Sample Category Title

EUR/CHF Moving Sideways, EUR/JPY Stabilizing, EUR/GBP Grinding Lower.

EUR/CHF Moving sideways.

EUR/CHF has paused near the key support at 1.0684 (see also the falling channel). However, the persistent succession of lower highs favours a bearish bias. Hourly resistances can be found at 1.0691 (07/04/2017 high). The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Expected to see further decline.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/JPY Stabilizing.

EUR/JPY recovery bounce off support was short lived and is now challenging the trendline support at 115.95. Next support is given at 113.73 (09/11/2016 low). Resistance stands at 117.43 then 122.88 (13/03/0217 high).

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Grinding lower.

EUR/GBP has broken the key supports area between 0.8787 (13/03/2017) high and 0.8484 (31/03/2017 low). The short-term technical structure is negative as long as the hourly resistance at 0.8596 holds. Another resistance can be found at 0.8645. An hourly support lies at 0.8450 (03/01/2017 low). Expected to show continued weakness.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

USD/CHF Trying To Stabilize, USD/CAD Making Fresh New Lows, AUD/USD Sharp Rally.

USD/CHF Trying to stabilize.

USD/CHF failed to breach 1.0107 dropping sharply to support. The short-term technical structure is negative as long as prices remain below the hourly resistance at 1.0171 (07/03/2017). Hourly support is given at 1.0017 (intraday base low) then 0.9814 (27/03/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/CAD Making fresh new lows.

USD/CAD has broken the support at 1.3265 confirming an underlying bearish trend. Hourly resistances can now be found at 1.3340 (intraday high) and 1.3456 (04/04/2017 high). Support is given at 1.2969 (31/01/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Sharp rally.

AUD/USD continues to strengthen after successful recovery bounce above 0.7510/15 (12/04/2017 high and downtrend channel top) Key resistance stands at 0.7681 (30/03/2017 high). Hourly support is located at 0.7449 (13/01/2017 low).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Recovery Bounce, GBP/USD Bounce Gains More Momentum, USD/JPY Remains Weak.

EUR/USD Recovery bounce.

EUR/USD improved yesterday, yet failure to break resistance indicates a reversal. Monitor the hourly resistances area given by 1.0679. Hourly support can be found at 1.0570 (i11.04.2017 low). Stronger support can be found at 1.0494 (22/02/2017 low). A key resistance stands at 1.0874.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Bounce gains more momentum.

GBP/USD has rallied off key support at 1.2334, suggesting a potential short-term base formation. Key resistance stands at 1.2605 (27/03/2017 high). An hourly support can be found at 1.2581 (12/04/2017 base) then 1.2405 (11/04/2017 low).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Remains weak.

USD/JPY has broken to the downside out of the horizontal support at 110.11 confirming a bearish bias. Other key supports lie at a distant 106.04 (11/11/2016 low). An hourly resistance can be found at 110.11, while a key resistance stands at 112.20 (31/03/2017 high).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

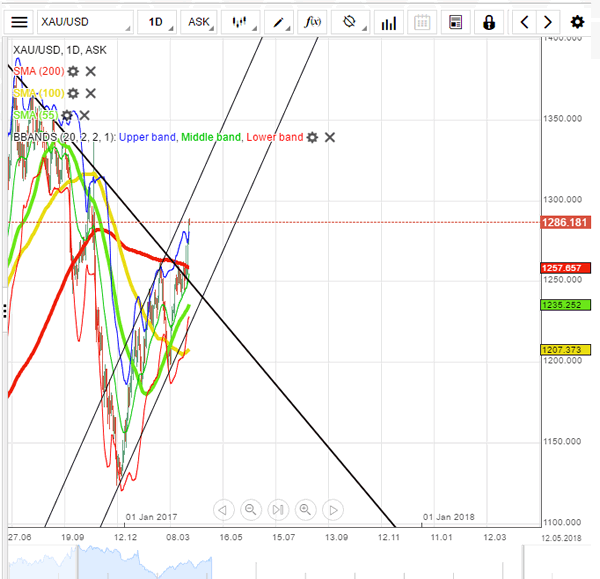

Technical Outlook: Gold May Extend To Psychological $1300 Barrier On Break Above Weekly Cloud Top

Spot Gold is consolidating within narrow range around $1286 target (Fibo 76.4% of $1337/$1122 descend) which was met on strong two-day bullish acceleration.

