Sample Category Title

GBP/USD Nears Mid-Term Major Resistance After Theresa May Calls Early General Election

The UK Prime Minister made a speech today around 11:15 am at 10 Downing Street.

She stated that the Cabinet had agreed to call an early general election, to be held on June 8. The UK government is determined to execute Brexit process and negotiation with the EU, and this is the right decision for the country's interests. The post-Brexit vote economic indicators have shown that the UK economy is more solid than expected to withstand Brexit impact.

However, some other political parties are still against Brexit and the deal the UK reach with the EU, such as the Labour, Liberal and Scottish National Party. Although the Conservative Party is the majority in the Parliament. Nevertheless, the unity of other opposing parties will outnumber the Conservative, and hence it will weaken the UK government's negotiation position with the EU.

In order to remove the political opposition and eliminate uncertainties, Theresa May attempts to increase the number of Conservative MPs by moving forward the general election.

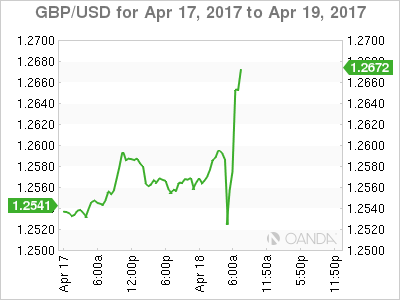

GBP/USD saw a dramatic reversal this morning ahead of the speech due to the uncertainties. It surged around 110 points after the speech with strong bullish momentum on realization of speculation, breaking the psychological resistance level at 1.2600.

The bulls are currently edging up, with an attempt to test the next significant resistance level at 1.2700. However, the level is the mid-term major resistance level, where there is heavy pressure, be aware that the bullish momentum is likely to be restrained while nearing the level.

GBP/USD has been trading above the downside uptrend line support since April 10.

The resistance level is at 1.2680, followed by 1.2700.

The support line is at 1.2650, followed by 1.2620.

DAX Dips on North Korea, French Election Concerns

The DAX has posted slight losses on Tuesday, as the index trades at 12,025.00. On the release front, there are no events in the eurozone. On Wednesday, the eurozone releases Final CPI, with the indicator expected to soften to 1.5 percent.

The DAX was closed on Monday for Easter, and has resumed trade on Tuesday with slight losses. Investors are keeping a close eye on the French presidential election, with the first round of voting slated for April 23. The race remains extremely tight, with centrist Emmanuel Macron and far-right candidate Marine Le Pen tied at 22 percent. They are followed by Francois Fillon at 21% and Jean-Luc Melenchon at 18 percent. If Macron and Le Pen reach the second round, Macron is expected to win decisively by a margin of 64-36. With only a few days to go before the vote, any change in poll numbers could have a significant impact on the stock markets. Another factor weighing on the markets is the crisis over North Korea, as the US continues to warn North Korea that that it will not allow the rogue country to continue to test ballistic missiles. US vice-president Mike Pence is in Japan for talks with Japanese officials, with trade issues and North Korea high on the agenda.

The eurozone won't release its first event this week until Wednesday, with the release of Eurozone Final CPI for March. CPI has improved over six straight months, and the February reading of 2.0% was noteworthy as it reached the ECB inflation target. This strong figure has raised speculation that if inflation levels continue to move higher, the ECB may have to consider tightening policy in order to curb inflation. However, the markets are expecting the March reading to drop to 1.5%, which would allow the ECB to hold its monetary course. The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

RBA Minutes Reflect The Meeting Statement

Overnight, the Reserve Bank of Australia released the minutes from its latest policy meeting. The minutes reflected more or less the meeting statement, highlighting the softness in labor market indicators, and that the recently announced supervisory measures with regards to lending could ease financial stability risks.

As we noted when we had the meeting, this suggests to us that once these measures take effect, the Bank would be more flexible to cut rates again if needed without being concerned that its actions would amplify risks to the economy. However, following the remarkable jobs report for March, released after the meeting, we don't think that the Bank will proceed with something like that at its upcoming gathering, scheduled on the 2nd of May.

