Sample Category Title

Loonie Trading On A Weaker Footing, Ahead Of Canada’s March Inflation Figures

For the 24 hours to 23:00 GMT, the USD declined 0.1% against the CAD and closed at 1.3465.

In the Asian session, at GMT0300, the pair is trading at 1.3479, with the USD trading 0.1% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3456, and a fall through could take it to the next support level of 1.3432. The pair is expected to find its first resistance at 1.3501, and a rise through could take it to the next resistance level of 1.3522.

Looking ahead, Canada's consumer price index for March, scheduled to be released later today, will be on investor's radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Is The Crude Oil Short Trade Over Crowded?

Key Points:

- Price action fails to breach $50.00 handle and short move is stalled.

- 100 day MA and key support zone is limiting downside moves.

- Watch for a bounce towards the $51.90 target in the coming week.

The past few days have seen the price of crude oil (WTI) collapsing towards a major support zone around the $50.00 handle. The move was relatively obvious given the fact that price action failed to break through resistance at $53.74 leading to a sharp rejection and sentiment swing to the short side. Subsequently, traders largely piled in to short positions but with WTI prices having now reached the $50.00 level its worth asking if the trade is now over crowded.

The reality is that crude oil prices are reacting to not just technical factors, but also a range of shifting fundamentals with OPEC chief amongst them. Subsequently, given that oil prices remain strongly within an ascending channel, the downside was always likely to be limited especially when OPEC is countering falling prices with a potential extension to their present supply cuts. Therefore, the short side push was only ever likely to take the commodity to striking distance of the $50.00 handle.

Currently, the large institutional money (smart money) is winding back its short positions and looking for some gains in crude oil prices in the coming week. Subsequently, the net positioning is shifting long and the initial signals early on Friday is one of some upward pressure. This is especially prescient given that price action is currently sitting right on the 100 day MA, as well as key support zone.

In addition, rumours are currently swirling that the next OPEC meeting in May could bring about an extension of the current supply freeze and even potentially further cuts to world OPEC supply. Given that OPEC leaks like a barbed wire canoe it is no surprise that this information is permeating markets. Subsequently, the production cut rhetoric is significantly limiting any further downside moves, from a fundamental perspective. Whether OPEC actually follows through with the purported cuts is another question but the risks are certainly slanted to the upside given many members needs for a higher oil price to balance their domestic books.

Ultimately, the short trade has now become overcrowded and any further decline below the $50.00 handle in the short term is unlikely. Additionally, the technical indicators are also suggesting another bullish wave higher given that price action rests at the junction of the 100 day MA and some key support. Subsequently, the most likely scenario for the week ahead is some sideways consolidation before a break back above the $51.00 handle and appreciation towards our short term target of $51.90 a barrel.

Swissy Heading For Further Losses Moving Ahead

Key Points:

- Despite recent bullishness, the decline should resume shortly.

- Losses could extend to around the 0.9817 mark.

- Fundamentals also remain in favour of further losses.

The Swissy's recent decline has been on pause over the past few sessions which cast some doubt on the likelihood of seeing a retracement all the way to the downside of its consolidation phase. Fortunately for the bears out there, the bias remains in your favour given both technicals and fundamentals are aligned and suggestive of further losses.

Starting with the technicals, there are a number of instruments indicating that, despite the recent uptick in buying pressure, losses are likely to resume in fairly short order. For one, the EMA bias is highly bearish as it is, in fact, now in the process of completing a crossover which could hint that a serious downtrend is getting underway. Furthermore, the MACD and Parabolic SAR readings remain in favour of additional losses which would support the argument for a retracement all the way back to the downside of the overarching wedge structure.

Due to the robust bearish technical bias, it may seem odd that we have had a number of rather bullish sessions from the USDCHF. Indeed, this could be indicative that something else is at play and working in opposition to the broader forecast. Luckily, one simpler explanation is available which doesn't entirely upset the apple cart so to speak. Specifically, the recent surge in buying is probably reflective of the stochastics being relievedafter being forced into oversold territory by the plunge seen on Tuesday.

