Sample Category Title

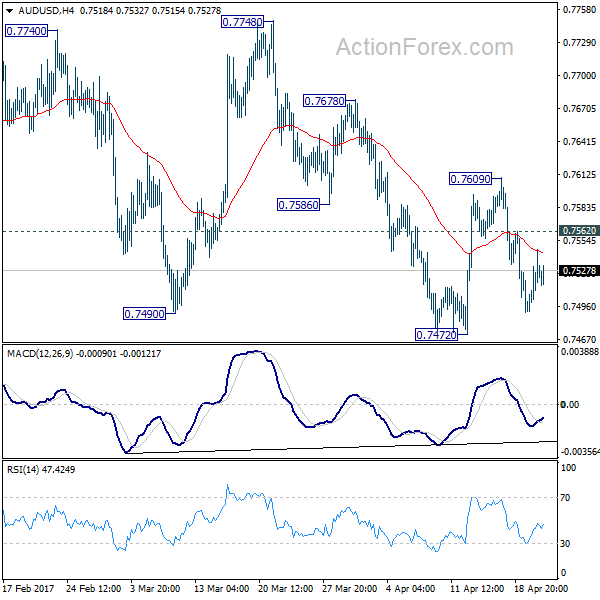

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7496; (P) 0.7522; (R1) 0.7551; More...

With 0.7562 minor resistance intact, deeper fall could be seen back to 0.7472 support. Firm break there will revive the case that whole rise from 0.7158 is completed at 0.7740. In that case, AUD/USD will target a test on 0.7158 key support level next. On the upside, above 0.7562 minor resistance will turn bias back to the upside for 0.7609 resistance. Break will target a test on 0.7748 high.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8144) and above.

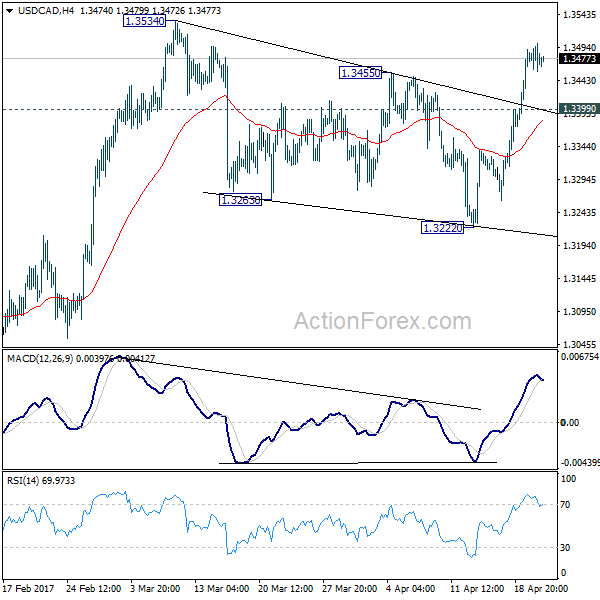

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3450; (P) 1.3474; (R1) 1.3494; More....

Intraday bias in USD/CAD remains mildly on the upside for 1.3399 minor support intact. Rallies from 1.2968 and 1.2460 are possibly resuming. Break of 1.3534 resistance will confirm this bullish case and target 1.3598 high first. Decisive break there will pave the way to next medium term fibonacci level at 1.3838. On the downside, below 1.3399 minor support will turn bias neutral and bring consolidation before staging another rally.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

