Sample Category Title

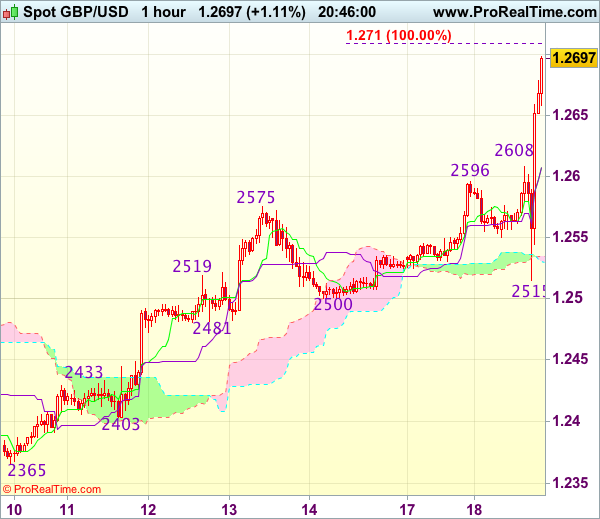

Trade Idea Update: GBP/USD – Buy at 1.2650

GBP/USD - 1.2719

Original strategy :

Buy at 1.2510, Target: 1.2610, Stop: 1.2475

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2650, Target: 1.2750, Stop: 1.2615

Position : -

Target : -

Stop : -

As cable has rallied again after finding renewed buying interest at 1.2515, signaling recent upmove is still in progress and bullishness remains for recent rise from 1.2109 to extend further gain to 1.2755-60 (1.236 times projection of 1.2365-1.2575 measuring from 1.2500), however, reckon previous resistance at 1.2775 would limit upside and risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as 1.2650-55 should limit downside and bring another rise later. Below previous resistance at 1.2616 (now support) would defer and risk correction to 1.2570-75 and possibly 1.2545-50 but price should stay well above support at 1.2515 and bring another upmove.

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.0690

Original strategy :

Sold at 1.0665, stopped at 1.0675

Position : - Short at 1.0665

Target : -

Stop : - 1.0675

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency has surged again after brief pullback and current break of resistance at 1.0670-78 resistance signals the erratic rise from 1.0570 low is still in progress and upside risk remains for further gain to 1.0698-02 (50% Fibonacci retracement of 1.0827-1.0570 and previous resistance), however, near term overbought condition should prevent sharp move beyond 1.0725-30 and reckon 1.0750 would hold from here, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below the Kijun-Sen (now at 1.0663) would suggest an intra-day top is possibly formed, brig test of support at 1.0635 but break there is needed to add credence to this view, bring subsequent test of 1.0602 support first.

