Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bullish momentum yesterday topped at 1.0736 after bounced off the trend line support as you can see on my H4 chart above and now traded above the H4 EMA 200. The bias is bullish in nearest term testing 1.0825 before retesting 1.0873 key resistance which remains a good place to sell with a tight stop loss. Immediate support is seen around 1.0700. A clear break below that area could lead price to neutral zone in nearest term testing 1.0650 region. Overall I remain neutral.

GBPUSD

The GBPUSD surged higher to 1.2903 yesterday and closed at 1.2841, just above the daily EMA 200 (1.2780) as you can see on my daily chart above. From a daily chart perspective, the movement above the daily EMA 200 following a double bottom formation at 1.2000 psychological level suggests a valid bullish scenario. The bias is bullish in nearest term testing 1.3000 – 1.3050 area. Immediate support is seen around 1.2780. A clear break and daily close back below that area would interrupt the bullish scenario and reactivate my neutral mode.

USDJPY

The USDJPY had a bearish momentum yesterday bottomed at 108.31. This is a good sign for the bearish scenario, but note that as long as stay above 108.13, the hammer/pin bar bullish reversal warning remains valid. The bias is bearish in nearest term testing 108.13. A clear break below that area would expose 107.50 or lower. Immediate resistance is seen around 108.80. A clear break above that area could lead price to neutral zone in nearest term testing 109.20 area but key resistance remains at 110.10.

USDCHF

The USDCHF had a significant bearish momentum yesterday bottomed at 0.9955. The bias is bearish in nearest term. Price fell below the H4 EMA 200 as you can see on my H4 chart above suggests a bearish outlook testing 0.9880 before retesting 0.9813. Immediate resistance is seen around 1.0020. A clear break and daily close back above that area could lead price to neutral zone in nearest term as direction would become unclear. Overall I remain neutral.

Trade Idea : USD/JPY – Hold long entered at 108.45

USD/JPY - 108.84

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 108.64

Kijun-Sen level : 108.74

Ichimoku cloud top : 108.90

Ichimoku cloud bottom : 108.68

Original strategy :

Bought at 108.45, Target: 109.45, Stop: 108.10

Position : - Long at 108.45

Target : - 109.45

Stop : - 108.10

New strategy :

Hold long entered at 108.45, Target: 109.45, Stop: 108.30

Position : - Long at 108.45

Target : - 109.45

Stop : - 108.30

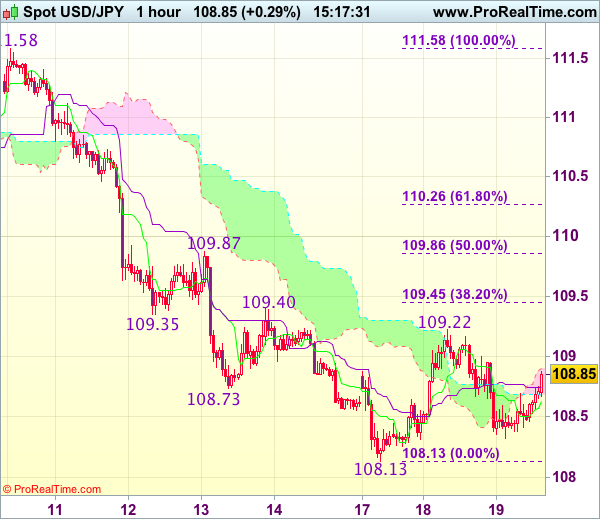

Although the greenback slipped to 108.32 overnight, as dollar found renewed buying interest there and has staged a rebound, retaining our view that further consolidation above this week’s low at 108.13 would be seen and test of resistance at 109.22 is likely, break there would add credence to our view that a temporary low has been formed there, bring retracement of recent decline to 109.40-45 (previous resistance and 38.2% Fibonacci retracement of 111.58-108.13), however, reckon upside would be limited to 109.86-87 (50% Fibonacci retracement and previous resistance) and price should falter below 110.25-30 (61.8% Fibonacci retracement), bring retreat later.

In view of this, we are holding on to our long position entered at 108.45. Below 108.30-32 would risk retest of 108.13 support (this week’s low) but break there is needed to signal recent decline has resumed and extend weakness to 107.75-80 later.

