Sample Category Title

Elliott Wave View: INDU Further Downside

Short term Elliott Wave view in INDU ( Dow) suggest that instrument is showing 5 swings sequence from 3/03 peak (21018) favoring more downside. From 3/03 peak INDU is following a Double three Elliott wave Structure , where Minor wave W ended at 20579 low and Minor wave X ended at 20887 peak. Index has since broken below the 20412 low, suggesting the next leg lower in Minor wave Y has started already. The Internal Subdivision of Minor wave Y is also unfolding as Double three Elliott wave structure where Minute wave ((w)) ended at 20453 and Minute wave ((x)) bounce turns out to be a flat correction . Where the Minutte wave (a) ended at 20644 peak and Minutte wave (b) at 20379 low, above from there index could have ended the 5 waves in Minutte wave (c) of a flat within blue box area at yesterday’s peak 20629, while near term bounces fails below there & more importantly as far as pivot from 20888 peak Minute wave X connector’s peak stays intact index has scope to resume lower 1 more leg at least. we don’t like selling the index.

INDU 1 Hour Elliott Wave Chart

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD,AUDUSD, GBPCAD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EURUSD pair broke above daily Kijun-sen barrier at 1.0738 which capped upside attempts in past two day and met next target at 1.0776 (Fibonacci 61.8% retracement of 1.0906/1.0570 downleg. Initial attempt higher was short-lived, as the pair failed to hold gains and fell back bear key 1.0700 support after strong bearish signal was generated on formation of hourly double-top pattern.

Quick reversal was so far contained by the top of hourly Ichimoku cloud (spanned between 1.0715 & 1.0685) within 1.0700 support lies, marking strong support zone.

Dips are expected to hold above these supports in order to keep near-term studies in bullish alignment, as the pair remains biased higher overall, keeping positive tone ahead of Sunday’s French election.

However, close below Kijun-sen line and Thursday’s daily candle with long upper wick is expected to weigh on near-term action.

The pair may hold in extended consolidation between 1.0700 and 1.0738 ahead of releases of Eurozone PMI data, due on Friday which are expected to come out slightly below previous month’s figures and may further pressure the Euro on weaker-than-expected numbers.

Bearish scenario requires firm break below hourly Ichimoku cloud to signal further retracement of 1.0601/1.0776 upleg.

Otherwise, renewed attempts higher could be expected while 1.0715/00 supports hold. Close above daily Kijun-sen will be bullish signal, while lift above 1.0776 pivot would signal bullish continuation towards 1.0800/26 targets.

Support: 1.0715, 1.0700, 1.0684, 1.0658

Resistance: 1.0738, 1.0777, 1.0800, 1.0826

USD/JPY

USD JPY pair is on track for the second consecutive bullish daily close, signalling that consolidation above fresh low at 108.11 may extend higher. Thursday’s rally that firmly broke above 200SMA (108.87) and now acting as support, also cracked next pivot at 109.43 (Fibonacci 38.2% retracement of 111.57/108.11 downleg), signalled fresh strength of the dollar, despite weaker-than-expected releases of US economic indicators. US weekly jobless claims rose by 10K to 244K, above forecasted 242K, while Philadelphia Fed Manufacturing Index came at 22.0 in April, missing forecast at 25.0 and holding well below 32.8 release of March.

Extended recovery on close above 109.43 may challenge next strong barriers at 109.84 (daily Tenkan-sen) and psychological 110.00 barrier, as daily indicators that emerged from oversold territory show more room at the upside.

The pair is also on track for positive weekly close after two consecutive weeks in red which may signal further recovery.

Firmer bullish signal could be expected on sustained break above 109.84/110.00 pivots.