AUD/USD reacted little at the time the minutes came out. The pair has been trading south ahead of the release, and continued drifting lower in the aftermath. It started sliding after it hit resistance near the 0.7600 (R1) barrier and the 50% retracement level of the March 21st – April 12th downtrend. The decline was stopped by the 0.7555 (S1) support, where a decisive dip is possible to carry more bearish extensions, perhaps towards our next support of 0.7515 (S2) marked by the inside swing high of the 11th of April.

With regards to the bigger picture of the pair, the price structure on the daily chart suggests a neutral outlook. The pair has been oscillating within a wide range between the 0.7160 and 0.7800 zones for more than a year.

US Treasury Secretary helps the dollar recover somewhat

On Monday, the US dollar recovered some of its latest losses against the yen after the US Treasury Secretary Steven Mnuchin told the Financial Times that a strong dollar would be a good thing in the long term. His remarks come a few days after US President Trump jawboned the currency by saying that it is “getting too strong”. However, Mnuchin said that Trump's remarks were about the short-term and agreed that this is hurting exports.

USD/JPY traded higher after it hit support near the 108.15 (S2) level, and broke back above 108.80 (S1). The recovery was stopped slightly below our resistance of 109.30 (R1). Even if the pair continues to trade higher for a while, we would tread any further recovery as a corrective move and we expect it to remain limited. Tensions over North Korea are far from diminished and as such, headlines that could heighten these concerns further may cause the pair to turn down again. A dip back below 108.80 (S1) may confirm the case and is possible to pave the way for another test near 108.15 (S2). The nervousness over the economic dialog between the US and Japan, as well as the upcoming French presidential elections could also keep any USD/JPY rebounds limited.

Today:

From the US we get industrial production for March. Expectations are for industrial output to have accelerated to +0.5% mom from +0.1% mom the previous month, which could support somewhat the greenback. However, for the reasons we just outlined, we expect any possible USD-strength from this data point to remain short-lived, especially against safe havens like the yen. We also get building permits and housing starts, both for March.

From New Zealand, the GDT (Global Dairy Trade) index is coming out, though no forecast is available. Although this could impact the Kiwi at the release, we believe that NZD-traders have their gaze locked on the nation's CPI data for Q1 due out on Thursday. As such, any reaction on the GDT index could stay limited.

As for the speakers, we have one scheduled on the agenda: Kansas City Fed President Esther George.

AUD/USD

Support: 0.7555 (S1), 0.7515 (S2), 0.7475 (S3)

Resistance: 0.7600 (R1), 0.7625 (R2), 0.7650 (R3)

USD/JPY

Support: 108.80 (S1), 108.15 (S2), 107.70 (S3)

Resistance: 109.30 (R1), 110.00 (R2), 110.75 (R3)

Daily Technical Analysis: EUR/USD Breaks Resistance And Continues Retracement To 1.0750

Currency pair EUR/USD

The EUR/USD broke above the resistance trend line (dotted red) as expected which could signal a larger retracement within wave 2 (brown). Price could head back to 1.0750-1.0775 at the 50-61.8% Fibonacci levels.

The EUR/USD break above the resistance trend line (dotted orange) which could trigger the development of an ABC (purple) zigzag.

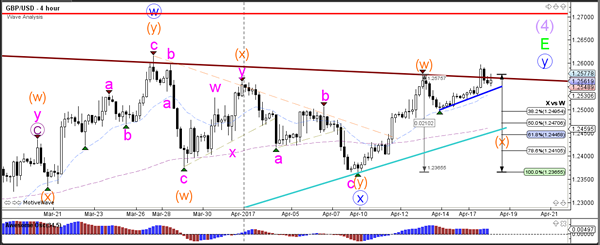

Currency pair GBP/USD

The GBP/USD is challenging the resistance trend line (brown) which is a bounce or break decision zone. A bearish bounce could price fall towards the Fibonacci levels of wave X (orange) whereas a bullish breakout could see price complete wave Y (blue).

The GBP/USD is testing the Fibonacci levels of potential wave B (pink). A break above the 138.2% Fibonacci level would invalidate the wave B (pink).

Currency pair USD/JPY

The USD/JPY is building a potential wave 4 correction (orange), which would become invalid if price retraced above the bottom of wave 1 (red line).

The USD/JPY could be building an ABC (purple) zigzag correction towards the Fibonacci levels of wave 4 (orange). A break below the support trend line (blue) could indicate the completion of that wave 4 (orange).

