Sample Category Title

Technical Outlook: EURUSD – Remains Supported Above 1.0700

The Euro holds in extended consolidation above 1.0700 support (broken Fibo 38.2% of 1.0905/1.0568 downleg) reinforced by 5/30 SMA's bull-cross) in early Friday's trading.

The pair spiked to 1.0776 on Thursday and hit target at 1.0776 (Fibo 61.8%), but probe above 1.0738 pivot (sideways-moving daily Kijun-sen line which capped Tue/Wed upside attempts), proved to be short-lived.

Strong upside rejection that left daily candle with long upper shadow on Thursday weighs, however, immediate downside risk will be sidelined while the price is holding above supports at 1.0700 and 1.0680 (rising daily Tenkan-sen / 20SMA).

Release of EU PMI data is in focus today, as the Euro is eyeing an outcome of the first round of French presidential election.

Res: 1.0738, 1.0776, 1.0800, 1.0837

Sup: 1.0700, 1.0680, 1.0661, 1.0627

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

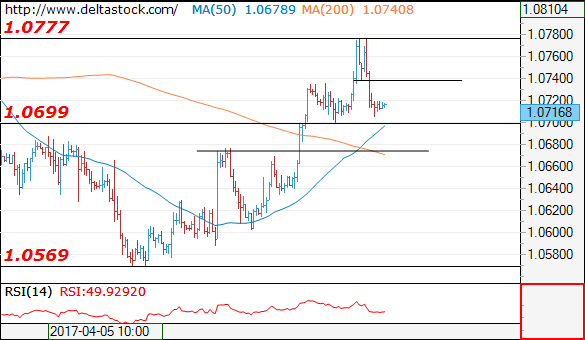

EUR/USD

Current level - 10716

Yesterday's 'double top' formation at 1.0777 signals a reversal and the intraday outlook is bearish, for a break through 1.0700 static support, towards 1.0570 low. Crucial resistance lies at 1.0740.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0740 | 1.0828 | 1.0700 | 1.0600 |

| 1.0828 | 1.0904 | 1.0600 | 1.0490 |

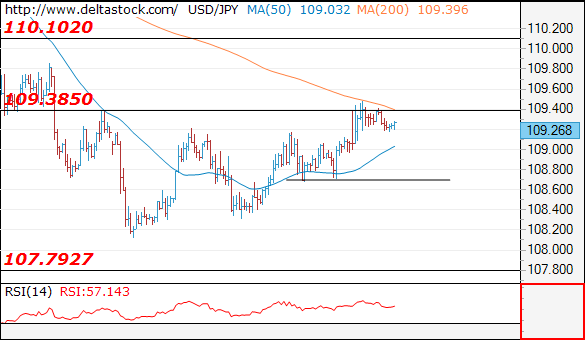

USD/JPY

Current level - 109.26

My intraday outlook is positive above 109.09, for a rise towards 110.10. Crucial on the downside is 108.70.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.40 | 113.50 | 109.09 | 107.80 |

| 110.10 | 115.65 | 108.70 | 105.80 |

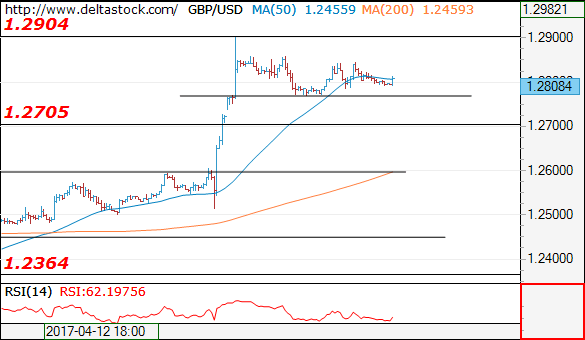

GBP/USD

Current level - 1.2808

Still in the consolidation pattern below 1.2904 peak and the intraday outlook is rather bearish, for a break through 1.2770, towards 1.2705 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2904 | 1.3000 | 1.2770 | 1.2610 |

| 1.3000 | 1.3500 | 1.2705 | 1.2510 |

Currencies: EUR/USD Fails To Extend Gains Going Into The French Election

Sunrise Market Commentary

- Rates: Side-lined ahead of French elections?

