Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.76; (P) 113.27; (R1) 113.62; More...

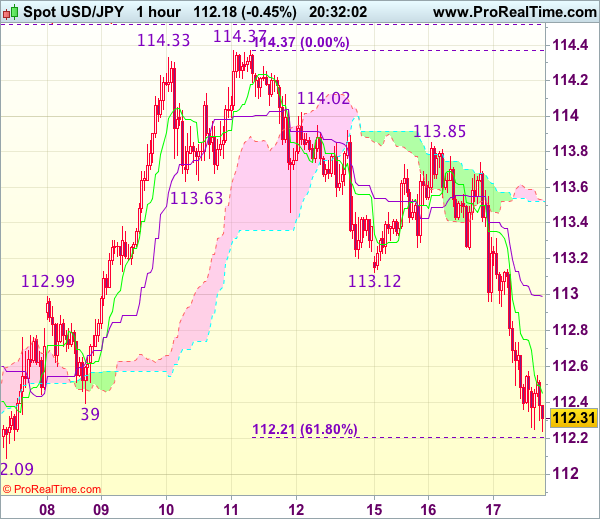

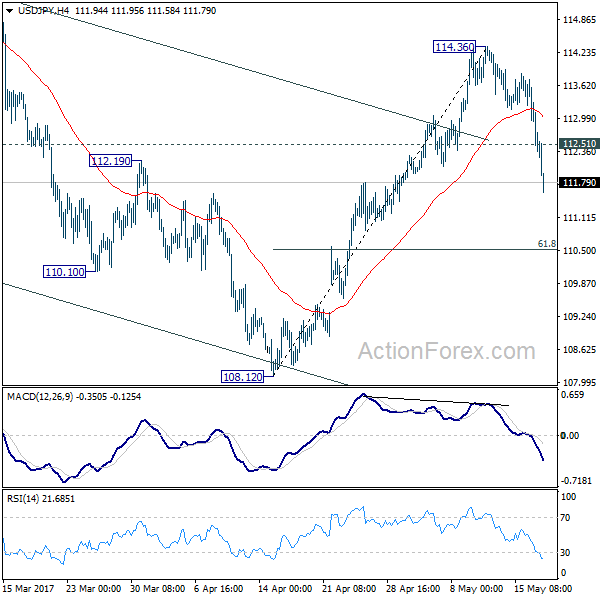

USD/JPY's decline accelerates to as low as 111.58. 112.08 cluster support (38.2% retracement of 108.12 to 114.36 at 111.97) was taken out without hesitation. Intraday bias remains on the downside and deeper fall would be seen to 61.8% retracement at 110.50. The development also dampen the bullish case that correction from 118.65 has completed at 108.12. We'll asses that part of the outlook later. For now, above 112.51 minor resistance will turn bias neutral and bring consolidations first.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9942; (P) 0.9980; (R1) 1.0003; More.....

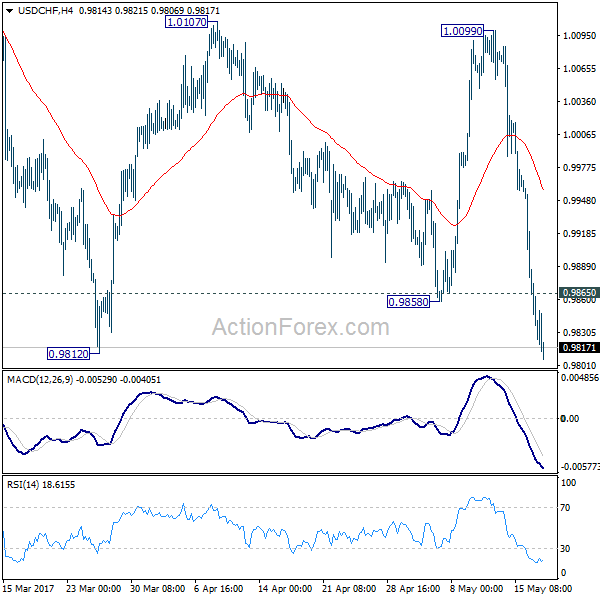

USD/CHF's decline is still in progress and breaches 0.9812 support. Current fall is seen as part of the decline from 1.0342. Next target will be target lower trend line support (now at 0.9762) and below. At this point, such decline from 1.0342 is still seen as a correction. Therefore, we'd expect strong support above 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617 to contain downside. On the upside, above 0.9865 minor resistance will turn bias neutral and bring recovery before staging another fall.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