Moving onto the fundamental bias, this remains bearish for largely the same reasons as discussed previously. In particular, the deterioration of both the Syrian and North Korean situations, alongside the ongoing uncertainty over Brexit, continue to drag the pair lower due to the Franc's safe haven status. Although, more recently, the snap election announcement from the UK government and the slight, yet not insignificant, gains made by Le Pen in the French Election polls are adding to global anxiety. As a result, it's little wonder that the Swissy has a rather grim outlook and is predisposed to the downside over the coming weeks.

Ultimately, the combination of the above mentioned technicals and fundamentals should be more than enough to keep the pressure on the USDCHF and see the forecasted decline take hold. This being said, monitor the 38.2% Fibonacci level around parity as, if the pair crosses back above this price, it could move to retest the upside.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

As we highlighted in Thursday's report, the single currency was likely to find resistance within the H4 (green) sell zone at 1.0777/1.0750. The area comprised of a H4 supply zone at 1.0773-1.0751, a H4 mid-level resistance at 1.0750 and a H4 61.8% Fib resistance at 1.0777 (taken from the high 1.0905). Also of note was the daily resistance found within the upper limits of the said H4 supply base at 1.0772.

H4 price, as you can see, aggressively drove into the jaws of this zone and crossed swords with both the noted H4 61.8% resistance and daily resistance, before turning lower and closing the day ahead of the 1.07 handle. Although this move chalked up a nice-looking daily selling wick, sellers now not only have to contend with the 1.07 figure, they also have to compete with a daily support area seen in play at 1.0714-1.0683.

Our suggestions: Technically speaking, there's limited downside potential seen in this market at the moment. Even if 1.07 is cleared, there's a nearby H4 support area seen at 1.0677-1.0665, as well as the daily support area that's already in motion.

With that, what about considering longs from 1.07 given the current daily support area? This could be an option, although, we would prefer to see more H4 confluence fusing with 1.07. To be on the safe side, we'd highly recommend waiting for a reasonably sized H4 bull candle to form before committing. That way, price has a good chance of at least achieving 1.0750.

Data points to consider: Eurozone manufacturing at 8-9am. FOMC member Kashkari speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: 1.07 region ([waiting for a reasonably sized H4 bull candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

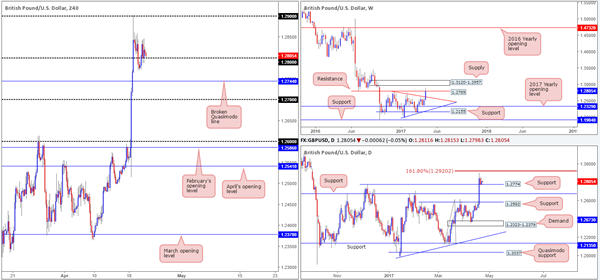

GBP/USD:

In view of the pair trading nearby a key weekly support level at 1.2789, further buying could be a struggle. In conjunction with this notion, daily price is seen consolidating below a Fib 161.8% extension at 1.2920 drawn from the low 1.2108. However, let's be mindful to the fact that nearby support has also been established from the 6th December high around 1.2774.

Over on the H4 candles, yesterday's flow managed to reclaim the 1.28 handle which is currently offering intraday support as we write. Entering long from this psychological number based on daily support mentioned above is chancy, owing to the aforementioned weekly resistance. In regard to shorts, a daily close below 1.2774 is required before we look at committing.

Our suggestions: As of this time, we do not see a lot to hang our hat on at the moment given the clear difference of opinion being seen from the higher-timeframe structures. Therefore, remaining on the sidelines may be the better path to take.