Investors Dump Risky Assets In Favor Of Treasuries, Pound On The Radar

Asian equity markets fell across the board on Wednesday, following a negative lead from the U.S. on earnings disappointment and lower commodity prices despite a weaker U.S. dollar.

The geopolitical tensions concerning North Korea, the French elections, and growing skepticism around the U.S. administration’s ability to deliver on policy pledges drove investors to treasuries, with U.S. 10-year yields dropping to their lowest levels since mid-November. The yield on Japan’s 10-year bonds fell into negative territory earlier today. The more worrying signs are in the shape of the yield curves which seem to be flattening nowadays, an indication of slowing economic growth leading to further selloff in equities. If yield curves continued to flatten further, we’re likely to see a steeper selloff in equities led by banks.

The focus in currency markets remains on the Pound. Yesterday’s surprise move by U.K. Prime Minister Theresa May calling a snap election sent the GBPUSD to its highest levels since October. The 400-pip move from low to high is not a reflection of the short-term fundamental outlook for the U.K.’s economy. But traders expect the snap election to lead to stronger negotiation powers with the EU on Brexit terms, thus a softer exit. Today we expect May to win parliamentary support for the snap election, but the reaction on the Pound to be mild, given it’s already priced in.

The Prime Minister was heavily criticized by some media yesterday, given that only last month she ruled out an early election, but any politician in her shoes would have followed a similar path given the weak position of the opponents.

Although a new vote will add some new uncertainties, the expected larger Conservative majority from an early election will reduce some of the longer-term noise, and given that the Pound is relatively cheap from a fundamental perspective, there’s more potential to see upside moves. However, a lot will depend on the EU side, and whether they decide to take a hard or soft stance.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD,AUDUSD, GBPCAD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EURUSD pair was dragged by strong rally of sterling and overall weaker dollar and rallied strongly on Tuesday, gaining almost 1% in the biggest one-day rally since Mar 15 that hit fresh three-week high above 1.0700 breakpoint. Lift above 1.0700 signalled extended correction of 1.0906/1.0570 descend, as the pair approaches next pivot at 1.0738 (daily Kijun-sen line / 50% retracement). Daily close above 1.0700 is seen as strong bullish signal, while extension above Kijun-sen barrier is needed to confirm bullish continuation which may extend towards next significant barrier at 1.0776 (Fibonacci 61.8% retracement).

The Euro will be looking for Wednesday's release of Eurozone CPI data for March, which may further boost teh single currency in better-than-expected release (CPI m/m is forecasted at 0.8% in March compared to 0.4% in Feb, while annualized inflation is seen unchanged at 1.5% in March.

The pair is also looking for Eurozone's Trade Balance which is expected to show significant surplus in March (forecast is for 16.2 billion Euros surplus vs 600 million deficit in Feb).

Tuesday's strong rally improved the structure of daily technical studies which became more supportive for further gains.

Broken 1.0700 barrier now acts as support, reinforced by 20SMA, which should ideally contain dips and keep fresh bulls intact.

Support: 1.0700. 1.0677. 1.0663. 1.0636

Resistance: 1.0738. 1.0777. 1.0800. 1.0826

USD/JPY

USD JPY came under pressure again and ended day in red, also closing below 200SMA, after failing to capitalize from bullish signal for stronger recovery, marked by Monday's long-tailed daily candle. The pair dipped below hourly Ichimoku cloud (spanned between 108.74 and 108.48 that was acting as solid support initially) after failure to sustain break above 109.00 handle.

Limited corrective action was forecasted on yesterday's technical comment, as technical studies remain in firm bearish mode and so far ignore strongly oversold daily studies, on the way to key near-term support at 108.11 (Monday's fresh five month low).

negative sentiment on strong safe haven buying on rising geopolitical tensions keeps yen well supported for further advance against the US dollar.

The pair is currently riding on the third wave of five-wave cycle from 118.60 and looking for close below cracked 100% Fibonacci Expansion level at 108.48, to validate wave principles and open way extension towards 106.82 (FE 123.6%).

Interim support lies at 107.86 (Fibonacci 61.8% retracement of 101.18/118.65 rally).