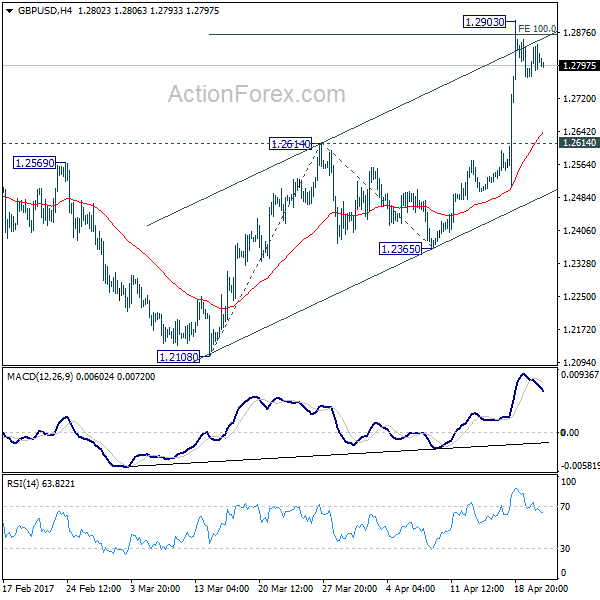

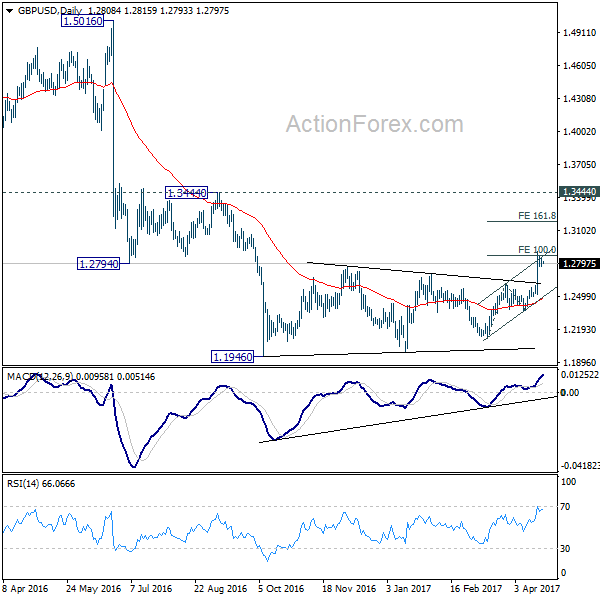

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2772; (P) 1.2809; (R1) 1.2847; More...

With a temporary top in place at 1.2903, intraday bias in GBP/USD is neutral for consolidations. With 1.2614 resistance turned support holds, near term outlook remains bullish for further rise. Firm break of 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871 will target 161.8% retracement at 1.3184. Still, price actions from 1.1946 are seen as a correction. Hence we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2614 resistance turned support will turn bias back to the downside for 1.2365 support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.85; (P) 109.17; (R1) 109.63; More....

USD/JPY's consolidative trading from 108.12 is still in progress and intraday bias stays neutral. With 110.10 resistance intact, near term outlook remains bearish. Rise from 98.97 is finished at 118.65 and fall from there would extend. On the downside, break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Sustained break there will pave the way back to 98.97 low. Nonetheless, break of 110.10 will be the first sign of near term bottoming and turn bias back to the upside for 112.19 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. Current development suggests that it's not completed yet and is extending. In case of deeper decline, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

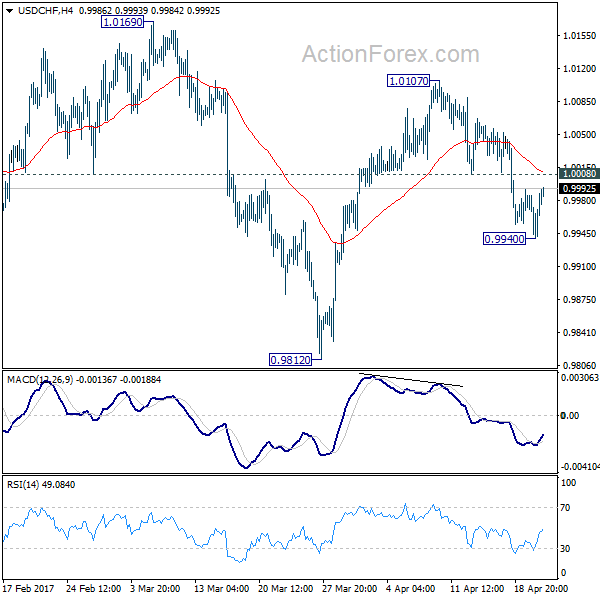

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9954; (P) 0.9971; (R1) 1.0001; More.....

A temporary low is in place at 0.9940 in USD/CHF and intraday bias is turned neutral. Another decline is in favor as long as 1.0008 minor resistance holds. Below 0.9940 will target 0.9812 and below. Fall from 1.0342 is seen as a correction. Hence, we'll look for bottoming signal below 0.9812. Meanwhile, on the upside, above 1.0008 minor resistance will turn bias back to the upside for 1.0107 resistance instead.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push higher yesterday topped at 1.0777 but closed lower at 1.0715, formed a pin bar formation just below the EMA 200 as you can see on my daily chart below. The bias is bearish in nearest term retesting the trend line support and 1.0650/25 area which also remains a key support and good place to buy with a tight stop loss. Immediate resistance is seen around 1.0750. A clear break above that area could lead price to neutral zone in nearest term testing 1.0777 and the daily EMA 200 located around 1.0800. Overall I remain neutral.