Data points to consider: UK retail sales at 9.30am, MPC member speaks at 12.45pm. FOMC member Kashkari speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

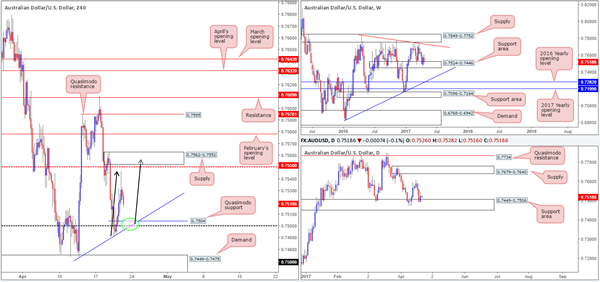

AUD/USD

The Aussie managed to recoup some of Wednesday's losses yesterday, as the bulls reclaimed the 0.75 number in early trading. Bolstering the move is both a weekly support area seen at 0.7524-0.7446 and a daily support area housed within at 0.7449-0.7506.

On account of the higher timeframes, the H4 candles may look to extend the current pullback and test the Quasimodo support at 0.7504 (green circle), since it also boasts the 0.75 handle and a trendline support extended from the low 0.7472. A bounce from this area could also encourage the couple to complete the D-leg to an AB=CD formation (see black arrows) which would terminate around supply at 0.7562-0.7552.

Our suggestions: Assuming one is able to enter with a reasonable stop around the 0.75 neighborhood, the risk/reward should be at least 1:2 up to 0.7550. Personally, we'd recommend waiting for a H4 (preferably with a full-bodied close) bull candle to form and enter based on this momentum with stops positioned below the tail.

Data points to consider: FOMC member Kashkari speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: 0.75 region ([waiting for a reasonably sized H4 bull candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

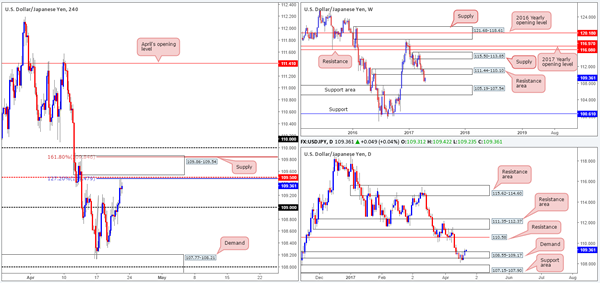

USD/JPY

The USD/JPY extended higher for a second consecutive day on Thursday, forcing price to clear the 109 handle and shake hands with a H4 AB=CD 127.2% Fib ext. at 109.47 (taken from the low 108.13) going into the closing bell. Supporting this AB=CD base is a H4 mid-way barrier at 109.50, a H4 supply area at 109.86-109.54 and a H4 AB=CD 161.8% Fib ext. at 109.84.

Selling from the above noted area may very well be inviting due to its confluence, but we‘re cautious. Throwing the higher timeframes into the mix shows that daily price is currently trading from demand at 108.55-109.17 and has room to advance up to resistance at 110.58. Furthermore, weekly movement reveals there's little resistance in view until price connects with the underside of a resistance area at 111.44-110.10. And considering that the 110 handle sits above our chosen H4 sell zone, this could eventually lead to a fakeout taking place.

Our suggestions: Trading short with absolutely no higher-timeframe structure is chancy, and not really something our team is comfortable with. However, if the noted H4 zone is something you can work with, you may want to consider waiting for a H4 bearish candle to form (preferably with a full-bodied close) before pulling the trigger.

Data points to consider: FOMC member Kashkari speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 109.86/109.47 (possible area to consider shorting from – waiting for a H4 bearish candle to form [preferably with a full-bodied close] is advised – stop loss: ideally beyond the candle's wick).

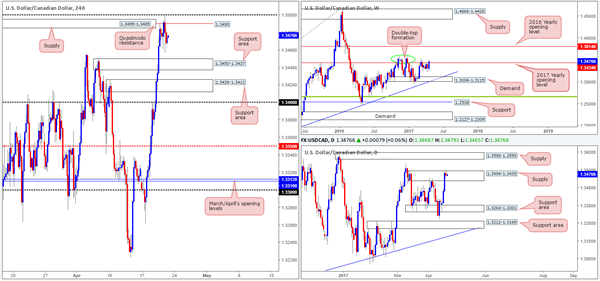

USD/CAD

For those who read Thursday's report you may recall that we showed interest in shorting from the 1.35 handle. Ultimately, we wanted to see H4 price print a selling wick that pierced above the H4 supply at 1.3495-1.3485 into 1.35. While this did come to fruition, we chose not to enter for the simple reason that the same H4 candle also boasted an incredibly large buying tail as well.