EMU and US PMI's colour today's trading, but risk ending up being irrelevant ahead of Sunday's first French presidential election round which probably keep most investors sidelined. The outcome will determine the start of next week's trading. If the tail risk (Mélenchon vs Le Pen or Fillon) manifests, markets will start discounting the “Frexit” possibility. - Currencies: EUR/USD fails to extend gains going into the French election

Yesterday, the euro gained temporary ground on hopes for a market-friendly outcome of the French election. However, the momentum couldn't be maintained. The dollar was in better shape later in the session. Today, trading in the major USD cross rates might shift in wait-and-see modus. We don't expect yesterday's pro-euro repositioning to continue.

The Sunrise Headlines

- US equities ended strong, gaining between 0.75% and 1% as US Treasury secretary Mnuchin promised details of tax reforms very soon. Overnight, Asian stock markets record similar gains with China underperforming (flat).

- The Trump administration will unveil a tax reform plan very soon and expects it will be approved by Congress this year whether a healthcare overhaul happens or not, Treasury Secretary Steven Mnuchin said.

- The US has set the stage for a global showdown over steel, launching a national security investigation that could lead to sweeping tariffs on steel imports in what would be the first significant act of economic protectionism by Trump.

- The Japanese manufacturing PMI rose to 52.8 from 52.4 in March. Sub-indices measuring output, new export orders, employment, input and output prices all increased at a faster rate than the previous month.

- It would not be a bad idea for the ECB and other central banks to follow the US Federal Reserve's example and change course away from an ultra-accommodative monetary policy, German Finance Minister Schaeuble said.

- France's presidential candidates embark on their last day of campaigning on Friday before this weekend's tight first-round election, marked by the collapse of the mainstream political parties and rise of the far left and far right.

- Today's eco calendar contains EMU manufacturing and services PMI's, UK retail sales, US PMI's and US existing home sales. Fed Kashkari is scheduled to speak

Currencies: EUR/USD Fails To Extend Gains Going Into The French Election

EUR/USD rebound slows ahead of French election

On Thursday, the euro initially rebounded as euro area yields recovered from recent lows and interest rate differentials narrowed in favour of the euro. However, the rally petered out later in the session. A good equity performance and US Treasury secretary Mnuchin confirming that the government will propose tax reform plans soon, helped the return the dollar. The headlines on the terrorist attack in Paris had little impact. At that time, EUR/USD had already reversed the intraday gains. The pair closed the session at 1.0717. USD/JPY finished the day at 109.32 (from 108.86 on Wednesday ). Even so, the gain remained modest given the rise in core yields and the positive equity sentiment.

Overnight, Asian equities are also trading with modest to moderate gains. Japanese equities are supported by comments from BOJ's Kuroda that the bank intends to keep monetary policy very accommodative. The BOJ governor acknowledged that the Japanese economy is doing better but inflation remains low. Kuroda also mentioned that a rise in the yen could delay Japan reaching the 2% inflation target. USD/JPY hovers in in the 109.20 area this morning, maintaining most of yesterday's gain. EUR/USD stabilizes in the low 1.07 area as investors ponder the impact of the terrorist attack in France yesterday evening, just days before the first round of the presidential election.

Today the April business sentiment in the US and the EMU will be released . In March, EMU composite PMI climbed to 56.4 from 56. The omens are good for yet another (slight) increase of the headline index in April, which would bring the index to a 6-yr high. The consensus expect a stabilization, but we see risks on the upside.US Markit PMI is expected to have risen slightly for both manufacturing and services. Regional surveys (Philly Fed and NY) fell sharply in April, suggesting that risks for the US PMI might be on the downside of consensus. So, the data might be slightly supportive for EUR/USD. The French election will remain an important factor for FX trading. Yesterday, markets adapted positions for a market friendly outcome of the first round on Sunday. This temporary supported the euro. Today, we assume a more neutral market bias after yesterday's attack in Paris. The euro probably won't get additional interest rate support. We expect the euro to return to wait-and-see modus. However, the downside of EUR/USD might be well protected as a market friendly outcome of the election is still a likely.

