Sample Category Title

Trade Idea Update: EUR/USD – Stand aside

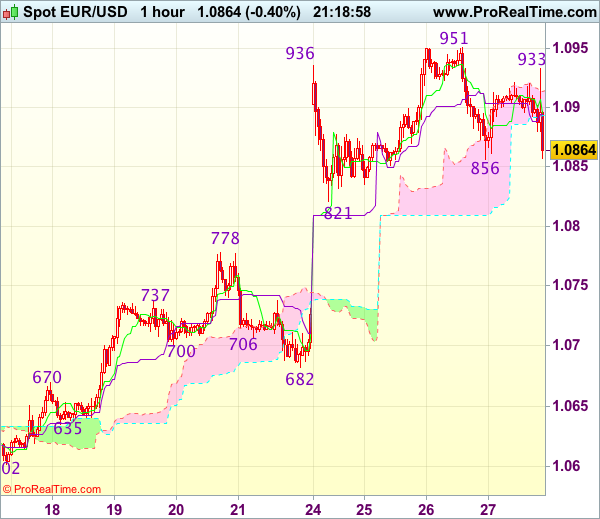

EUR/USD - 1.0860

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency met renewed selling interest at 1.0933 and has slipped again in NY morning, retaining our view that further consolidation below yesterday’s high of 1.0951 would be seen and test of support at 1.0821 cannot be ruled out, however, still reckon downside would be limited to 1.0800 and previous resistance at 1.0778 should hold from here, bring another rise later.

On the upside, above 1.0895-00 would bring test of said intra-day resistance at 1.0933 but break there is needed to signal the pullback from 1.0951 has ended, bring retest of this level later. Once this level is penetrated, this would extend recent upmove from 1.0340 low to 1.0975-80 and possibly towards 1.1000 which is likely to hold on first testing due to loss of momentum.

The Rising Risk from North Korea-and What it Means for Markets

A dangerous game of chicken is going on between the US and North Korea - this is a key risk factor for markets this year

The key driver driver behind the escalation is North Korea (NK) advancing fast in developing an Intercontinental Ballistic Missile (ICBM) that could reach the US with a nuclear warhead. The new leadership in the US has been clear that they will not allow this to happen and that the 'era of strategic patience' is over.

While the US is currently exercising brinkmanship, the bar for military intervention by the US is very high. A preemptive strike runs with a very high risk of a retaliatory response from North Korea on South Korea and/or Japan that could lead to a significant loss of life. Among the targets of retaliation would be the close to 30,000 US troops in South Korea and the South Korean capital Seoul, with a population of 10 million people.

Nevertheless, further escalation in the conflict is still likely. A trigger would be another nuclear test by North Korea and/or continued missile tests with a rising success rate. If the US shoots down a North Korean missile, it would also provoke North Korea and increase tensions.

First stage in a US plan to stop NK involves: (1) a strong show of force, (2) pressuring China to take a tougher stance on North Korea, (3) further sanctions through the UN and (4) continuing deployment of the THAAD anti-missile system in South Korea. If this is not enough, military intervention cannot be ruled out ultimately.

A further escalation of the US-NK crisis will be negative for risk sentiment - especially in Asia. It is also negative for commodity prices and the JPY and CNY, while it should be positive for bonds, USD and gold due to safe haven flows. If it comes to a war, the effects could be significant - at least for a period of time.

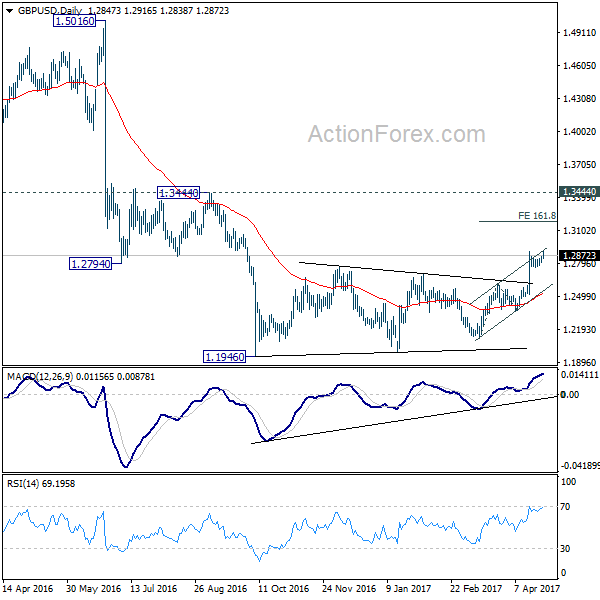

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2812; (P) 1.2838; (R1) 1.2871; More...