U.K’s May Calls June Election

Tuesday April 18: Five things the markets are talking about

While many markets were closed for Easter Monday, the pace of new economic data releases picks up today, especially in the U.S.

Gains are expected for the U.S industrial production report (+0.5%e vs. +0.0%) despite last month's poor weather having pulled down factory hours. Housing starts and permits have been good of late, but the March outlook is to be mixed with a dip expected for starts, but continued strength for permits.

The first round of the French presidential elections is this Sunday (April 23) and any anxiety surrounding the outcome is likely to push market risk sentiment higher closer to the end of this week.

Marine Le Pen is expected to be one of the top two to make it to round two, but markets will be content to a certain extent if the socially liberal and pro-business Emmanuel Macron, and not the far-left anti-austerity candidate Jean-Luc Melenchon, is to be her opponent in the run-off vote in a fortnight (May 7).

However, if Melenchon makes it into the next round with Le Pen, markets will be gripped by a new source of fear, bigger than Brexit!

Elsewhere, U.K Prime Minister Theresa calls a snap general election for June 8.

1. Stocks see Red

Markets in Sydney, Hong Kong and Europe have dropped after the Easter holidays, as investors caught up with global markets that have been weighed down by geopolitical concerns.

Japan's Topix has advanced +0.4% overnight on the back of a weaker yen (¥108.88) after U.S Treasury Secretary Mnuchin said the dollar's strength is “a good thing.” In Indonesia, the benchmark jumped +0.7%, while South Korea's Kospi added +0.1%.

In Australia, a selloff in iron ore has pulled down commodity producers. The S&P/ASX 200 fell -0.9%, the most thus far in April. Raw-materials shares in the benchmark index have retreated -4.5% over the past two sessions, the biggest drop for that period in almost a year.

In Hong Kong, stocks played catch up after the four-day long weekend. The Hang Seng lost -1.1% and the Hang Seng China Enterprises Index slumped -1.4%, its lowest close in nearly three months. In China, the Shanghai Composite lost -0.8%, after plummeting -1.6% in the previous two-sessions.

In Europe, equity indices are trading sharply lower after the holiday weekend. Banking stocks are trading generally lower weighing the Eurostoxx, while energy, commodity and mining stocks are all weighing heavily in the FTSE 100.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.6% at 3,429, FTSE -1.1% at 7,249, DAX -0.3% at 12,070, CAC-40 -0.9% at 5,025, IBEX-35 -0.6% at 10,266, FTSE MIB -0.8% at 19,621, SMI -0.5% at 8,589, S&P 500 Futures -0.2%

2. Oil under pressure from a hike in U.S output, gold holding firm

Crude prices fall in thin trade overnight as a U.S. government report indicated a rise in production.

Brent crude futures are down -4c at +$55.32. Yesterday they ended a quiet down -53c, after rising the three previous weeks. U.S. West Texas Intermediate (WTI) crude futures are also down -4c at +$52.61 a barrel. On Monday, they settled down -53c at +$52.65 a barrel.

U.S data yesterday showed that domestic shale production for May is likely to post the biggest monthly gain in more than two-years as producers step up the pace of drilling with oil prices holding above the psychological +$50 a barrel.

The EIA expects the month of May's output to rise by +123k bpd to +5.19m bpd. If so, it will be the biggest monthly increase since February 2015 and the highest monthly production level since November 2015.

Note: OPEC is due to meet on May 25 to weigh an extension of output cuts beyond June to alleviate a glut that has depressed prices for nearly three-years.

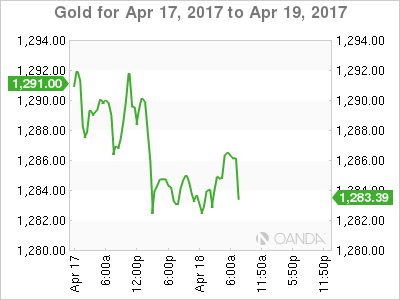

Gold prices held firm overnight (unchanged at +$1,284.56 per ounce) supported by geopolitical tensions over North Korea and market uncertainty re-French presidential election after falling from a five-month high on Monday (+$1,295.80) on a firmer dollar.

Elsewhere, Iron ore futures on the Dalian exchange dropped -4%, after sliding almost -3% yesterday.