GBPUSD

The GBPUSD had a moderate bullish momentum yesterday topped at 1.2847 but closed a little bit lower at 1.2810. The bias is neutral in nearest term. The double bottom bullish scenario should remain valid but we still need a consistent and convincing movement above the daily EMA 200 (1.2780). Immediate support remains around 1.2750. A clear break and daily/weekly close below that area would expose 1.2650 or lower next week. On the upside, a clear break and daily/weekly close above 1.2850 – 1.2900 would give us further confirmation of the double bottom bullish scenario with nearest target seen around 1.3000 – 1.3050.

USDJPY

The USDJPY continued its bullish momentum yesterday topped at 109.48. The bias is bullish in nearest term testing 110.10 and the trend line resistance as you can see on my H1 chart below which is a good place to sell as we know that the current short-term bullish trend is just a corrective movement. Immediate support is seen around 109.20. A clear break below that area could lead price to neutral zone in nearest term testing 108.70 region but only a clear break back below 108.13 would end the current bullish correction phase.

USDCHF

The USDCHF attempted to push lower yesterday bottomed at 0.9940 but closed higher at 0.9986 and hit 0.9991 earlier today in Asian session. The bias is neutral in nearest term probably with a little bullish bias testing 1.0020 resistance area which remains a good place to sell with a tight stop loss targeting 0.9880. Immediate support is seen around 0.9940. A clear break and daily/weekly close below that area would expose 0.9880 – 0.9813 next week. Overall I remain neutral.

Wolves Circle Oil And Gold Ahead Of Le Crunch

Oil continues it's bearish consolidation, while precious metals await this weekend's French election.

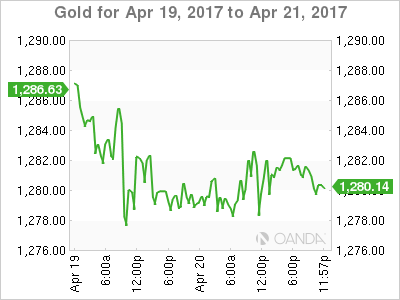

Gold has spent the overnight session consolidating to open quietly mid-range at 1281 this morning in Asia. The fact that gold is almost unchanged from its open of the previous day suggests that traders are now positioned and in a wait and see mode ahead of this weekend's French presidential voting.

From a chart perspective, however, gold appears to have run out of momentum, having made a series of lower highs over the past few days. Assuming the weekend passes without surprises election wise, there is potential for a correction on Monday as safe-haven hedges are lightened. However, a surprise win by both the extreme left and right candidates could make gold's price action when it opens early Monday emotional, to say the least.

Key levels for the Asian session and into the weekend are supports at 1270 and 1260 with resistance at 1296, 1300 and 1308.

Silver

Silver meanwhile, it looking even less constructive on the charts. Since peaking on Monday at 18.6550, Silver has made a series of lower daily highs and lows and is now perched precariously on its 200-day moving average at 18.0200. Clearly, this weekend's vote in France will set the price agenda into the next week, but like gold, its price action is not constructive from a technical perspective.

For today's session, Silver has support at 17.8650 initially and then 17.7400. Resistance lies at 18.2400 with a close above implying a move back to the 18.5000 area.

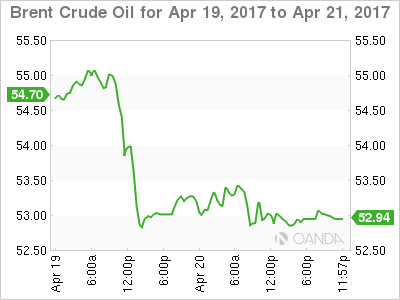

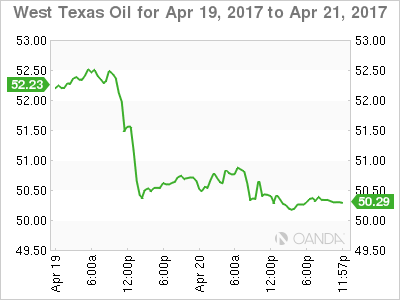

OIL

Crude has consolidated near the bottom of its recent ranges as Asian trading gets under way. After the midweek clean out of long positioning, traders appear averse to initiating fresh longs as the Street frets about record oil inventories globally and rising U.S. production.