Intraday bias in GBP/USD stays mildly on the upside as rise from 1.2108 is resuming. Current rally would target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

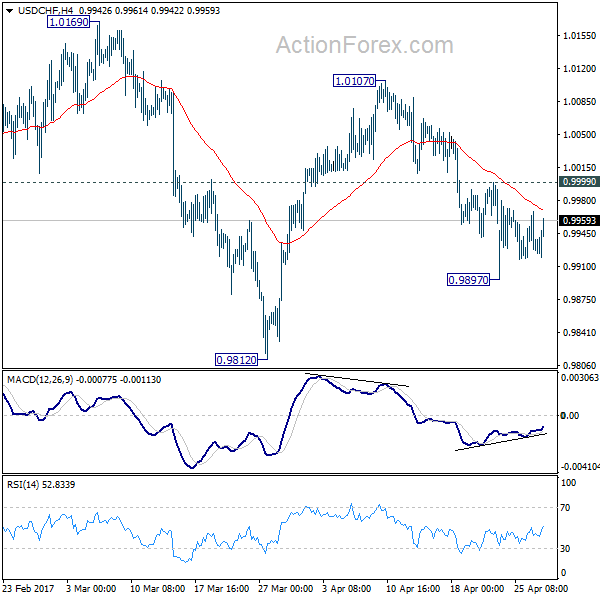

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9909; (P) 0.9939; (R1) 0.9960; More.....

USD/CHF is staying in tight range of 0.9897/0.9999 and intraday bias remains neutral for sideway trading. At this point, with 0.9999 minor resistance intact, deeper fall is still in favor. Below 0.9897 temporary low will turn bias to the downside for 0.9812 and possibly below. Nonetheless, whole decline from 1.0342 is seen as a correction. Hence, we'll look for bottoming signal below 0.9812. Meanwhile, on the upside, above 0.9999 minor resistance will turn bias back to the upside for 1.0107 resistance.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

Trade Idea Update: USD/JPY – Buy at 110.70

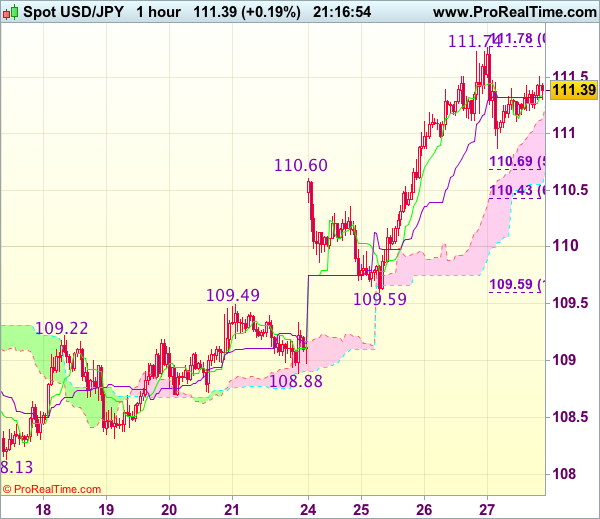

USD/JPY - 111.49

Original strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

As the greenback retreated after rising to 111.78 yesterday, suggesting consolidation below this level would be seen and pullback to 110.60-69 (previous resistance and 50% Fibonacci retracement of 109.59-111.78) cannot be ruled out, however, reckon downside would be limited and 110.40-45 (61.8% Fibonacci retracement) should hold, bring another rise later, above said resistance at 111.78 would signal recent rise from 108.13 low has resumed and extend further gain to 111.90-00 but overbought condition should prevent sharp move beyond another previous resistance at 112.20.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as previous resistance at 110.60 should limit downside, bring another rally. Below 110.40-45 (61.8% Fibonacci retracement of 109.59-111.78) would defer and suggest top is possibly formed, risk weakness to 109.80 but break of support at 109.59 is needed to provide confirmation.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.68; (P) 111.23; (R1) 111.60; More....

