Sample Category Title

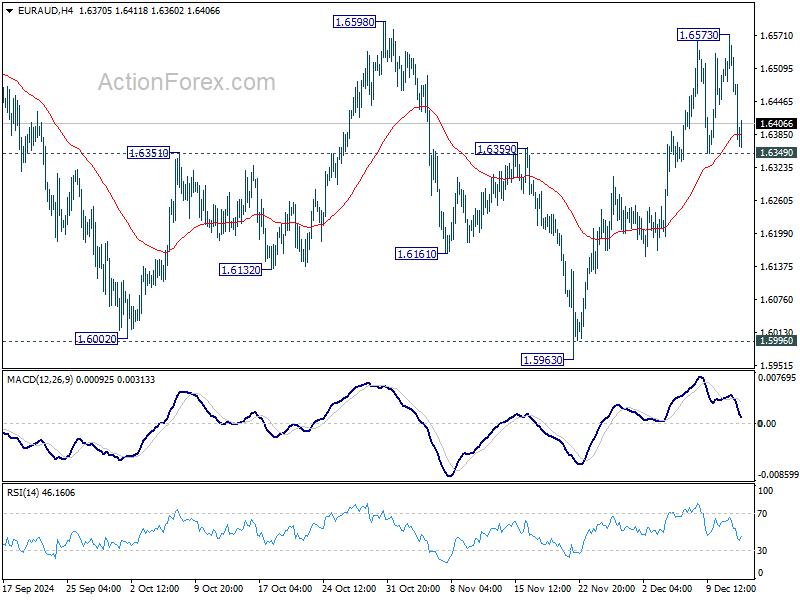

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6436; (P) 1.6506; (R1) 1.6551; More...

Intraday bias in EUR/AUD is turned neutral again with current retreat. But further rally remains in favor as long as 1.6349 support holds. On the upside, decisive break of 1.6598 resistance should confirm that whole fall from 1.7180 has complete with three waves down to 1.5963. Further rise should then be seen to retest 1.7180 next. Nevertheless, firm break of 1.6359 will indicate rejection by 16598, and turn bias back to the downside.

In the bigger picture, EUR/AUD is still holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction.