Having seen 1.35 hold ground, a retest of the H4 support area at 1.3450-1.3437 is a reasonable possibility, in our opinion. Even more so considering that daily price remains trading within the walls of a supply at 1.3494-1.3439, and weekly price is seen trading nearby a strong-looking double-top formation around the 1.3530 neighborhood (see green circle).

Our suggestions: Watch for price to pullback and test the H4 Quasimodo resistance at 1.3490. Ideally, we do not want to see price test the aforementioned H4 support area before striking this level as this would be the first take-profit target. Also, as price could possibly test the 1.35 handle again, we would advise waiting for a H4 bearish candle to form (preferably with a full-bodied close) before pulling the trigger.

Data points to consider: FOMC member Kashkari speaks at 2.30pm. Canadian inflation data at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.3490 region ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

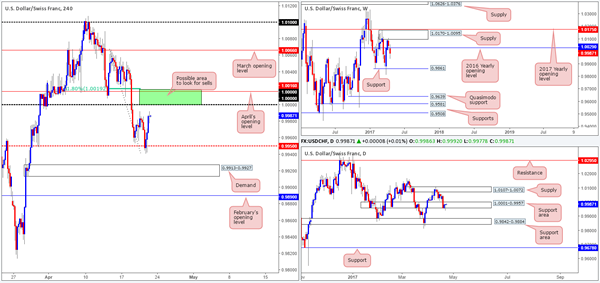

USD/CHF

During the course of yesterday's sessions, H4 price caught a fresh bid off the mid-level support at 0.9950 which eventually saw the unit tackle Wednesday's high 0.9992. In light of this, it's highly likely that the candles will bump heads with parity (1.0000) today. Nearby notable features here is April's opening level at 1.0016 as well as the 61.8% Fib retracement at 1.0019. Collectively, these levels form a promising sell zone (green area).

With weekly price still seen trading below the 2016 yearly opening level at 1.0029, the bears could potentially continue pumping the pair down to support penciled in at 0.9861. On the other side of the coin, however, bids remain defensive on the daily chart from the support zone drawn in at 1.0001-0.9957.

Our suggestions: A retest of 1.0019/1.0000 (green zone) would, if a reasonably sized H4 bearish candle took shape (preferably with a full-bodied close), be a relatively nice place to short from given weekly flow. The reason for requiring a confirming bearish candle prior to entry is simply due to the fact that daily buyers could push this market higher.

Data points to consider: FOMC member Kashkari speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.0019/1.0000 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

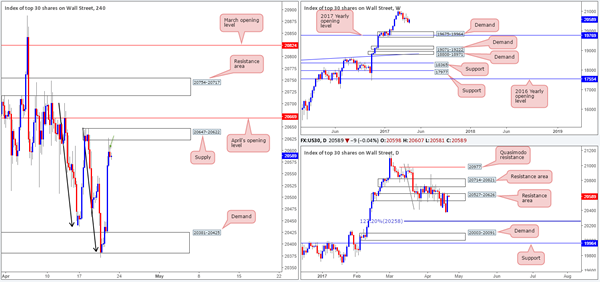

DOW 30

Following a 1:1 downside move seen on the H4 chart (see black arrows), US equities rose higher on Thursday resulting in price testing supply coming in at 20647-20622. Directly above this barrier is April's opening base line at 20669, while to the downside we see very little noteworthy support until demand at 20381-20425.

Swinging across to the bigger picture, we can see that daily movement is retesting the resistance area at 20527-20626 for the second time this week. The next downside target from this angle sits at 20258: an AB=CD 127.2 Fib ext. taken from the high 21022. Weekly flow on the other hand, still looks poised to extend the pullback seen from record highs of 21170 down to 19675-19964: a demand area that's bolstered by the 2017 yearly opening level at 19769.