No change in USD/JPY's outlook. While it's losing some upside momentum, with 109.58 minor support intact, further rise is expected. Sustained trading above 111.58 support turned resistance will indicate that fall from 118.65 is merely a corrective move and has completed. Outlook will then be turned bullish for 115.49 resistance and above. However, break of 109.58 will argue that fall from 118.65 is still in progress and will turn bias to the downside for 108.12 and below.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. Current development suggests that it's not completed yet and is extending. In case of deeper decline, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

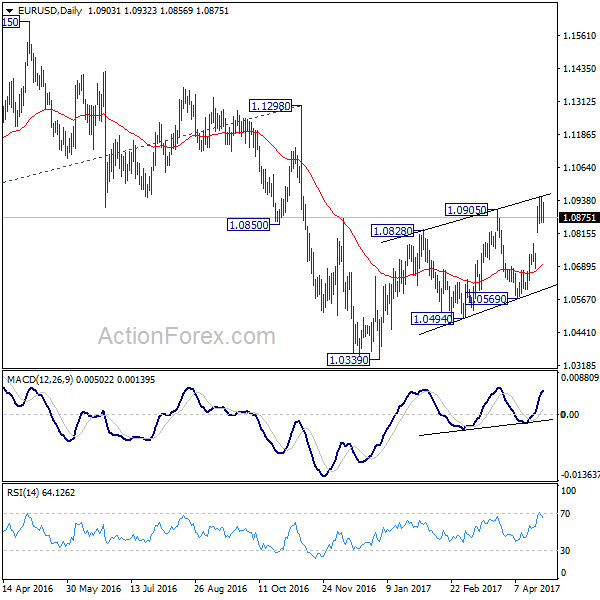

EUR/USD Trades Below 1.0900 Post the ECB Conference

The outcome of the first-round voting of the French presidential election pushed EUR/USD up, touching the highest level of 1.0950 on April 26 since November 10.

EUR/USD has been consolidating since April 24, flirting with the significant psychological level at 1.0900.

Today, the European Central Bank (ECB) announce its benchmark rate, marginal lending rate and deposit rate on hold, at 0.0%, 0.25% and -0.4% respectively, and leave the asset purchase programme unchanged of 60 billion Euro per month until December 2017,

Draghi stated that the economic recovery is becoming increasingly solid, and the downside risks have further diminished.

However, inflation has not yet seen a convincing upward trend. Therefore, the ECB will keep on providing support to keep inflation sustained.

Draghi's wordings gave mixed signals, the economy is recovering, however, the ECB seems to be unlikely to carry out the QE reduction in the near future.

Therefore, EUR/USD saw an initial rally, then followed by a fall, trading below the major resistance level at 1.0900.

The daily Stochastic Oscillator reading is above 80, suggesting a pullback.

The resistance level is at 1.0880, followed by 1.0900 and 1.0920.

The support line is at 1.0860, followed by 1.0835 and 1.0815.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0855; (P) 1.0903 (R1) 1.0950; More....

EUR/USD is staying in tight range below 1.0949 temporary top and intraday bias remains neutral for consolidations. At this point, another rise could be seen as long as 1.0777 support holds. But still, rise form 1.0339 is seen as a corrective move. Hence we'd pay attention to topping signal even if EUR/USD rises through 1.0949. On the downside, below 1.0777 minor support will turn bias to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Euro Steady as ECB Sees Recovery Becoming Increasing Solid, But Discourage Talks of Stimulus Exit

Euro is staying in tight range against Dollar and Yen, and weakens against Sterling. ECB kept monetary policies unchanged today as widely expected. The key interest rate is held at 0.00%, marginal lending facility rate at 0.25% and the deposit facility rate at -0.40%. Asset purchase at was also kept unchanged at EUR 60b per month. ECB President Mario Draghi said in the post meeting press conference that "downside risks have further diminished" as data confirmed "cyclical recovery of euro area economy is becoming increasingly solid". And he also described the improving growth and recovery as "solid and broad".

However, he also sounded cautious that there are still many "fragilities" to worry about. And the central bank reiterated that it "stands ready to increase" stimulus if the outlook for growth and inflation worsens. Such language is seen as a sign to discourage talk of stimulus exit. Regarding the result of French election, Draghi emphasized that "we actually don't do monetary policy based on likely election outcomes." And, "we have not seen sufficient evidence to alter our inflation outlook."

From Eurozone, German CPI accelerated to 2.0% yoy in April, up from 1.6% yoy and beat expectation of 1.9% yoy. German Gfk consumer sentiment improved to 10.2 in May, up from 9.8. Eurozone business climate rose to 1.09 in April, up from 0.83 beat expectation of 0.82. Economic confidence rose to 109.6, industrial confidence rose to 2.6, services confidence rose to 14.2. Consumer confidence was finalized at -3.6. Also from Europe, UK CBI realized sales rose to 38 in April. Swiss trade surplus came in at CHF 3.1b in March.