Support: 108.32. 108.11. 107.86. 107.00

Resistance: 108.94. 109.22. 109.43. 109.84

GBP/USD

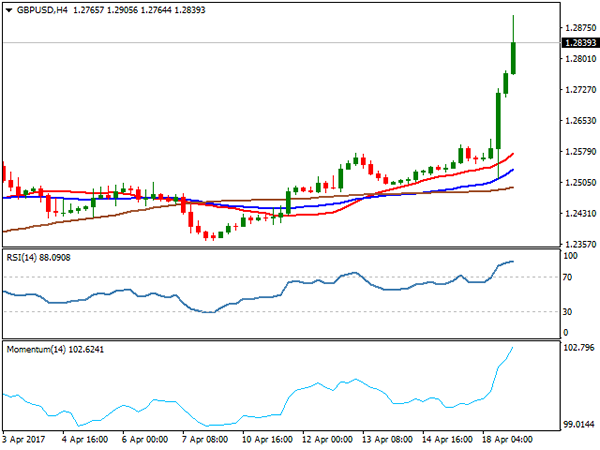

British pound was top performer on Tuesday, gaining over 2.2% against the dollar, on the biggest one-day rally after 17Jan surge. The pair was in quiet mode during Asian and early European session, before jumping on the roller-coaster. News that UK PM Theresa May was going to deliver the statement in front of her Downing Street 10 office, signalled something serious ahead. Initial rumours about May's possible resignation pushed pound around 100-pips lower to hit daily low at 1.2513 against the greenback. After speculations proved to be false, sterling recovered almost all losses, and surged higher after PM May announced early election in UK, scheduled for June 8. May said that early election was the only way to guarantee political stability for the two-year process of divorce from the EU which started last month on triggering an Article 50.

In strong bullish acceleration, cable surged through three round-figure barriers and extended well above the top of post-referendum 1.2722/1.1986 consolidation phase, generating bullish signal for stronger correction of 1.5015/1.1986 fall.

The pair hit daily high at 1.2905, opening way towards psychological 1.3000 barrier and signalling possible extension towards next pivotal barriers at 1.3113/43 (weekly Ichimoku cloud base / Fibonacci 38.2% retracement of 1.5015/1.1986 downleg, on fresh strong bullish sentiment.

Profit-taking on strong Tuesday's rally should be anticipated, however, no firmer bearish signals being generated for now. Initial support lies at 1.2800 zone, followed by pivot at 1.2755 (38.2% of Tuesday's rally) with stronger pullback expected to hold above 1.2663 (Fibonacci 61.8%) to keep strong bulls intact for fresh upside attempts.

Support: 1.2800. 1.2755. 1.2704. 1.2663

Resistance: 1.2905. 1.2950. 1.3000. 1.3060

AUDUSD

The Aussie dollar fell sharply on Tuesday, making the first day in red after four straight days of strong gains. Pullback from recovery high at 0.7610, where rally was capped by daily Tenkan-sen line, on failure above daily cloud top, has accelerated after release of minutes of RBA's April policy review when the central bank held rates steady at record 1.5% low, as minutes suggested caution on rate views. The pair was also under pressure ahead of comments of US Vice President Pence in Tokyo on continued tensions over North Korea.

The pair spiked to 0.7533 low of the day and the lowest since Apr 13, on probe below pivotal 200SMA at 0.7550, but was unable to close below it, as the price bounced on profit-taking action.

Indicators on daily studies are in negative territory and signal increased downside risk, which requires close below 200SMA to trigger further weakness for test of next strong support at 0.7519 (100SMA).

Meantime, corrective attempts should be capped under 0.7570 (4-hr cloud top / Tenkan-sen) to keep fresh bearish sentiment in play.

Support: 0.7541. 0.7533. 0.7519. 0.7500

Resistance: 0.7570. 0.7605. 0.7611. 0.7630

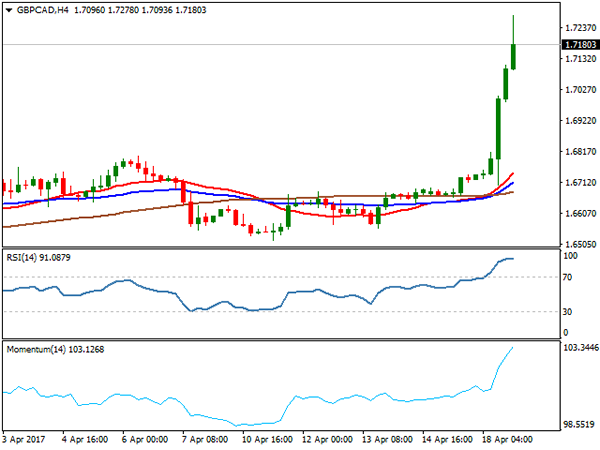

GBPCAD

The GBPCAD cross surged to 1.7278 on Tuesday, hitting the highest since end of Sep 2016, on strong rally of the pound, which was boosted by surprise call for snap election in UK.