Trade Idea: USD/CAD – Buy at 1.3535

USD/CAD - 1.3623

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3535, Target: 1.3735, Stop: 1.3475

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3535, Target: 1.3735, Stop: 1.3475

Position: -

Target: -

Stop:-

This week’s decline has retained our view that near term downside risk remains for the fall from 1.3794 top to bring retracement of recent rise, hence weakness to 1.3575-80 would be seen, however, reckon downside would be limited to support at 1.3530 and bring rebound later, above 1.3665-70 would bring rebound to 1.3700 but break of 1.3740-45 is needed to signal the pullback from recent high at 1.3794 has ended, bring test of 1.3770 resistance first, then towards 1.3794. Looking ahead, only a break above there would confirm recent upmove has resumed and extend further gain to 1.3840-50, then towards 1.3900.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.3530-35 should limit downside and bring another rise later. A firm break below 1.3530 would abort and suggest a temporary top is formed, bring retracement of recent upmove to 1.3500 and later towards 1.3450-60 but support at 1.3411 should remain intact, bring another upmove later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

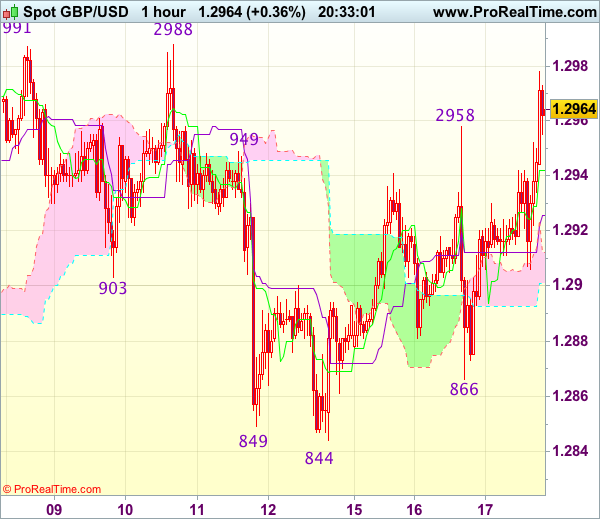

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2870; (P) 1.2913; (R1) 1.2962; More...

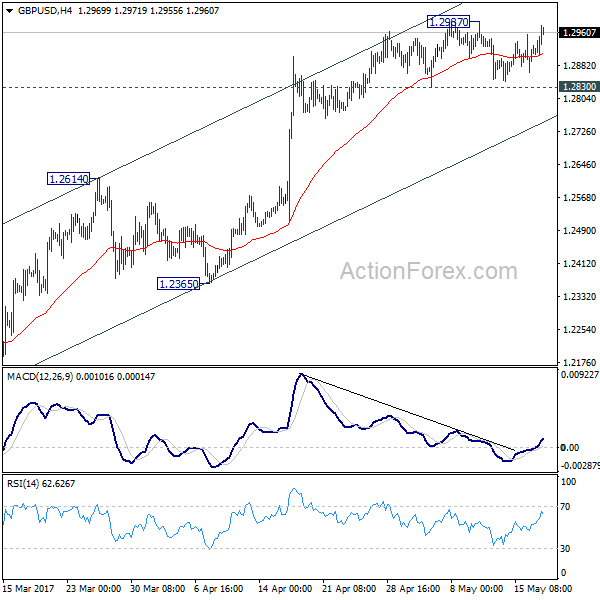

GBP/USD recovers today but it's still staying in range of 1.2830/2987. Intraday bias remains neutral for the moment. With 1.2830 minor support intact, another rise cannot be ruled out. However, price actions from 1.1946 are viewed as a corrective pattern. Therefore, in case of another rise, we'd start to look for reversal signal again above 1.2987. Meanwhile, break of 1.2830 will indicate short term topping. In such case, intraday bias is turned back to the downside for 1.2614 resistance turned support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