Support: 108.85, 108.68, 108.32, 108.11

Resistance: 109.48, 109.84, 110.00, 110.25

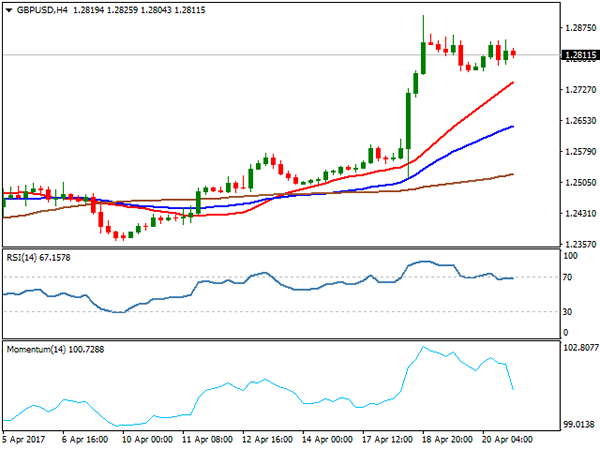

GBP/USD

GBPUSD currency pair remains in extended consolidation below fresh multi-month high at 1.2905, with downside being limited at 1.2770 (lows of Wed / Thu). Consolidation is forming bullish flag pattern on 4-hr chart which may signal fresh upside attempts towards 1.2905 and attack at psychological 1.3000 barrier in extension. Strong bullish sentiment continues to underpin the pound, along with bullish technical studies.

However, risk of deeper correction remains on the table, signalled by extended daily studies, as daily RSI and slow stochastic are hovering around overbought boundary line, but remain in sideways mode in the near-term and without firmer bearish signal so far.

On the other side, cable is on track for the second strong weekly close which is seen supportive for fresh advance.

Initial support lies at 1.2770, guarding 1.2750 (Fibonacci 38.2% retracement of 1.2500/1.2905 rally) and firm break here would generate stronger bearish signal for extended pullback.

The pair is looking for release of UK Retail Sales data for March on Friday, which may impact pair near-term action. Monthly Retail Sales are forecasted at -0.2% in March, well below Feb’s 1.4% release, with forecast for annualized Retail Sales at 3.4%, also being under previous month’s release at 3.7%.

Support: 1.2701, 1.2750, 1.2702, 1.2654

Resistance: 1.2846, 1.2859, 1.2905, 1.2950

AUDUSD

The AUDUSD pair recovered part of past two-day strong fall from 0.7610 that found footstep at 0.7490, just ahead of key near-term support at 0.7472 (lows of Apr 10,11,12 / base of thick daily Ichimoku cloud). Thursday’s bounce could be seen as a breather of downmove from 0.7610, before final attack at 0.7472 pivot, as daily technical studies remain in firm bearish setup and extended upticks on Thursday were capped under 200SMA (0.7550) and remain below strong resistance zone at 0.7541/50, formed by daily Tenkan-sen and 200SMA.

While the latter barriers hold, the downside is expected to remain at risk for renewed attempt through 0.7472, which would signal stronger bearish acceleration and expose targets at 0.7453 (50% retracement of 0.7158/0.7749 rally) and 0.7384 (Fibonacci 61.8% retracement) in extension.

Alternative scenario needs firm break and close above 200SMA to shift near-term focus higher.

Support: 0.7510, 0.7490, 0.7472, 0.7453

Resistance: 0.7541, 0.7550, 0.7576, 0.7596

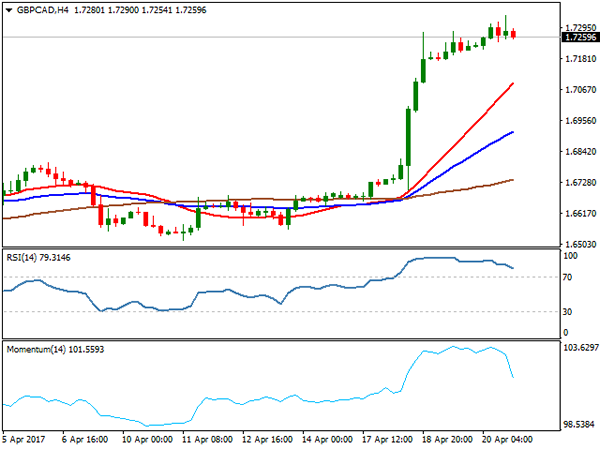

GBPCAD

The GBPCAD cross maintains firm bullish tone and posted fresh high at 1.7340, the highest level since mid-September 2016. The pair continues to move higher despite strongly overbought daily studies, which are lacking to produce any firmer bearish signal. However, correction should be anticipated before the pair attacks next target at 1.7436 (50% retracement of Jun/Oct 2016 1.9127/1.5745 descend.