Strong rally that took initial barriers at 1.6800/88, as well as psychological 1.7000 barrier, penetrated into thick weekly Ichimoku cloud (cloud base lies at 1.7078) to peak at 1.7278.

Tuesday's strong bullish acceleration broke above med-term consolidation between 1.7119 and 1.5736 and also confirmed double-bottom at 1.5736 (Oct/Jan lows) that is seen as another bullish signal for extension towards net target at 1.7524 (15 Sep 2016 peak).

Support: 1.7100. 1.7000. 1.6896. 1.6806

Resistance: 1.7278. 1.7454. 1.7524. 1.7542

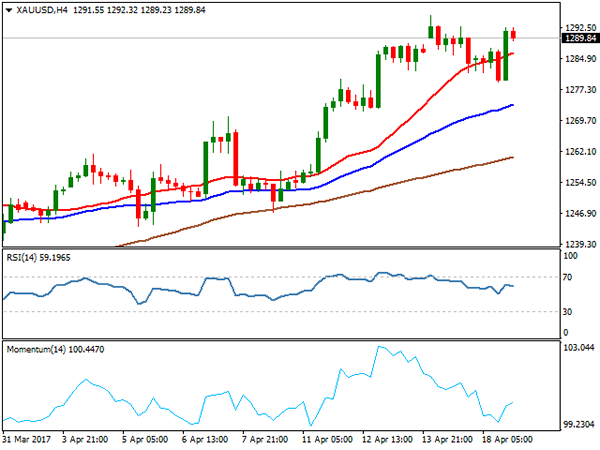

GOLD

Spot Gold remained steady on Tuesday and bounced back to $1292 after posting marginally lower correction low at $1279. The yellow metal remains supported by geopolitical tensions that boost its safe haven appeal and also by weaker dollar. Extended consolidation is expected to precede fresh attack at psychological $1300 barrier and extension towards next target at $1307 on break.

Technical studies remain firmly bullish but overextended that requires caution. However, strong global risk-off mode for now offsets threats of stronger correction on overbought daily RSI / slow stochastic.

Bearish scenario would require firm break below $1277 pivot to signal stronger correction.

Support: 1281. 1279. 1277. 1271

Resistance: 1292. 1295. 1300. 1307

WTI CRUDE OIL

WTI oil remains at the back foot for the fourth consecutive day and extended pullback from fresh five-week high at $53.74 to $52.09, slightly below Fibonacci 23.6% retracement of $47.07/$53.74 rally.

Daily slow stochastic is heading south and showing more room at the downside, after signalling correction on forming bearish divergence. Correction should be ideally contained at $51.66 (daily 55/100SMA bull-cross) to keep intact overall bullish sentiment which was dented by surge in US shale oil output that offsets attempts of oil producers to curb global oversupply by cutting output and boost oil prices.

Conversely, extension below $51.66 would risk test of next pivot at $51.19 (Fibonacci 38.2% retracement) loss of which would signal deeper correction.

Support: 52.09. 51.76. 51.19. 50.41

Resistance: 52.83. 53.18. 53.37. 53.74

DJIA

Dow was dragged lower on Tuesday as call for general election in UK added to the list of uncertainties for investors which were heated by growing tensions from North Korea, through Middle East to France.

Dow was down 0.6% on Tuesday, on bearish acceleration after Monday's recovery was capped by 20/55AMA bear-cross. This has added on already weak technical outlook and increased risk of renewed probe below key daily Ichimoku cloud base support at 20385, which so far managed to contain two attacks. Firm break below cloud base would be seen as strong signal for fresh extension of pullback from all-time high at 21160 (posted on Mar 1) for test of 20266 (Fibonacci 61.8% of 19713/21160 ascend).

Daily Tenkan-sen / Kijun-sen lines in firm bearish a=setup are supportive for further weakness.