From a technical perspective, neither Brent nor WTI's price action is constructive. Instead, both seem to be making bearish consolidation patterns before another move to the downside.

Brent spot has clearly defined support at 52.50 with resistance at 53.50 intraday.

WTI spot has support at 50.00 with resistance at 51.00 intraday.

The price action over the last 48 hours, suggests a break of the support levels in both, could trigger more stop-loss selling as optimism meets reality.

Summary

Were it not for the French election this weekend; commodities would not be looking constructive technically. However with “Le Crunch” this Sunday, surprises cannot be ruled out, and they have the potential to override the technical picture. Some more short-term consolidation cannot be ruled out over today's session, but traders should be watching their news feeds late Sunday, and the metals open at 6 am Singapore for further clues.

Market Morning Briefing: Muted Price Action Had Been Seen In Gold

STOCKS

Almost all major indices have bounced from immediate support levels and could move up for at least the next 2-3 sessions.

Dow (20578.71, +0.85%) has bounced back from support near 20400 as expected. A rise towards 20700 is a possibility in the near term.

Dax (12027.32, +0.09%) is also up from levels near 11930 and could move back towards 12100-12200in the coming sessions if this holds.

Shanghai (3175.86, +0.12%) has moved up from 3150 and is testing important resistance near 3175-3180 levels. In case 3180 produces a rejection, we could see a re-test of 3150 and may be even lower. A sustained break above 3180 is needed to ensure a rise towards 3225 for the near term.

Nikkei (18585.31, +0.84%) is also trading higher while the support near 18227 holds good. At the same time also note that we could see a slight dip from 18650-18745 region in the near term which could possibly bring back the price towards 18230.

9160-9075 is an important near term band for Nifty (9136.40, +0.36%). A break on either side would decide the next course of movement. We should be prepared to a see a fall towards 9000 in case of a break below 9100-9075 levels. But while 9100-9075 holds, we prefer a bounce back to higher levels in the medium term.

COMMODITIES

Muted price action had been seen in Gold (1281).Correction towards 1260-65 can be expected due to near-term overbought condition. We have been expecting 1260 to hold for some time as buyers are taking every dip as a further opportunity for buying. 1301 could be a level where the price action has to be checked to assess the chances of further bounce to 1328 to 1350 levels.

Silver (17.98) had also moved lower in line with our expectation. Immediate trading range could be 17.70-18.35. We think that the corrective phase could be restricted till 17.60-70 levels due to near term oversold condition.

Copper (2.54) has been stuck in the range of 2.50-2.66. A close below 2.50 could open up 2.48 and 2.45 levels respectively. Gradual buying at 2.45-48 levels can’t be ruled out due to near term oversold condition. Only above 2.66, higher resistances of 2.72 -80 can come into consideration.

Brent (53.06) and WTI (50.30) both had moved lower in line with our expectation. They are within their trading ranges of 52.20-53.60 and 50.30-51.70 respectively. Brent may consolidate within these levels for few more sessions though the possibility of a decline towards supports can’t be ruled out, but a close below 50.30 could drag WTI towards 48.36 levels. We will remain bearish while Brent and WTI are trading below 53.60 and 51.70 levels respectively.

FOREX

Dollar Index (99.74) is hovering around its pivot of 99.80 of its entire trading range of 98.80-100.75. If it breaches its pivot then we might see 100.45-80 within 3 to 5 trading sessions.

Euro (1.0716) was rejected from levels near 1.0770 yesterday. We could see a pause in Euro today trading within the 1.0770-1.0680 region. Looking at the German-US 10Yr yield spread (REFER TO INTEREST RATES SECTION BELOW) there could be some possibility that further upside for euro could be limited just now.

Pound (1.2799) is in a pause mode after the recent sharp rise from levels near 1.25. We may see trade within 1.2750-1.29 for the next 2-sessions. 1.29 may act as a decent resistance for the coming sessions.

Dollar-Yen (109.215) could test 109.50-110.08 levels before dipping back to 109-108.5 levels again. Overall some sideways consolidation might be on the cards for the coming sessions.

Aussie (0.7526) could move up towards 0.760-0.761 in the next 2-3 sessions before again coming off towards 0.7450 levels. As mentioned yesterday, the 0.76-0.7450 region could hold for a few more sessions.