Daily candles with long upper wicks could be seen as initial signal of strong rally running out of steam.

Initial supports lay at 1.7215/1.7176, with 1.7024/00 zone expected to ideally contain correction.

Support: 1.7215, 1.7176, 1.7145, 1.7100

Resistance: 1.7340, 1.7436, 1.7524, 1.7542

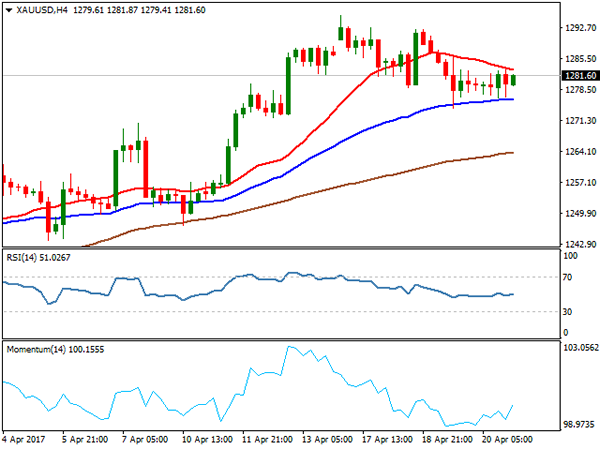

GOLD

Spot Gold recovered part of losses of the previous day on Thursday, recovering from correction low at $1274, after pullback was contained by Fibonacci 38.2% retracement of $1243/$1295 upleg. The yellow metal bounced after the biggest one-day drop since Mar 30, after weaker than expected US jobs and manufacturing data released on Thursday, dented the tone of strengthening of US economy. Gold is also eyeing French election on Sunday, which may boost its existing safe haven appeal, built on recent uncertainty on rising geopolitical tensions that triggered strong risk-off mode among the traders.

From technical point of view, overall structure remains firmly bullish, with corrective easing on overbought studies seen preceding fresh upside actions.

Technical studies on lower timeframes are mixed and suggest prolonged consolidation phase. Thursday’s recovery was capped by thin hourly cloud (spanned between $1281 & $1283), break above which would gain fresh bullish momentum for further retracement of $1295/$1274 bear-leg and expose pivots at $1287 (Fibonacci 61.8%) and lower top at $1292.

Conversely, weakness below $1274 and violation of next pivot at $1271 (daily Tenkan-sen) would weaken near-term structure and risk stronger correction.

Support: 1276, 1274, 1275, 1271

Resistance: 1283, 1287, 1292, 1295

WTI CRUDE OIL

WTI oil remained in red on Thursday but managed to hold above Wednesday’s spike low at $50.06, as concerns over rising U.S. oil production offset bullish comments from oil producers on a possible extension to the OPEC-led deal to cut global supply. Oil price moved in and out of positive territory in volatile Thursday’s trading, but settled lower, despite bullish comments from OPEC members Saudi Arabia and Kuwait concerning a possible extension to the OPEC-led deal to cut global supply.

Technical studies remain negatively aligned and keep downside at risk, as price approached cracked Kijun-sen support at $50.40 and see risk of renewed attack at psychological $50.00 support, as the price closed below thickening daily Ichimoku cloud, which is seen as negative signal.

Support: 50.40, 50.00, 49.62, 48.92

Resistance: 51.36, 51.54, 51.84, 51.90

DJIA

Dow Jones bounced on Thursday and made strong bullish close after two days in red. The price found footstep at at 20310 and returned back into thick daily cloud after closing below cloud base on Wednesday, signalling false break lower.

Wall Street was higher on Thursday, led by a sharp rally in the shares of American Express , after the company posted better than expected earnings, as comments of US Treasury secretary Mnuchin on tax reform lifted sentiment.