Of late, by default dollar softness dominated FX trading. This week, the dollar (trade-weighted) showed cautious signs of bottoming out. We look out whether this process is confirmed. For the overall USD performance we continue to keep a close eye on the US bond markets. We maintain the view that the correction higher on the US bond markets has gone far enough. However, for now there is no trigger for a U-turn and the French election remains a factor of uncertainty. A constructive outcome of the French election might be supportive for both EUR/USD and USD/JPY.

From a technical point of view, USD/JPY broke through the 110 key support. We downgraded our USD/JPY assessment to bearish, as long as the pair doesn't regain 112.20 (neckline ST double bottom). Next key support (62% retracement) comes in at 107.18. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March, but the test was rejected. EUR/USD returned lower in the 1.0875/1.05. The move met support in the 1.06 area. The picture turned more neutral as the pair returnsedto the middle of the ST range. We slightly prefer to sell EUR/USD on upticks in case of a return higher in the range as we see room for a broader USD comeback.

EUR/USD: pre-French election has nog strong legs

EUR/GBP

Sterling holds near the recent highs

Sterling trading was mostly driven by global moves and technical considerations yesterday. EUR/GBP was supported by the overall euro rebound. EUR/GBP temporary moved to the 0.84 area, but the gains were reversed as the euro returned intraday gains later in the session. EUR/GBP closed the session at 0.8364 (from 0.8383). EUR/GBP 0.83 support holds for now. Cable basically drifted sideways in the 1.28 area

The UK retail sales data might bring some animus for sterling trading today. March sales are expected to decline 0.5% M/M after a strong performance in February. We don't have strong reasons to take a different view from the consensus. A substantial negative surprise is probably needed to trigger a meaningful sterling correction given current momentum. If the EUR/USD rally slows, it will probably be difficult for EUR/GBP to break north of the 0.83/0.84 corridor. In a longer term perspective, the sterling rally is probably overdone. However, short-term we still see no obvious trigger for a sustained sterling correction.

We had a neutral short-term bias on EUR/GBP. On Tuesday, sterling dropped below the bottom of the EUR/GBP 0.84 support, improving the picture for sterling. The pair came with reach of the key 0.8305 support (Dec low). We look whether this level holds. A break below would be highly significant from a technical point of view. Longer term, Brexit-complications remain a potential negative for sterling. However, this is not the focus of sterling trading at this stage.

EUR/GBP: key 0.83 support still within reach, but no real test occurred

Market Update – Asian Session: Asian Indices Trading With The Tailwind Of A Broad-Based Rally In US Markets On...

US Session Highlights

(US) APR PHILADELPHIA FED BUSINESS OUTLOOK: 22.0 V 25.5E (lowest since Dec)

(US) INITIAL JOBLESS CLAIMS: 244K V 240KE; CONTINUING CLAIMS: 1.98M V 2.02ME (lowest continuing claims level since Apr 2000)

(US) MAR LEADING INDEX: 0.4% V 0.2%E

(US) WEEKLY EIA NATURAL GAS INVENTORIES: +54 BCF VS. +47 TO +49 BCF EXPECTED RANGE

(US) Fed's Powell (moderate, voter): economy is at or close to full employment; economy is improving but all is not well

US equities opened the morning higher and strengthened throughout the session to close just off the day's highs. Industrials and financials led the outperformers, while utilities and telecom lagged. Treasury yields gained as investors maintained a risk-on appetite. The U.S. Dollar Index rose slightly, advancing against the yen, while gold was little changed.

US markets on close: Dow +0.9%, S&P500 +0.8%, Nasdaq +0.9%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Utilities

Biggest gainers: ADS +8.3%; DGX +6.0%; NAVI +6.0%

Biggest losers: URI -5.2%; DHR -4.1%; EBAY -3.9%

At the close: VIX 14.1 (-0.8pts); Treasuries: 2-yr 1.20% (+2bps), 10-yr 2.24% (+4bps), 30-yr 2.89% (+3bps)

US movers afterhours

PFPT Reports Q1 $0.12 v $0.09e, R$113.3M v $110Me; Guides Q2 $0.11-0.13 v $0.11e, R$118-120M v $119Me; +9.2% afterhours