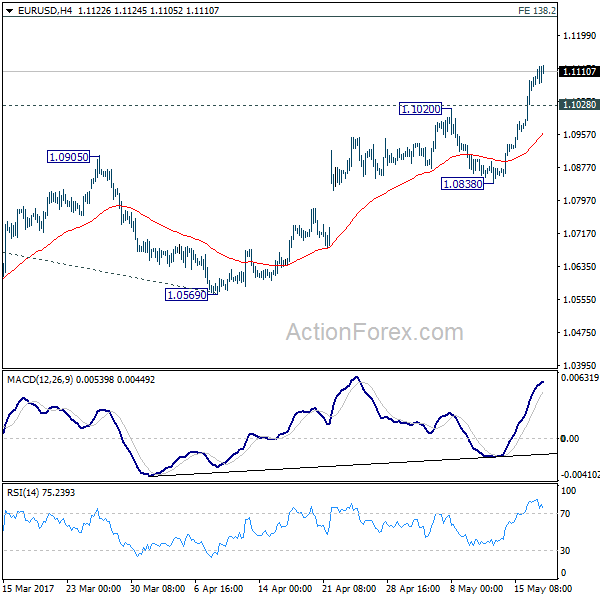

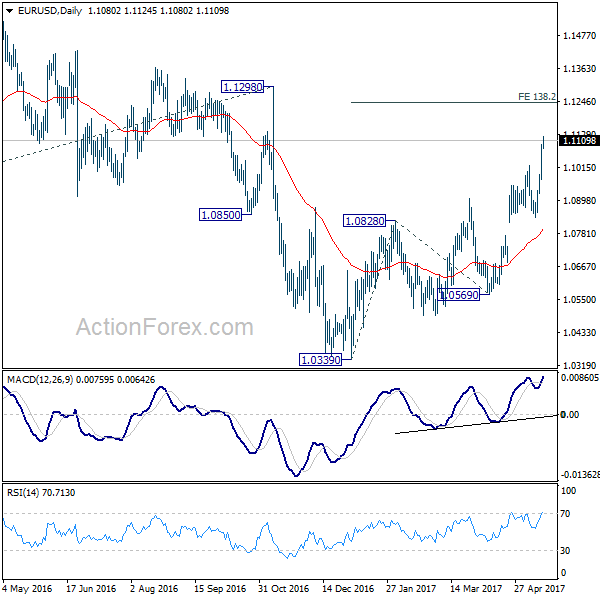

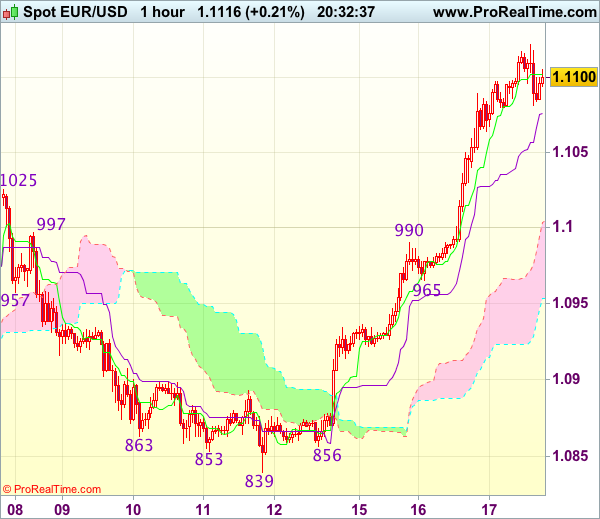

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1003; (P) 1.1050 (R1) 1.1128; More....

Intraday bias in EUR/USD remains on the upside as current rally continues. The pair would target 138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245, which is close to 1.1298 key resistance. For now, rise from 1.0339 is still viewed as a corrective move. Hence we'd expect strong resistance below 1.1245/98 to limit upside and bring reversal. On the downside, below 1.1028 minor support will turn bias neutral and bring consolidation. But break of 1.0838 support is needed to indicate short term topping. Otherwise, further rise will remain in favor.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

Dollar Selloff Continues as Trump-Comey Correspondences Demanded by House Oversight Chair

Dollar's selloff continues today as markets are in deep concerned with US President Donald Trump's political turmoil. The situation worsens after a report that Trump has intervened in FBI investigation on national security adviser Michael Flynn. House Oversight Committee chair Jason Chaffetz, a Republican, requested FBI to hand over all records of correspondence between form FBI director James Comey and Trump, by May 24. Chaffetz tweeted that "@GOPoversight is going to get the Comey memo, if it exists. I need to see it sooner rather than later. I have my subpoena pen ready." Meanwhile, Russian President Vladimir Putin offered to provide US Congress with a record of Trump's meeting with Russian officials, just after firing Comey. It's reported that Trump passed highly sensitive classified information to Russia at the meeting.