3. French/Bund spread remains wide on election jitters

The French Presidential forecast remains too close for comfort. This morning's Ifop poll puts Macron and Le Pen each on +23%, just +3% ahead of Fillon and the far-left Melenchon.

The spread between French and German 10-year bond yields – another indicator of market worries – ranged from +0.767 bps as markets opened, to +0.72 bps ahead of the U.S open. In November, the spread was as little as +0.22 bps.

Elsewhere, the yield on U.S 10's fell -1 bps to +2.24%, while the Aussie benchmark yield backed up +1 bps to +2.49%.

4. Pound collapse on May's impromptu announcement

The pound fell sharply against the USD (£1.2525) and EUR (€0.8490) on the news that U.K PM Theresa May would make an unexpected statement at 11:15 a.m. GMT. It has since taken back some of those earlier losses after PM Theresa May called a June 8 snap election (see below).

EUR/USD will be driven this week by French political development ahead of Sunday's first round of presidential elections. Currently, the EUR is up +0.06% outright (€$1.0650), but stress relating to the French election remains clear in other parts of the currency market.

Note: One-month Euro-dollar risk reversals, which measure the cost to investors of protecting against a sudden decline in the single unit, touched -4.3, the most extreme reading in six-years.

U.S Treasury Secretary Mnuchin has also talked up the USD after Trump's remarks last week that the greenback has gotten “too strong,” noting that “strength of dollar over the long term is a positive.” USD/JPY is trading at ¥108.90 ahead of the U.S open.

5. PM Theresa calls snap election

PM Theresa May has called a snap general election for June 8. Her obvious aim is to strengthen her position going into talks on leaving the European Union. Technically, she seeks a direct mandate to take the country through the “divorce” with the E.U.

Note: Two polls over the weekend put the Conservatives +21 points ahead of Labour, a lead that is likely to greatly increase.

In Brussels May's announcement is likely to be seen as merely adding to the unpredictability of relations with the U.K since last years Brexit referendum.

Stocks, Dollar And Yields Under Geopolitical And Economic Pressure

Global equities and the 'mighty' dollar have again dipped overnight while U.S Treasury yields have fallen to new five-month lows after soft U.S data on Friday hurts investor sentiment already in distress by worries over North Korea and upcoming French elections.

Note: U.S. retail sales dropped more than expected in March (+0.0% vs. +0.2%) while annual core inflation slowed to +2.0%, the smallest advance since November 2015, from +2.2% in Feb.

A raft of Chinese economic data (see below) beat market expectations, but did not produce a notable market reactions, as investors had been already optimistic following a recent string of positive China numbers.

In Turkey, President Erdogan snatched a victory in a referendum Sunday to grant him sweeping powers in the biggest overhaul of modern Turkish politics.

Note: Markets in Australia, New Zealand and Hong Kong, as well as most European exchanges, are closed for Easter Monday.

1. Global equities under pressure

Stock markets across Asia ended mostly lower overnight, as China's securities regulator urged tighter supervision of listed companies, while geopolitical tensions in Korea continued to discourage investors from buying.

Japan's Nikkei Stock Average opened lower, but later recouped the declines to end up +0.1%, snapping a four-session losing streak – the yen (¥108.76) spiked to new yearly highs (¥108.13).

In China, investor market sentiment has worsened over an escalating regulatory crackdown on stock manipulation, despite stronger-than-expected economic data for the Q1. The Shanghai Composite Index ended down -0.7%, while the Shenzhen Composite Index lost -1.4%.

Elsewhere, Singapore's Straits Times Index lost -0.9%, while Taiwan's Taiex ended down -0.2%.

In Turkey, the Borsa Istanbul 100 Index climbed +0.6% – the highest level in more than two-years after President Erodgan's referendum victory yesterday (see below).

In Europe, markets remain closed due to Easter Monday holiday.

U.S stocks are set to open in the 'red' (-0.1%).

2. Oil falls after failed North Korean missile test, U.S rig count gains

Crude oil prices are again under pressure overnight in quiet trading after the Easter break on signs that the U.S continues to add output, undermining OPEC efforts to support prices, and as the market digest North Korea's failed missile launch yesterday.