Fresh rally on Thursday improved Dow’ s near-term sentiment, as Thursday’s rally marks the biggest one-day gains since Mar 1 and rally also cracked significant resistance at 20500 (daily Tenkan-sen). Recovery needs to regain next pivots at 20580 and 20669 (daily Kijun-sen) to expose daily Ichimoku cloud top at 20757 and signal stronger recovery on break.

On the downside, daily cloud base is expected to hold and maintain fresh bullish sentiment.

Support: 20500, 20385, 20310, 20211

Resistance: 20567, 20580, 20669, 20757

FTSE100

FTSE index is holding in narrowing consolidation for the second day, following strong fall on Tuesday, which so far found footstep at 7032. Firm bearish setup on daily technical studies keeps the downside in focus, as strong bearish sentiment remains in play on firm pound.

The price is looking for test of psychological 7000 support, break of which will open way towards next pivotal support at 6969 (Fibonacci 61.8% retracement of larger 6675/7444 rally.

Recovery attempts were limited for now and capped at 7092 (Fibonacci 23.6% of 7285/7032 fall) keeping intact more significant barriers at 7129 (Fibonacci 38.2%) and 7147 (broken 100SMA) which guard upper triggers at 7189/97 (daily Tenkan-sen / Ichimoku cloud base).

Support: 7032, 7024, 7000, 6969

Resistance: 7070, 7092, 7144, 7192

DAX

DAX ended Thursday’s trading positively, after spiking lower to 11962, but repeated probe below 12000 handle was short-lived and contained by rising 55SMA. Index was dragged higher by improved sentiment and Wall St rally and bounced back to broken Fibonacci 61.8% support at 12081, which capped the rally on Thursday.

Daily studies remain weak, but oversold conditions suggest extended correction, as daily indicators are turning up.

We look for recovery extension to 12133 (Fibonacci 38.2% of 12410/11962 pullback) which is expected to ideally cap, as barrier is reinforced by bearish-cross of daily Tenkan-sen / Kijun-sen lines.

Only sustained break above the latter would improve the structure and signal further recovery.

Support: 12026, 11962, 11943, 11878

Resistance: 12081, 12133, 12144, 12220

Countdown to the French Election

First there was Brexit, then Trump and now it's the French election; or at least that's the narrative playing out in the markets. We take a closer look. The Australian dollar was the top performer Thursday while the yen lagged. The Japan Nikkei PMI is due next. The Premium Insights closed the EURCAD long at 1.4495 for a 235-pip gain in order to make a way for a tactical dual EUR trade on Friday ahead of Sunday's French elections.

Polls showed fractional momentum for Macron, helping to boost the CAC-40 in countdown mode to the Sunday's 1st round vote. That uptick may be telling because a large number of voters said they were undecided earlier in the month.

A poll from Harris showed Macron at 24.5%, Le Pen at 21%, Fillon at 20% and Melenchon at 19%. Given the margin of error and other factors like turnout and undecideds, it's conceivable the second round could be the far right candidate Le Pen and the far left candidate Melenchon. Polls show Melenchon would win that contest but German Fin Min Schaeuble called it a 'nightmare scenario' because both are euroskeptics.

What's important to remember is that's a highly unlikely scenario and the only result that could immediately upend the euro. If Macron finishes in the top-two and moves to the runoff, he's heavily favoured against any of the candidates. Fillon would also be a big favorite against Le Pen or Melenchon.

So while the market sees this as a potential redux of Brexit or Trump, it would take a far bigger swing. Brexit polls were close in the days ahead of the vote and Trump lost the popular vote but won the electoral college. In France, it's a national popular vote so polling is simplified.

That said, there is always the risk that voters are playing coy with pollsters again or could swing late. The risks may be even higher after what looked like a terrorist attack on the Champs Elysee late Thursday. That alone could add to jitters Friday.

After talking with many traders and analysts, there is a distinct fear of history repeating itself but those fears (and market pricing) overstate the odds of a major surprise.

Sunday Afternoon Volatility

Watch for exit polls hitting at 8 pm Paris time on Sunday (7 pm London, 2 pm New York), coinciding with the market open in the Pacific.