The dollar index dives through 98.54 support this week, partly also due to strength in Euro. Downside acceleration now put 50% retracement of 91.91 to 103.82 at 97.86 at risk. And a firm break there will pave the way to 61.8% retracement at 96.43. At this point, we're still treating the decline from 103.82 as a correction. Hence, while it's going deeper than expected, we'd expect support from 95.88 to contain downside and bring near term reversal.

European Council Tusk and European Commission Juncker talked on Brexit

European Council President Donald Tusk said today, referring to UK, that "the relationship between the EU and a non-member state cannot offer the same benefits as EU membership." And, a free trade agreement "even if it is ambitious and wide-ranging cannot mean participation in the single market or its parts." Also, "UK must be aware that any free trade agreement will have to ensure a level playing field and encompass safeguards against unfair competitive advantages through inter alia tax, social, environmental and regulatory measures and practices."

European Commission President Jean-Claude Juncker said three are three priorities for the first phase of Brexit negotiations. First and "foremost" both sides have to deal with the situation of more than four milling people. Those include 3.2m EU nationals living in UK and 1.2m Britons living in EU. Secondly, "all financial commitments given by the EU will be honoured by the UK". Thirdly,avoiding a hard border between Northern Ireland and the Republic of Ireland is one the the three priorities.

German DFM Spahn urged ECB exit

In Eurozone, German Deputy Finance Minister Jens Spahn urged ECB to exit from the ultra loose monetary policy soon. Spahn warned in a conference at the German foreign ministry that "unless monetary policy starts normalizing soon, negative side-effects will become more damaging." And, "regarding the euro zone, the ECB should be ready to exit the unconventional monetary policy not too late." However, there are also talks that ECB policy makers are likely still unconvinced by the inflation outlook even through headline CPI was at 1.9% in April. The key on ECB outlook will lie on the new staff economic projections to be released at the June ECB meeting.

BoJ Kuroda told PM Abe stimulus still needed

BoJ Governor Haruhiko Kuroda said he told Prime Minister Shinzo Abe that "Japan's economy is steadily recovering and will continue to grow above its potential." Kuroda also expressed his confidence that price will rise. Nonetheless as inflation is still far from the 2% target, he told Abe that "we will continue with out monetary easing program. it's generally expected that Kuroda will be given another five year term as BoJ Governor next year, after the current term ends.

On the data front...

Canada manufacturing shipments rose 1.0% mom in March, above expectation of 0.4% mom. Eurozone CPI was confirmed at 1.9% yoy in April, while core CPI was at 1.2% yoy. From UK, claimant counts rose 19.4k in April. Unemployment rate dropped to 4.6% in March. Average weekly earnings rose 2.4% 3moy in March. New Zealand PPI inputs rose 0.8% qoq in Q1, above expectation of 0.7% qoq. PPI outputs rose 1.4% qoq, above expectation of 1.1% qoq. Australia wage cost index rose 0.5% in qoq, meeting consensus. Westpac consumer sentiment dropped -1.1%. Japan machine orders rose 1.4% mom in March.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1003; (P) 1.1050 (R1) 1.1128; More....

Intraday bias in EUR/USD remains on the upside as current rally continues. The pair would target 138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245, which is close to 1.1298 key resistance. For now, rise from 1.0339 is still viewed as a corrective move. Hence we'd expect strong resistance below 1.1245/98 to limit upside and bring reversal. On the downside, below 1.1028 minor support will turn bias neutral and bring consolidation. But break of 1.0838 support is needed to indicate short term topping. Otherwise, further rise will remain in favor.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Inputs Q/Q Q1 | 0.80% | 0.70% | 1.00% | |

| 22:45 | NZD | PPI Outputs Q/Q Q1 | 1.40% | 1.10% | 1.50% | |

| 23:50 | JPY | Machine Orders M/M Mar | 1.40% | 2.50% | 1.50% | |

| 00:30 | AUD | Westpac Consumer Confidence May | -1.10% | -0.70% | ||

| 01:30 | AUD | Wage Cost Index Q/Q Q1 | 0.50% | 0.50% | 0.50% | |

| 04:30 | JPY | Industrial Production M/M Mar F | -1.90% | -2.10% | -2.10% | |

| 08:30 | GBP | Jobless Claims Change Apr | 19.4K | 25.5K | 33.5K | |

| 08:30 | GBP | Claimant Count Rate Apr | 2.30% | 2.20% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Mar | 2.40% | 2.40% | 2.30% | |

| 08:30 | GBP | ILO Unemployment Rate 3M Mar | 4.60% | 4.70% | 4.70% | |

| 09:00 | EUR | Eurozone CPI M/M Apr | 0.40% | 0.40% | 0.80% | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 1.90% | 1.90% | 1.90% | |