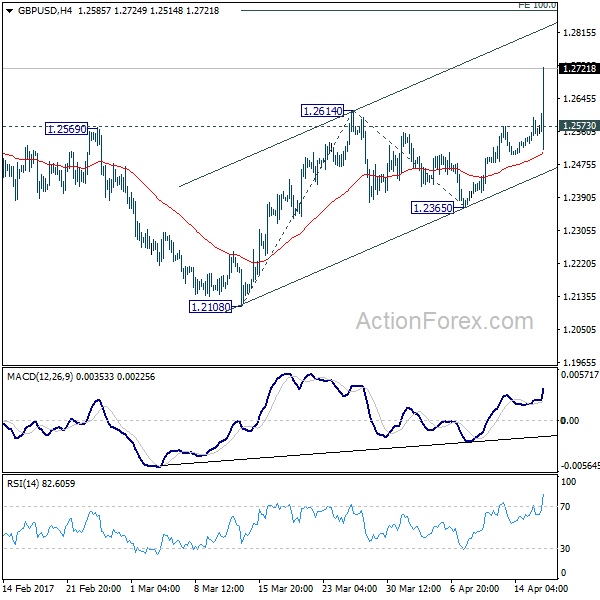

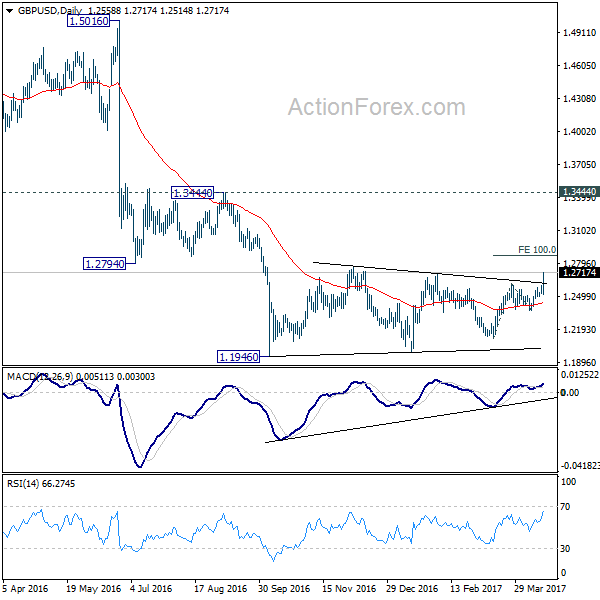

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2522; (P) 1.2558; (R1) 1.2599; More...

GBP/USD's rally accelerates to as high as 1.2714 so far today. The strong break of 1.2614 resistance confirms resumption of rise from 1.2108. Intraday bias stays on the upside for 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871. However, such rally is seen as part of the consolidation from 1.1946 low. Hence, we'd expect strong resistance around 55 week EMA (now at 1.3016) to limit upside and bring down trend resumption. On the downside, break of 1.2573 minor support will turn bias back to the downside for 1.2365 support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

British Pound Jumps Broadly after UK PM Theresa May Calls for Snap Election

Sterling jumps broadly today as currency markets respond positive to UK Prime Minister Theresa May's call for a snap election this June. GBP/USD powers through 1.2614 near term resistance and reaches as high as 1.2695 so far. GBP/JPY also took out 137.51 near term resistance which now suggests trend reversal. FTSE 100, however, is trading down -1.8% as stocks investments clearly dislike the uncertainties. Meanwhile, Euro also follows the Pound higher as markets are calm on French election. US Dollar, on the other hand, reversed earlier gains, against European majors but stays firm against commodity currencies.

UK PM May called snap elections

UK Prime Minister Theresa May surprised the world by calling for a snap election on June 8, "with reluctance", today. A election isn't due until 2020. But opinion polls showed that May's Conservative is having more than 20 points over Labour for the first time in nine years. The call for election is seen as an act to solidify public support for Brexit negotiation with EU. May emphasized that "we want a deep and special partnership between a strong and successful European Union and a United Kingdom that is free to chart its own way in the world." And, "our opponents believe that because the Government's majority is so small, our resolve will weaken and that they can force us to change course. They are wrong."

US housing data missed

Released from US, housing starts dropped to 1.22m annualized rate in march, below expectation of 1.28m. Building permits rose to 1.26m annualized rate, meeting consensus. US Treasury Secretary Steven Mnuchin noted yesterday that "as the world's currency, the primary reserve currency, I think that over long periods of time the strength of the dollar is a good thing." And, "it's a function of the confidence and the strength of the US economy." Nonetheless, he still agreed with President Donald Trump's comments regarding strength of the greenback in short term. Mnuchin said that "The president's comment - which again I agree with - is that over short periods of time the strength of the dollar creates certain issues that hurt our exports. I think that is what he has referred to, which is again factually correct."

French election in focus

French presidential election will be a major focus in April and May. Recent surge in support for far-left Jean-Luc Melenchon is seen as making the election a four way match with far right Marine Le Pen, centrist Emmanuel Macron and conservative François Fillon. Some see increasing risk of having two euro-sceptic candidates, Le Pen and Melenchon, heading to the run-off in May. The markets responded by dumping French bonds and stocks. The five year French-German yield spread has indeed jumped to the highest level since 2013. However, it's believed that support for Melenchon mainly came within the left-wing and is approaching limit. Thus, a run-off of Le Pen and Macron is still the base case. More in French Presidential Election: Macron and Le Pen Still Favorite as Melenchon Closing to Limit

Japan PM Abe nominated one dove, one centrist to replace two hawks in BoJ

In Japan, Prime Minister Shinzo Abe nominated two new members to replace Takehiro Sato and Takahide Kiuchi. Both are seen as hawks by the markets as they regularly dissented the ultra-loose monetary policies of the central bank. The two nominated are Goshi Kataoka, senior economist at Mitsubishi UFJ Research & Consulting, and Hitoshi Suzuki, an executive at the Bank of Tokyo-Mitsubishi UFJ. They are seen as one dove and one centrist. If the nominations are approved by the parliament, Abe would have then selected the entire BoJ policy board. And that would give him the advantage to continue with Abenomics.