Before that, we'll watch for continue comments from leaders at IMF meetings in Washington and the Japan Nikkei PMI at 0030 GMT. The prior was 52.4.

Stating the Obvious. SP500 is in a Bull Market

It's always nice to end the week with the obvious and you don't get much more obvious than this bullish setup on the S&P 500.

S&P 500 Daily:

The SP500 daily chart simply shows the textbook bull market that we've spoken about on the blog previously.

Look left to right and you can see that price is going up. You really don't need me to draw a trend line to show you that it's in a bull market no matter which higher time frame chart you click on.

S&P 500 4 Hourly:

Inside the higher time frame bullish trend, price has been drifting sideways and printed what looks to me like some sort of flag.

USDCAD Loonie Flat After Mnuchin Boosts USD

The Canadian dollar will end up near where it started the trading session. The USD/CAD is trading at 1.3476 as the pair was caught in a tight trading range were the US dollar weakness started dissipating as the session wore on. The price of oil continued on a downward trend, but there as a ray of hope for higher prices as Organization of the Petroleum Exporting Countries (OPEC) members Saudi Arabia and Kuwait signalled that an extension to the production cut agreement is likely ahead of a general meeting of the organization this weekend. There are rumours that even non-OPEC members who are part of the deal like Russia are on board with extending the original six month term.

Several think tanks and economic agencies have warned about Canadian real estate overheating and following the lead from Vancouver, Ontario announced a 15 percent tax on property purchases by foreign buyers who don't intend to reside in Canada. The tax is effectively immediately and aimed at curbing prices in Toronto and surrounding areas where properties have jumped 33 percent year over year. The move has been triggered by backlash from residents who have seen housing prices sky rocket ahead of the June provincial elections. The same tax applied in Vancouver is seen as resulting in a 9 percent drop when compared to last year.

US President Donald Trump took aim at the Canadian dairy industry as part of another attack on NAFTA. Canadian Prime Minister Justin Trudeau responded to those comments by pointing out that the US has a dairy surplus with Canada and that regarding agriculture every country protects, for good reason. The USD is still reeling from comments made by Trump who said the greenback was too strong prompting a sell off of the currency. Geopolitical risk is also on the rise as US rhetoric against North Korea has escalated and the French presidential elections have markets on edge.

The USD/CAD lost 0.032 percent in the last 24 hours. The pair is trading at 1.3476 in a tight range on Thursday. The price of oil has been volatile as OPEC comments and US production have kept the price of a barrel of crude around $50. The USD has regained some traction after the comments from US Secretary of Treasury Mnuchin in Washington, but not enough to fully offset earlier losses triggered by Trump's comments on the strength of the US dollar. The loonie is flat as there will be further quotes from Washington as the IMF/World Bank summit continues.

Oil fell 0.548 percent on Thursday. The price of West Texas is trading at $50.26 in a session where crude almost broke through the $51 price level but the battle between higher US production and the Organization of the Petroleum Exporting Countries (OPEC) production cuts continues. Saudi Arabia and Kuwait made comments on the possible extension of the deal with producers such as Russia theoretically on board. The rise in gasoline inventories on Wednesday, specially ahead of the US driving season, has put the black stuff on the back foot as there still seems to be more supply than demand despite the cuts from OPEC and non-OPEC producers.

Market events to watch this week:

Thursday, April 20

- 8:30am USD Philly Fed Manufacturing Index

- 8:30am USD Unemployment Claims

- 11:30am GBP BOE Gov Carney Speaks

- 12:30pm GBP BOE Gov Carney Speaks

- 1:15pm USD Treasury Sec Mnuchin Speaks

Friday, April 21

- 4:30am GBP Retail Sales m/m

- 8:30am CAD CPI m/m

Saturday, April 22

- All Day OPEC Meeting

Sunday, April 23

- All Day French Elections

*All times EDT

French Presidential Election Outcome Raising Market Anxiety

No majority win will result in a 2nd round in May 7

French voters will cast their ballots in the presidential elections on Sunday, April 23. The results will have a significant impact on the EUR as the tight 4 way race has could result in a variety of uncertain scenarios. Currently four candidates: Marine Le Pen, Emmanuel Macron, Francois Fillon and Jean-Luc Melenchon are close to evenly splitting the vote amongst themselves which means that regardless of who wins, it won't be a majority win. The second round will be held on May 7, but as more voters grow tired of the campaign and the fact that their vote will only decide who goes through to the run-off absenteeism expectations are high complicating matters even more. The EUR will be priced according to the eventual combination of the two politicians who go through with the best case scenario for the single currency the more market friendly Macron and Fillon and at the other end of the spectrum both extremists candidates Le Pen and Melenchon.