Dollar-Rupee (64.56) could open near resistance at 64.70/80 today and may see a dip in the later hours of the session today. It would be important to watch if the pair moves above 64.70/80 or comes off from there to reinforce 64.40/30 on the downside.

INTEREST RATES

The US yields have moved up as expected. We could see some more rise in the near term.

The German-US 2Yr (-1.97%) and the 10Yr (-2.00%) have risen. The 2Yr yield spread has broken above immediate resistance level whereas the 10yr spread is testing important resistance at current levels. In case the 10Yr spread comes off from current levels in the early sessions of next week, we could expect a dip in Euro also in the neat week.

The UK-US 10yr (-1.19%) is trying to come off from a long term channel resistance and while that holds, we could see a fall towards -1.25%. in that case Pound may either consolidate sideways or come down in the near term.

The 10YR GOI may rise towards 6.95-7% if it breaks above 6.90%. Else a fall towards 6.85 or lower is possible.

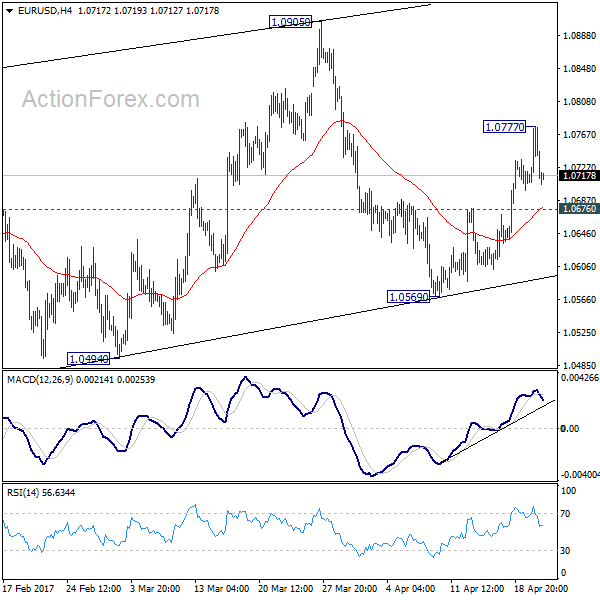

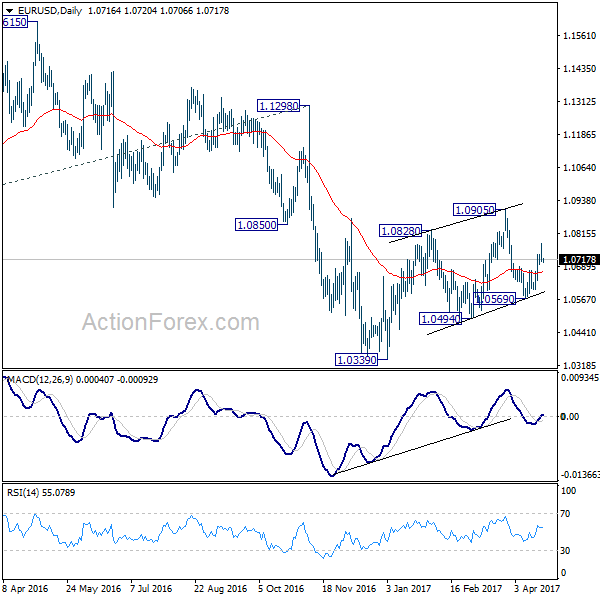

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0688; (P) 1.0733 (R1) 1.0759; More....

A temporary top is in place at 1.0777 in EUR/USD and intraday bias is turned neutral first. With 1.0676 minor support intact another rise is in favor. Above 1.0777 will target 1.0905 and above. But still, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Euro Drops on Paris Terrorist Shooting ahead of Election, Dollar Lifted as Tax Reform News

Euro dropped notably against Dollar overnight after news of terrorist attack in Paris, just ahead of presidential election this Sunday. A shooting occurred on the famous Champs-Elysees shopping boulevard, resulting in death of one police and injuries of two others. The Islamic State group claimed responsibility for the shooting. The incident disrupts the election campaign as conservative candidate Francois Fillon cancelled his trip to the Alps to "first show our solidarity with the police". Far-left Jean-Luc Melenchon said urged people to "attend to our duties as citizens: no panic, we shouldn't interrupt our democratic process". Far-right Marine Le Pen said she was "deeply angry" on the shooting and sad for the victims. Centrist Emmanuel Macron said that "this threat, this imponderable problem, is part of our daily lives for the years to come."