V Reports Q2 $0.86 v $0.79e, R$4.48B v $4.30Be; announces $5B buyback (2% of market cap); Affirms FY17 op margin mid 60%s (prior mid 60's%); +2.4% afterhours

MAT Reports Q1 -$0.32 adj v -$0.17e, R$814.6M v $810Me; Total net sales (cc) -15% y/y; -6.8% afterhours

Key economic data

(JP) JAPAN APR PRELIMINARY PMI MANUFACTURING: 52.8 V 52.4 PRIOR (8th month of expansion)

(NZ) NEW ZEALAND MAR ANZ CONSUMER CONFIDENCE INDEX: 121.7 V 125.2 PRIOR; M/M: -2.8% (3rd straight decline) V -1.7% PRIOR

(KR) South Korea Apr First 20-days Exports y/y: 28.4% v 14.8% prior; Imports y/y: 16.4% v 29.4% prior

Asia Session Notable Observations, Speakers and Press

Asian indices trading with the tailwind of a broad-based rally in US markets on Thursday. The gains were particularly impressive considering ISIS terror activity in France on the eve of the elections - nonetheless, today's Elabe poll shows Macron widening his lead on far-right candidate Le Pen in both primary and run-off contests. Traders point to better earnings performance as well as the pledge by Treasury Sec Mnuchin to pass tax reform this year, promising to unveil the sweeping legislation very soon.

In economic data, Japan prelim Apr Manuf PMI marked 8th straight month of expansion, with both New Export Orders and Employment components showing conditions improving at a faster rate. New Zealand ANZ consumer confidence fell for the 3rd straight month, as ANZ economist pointed to the slowdown in the property market in Auckland as a likely culprit.

China

(CN) PBOC Gov Zhou met with US Economic Council Cohn and discussed financial cooperation - press

(CN) China banking regulator (CBRC) said to have requested a check of mutual guarantee risks - Chinese press

(CN) China Social Security Fund chief / former Fin Min Lou: Household leverage ratio has risen above 50% - press

Japan

(JP) BOJ said to plan to raise its FY17/18 GDP target from 1.5% to upper 1% range as part of its policy decision next week - Japan press

(JP) Japan Fin Min Aso: No issue with US Pres Trump's comments that USD is too strong; Discussed Japan efforts to raise potential growth rate and global economy at G20 - press

(JP) Japan PM Abe sends ritual offering to Yasukuni shrine - Japan press

Australia

CBA raises fixed interest rates on investor loans by 25-50bps and interest-only home loans by 25bps - SMH

(NZ) Real Estate Institute of New Zealand (REINZ) latest data suggest New Zealand rural property market has performed well - press

Korea

(KR) North Korea warns of "super-mighty preemptive strike" following recent comments by State Sec Tillerson

(KR) South Korea to consider all measures, including WTO complaint, in response to US protectionism - press

(KR) Pres Trump said to have "absolute confidence" that China Pres Xi to work very hard to defuse North Korea tensions - press

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.7%, Hang Seng flat, Shanghai Composite +0.1%, ASX200 +0.7%, Kospi +0.9%

Equity Futures: S&P500 flat; Nasdaq +0.1%, Dax flat, FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0707-1.0721; JPY 109.18-109.42; AUD 0.7515-0.7535; NZD 0.6983-0.7010

June Gold -0.2% at 1,281/oz; June Crude Oil +0.1% at $50.75/brl; May Copper +0.2% at $2.55/lb

SPDR Gold Trust ETF daily holdings fall 6.5 tonnes to 854.3 tonnes; first decline since Mar 30th

iShares Silver Trust ETF daily holdings fall to 10,149 tonnes from 10,178 tonnes prior

(CN) PBOC SETS YUAN MID POINT AT 6.8823 V 6.8792 PRIOR

(CN) China Finance Min sells 30-yr bonds at 3.899% v 3.87%e; Bid-to-cover 1.62x

(CN) PBOC to inject combined CNY100B v CNY100B prior in 7-day, 14-day and 28-day reverse repos, 4th straight injection; For the week, injected CNY170B v CNY70B in the prior week

(AU) Australia MoF (AOFM) sells A$600M in 2.0% 2021 Bonds; avg yield: 2.044%; bid-to-cover: 4.96x

Asia equities / Notables / movers by region

Australia:

CC Amatil (CCL) -9.8%; soft H1 guidance

Duet Group (DUE) +9.6%; CKI buyout approved

Oz Minerals (OZL) +2.7%; Q1 production

Hong Kong:

ASM Pacific Technology Limited (522) +6.8%; Q1 results

China Yongda Automobile Services (3669) +4.9%; Q1 results

China National Materials Company Limited (1893) +2.6%; positive guidance

China Mobile (941) -0.2%; Q1 results

Japan:

Fujifilm (4901) -4.3%; To delay earnings announcement

Toshiba (6502) -5.0%; Four domestic companeis file lawsuit for compensation; chairman of SK Hynix to meet with board within days

Hino Motors (7205) +3.8%; FY16 results speculation

Tokyo Seimitsu (7729) +3.8%; FY16 results speculation

Equities Have Had A Decent Run Overnight

Market movers today

Markets are set for the big PMI day today, with releases out in the US, euro area and Scandi region alike and should give some hints as to whether our call that the business cycle is near a peak is starting to play out .

In the US, the flash Markit PMI manufacturing for April is due. In March, PMI manufacturing declined, although it is still at a level that suggests increased activity. We expect manufacturing PMI to be unchanged at 53.3.

Similarly, in the euro area, PMIs are set for release across regions. We believe these will remain strong in April but with a small downward correction with regard to services. Business and economic sentiment still seem optimistic; however, the final services PMIs were corrected significantly downwards in the March figures, which indicates some weakness towards the end of the month. This weakness could transition into lower service PMIs for April. Additionally, the recent months, with upside surprises in PMIs, make a coming moderation increasingly likely.

Manufacturing survey due in Norway. For more on the Scandi region, see page 2.

Selected market news

Al though equities have had a decent run overnight, global risk sentiment is set to remain fragi le ahead of the first round of the French pres idential elections this weekend, with the shooting in Paris yesterday evening adding further to uncertainty. Polls cont inue to project the possibility of a wide range of outcomes, and for markets the most high-risk scenario would be a run-off in the second round between the two euro-sceptics, Marine Le Pen and Jean-Luc Mélenchon.

The Bank of Japan's (BoJ) Haruhiko Kuroda stressed in an interview last night that the bank is far from heading for the exit and that the cent ral bank is determined to keep st imulus in place (in the form of quant itat ive easing with yield-curve control) to drive inflat ion up. However Kuroda's ability to keep policy accommodat ive could be quest ioned given the const raints the BoJ could see in operat ing its asset -purchase programme given that the central bank now owns some 40% of JGBs outstanding and has a balance sheet amount ing to around 80% of GDP. In our base case of US rates moving gradually higher as the Fed hikes, USD/JPY should follow and provide some support to Japanese inflat ion but with wage growth in Japan still very subdued and operat ional const raints set to rise as the BoJ balance grows, markets may become increasingly reluctant to buy into the BoJ willingness to stay in the inflation game.

Next week will see policy meetings at the BoJ, the ECB and the Riksbank, all of which are struggling to beef up underlying inflationary pressure. In our view, all three central banks will be keen to avoid sending any hawkish messages but in the current environment markets could request that they dig deeper yet into their toolboxes to refrain from pricing an end to easing and send their respect ive currencies higher to add insult to injury on inflation.

Aussie Trading Flat In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.35% against the USD and closed at 0.7525.

LME Copper prices rose 0.2% or $11.0/MT to $5611.0/MT. Aluminium prices rose 2.0% or $37.5/MT to $1933.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7525, with the AUD trading flat against the USD from yesterday's close.

The pair is expected to find support at 0.7501, and a fall through could take it to the next support level of 0.7476. The pair is expected to find its first resistance at 0.7548, and a rise through could take it to the next resistance level of 0.7570.

Next week, traders would closely monitor a speech by the Reserve Bank of Australia's (RBA) Governor, Philip Lowe as well as Australia's consumer price index and private sector credit data.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Euro-Zone’s Consumer Confidence Hits A Nearly 9-Year High Level In April

For the 24 hours to 23:00 GMT, the EUR slightly declined against the USD and closed at 1.0713.