Support: 20385. 20266. 20126. 20068

Resistance: 20481. 20580. 20600. 20692

FTSE100

FTSE100 index was among the top losers on Tuesday, as the index was pushed strongly down on UK election decision and sharply higher pound, on the first working day after extended Easter holiday break. FTSE lost nearly 3% on Tuesday's strong bearish acceleration from day's high at 7285 to the lowest of the day at 7056.

Sharp fall that surged through strong support, shaped in rising daily Ichimoku cloud (7253/7184) has weakened daily technical studies which gained strong bearish momentum for further downside, as the price is eyeing key med-term support at 7024 (Feb 2 trough) for full retracement of 7024/7444 rally.

Also completion of asymmetric Head & Shoulders pattern on daily chart adds on strong bearish pressure.

Support: 7056. 7024. 7000. 6954

Resistance: 7100.7125. 7192. 7235

DAX

DAX was firmly in red on Tuesday, following general negative trend for stocks and losing 1.4% for the day. Extension of pullback from record high at 12410 (posted on Apr 03) extended below psychological 12000 support and retracing over 76.4% of 11878/12410 upleg.

Tuesday's long red daily candle weighs on market as daily technical studies are losing traction. Near-term risk is turned lower, as index is eyeing key short-term support at 11878 (Mar 22 low) for full retracement of 11878/12410 bull-leg, loss of which would trigger further easing. Tuesday's fall found temporary footstep at daily 55SMA, with limited upside attempts expected ahead of final push towards 11878 target.

Support: 12000. 11960. 11878. 11718

Resistance: 12081. 12162. 12220. 12267

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8272; (P) 0.8392; (R1) 0.8473; More...

EUR/GBP drops to as low as 0.8312 so far and intraday bias remains on the downside for 0.8303 low. Current fall is seen as the third leg of the corrective pattern from 0.9034. Break of 0.8303 will target 0.8116.20 key cluster support. We'd expect strong support there to completion the correction and bring rebound. But for now, break of 0.8511 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

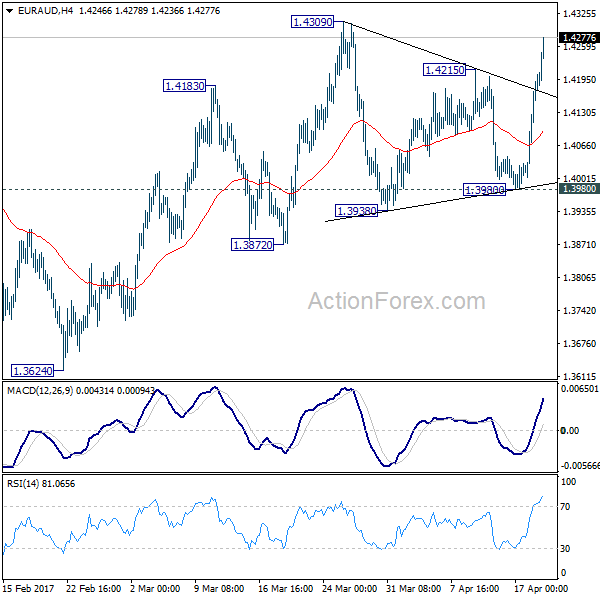

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4061; (P) 1.4134; (R1) 1.4263; More...

EUR/AUD's strong rise and break of 1.4215 resistance suggests that whole rebound from 1.3624 is resuming. Intraday bias is back on the upside fort 1.4039 resistance first. Break will target 1.4721 key resistance next. As noted before, we're favoring the case that larger fall from 1.6587 is completed at 1.3624, after defending 1.3671 key support. And the trend is reversing. Decisive break of 1.4721 should confirm our view. On the downside, however, break of 1.3980 support will dampen this view and turn bias back to the downside for retesting 1.3624 low.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

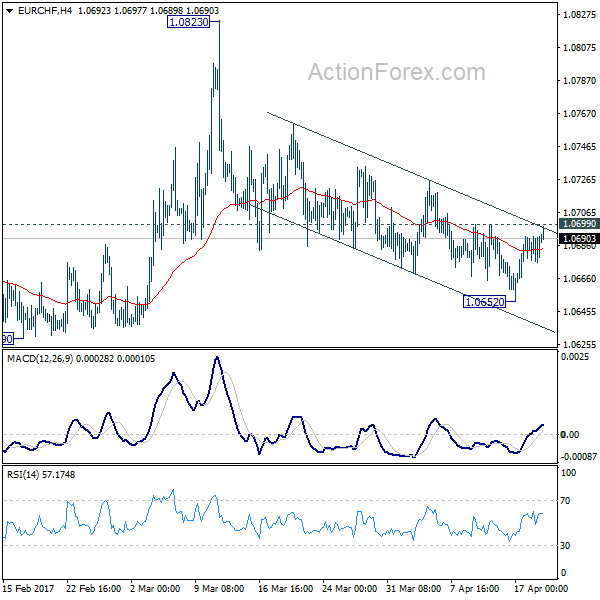

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0678; (P) 1.0685; (R1) 1.0694; More...