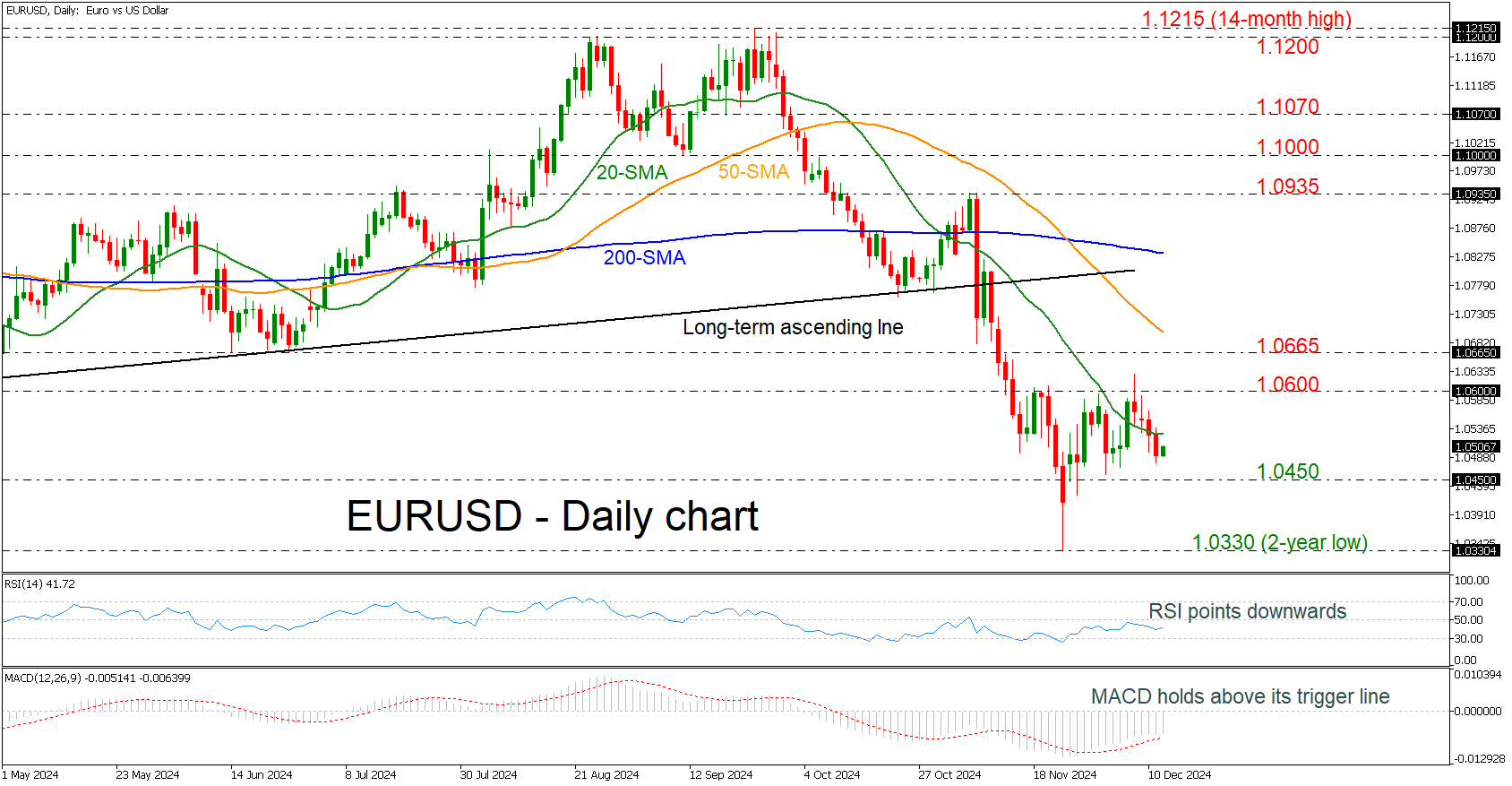

EURUSD Holds Near 1.0500 Again

- EURUSD retains neutral phase in short term

- MACD and RSI extend bearish momentum

EURUSD slides significantly after the failed attempt to surpass the 1.0600 round number and is currently challenging the 1.0500 handle. The pair has remained in a tight range of 1.0450–1.0600 over the last month, with the technical oscillators suggesting more declines. The RSI indicator is falling below the neutral threshold of 50, while the MACD is extending its negative momentum below the zero level.

More downside pressure could see traders revisiting the 1.0450 barrier ahead of the two-year low of 1.0330. Even lower, the pair may have a pause near November 2022’s low of 1.0220.

On the other hand, a climb above the 20-day simple moving average (SMA) at 1.0530 could send traders back to the 1.0600 key level again. If this time the market proves strong enough to break that area, then the next resistance could come from 1.0665.

To conclude, EURUSD has been strongly bearish since it peaked at 1.1215, and only a rally above the 200-day SMA at 1.0830 may switch the outlook to bullish.

SNB cuts by 50bps, projects weaker inflation and modest growth in 2025

SNB took a decisive step by lowering its policy rate by 50 basis points to 0.50%. In its accompanying statement, the central bank highlighted that underlying inflationary pressures have "decreased again" this quarter, warranting the larger-than-expected rate cut. SNB reiterated its commitment to "monitor the situation closely" and stated that it would "adjust its monetary policy if necessary."

The latest conditional inflation forecasts reflect a significantly subdued outlook, even with interest rate down from 1.00% to 0.50%.

For 2025, inflation is now projected at just 0.3%, a notable downgrade from the 0.6% forecast in September. However, the 2026 outlook saw a slight upward revision to 0.8%, from 0.7% previously.

Looking at some details, inflation is expected to decline sharply from 0.7% in Q4 2024 to a low of 0.2% in Q2 2025, before gradually recovering to 0.8% in 2026 and 0.7% in 2027. These figures underscore the SNB’s view of persistent deflationary risks, necessitating its proactive policy stance.

In terms of economic growth, SNB estimates GDP growth for 2024 to come in at around 1%, with a modest pickup to 1-1.5% expected in 2025. Despite this improvement, challenges remain, including slightly rising unemployment and declining utilization of production capacity.

(SNB) Swiss National Bank eases monetary policy and lowers SNB policy rate to 0.5%

The Swiss National Bank is lowering the SNB policy rate by 0.5 percentage points to 0.5%. The new policy rate applies from tomorrow, 13 December 2024. Banks’ sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold, and at 0% above this threshold. The SNB also remains willing to be active in the foreign exchange market as necessary.

Underlying inflationary pressure has decreased again this quarter. The SNB’s easing of monetary policy today takes this development into account. The SNB will continue to monitor the situation closely, and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

Inflation in the period since the last monetary policy assessment has again been lower than expected. It decreased from 1.1% in August to 0.7% in November. Both goods and services contributed to this decline. Overall, inflation in Switzerland is still being driven mainly by domestic services.