BoJ Governor Haruhiko Kuroda said yesterday that consumer spending is picking up. And this is supported by steady improvements in employment and wages. And he noted that firms are likely to offer base-salary raise for staff during the current financial year. Separately, Deputy Governor Hiroshi Nakaso said that the central bank has been discussing the "means and how" of monetary stimulus exit" that could affect its revenues. But for now, BoJ's priority is still on maintaining sustainable inflation through the massive stimulus program.

RBA April minutes less upbeat that the March one

RBA minutes for the April meeting came in less upbeat than the March one, underpinning concerns over developments in Australia's labor and housing market. Policymakers refrained from delivering an upbeat forward guidance as it was in March. In the March minutes, RBA suggested that "year-ended growth was expected to pick up gradually to be above its potential rate over the forecast period". However, it only noted this month that "Australian economy had continued to grow moderately at the beginning of 2017, supported by the low level of interest rates". This apparently sounded less confident over the growth outlook. In the concluding statement, it was added that that "developments in the labour and housing markets warranted careful monitoring over coming months". More in RBA's April Minutes Revealed Concerns Over Labor And Housing Markets.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2522; (P) 1.2558; (R1) 1.2599; More...

GBP/USD's rally accelerates to as high as 1.2714 so far today. The strong break of 1.2614 resistance confirms resumption of rise from 1.2108. Intraday bias stays on the upside for 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871. However, such rally is seen as part of the consolidation from 1.1946 low. Hence, we'd expect strong resistance around 55 week EMA (now at 1.3016) to limit upside and bring down trend resumption. On the downside, break of 1.2573 minor support will turn bias back to the downside for 1.2365 support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes Apr | ||||

| 12:30 | CAD | International Securities Transactions (CAD) Feb | 6.20b | |||

| 12:30 | USD | Housing Starts Mar | 1.22M | 1.28M | 1.29M | 1.30M |

| 12:30 | USD | Building Permits Mar | 1.26M | 1.26M | 1.21M | 1.22M |

| 13:15 | USD | Industrial Production Mar | 0.50% | 0.00% | ||

| 13:15 | USD | Capacity Utilization Mar | 76.00% | 75.40% |

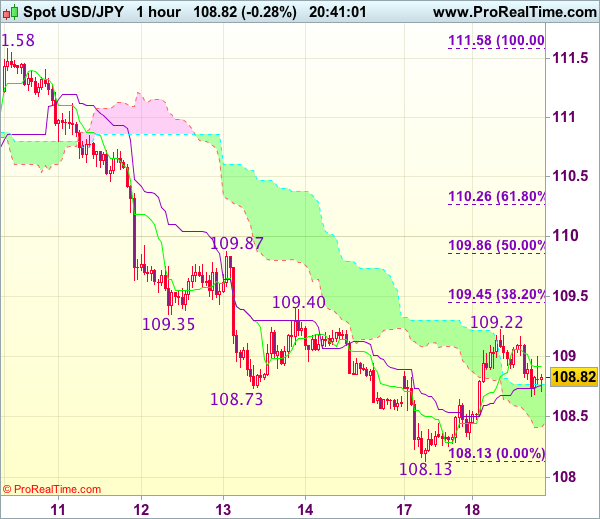

Trade Idea Update: USD/JPY – Sell at 109.90 or buy at 108.60

USD/JPY - 108.82

Original strategy :

Sell at 109.90, Target: 108.90, Stop: 110.25

O.C.O.

Buy at 108.60, Target: 109.60, Stop: 108.25

Position : -

Target : -

Stop : -

New strategy :

Sell at 109.90, Target: 108.90, Stop: 110.25

O.C.O.

Buy at 108.60, Target: 109.60, Stop: 108.25

Position : -

Target : -

Stop : -

Although the greenback extended recent decline to as low as 108.13 yesterday, the subsequent strong rebound suggests a temporary low has been formed there and consolidation with mild upside bias is seen for retracement of recent decline, hence gain to 109.40-45 (previous resistance and 38.2% Fibonacci retracement of 111.58-108.13) is likely, however, reckon upside would be limited to 109.86-87 (50% Fibonacci retracement and previous resistance) and price should falter below 110.25-30 (61.8% Fibonacci retracement), bring retreat later to 108.50-60 but price should stay above 108.30-35, bring another rebound.

In view of this, whilst we are looking to turn long on dips for such a rebound, we are inclined to sell dollar on subsequent bounce as 109.90-00 should limit upside, bring another decline. Below 108.30-35 would risk retest of 108.13 support (yesterday’s low) but break there is needed to signal recent decline has resumed and extend weakness to 107.75-80 later.