EUR/CHF is staying in consolidative trading below 1.0699 minor resistance and intraday bias remains neutral first. With 1.0699 minor resistance intact, deeper decline is still expected. Below 1.0652 will target 1.0620/0629 support zone. Decisive break there will confirm resumption of whole fall from 1.1198. In that case, EUR/CHF should target next long term fibonacci level at 1.0485. On the upside, break of 1.0699 minor resistance will argue that choppy fall from 1.0823 has completed and turn bias back to the upside.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Current development suggests that it's not completed yet. Sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. In any case, break of 1.0823 resistance is needed to be the first indication of reversal. Otherwise, deeper fall is still expected even in case of recovery.

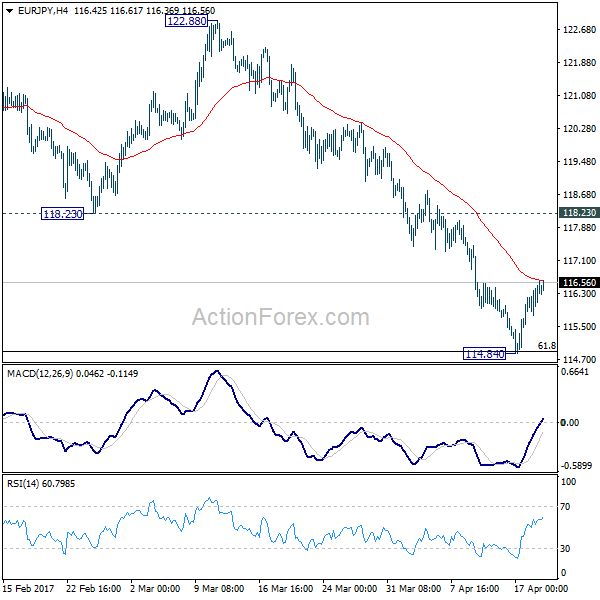

EUR/JPY Daily Outlook

Daily Pivots: (S1) 115.91; (P) 116.19; (R1) 116.64; More...

EUR/JPY's recovery from 114.84 low is still in progress. Intraday bias remains neutral for the moment. At this point, we'd still expect upside to be limited by 118.23 resistance and bring another fall. Corrective rise from 109.20 should have completed at 124.08. Sustained break of 61.8% retracement of 109.20 to 124.08 at 114.88 will pave the way to retest 109.20 low.

In the bigger picture, medium term corrective rise from 109.20 should have completed at 124.08, ahead of 126.09 support turned resistance. Medium term down trend from 149.76 is likely resuming. Break of 109.20 will target 94.11 low. In any case, break of 126.09 is needed needed to confirm medium term reversal. Otherwise, outlook will remain bearish in case of another rebound.

Currencies: Sterling Jumps Sharply Higher As PM May Calls Early Elections

Sunrise Market Commentary

- Rates: Can overbought conditions halt the core bond rally?

Today's eco calendar is empty apart from final EMU inflation data which we don't expect to influence trading. Sentiment remains positive for core bonds, but both the Bund and the US Note future are in overbought conditions, suggesting some consolidation around current levels instead of continuation of the rally. - Currencies: Sterling jumps sharply higher as PM May calls early elections

Yesterday, USD softness persisted as US yields declined further. EUR/USD regained the 1.07 barrier. Today, the calendar is thin so there is probably no trigger to change the dollar's fortunes. Sterling jumped sharply higher as PM May announced early elections. Markets apparently expect the election outcome to provide more stability for the Brexit negotiations

The Sunrise Headlines

- US equities equity markets closed up to 0.3% lower with the Dow Jones underperforming (-0.5%). Overnight, most Asian stock markets lose ground as well with China underperforming (-1%).

- The German government believes an interest rate increase by the ECB would help to reduce Germany's often-criticised export surplus, the Funke Mediengruppe newspaper chain reported.