In the shorter term, the new conditional inflation forecast is below that of September. This above all reflects the lower-than-expected inflation in the case of oil products and food. Thanks to the policy rate cut today, there is little change in the medium term. The new forecast is within the range of price stability over the entire forecast horizon (cf. chart). It puts average annual inflation at 1.1% for 2024, 0.3% for 2025 and 0.8% for 2026 (cf. table). The forecast is based on the assumption that the SNB policy rate is 0.5% over the entire forecast horizon. Without today’s rate cut, the conditional inflation forecast would have been lower.

Global economic growth was moderate in the third quarter of 2024. Recently, inflation in many countries was again close to central banks’ targets. However, core inflation remained elevated. In anticipation of a continued decline in inflation, various central banks cut their policy rates further this quarter.

Underlying inflationary pressure abroad is likely to carry on easing gradually over the next quarters. At the same time, the moderate pace of global growth should continue.

Uncertainty about the economic outlook has increased in recent months. In particular, the future course of economic policy in the US is still uncertain, and political uncertainty has also risen in Europe. In addition, geopolitical tensions could result in weaker development of global economic activity. Equally, it cannot be ruled out that inflation could remain higher than expected in some countries.

As anticipated, GDP growth in Switzerland was only modest in the third quarter of 2024. Growth in the services sector was again somewhat stronger, while value added in manufacturing declined. There was a further slight increase in unemployment, and employment growth was only subdued. The utilisation of overall production capacity was normal.

The SNB anticipates GDP growth of around 1% for the current year. Thanks also to the easing of monetary policy in recent quarters, growth should pick up somewhat next year, albeit only slightly due to the moderate global economic activity. The SNB currently expects growth of between 1% and 1.5% for 2025. In this environment, unemployment should continue to rise slightly, while the utilisation of production capacity is likely to decline somewhat.

ECB Will Conduct a Third Consecutive (and 4th in total) 25 bps Rate Cut

Markets

November US CPI data came in bang in line with consensus. Monthly growth of 0.3% for both the headline and the core series resulted in annual readings of respectively 2.7% (from 2.6%) and 3.3% (stable). Contrarians betting on a status quo at next week’s FOMC meeting threw in the towel in absence of an upward surprise. The 25 bps rate cut is now fully discounted. The stalling disinflation process simultaneously strengthened the case for a Fed pause in January in anticipation of Trump’s inauguration and first official policy moves. The US yield curve initially bull steepened, but that morphed into a bear steepening pattern as tech and AI-stocks pushed Nasdaq to closing gains of 1.77%. The US $39bn 10-yr Note auction met with stellar demand, but couldn’t prevent more selling pressure into the bell. Daily changes on the US yield curve ranged between +0.9 bps (2-yr) and +6.3 bps (30-yr). We recently stressed the nascent bottoming out process at the (very) long end on (global) yield curves and find more evidence in Europe as well. German yield changes varied between -1.1 bp (2-yr) and +2.3 bps (30-yr) yesterday. The single currency abides to the rules of gravity going into today’s ECB decision with EUR/USD changing hands around 1.05 and EUR/GBP closing in on the post-brexit low of 0.8203.

The ECB will conduct a third consecutive (and 4th in total) 25 bps rate cut. A lower GDP and CPI outlook will be covered by uncertainty (and downside risks). It will prompt a different tone in the policy statement, erasing the expressed need to keep policy restrictive for as long as necessary to bring inflation sustainably back to 2%. Returning to forward looking decision making instead of data dependence allows the ECB early next year to ignore any possible hick-ups in a still bumpy inflation path, instead arguing that price stability will be achieved in the longer run. We expect those dovish twists to hold end of 2025 money market rates below neutral levels (+- 2.25%) even if we don’t think that this will eventually materialize. Apart from the most dovish governors, no ECB official suggested moving back below neutral. As (hawkish) ECB Schnabel pointed out, a stimulative monetary policy can help overcome cyclical economic weakness but doesn’t fix the structural issues Europe is struggling with. More curve steepening and a lower euro are today’s likely way forward.