Gold was initially supported by rising geopolitical concerns that boosted demand for safe haven assets and fresh weakness of the dollar, triggered by comments from US President Donald Trump who said that the dollar is too strong and that he prefers lower rates.

Interest rate sensitive gold reacted on comments on strong bullish acceleration that ended with nearly 2.5% gains in past two days.

Strong bullish sentiment keeps gold well supported for attack at next strong barrier at $1293 (weekly cloud top) and psychological $1300 barrier in extension.

Overbought daily studies warn of easing, which might be boosted by profit-taking after strong rally at the end of holiday-shortened week, however, no firmer technical signals have been generated for now.

Session low at $1283 marks immediate support, ahead of Wednesday’s low at $1271 and rising daily Tenkan-sen at $1265.

Res: 1287, 1293, 1300, 1307

Sup: 1283, 1279, 1271, 1265

Technical Outlook: Aussie Surged In Asia On Weaker Greenback, Upbeat Jobs Data

The Aussie dollar was the top winner in Asian session, gaining nearly 1% against the US dollar and hitting session high at 0.7600 zone.

The pair accelerated higher in late Wednesday after President Donald Trump said that the US dollar is getting too strong that pushed the greenback sharply lower across the board.

The Aussie received fresh boost from Australian jobs data that showed unexpected increase in number of employed people in March by 60.900, which came well above forecasted 20.000 and upwards-revised number of 2800 new jobs in February.

Aussie rallied sharply from session low at 0.7514 and peaked ticks ahead of psychological 0.7600 barrier (Fibo 61.8% of 0.7677/0.7472 downleg), which is reinforced by converged daily 30/20SMA’s.

Initial bullish signal was generated on Wednesday’s close above 100SMA (0.7515), with subsequent strong bullish acceleration that took out next pivot at 0.7550 (200SMA), turning near-term picture bullish.

The pair may enter consolidative /corrective phase ahead of cluster of resistances at 0.7600/20 zone, as near-term studies are extremely overbought. Downticks should hold above broken 200SMA to keep fresh near-term bulls in play for further upside action.

Conversely, loss of 200SMA handle would soften near-term structure and turn risk lower.

Res: 0.7593, 0.7620, 0.7642, 0.7677

Sup: 0.7575, 0.7550, 0.7515, 0.7472

EUR/USD: Trades Near 1.06 Mark

'I think our dollar is getting too strong, and partially that's my fault because people have confidence in me.' – Donald Trump (based on Bloomberg)

Pair's Outlook

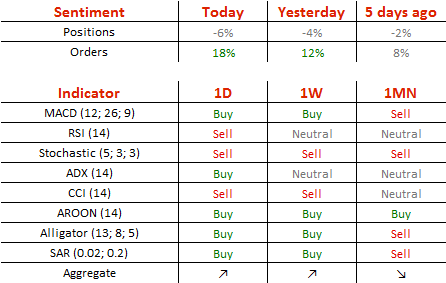

The common European currency traded above the 1.0650 mark against the US Dollar on Wednesday morning, as the currency exchange rate was approaching the monthly PP, which was located at the 1.0686 level. The pair traded a lot higher and had surged on Wednesday due to comments made by the President of the US Donald Trump, who remarked that he would like to see the Greenback weaker for the purpose of stimulating exports. The rate is most likely going to pass the resistance of the monthly PP and begin to move higher. Afterwards the next resistance is the weekly R2 at 1.0729 mark.

Traders' Sentiment

SWFX trades have not changed their opinion, as 51% of open positions are long. However, 56% of trader set up orders are to buy.