Marine Le Pen has been the highest profile candidate running on a protectionist platform and is the biggest eurosceptic. Le Pen poll numbers have always put her through in the second round but always losing by a wide margin as her view are too polarizing and voters will default to their second choice if their candidate did not make it to the run off. The French presidential campaign has been so volatile that Macron, the most inexperienced at this stage and with a new party and Melenchon have quickly built strong momentum, but also signalling the fickleness of voters at this stage.

Political uncertainty has increased its influence on global markets after the shocks of the Brexit referendum outcome and the election of Donald Trump. Pollsters were pointing to an altogether different result for both which the markets had already priced in, only to be caught on the wrong side as forecasters had missed the mark. The already packed election calendar in Europe just got another entry as the British Prime Minister Theresa May called for a snap election on June 8. The French presidential elections will be eclipsed by the parliamentary elections in June 11 where another lack of majority is expected leading to a comprised cohabitation between political parties.

The EUR/USD gained 0.048 in the last 24 hours. The single currency is trading at 1.0717 and has stayed on a tight trading range that has seen the euro up as Macron's poll numbers rise, but remains pressured by the ghost of high abstention numbers as there is almost a guarantee of a second round in the French elections this weekend. The tight race has put the worst case scenario for the markets of two extreme candidates making it through to the second round with little possibility of consolidating a coalition in the upcoming parliamentary elections.

The Brexit referendum as well as rhetoric from Le Pen has resonated with part of the French electorate which while not a high possibility Frexit is still in the cards putting downward pressure on the EUR as the stability of the Union is once again threatened. MarketPulse VP of Research Dean Popplewell wrote about the different French election scenarios

The economy of the European Union has shown signs of life and while not completely out of the woods it has given more breathing room to the European Central Bank (ECB) that after reaching negative rates and a massive stimulus program was running out of monetary policy tools to boost growth. The International Monetary Fund (IMF) has upgraded global growth, but now the biggest risks come from more protectionist governments and their quest for one-sided gains that appear to be directly lifted from the political campaigns around the globe.

Market events to watch this week:

Friday, April 21

- 4:30am GBP Retail Sales m/m

- 8:30am CAD CPI m/m

Saturday, April 22

- All Day OPEC Meeting

Sunday, April 23

- All Day French Elections

*All times EDT

Gold Unchanged on Higher Jobless Claims and French Election Jitters

Gold is unchanged in the Thursday session, after posting losses on Wednesday. In North American trade, gold is trading at $1279.91 per ounce. On the release front, manufacturing and employment numbers were soft, as the Philly Fed Manufacturing Index and unemployment claims missed their estimates. Later in the day, US Treasury Secretary Robert Mnuchin will deliver remarks in Washington.

Gold prices have climbed sharply in April, with gains of 2.6 percent. The base metal has benefited from geopolitical tensions in Syria and North Korea, as well as uncertainty over the French election on April 23. These concerns have dampened risk appetite, as investors have snapped up gold, traditionally a safe-haven asset.The French election race is one of the tightest in decades, with the four front-runners clustered within a few percentage points. Given the closeness and unpredictability of the election, the latest opinion polls are moving the markets. On Thursday, a Harris Interactive opinion poll showed centrist Emmanuel Macron gaining ground, with 25% of the vote. Far-right candidate Marine Le Pen follows with 22%. Next are Republican candidate Francois Fillon and left-wing candidate Jean-Luc Melenchon, both tied at 19%. Le Pen and Melenchon are both running on an anti-EU platform, so the markets are cheering for Macron and Fillion. We can expect more volatility from gold as the turbulent election winds up and French voters have their say.