News & Views

Brazil went big yesterday by raising the policy rate a more-than-anticipated 100 bps to 12.25%. The central bank (BCB) went even further and clearly indicated similar hikes over the next two meetings if the scenario unfolds as expected. The domestic economy keeps on booming and (underlying) inflation has increased further above the 3% (+/- 1.5ppt) target. Inflation expectations rose significantly to hover around 4.8% and 4.6% for this year and 2025 respectively. The central bank notes that the upside inflation risks mentioned last time have now materialized, turning the inflation scenario more adverse. Risks remain tilted to the upside and include a more prolonged period of deanchoring inflation expectations, a stronger economy and currency depreciation. The Brazilian real slid against USD with the latest downleg spanning from USD/BRL 5.4 mid-September to a record low around 6, fanning the inflation fire. The real has yet to react to yesterday’s monetary policy decision. The Brazilian central bank does not take a formal stand on the fiscal policy developments, including some spending cuts announced end of November, but concluded that market’s perceptions of it have only contributed to more adverse inflation dynamics.

Australian employment rose 35.6k in November, more than the 15.9k in October and above the 25k consensus estimate. Full time employment carried the headline figure by adding 52.6k jobs. The unemployment rate unexpectedly fell to 3.9%. The participation rate ease to 67%, be it from a historical high 67.1% in October. The Bureau of Statistics said that “Compared with outcomes before the COVID-19 pandemic, the unemployment and underemployment measures are still low, while trend employment and participation measures are around all-time highs. This suggests the labour market continues to be relatively tight.” The strong labour market report follows a dovish RBA-twist earlier this week. The RBA brought life in the December rate cut expectations. Such a move was priced in for two-thirds up until this morning. A first full rate cut is now only seen in April next year. Australian swap rates soar 11 bps at the front end of the curve. AUD/USD rebounds from recent lows sub 0.64 to 0.642.

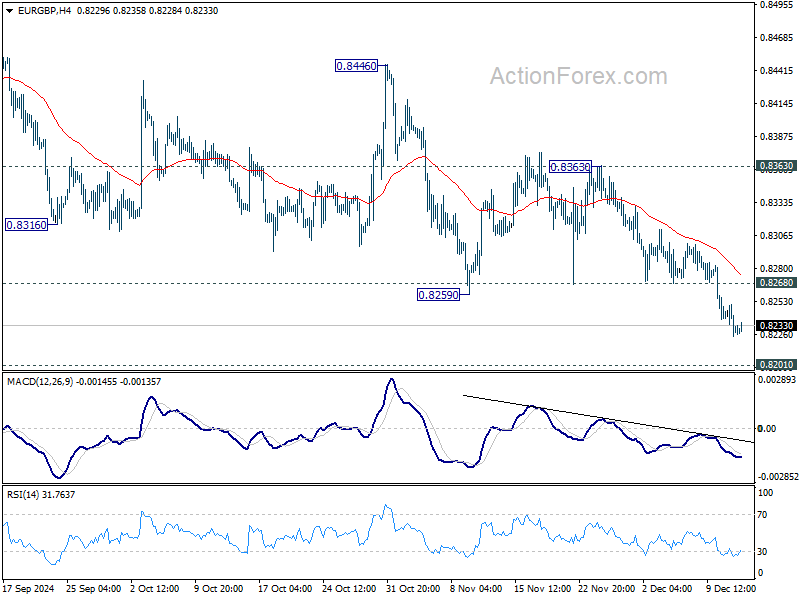

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8221; (P) 0.8236; (R1) 0.8248; More...

EUR/GBP's down trend is still in progress and intraday bias stays on the downside for 0.8201 key support. Strong support could be seen there to bring rebound. On the upside, above 0.8268 minor resistance will turn intraday bias neutral first. Further break of 0.8363 resistance will be the first signal of bullish trend reversal. However, sustained break of 0.8201 will carry larger bearish implications.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

SNB and ECB to Cut, Aussie Rebounds on Job Data

Australian Dollar staged an impressive rebound today, driven by robust employment data that surprised markets and cast doubt on the likelihood of a February rate cut by RBA. The stronger-than-expected labor market performance challenges the dovish sentiment established earlier in the week when RBA softened its inflation vigilance stance.

In the aftermath of RBA meeting, market participants had sharply increased their bets on a February rate cut, with swaps pricing in a 75% probability. However, today’s data shifted the narrative, bringing those odds down to around 50%.

The report highlighted the ongoing tightness in the labor market, suggesting that immediate easing may not be necessary. Still, the ultimate decision hinges on Q4 CPI data, set for release in late January. Without clear progress on disinflation, the RBA may opt to maintain its cautious approach, delaying any action until May until further confidence on inflation is gained.

