it's no wonder that the BoE downgraded its growth forecasts last week. Should we see a revival in the consumer in the coming months and the first quarter prove to be a blip, then the outlook could look a little brighter. Given the latest data on inflation and wages though, it's not looking great.

A mini spending revival is expected for April, with overall and core retail sales seen rising 1% from a month earlier, and 2% and 2.5%, respectively, from the same month a year earlier. While this may give reason for some optimism, it is worth remembering again that Easter fell in April this year and March last year which will flatter the numbers in much the same way that it made them appear worse last month. We may need to see more evidence of a consumer revival if we're truly going to see the resilience that we've heard so much about.

Pound Rises on Strong UK Wage Growth Report

GBP/USD has posted gains in the Wednesday session. In North American trade, GBP/USD is trading at 1.2950. On the release front, British employment numbers were mixed. Wage growth climbed 2.4%, matching the forecast, and the unemployment rate dipped to 4.6%, below the estimate of 4.7%. The news was not as good from unemployment claims, which rose 19.4 thousand, well above the estimate of 7.5 thousand. In the US, there are no major releases on the schedule. On Thursday, the UK releases Retail Sales, which is expected to rebound with a gain of 1.2%. The US will release unemployment claims and the Philly Fed Manufacturing Index.

The Bank of England has been saying that Britons will have to get used to a lower standard of living, and the warning has become reality with the release of the latest wage growth report. Wages rose 21% year-on-year in the first quarter, resulting in real wages dropping for the first time since 2014, after adjusting for inflation. CPI, the primary gauge of consumer inflation, continued to move upwards, posting a sharp gain of 2.7% in April, matching the BoE forecast for inflation in the first quarter. This reading marked the strongest gain in CPI since September 2013. The BoE is expecting inflation to hit 3 percent, raising speculation that the central bank may raise interest rates to keep inflation under control. The weak pound has contributed to higher inflation, which has hurt wage growth and caused consumers to scale back on spending, a key component of economic growth.

The political turmoil which has gripped Washington appears to be spreading. The US media is having a field day, as the Trump administration lurches from scandal to scandal. On Tuesday, reports surfaced that President Trump asked former FBI director James Comey to end an investigation into ties between Russia and Trump's former security adviser, Michael Flynn. Another brewing controversy is Trump's passing of classified intelligence to the Russian foreign minister earlier this week. Trump initially denied the claim, but has since backtracked, admitting that he did share intel with the Russians, but that he had acted within his rights. With the Trump administration busy putting out political fires, investors are growing increasingly nervous that the president's agenda for a stimulus package and tax reform will stall.

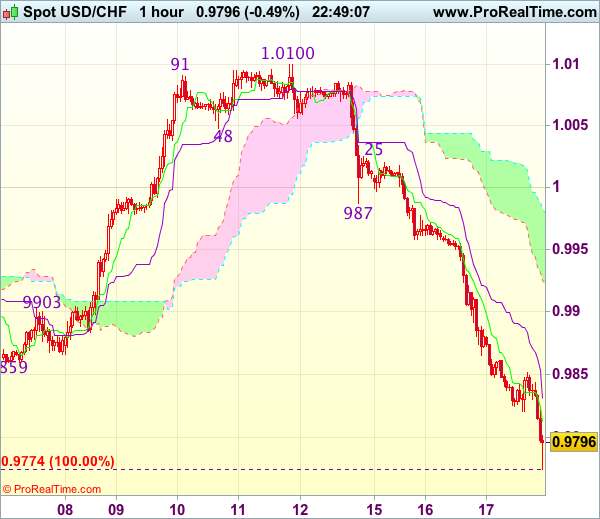

Trade Idea Wrap-up: USD/CHF – Sell at 0.9870

USD/CHF - 0.9790

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9813

Kijun-Sen level : 0.9831

Ichimoku cloud top : 0.9980

Ichimoku cloud bottom : 0.9922

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9870, Target: 0.9770, Stop: 0.9905

Position : -

Target : -

Stop : -

As dollar has continued heading south and broke below indicated previous support at 0.9813, confirming our bearish view that the decline from 1.0344 top is still in progress, hence bearishness remains for this move to extend further weakness to 0.9770, then towards 0.9735-40 (76.4% retracement of 0.9550-1.0344), however, near term oversold condition should prevent sharp fall below 0.9700, risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 0.9870 should limit upside. Above 0.9900 would defer and risk rebound to the lower Kumo (now at 0.9922) but upside should be limited to 0.9950 and price should falter well below previous support at 0.9987, bring another decline.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2971

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2949

Kijun-Sen level : 1.2943

Ichimoku cloud top : 1.2912

Ichimoku cloud bottom : 1.2901

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Cable’s rally after breaking indicated resistance at 1.2958 confirms the correction from 1.2991 has ended at 1.2844 earlier and retest of this level would be seen, however, above indicated level of 1.2999-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance) is needed to retain bullishness and signal early upmove has resumed for headway to 1.3040-50, then 1.3075-80.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.2940 would bring weakness to 1.2900-10 but only break of latter level would prolong consolidation and risk weakness towards support at 1.2866, however, price should stay above said support at 1.2844.