- Another Federal Reserve policymaker backed an emerging US central bank plan to begin trimming its bond holdings later this year, as Kansas City Fed George warned against waiting too long in order to "overheat" labour markets.

- US President Trump signed a new 'Buy American, Hire American' executive order aimed at cracking down on skilled worker visa abuse and forcing US government agencies to buy more domestically produced products.

- Primary dealers have been asked to respond to questions on the potential demand, pricing and other factors for 40-, 50-, or 100-year bonds, as part of the US Treasury's latest quarterly survey.

- The IMF raised its 2017 global growth forecast from 3.4% to 3.5% due to manufacturing and trade gains in Europe, Japan and China, but warned that protectionist policies threaten to choke a broad-based recovery.

- Today's eco calendar remains thin with only final EMU inflation data. ECB members Coeure, Praet, Hansson and Fed governor Rosengren are scheduled to speak. The Fed releases its Beige Book and Germany taps the market.

Currencies: Sterling Jumps Sharply Higher As PM May Calls Early Elections

Decline US yields continues to weigh on dollar

On Tuesday, global equity softness was again more negative for the dollar than for the euro. The US eco data were mixed with no impact on USD trading. Later in the session, the dollar came under further pressure as the decline in core/US bond yields accelerated. USD/JPY failed to sustain north of 109 and closed the session at 108.43, but Monday's correction low (108.13) was left intact. The dollar also lost ground against the euro. EUR/USD rebounded north of 1.07 and closed the session at 1.0730. Are investors reducing euro shorts ahead of the French presidential election?

Overnight, most Asian equities are trading with modest losses. The yen remains strong with USD/JPY holding in the mid 108 area. The Japanese 10-yield remains around 0.0%, away from the 0.1% BOJ target, but that is no negative for the yen. EUR/USD maintains yesterday's gains, holding in the 1.0720/25 area. So, by default dollar softness remains the name of the game. The Aussie dollar is ceding further ground against a declining USD. Overall negative sentiment on risk, a further decline in the Iron ore price and a soft performance of Chinese equities all weigh on the Aussie dollar. AUD/USD is trading in the 0.7525 area.

Today, the market calendar remains thin. There are no important eco data in the US. In the euro area, the final March CPI and the February trade balance are no market movers. Or is there risk for an upward revision for the CPI?. Earnings reports include Morgan Stanley and Blackrock. Wild cards are the appearances of ECB Coeuré, Praet and Boston Fed Rosengren. The former two are well behind Draghi's policy. Rosengren favoured 4 rate hikes in 2007. We will closely listen whether he backtracks on that rather aggressive stance. The Fed's Beige book is a bit more interesting than usual as the divide between the survey data and the hard data has rarely been wider.

Yesterday, by default dollar softness still dominated FX trading. The move was reinforced by a further decline in US bond yields. Contrary to what was the case of late, USD weakness was mainly visible in USD/EUR and less in USD/JPY. We look out whether this pattern continues. We don't see much room for a sustained EUR/USD rebound. Even so, dollar softness combined with some profit taking on euro shorts a head of the French elections might cause a (temporary ?) bid for the euro.

For the overall USD performance we continue to keep a close eye on the US bond markets. We maintain the view that the correction on the US bond markets has gone far enough. However for now there is no trigger for U-turn. So, it is still too early to position for a rebound of the dollar.

From a technical point of view, USD/JPY broke through the 110 key support, after having failed to regain the 111.36/60 previous range bottom. We downgraded our USD/JPY assessment to bearish, as long as the pair doesn't regain 112.20 (neckline ST double bottom). Next key support (62% retracement) comes in at 107.18. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March, but the test was rejected. EUR/USD returned lower in the 1.0875/1.05. The move did meet support in the 1.06 area as the dollar traded weakish of late. The picture is turning more neutral as the pair returns to the middle of the ST range. We slightly prefer to sell EUR/USD on upticks in case of a return higher in the range as we see room for a broader USD comeback.