In currency markets, Aussie leads gains today, followed by Kiwi and Euro. On the other hand, Dollar is the weakest performer, with Yen and Swiss Franc also under pressure. Sterling and the Canadian Dollar are mixed in the middle. Traders are now shifting their attention to SNB and ECB rate decisions scheduled later in the day.

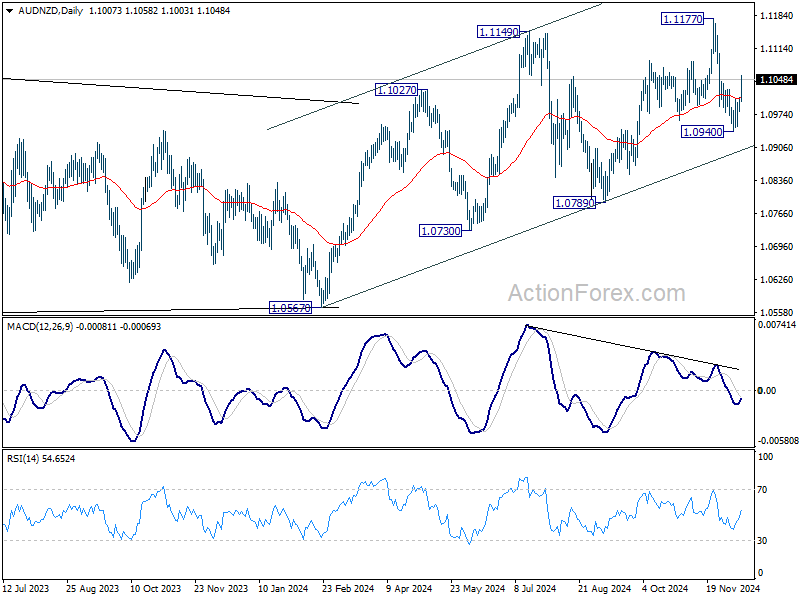

Technically, AUD/NZD's strong rebound today suggests that pull back from 1.1177 might have completed at 1.0940 already. The development also keeps the up trend from 1.0567 alive. Nevertheless, while further upside is likely in the near term, AUD/NZD's upside would likely be capped by 1.1177 resistance to extend sideway consolidations first.

In Asia, Nikkei rose 1.21%. Hong Kong HSI is up 1.63%. China Shanghai SSE is up 0.85%. Singapore Strait Times is up 0.35%. Japan 10-year JGB yield fell -0.0228 to 1.049. Overnight, DOW fell -0.22%. S&P 500 rose 0.87%. NASDAQ rose 1.77%. 10-year yield rose 0.50 to 4.271.

Australia’s employment data beats expectations, unemployment drops below to 3.9%

Australia’s labor market showed surprising resilience in November as employment grew by 35.6k, surpassing expectations of a 29.6k increase. The standout figure was the 52.6k gain in full-time jobs, offsetting a decline of -17k in part-time positions.

Unemployment rate fell significantly, dropping from 4.1% to 3.9%, well below the anticipated 4.2%. However, a slight dip in the participation rate, from a record high of 67.1% to 67.0%, tempered the optimism.

Employment-to-population ratio nudged up to 64.4%, matching levels from a year ago and maintaining its position 2.2% above pre-pandemic levels. Monthly hours worked showed no growth, indicating stability in workforce activity despite the overall gains in employment.

David Taylor, Head of Labour Statistics at the ABS, noted that an unusually high number of unemployed individuals transitioned into employment during November. This dynamic contributed to both the rise in job creation and the sharp fall in unemployment. Taylor also highlighted the role of population growth, which has bolstered labor supply and helped maintain the balance between employment growth and demographic expansion.

SNB and ECB in spotlight as markets gauge depth of cuts and dovish signals

Today’s focus is firmly on the monetary policy decisions from SNB and ECB, with markets eager to gauge not just the magnitude of the expected rate cuts but also the tone of their forward guidance. Both central banks are expected to ease, but the precise depth of the cuts and their outlook on future policy will drive market reactions.

SNB is widely anticipated to cut its policy rate by 25bps 1.00% to 0.75%. However, speculation of a more aggressive 50bps cut persists, with financial market pricing increasingly leaning toward this scenario.

SNB has considerable room to maneuver, given Switzerland’s inflation rate of just 0.7%—the lowest among major economies. However, with rates already close to zero, SNB must balance immediate economic support with preserving policy ammunition for the future.

After all, today’s move will not mark the end of the easing cycle of SNB, as economists project further reductions through 2025, driving the policy rate to 0.25% or even zero by the end of next year.