With the US economy continuing to perform well, the markets are expecting the Fed to continue to gradually raise rates in 2017. The Fed has broadly hinted that it plans two more rate hikes this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March are likely to make the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. The odds of a June hike have slipped to 46% according to the CME Group, down sharply from 65% in early April.

Pound Higher as US Manufacturing, Job Numbers Disappoint

GBP/USD has posted gains on Thursday, erasing most of the losses which marked the Wednesday session. In North American trade, GBP/USD is trading at 1.2830. There are no British economic releases on the schedule, although the markets are keeping an eye on BoE Governor Mark Carney, who will speak at two events in Washington. In the US, manufacturing and employment numbers were soft, as the Philly Fed Manufacturing Index and unemployment claims missed their estimates. Later in the day, US Treasury Secretary Robert Mnuchin will deliver remarks in Washington. On Friday, the UK releases Retail Sales, which is expected to decline 0.3%. The US will publish Existing Home Sales, with a forecast of 5.61 million.

It's been a great week for the pound, as GBP/USD has jumped 2.4 percent. On Tuesday, the currency punched above 1.29, its highest level since October 2016, on the news that Prime Minister May had called a snap national election on June 8. The announcement caught the markets by surprise, as the government's term runs until 2020 and May had previously said that she would not call early elections. May's Conservative Party currently has 330 seats in Parliament, which is a slim majority of just 17 seats. If, as current opinion polls predict, the government wins a larger majority, this would likely propel the pound to higher levels.

With the US economy continuing to perform well, the markets are expecting the Fed to continue to gradually raise rates in 2017. The Fed has broadly hinted that it plans two more rate hikes this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March are likely to make the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. The odds of a June hike have slipped to 46% according to the CME Group, down sharply from 65% in early April.

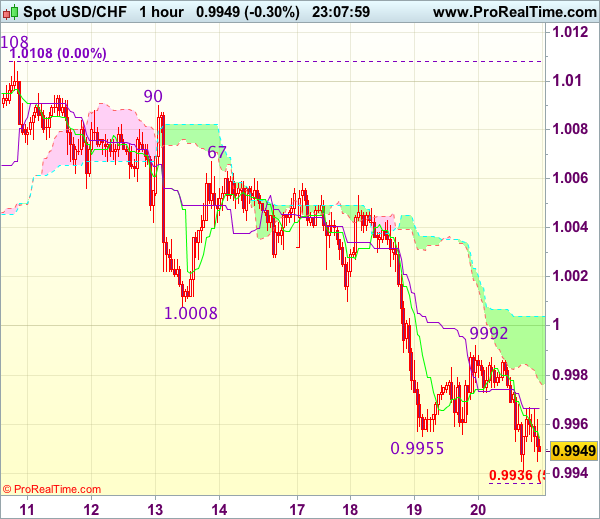

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9945

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9955

Kijun-Sen level : 0.9967

Ichimoku cloud top : 1.0004

Ichimoku cloud bottom : 0.9978

Original strategy :

Exit short entered at 1.0000,

Position : - Short at 1.0000

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback has remained under pressure and mild downside bias remains for recent decline from 1.0108 top to extend weakness to 0.9935-38 (50% projection of 1.0067-0.9955 measuring from 0.9992) and then 0.9926 (61.8% Fibonacci retracement of 0.9813-1.0108) but reckon 0.9900-05 (1.618 times projection of 1.0108-1.0008 measuring from 1.0067) would hold, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above resistance at 0.9992 would suggest low is possibly formed but break of previous support at 1.0008 is needed to add credence to this view, bring a stronger rebound to 1.0020-30.

Elliott Wave Analysis: Gold Can Face Some Corrective Retracement In The Near-term

Gold is trading near the highs, but we see metal in fifth wave of an impulsive structure from Mar 10, so pair can be trading in late stages of an uptrend. Therefore be aware of a turn lower into a three wave set-back that can show up by the end of the month.

GOLD, 4H