For the moment, Macron and Le Pen are still tipped by polls to win the election on Sunday to go through to the run-off on May 7. But markets would be lightening up position on Euro, in case that both Euro sceptic Le Pen and Melenchon win. For the moment, EUR/USD is holding above 1.0676 minor support and further rise is still expected technically. But the common currency is staying bearish against Sterling and Yen. EUR/GBP is holding below 0.8511 resistance while EUR/JPY is kept below 118.23 resistance. Euro could turn softer before weekly close.

US Treasury Mnuchin: Close to bring forward major tax reform

On the other hand, US equities, treasury yields and Dollar were lifted by comments from US Treasury secretary Steven Mnuchin. Mnuchin said yesterday that Donald Trump's administration is close to bringing forward "major tax reform". And, he hoped that passing the tax overhaul bills won't "take till the end of the year". Mnuchin changed his tone on the issue and said that "whether health care gets done or health care doesn't get done, we're going to get tax reform done." Separately, Trump's economic adviser Gary Cohn said that the administration is going to come up with a "unified, united tax proposal from the White House that will include individual as well as corporate". Nonetheless, no detail is given to the public by any one so far.

Staying in US, President Donald Trump praised Chinese efforts regarding North Korea and said Chinese President Xi Jinping would "try very hard" on it. However, on the other hand, Trump launched a probe against exporters of cheap steel, including China, to US. And he emphasized that steel is "critical" to both the economy and military. Meanwhile, Trump's earlier comments that Korea used to be a part of China infuriated people in South Korea. South Korean foreign ministry spokesman Cho June Hyuck said yesterday that "it's a clear fact acknowledged by the international community that, for thousands of years of history, Korea has never been part of China." Meanwhile, the Liberal Korea Party presidential candidate Hong Joon Pyso said through a spokesman that Trump's comment " is clearly a distortion of history and an invasion of the Republic of Korea's sovereignty."

Dallas Fed president Robert Kaplan said yesterday that "three rate increases this year...is still a good baseline." And, "if the economy develops a little more slowly, then we can do less than that and if the economy is a little stronger, we can do more than that." Regarding unwinding the balance sheet, Kaplan said that "as soon as later this year or maybe early next year, we should begin the process of letting the balance sheet roll off."

On the data front

Japan PMI manufacturing rose to 52.8 in April, up from 52.4 and beat expectation of 52.5. New export jumped to 53.9, up fro 51.9. Output rose to 53.6, up from 53.0. Markit noted that "April's PMI data signaled continued healthy growth of Japans manufacturing sector, and the latest results were again consistent with production rising at a quarterly rate of around 2 percent."

Eurozone PMIs will be released in European session today while UK retail sales will be featured. Canada will release CPI. US will release PMIs and existing home sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0688; (P) 1.0733 (R1) 1.0759; More....

A temporary top is in place at 1.0777 in EUR/USD and intraday bias is turned neutral first. With 1.0676 minor support intact another rise is in favor. Above 1.0777 will target 1.0905 and above. But still, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing Apr P | 52.8 | 52.5 | 52.4 | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.30% | 0.00% | ||

| 07:00 | EUR | France Manufacturing PMI Apr P | 53.2 | 53.3 | ||

| 07:00 | EUR | France Services PMI Apr P | 57.2 | 57.5 | ||

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 58.1 | 58.3 | ||

| 07:30 | EUR | Germany Services PMI Apr P | 55.5 | 55.6 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 56.1 | 56.2 | ||

| 08:00 | EUR | Eurozone Services PMI Apr P | 56 | 56 | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 26.3B | 24.1B | ||

| 08:30 | GBP | Retail Sales M/M Mar | -0.30% | 1.40% | ||

| 12:30 | CAD | CPI M/M Mar | 0.40% | 0.20% | ||

| 12:30 | CAD | CPI Y/Y Mar | 2.00% | |||

| 12:30 | CAD | CPI Core - Trim Y/Y Mar | 1.60% | |||

| 12:30 | CAD | CPI Core - Median Y/Y Mar | 1.90% | |||

| 12:30 | CAD | CPI Core - Common Y/Y Mar | 1.30% | |||

| 13:45 | USD | Manufacturing PMI Apr P | 53.9 | 53.3 | ||

| 13:45 | USD | Services PMI Apr P | 53.7 | 52.8 | ||

| 14:00 | USD | Existing Home Sales Mar | 5.61M | 5.48M |