For ECB, the debate has also revolved around the scale of its next move. Recent speculation about a 50bps cut has largely been dismissed following comments from ECB officials, leaving a 25bps reduction in the Deposit Rate to 3.00% as the more probable outcome.

However, market participants are paying close attention to the tone of ECB’s statement and press conference. With inflation expected to settle earlier at target by mid-2025 amid weak economic activity, ECB would signal explicitly the need for sustained easing into next year.

Investors currently expect a cut at every meeting until mid-2025, with the Deposit Rate potentially reaching 1.75% by year-end. However, such an aggressive pace could bring rates below the neutral level.

In terms of market impact, EUR/CHF is the currency pair to watch. Outlook is clearly bearish with EUR/CHF staying well below falling 55 D EMA. However, in case of another dive, 0.9209 key support might continue to provide support for a bounce a second time, barring any drastic surprises. Meanwhile, there would be no clear confirmation of bullish reversal until decisive break of 55 D EMA (now at 0.9362).

Elsewhere

In addition to ECB and SNB, Canada building permits, US PPI and jobless claims will also be featured.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8221; (P) 0.8236; (R1) 0.8248; More...

EUR/GBP's down trend is still in progress and intraday bias stays on the downside for 0.8201 key support. Strong support could be seen there to bring rebound. On the upside, above 0.8268 minor resistance will turn intraday bias neutral first. Further break of 0.8363 resistance will be the first signal of bullish trend reversal. However, sustained break of 0.8201 will carry larger bearish implications.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

Rates and Chips

Yesterday’s US inflation data was the last possible barrier to the much-expected extra 25bp cut from the Federal Reserve (Fed) next week, and the release went well. The figures came spot on expectations. Headline inflation inched slightly higher from 2.6% to 2.7% while core inflation remained sticky at 3.3%. If you ask me, with Trump’s pro-growth policies and tariff threats threatening to give a positive jolt to inflation in the coming months, a core inflation figure that’s insistently above the 3% doesn’t necessarily call for an extra 25bp cut, but this is most probably what the Fed will do. The Fed will most probably cut one more time this year with activity on Fed funds futures assessing nearly 100% probability to it, and take a breather in January.

As such, the US 2-year yield is now around 4.16% - having held ground above the 4.10% mark, certainly on the thinking that the Fed should slow down rate cuts next year. The 10-year yield is advancing toward 4.30% level, up from 4.13% at the lowest of December, and the major indices rally with joy. The S&P500 closed a few points below an ATH yesterday, while Nasdaq 100 jumped 1.82% to an ATH. But it’s not only the Fed. It’s also tech related news. Google for example jumped nearly 5.5% to a record high on news that the company made a ‘major development’ in quantum computing using its Willow quantum chip that helped the company’s quantum computer to solve a problem in just five minutes instead of septillion years by using a supercomputer. The company didn’t give away any use case for such a powerful computing, and quantum computers are far from mass adoption, but the latest news gave hope to investors that the Willow chip could give them an advantage in their AI race. Before I move forward, quantum stocks gained yesterday on the news, Defiance Quantum ETF jumped to an ATH before giving back gains. The price moves in quantum will likely be volatile at this stage given that commercialization is not due in the foreseeable future, but chasing interesting entry levels is interesting. Coming back to my chip story, Broadcom – that’s due to announce earnings today - flirted with ATH yesterday on news that they are developing an AI chip with Apple – who is also interested in Amazon’s Trainium chips, mind you. Of course, the news that the Big Tech companies are now building their own chips to train their own AI models could be bad news for Nvidia which made around 50% of its last quarter revenue from the Big Tech companies. But happily, TSMC said that its sales rose 34% in November – hinting that AI demand remains strong despite the growing worries of slower spending. Nvidia gained more than 3% yesterday, while AMD rebounded 1.90% from the lowest level since summer.