EUR/USD: rebounds in the range. USD softness prevails, but a modest euro short-squeeze is probably also in play

EUR/GBP

Sterling propelled as PM calls early elections

Yesterday sterling briefly fell-off a cliff on headlines that UK PM May would make a statement. Rumours on early elections were confirmed as the UK PM called a vote for June 8. Initial sterling weakness was reversed and the UK currency started an impressive rebound. The UK government is largely expected to get a much bigger majority. Markets consider it as a sources of stability. It might give room of manoeuvre in the Brexit negotiations. The jury is still out whether the new political context will really lead to a more balanced Brexit outcome. Anyway, it was used to further reduce sterling shorts. EUR/GBP tumbled more than one big figure (even as the euro traded fairly strong). The pair closed the session at 0.8356. The gain in cable was even more spectacular. The pair closed the session at 1.2824 area, a level not seen since October last year.

Today, there are again no eco data in the UK. PM May will formally ask the House of Commons to support her call for early elections on June 8. The call is expected to get the green light as opposition parties support the call. The day-to-day momentum of sterling is obviously strong. In a longer term perspective, the sterling rally is probably a bit overdone. However, at this stage there is no reason to row against the strong sterling tide.

We had a neutral short-term bias on EUR/GBP. Yesterday sterling dropped below the bottom of the EUR/GBP 0.88/0.84 range. The pair came with reach of the 0.8305 support (Dec low). We look whether this level holds. A break below would be highly significant from a technical point of view. Longer term, Brexitcomplications remain a potential negative for sterling. However, this is not the focus of sterling trading at this stage.

EUR/GBP: nearing the key 0.83 support as PM May calls for early elections

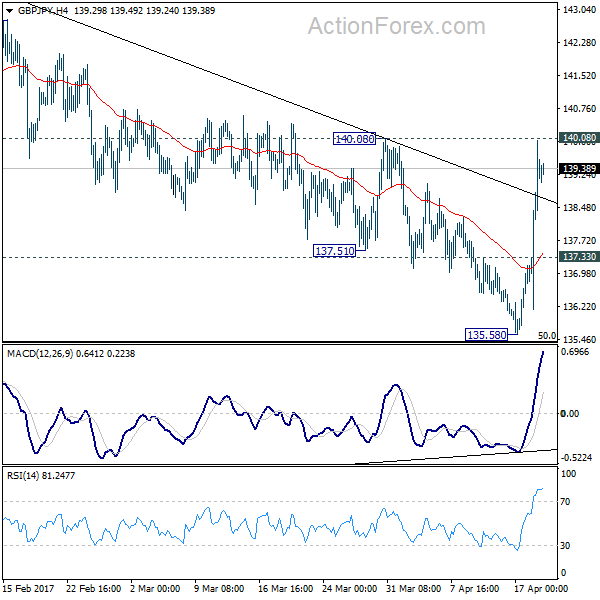

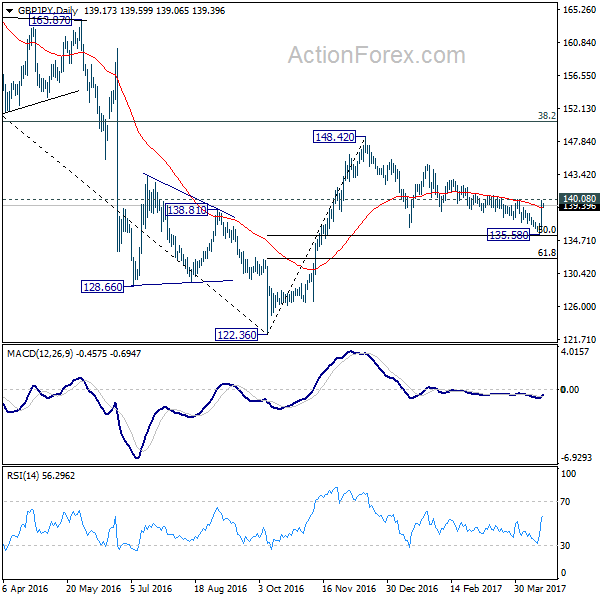

GBP/JPY Daily Outlook

Daily Pivots: (S1) 136.92; (P) 138.46; (R1) 140.80; More...

GBP/JPY rises to as high as 140.01 so far, just inch below 140.08 near term resistance. Current developments argues that consolidation pattern from 148.42 is possibly completed at 135.58, just ahead of 135.39 fibonacci level. Intraday bias stays on the upside and break of 140.08 will affirm this case. GBP/JPY should then target a test on 148.42 key resistance level. Meanwhile, this bullish case will be favored as long as 137.33 minor support holds, in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.