On the data front, the Euro-zone's flash consumer confidence index improved more-than-expected to a level of -3.6 in April, surging to its highest level in nearly nine years, thus pointing to a continued pickup in the region's consumer optimism, despite political uncertainties ahead of upcoming French elections.

Markets expected for an advance to a level of -4.8, after recording a level of -5.0 in the previous month. Moreover, the region's seasonally adjusted construction output climbed 6.9% on a monthly basis in February, accelerating at its fastest pace in nearly five-years. Construction output had registered a revised drop of 2.4% in the previous month.

Elsewhere, Germany's producer prices rose 3.1% YoY in March, less than market expectations for a gain of 3.2% and following a similar rise in the prior month.

Meanwhile, the latest polls indicated that French centrist presidential candidate, Emmanuel Macron, is maintaining a slim lead over his rivals.

Macroeconomic data released in the US showed that initial jobless claims advanced more-than-anticipated to a level of 244.0K in the week ended 15 April 2017, compared to a reading of 234.0K in the previous week. Market were expecting initial jobless claims to rise to a level of 240.0K. Additionally, the nation's Philadelphia Fed manufacturing index eased to a level of 22.0 in April, more than market expectations of a fall to a level of 25.5 and following a level of 32.8 in the prior month.

On the other hand, the US leading indicator climbed 0.4% in March, surpassing market consensus for a rise of 0.2%. In the previous month, leading indicator had registered a rise of 0.6%.

In the Asian session, at GMT0300, the pair is trading at 1.0714, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.0687, and a fall through could take it to the next support level of 1.0660. The pair is expected to find its first resistance at 1.0759, and a rise through could take it to the next resistance level of 1.0804.

Going ahead, investors will keenly await the release of preliminary Markit manufacturing and services PMIs data for April across the Euro-zone, slated to release in a few hours. Moreover, market participants will also eye the first-round of voting in French presidential election, scheduled this Sunday. In the US, the flash print of Markit manufacturing and services PMIs for April along with existing home sales for March, will garner a significant amount of investor attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading On A Weaker Footing, Ahead Of UK’s Retail Sales Data

For the 24 hours to 23:00 GMT, the GBP rose 0.2% against the USD and closed at 1.2806.

In the Asian session, at GMT0300, the pair is trading at 1.2794, with the GBP trading 0.09% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2761, and a fall through could take it to the next support level of 1.2727. The pair is expected to find its first resistance at 1.2837, and a rise through could take it to the next resistance level of 1.2879.

Ahead in the day, investors will focus on Britain's retail sales data for March, to gauge strength in the nation's consumer spending.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japan’s Manufacturing Sector Activity Expands To A 2-Month High Level In April

For the 24 hours to 23:00 GMT, the USD rose 0.44% against the JPY and closed at 109.37.

In the Asian session, at GMT0300, the pair is trading at 109.22, with the USD trading 0.14% lower against the JPY from yesterday's close.

The Japanese Yen gained ground, after overnight data revealed that Japan's flash Nikkei manufacturing PMI jumped to a two-month high level of 52.8 in April, underpinned by a stronger export performance, thus highlighting solid growth in the nation's manufacturing sector. The PMI had registered a reading of 52.4 in the previous month.

Early morning data indicated that the nation's tertiary industry index recorded a rise of 0.2% on a monthly basis in February, falling short of market expectations for a rise of 0.3%. In the previous month, the tertiary industry index had recorded a flat reading.

The pair is expected to find support at 108.78, and a fall through could take it to the next support level of 108.34. The pair is expected to find its first resistance at 109.57, and a rise through could take it to the next resistance level of 109.92.

Going ahead, market participants will look forward to Bank of Japan's interest rate decision, coupled with Japan's inflation, jobless rate, small business confidence, industrial production and retail trade data, all set to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.1% against the CHF and closed at 0.9987.

In the Asian session, at GMT0300, the pair is trading at 0.9993, with the USD trading 0.06% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9956, and a fall through could take it to the next support level of 0.9919. The pair is expected to find its first resistance at 1.0012, and a rise through could take it to the next resistance level of 1.0031.

Moving ahead, traders would concentrate on Switzerland’s UBS consumption indicator, ZEW expectations index and trade balance data, all due to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.