Ahead of the U.S open, Brent crude futures are down -56c at +$55.33, while West Texas Intermediate (WTI) crude futures are down -51c at +$52.67 a barrel.

Note: Both benchmarks last week rose for a third consecutive week, with Brent adding +1.2% over the four days (Good Friday holiday) while WTI was up +1.8%.

Last Thursday's Baker Hughes (energy services) report indicated that drillers added +11 oil rigs in the week to April 13, bringing the count up to 683, highest in about two-years.

Note: The latest EIA report shows that U.S crude oil production has climbed to +9.24m barrels per day (bpd), making it the world's third-largest producer after Russia and Saudi Arabia.

Gold prices hit a five-month high overnight (+$1,295.42 an ounce) as the dollar weakened with investors taking refuge in safe-haven assets in the wake of rising geopolitical tensions over North Korea.

The 'yellow' metal last week rose +2.5%, posting its biggest weekly gain in 10-months.

3. Global yield curves flatten

Last Friday's disappointing U.S data (retails sales and CPI) has helped to drive down the U.S 10-year Treasury yield to +2.20%, its lowest level since mid-Nov.

In March, U.S 10's were trading atop of +2.6% on expectations of a Trump stimulus package. However, with Trump expected to struggle to push any tax cuts and fiscal spending programs through Congress has supported the markets unwinding of the “Trump” trade.

Current Fed fund futures for June are now pricing in less than a +50% chance of a rate hike in its June 13-14 meeting for the first time in about a month.

Elsewhere, geopolitical and French Presidential election risks have seen the yield on 10-year Bunds fall over -33 bps from its mid-March peak of +0.51% to +0.18%.

The gap between French and German 10-year borrowing costs, an indicator of concerns over the election, is at +71.4 bps, +4 points off one-month highs hit earlier last week.

4. Dollar under geopolitical pressure

The Turkish Lira (TRY) has rallied over +2.4% outright in the wake of this weekend's referendum to expand the executive powers of President Erdogan.

While the “Yes” vote was deemed victorious, the margin of victory at 51.3% vs. 48.7% opposed was well below the 55% mandate predicted by Erdogan and is expected to be challenged by the opposition.

Note: Under upcoming constitutional changes, the winner of next election in 2019 will “gain full control of the government, ending the current parliamentary system, which treated office of the president as a role without full executive authority.”

The 'mighty' USD is trading a tad softer across the board after last week's release of March CPI and retail sales data both underwhelmed. Fixed income dealers are paring back the probability of another Fed rate hike in June.

The EUR is trading +0.2% higher at €1.0630 in quiet trading with most European markets remaining closed for Easter Monday holiday. USD/JPY is trading softer, down -0.3% at ¥108.32. Expect geopolitical worries to continue to support the yen's strength.

5. China data beats expectations

Over the weekend, China economic data offered some positive surprises – GDP, industrial output, and retail sales for Q1 all topped consensus to hit multi-month rates of growth.

Note: The world's second-biggest economy accounted for about one-third of global growth last year and, given the strong Q1, is on track to contribute at least as much this year.

Digging deeper, Q1 GDP y/y rallied to a six-quarter high of +6.9%. Consumption accounted for +77.2% of that growth, up from +64.6% in 2016. Fixed asset investment rose over +10% as property investment value rose +9%, sales value rose +25% and construction up +11%.

Industrial output growth was similarly impressive, rising at the fastest pace in three-years. Power generation was up +7%, while coal and steel output were both up +2% despite the recent production curbs. While March retail sales y/y was +10.9% vs. +9.7%e (3-month high).

USD Strengthens as US and North Korean Tensions Increase

- Sterling slips in data vacuum

- USD strengthens as US and North Korean tensions increase

- Australian Dollar stronger as Aussie employment jumps

The US Dollar strengthened a little over the last few days. Tensions around the US's warning to China over North Korean sabre rattling has dragged funds into safe US treasuries. US President Trump shook the markets on Wednesday when he suggested the US Dollar was too strong. In spite of this strength in the latter part of the week, the Dollar ended the week weaker than it started. This week brings the US Federal Reserve Beige book, manufacturing data in various forms and a slew of Purchasing Managers' Indices (PMI).

The GBP-USD rate is stuck in a narrow band for now but the US Federal Reserve, Kim Jong Un and other factors could change that.