In Europe, the news are much less future-oriented and exciting, to be honest. But the Stoxx 600 is better bid on hope that the European Central Bank (ECB) will step up its support to the economy. In this context, the ECB is expected to deliver another 25bp cut at today’s meeting. Some have been expecting the ECB to do more than that. Since Donald Trump won the US presidential election, the increased risks on European economies due to tariff threats brought some investors and analysts to bet for a 50bp cut as an immediate reaction. Others, like me, think that the ECB would better deliver a cautious 25bp cut today AND shift its focus from inflation to growth, as doing so will open the way for a series of rate cuts instead of a jumbo cut that the zone doesn’t need in a hurry. As I wrote earlier this week, the euro could avoid an aggressive selloff provided that the dovishness from the ECB has been already priced in – starting from Trump’s victory day. The EURUSD fell from around 1.10 down to 1.0340 over that period. As such, I wouldn’t be surprised to see the euro bulls resist to a dovish announcement – if Lagarde could convince investors that they are taking measures to boost growth and that the measures could work. Of course, there is no telling that a growth-supportive monetary policy will lead to growth – especially given that the member states are expected to tighten their fiscal policies to control their budget deficit, and that’s not necessarily growth supportive– yes I am looking at you, France and Germany. But a sufficiently supportive ECB stance and a contained euro depreciation could back a further rise in European stock valuations and help them to extend this year’s rally. Of course, the valuations on index level hide the ugly economic fundamentals of the Eurozone companies, as only a handful of the companies contributed to the gains at the index level. Those companies include SAP that benefits from the AI rally, Siemens, and Novo Nordisk. But the carmakers and luxury-stuff makers for example struggle big time. Therefore, stock picking in the European equity complex is a good idea.

Other than the ECB, the BoC cut by 50bp yesterday, and the SNB could opt for 50bp to counter the franc’s appreciation.

We Expect 25bp Rate Cut from ECB Today

In focus today

In the euro area, we expect the ECB to deliver a 25bp rate cut. Although that is the consensus, markets price in around a 15% probability of a 50bp cut this morning according to Reuters. Rather than focusing on the size of the rate cut, we should focus on where the policy rate will end in this cutting cycle, albeit we do not expect any verbal guidance on this. Markets may however interpret a 50bp cut as a signal of a lower terminal rate - and that may even be a signal that the ECB wants to send. For further details see ECB Preview - A disputed 25bp rate cut, 6 December.

In Switzerland, markets are pricing in around 35bp for the meeting and consensus favours the 25bp cut over the larger 50bp. We expect another cut in March with risks skewed towards further cuts.

In Sweden, we get the full Swedish inflation report for November. Last week's flash release showed a sharp uptick in CPIF to 1.9% - a whopping full percentage point above the Riksbank's forecast. Thus far, the flash estimates have proven reliable and as such we do not expect any revisions today.

In Norway, we expect the regional survey to signal continued restrained optimism among domestic corporates, indicating a 0.2-0.3% growth rate in the next quarter (Q1/25). In that case we expect Norges Bank to consider domestic growth 'as expected' and be neutral to the rate path in the monetary policy report next week, despite actual growth in Q3 being higher than anticipated. The crucial point will be the indicators for capacity utilization and labour shortage. Another significant lift in these measures of slack makes it more likely that Norges Bank will consider growth as 'accelerating and above trend'. Also, keep an eye on the expected wage growth for next year. A downward revision to around 4% should reduce the rate path directly, but also affect risk assessment as the risk of cost-driven inflation should abate.

In Japan, overnight we get the Bank of Japan's (BoJ) extensive quarterly Tankan business survey, which will shed some more light on how the economic recovery has fared in Q4. PMI data has been on the weak side. The survey will be scrutinised by the BoJ, and it will be key to the decision on the policy meeting next week.

Economic and market news

What happened yesterday

In the US, headline prices grew 0.3% m/m seasonally adjusted (cons. 0.3%, 2.7% y/y) while core inflation was also 0.3% (cons. 0.3%, 3.3% y/y), in line with consensus. The data is very volatile from one month to another, so it is important not to put too much weight on any single reading, but the overall signal is still positive for the Fed. Short-end UST yields ticked lower as markets have now basically fully priced in the Fed's rate cut next week.

In Canada, Bank of Canada delivered a 50bp cut, as expected by markets and most analysts. Importantly, the forward guidance included a hawkish twist, with the central bank no longer explicitly stating an expectation of further rate cuts. USD/CAD took a knee-jerk move lower amid the hawkish twist, while the reaction in Canadian yields was more mixed. A 50bp cut to 3.25% also meant that the policy rate was at the upper range of the BoC's estimate for the neutral rate. With the communication that day, it seemed increasingly likely that the BoC would slow down its incremental cut pace to at least 2x25, reaching its midpoint estimate for the neutral rate of 2.75% in March.

In China, the monetary authorities are considering a currency devaluation of the CNY according to Reuters who spoke to persons who have knowledge about the discussion. The reason for the consideration is US President elect Trump's threat of imposing even higher tariffs on goods produced in China, which could hit Chinese exports.