Markets yawned Trump's Tax Plan

Markets had basically no reaction to US President Donald Trump's tax reform plan. Trump revealed that there would be vigorous change to the tax system, for both individuals and businesses. For individuals, the new tax structure would reduce the number of tax brackets from seven to three (10%, 25% and 35%) and cut the top marginal rate from 39.6% to 35%. Meanwhile, several taxes, including the Alternative Minimum Tax, the estate tax, and the Obamacare tax on investment income, are repealed. For businesses, the corporate tax rate is reduced to 15%, from 35%. Tax rate for smaller pass-through businesses (such as partnerships) would also be 15%. Meanwhile, the reform plan proposes a switch to the territorial tax system under which US companies would only pay US tax on what they earn in the US. This is compared with the current system that US companies must pay tax on all their profits, regardless of where the profits are earned. The controversial border adjustment tax (BAT) does not appear in the announcement. Treasury Secretary Steve Mnuchin suggested that the current form of BAT might not work and there will be discussions on the revisions.

While the headlines look rosy, details on execution are not yet available. For instance, there is no information on how much of one's income would apply to each of the three rates. Therefore, it is impossible to understand who the beneficiaries of the new system are. The huge cut in corporate tax rate might cost the government a -USD 2T loss in revenue. Alternative revenue sources for the government remained uncertain. Congress' response to the proposal is the most critical as only it can make major tax law changes. The instant response of Democrats is condemnation of the plan as "fiscally irresponsible".

Released from US, initial jobless claims rose 14k to 257k in the week ended April 22, above expectation of 241k. Four week moving average dropped 0.5k to 242.25k. Continuing claims rose 10k to 1.99m in the week ended April 15. Also from US, trade deficit widened slightly to USD -64.8b in March. Wholesale inventories dropped -0.1% in March. Durable goods orders rose 0.7% in March, below expectation of 1.3%. Ex-auto sales dropped -0.2% in March, below expectation of 0.5%.

BoJ sounded most positive in 9 years

BoJ left monetary policies unchanged today as widely expected. Short-term interest rate target was held at -0.10%. And under the Yield Curve Control framework to guide 10 year bond yield to zero, the central bank will keep the annual asset purchase size at JPY 80T. BoJ sounded upbeat as it noted that "Japan's economy has been turning toward a moderate expansion." It should be noted it's the first time since 2008 that BoJ used the word "expansion" to describe the state of the economy. BoJ Governor Haruhiko Kuroda said in the press conference that inflation is expected to "accelerate towards 2%" even though it's currently at around 0%. Meanwhile, Kuroda still sounded a bit cautious that "talking about a specific exit strategy now would cause undue confusion in markets."

In the quarterly report of Outlook for Economic Activity and Prices, the central bank lowered inflation forecast for the current fiscal year to 1.4%, down from January's projection of 1.5%. Inflation forecast for fiscal 2018 was held unchanged at 1.7%. On the other hand, growth forecast for fiscal 2017 was revised up to 1.6%, from 1.5%. For fiscal 2018, growth is projected to be at 1.3%, up from prior estimation of 1.1%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0855; (P) 1.0903 (R1) 1.0950; More....

EUR/USD is staying in tight range below 1.0949 temporary top and intraday bias remains neutral for consolidations. At this point, another rise could be seen as long as 1.0777 support holds. But still, rise form 1.0339 is seen as a corrective move. Hence we'd pay attention to topping signal even if EUR/USD rises through 1.0949. On the downside, below 1.0777 minor support will turn bias to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | Monetary Policy Statement | |||||

| 01:30 | AUD | Import Price Index Q/Q Q1 | 1.20% | -0.50% | 0.20% | |

| 06:00 | CHF | Trade Balance (CHF) Mar | 3.10B | 3.01B | 3.12B | |

| 06:00 | EUR | German GfK Consumer Confidence May | 10.2 | 9.9 | 9.8 | |

| 09:00 | EUR | Eurozone Economic Confidence Apr | 109.6 | 108.1 | 107.9 | |

| 09:00 | EUR | Eurozone Business Climate Indicator Apr | 1.09 | 0.82 | 0.82 | 0.83 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | 2.6 | 1.3 | 1.2 | 1.3 |

| 09:00 | EUR | Eurozone Services Confidence Apr | 14.2 | 12.9 | 12.7 | 12.8 |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -3.6 | -3.6 | -3.6 | |

| 10:00 | GBP | CBI Realized Sales Apr | 38 | 6 | 9 | |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 11:45 | EUR | ECB Marginal Lending Facility | 0.25% | 0.25% | 0.25% | |