The Sterling-Euro exchange rate is similarly range-bound but the Euro struggled to gain any traction last week as tension mounted over the French elections. Polls suggest Marine Le Pen and Emmanuel Macron are neck and neck for the Presidency with Jean-Luc Mélenchon coming up on the rails. To add to the tension, Le Pen has promised to shut France's borders to get to grips with frenzied immigration. Aside from this, Eurozone inflation data is due on Wednesday, and we'll get German and EU manufacturing PMIs on Friday. That should be enough to keep the Euro busy but perhaps not enough to break it out of its current ranges.

Higher UK inflation boosted the Pound last week but it gave up some of those gains before Thursday's Bank Holiday close. The UK data diary in this foreshortened week is pretty quiet but Friday's UK retail sales numbers will liven things before the weekend.

The Aussie Dollar was boosted last week by very positive employment data. A gain of 60,900 jobs in March trounced the forecast of roughly 20,000. That was helped by positive Chinese trade data - China is Australia's number one export market. The Aussie Dollar could tread water for most of the week, as the minutes from the last RBA meeting is the only notable news to be expected.

And The Metro is reporting about two intact Easter eggs going on display which are from the 1920s. I am mightily impressed; my children's eggs never made it past Easter Monday....and that's if we remembered to hide some.

Short Jokes

Two cows are in a field and one says, "Mooooooooooo"

The other one says, "That was what I was going to say."

Two cows are in a field and one says, "It's hot isn't it."

The other one says, "Blimey, a talking cow."

Two cows are in a field and one says, "Aren't you worried about this Mad Cow disease going around?"

The other cow says, "It doesn't bother me. I'm a hovercraft!''

I met a bloke yesterday who kept shouting about architectural elements of castles. I think he had Turrets Syndrome

What do you call a Russian tyrant with asthma? Vlad the inhaler.

Tomorrow is International Jamaican Hairstyle Day......I'm dreading it.

I have a new hobby. I like to play chess with the old men in the park although sometimes it's hard to find 32 of them.

USDJPY – Looks To Recover Further Higher

USDJPY - The pair rejected lower prices to close higher on Monday leaving risk of more gains on the cards. On the downside, support comes in at the 108.50 level where a break if seen will aim at the 108.00 level. A cut through here will turn focus to the 107.50 level and possibly lower towards the 107.00 level. On the upside, resistance resides at the 109.50 level. Further out, we envisage a possible move towards the 110.00 level. Further out, resistance resides at the 110.50 level with a turn above here aiming at the 111.00 level. On the whole, USDJPY looks to recover further.

Euro Quiet, Markets Eye CPI

EUR/USD is unchanged in the Tuesday session, as the pair trades at 1.0650. There are no eurozone events on the schedule. In the US, there are two key releases – Building Permits and Housing Starts. On Wednesday, the eurozone releases Final CPI.

It's been a quiet start for the euro this week. European markets were closed for Easter Monday, and the euro has shown little movement on Tuesday. The markets are awaiting the release of Eurozone Final CPI for March. CPI has improved over six straight months, and the February reading of 2.0% was noteworthy as it reached the ECB inflation target. This strong figure has raised speculation that if inflation levels continue to move higher, the ECB may have to consider tightening policy in order to curb inflation. However, the markets are expecting the March reading to drop to 1.5%, which would allow the ECB to hold its monetary course. The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

In the US, consumer indicators wrapped up last week on a sour note. CPI declined 0.3%, and Core CPI dropped 0.1%, as both indicators missed their estimates. Consumer spending was no better, as Retail Sales and Core Retail Sales also missed estimates with readings of 0.2% and 0.0%, respectively. Earlier in the week, UoM Consumer Sentiment improved to 98.0, beating expectations and hitting a 3-month high.What is unusual is this data is that consumer confidence levels improved in March, yet consumer spending declined. The US consumer behavior continues to be marked by a “hard/soft discrepancy”, as confidence levels (“soft data”), has not translated into actual spending numbers (“hard data”). The odds of a June rate hike from the Fed has fallen to 46%, down from 64% earlier in April. Janet Yellen & C0. will likely want to see stronger inflation numbers before pressing the rate trigger.