Our suggestions: According to our technicals, the bears have the upper hand at the moment. As such, we have entered short on the close of the bearish candle seen marked with a green arrow, with stops planted above the supply at 20649 and an overall take-profit target set at the above said H4 demand.

Data points to consider: FOMC member Kashkari speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 20586 ([live position] stop loss: 20649).

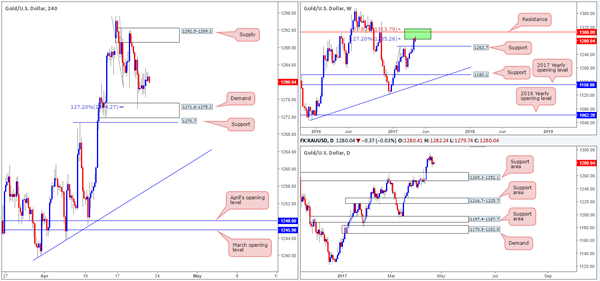

GOLD:

Following Wednesday's bounce from the H4 AB=CD 127.2% ext. at 1274.2 (housed within a H4 demand area at 1271.8-1275.2), gold prices are little changed this morning. Therefore much of the following report will echo similar thoughts put forward in yesterday's analysis…

Although the H4 demand zone has already done a fine job of supporting the bulls, both weekly and daily structure show that the bears could remain in control. Weekly flow shows price trading nicely from two Fibonacci extensions 161.8/127.2% at 1313.7/1285.2 taken from the low 1188.1 (green zone), while daily action has room to stretch down to a support area marked at 1265.2-1252.1 (a weekly support line at 1263.7 is seen housed within this daily area which is the next downside target on the weekly scale).

Our suggestions: Given the little change, we do not see much to go on at the moment. Here's why:

A long would, of course, place one against potential weekly and daily sellers.

A short, although supported by higher-timeframe flow, is risky given the current H4 demand and nearby H4 support at 1270.7. Even with a H4 close seen beyond these two areas, price would then be too close to the top edge of the daily support area to consider a sell!

Maybe we're missing something here, but it seems like we're trapped at both ends!

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

European Open Briefing: EUR/USD Ran Into Strong

Global Markets:

- Asian stock markets: Nikkei up 0.10 %, Shanghai Composite gained 0.05 %, Hang Seng rose 0.05 %, ASX 200 gained 0.65 %

- Commodities: Gold at $1281 (-0.20 %), Silver at $17.96 (-0.30 %), WTI Oil at $50.75 (+0.05 %), Brent Oil at $53.00 (+0.05 %)

- Rates: US 10 year yield at 2.24, UK 10 year yield at 1.07, German 10 year yield at 0.25

News & Data:

- Japan Nikkei Manufacturing PMI (Apr): 52.8 (prev 52.4)

- New Zealand ANZ Consumer Confidence (MoM) (Apr): -2.8% to 121.7 (prev -1.70% to 125.2)

- Asian stocks climb, euro surrenders gains as French election jitters return – RTRS

- Oil prices set for biggest weekly drop in a month – RTRS

Markets Update:

EUR/USD ran into strong resistance at 1.0775 yesterday and retraced back to 1.0715 later in the NY session. In Asia, the pair consolidated within a 1.0705-20 range. Larger gains seem unlikely ahead of the weekend, as most traders are waiting for the outcome of the first round of the French presidential election.

GBP/USD volatility has decreased significantly following Tuesday's big rally. The pair traded in a 1.2795-1.2815 range. However, GBP will likely remain bid in the short-term and good support is seen at 1.2750.

USD/JPY managed to break above 109.20 resistance yesterday, but still lacks momentum. Strong resistance is seen at 110, and selling rallies is still preferred as the downtrend remains intact.

Amid a lack of data and events, the Australian Dollar consolidated as well. AUD/USD traded in a 0.7515-35 range.