GBP/USD: Takes A Shot At Breaking The Down-Trend

'In view rising geopolitical risk and Brexit uncertainties, we expect limited upside potential in GBPUSD this week.' – BMO Capital Markets (based on PoundSterlingLive)

Pair's Outlook

The Cable's upside development yesterday caused the six-month down-trend to be put to the test again, pointing to a possible trend reversal. Technical indicators once more suggest the British Pound is to outperform the Greenback, but even if the resistance line gets fully pierced, there are still obstacles on the Cable's path, the main one being the 200-day SMA around 1.2634. Nevertheless, in case of another bullish development today gains are unlikely to exceed the 1.26 major level. On the other hand, a set of positive US fundamentals could provide the Buck with a sufficient boost, which would result in the pair's decline and a solid reconfirmation of the bearish trend-line.

Traders' Sentiment

Today only 54% of all open positions are long (previously 55). At the same time, the share of sell orders inched up from 49 to 55%.

USD/JPY: Attempts To Erase Wednesday’s Losses

'The dollar's already under pressure, so I think any excuse for further pressure is likely to bring the greenback even lower.' – Kathy Lien, BK Asset Management (based on Business Recorder)

Pair's Outlook

The USD/JPY currency pair experienced another leg down on Wednesday, causing the descending channel's support line to be reconfirmed. From a technical perspective another decline is doubtful, as the channel's support line is now also reinforced by the weekly S3 and the 200d-day SMA. Although the Greenback has a number of resistances on its path today, those are not expected to prevent the US Dollar from recovering today, despite technical indicators suggesting otherwise. However, gains are likely to be capped near 110.00, with the exchange rate beginning its journey towards the channel's upper border.

Traders' Sentiment

Bullish market sentiment remains unchanged at 70%, while the portion of purchase orders inched lower from 61 to 56%.

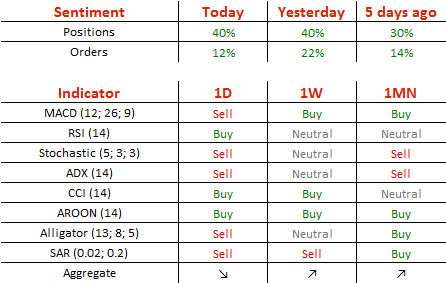

Gold: Reaches Above 1,285 Level

"The market is slightly on the overbought side, but given what we have seen in the past few days, we might see prices testing $1,300." – Wang Tao, Reuters Pair's Outlook Due to US Dollar weakness caused by comments made by Donald Trump on Wednesday the yellow metals price jumped and reached above the 1,285 level. There it remained on Thursday morning. The bullion is most likely going to continue the surge and test the resistance levels near the 1,300 mark, as it faces no resistance up to the 1,297.58 mark, where the weekly R3 is located at. Meanwhile, the rate is supported by the weekly R2, which is located at the 1,284.58 level. However, it is unlikely that the 1,300 mark will be passed, as a strong cluster of resistance surrounds it. Traders' Sentiment Traders remain bearish, as 53% of open positions are short. Meanwhile, 59% of pending commands are to buy the metal.

United Kingdom Inflation-Adjusted Pay Growth Inches Up Just 0.2% In Three Months To February

'Big picture remains a labour market with very strong employment plateauing at record highs ... combined with a pay disaster.' - Torsten Bell, Resolution Foundation

Employment data released on Wednesday confirmed the view that pay growth in the United Kingdom slowed significantly following the country's decision to leave the European Union, which boosted inflation across the country amid the sharp fall in the value of the Pound. The Office for National Statistics reported that wage growth adjusted for inflation climbed just 0.2% in the three-month period to February. Including bonuses, average hourly earnings advanced 2.3%, unchanged from the prior period, whereas analysts anticipated a 2.1% gain. Pay growth is closely followed by the Bank of England, as it is tied to consumer spending, which account for more than 60% of the UK economy. At its latest meeting, the BoE said that consumer inflation would average 2.7% this year. Meanwhile, the unemployment rate came in at a record low of 4.7%, unchanged from the three-month period to January and in line with analysts' expectations. The number of Britons filing for unemployment aid rose 25,500 to 765,400 in March, the largest gain since July 2011, compared to the preceding month's downwardly revised fall of 6,100, while markets held expectations for a decline of 10,200. The data also showed that job vacancies advanced 16,000 to a record high of 767,000.