| 11:45 | EUR | ECB Deposit Facility Rate | -0.40% | -0.40% | -0.40% | |

| 11:45 | EUR | ECB Asset Purchase Target (EUR) Apr | 60B | 60B | 80B | |

| 12:00 | EUR | German CPI M/M Apr P | 0.00% | -0.10% | 0.20% | |

| 12:00 | EUR | German CPI Y/Y Apr P | 2.00% | 1.90% | 1.60% | |

| 12:30 | USD | Advance Goods Trade Balance Mar | -64.8B | -65.2B | -63.9B | -63.9B |

| 12:30 | USD | Wholesale Inventories Mar P | -0.10% | 0.30% | 0.40% | 0.20% |

| 12:30 | USD | Durable Goods Orders Mar P | 0.70% | 1.30% | 1.80% | |

| 12:30 | USD | Durables Ex Transportation Mar P | -0.20% | 0.50% | 0.50% | |

| 12:30 | USD | Initial Jobless Claims (22 APR) | 257K | 241K | 244K | 243K |

| 14:00 | USD | Pending Home Sales M/M Mar | -1.00% | 5.50% | ||

| 14:30 | USD | Natural Gas Storage | 54B |

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 27 April 2017

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council, which was also attended by the Commission Vice-President, Mr Dombrovskis.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at present or lower levels for an extended period of time, and well past the horizon of our net asset purchases. Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the new monthly pace of €60 billion, are intended to run until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The net purchases will be made alongside reinvestments of the principal payments from maturing securities purchased under the asset purchase programme.

Our monetary policy measures have continued to preserve the very favourable financing conditions that are necessary to secure a sustained convergence of inflation rates towards levels below, but close to, 2% over the medium term. Incoming data since our meeting in early March confirm that the cyclical recovery of the euro area economy is becoming increasingly solid and that downside risks have further diminished. At the same time, underlying inflation pressures continue to remain subdued and have yet to show a convincing upward trend. Moreover, the ongoing volatility in headline inflation underlines the need to look through transient developments in HICP inflation, which have no implication for the medium-term outlook for price stability.

A very substantial degree of monetary accommodation is still needed for underlying inflation pressures to build up and support headline inflation in the medium term. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase our asset purchase programme in terms of size and/or duration.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.5%, quarter on quarter, in the fourth quarter of 2016, following a growth rate of 0.4% in the third quarter. Incoming data, notably survey results, bolster our confidence that the ongoing economic expansion will continue to firm and broaden. The pass-through of our monetary policy measures is supporting domestic demand and facilitates the ongoing deleveraging process. The recovery in investment continues to benefit from very favourable financing conditions and improvements in corporate profitability. Employment gains, which are also benefiting from past labour market reforms, are supporting real disposable income and private consumption. Moreover, the signs of a stronger global recovery and increasing global trade suggest that foreign demand should increasingly add to the overall resilience of the economic expansion in the euro area. However, economic growth continues to be dampened by a sluggish pace of implementation of structural reforms, in particular in product markets, and by remaining balance sheet adjustment needs in a number of sectors. The risks surrounding the euro area growth outlook, while moving towards a more balanced configuration, are still tilted to the downside and relate predominantly to global factors.

Headline inflation has been recovering from the very low levels seen in 2016, largely owing to higher energy price increases. After reaching 2.0% in February 2017, euro area annual HICP inflation stood at 1.5% in March. This reflected mainly lower energy and unprocessed food price inflation, but also a decline in services price inflation. Looking ahead, on the basis of current futures prices for oil, headline inflation is likely to increase in April and thereafter to hover around current levels until the end of this year. However, as unutilised resources are still weighing on domestic wage and price formation, measures of underlying inflation remain low and are expected to rise only gradually over the medium term, supported by our monetary policy measures, the expected continuing economic recovery and the corresponding gradual absorption of slack.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual rate of growth of 4.7% in February 2017, after 4.8% in January. As in previous months, annual growth in M3 was mainly supported by its most liquid components, with the narrow monetary aggregate M1 expanding at an annual rate of 8.4% in February 2017, unchanged from the previous month.

The recovery in loan growth to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations declined to 2.0% in February 2017, from 2.3% in the previous month, while the annual growth rate of loans to households remained broadly stable at 2.3% in February. At the same time, the euro area bank lending survey for the first quarter of 2017 indicates that net loan demand has increased and bank lending conditions have further eased across all loan categories. The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for a continued very substantial degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2% without undue delay.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute much more decisively to strengthening economic growth. The implementation of structural reforms needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost productivity and potential output growth. Regarding fiscal policies, all countries should intensify efforts towards achieving a more growth-friendly composition of public finances. A full and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalances procedure over time and across countries remains crucial to enhance the resilience of the euro area economy.

We are now at your disposal for questions.