| 09:00 | EUR | Eurozone CPI - Core Y/Y Apr F | 1.20% | 1.20% | 1.20% | |

| 12:30 | CAD | Manufacturing Shipments M/M Mar | 1.00% | 0.40% | -0.20% | -0.60% |

| 14:30 | USD | Crude Oil Inventories | -2.5M | -5.2M |

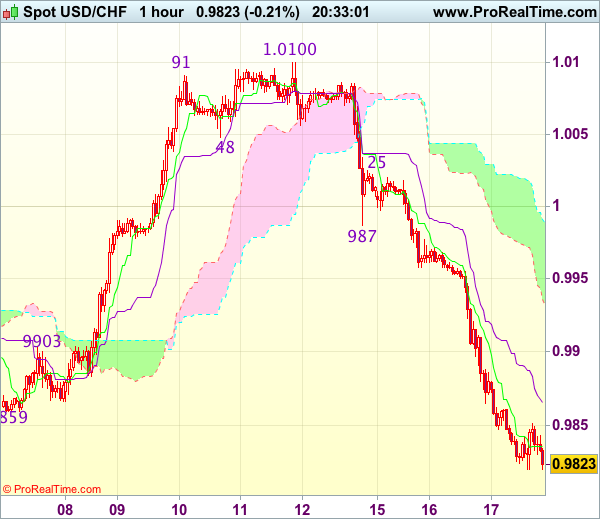

Trade Idea Update: USD/CHF – Sell at 0.9910

USD/CHF - 0.9825

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

As dollar has continued heading south and broke below indicated previous support at 0.9859, confirming our bearish view that the decline from 1.0108 top is still in progress, hence bearishness remains for this move to extend further weakness to 0.9813 support, break there would bring subsequent fall to 0.9790-95 (1.236 times projection of 1.0108-0.9859 measuring from 1.0100), however near term oversold condition should limit downside to 0.9770 and reckon 0.9745-50 would hold on first testing.

In view of this, would not chase would be prudent to sell dollar on recovery as 0.9910-20 should limit upside. Above 0.9940-45 would defer but only break of previous support at 0.9987 would abort and signal a temporary low is formed instead, risk rebound to 1.0000 and then test of 1.0025 resistance.

Trade Idea Update: GBP/USD – Stand aside

GBP/USD - 1.2961

Original strategy :

Sold at 1.2925, stopped at 1.2960

Position : - Short at 1.2925

Target : -

Stop : - 1.2960

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Current break of indicated resistance at 1.2958 has dampened our bearishness and suggests the correction from 1.2991 has ended at 1.2844 earlier, hence further gain towards this level would be seen, however, break there is needed to confirm recent upmove has resumed for gain to 1.2999-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance) and then headway to 1.3040-50 first.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.2900-10 would prolong consolidation and risk weakness towards support at 1.2866 but only break there would revive bearishness and signal the rebound from 1.2844 has ended, bring test of this this level, then 1.2831.

Trade Idea Update: EUR/USD – Buy at 1.1050

EUR/USD - 1.1113

Original strategy :

Buy at 1.1050, Target: 1.1150, Stop: 1.1015

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1050, Target: 1.1150, Stop: 1.1015

Position : -

Target : -

Stop : -

As the single currency has continued moving higher after recent rally above previous resistance at 1.1025 (now support), adding credence to our view that recent upmove has resumed and bullishness remains for further gain to 1.1150-55 (1.236 times projection of 1.0839-1.0990 measuring from 1.0965), then towards 1.1175-80, however, near term overbought condition should limit upside and reckon 1.1205-10 (1.618 times projection) would hold from here, bring retreat later.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as 1.1050 should limit downside. Below previous resistance at 1.1025 (now support) would defer and suggest top is possibly formed instead, risk test of another previous resistance at 1.0990 first.

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 112.22

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the decline from 114.37 has accelerated on dollar’s broad-based weakness, dampening our near term bullishness and downside risk remains for the selloff from 114.37 top to extend weakness to previous support at 112.09, break there would bring subsequent decline to 111.75-80 but near term oversold condition should limit downside to another previous support at 111.43, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above the Tenkan-Sen (now at 112.71) would bring recovery to the Kijun-Sen (now at 113.03) but previous support at 113.12 should limit upside and price should falter well below 113.40-50, bring another decline later.