Market Update – European Session: Pending UK PM Statement Stirs Up A Quiet EU Session

Notes/Observations

Quiet European session; Focus turning to 1st round of the French election on Sunday

UK PM to make statement at 06:15 ET/10:15 GMT (no details) but rampant speculation of 'big news'

Fed Vice Chair Fischer clarified again the Fed putting its focus on controlling volatility when reducing the size of its balance sheet

Overnight:

Asia:

China's Mar Property Prices improve, defy curbs, further tightening expected

Japan nominated Goshi Kataoka and Hitoshi Suzuki to BOJ board; will replace BOJ dissenters Sato and Kiuchi (**Note: Appointment suugests that the Abe's government wants to keep the current unprecedented stimulus program in place)

RBA Apr Minutes: Developments in the labour and housing markets warranted careful monitoring over coming months

Europe:

Turkey President Erdogan: European Union should go ahead and make its decision on Turkey; Turkey could hold referendum on suspending EU accession talks if needed

Americas:

Treasury Sec Mnuchin: timeline to get tax reform by Aug is "highly aggressive to not realistic at this point"; schedule has been slowed by the healthcare bill passage problems

Fed Vice Chairman Fischer: Reduction in size of our balance sheet that has taken place so far is that we appear less likely to face major market disturbances now than we did in the case of the taper tantrum

Energy:

EIA forecasts May total shale regions oil production at 5.19M bpd, +123K bbd m/m (vs +109K bpd rise in April)

Economic Data

(DK) Denmark Mar PPI M/M: -0.9% v +0.3% prior; Y/Y: 4.3% v 4.1% prior

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €1.55B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills

(ID) Indonesia sold total IDR3.47T in 2-year,4-year,7-year and 15-year Project-based Sukuk (PBS)

(SK) Slovakia Debt Agency (Ardal) sold total €310.5M in 2026 and 2031 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 -0.6% at 3,429, FTSE -1.1% at 7,249, DAX -0.3% at 12,070, CAC-40 -0.9% at 5,025, IBEX-35 -0.6% at 10,266, FTSE MIB -0.8% at 19,621, SMI -0.5% at 8,589, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes: European equity indices are trading sharply lower in the morning session after a 4-day holiday weekend, as China markets also end the session lower overnight; Further geopolitical tensions adding pressure to the markets amid North Korea concerns and as the French presidential race tightens; Banking stocks trading generally lower adding weight to the indices with shares of BNP Paribas, Deutsche Bank, and SocGen trading notably lower in the Eurostoxx; Energy, commodity and mining stocks all weighing heavily in the FTSE 100 as both copper and oil prices trade sharply lower intraday ahead of API stockpile data. In large M&A news, Post Holdings in the US confirmed to acquire Weetabix for £1.4B.

Upcoming scheduled US earnings (pre-market) include Bank of America, Comerica, GNC Holdings, Goldman Sachs, WW Grainger, Harley Davidson, Johnson & Johnson, Lincoln Electric Holdings, Omnicom Group, Progressive Corp, ProLogis, Regions Financial, Charles Schwab, Synovus Financial, and UnitedHealth Group.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Casino Guichard CO.FR -2.0% (Q1 sales), Hennes & Mauritz HMB.SE -0.5% (March sales)]

Consumer Staples: [Refresco Gerber RFRG.NL +2.4% (PAI said to consider raising bid to ~€20/shr)]

Financials: [Gam Holding GAM.CH -1.2% (Q1 AUM)] - Healthcare: [Circassia CIR.UK -2.2% (Top-Line Results from House Dust Mite Allergy Field Study did not meet primary endpoint)]

Speakers

IMF chief Lagarde reiterated call that Euro Area needed a common finance minister. Reform of euro area remains incomplete as all budgetary measures still taken at national level

Swiss Govt: SNB is independent; currency purchases not aimed at devaluing CHF currency (Swiss Franc) to gain export advantage. Reiterated view that CHF currency remains over-valued

Sweden Fin Min Andersson: Govt considering a sovereign wealth fund as a way of solving its illiquid bond market problem. Ready to take more measures over housing market if needed

Sweden govt present Spring Budget raised both 2017 and 2018 GDP growth forecasts. Forecasted 2017 budget surplus at 0.3% of GDP and 2018 at 0.6% surplus.