EURAUD Technical Analysis

On April 11/2017 bears pushed EURAUD lower and it seems lower prices are yet to come in the following trading sessions. At the current moment, bias remains bearish and traders should look for any possible selling opportunities.

1 Hour Chart Bearish Pattern: Bearish pattern is visible on short term analysis but traders need to be patient and wait for price to retrace higher towards the BC 0.50% Fib. retracement level and wait for the point D (blue pattern) to enter the possible reversal zone (blue box) to trigger sells. We do not recommend buying the pair to the proposed selling zone but rather advise to wait for price to enter the possible reversal zone and look for selling opportunities. There is also support/resistance levels near the BC 0.50% Fib. level so we should expect a reaction/reversal in price action in this area. Only time will tell what EURAUD will do but for now bias remains bearish.

If looking to sell EURAUD traders should wait for price to move above the BC 0.50% and watch for price to stall in the possible reversal zone (blue box) for any selling opportunities. Waiting for price to move above the BC 0.50% Fib. retracement level will offer a better risk/reward trade setup. A break above the point B high will invalidate the bearish pattern. If the pair moves lower from the possible reversal zone traders should place targets below the AB 2.24% level.

Of course, like any strategy/technique, there will be times when the strategy/technique fails so proper money/risk management should always be used on every trade.

CAC Under Pressure Ahead of French Election

The CAC 40 has dropped to the 5000 level, as the index is trading at 5,007.80 in Tuesday trade. On the release front, there are no events out of the eurozone. On Wednesday, the eurozone releases Final CPI, with the indicator expected to soften to 1.5 percent.

After an Easter holiday on Monday, the CEC has resumed trade on Tuesday. The CAC has posted losses, and briefly dropped below the symbolic 5000 level. Investors are keeping a keen eye on the French presidential election, with the first round of voting on April 23. The race remains extremely tight, with centrist Emmanuel Macron and far-right candidate Marine Le Pen tied at 22 percent. They are followed by Francois Fillon at 21% and Jean-Luc Melenchon at 18 percent. If Macron and Le Pen reach the second round, Macron is expected to win decisively by a margin of 64-36. With only a few days to go before the vote, any change in polling numbers could have a significant impact on the stock markets. Another factor weighing on the stock market is the crisis over North Korea, as the US continues to warn North Korea that that it will not allow the rogue country to continue to test ballistic missiles. US vice-president Mike Pence is in Japan for talks with Japanese officials, with trade issues and North Korea high on the agenda.

The eurozone won't release its first event this week until Wednesday, with the release of Eurozone Final CPI for March. CPI has improved over six straight months, and the February reading of 2.0% was noteworthy as it reached the ECB inflation target. This strong figure has raised speculation that if inflation levels continue to move higher, the ECB may have to consider tightening policy in order to curb inflation. However, the markets are expecting the March reading to drop to 1.5%, which would allow the ECB to hold its monetary course. The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

French Election Monitor: Mélenchon Could Enter Second Election Round in May

The most notable development since French Election Monitor #1 has been the stellar rise of left-wing candidate Mélenchon in the polls after a strong performance in the TV debates (see Chart 1). Ahead of the first election round this Sunday, the race between the four leading candidates Marine Le Pen, Emmanuel Macron, Francois Fillon and Jean- Luc Mélenchon remains wide open and the outcome is likely to be tight. Although a runoff on 7 May between Le Pen and Macron still seems to be the most likely outcome according to the polls, Mélenchon entering the second round now cannot be ruled out.

Should Mélenchon reach the run-off, opinion polls show that he could win against Fillon or Le Pen (see Chart 2). With his wish to renegotiate EU treaties and hold a subsequent EU exit referendum on the result as well as ending the independence of the ECB, his programme displays a similar EU-sceptic and anti-globalisation stance to Le Pen's. He rejects free trade agreements and the rules of the Stability and Growth Pact and advocates an alliance of southern European countries to fight austerity. Furthermore, Mélenchon wants the Bank of France to buy public debt and repeal the El Khomri labour market reforms. A potential run-off between the two EU-sceptics Mélenchon and Le Pen seems to be the biggest risk-scenario in the market at the moment and as a result we already saw the France 10Y spread to Germany widen to just a few bps from the highs in February (see Chart 3). However, even if Mélenchon should win the presidency, he faces the same parliamentary hurdles as Le Pen in implementing his programme or holding a referendum, as his party is unlikely to obtain sufficient seats for a majority.