Upcoming Events:

- 08:00 GMT – French Manufacturing PMI

- 08:00 GMT – French Services PMI

- 08:30 GMT – German Manufacturing PMI

- 08:30 GMT – German Services PMI

- 09:00 GMT – Euro Zone Manufacturing PMI

- 09:00 GMT – Euro Zone Services PMI

- 09:30 GMT – UK Retail Sales

- 13:30 GMT – Canadian CPI

- 14:45 GMT – US Manufacturing PMI

- 14:45 GMT – US Services PMI

- 15:00 GMT – US Existing Home Sales

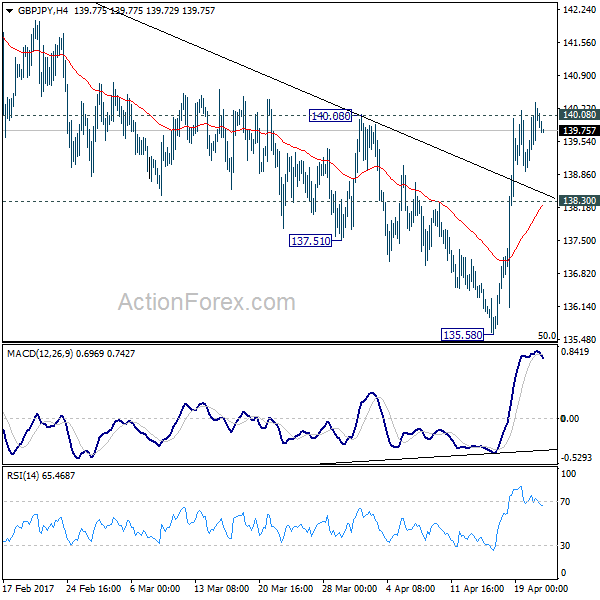

GBP/JPY Daily Outlook

Daily Pivots: (S1) 139.21; (P) 139.77; (R1) 140.59; More....

With 138.30 minor support intact, further rise is still expected in GBP/JPY. Current developments argues that consolidation pattern from 148.42 is possibly completed at 135.58, just ahead of 135.39 fibonacci level. Decisive break of 140.08 resistance will affirm this case. GBP/JPY should then target a test on 148.42 key resistance level. However, break of 138.30 will turn focus back to 135.58 low instead.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.