Bank of Spain (BOS): Feb Bad loans at 9.1%

Japan Fin Min Aso: Japan and US agreed to combat unfair trade practices - comments alongside US VP Pence

BOJ reportedly considering a slight cut to its FY17/18 inflation estimate of 1.5%

Australia PM Turnbull: To introduce stricter rules on working visas. Our reforms will have a simple focus: Australian jobs and Australian values S&P affirmed Japan's sovereign rating at A+; outlook stable

UAE Energy Min Al Mazrouei reiterated view that compliance between both OPEC and non-OPEC members was improving month by month

Saudi Arabia Feb oil production at 10.011M v 9.748M bpd prior. On Apr 12th OPEC Mar Monthly Report showed Saudi Arabia Mar production at 9.90M vs. 10.01M bpd m/m (Feb)

Fixed Income

Bund futures trade at 163.57 up 3 ticks trading mid range ahead of a busy data week. Futures look to 163.82 initially, with a break back above targeting 163.99 followed by 164.20. A reversal targets 163.41 former high followed by 163.18.

Gilt futures trade at 128.73 up 16 ticks trading approaching 129.00 on risk aversion flows. Support moves to 128.56 followed by 128.24 then 127.94. Continuation higher targets 128.96 followed by 129.24. Short Sterling curve trades flat with Jun17Jun18 trading steady at 9.5bp choice.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.587T a fall of €9B from €1.596T prior. Use of the marginal lending facility rose to €721M from €271M prior.

Corporate issuance saw just $800M come to market via a sole issuer in a light day, with activity expected to pick up today, following the long weekend.

Currencies

FX markets were little changed but the USD remained facing headwinds following the recent string of soft economic data.

USD/JPY began the session back above the 109 level aided by comments from US Treasury Sec Mnuchin suggesting that the US remained committed to its strong USD long-term strategy.Reports circulated that BOJ was considering a slight cut to its FY17/18 inflation estimate of 1.5% at its next policy decision on Apr 27th. The EUR/USD steady in the mid-1.06 area. Focus turning to 1st round of the French election on Sunday

GBP/USD initially hit 3-year highs as the pair tested above the 1.26 level. GBP was softer after PM Theresa May would make a statement (no dteails). The rumor mill went into high gear with suggestions of snap elections or that PM might step down due to health concerns. Dealers noted that the suggested 10:15 GMT time slot was historically used for most serious moments. Pair tested below 1.2550 just ahead of the NY morning.

Looking Ahead

(UK) House of Commons reconvenes after Easter Recess

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (NL) Netherlands Debt Agency (DSTA) to sell up to €2-4B in 3-month and 6-month bills

06:00 (IL) Israel to sell 2020, 2021, 2025, 2027 and 2045 bonds

06:15 (UK) PM Theresa May to make statement

06:30 (EU) ESM to sell €1.5B in 6-month Bills

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Central Bank (BCB) Apr COPOM Minutes

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (BR) Brazil CONAB Report

08:00 (IS) Iceland Mar Unemployment Rate: No est v 2.9% prior

08:00 (RU) Russia announces weekly OFZ bond auction

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Mar Housing Starts: 1.25Me v 1.288M prior; Building Permits: 1.25Me v 1.213M prior

08:30 (CA) Canada Feb Int'l Securities Transactions (CAD): No est v 6.2B prior

08:55 (US) Weekly Redbook Sales

08:50 (FR) France Debt Agency (AFT) to sell combined €5.1-6.3B in 3-month, 6-month and 12-month BTF Bills

09:00 (BE) Belgium Feb Trade Balance: No est v -€1.6B prior

09:00 (CA) Canada Mar Existing Home Sales M/M: No est v 5.2% prior

09:00 (NZ) Fonterra Global Dairy Trade Auction

09:00 (US) Fed's George (non-voter)

09:30 (UK) Chancellor Hammond in House of Commons

09:15 (US) Mar Industrial Production M/M: 0.4%e v 0.0% prior; Capacity Utilization: 76.1%e v 75.4% prior, Manufacturing Production: 0.1%e v 0.5% prior

09:30 (EU) ECB announces Covered-Bond Purchases

10:30 (CA) Canada to sell 3-month, 6-month and 12-motn Bills

11:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:30 (US) Treasury to sell 4-Week Bills

16:30 (US) Weekly API Oil Inventories