Should he qualify for the second round, Macron is still seen winning the presidency irrespective of his opponent, according to the latest poll. However, the indecision of his supporters (only 72% are certain of their choice) and the expected lower participation rate (68%), due to widespread dissatisfaction with the established political class, could decrease his chances on election day and benefit Le Pen, whose supporters remain the most certain of their choice (89%). However, our base case remains that she will not win the presidency.

UK Snap General Election Shocker Revives British Pound

Sterling was back in fashion on Tuesday, with the GBPUSD lurching towards 1.2675 following Theresa May's unexpected announcement that there will be a snap general election on 8 June. This bombshell development has offered Sterling a solid boost, with markets now evaluating what impact this may have on the Brexit negotiations. The fact that May stated that she wants an election to ensure strong leadership that will deliver on Brexit may quell some related jitters in the short term.

While short-term bulls may reign as a result of this fresh development, longer-term bears could exploit the potential political uncertainty to drag Sterling lower. A very strong likelihood remains that Sterling sensitivity will intensify moving forward, with a vote in parliament on Wednesday to decide whether or not the election will take place acting as the first test.

From a technical standpoint, the GBPUSD is bullish on the daily charts. The upside momentum could propel prices towards the 1.2775 resistance level.

Trump rally put to the test

The ongoing anxiety surrounding geopolitical tensions across the globe has left investors jittery during Tuesday's trading session, with stock markets struggling to maintain gains. Asian shares were mostly lower amid cautious trading, with the sheer lack of appetite for risk exposing European equities to steep losses. Although Wall Street received a boost on Monday as participants redirected their attention to first quarter corporate earnings, the upside may be limited by a return of risk aversion. With confidence slowly deteriorating over Trump's ability to implement the phenomenal tax cuts and infrastructure spending he promised during his election campaign, the Trump rally could be put to test moving forward.

Dollar Trumped again

The Greenback was dealt a crippling blow last week after Donald Trump repeated his now iconic statement that the Dollar was "getting too strong". Dollar bears exploited the confusion created to attack the prices further, after Trump decided not to name China a currency manipulator. With Trump's comments on how he "liked" the low interest rates policy displaying a noticeable campaign U-turn and compounding the uncertainty, the Dollar could be in store for further punishment. The visible fact that the Greenback has found itself on the back foot every time Trump has shared his bearish thoughts on the Dollar does raise questions over whether the currency remains dictated by him in the short to medium term. From a technical standpoint, the Dollar Index has found itself pressured on the daily charts, with a break below 100.00 opening a path towards 99.50.

Commodity spotlight - Gold

The geopolitical tensions across the globe and political risks may continue to support Gold moving forward. Although prices edged lower on Monday, the metal remains bullish on the daily charts with buyers potentially exploiting the technical correction. From a technical standpoint, bulls remain in firm control above $1260 with $1300 acting as the next major level of interest.

GBP/USD Nears Mid-Term Major Resistance After Theresa May Calls Early General Election

The UK Prime Minister made a speech today around 11:15 am at 10 Downing Street.

She stated that the Cabinet had agreed to call an early general election, to be held on June 8. The UK government is determined to execute Brexit process and negotiation with the EU, and this is the right decision for the country's interests. The post-Brexit vote economic indicators have shown that the UK economy is more solid than expected to withstand Brexit impact.

However, some other political parties are still against Brexit and the deal the UK reach with the EU, such as the Labour, Liberal and Scottish National Party. Although the Conservative Party is the majority in the Parliament. Nevertheless, the unity of other opposing parties will outnumber the Conservative, and hence it will weaken the UK government's negotiation position with the EU.

In order to remove the political opposition and eliminate uncertainties, Theresa May attempts to increase the number of Conservative MPs by moving forward the general election.

GBP/USD saw a dramatic reversal this morning ahead of the speech due to the uncertainties. It surged around 110 points after the speech with strong bullish momentum on realization of speculation, breaking the psychological resistance level at 1.2600.

The bulls are currently edging up, with an attempt to test the next significant resistance level at 1.2700. However, the level is the mid-term major resistance level, where there is heavy pressure, be aware that the bullish momentum is likely to be restrained while nearing the level.

GBP/USD has been trading above the downside uptrend line support since April 10.

The resistance level is at 1.2680, followed by 1.2700.

The support line is at 1.2650, followed by 1.2620.