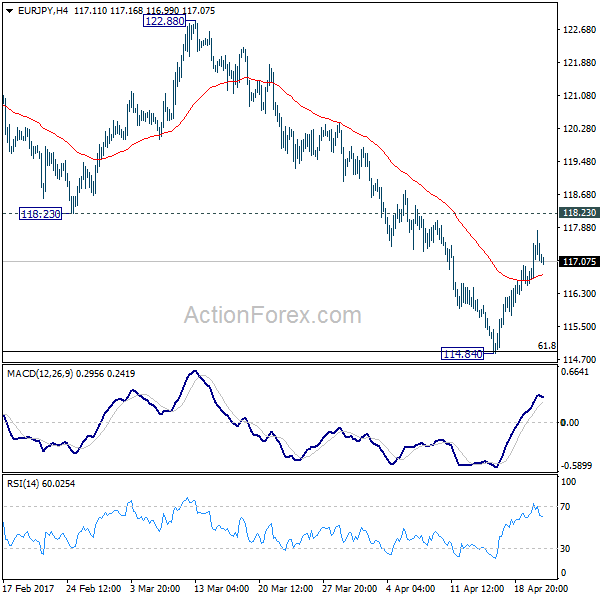

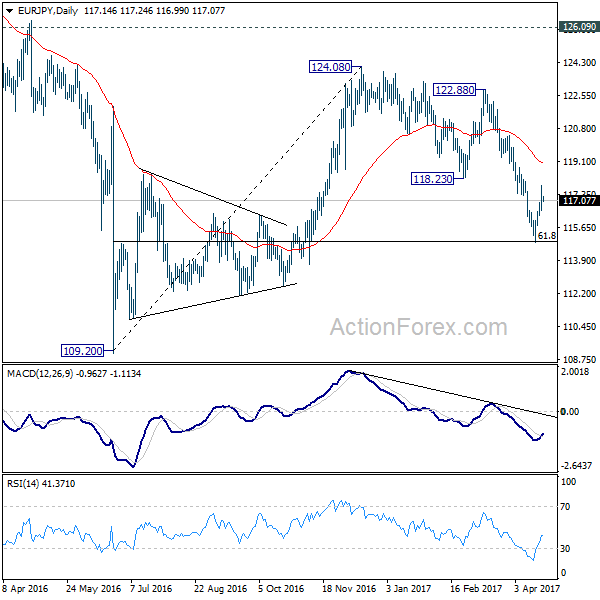

EUR/JPY Daily Outlook

Daily Pivots: (S1) 116.49; (P) 117.15; (R1) 117.80; More...

EUR/JPY's rebound from 114.84 extended higher but at this point, it's kept below 118.23 support turned resistance. Hence, intraday bias stays neutral at this point and outlook remains bearish. Below 61.8% retracement of 109.20 to 124.08 at 114.88 will extend the decline from 124.08 to retest 109.20 low. However, firm break of 118.23 will indicate near term reversal and target 122.88 resistance instead.

In the bigger picture, medium term corrective rise from 109.20 should have completed at 124.08, ahead of 126.09 support turned resistance. Medium term down trend from 149.76 is likely resuming. Break of 109.20 will target 94.11 low. In any case, break of 126.09 is needed needed to confirm medium term reversal. Otherwise, outlook will remain bearish in case of another rebound.

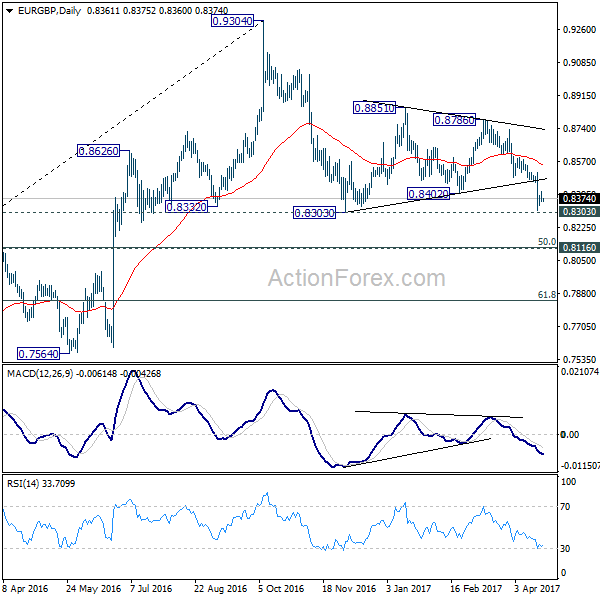

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8344; (P) 0.8379; (R1) 0.8398; More...

A temporary low is in place at EUR/GBP at 0.8312, ahead of 0.8303 low. Intraday bias is turned neutral for consolidation. But upside of recovery should be limited below 0.8511 resistance and bring another decline. Below 0.8303 will extend the whole corrective fall from 0.9304 towards 0.8116/20 key cluster support. We'd expect strong support there to completion the correction and bring rebound.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4199; (P) 1.4267; (R1) 1.4305; More...

A temporary top is in place at 1.4334 and intraday bias in EUR/AUD is turned neutral first. We're holding on to the case off trend reversal after defending 1.3671 key support. Downside of current retreat should be contained well above 1.3980 support and bring another rally. Above 1.4334 will target 1.4721 key resistance. Decisive break there will confirm our bullish view.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0680; (P) 1.0700; (R1) 1.0720; More...

The break of 1.0699 minor resistance indicates short term bottoming at 1.0652. And the corrective fall from 1.0823 has completed. Intraday bias is turned back to the upside for 1.0823 resistance. At this point, there is no clear sign of trend reversal yet. Hence, we'd be cautious on strong resistance from 1.0823 to limit upside. Meanwhile, below 1.0652 will turn bias back to the downside for 1.0620/29 support zone.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Current development suggests that it's not completed yet. Sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. In any case, break of 1.0823 resistance is needed to be the first indication of reversal. Otherwise, deeper fall is still expected even in case of recovery.