Equities: Global equities were higher yesterday with notable sectoral differences. Large-cap cyclical growth, particularly in consumer discretionary and communications services, registered markedly higher, while the majority of sectors, led by defensives, were lower. This divergence was also evident in the US indices' performance yesterday, with the Dow losing 0.2% and Nasdaq gaining 1.8%. We have discussed this phenomenon previously, but it bears repeating: This is a classic late-cycle scenario in which investors continue to chase the winners and abandon the losers, leading to a widening spread in relative valuations. In the US yesterday, the Dow registered a decrease of 0.2%, the S&P 500 increased by 0.8%, the Nasdaq rose by 1.8%, and the Russell 2000 saw a gain of 0.5%. Most Asian markets are higher this morning, and the same is true for European futures. US futures on major indices are all lower this morning.

FI: A waiting-for-today's-ECB trading session ended with very little volatility yesterday. German yields traded in a narrow 2bp range through the day across all maturities. The Bank of Canada's decision to cut 50bp was widely anticipated and thus did not inject volatility either. Bank of Canada left out the guidance of further cuts if their baseline outlook materialised. Markets are pricing 26bp for today's ECB meeting and a cumulative 155bp by end of next year.

FX: The market reaction to the in-line US November CPI print was modestly dovish. Front-end US yields initially edged lower following the release but later reversed higher. The USD strengthened broadly across the G10 space. The CAD outperformed in G10, supported by a hawkish 50bp BoC rate cut. EUR/USD declined to around 1.05. In the Scandi space, both NOK and SEK gained against the EUR, with EUR/NOK dropping to around 11.70 and EUR/SEK to just above 11.50. Meanwhile, EUR/GBP continued its downward trend, breaking below 0.8250 for the first time since early 2022. EUR/DKK is trading slightly on the strong side of the central parity ahead of today's ECB meeting. Elsewhere, oil prices have rebounded modestly this week. The market reaction to the in-line US November CPI print was modestly dovish. Front-end US yields initially edged lower following the release but later reversed higher. The USD strengthened broadly across the G10 space. The CAD outperformed in G10, supported by a hawkish 50bp BoC rate cut. EUR/USD declined to around 1.05. In the Scandi space, both NOK and SEK gained against the EUR, with EUR/NOK dropping to around 11.70 and EUR/SEK to just above 11.50. Meanwhile, EUR/GBP continued its downward trend, breaking below 0.8250 for the first time since early 2022. EUR/DKK is trading slightly on the strong side of the central parity ahead of today's ECB meeting. Elsewhere, oil prices have rebounded modestly this week.

SNB and ECB in spotlight as markets gauge depth of cuts and dovish signals

Today’s focus is firmly on the monetary policy decisions from SNB and ECB, with markets eager to gauge not just the magnitude of the expected rate cuts but also the tone of their forward guidance. Both central banks are expected to ease, but the precise depth of the cuts and their outlook on future policy will drive market reactions.

SNB is widely anticipated to cut its policy rate by 25bps 1.00% to 0.75%. However, speculation of a more aggressive 50bps cut persists, with financial market pricing increasingly leaning toward this scenario.

SNB has considerable room to maneuver, given Switzerland’s inflation rate of just 0.7%—the lowest among major economies. However, with rates already close to zero, SNB must balance immediate economic support with preserving policy ammunition for the future.

After all, today’s move will not mark the end of the easing cycle of SNB, as economists project further reductions through 2025, driving the policy rate to 0.25% or even zero by the end of next year.

For ECB, the debate has also revolved around the scale of its next move. Recent speculation about a 50bps cut has largely been dismissed following comments from ECB officials, leaving a 25bps reduction in the Deposit Rate to 3.00% as the more probable outcome.

However, market participants are paying close attention to the tone of ECB’s statement and press conference. With inflation expected to settle earlier at target by mid-2025 amid weak economic activity, ECB would signal explicitly the need for sustained easing into next year.

Investors currently expect a cut at every meeting until mid-2025, with the Deposit Rate potentially reaching 1.75% by year-end. However, such an aggressive pace could bring rates below the neutral level.

In terms of market impact, EUR/CHF is the currency pair to watch. Outlook is clearly bearish with EUR/CHF staying well below falling 55 D EMA. However, in case of another dive, 0.9209 key support might continue to provide support for a bounce a second time, barring any drastic surprises. Meanwhile, there would be no clear confirmation of bullish reversal until decisive break of 55 D EMA (now at 0.9362).